1. Introduction

In recent decades, environmental sustainability has been one of the most challenging issues for global leaders, policymakers, and scientists. Environmental sustainability requires meeting existing needs without jeopardizing the ability of forthcoming generations to fulfill their wants in the future [

1]. As a broad concept, sustainability is applicable to every element of human existence on Earth at the local, regional, national, and international levels and throughout a wide range of periods. Wetlands and forests that have survived for an extended period and are in good condition are examples of healthy biological systems. Unfortunately, as the world’s population has increased, ecosystems have degraded as a result. A disruption in the natural cycle’s equilibrium has significantly impacted humans and other living beings [

2]. Opportunities to minimize generations of waste through the use of hazardous materials, to reduce soil, water, and air pollution, and to preserve and reuse resources to the maximum degree practicable should be identified and used.

Environmental sustainability is, by definition, a multidisciplinary challenge that requires interdisciplinary solutions. Poor environmental circumstances are harmful to citizens’ health and economic well-being. According to [

3], the necessities of human existence, such as health, natural and physical capital, and access to water, food, and land, are vulnerable to climate change. These environmental concerns sparked a worldwide effort to tackle climate change, culminating in adopting the Paris Agreement and the Kyoto Protocol. The fundamental aim of these worldwide initiatives is to reduce the environmental impacts of carbon dioxide (CO

2) emissions. Despite attempts to minimize CO

2 emissions, the Worldwide Energy and CO

2 Status (2019) stated that global CO

2 emissions climbed by 1.7 percent in 2018. According to the research, the 1.7 percent rise in global carbon emissions is the fastest growth since 2013 and is 70 percent greater than the average increase in carbon emissions since 2010. However, SSA saw a 4.11 percent decrease in carbon emissions in 2015 but climbed by 2.6 percent in 2016. Given the increase in CO

2 emissions in SSA, despite a minor reduction in 2015, there is no question that CO

2 emissions have a detrimental influence on environmental quality in SSA, which negatively impacts citizen welfare and requires immediate attention. Less focus will exacerbate the harmful effects of climate change on human existence, economic development, and climatic and ecological systems [

4]. The literature on environmental sustainability has exploded, however, study into the role of institutions and governance in ensuring environmental sustainability is still needed.

The literature has demonstrated the relationship between institutions and environmental sustainability and gained various researchers’ attention. Different economists have used different institutional quality indicators (for example, political stability, democracy, the rule of law, political globalization, economic freedom, and control of corruption) in the case of the SAARC, G-7, EU, G20, BRICS, and OECD countries [

5,

6]. They found a link between institutions and environmental sustainability and established that improved institutional quality leads to better environmental eminence. [

7] investigated the impact of institutional quality indicators such as civil liberty and political rights on CO

2 emissions from 1980–2007, considering 129 countries. According to their findings, institutional quality indices increase the quantity of CO

2 emissions in the nations under investigation.

Similarly, [

8] investigated the impact of institutional quality factors on CO

2 emissions in the Malaysian economy. The research looked at institutional quality variables such as law and order, and it reported that Malaysia had established institutions that help keep CO

2 emissions under control. Finally, using data from 40 sub-Saharan African nations and the generalized method of moments (GMM), the impact of trade and institutional quality on environmental quality was studied by [

9]. Institutional qualities have a considerable favorable influence on environmental quality, according to the findings.

Another complicated problem is the link between institutions and environmental quality. Institutional performance is a multifaceted structure that impacts political and commercial dynamics through various institutional channels [

10]. Targeted ecological and economic policies play a crucial role in facilitating the transition. Still, they will need to be complemented with strengthened institutions to ensure monitoring and successful execution [

11]. As a result, environmental policy success is determined by policy acceptance and institutional performance, cultural discourses, prevailing beliefs, resource allocation, and industrial structure [

12]. Constitutionally and thriftily open civilizations that uphold rules and regulations, market resource allocation, and private property rights evolved quicker than ones that did not [

13].

Environmental taxes are among the most used institutional policies to contain ecological degradation. According to [

14], environmental taxes play a dynamic role in mitigating environmental corrosion in 26 European economies. According to [

15], environmental tax measures in Spain were critical in reducing pollutant emissions in 39 significant businesses. According to [

16], environmental tax measures increase the energy–trade balance and energy efficiency. This study is an addition to the already existing rich literature on environmental sustainability. However, the study is unique in three different ways—first, studies on the effect of country risk on environmental degradations are minimal; thus, the study bridges this gap. Second, we hope that the survey of institutions–environment interlinkage for a democratic, multi-cultural developing economy such as India adds value to the area of research. Third, we included a unique set of variables such as GDP, renewable energy consumption, urbanization, environmental taxation, corruption, and country risk in the reading. The primary objective of this study is to elaborate the inter-relation between institutional arrangements and environmental sustainability using time series data in India along with other controlled variables. The rest of the paper is designed in five sections.

Section 2 contains an overview of the available literature, whereas

Section 3 discusses the study variables and econometric modeling.

Section 4 contains the empirical results and discussion. The last two sections present the conclusion from the study and its policy implications.

2. Review of Past Studies

The existing literature on environmental sustainability is enormous. To validate the Environmental Kuznets curve hypothesis, many studies relate environmental degradation to the economic growth process. Similarly, studies examine the effect of different energy sources on carbon emissions. Researchers also analyzed the impact of many economic variables such as population and urbanization on environmental quality. Another set of studies relates institutions and institutional quality to ecological sustainability.

Studies attempted to validate the Environmental Kuznets curve and arrived at different results. These studies have used CO

2 emission or more sophisticated environmental footprints to proxy environmental degradation. This difference argues that human activities are not mono-dimensional, i.e., limited to air pollution [

17,

18] reported a U-shaped EKC for 35 OECD countries; similarly, [

19] validated a U-shaped EKC for France. [

20] categorized 93 economies into four sub-groups and found EKC valid only for the higher and upper-middle-income economy panels. [

21] validated an inverted U-shaped EKC for the MENA countries while reporting a U-shaped relationship for the non-oil exporting MENA economies panel. In contrast, several studies concluded a monotonically increasing environmental Kuznets curve [

22,

23,

24,

25]. Many studies found no evidence of EKC in the referred economies [

26].

Energy consumption is one of the primary causes of carbon emissions [

27,

28]. However, it is the energy source that matters the most in emissions. Studies reported that renewable energy use leads to fewer emissions than fossil fuels [

29,

30,

31,

32]. Few studies have even determined that non-renewable energy sources have a negative impact on the environment [

33,

34,

35,

36,

37]. The conclusions of the studies lend support to the alternative energy policy.

Many other factors such as population, human capital, foreign direct investment, etc., cause environmental degradation. For example, the rise in population leads to higher demand for energy, housing, transportation and industrialization and thus, causes ecological degradation both directly and indirectly [

28]. [

38] conducted a study using panel data on the interrelation between human capital, economic growth, and environmental degradation, and they concluded that human capita and economic development improves environmental quality in China’s provinces. Similarly, [

39] reached the same conclusion, and they argued that human capital always improves the environmental quality. Whereas, in the context of economic development this study, showed a U-shaped relation with environmental degradation.

Several research articles tested Porter’s hypothesis, the Pollution Haven hypothesis, and the Pollution Haloes hypothesis, which depict the relationship between foreign direct investment and environmental pollution [

40,

41,

42,

43,

44,

45,

46,

47]. The effect of trade openness on environmental degradation can be of three types, i.e., scale, technique, or composition effect [

48]. The technique effect reduces ecological degradation, while the scale and composition effects lead to more pollution [

49,

50]. The positive technique effect of trade on the environment has been reported for India in recent years [

51,

52]. Human capital helps reduce pollution through awareness, skill, environment-friendly practices, and lifestyle [

53,

54] concluded the positive impact of human capital in Latin American countries. In contrast, some studies reported no adverse effects of human capital on the environment [

55]. Many studies also reported the disturbing effect of urbanization on the environment [

56,

57].

The final literature set concerns the effect of institutions and institutional quality on the environment. Corruption, specifically, is one of the significant indicators of institutional quality. Empirical studies found that a decrease in corruption affects carbon emissions in the short term while a long-run effect is insignificant [

58,

59]. [

60] reported the limiting impact of corruption on sustainable policy implementations. Similarly, corruption jeopardizes the green environment policy in European countries [

61]. Studies found that the pernicious effect of corruption on the environment reduces the positive impacts of energy innovation [

62]. Chinese provinces also follow the same effects, and the more corruption, the more the per capita emission will be [

63]. The authors also reported that the marginal effect of corruption is higher in the low-emission provinces. [

64] concluded that anti-corruption policies rooted in the use of renewable energy consumption help to mitigate degradation. In another study, [

65] estimated the moderating effect of corruption on emission, trade, and economic growth in the BRICS countries. [

66] found a heterogeneous impact of corruption on emissions. In developing and less developed countries, it is more intense, while in developed countries, its effect is mitigated by proper policy implementation [

67]. Environmental taxes are another instrument aiming at reduction in environmental degradation. Many empirical studies reported a positive impact of environmental taxation [

68,

69]. Environmental tax may also promote green technology and energy efficiency [

70]. However, China recently implemented carbon tax to improve environmental quality; initially, carbon tax has a deleterious effect on other macro-economic variables instead of environmental degradation, but it does not improve environmental quality immediately [

71]. Whereas, [

72] argued that environmental taxes have no significant impact on energy, and may improve the environmental quality, but are not necessary conditions.

However, if the producer shifts the tax burden to the consumer, such tax will be a revenue-generating policy. In addition, studies remain inconclusive about the use of energy tax to promote green innovation and less energy consumption [

73,

74]. In contrast, several studies reported no effect of environmental taxation on emissions [

75,

76].

Moreover, the governance, political stability, economic stability, capacity, and operation of the banking system also play an essential role in moderating environmental degradation. Therefore, the country risk index is a comprehensive multi-dimensional measure of these institutions. [

77] investigated the moderating influence of national risk on the environmental impact of income disparity. The authors reported varying consequences depending on income inequality in low- or upper-income countries. Many studies concluded that the current environmental issues are due to institutional policy failure, lower institutional quality, terrible policy choice, and limiting democratic practices [

78,

79,

80]. In another study, [

81] developed a sovereign index using the extreme value theory. This particular index takes care of the industrial environment only. Carbon emissions will increase the sovereign risk. Thus, we can see attempts to scrutinize the direction of causality among risk and emissions [

82,

83,

84].

From the above brief review of the existing literature, we realize that institutions and the environment are strongly associated and invite research in different spheres and economies. To the best of the authors’ knowledge, no study has been conducted on the relationship between corruption and environmental degradation in India. In addition, we do not have an acquaintance with studies on ecological taxes and their effect on the environment in India. The main objective of this study is to address the burning issue of institutional arrangements and environmental sustainability along with other controlled variables using robust econometric techniques in India. This study also analyzes that the association between country risk and emissions for India is lacking. Thus, we believe the present research has enough scope to enrich the existing literature.

5. Conclusions and Policy Suggestions

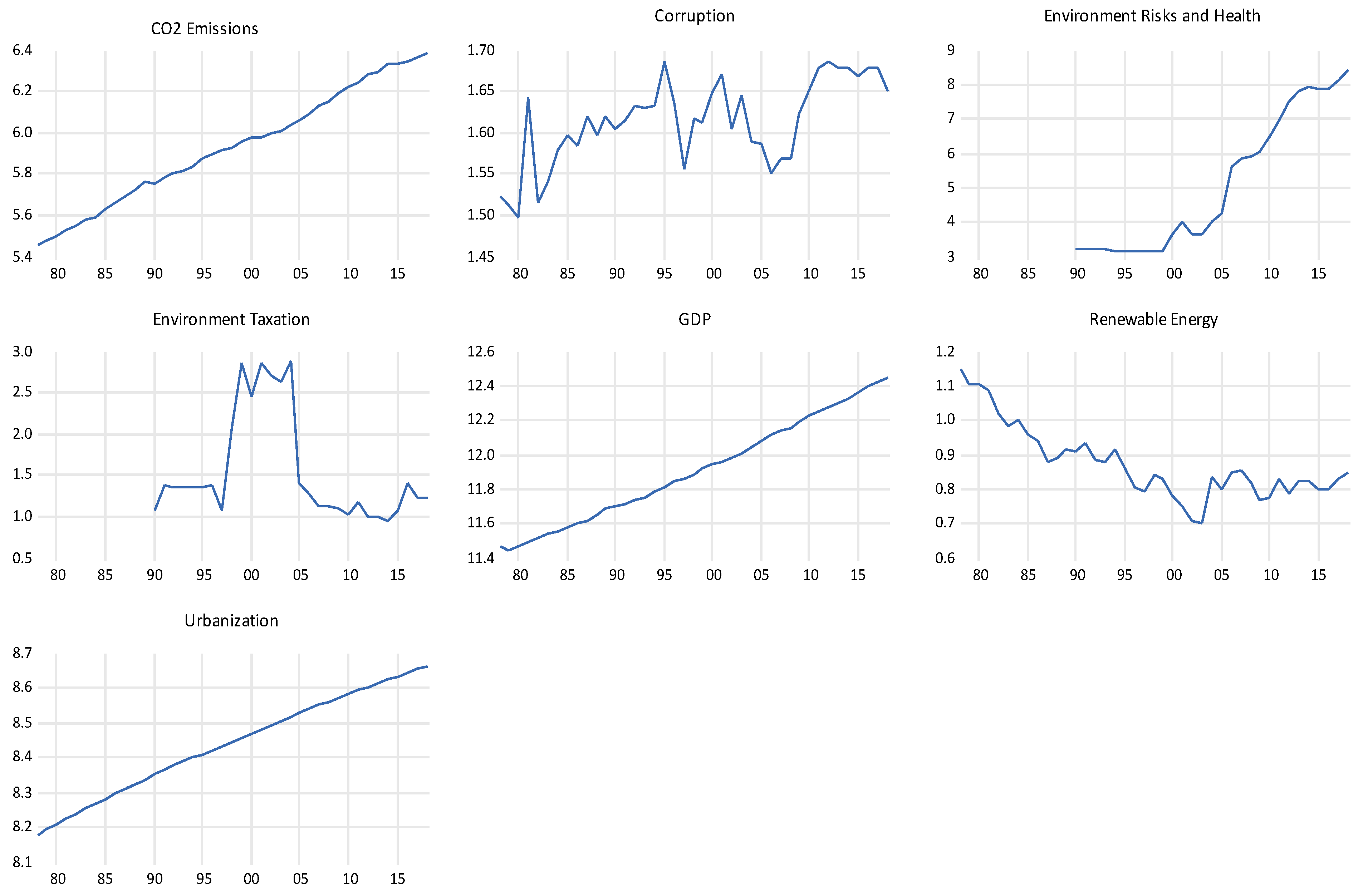

This study examined the impact of environmental taxation, corruption, urbanization, economic growth, environmental risk, and renewable energy on CO2 emissions in India. On the one hand, some researchers have found a positive correlation between CO2 emissions and environmental hazards and taxes, while other studies have found a negative or statistically negligible correlation. The current study examines the relationship between carbon dioxide emissions, environmental taxation, and risks in India from 1978 to 2018 using the ARDL model.

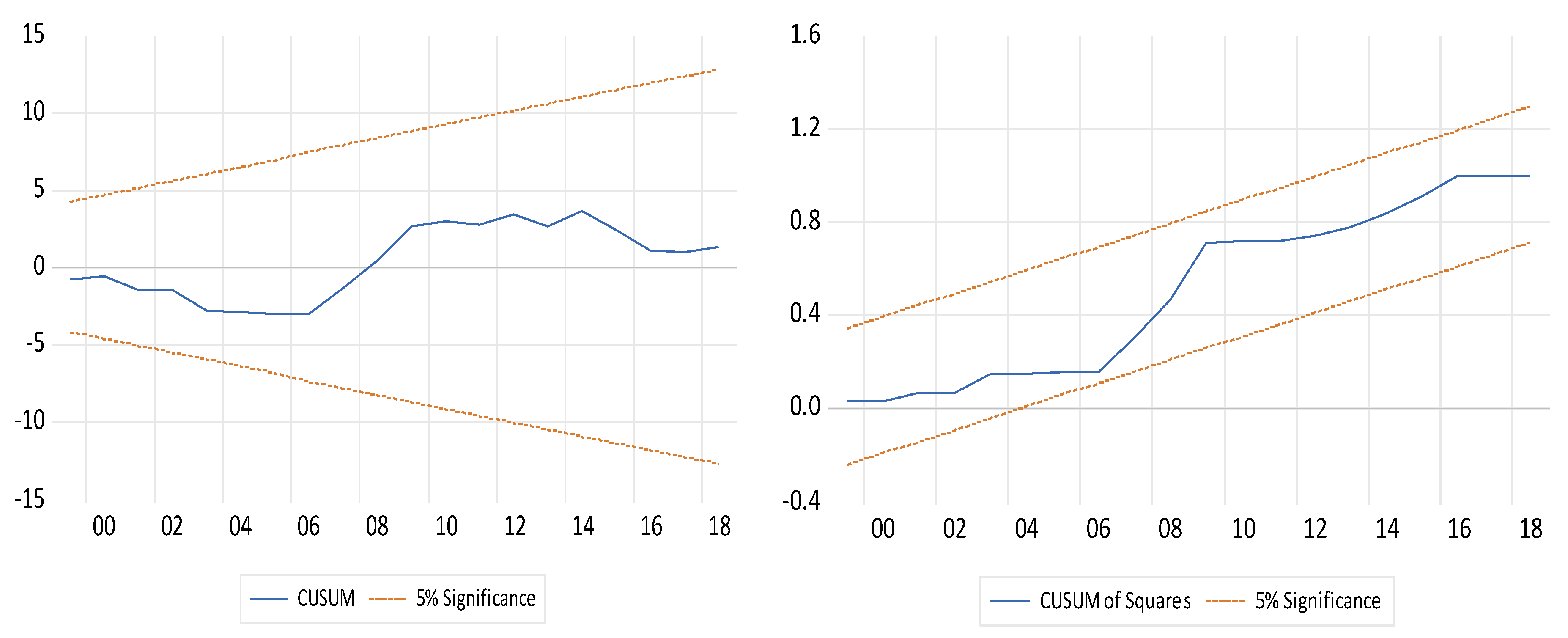

The outcome of several unit root tests revealed that the study’s variables are stationary. After that, the bound test was applied, and the results demonstrated that there is long-term relationship among variables. Before moving on with short-run and long-run elasticities, our model should be free from any bias; the diagnostic test findings of our study show that there is the nonappearance of serial correlation, non-normality, and heteroscedasticity. Finally, CUSUM and CUSUMSQ are used to check the model’s stability; according to our findings, there is no association outside the acute lines, indicating that the regression parameters are unchanging.

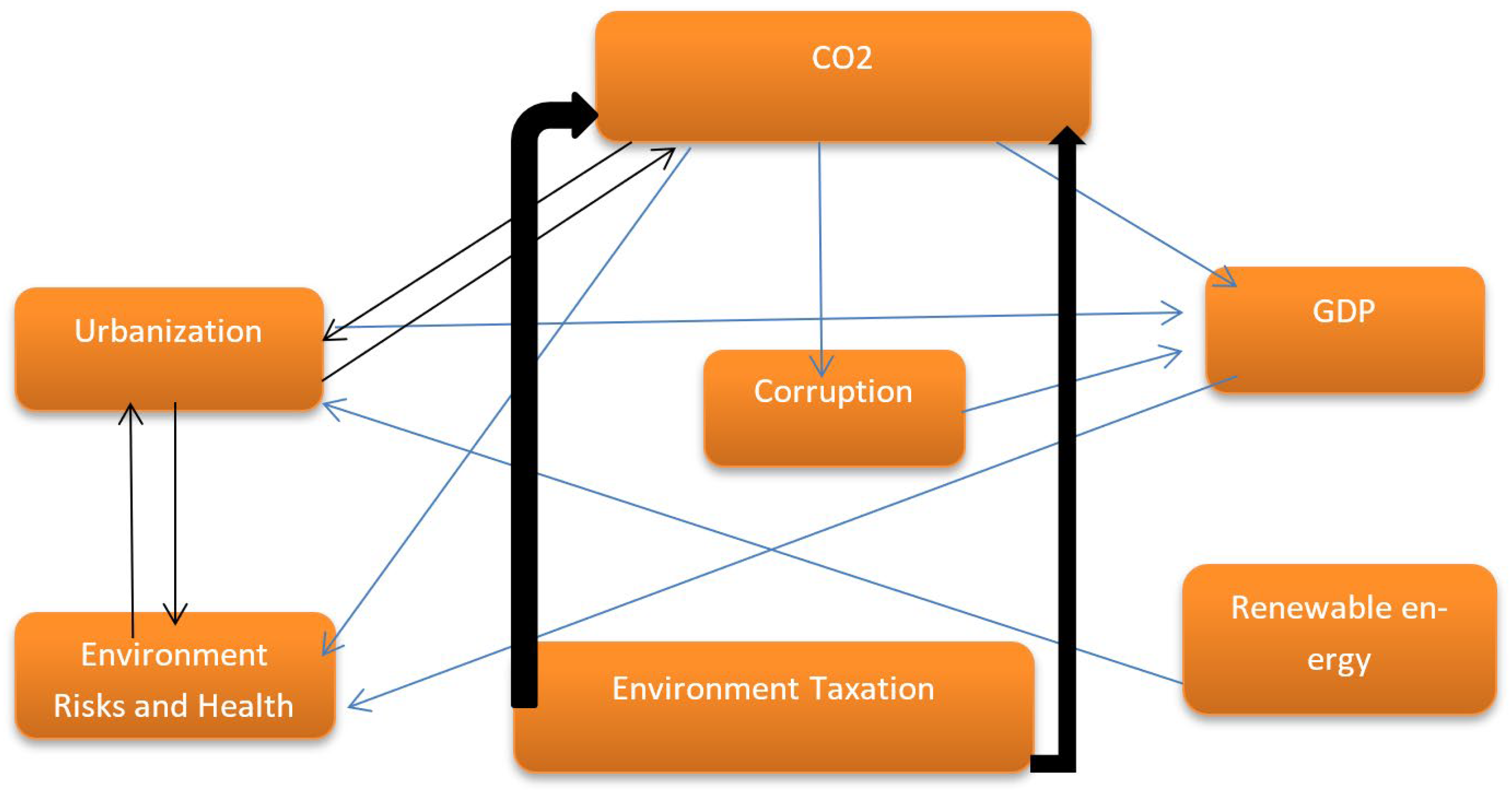

The study’s major goal is to compare the impact of CO

2 on environmental taxes and hazards, corruption, economic growth, renewable energy, and urbanization. Estimates were established for both short- and long-term outcomes. We used the ARDL model, which shows that corruption, environment risks, GDP, and urbanization have a positive connection with carbon emissions in India. A 1% increase in corruption, environment risks, GDP, and urbanization leads to carbon emissions of 0.12, 0.01, 0.63, and 35.92 percent. All four variables are statistically significant at 1 and 5 percent significance levels. These results are dependable with [

21] for Malaysia, [

62] for China but opposing with [

102] for BRICS. According to [

67], higher pollution taxes and charges may be advantageous in developing an efficient way of utilizing available resources and encouraging economic growth. The negative sign for environment taxation and renewable energy on carbon emissions means that higher environment taxation and renewable energy have successfully debilitated carbon emissions in India. To be more precise, a 1% rise in environmental taxation and renewable energy will decline carbon emissions by 3.57% and 2.56%, correspondingly.

Even though short-run elasticities based on the error correction mechanism (ECM) found that carbon emissions decline environmental sustainability, at the same time, environmental taxation and environment risks also influence the carbon emissions in India. These outcomes are comparable to [

102] for developed countries. The significant and negative valves of the error correction term were used to check the outcome of the long-run estimate (ECT). The negative valve validates that the variables will gather in the long term, and ECT displays the “speed of adjustment” for this model. In the current year, about 66 percent of the disequilibria from the previous year’s shock converged on the long-run equilibrium.

The finding of the study recommends several policy suggestions for the Indian government, which are as follows: First, the Government of India should set up strict environmental regulations and anti-corruption measures to combat unfair practice that distorts competition laws and policies. Second, it should continue to promote standardized emissions reduction measures, as it has done with the deployment of renewable energy sources and more sustainable trade that considers innovation and diversity. Third, long-term sensible urban planning is required to prevent further environmental degradation, as emissions from urban industrial regions also harm the environment; consequently, more emphasis should be on industry adoption of energy-efficient/green technologies. Fourth, it is need of the hour that the government should emphasize clean and renewable energy like wind, natural gas, and solar instead of non-renewable energy such as coal and petroleum that depletes the quality of the environment very quickly. Fifth, the government concentrates more on energy efficiency policies that diminish carbon emissions without hampering economic growth in the country. Sixth, the rising population is a burning issue in India, and it is challenging to diminish its energy demand. However, the government should conduct an environmental awareness program for residents. Ecological awareness and regulatory pressure might have been a solution to the problem of environmental damage. Finally, the Indian government should set an emissions threshold for manufacturing firms, with pollution monitoring equipment deployed to verify compliance. In addition, the development of India’s financial markets can help to introduce sophisticated energy-efficient technologies to the country and increase investment in R&D, resulting in lower emissions. Furthermore, because CO2 is worldwide pollution rather than a regional problem, global cooperation may reduce CO2 emissions. Forming an amalgamation between different countries to establish unified environmental laws will improve the efficiency of pollution regulations. Individual national ecological rules and regulations are not excluded, in any case.

,

,

{kind=link}

{kind=link}

{kind=link}