Strategic Orientation, Dynamic Capabilities, and Digital Transformation of Commercial Banks: A Fuzzy-Set QCA Approach

Abstract

:1. Introduction

2. Literature Review

2.1. Digital Transformation of Commercial Banks

2.2. Strategic Orientation

2.3. Dynamic Capabilities

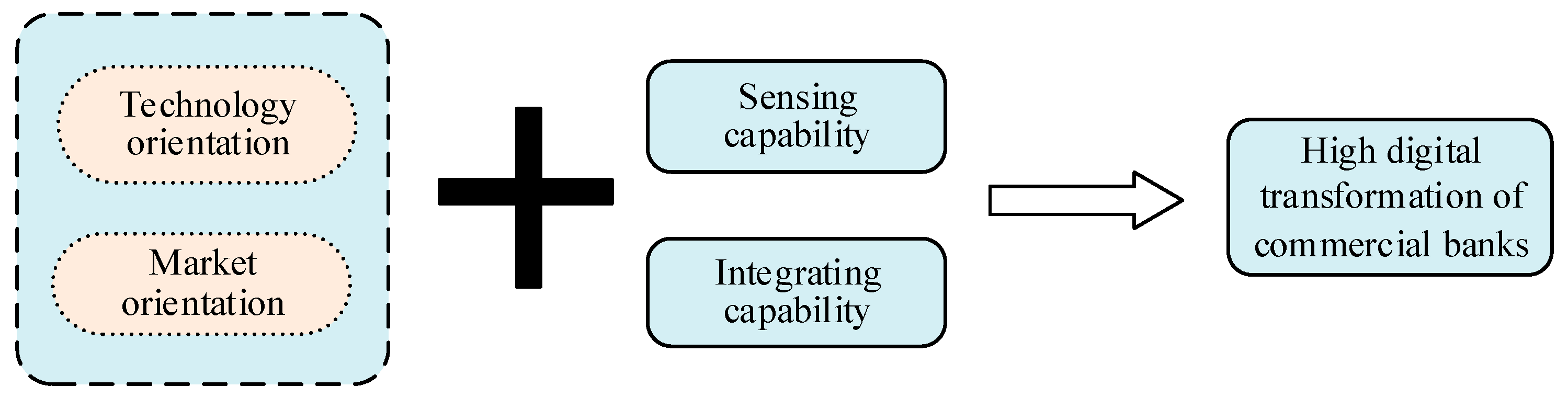

2.4. Configurational Framework

3. Research Methods

3.1. Sample and Data Collection

3.2. The fsQCA Approach

3.3. Measurement

3.3.1. Outcome Variables

3.3.2. Antecedent Conditions

3.3.3. Calibration

4. Results

4.1. Necessity Conditions Analysis

4.2. Sufficiency Analysis of the Configuration

4.2.1. The Configuration That Generates High Digital Transformation of Commercial Banks

represents the existence of the core condition,

represents the existence of the core condition,  represents the existence of the edge condition,

represents the existence of the edge condition,  represents the lack of the core condition,

represents the lack of the core condition,  represents the lack of the periphery condition, and blank represents the optional condition. In the expression, * represents and, and ~ represents negation.

represents the lack of the periphery condition, and blank represents the optional condition. In the expression, * represents and, and ~ represents negation.4.2.2. The Configuration That Generates Non-High Digital Transformation of Commercial Banks

4.2.3. Horizontal Analysis of Antecedent Conditions

4.3. Robustness Checks

5. Discussion

5.1. Research Conclusions

5.2. Theoretical Contributions

5.3. Practical Implications

5.4. Limitations and Future Research

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Benner, M.J.; Waldfogel, J. Changing the channel: Digitization and the rise of “middle tail” strategies. Strateg. Manag. J. 2020, 44, 264–287. [Google Scholar] [CrossRef]

- Thakor, A.V. Fintech and banking: What do we know? J. Financ. Intermediation 2020, 41, 100833. [Google Scholar] [CrossRef]

- Cappa, F.; Oriani, R.; Peruffo, E.; McCarthy, I. Big data for creating and capturing value in the digitalized environment: Unpacking the effects of volume, variety, and veracity on firm performance. J. Prod. Innov. Manag. 2021, 38, 49–67. [Google Scholar] [CrossRef]

- Hassan, M.K.; Rabbani, M.R.; Ali, M.A.M. Challenges for the Islamic finance and banking in post COVID era and the role of Fintech. J. Econ. Coop. Dev. 2020, 41, 93–116. [Google Scholar]

- Candy, C.; Robin, R.; Sativa, E.; Septiana, S.; Can, H.; Alice, A. Fintech in the time of COVID-19: Conceptual overview. J. Akunt. Keuang. Dan Manaj. 2022, 3, 253–262. [Google Scholar] [CrossRef]

- Tang, S.; Wu, X.C.; Zhu, J. Digital finance and enterprise technology innovation: Structural feature, mechanism identification and effect difference under financial supervision. Manag. World 2020, 36, 52–67. (In Chinese) [Google Scholar]

- Wang, S.H.; Xie, X.L. Economic pressure or social pressure: The development of digital finance and the digital innovation of commercial banks. Economist 2021, 1, 100–108. (In Chinese) [Google Scholar]

- Chen, H.; Tian, Z. Environmental uncertainty, resource orchestration and digital transformation: A fuzzy-set QCA approach. J. Bus. Res. 2022, 139, 184–193. [Google Scholar] [CrossRef]

- Xie, X.L.; Wang, S.H. Digital transformation of commercial banks in China: Measurement, progress and impact. China Econ. Q. 2022, 22, 1937–1956. (In Chinese) [Google Scholar]

- Chen, H.; Huang, Y.T.; Yang, Y.C. The impact of government tax incentives on enterprises' digital transformation: Empirical evidence from the policy of accelerated depreciation of fixed assets. Rev. Ind. Econ. 2022, 1–15. (In Chinese) [Google Scholar] [CrossRef]

- Bonnet, D.; Westerman, G. The new elements of digital transformation. MIT Sloan Manag. Rev. 2021, 62, 82–89. [Google Scholar]

- McCarthy, P.; Sammon, D.; Alhassan, I. Digital transformation leadership characteristics: A literature analysis. J. Decis. Syst. 2021, 1–31. [Google Scholar] [CrossRef]

- Wang, S.H.; Xie, X.L. Know before you act? Managerial cognition and bank digital transformation. Chin. Rev. Financ. Stud. 2021, 13, 78–97. (In Chinese) [Google Scholar]

- Kane, G.C.; Palmer, D.; Phillips, A.N.; Kiron, D.; Buckley, N. Strategy, not Technology, Drives Digital Transformation. MIT Sloan Management Review and Deloitte University Press. 2015, pp. 1–25. Available online: https://www2.deloitte.com/content/dam/Deloitte/fr/Documents/strategy/dup_strategy-not-technology-drives-digital-transformation.pdf (accessed on 9 November 2022).

- Niemand, T.; Rigtering, J.P.C.; Kallmünzer, A.; Kraus, S.; Maalaoui, A. Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. Eur. Manag. J. 2021, 39, 317–326. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef] [Green Version]

- Ghosh, S.; Hughes, M.; Hodgkinson, I.; Hughes, P. Digital transformation of industrial businesses: A dynamic capability approach. Technovation 2022, 113, 102414. [Google Scholar] [CrossRef]

- Yu, J.; Moon, T. Impact of digital strategic orientation on organizational performance through digital competence. Sustainability 2021, 13, 9766. [Google Scholar] [CrossRef]

- Fainshmidt, S.; Wenger, L.; Pezeshkan, A.; Mallon, M.R. When do dynamic capabilities lead to competitive advantage? The importance of strategic fit. J. Manag. Stud. 2019, 56, 758–787. [Google Scholar] [CrossRef]

- Cheng, J.Q.; Luo, J.L.; Du, Y.Z.; Liu, Q.C. What kinds of entrepreneurial ecosystem can produce country-level female high entrepreneurial activity? Stud. Sci. Sci. 2021, 39, 695–702. (In Chinese) [Google Scholar]

- Fiss, P.C. A set-theoretic approach to organizational configurations. Acad. Manag. Rev. 2007, 32, 1180–1198. [Google Scholar] [CrossRef] [Green Version]

- Du, Y.Z.; Jia, L.D. Configurational perspective and qualitative comparative analysis (QCA): A new way of management research. Manag. World 2017, 6, 155–167. (In Chinese) [Google Scholar]

- Fiss, P.C. Building better causal theories: A fuzzy set approach to typologies in organization research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef] [Green Version]

- Ragin, C.C. Comparative Method: Moving Beyond Qualitative and Quantitative Strategies; University of California Press: Oakland, CA, USA, 2014; pp. 1–185. [Google Scholar]

- Douglas, E.J.; Shepherd, D.A.; Prentice, C. Using fuzzy-set qualitative comparative analysis for a finer-grained understanding of entrepreneurship. J. Bus. Ventur. 2020, 35, 105970. [Google Scholar] [CrossRef]

- Ragin, C.C. Redesigning Social Inquiry: Fuzzy Sets and Beyond; University of Chicago Press: Chicago, IL, USA, 2008. [Google Scholar]

- Furnari, S.; Crilly, D.; Misangyi, V.F.; Greckhamer, T.; Fiss, P.C.; Aguilera, R.V. Capturing causal complexity: Heuristics for configurational theorizing. Acad. Manag. Rev. 2021, 46, 778–799. [Google Scholar] [CrossRef]

- Naimi-Sadigh, A.; Asgari, T.; Rabiei, M. Digital transformation in the value chain disruption of banking services. J. Knowl. Econ. 2022, 13, 1212–1242. [Google Scholar] [CrossRef]

- Dul, J. Necessary condition analysis (NCA): Logic and methodology of “necessary but not sufficient” causality. Organ. Res. Methods 2016, 19, 10–52. [Google Scholar] [CrossRef]

- Parmigiani, A.; Irwin, J.; Lahneman, B. Building greener motorhomes: How dual-purpose technical and relational capabilities affect component and full product innovation. Strateg. Manag. J. 2022, 43, 1110–1140. [Google Scholar] [CrossRef]

- Liu, D.Y.; Chen, S.W.; Chou, T.C. Resource fit in digital transformation: Lessons learned from the CBC Bank global e-banking project. Manag. Decis. 2011, 49, 10. [Google Scholar] [CrossRef]

- Diener, F.; Špaček, M. Digital transformation in banking: A managerial perspective on barriers to change. Sustainability 2021, 13, 2032. [Google Scholar] [CrossRef]

- Lucas, H.C.; Oh, W.; Weber, B.W. The defensive use of IT in a newly vulnerable market: The New York Stock Exchange, 1980–2007. J. Strateg. Inf. Syst. 2009, 18, 3–15. [Google Scholar] [CrossRef]

- Fu, J.; Mishra, M. Fintech in the time of COVID−19: Technological adoption during crises. J. Financ. Intermediation 2022, 50, 100945. [Google Scholar] [CrossRef]

- Hanelt, A.; Bohnsack, R.; Marz, D.; Antunes Marante, C. A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. J. Manag. Stud. 2021, 58, 1159–1197. [Google Scholar] [CrossRef]

- Dong, B.; Xu, H.; Luo, J.; Nicol, C.D.; Liu, W. Many roads lead to Rome: How entrepreneurial orientation and trust boost the positive network range and entrepreneurial performance relationship. Ind. Mark. Manag. 2021, 88, 173–185. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Yim, C.K.; Tse, D.K. The effects of strategic orientations on technology- and market-based breakthrough innovations. J. Mark. 2005, 69, 42–60. [Google Scholar] [CrossRef]

- Hamada Fawzy Thabet, A.; Abbas, M. Banks performance and impact of market orientation strategy: Do employee satisfaction and customer loyalty augment this relationship? Int. Rev. Manag. Mark. 2017, 7, 60–66. [Google Scholar]

- Xie, Z.C.; Zhao, X.L.; Liu, Y. Fin-tech driving and strategic digitization transformation of commercial banks. China Soft Sci. 2018, 8, 184–192. (In Chinese) [Google Scholar]

- Mubarak, M.F.; Petraite, M. Industry 4.0 technologies, digital trust and technological orientation: What matters in open innovation? Technol. Forecast. Soc. Chang. 2020, 161, 120332. [Google Scholar] [CrossRef]

- Setia, P.; Venkatesh, V.; Joglekar, S. Leveraging digital technologies: How information quality leads to localized capabilities and customer service performance. MIS Q. 2013, 37, 565–590. [Google Scholar] [CrossRef] [Green Version]

- Agrawal, A.; Gans, J.S.; Goldfarb, A. What to expect from artificial intelligence. MIT Sloan Manag. Rev. 2017, 58, 23–26. [Google Scholar]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital transformation and customer value creation in Made in Italy SMEs: A dynamic capabilities perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Svahn, F.; Mathiassen, L.; Lindgren, R. Embracing digital innovation in incumbent firms: How Volvo Cars managed competing concerns. MIS Q. 2017, 41, 239–253. [Google Scholar] [CrossRef]

- Warner, K.S.R.; Wäger, M. Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Plan. 2019, 52, 326–349. [Google Scholar] [CrossRef]

- Schilke, O.; Hu, S.; Helfat, C.E. Quo vadis, dynamic capabilities? A content-analytic review of the current state of knowledge and recommendations for future research. Acad. Manag. Ann. 2018, 12, 390–439. [Google Scholar] [CrossRef] [Green Version]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Giudici, A.; Reinmoeller, P.; Ravasi, D. Open-system orchestration as a relational source of sensing capabilities: Evidence from a venture association. Acad. Manag. J. 2018, 61, 1369–1402. [Google Scholar] [CrossRef] [Green Version]

- Ross, J.W.; Sebastian, I.M.; Beath, C.M. How to develop a great digital strategy. MIT Sloan Manag. Rev. 2017, 58, 7–9. [Google Scholar]

- Helfat, C.E.; Raubitschek, R.S. Dynamic and integrative capabilities for profiting from innovation in digital platform-based ecosystems. Res. Policy 2018, 47, 1391–1399. [Google Scholar] [CrossRef]

- Cannas, R. Exploring digital transformation and dynamic capabilities in agrifood SMEs. J. Small Bus. Manag. 2021, 1–27. [Google Scholar] [CrossRef]

- Cronqvist, L.; Berg-Schlosser, D. Multi-value QCA (mvQCA). Config. Comp. Methods Qual. Comp. Anal. (QCA) Relat. Tech. 2009, 51, 69–86. [Google Scholar]

- Sharma, A.; Iyer, G.R.; Mehrotra, A.; Krishnan, R. Sustainability and business-to-business marketing: A framework and implications. Ind. Mark. Manag. 2010, 39, 330–341. [Google Scholar] [CrossRef]

- Du, Y.; Kim, P.H. One size does not fit all: Strategy configurations, complex environments, and new venture performance in emerging economies. J. Bus. Res. 2021, 124, 272–285. [Google Scholar] [CrossRef]

- Dai, X. Supply chain relationship quality and corporate technological innovations: A multimethod study. Sustainability 2022, 14, 9203. [Google Scholar] [CrossRef]

- Gupta, K.; Crilly, D.; Greckhamer, T. Stakeholder engagement strategies, national institutions, and firm performance: A configurational perspective. Strateg. Manag. J. 2020, 41, 1869–1900. [Google Scholar] [CrossRef]

- Länsiluoto, A.; Joensuu-Salo, S.; Varamäki, E.; Viljamaa, A.; Sorama, K. Market orientation and performance measurement system adoption impact on performance in SMEs. J. Small Bus. Manag. 2019, 57, 1027–1043. [Google Scholar] [CrossRef]

- Kohli, A.K.; Jaworski, B.J.; Kumar, A. MARKOR—A measure of market orientation. J. Mark. Res. 1993, 30, 467–477. [Google Scholar] [CrossRef] [Green Version]

- Homburg, C.; Pflesser, C. A multiple layer model of market-oriented organizational culture: Measurement issues and performance outcomes. J. Mark. Res. 1999, 10, 198. [Google Scholar]

- Lu, Q.C.; Liang, L.L.; Jia, F. How does strategic learning impact on organizational innovation: A dynamic capability perspective. Manag. World 2018, 34, 109–129. [Google Scholar]

- Schneider, C.Q.; Wagemann, C. Set-Theoretic Methods for the Social Sciences: A Guide to Qualitative Comparative Analysis; Cambridge University Press: Cambridge, UK, 2009. [Google Scholar]

- Ribeiro-Navarrete, S.; Palacios-Marqués, D.; Lassala, C.; Ulrich, K. Key factors of information management for crowdfunding investor satisfaction. Int. J. Inf. Manag. 2021, 59, 102354. [Google Scholar] [CrossRef]

- De Crescenzo, V.; Ribeiro-Soriano, D.E.; Covin, J.G. Exploring the viability of equity crowdfunding as a fundraising instrument: A configurational analysis of contingency factors that lead to crowdfunding success and failure. J. Bus. Res. 2020, 115, 348–356. [Google Scholar] [CrossRef]

- Leppänen, P.; George, G.; Alexy, O. When do novel business models lead to high firm performance? A configurational approach to value drivers, competitive strategy, and firm environment. Acad. Manag. J. 2021. [Google Scholar] [CrossRef]

- Wilden, R.; Devinney, T.M.; Dowling, G.R. The architecture of dynamic capability research identifying the building blocks of a configurational approach. Acad. Manag. Ann. 2016, 10, 997–1076. [Google Scholar] [CrossRef]

- Ma, H.J.; Xiao, L.; Han, S.T. Review on dynamic capabilities in the entrepreneurship field—Based on the LDA topic model. Nankai Bus. Rev. 2022, 25, 1–20. (In Chinese) [Google Scholar]

- Omoregbe, O.; Azage, J.; Alufohai, D.I. Innovation strategies and market orientation in seleccted Nigerian banks. Oradea J. Bus. Econ. 2022, 7, 45–61. [Google Scholar] [CrossRef]

- Sia, S.K.; Soh, C.; Weill, P. How DBS bank pursued a digital business strategy. MIS Q. Exec. 2016, 15, 105–121. [Google Scholar]

- Tang, K.Y.; Ouyang, J.; Zhen, J.; Ren, H. How does regional innovation ecosystem drive innovation performance? A fuzzy set Qualitative Comparative Analysis based on 31 provinces. Sci. Sci. Manag. S. T. 2021, 42, 53–72. (In Chinese) [Google Scholar]

- Rihoux, B.; Ragin, C.C. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques; Sage Publications: Thousand Oaks, CA, USA, 2008. [Google Scholar]

- Kohtamäki, M.; Parida, V.; Patel, P.C.; Gebauer, H. The relationship between digitalization and servitization: The role of servitization in capturing the financial potential of digitalization. Technol. Forecast. Soc. Chang. 2020, 151, 119804. [Google Scholar] [CrossRef]

- Mainardes, E.W.; Ferreira Costa, P.M.; Nossa, S.N. Customers' satisfaction with fintech services: Evidence from Brazil. J. Financ. Serv. Mark. 2022. [Google Scholar] [CrossRef]

- Du, Y.Z.; Li, J.X.; Liu, Q.C.; Zhao, S.T.; Chen, K.W. Configurational theory and QCA method from a complex dynamic perspective: Research progress and future directions. Manag. World 2021, 37, 180–197. (In Chinese) [Google Scholar]

- Momoh, M.O.; Chinedu, P.U.; Nwankwo, W.; Aliu, D.; Shaba, M.S. Blockchain Adoption: Applications and Challenges. Int. J. Softw. Eng. Comput. Syst. 2021, 7, 19–25. [Google Scholar] [CrossRef]

- Asadi, S.; Nilashi, M.; Husin, A.R.C.; Yadegaridehkordi, E. Customers perspectives on adoption of cloud computing in banking sector. Inf. Technol. Manag. 2017, 18, 305–330. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Category | Frequency | Percent (%) | |

|---|---|---|---|

| Nature of the bank | City commercial bank | 17 | 38.64 |

| Rural commercial bank | 27 | 61.36 | |

| Region | Jiangsu | 19 | 43.18 |

| Zhejiang | 15 | 34.09 | |

| Other | 10 | 22.73 | |

| Years of establishment | Less than 10 years | 7 | 15.91 |

| 10–20 years | 23 | 52.27 | |

| More than 20 years | 14 | 31.82 | |

| The number of employees | Less than 1000 employees | 18 | 40.91 |

| 1000–5000 employees | 16 | 36.36 | |

| 5000–10,000 employees | 7 | 15.91 | |

| More than 10,000 employees | 3 | 6.82 | |

| Operating income (Yearly/RMB) | Less than 1 billion | 7 | 15.91 |

| 1–3 billion | 14 | 31.82 | |

| 3–6 billion | 11 | 25 | |

| More than 6 billion | 12 | 27.27 |

| Fuzzy Set Calibration | Descriptive Statistics | ||||||

|---|---|---|---|---|---|---|---|

| Set | Fully In | Crossover Point | Fully Out | Mean | Std. Dev. | Min. | Max. |

| Digital transformation of commercial banks | 17.108 | 25.013 | 36.351 | 31.899 | 21.970 | 8.15 | 102.87 |

| Technology orientation | 4.00 | 4.33 | 4.67 | 4.030 | 0.937 | 1.67 | 5 |

| Market orientation | 3.42 | 4.17 | 4.67 | 3.856 | 1.176 | 1.00 | 5 |

| Sensing capability | 4.00 | 4.25 | 4.50 | 3.943 | 1.028 | 1.25 | 5 |

| Integrating capacity | 3.80 | 4.40 | 4.55 | 3.964 | 0.953 | 1.40 | 4.8 |

| Transforming capability | 4.00 | 4.33 | 4.67 | 3.894 | 1.031 | 1.00 | 5 |

| Conditional Variables | Outcome Variables | |||

|---|---|---|---|---|

| High Digital Transformation of Commercial Banks | Non-High Digital Transformation of Commercial Banks | |||

| Consistency | Coverage | Consistency | Coverage | |

| Technology orientation | 0.486 | 0.514 | 0.586 | 0.629 |

| ~Technology orientation | 0.649 | 0.607 | 0.547 | 0.519 |

| Market orientation | 0.628 | 0.610 | 0.452 | 0.446 |

| ~Market orientation | 0.429 | 0.436 | 0.605 | 0.623 |

| Sensing capability | 0.564 | 0.501 | 0.658 | 0.593 |

| ~Sensing capability | 0.542 | 0.610 | 0.446 | 0.509 |

| Integrating capacity | 0.464 | 0.518 | 0.537 | 0.608 |

| ~Integrating capacity | 0.649 | 0.580 | 0.575 | 0.521 |

| Transforming capability | 0.399 | 0.490 | 0.495 | 0.617 |

| ~Transforming capability | 0.689 | 0.573 | 0.592 | 0.500 |

| Conditional Variables | High Digital Transformation of Commercial Banks | Non-High Digital Transformation of Commercial Banks | |||

|---|---|---|---|---|---|

| S1a | S1b | S2 | NS1 | NS2 | |

| Technology orientation | | | | | |

| Market orientation | | | | | |

| Sensing capability | | | | ||

| Integrating capacity | | | | | |

| Transforming capability | | | | | |

| Consistency | 0.784 | 0.702 | 0.787 | 0.846 | 0.848 |

| Raw coverage | 0.226 | 0.191 | 0.154 | 0.210 | 0.249 |

| Unique coverage | 0.053 | 0.018 | 0.087 | 0.112 | 0.150 |

| Solution coverage | 0.331 | 0.361 | |||

| Solution consistency | 0.741 | 0.868 | |||

and indicate the existence and absence of core conditions; and represent the existence and absence of periphery conditions; blank spaces indicate that the condition may be present or absent.| Characteristics of Conventional Regression Methods | Our Findings from a Configurational fsQCA Approach | Theoretical Contributions |

|---|---|---|

| Organizational strategy, capability, and digital transformation are significantly correlated | Organizational strategic orientation and dynamic capabilities are not necessary conditions for high digital transformation alone | Analyzing the digital transformation of commercial banks from the configurational perspective of causal complex factors such as organizational strategy and capability is helpful to reconcile the conflicts of inconsistent research results |

| Market orientation is an important condition for commercial banks to achieve high digital transformation | Confirming the powerful effect of market orientation on digital transformation of commercial banks | |

| The configuration model of strategic orientation and dynamic capabilities has been constructed | Providing new ideas for the research on the coupling of organizational elements and digital ecology of commercial banks, and partially responding to the digital transformation framework proposed by Hanelt (2021) [35] | |

| The relationships between and among the elements of dynamic capabilities are progressive | Sensing capability and integrating capability play a completely substitutive role in promoting the digital transformation of commercial banks | Deepening the symbiotic relationship of organizational capability elements and make up for the deficiency of existing literature on the potential substitutive relationship between and among dynamic capabilities factors |

| Supporting the initiative of Wilden et al. (2016) [65] and Ma et al. (2022) [66] to systematically study dynamic capabilities using configuration theory | ||

| Showing the advantages of QCA in discerning the relationship between various elements within the model and in providing methodological guidance for the follow-up exploration of complex digital transformation phenomenon | ||

| There is symmetry in the research conclusion. The high market orientation can promote commercial banks to achieve high digital transformation, while the low market orientation cannot. | The driving mechanism of commercial banks’ digital transformation has causal asymmetry: three configuration paths to achieve high digital transformation are not directly opposed to two paths leading to non-high digital transformation | Demonstrating that the QCA method can break through the unified symmetry assumption of causality effect in linear regression and further clarify the complex causes in more detail |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cheng, S.; Fan, Q.; Huang, M. Strategic Orientation, Dynamic Capabilities, and Digital Transformation of Commercial Banks: A Fuzzy-Set QCA Approach. Sustainability 2023, 15, 1915. https://doi.org/10.3390/su15031915

Cheng S, Fan Q, Huang M. Strategic Orientation, Dynamic Capabilities, and Digital Transformation of Commercial Banks: A Fuzzy-Set QCA Approach. Sustainability. 2023; 15(3):1915. https://doi.org/10.3390/su15031915

Chicago/Turabian StyleCheng, Songsong, Qunpeng Fan, and Minghao Huang. 2023. "Strategic Orientation, Dynamic Capabilities, and Digital Transformation of Commercial Banks: A Fuzzy-Set QCA Approach" Sustainability 15, no. 3: 1915. https://doi.org/10.3390/su15031915