On the Determinants of Bitcoin Returns and Volatility: What We Get from Gets?

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Brief Description of Gets

3.2. The Considered GUM

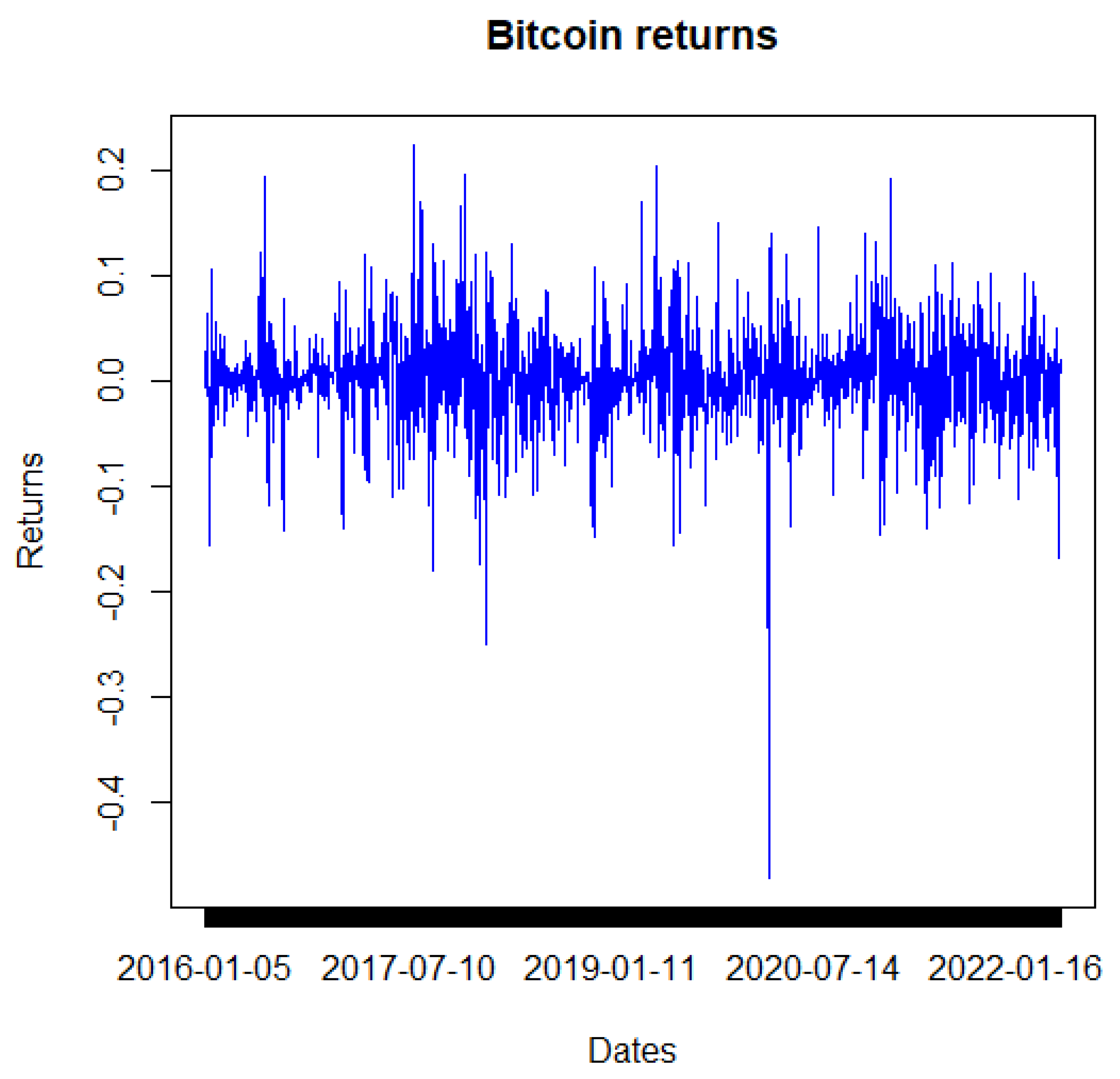

3.3. Data: Sources and Description

4. Results

4.1. Determinants of Conditional Mean Equation

4.2. Determinants of Conditional Variance Equation

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jones, B.A.; Goodkind, A.L.; Berrens, R.P. Economic estimation of Bitcoin mining’s climate damages demonstrates closer resemblance to digital crude than digital gold. Sci. Rep. 2022, 12, 14512. [Google Scholar] [CrossRef] [PubMed]

- Bowala, S.; Singh, J. Optimizing Portfolio Risk of Cryptocurrencies Using Data-Driven Risk Measures. J. Risk Financ. Manag. 2022, 15, 427. [Google Scholar] [CrossRef]

- Yan, Y.; Lei, Y.; Wang, Y. Bitcoin as a Safe-Haven Asset and a Medium of Exchange. Axioms 2022, 11, 415. [Google Scholar] [CrossRef]

- Baur, D.G.; Hong, K.; Lee, A.D. Bitcoin: Medium of exchange or speculative assets? J. Int. Financ. Mark. Inst. Money 2018, 54, 177–189. [Google Scholar] [CrossRef]

- Dubey, P. Short-run and long-run determinants of bitcoin returns: Transnational evidence. Rev. Behav. Finance 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Bouri, E.; Roubaud, D.; Kristoufek, L. Safe haven, hedge and diversification for G7 stock markets: Gold versus bitcoin. Econ. Model. 2020, 87, 212–224. [Google Scholar] [CrossRef]

- Corbet, S.; Meegan, A.; Larkin, C.; Lucey, B.; Yarovaya, L. Exploring the Dynamic Relationships between Cryptocurrencies and Other Financial Assets. Econ. Lett. 2018, 165, 28–34. [Google Scholar] [CrossRef] [Green Version]

- Cheah, E.T.; Fry, J. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Econ. Lett. 2015, 130, 32–36. [Google Scholar] [CrossRef] [Green Version]

- Ji, Q.; Bouri, E.; Kristoufek, L.; Lucey, B. Realised volatility connectedness among Bitcoin exchange markets. Financ. Res. Lett. 2021, 38, 101391. [Google Scholar] [CrossRef]

- Dyhrberg, A.H. Bitcoin, gold and the dollar–A GARCH volatility analysis. Financ. Res. Lett. 2016, 16, 85–92. [Google Scholar] [CrossRef]

- Baur, A.W.; Bühler, J.; Bick, M.; Bonorden, C.S. Cryptocurrencies as a disruption? Empirical findings on user adoption and future potential of bitcoin and co. In Proceedings of the Conference on e-Business, e-Services and e-Society, Delft, The Netherlands, 13–15 October 2015; Springer: Cham, Switzerland, 2015; pp. 63–80. [Google Scholar]

- Dias, I.K.; Fernando, J.R.; Fernando, P.N.D. Does investor sentiment predict bitcoin return and volatility? A quantile regression approach. Int. Rev. Finan. Anal. 2022, 84, 102383. [Google Scholar] [CrossRef]

- Bouri, E.; Molnár, P.; Azzi, G.; Roubaud, D.; Hagfors, L.I. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Financ. Res. Lett. 2017, 20, 192–198. [Google Scholar] [CrossRef]

- Krolzig, H.M.; Hendry, D.F. Computer automation of general-to-specific model selection procedures. J. Econ. Dyn. Control 2001, 25, 831–866. [Google Scholar] [CrossRef] [Green Version]

- Lütkepohl, H. General-to-specific or specific-to-general modelling? An opinion on curent econometric terminology. J. Econom. 2007, 136, 319–324. [Google Scholar] [CrossRef]

- Orléan, A. La notion de valeur fondamentale est-elle indispensable à la théorie financière? Regards Croisés Sur L’économie 2008, 3, 120–128. [Google Scholar] [CrossRef]

- Treiblmaier, H. Do cryptocurrencies really have (no) intrinsic value? Electron. Mark. 2021, 32, 1749–1758. [Google Scholar] [CrossRef]

- Chaim, P.; Laurini, M.P. Is Bitcoin a bubble? Phys. A Stat. Mech. Appl. 2019, 517, 222–232. [Google Scholar] [CrossRef]

- Baek, C.; Elbeck, M. Bitcoins as an investment or speculative vehicle? A first look. Appl. Econ. Lett. 2015, 22, 30–34. [Google Scholar] [CrossRef]

- Chen, W.; Xu, H.; Jia, L.; Gao, Y. Machine learning model for Bitcoin exchange rate prediction using economic and technology determinants. Int. J. Forecast. 2021, 37, 28–43. [Google Scholar] [CrossRef]

- Panagiotidis, T.; Stengos, T.; Vravosinos, O. A principal component-guided sparse regression approach for the determination of bitcoin returns. J. Risk Financ. Manag. 2020, 13, 33. [Google Scholar] [CrossRef]

- Panagiotidis, T.; Stengos, T.; Vravosinos, O. On the determinants of bitcoin returns: A LASSO approach. Financ. Res. Lett. 2018, 27, 235–240. [Google Scholar] [CrossRef]

- Kapar, B.; Olmo, J. Analysis of Bitcoin prices using market and sentiment variables. World Econ. 2021, 44, 45–63. [Google Scholar] [CrossRef]

- Klose, J. Comparing cryptocurrencies and gold-a system-GARCH-approach. Eurasian Econ. Rev. 2022, 12, 653–679. [Google Scholar] [CrossRef]

- Brauneis, A.; Mestel, R.; Riordan, R.; Theissen, E. Bitcoin unchained: Determinants of cryptocurrency exchange liquidity. J. Empir. Financ. 2022, 69, 106–122. [Google Scholar] [CrossRef]

- Ciner, C.; Lucey, B.; Yarovaya, L. Determinants of cryptocurrency returns: A Lasso quantile regression approach. Financ. Res. Lett. 2022, 49, 102990. [Google Scholar] [CrossRef]

- Li, X.; Wang, C.A. The technology and economic determinants of cryptocurrency exchange rates: The case of Bitcoin. Decis. Support Syst. 2017, 95, 49–60. [Google Scholar] [CrossRef]

- Panagiotidis, T.; Stengos, T.; Vravosinos, O. The effects of markets, uncertainty and search intensity on bitcoin returns. Int. Rev. Financ. Anal. 2019, 63, 220–242. [Google Scholar] [CrossRef]

- Mokni, K.; Youssef, M.; Ajmi, A.N. COVID-19 pandemic and economic policy uncertainty: The first test on the hedging and safe haven properties of cryptocurrencies. Res. Int. Bus. Financ. 2022, 60, 101573. [Google Scholar] [CrossRef]

- Briere, M.; Oosterlinck, K.; Szafarz, A. Virtual currency, tangible return: Portfolio diversification with bitcoin. J. Asset Manag. 2015, 16, 365–373. [Google Scholar] [CrossRef]

- Guesmi, K.; Saadi, S.; Abid, I.; Ftiti, Z. Portfolio diversification with virtual currency: Evidence from bitcoin. Int. Rev. Financ. Anal. 2019, 63, 431–437. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Tiwari, A.K.; Roubaud, D. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Financ. Res. Lett. 2017, 23, 87–95. [Google Scholar] [CrossRef] [Green Version]

- Demir, E.; Gozgor, G.; Lau, C.K.M.; Vigne, S.A. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Res. Lett. 2018, 26, 145–149. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Y.; Wang, G.J.; Wen, D.Y.; Yang, X.G. Business conditions, uncertainty shocks and Bitcoin returns. Evol. Inst. Econ. Rev. 2020, 17, 415–424. [Google Scholar] [CrossRef]

- Yen, K.C.; Cheng, H.P. Economic policy uncertainty and cryptocurrency volatility. Financ. Res. Lett. 2021, 38, 101428. [Google Scholar] [CrossRef]

- Wu, W.; Tiwari, A.K.; Gozgor, G.; Leping, H. Does economic policy uncertainty affect cryptocurrency markets? Evidence from Twitter-based uncertainty measures. Res. Int. Bus. Financ. 2021, 58, 101478. [Google Scholar] [CrossRef]

- Aharon, D.Y.; Demir, E.; Lau, C.K.M.; Zaremba, A. Twitter-Based uncertainty and cryptocurrency returns. Res. Int. Bus. Financ. 2022, 59, 101546. [Google Scholar] [CrossRef]

- Kristoufek, L. BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Sci. Rep. 2013, 3, 3415. [Google Scholar] [CrossRef] [Green Version]

- Ciaian, P.; Rajcaniova, M. The digital agenda of virtual currencies: Can BitCoin become a global currency? Inf. Syst. e-Bus. Manag. 2016, 14, 883–919. [Google Scholar] [CrossRef] [Green Version]

- Polasik, M.; Piotrowska, A.I.; Wisniewski, T.P.; Kotkowski, R.; Lightfoot, G. Price fluctuations and the use of bitcoin: An empirical inquiry. Int. J. Electron. Commer. 2015, 20, 9–49. [Google Scholar] [CrossRef] [Green Version]

- Bouteska, A.; Mefteh-Wali, S.; Dang, T. Predictive power of investor sentiment for Bitcoin returns: Evidence from COVID-19 pandemic. Technol. Forecast. Soc. Change 2022, 184, 121999. [Google Scholar] [CrossRef]

- Güler, D. The Impact of investor sentiment on bitcoin returns and conditional volatilities during the era of COVID-19. J. Behav. Financ. 2021, 1–14. [Google Scholar] [CrossRef]

- Naeem, M.A.; Mbarki, I.; Shahzad, S.J.H. Predictive role of online investor sentiment for cryptocurrency market: Evidence from happiness and fears. Int. Rev. Econ. Financ. 2021, 73, 496–514. [Google Scholar] [CrossRef]

- Bouri, E.; Gabauer, D.; Gupta, R.; Tiwari, A.K. Volatility connectedness of major cryptocurrencies: The role of investor happiness. J. Behav. Exp. Financ. 2021, 30, 100463. [Google Scholar] [CrossRef]

- Eom, C.; Kaizoji, T.; Kang, S.H.; Pichl, L. Bitcoin and investor sentiment: Statistical characteristics and predictability. Phys. A Stat. Mech. Appl. 2019, 514, 511–521. [Google Scholar] [CrossRef]

- Figa-Talamanca, G.; Patacca, M. Does market attention affect Bitcoin returns and volatility? Decis. Econ. Financ. 2019, 42, 135–155. [Google Scholar] [CrossRef]

- Hayes, A.S. Cryptocurrency value formation: An empirical study leading to a cost of production model for valuing bitcoin. Telemat. Inform. 2017, 34, 1308–1321. [Google Scholar] [CrossRef]

- Adjei, F. Determinants of Bitcoin Expected Returns. J. Financ. Econ. 2019, 7, 42–47. [Google Scholar] [CrossRef] [Green Version]

- Castle, J.L.; Doornik, J.A.; Hendry, D.F. Robust discovery of regression models. Econ. Stat. 2021, in press. [Google Scholar] [CrossRef]

- Hoover, K.D.; Perez, S.J. Data mining reconsidered: Encompassing and the general-to-specific approach to specification search. Econom. J. 1999, 2, 167–191. [Google Scholar] [CrossRef]

- Pagan, A. Three Econometric Methodologies: A Critical Appraisal. J. Econ. Surv. 1987, 1, 3–24. [Google Scholar] [CrossRef]

- Campos, J.; Ericsson, N.R.; Hendry, D.F. General-to-specific modeling: An overview and selected bibliography. FRB Int. Financ. Discuss. Pap. 2005, 838. [Google Scholar] [CrossRef] [Green Version]

- Hendry, D.F.; Doornik, J. Empirical Model Discovery and Theory Evaluation; The MIT Press: London, UK, 2014. [Google Scholar]

- Castle, J.L.; Doornik, J.A.; Hendry, D.F. Evaluating Automatic Model Selection. J. Time Ser. Econ. 2011, 3, 1–31. [Google Scholar] [CrossRef] [Green Version]

- Pretis, F.; Reade, J.J.; Sucarrat, G. Automated general-to-specific (GETS) regression modeling and indicator saturation for outliers and structural breaks. J. Stat. Softw. 2018, 86, 1–44. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. J. Financ. 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Newey, W.; West, K. A Simple Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica 1987, 55, 703–708. [Google Scholar] [CrossRef]

- Aggarwal, C.C. Data Mining: The Textbook; Springer: New York, NY, USA, 2015. [Google Scholar]

- Bashir, H.A.; Kumar, D. Investor attention, Twitter uncertainty and cryptocurrency market amid the COVID-19 pandemic. Manag. Financ. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Barson, Z.; Junior, P.O.; Adam, A.M.; Asafo-Adjei, E. Connectedness between Gold and Cryptocurrencies in COVID-19 Pandemic: A Frequency-Dependent Asymmetric and Causality Analysis. Complexity 2022, 2022, 7648085. [Google Scholar] [CrossRef]

- Palazzi, R.B.; Júnior, G.D.S.R.; Klotzle, M.C. The dynamic relationship between bitcoin and the foreign exchange market: A nonlinear approach to test causality between bitcoin and currencies. Financ. Res. Lett. 2021, 42, 101893. [Google Scholar] [CrossRef]

- Wang, P.; Li, X.; Shen, D.; Zhang, W. How does economic policy uncertainty affect the Bitcoin market? Res. Int. Bus. Financ. 2020, 53, 101234. [Google Scholar] [CrossRef]

- Kelly, F. Why You Win or Lose: The Psychology of Speculation; Houghton Mifflin: Boston, MA, USA, 1930. [Google Scholar]

- Zilca, S. The evolution and cross-section of the day-of-the-week effect. Financ. Innov. 2017, 3, 1–12. [Google Scholar] [CrossRef]

- Aharon, D.Y.; Qadan, M. Bitcoin and the day-of-the-week effect. Financ. Res. Lett. 2019, 31. [Google Scholar] [CrossRef]

- Sucarrat, G.; Grønneberg, S.; Escribano, A. Estimation and inference in univariate and multivariate log-GARCH-X models when the conditional density is unknown. Comput. Stat. Data Anal. 2016, 100, 582–594. [Google Scholar] [CrossRef] [Green Version]

- Wu, C.C.; Ho, S.L.; Wu, C.C. The determinants of Bitcoin returns and volatility: Perspectives on global and national economic policy uncertainty. Financ. Res. Lett. 2022, 45, 102175. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Data | Methodology | Results |

|---|---|---|---|

| Polasik et al. [40] | July 2010–March 2014 (Bitcoin) 10 variables | Ordinary and Tobit regressions | Newspaper reports (+) The tone (+) Google trends (+) Total number of transactions (+) |

| Ciaian et al. [39] | 2009–2014 (Bitcoin) 9 variables | Cointegration Short term and long term | Bitcoin attractiveness indicators |

| Dyhrberg [10] | July 2010–May 2015 | GARCH-E | USD/GBP (−)FTSE (+) FED fund rate (+) USD/EUR (+) |

| Hayes [47] | 18 September 2014 (66 cryptocurrencies) 7 variables | OLS regression (Ordinary Least Squares) | Costs of production (−) Computational power (+) |

| Li and Wang [27] | 1 January 2011–12 December 2014 (2 periods) Bitcoin 13 variables | The autoregressive distributed lag (ARDL) model | Trading volume of Bitcoin (+) Bitcoin transaction value (+) Bitcoin transactions volume (−) US interest rate (+) |

| Bouri et al. [32] | 17 March 2011–17 October 2016, Bitcoin 1 variable | Wavelet multiscale decomposition, and Quantile on Quantile regression | Uncertainty (WVIX) (−) |

| Panagiotidis et al. [22] | 24 July 2010–23 June 2017 (3 periods) Bitcoin 21 variables | least absolute shrinkage and selection operator (lasso) | Economic Policy Uncertainty (−) Exchange rates (+) Interest rates (ECB) (+) Gold and oil (+) |

| Adjei [48] | 17 July 2010–28 Februray 2018 Bitcoin 5 variables | Garch-M | Mining difficulty (−) Block size (−) Number of transactions (+) |

| Panagiotidis et al. [21] | 21 July 2010–31 May 2018 (3 periods) Bitcoin 41 variables | (PC-LASSO) | Economic policy uncertainty Stock market volatility |

| Chen et al. [20] | August 2011–July 2018 (4 Periods) Bitcoin 24 variables | VAR OLS Quantile Regression | Market indices; exchange rates, market capitalization, transactions fees; Transaction value; Internet searches; oil and gold; block size. |

| Guler [42] |

January 2014–August 2020

5 variables |

VAR model

GARCH CGARCH EGARCH AP-ARCH GJR-GARCH | Trading volumes |

| Kapar and Olmo [23] | 22 July 2010–19 May 2019 (2 periods) 4 variables | VECM | The S and P 500 index, gold, Google searches Fear index |

| Wu et al. [36] | 9 August 2015–17 July 2020 (Bitcoin, Ethereum, Litecoin, and) 2 variables | Granger causality | EPU (+) |

| Yen and Cheng [35] | February 2014–June2019 4 variables | Stochastic volatility model | EPU of China(−) |

| Aharon et al. [37] | 29 April 2013–14 July2020 (Bitcoin), 7 August 2015–14 July 2020 (Ethereum) 4 August 2013–14 July 2020 (Ripple) 23 July 2017–14 July 2020 (Bitcoin Cash) | OLS, GARCH, Quantile and Causality in Quantiles | Uncertainty in social media |

| Bouteska et al. [41] | 1 January 2015–31 October 2020 10 variables | Vector Autoregressive Analysis | The sentiment index |

| Abbreviation | Variable | Sources |

|---|---|---|

| rBTC | bitcoin return | https://coinmetrics.io/ (accessed on 2 June 2022) |

| ADS | the Aruoba–Diebold–Scotti business conditions index | https://www.philadelphiafed.org/surveys-and-data/real-time-data-research/ads (accessed on 2 June 2022) |

| logTEU | log of Twitter-based economic uncertainty index | https://www.policyuncertainty.com/twitter_uncert.html (accessed on 2 June 2022) |

| logTMU | log of Twitter-based Market Uncertainty index (TMU) | https://www.policyuncertainty.com/twitter_uncert.html (accessed on 2 June 2022) |

| logEPU | log of economic policy uncertainty | |

| Rgold | return of gold | Datastream |

| Rwti | return of wti | https://www.eia.gov/ (accessed on 2 June 2022) |

| loggbtc | log of Google trend for Bitcoin | https://trends.google.com (accessed on 2 June 2022) |

| logwbtc | log of Wikipedia trend for Bitcoin | https://www.wikishark.com (accessed on 2 June 2022) |

| DFF | the federal funds rate | https://fred.stlouisfed.org (accessed on 2 June 2022) https://www.federalreserve.gov/ (accessed on 2 June 2022) |

| ECB | daily, ECB Deposit facility—date of changes (raw data), level | https://www.ecb.europa.eu (accessed on 2 June 2022) |

| rGBP | return GBP/USD exchange rate | https://fred.stlouisfed.org/ (accessed on 2 June 2022) Federal Reserve Economic Data |

| Reuro | return Euro/USD exchange rate | |

| rYen | return Yen/USD exchange rate | |

| rCNY | return CNY/USD exchange rate | |

| rDow Jones | return of Dow Jones stock exchange index USA market | Datastream |

| rs&P | return of Standard and Poor’s 500 stock exchange index USA market | |

| rnasdaq | return of Nasdaq stock exchange index USA market | |

| Rdax | return of Dax stock exchange index Germany | |

| rftse100 | return of Ftse stock exchange index GB | |

| rnekkei225 | return of stock exchange index Japan | |

| rshanghai | return of stock exchange index China | |

| Rvix | return of CBOE S&P500 Volatility Index—Close | |

| logBTCMC | log of Bitcoin market capitalisation | https://coinmetrics.io/ (accessed on 2 June 2022) |

| logBTCVOLM | log of Bitcoin volume stock exchange | |

| logBTCVlty | log of Bitcoin volatility 30 day | |

| logBTCASply | log of Bitcoin active supply 1 day | |

| logBTCAddr | log of Bitcoin active address | |

| logBTC Tfees | Log of Bitcoin total fees | |

| logBTCMinerRev | log pf Bitcoin miner revenue | |

| logBTCDflty | log of Bitcoin mining difficulty | |

| logBTCHash | log of Bitcoin hash rate |

| COEF | STD.ERROR | T-STAT | p-Value | |

|---|---|---|---|---|

| mconst | −0.24833641 | 0.29189157 | −0.8508 | 0.3950163 |

| dummy_Monday | −0.00244744 | 0 0.00201489 | −1.2147 | 0.2246666 |

| dummy_Tuesday | 0.00245124 | 0.00508857 | 0.4817 | 0.6300735 |

| dummy_Wednesday | 0.00115776 | 0.00227812 | 0.5082 | 0.6113759 |

| dummy_Thursday | −0.00165866 | 0.00335336 | −0.4946 | 0.6209310 |

| dummy_Friday | 0.00249514 | 0.00371173 | 0.6722 | 0.5015343 |

| dummy_Saturday | 0.00627863 | 0.00506968 | 1.2385 | 0.2157231 |

| ADS | −0.00036612 | 0.00029886 | −1.2251 | 0.2207279 |

| logTEU | 0.00653662 | 0.00377787 | 1.7302 | 0.0837791 * |

| logTMU | −0.00426973 | 0.00298737 | −1.4293 | 0.1531233 |

| logEPU | 0.00172762 | 0.00258747 | 0.6677 | 0.5044274 |

| rgold | 0.26335969 | 0.09671010 | 2.7232 | 0.0065353 *** |

| rwti | 0.02880190 | 0.02652524 | 1.0858 | 0.2777167 |

| loggbtc | 0.00365110 | 0.00233055 | 1.5666 | 0.1173982 |

| logwbtc | −0.00567614 | 0.00387748 | −1.4639 | 0.1434241 |

| DFF | 0.00513509 | 0.00260848 | 1.9686 | 0.0491689 ** |

| ECB | −0.06292176 | 0.04414792 | −1.4252 | 0.1542790 |

| rGBP | 0.18460286 | 0.22266852 | 0.8290 | 0.4072002 |

| Reuro | 0.01241261 | 0.00455040 | 2.7278 | 0.0064449 *** |

| rYen | −0.54661047 | 0.26355589 | −2.0740 | 0.0382394 ** |

| rCNY | 0.92177202 | 0.56191690 | 1.6404 | 0.1011159 |

| rDow.Jones | 0.47624933 | 0.49490927 | 0.9623 | 0.3360452 |

| rs.P | −1.22631784 | 0.81746151 | −1.5002 | 0.1337706 |

| Rnasdaq | 1.21263845 | 0.33222624 | 3.6500 | 0.0002706 *** |

| rdax | −0.00043787 | 0.00090514 | −0.4838 | 0.6286200 |

| rftse100 | 0.50169621 | 0.25169685 | 1.9933 | 0.0464019 ** |

| rnekkei225 | −0.15344150 | 0.10534513 | −1.4566 | 0.1454328 |

| rshanghai | −0.09109219 | 0.11031150 | −0.8258 | 0.4090555 |

| Rvix | −0.01705950 | 0.03575111 | −0.4772 | 0.6333031 |

| logBTCMC | 0.00981076 | 0.00820393 | 1.1959 | 0.2319267 |

| logBTCVOLM | −0.00262009 | 0.00326415 | −0.8027 | 0.4222745 |

| logBTCASply | −0.00346672 | 0.00622121 | −0.5572 | 0.5774393 |

| logBTC.Addr | 0.02022164 | 0.01605289 | 1.2597 | 0.2079644 |

| logBTC.Tfees | 0.00082320 | 0.00257831 | 0.3193 | 0.7495569 |

| logBTCMinerRev | 0.00252428 | 0.00868958 | 0.2905 | 0.7714747 |

| logBTCDflty | −0.00179025 | 0.01706709 | −0.1049 | 0.9164723 |

| logBTCHash | −0.01067656 | 0.01650652 | −0.6468 | 0.5178478 |

| Chi-sq df | df | p-Value | |

|---|---|---|---|

| Ljung-Box AR(1) | 0.79124 | 1 | 0.3737264 |

| Ljung-Box ARCH(1) | 10.25477 | 1 | 0.0013633 |

| COEF | STD.ERROR | T-STAT | p-Value | |

|---|---|---|---|---|

| mconst | 0.0138258 | 0.0165001 | 0.8379 | 0.402196 |

| logTEU | 0.0057297 | 0.0025216 | 2.2722 | 0.023203 ** |

| rgold | 0.2759225 | 0.0961848 | 2.8687 | 0.004175 *** |

| reuro | 0.0109965 | 0.0041673 | 2.6387 | 0.008400 *** |

| rnasdaq | 0.7798533 | 0.1697237 | 4.5948 | 4.662 × 10−6 *** |

| logBTCMC | 0.0077049 | 0.0027146 | 2.8383 | 0.004592 *** |

| logBTCDflty | −0.0080921 | 0.0025693 | −3.1496 | 0.001665 *** |

| Chi-sq df | df | p-Value | |

|---|---|---|---|

| Ljung-Box AR(1) | 0.40993 | 1 | 0.52201 |

| Ljung-Box ARCH(1) | 5.84535 | 1 | 0.01562 |

| REG.NO | KEEP | COEF | STD.ERROR | T-STAT | p-Value | |

|---|---|---|---|---|---|---|

| vconst | 1 | 1 | −5.9457940 | 0.8489236 | −7.003921 | 2.489 × 10−12 *** |

| arch1 | 2 | 0 | 0.0441647 | 0.0258502 | 1.7085 | 0.0877380 * |

| arch2 | 3 | 0 | 0.0954482 | 0.0258276 | 3.6956 | 0.0002267 *** |

| arch3 | 4 | 0 | 0.0664196 | 0.0258573 | 2.5687 | 0.0102969 ** |

| arch4 | 5 | 0 | 0.0604699 | 0.0258301 | 2.3411 | 0.0193494 ** |

| arch5 | 6 | 0 | 0.0713215 | 0.0247608 | 2.8804 | 0.0040236 *** |

| arch6 | 7 | 0 | 0.0217819 | 0.0247235 | 0.8810 | 0.3784367 |

| arch7 | 8 | 0 | 0.0391956 | 0.0246798 | 1.5882 | 0.1124432 |

| asym1 | 9 | 0 | 0.0257971 | 0.0141180 | 1.8273 | 0.0678458 ** |

| asym2 | 10 | 0 | −0.0095816 | 0.0141283 | −0.6782 | 0.4977499 |

| asym3 | 11 | 0 | −0.0026120 | 0.0141296 | −0.1849 | 0.8533644 |

| asym4 | 12 | 0 | 0.0153561 | 0.0141189 | 1.0876 | 0.2769183 |

| dummy_Monday | 13 | 0 | −0.0255993 | 0.1300362 | −0.1969 | 0.8439593 |

| dummy_Tuesday | 14 | 0 | −0.2155196 | 0.3149476 | −0.6843 | 0.4938817 |

| dummy_Wednesday | 15 | 0 | −0.0607081 | 0.1299821 | −0.4670 | 0.6405271 |

| dummy_Thursday | 16 | 0 | −0.0415888 | 0.2238933 | −0.1858 | 0.8526618 |

| dummy_Friday | 17 | 0 | −0.1141483 | 0.2236385 | −0.5104 | 0.6098306 |

| dummy_Saturday | 18 | 0 | −0.2671189 | 0.3164035 | −0.8442 | 0.3986626 |

| logBTCVOLM | 19 | 0 | 0.1345515 | 0.0281129 | 4.7861 | 1.855 × 10−6 *** |

| Chi-sq | df | p-Value | |

|---|---|---|---|

| Ljung-Box AR(1) | 0.26908 | 1 | 0.60395 |

| Ljung-Box ARCH(8) | 4.59953 | 8 | 0.79940 |

| Specifications | Regressors’ Numbers | ||||||

|---|---|---|---|---|---|---|---|

| Specification 1 | 1 | 3 | 4 | 5 | 6 | 19 | - |

| Specification 2 | 1 | 3 | 4 | 5 | 6 | 9 | 19 |

| Specification 3 | 1 | 2 | 3 | 4 | 5 | 6 | 19 |

| Info (sc) | Logl | n | K | |

|---|---|---|---|---|

| spec 1 (1-cut) | −3.384580 | 2799.257 | 1641 | 6 |

| spec 2 | −3.390194 | 2807.565 | 1641 | 7 |

| spec 3 | −3.394228 | 2810.875 | 1641 | 7 |

| COEF | STD.ERROR | T-STAT | p-Value | |

|---|---|---|---|---|

| vconst | −6.304240 | 0.808949 | −7.793124 | 6.537 × 10−15 *** |

| arch1 | 0.059799 | 0.024603 | 2.4306 | 0.0151828 * |

| arch2 | 0.094069 | 0.024552 | 3.8314 | 0.0001322 *** |

| arch3 | 0.072226 | 0.024588 | 2.9374 | 0.0033560 ** |

| arch4 | 0.072727 | 0.024534 | 2.9643 | 0.0030774 ** |

| arch5 | 0.074626 | 0.024535 | 3.0416 | 0.0023911 ** |

| logBTCVOLM | 0.138338 | 0.027829 | 4.9711 | 7.358 × 10−7 *** |

| Chi-sq | df | p-Value | |

|---|---|---|---|

| Ljung-Box AR(1) | 0.30148 | 1 | 0.5830 |

| Ljung-Box ARCH(8) | 4.08423 | 8 | 0.8494 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Benhamed, A.; Messai, A.S.; El Montasser, G. On the Determinants of Bitcoin Returns and Volatility: What We Get from Gets? Sustainability 2023, 15, 1761. https://doi.org/10.3390/su15031761

Benhamed A, Messai AS, El Montasser G. On the Determinants of Bitcoin Returns and Volatility: What We Get from Gets? Sustainability. 2023; 15(3):1761. https://doi.org/10.3390/su15031761

Chicago/Turabian StyleBenhamed, Adel, Ahlem Selma Messai, and Ghassen El Montasser. 2023. "On the Determinants of Bitcoin Returns and Volatility: What We Get from Gets?" Sustainability 15, no. 3: 1761. https://doi.org/10.3390/su15031761