Heterogeneous Impacts of Policy Sentiment with Different Themes on Real Estate Market: Evidence from China

Abstract

:1. Introduction

2. Related Literature and Hypotheses

2.1. The Volatility in Real Estate Market

2.2. The Role of Media Sentiment in the Real Estate Market

2.3. Heterogeneous Impacts of Policies with Different Themes

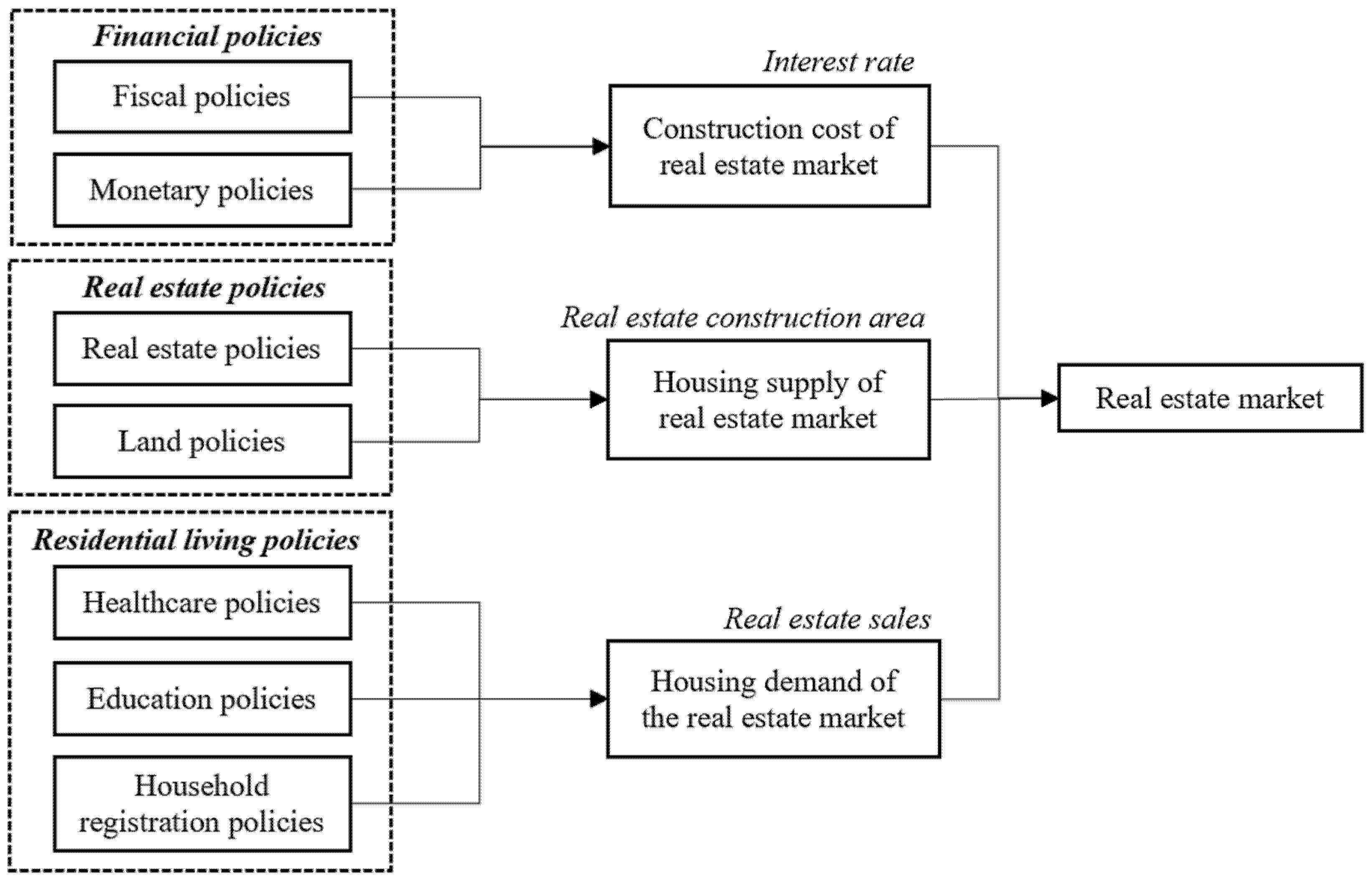

2.4. Impact Mechanism of Policies on Real Estate Price

3. Data and Methodology

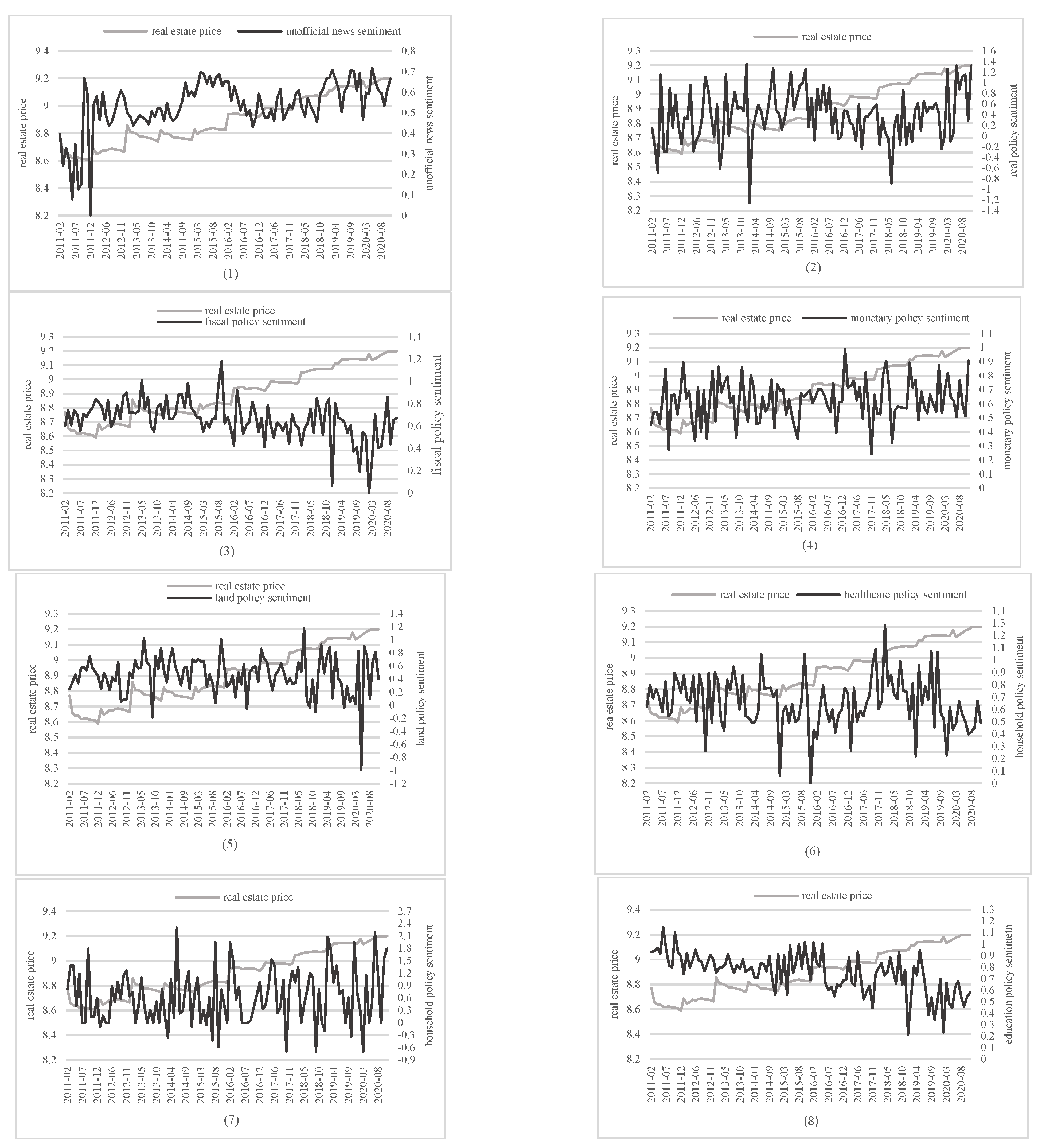

3.1. Data and Sentiment Index Construction

3.2. Heterogeneous Impacts of Policy Themes on Real Estate Price

3.3. Heterogeneous Impacts of Policy Themes on Real Estate Market Volatility

4. Empirical Results

4.1. Measuring Policy Sentiment

4.2. Real Estate Market Price Models

4.3. Real Estate Market Volatility Models

5. Heterogeneous Effects during Different Periods

6. Asymmetric Effect Analysis

7. Robustness Tests

7.1. Replacing the Dependable Variable

7.2. Addressing the Endogeneity of Policy Sentiment

8. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Su, X.; Zhu, Q. State intervention in land supply and its impact on real estate investment in China: Evidence from prefecture-level cities. Sustainability 2020, 12, 1019. [Google Scholar] [CrossRef] [Green Version]

- Wei, Y.; Patrick, T.L.; Chiang, Y.H.; Leung, B.Y.; Seabrooke, W. An exploratory analysis of impediments to China’s credit control on the real estate industry: An institutional perspective. J. Contemp. China 2013, 23, 44–67. [Google Scholar] [CrossRef]

- Kishor, N.K.; Marfatia, H.A. The time-varying response of foreign stock markets to U.S. monetary policy surprises: Evidence from the federal funds futures market. J. Int. Financ. Mark. Inst. Money 2012, 24, 1–24. [Google Scholar] [CrossRef]

- Belgacem, A.; Creti, A.; Guesmi, K.; Lahiani, A. Volatility spillovers and macroeconomic announcements: Evidence from crude oil markets. Appl. Econ. 2015, 47, 2974–2984. [Google Scholar] [CrossRef]

- Cakan, E.; Doytch, N.; Upadhyaya, K.P. Does U.S. macroeconomic news make emerging financial markets riskier? Borsa Istanb. Rev. 2015, 15, 37–43. [Google Scholar] [CrossRef] [Green Version]

- Caporale, G.M.; Spagnolo, F.; Spagnolo, N. Macro news and commodity returns. Int. J. Financ. Econ. 2017, 22, 68–80. [Google Scholar] [CrossRef] [Green Version]

- Shleifer, A.; Summers, L.H. The noise trader approach to finance. J. Econ. Perspect. 1990, 4, 19–33. [Google Scholar] [CrossRef] [Green Version]

- Verma, R.; Soydemir, G. The impact of individual and institutional investor sentiment on the market price of risk. Q. Rev. Econ. Financ. 2009, 49, 1129–1145. [Google Scholar] [CrossRef]

- Shen, S.; Zhao, Y.; Pang, J. Local Housing market sentiments and returns: Evidence from China. J. Real Estate Financ. Econ. 2022, 25, 30–40. [Google Scholar] [CrossRef]

- Dolde, W.; Tirtiroglue, D. Temporal and spatial information diffusion in real estate price changes and variances. Real Estate Econ. 1997, 25, 539–565. [Google Scholar] [CrossRef]

- Dolde, W.; Tirtiroglue, D. Housing price volatility changes and their effects. Real Estate Econ. 2002, 30, 41–66. [Google Scholar] [CrossRef]

- Capozza, D.R.; Hendershott, P.H.; Mack, C. An anatomy of price dynamics in illiquid markets: Analysis and evidence from local housing markets. Real Estate Econ. 2004, 32, 1–32. [Google Scholar] [CrossRef] [Green Version]

- Crawford, G.W.; Fratantoni, M.C. Assessing the forecasting performance of regime- switching, ARIMA and GARCH Models of house prices. Real Estate Econ. 2003, 31, 223–243. [Google Scholar] [CrossRef]

- Miller, N.; Peng, L. Exploring metropolitan housing price volatility. J. Real Estate Financ. Econ. 2006, 33, 5–18. [Google Scholar] [CrossRef] [Green Version]

- Lee, C.L. Housing price volatility and its determinants. Int. J. Hous. Mark. Anal. 2009, 2, 293–308. [Google Scholar]

- Ghosh, S. Housing price volatility: Uncertainty, an asymmetric econometric analysis–some European country experiences. Int. J. Hous. Mark. Anal. 2021, 14, 1004–1026. [Google Scholar] [CrossRef]

- Yang, Y.; Rehm, M.; Zhou, M. Housing price volatility: What's the difference between investment and owner-occupancy? Econ. Rec. 2021, 97, 548–563. [Google Scholar] [CrossRef]

- Lee, C.L.; Reed, R.G. The Relationship between housing market intervention for first-time buyers and house price volatility. Hous. Stud. 2014, 29, 1073–1095. [Google Scholar] [CrossRef] [Green Version]

- Stephens, M. Tackling Housing Market Volatility in the UK: A Progress Report; Joseph Rowntree Foundation: North Yorkshire, UK, 2011. [Google Scholar]

- Ma, Y.; Xu, B.; Xu, X. Real estate confidence index based on real estate news. Emerg. Mark. Financ. Trade 2017, 54, 747–760. [Google Scholar] [CrossRef]

- Kang, H.; Lee, K.; Shin, D.H. Short-term forecast model of apartment jeonse prices using search frequencies of news article keywords. KSCE J. Civ. Eng. 2019, 23, 4984–4991. [Google Scholar] [CrossRef]

- Beracha, E.; Lang, M.; Hausier, J. On the relationship between market sentiment and commercial real estate performance-A textual analysis examination. J. Real Estate Res. 2019, 41, 605–638. [Google Scholar] [CrossRef]

- Bonato, M.; Çepni, O.; Gupta, R.; Pierdzioch, C. Uncertainty due to infectious diseases and forecastability of the realized variance of united states real estate investment trusts: A note. Int. Rev. Financ. 2021, 7, 1–11. [Google Scholar] [CrossRef]

- Mercille, J. The role of the media in sustaining Ireland's housing bubble. New Political Econ. 2013, 19, 282–301. [Google Scholar] [CrossRef]

- Baker, S.A.; Wade, M.; Walsh, M.J. The challenges of responding to misinformation during a pandemic: Content moderation and the limitations of the concept of harm. Media Int. Aust. 2020, 177, 103–107. [Google Scholar] [CrossRef]

- Liu, P.; Xia, X.; Li, A. Tweeting the financial market: Media effect in the era of big data. Pac. -Basin Financ. J. 2018, 51, 267–290. [Google Scholar] [CrossRef]

- Yu, Y.; Duan, W.; Cao, Q. The impact of social and conventional media on firm equity value: A sentiment analysis approach. Decis. Support Syst. 2013, 55, 919–926. [Google Scholar] [CrossRef]

- Goukasian, L.; Majbouri, M. The reaction of real estate–related industries to the monetary policy actions. Real Estate Econ. 2010, 38, 355–398. [Google Scholar] [CrossRef]

- Zhang, X.; Pan, F. Asymmetric effects of monetary policy and output shocks on the real estate market in China. Econ. Model. 2021, 103, 105600. [Google Scholar] [CrossRef]

- Ahmed, I.; Socci, C.; Severini, F.; Pretaroli, R.; Al Mahdi, H.K. Unconventional monetary policy and real estate sector: A financial dynamic computable general equilibrium model for Italy. Econ. Syst. Res. 2019, 32, 221–238. [Google Scholar] [CrossRef]

- Manganelli, B.; Morano, P.; Rosato, P.; Paola, P.D. The effect of taxation on investment demand in the real estate market: The Italian experience. Buildings 2020, 10, 115. [Google Scholar] [CrossRef]

- Hofman, A.; Manuel, B.A. A finance- and real estate-driven regime in the United Kingdom. Geoforum 2019, 100, 89–100. [Google Scholar] [CrossRef]

- Zhang, R.; Ma, W. Assessing the role of reward and punishment mechanism in house price regulation in China: A game-theoretic approach. J. Urban Plan. Dev. 2020, 146, 1–11. [Google Scholar] [CrossRef]

- Zhang, C. Money, housing, and inflation in China. J. Policy Model. 2013, 35, 75–87. [Google Scholar] [CrossRef]

- Sunega, P.; Lux, M.; Zemčík, P. Housing price volatility and econometrics. Crit. Hous. Anal. 2014, 1, 70–78. [Google Scholar] [CrossRef]

- Alexander, E. Land-property markets and planning: A special case. Land Use Policy 2014, 41, 533–540. [Google Scholar] [CrossRef]

- Xu, X.E.; Chen, T. The effect of monetary policy on real estate price growth in China. Pac. -Basin Financ. J. 2012, 20, 62–77. [Google Scholar] [CrossRef]

- Antweiler, W.; Frank, M.Z. Is all that talk just noise? The information content of internet stock message boards. J. Financ. 2004, 59, 1259–1294. [Google Scholar] [CrossRef]

- Lee, W.Y.; Jiang, C.X.; Indro, D.C. Stock market volatility excess returns, and the role of investor sentiment. Bank Financ. 2002, 26, 2277–2299. [Google Scholar] [CrossRef]

- Uygur, U.; Taş, O. The impacts of investor sentiment on returns and conditional volatility of international stock markets. Qual. Quant. 2013, 48, 1165–1179. [Google Scholar] [CrossRef]

- Bahloul, W.; Bouri, A. Profitability of return and sentiment-based investment strategies in US futures markets. Res. Int. Bus. Financ. 2016, 36, 254–270. [Google Scholar] [CrossRef]

- Fritz, M.S.; Mackinnon, D.P. Required sample size to detect the mediated effect. Psychol. Sci. 2007, 18, 233–239. [Google Scholar] [CrossRef]

- Huang, Y.; Yang, C.; Baek, H.; Lee, S.G. Erratum to: Revisiting media selection in the digital era: Adoption and usage. Serv. Bus. 2016, 10, 261. [Google Scholar] [CrossRef] [Green Version]

- Chatrath, A.; Miao, H.; Ramchander, S. Does the price of crude oil respond to macroeconomic news? J. Futur. Mark. 2012, 32, 536–559. [Google Scholar] [CrossRef]

- Li, J.; Wang, Y.; Liu, C. Spatial effect of market sentiment on housing price: Evidence from social media data in China. Int. J. Strateg. Prop. Manag. 2022, 26, 72–85. [Google Scholar] [CrossRef]

- Ahmed, I.; Socci, C.; Medabesh, A.; Severini, F.; Zotti, J. MP Economic impact of monetary policy: Focus on real estate sector in Italy. Int. J. Financ. Econ. 2021, 26, 1256–1269. [Google Scholar] [CrossRef]

- Barnhart, S.W. The effects of macroeconomic announcements on commodity prices. Am. J. Agric. Econ. 1989, 71, 389–403. [Google Scholar] [CrossRef]

- Cai, J.; Cheung, Y.L.; Wong, M. What moves the gold market? J. Futur. Mark. 2001, 21, 257–278. [Google Scholar] [CrossRef]

- Liu, C.H.; Nowak, A.; Rosenthal, S.S. Housing price bubbles, new supply, and within-city dynamics. J. Urban Econ. 2016, 96, 55–72. [Google Scholar] [CrossRef]

- Walker, C.B. Housing booms and media coverage. Appl. Econ. 2014, 46, 3954–3967. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Name | Obs. | Mean | S.E. | Min | Max |

|---|---|---|---|---|---|

| Unofficial media sentiment | 139 | 0.588 | 0.262 | 0 | 1.792 |

| Real estate policy sentiment | 113 | 0.386 | 0.491 | −1.253 | 1.353 |

| Fiscal policy sentiment | 109 | 0.660 | 0.175 | 0.005 | 1.182 |

| Monetary policy sentiment | 148 | 0.654 | 0.247 | 0 | 2.079 |

| Land policy sentiment | 125 | 0.478 | 0.297 | −0.980 | 1.334 |

| Healthcare policy sentiment | 120 | 0.667 | 0.216 | 0.001 | 1.283 |

| Household registration sentiment | 123 | 0.730 | 0.645 | −0.693 | 2.303 |

| Education policy sentiment | 120 | 0.757 | 0.166 | 0.214 | 1.145 |

| Variables | Financial Policies | Variables | Real Estate Policies | Variables | Residential Living Policies | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |||

| Dependent variable | Real estate price | Interest rate | Real estate price | Dependent variable | Real estate price | Real estate construction | Real estate price | Dependent variable | Real estate price | Real estate sales | Real estate price |

| Financial policies | −0.457 *** (−5.121) | 1.178 ** (2.613) | −0.315 *** (−4.294) | Real estate policies | 0.021 (0.607) | 0.107 ** (2.462) | −0.048 ** (−2.233) | Residential living policies | −0.642 *** (−7.983) | −1.633 *** (−3.634) | −0.564 *** (−6.838) |

| Interest rate | −0.121 *** | Real estate | 0.649 *** | Real estate sales | 0.047 *** | ||||||

| (−7.909) | construction | (13.910) | (2.819) | ||||||||

| N | 109 | 109 | 109 | N | 109 | 109 | 109 | N | 109 | 109 | 109 |

| _cons | 9.198 *** | 2.270 *** | 9.471 *** | _Cons | 8.887 *** | 13.309 *** | 0.253 | _cons | 9.377 *** | 11.834 *** | 8.818 *** |

| (150.888) | (7.369) | (158.831) | (401.749) | (485.577) | (0.408) | (151.552) | (34.208) | (42.569) | |||

| mediating effect | −0.143 | mediating effect | 0.069 | mediating effect | −0.077 | ||||||

| mediating effect/total effect | 0.313 | mediating effect /total effect | 3.307 | mediating effect /total effect | 0.120 | ||||||

| Variables | Unofficial | Real Estate Policies | Fiscal Policies | Monetary Policies |

|---|---|---|---|---|

| 2.924 *** | 0.401 *** | −1.743 *** | 1.013 *** | |

| (−112.119) | (−8.931) | (−92.131) | −105.512 | |

| −0.002 | −0.023 *** | −0.001 | −0.001 | |

| (−1.490) | (−7.258) | (−0.238) | (−1.542) | |

| Land policies | Healthcare policies | Household registration policies | Education policies | |

| −3.173 *** | −3.174 *** | −2.025 *** | −1.875 *** | |

| (−480.968) | (−41.028) | (−21.034) | (−73.245) | |

| −0.002 (−1.272) | −11.719 (−0.895) | −0.016 * (−1.842) | 0.001 −0.208 |

| Variables | Unofficial | Real Estate Policies | Fiscal Policies | Monetary Policies |

|---|---|---|---|---|

| 2.817 *** | 0.342 | −1.749 *** | 1.281 *** | |

| 3.366 | (0.857) | (−3.132) | (158.657) | |

| 0.041 * | 0.081 *** | −0.094 *** | 0.028 ** | |

| (1.851) | (5.937) | (−8.259) | (2.389) | |

| Land policies | Healthcare policies | Household registration policies | Education policies | |

| −2.388 *** | −1.379 | 0.992 *** | −2.059 *** | |

| (−38.533) | (−1.263) | (4.787) | (−17.666) | |

| −0.184 *** (−10.490) | −0.228 *** (−969.363) | 0.081 * (1.673) | −0.066 *** (−3.114) |

| Variables | Financial Policies | Variables | Real Estate Policies | Variables | Residential Living Policies | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |||

| Dependent variable | Real estate price | Interest rate | Real estate price | Dependent variable | Real estate price | Real estate construction | Real estate price | Dependent variable | Real estate price | Real estate sales | Real estate price |

| Financial policies | 0.072 (0.842) | −1.243 (−1.278) | 0.048 (0.556) | Real estate policies | 0.023 (1.136) | 0.470 ** (2.651) | 0.045 ** (2.338) | Residential living policies | −0.301 *** (−3.385) | 0.576 (0.588) | −0.300 *** (−3.334) |

| Interest rate | −0.020 | Real estate | −0.049 *** | Real estate sales | −0.001 | ||||||

| (−1.602) | construction | (−3.337) | (−0.074) | ||||||||

| N | 52 | 52 | 52 | N | 52 | 52 | 52 | N | 52 | 52 | 52 |

| _cons | 8.680 *** | 4.541 *** | 8.770 *** | _Cons | 8.725 *** | 11.142 *** | 9.266 *** | _cons | 8.987 *** | 9.764 *** | 8.996 *** |

| (134.019) | (6.197) | (103.413) | (665.178) | (95.797) | (57.029) | (119.228) | (11.727) | (61.012) | |||

| mediating effect | 0.025 | mediating effect | −0.023 | mediating effect | −0.001 | ||||||

| mediating effect/total effect | 0.345 | mediating effect /total effect | −1.001 | mediating effect /total effect | 0.002 | ||||||

| Variables | Financial Policies | Variables | Real Estate Policies | Variables | Residential Living Policies | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |||

| Dependent variable | Real estate price | Interest rate | Real estate price | Dependent variable | Real estate price | Real estate construction | Real estate price | Dependent variable | Real estate price | Real estate sales | Real estate price |

| Financial policies | −0.086 (−1.231) | 0.151 (0.661) | −0.065 (−1.030) | Real estate policies | 0.058 ** (2.102) | 0.330 (1.352) | 0.055 * (1.943) | Residential living policies | −0.193 *** (−2.855) | −1.050 (−1.667) | −0.186 ** (−2.643) |

| Interest rate | −0.137 *** | Real estate | 0.009 | Real estate sales | 0.007 | ||||||

| (−3.407) | construction | (0.535) | (0.454) | ||||||||

| N | 49 | 49 | 49 | N | 49 | 49 | 49 | N | 49 | 49 | 49 |

| _cons | 9.115 *** | 2.449 *** | 9.450 *** | _Cons | 9.046 *** | 11.261 *** | 8.947 *** | _cons | 9.193 *** | 11.684 *** | 9.109 *** |

| (217.875) | (17.834) | (89.731) | (577.080) | (80.469) | (48.081) | (199.458) | (27.263) | (47.789) | |||

| mediating effect | −0.02 | mediating effect | 0.003 | mediating effect | −0.007 | ||||||

| mediating effect/total effect | 0.240 | mediating effect /total effect | 0.051 | mediating effect /total effect | 0.038 | ||||||

| Variables | Unofficial | Real Estate Policies | Fiscal Policies | Monetary Policies |

|---|---|---|---|---|

| −1.105 ** | −0.640 | −0.675 | −0.125 | |

| (−2.554) | (−1.089) | (−1.377) | (−0.410) | |

| 0.888 *** | 0.924 *** | 0.773 *** | 0.929 *** | |

| (4.207) | (4.196) | (3.720) | (6.383) | |

| Land policies | Healthcare policies | Household registration policies | Education policies | |

| −0.251 | −0.411 | −0.324 | −1.238 *** | |

| (−1.018) | (−1.249) | (−0.666) | (−3.014) | |

| 0.824 (0.652) | 0.912 *** (4.661) | 0.796 *** (8.368) | 0.764 *** (4.235) |

| Variables | Financial Policies | Variables | Real Estate Policies | Variables | Residential Living Policies | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |||

| Dependent variable | Residential real estate price | Interest rate | Residential real estate price | Dependent variable | Residential real estate price | Real estate construction | Residential real estate price | Dependent variable | Residential real estate price | Real estate sales | Residential real estate price |

| Financial policies | −0.536 *** (−5.102) | 1.221 *** (2.636) | −0.360 *** (−4.269) | Real estate policies | 0.032 (0.760) | 0.411 *** (2.832) | 0.034 (0.780) | Residential living policies | −0.757 *** (−8.000) | −1.562 *** (−3.299) | −0.666 *** (−6.948) |

| Interest rate | −0.144 *** | Real estate | −0.006 | Real estate sales | 0.059 *** | ||||||

| (−8.145) | construction | (−0.192) | (3.032) | ||||||||

| N | 101 | 101 | 101 | N | 101 | 101 | 101 | N | 101 | 101 | 101 |

| _cons | 9.209 *** | 2.287 *** | 9.538 *** | _Cons | 8.843 *** | 11.198 *** | 8.906 *** | _cons | 9.424 *** | 11.785 *** | 8.734 *** |

| (128.275) | (7.222) | (138.539) | (339.480) | (125.161) | (26.962) | (129.066) | (32.253) | (36.693) | |||

| mediating effect | −0.175 | mediating effect | −0.002 | mediating effect | −0.092 | ||||||

| mediating effect/total effect | 0.328 | mediating effect /total effect | 0.077 | mediating effect /total effect | 0.122 | ||||||

| Variables | Financial Policies | Variables | Real Estate Policies | Variables | Residential Living Policies | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |||

| Dependent variable | Real estate price | Interest rate | Real estate price | Dependent variable | Real estate price | Real estate construction | Real estate price | Dependent variable | Real estate price | Real estate sales | Real estate price |

| Financial policies-1 | −0.467 *** (−5.256) | 1.670 *** (−5.256) | −0.273 *** (−3.490) | Real estate policies-1 | 0.014 (0.381) | 0.271 * (1.901) | 0.016 (0.439) | Residential living policies-1 | −0.631 *** (−7.713) | −1.356 *** (−3.024) | −0.558 *** (−6.817) |

| Interest rate | −0.116 *** | Real estate | −0.009 | Real estate sales | 0.054 *** | ||||||

| (−7.150) | construction | (−0.362) | (3.169) | ||||||||

| N | 108 | 108 | 108 | N | 108 | 108 | 108 | N | 108 | 108 | 108 |

| _cons | 9.205 *** | 1.939 *** | 9.431 *** | _Cons | 8.892 *** | 11.241 *** | 8.992 *** | _cons | 9.372 *** | 11.647 *** | 8.744 *** |

| (151.559) | (6.499) | (159.355) | (400.269) | (127.575) | (32.427) | (148.461) | (33.658) | (42.211) | |||

| mediating effect | −0.194 | mediating effect | −0.002 | mediating effect | −0.073 | ||||||

| mediating effect/total effect | 0.415 | mediating effect /total effect | −0.174 | mediating effect /total effect | 0.116 | ||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, D.; Lv, B.; Li, X.; Li, X.; Liu, S. Heterogeneous Impacts of Policy Sentiment with Different Themes on Real Estate Market: Evidence from China. Sustainability 2023, 15, 1690. https://doi.org/10.3390/su15021690

Ma D, Lv B, Li X, Li X, Liu S. Heterogeneous Impacts of Policy Sentiment with Different Themes on Real Estate Market: Evidence from China. Sustainability. 2023; 15(2):1690. https://doi.org/10.3390/su15021690

Chicago/Turabian StyleMa, Diandian, Benfu Lv, Xuerong Li, Xiuting Li, and Shuqin Liu. 2023. "Heterogeneous Impacts of Policy Sentiment with Different Themes on Real Estate Market: Evidence from China" Sustainability 15, no. 2: 1690. https://doi.org/10.3390/su15021690