1. Introduction

An asset is considered to be information-sensitive if the benefits of producing private information about the asset’s payoff outweigh the costs; otherwise, the asset is information-insensitive. Money-like assets such as money market funds (MMFs) are designed to be information-insensitive. This is because information-insensitive assets can protect uninformed investors from adverse selection problems and hence have greater liquidity [

1,

2]. However, these assets may become information-sensitive when investors are increasingly suspicious of debt defaults [

3] and have greater incentives to learn the value of those assets [

2,

4]. As a result, safety-seeking investors may be reluctant to trade, leading to a market freeze. Recent theoretical and empirical studies have demonstrated that the failure of financial institutions to maintain the information insensitivity of their assets leads to greater risks themselves, which can spill over to other institutions and even trigger financial crises [

4,

5,

6,

7]. Therefore, it is important to understand how financial institutions manage the information sensitivity of money-like assets that they have issued.

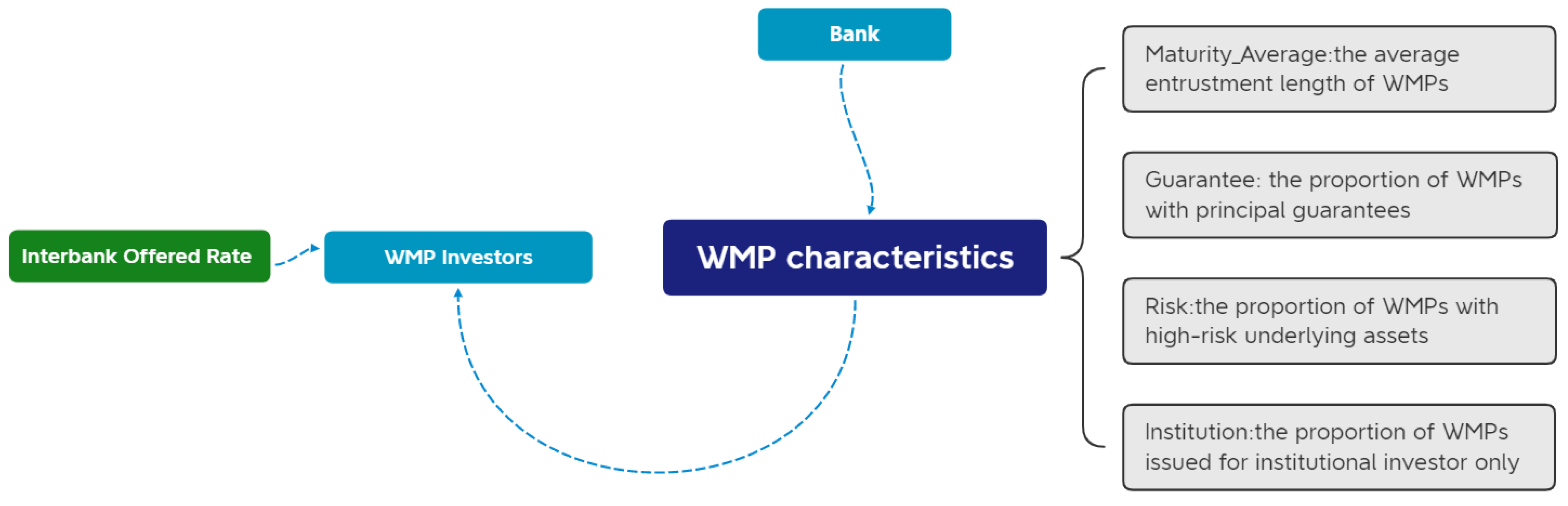

In this paper, we examine how banks in China manage the information sensitivity of their money-like assets, i.e., wealth management products (WMPs). As the most important shadow banking asset for the Chinese banking industry, WMPs gain their money-like attributes through two main channels. First, WMPs have a very short maturity. Most WMPs have a maturity within 3 months and offer investors an early exit option. Second, WMPs are perceived to be implicitly guaranteed by banks. Investors believe that banks will bear the loss of WMPs in the case of default. While these two factors may enable WMPs to be information-insensitive, they may also pose potential risks to WMPs. Regarding the maturity, the mismatch between the shorter maturity of WMPs and the longer term of their underlying investment assets can lead to rollover risks (according to the “Report on the Development of Wealth Management Business in the Chinese Banking Industry” (2018), jointly released by the China Banking Association and the Banking Wealth Management Registration and Custody Center, more than 80% of the funds raised by WMPs are invested in long-term assets). The so-called implicit guarantee is actually built on a misperception between investors and banks about the risks of WMPs (since most WMPs are not reflected on banks’ balance sheets, banks are not legally obligated to guarantee their WMPs against losses). Therefore, there is still an incentive for WMP investors to produce private information when their suspicions about the risk of WMPs increase.

Our study begins with an analysis of situations in which investors are motivated to engage in private information production. We then examine how banks manage the WMPs’ information sensitivity by adjusting the characteristics of their WMPs in these situations. WMP investors are concerned about their principals and returns. Therefore, when investors have greater suspicions about the safety and riskiness of their WMPs, their incentives to engage in private information production increase. Two situations may affect whether a WMP can be redeemed as promised. One is whether the value of the underlying asset is sufficiently high when it eventually matures. The other is whether a bank has sufficient liquidity to meet the repayment when the underlying asset has not yet matured. In this paper, we use the interbank offered rate to measure both of these scenarios. There are two reasons why interbank market rates are a good measure of this metric. First, as an efficient market interest rate in China, the interbank offered rate has a great impact on the value of WMPs’ underlying assets. An elevated interbank offered rate implies a decline in the present value of underlying assets, increasing the incentive for investors to engage in private information production [

4,

8]. Second, the interbank lending market serves an important role in short-term funding for banks. Previous studies have found that banks’ liquidity status, such as loan-to-deposit ratios, affects their probability of entering the interbank market [

9]. Moreover, interbank business is associated with increased risks for banks, such as mismatch between assets and liabilities, and the risks can be transmitted through interbank business [

10]. Previous literature has argued that the interbank offered rates reflect banks’ credit risk and liquidity risk [

11,

12,

13,

14] and banks seeking funds through the interbank market for the redemption of maturing WMPs [

15,

16,

17]. Thus, higher interbank offered rates imply greater liquidity difficulties for banks, increasing the incentives for investors to engage in private information production.

We then focus on how banks adjust the characteristics of WMPs that reduce investors’ incentives for private information production (i.e., that maintain the information insensitivity of WMPs) when the interbank offered rates increase. Four characteristics of WMPs are taken into account, namely, maturity, guarantee for the principal, underlying asset risk, and investor types. First, previous studies find that debts with a short commitment period are less prone to adverse selection problems and, hence, are less information-sensitive [

1,

4,

18,

19]. Therefore, reducing the maturity of WMPs can help reduce investors’ incentives to engage in private information production. Second, some scholars find that guarantees against future losses can reduce the need for investors to produce private information [

19,

20]. For WMPs investors, the principal guarantee provided by banks is essentially a guarantee against future losses and, therefore, reduces their incentives to perform private information production. Third, previous research finds that money-like assets such as MMFs with riskier underlying assets are more information-sensitive [

6,

21]. Thus, reducing the risk of the underlying assets helps reduce WMPs investors’ concerns about future losses and, thus, reduces their incentives to engage in private information production. Lastly, the possibility of engaging in private information production varies between different types of investors. Previous studies have found that institutional investors are more motivated to produce private information [

3,

6,

21]. Therefore, banks can reduce the incentive for investors to engage in private information production by reducing the issuance of WMPs to institutional investors. We do not include the yield of WMP because previous literature shows that price adjustment is not an effective means of maintaining assets’ information insensitivity [

4,

18]. In summary, banks can manage WMPs’ information sensitivity by adjusting the above four characteristics when investors’ incentives to engage in private information production increase.

Our empirical results show that when the interbank offered rate rises, for the newly issued WMPs, banks are more likely to shorten product maturity, provide them with more guarantees, and reduce the risk of the underlying assets. We also investigate the effects of heterogeneity on banks of different sizes. Previous literature argues that investors perceive implicit guarantees by large state-owned banks to be more credible compared to those of small and medium-sized banks (SMBs) [

22,

23]. This implies that investors perceive WMPs issued by large state-owned banks as safer and, therefore, have less incentive to produce private information about them. Accordingly, large state-owned banks have less need to adjust the characteristics of WMPs to maintain WMPs’ information insensitivity when interbank interest rate rises. We do find that the effects of the interbank offered rate on the WMPs characteristics are more pronounced in the SMBs sample relative to the largest five state-owned banks (Big5) sample (the Big5 banks in China are the Bank of China, the Industrial and Commercial Bank of China, the Agricultural Bank of China, the China Construction Bank, and the Bank of Communications). Furthermore, we also find that banks reduced the number of WMPs issued to institutional investors when the interbank offered rate rises. This effect exists in both Big5 banks and SMBs. This result is also consistent with previous literature findings that skeptical institutional investors are more motivated to produce private information [

3,

6], and institutional investors are more sensitive to information production [

22].

This paper contributes to the existing research in the following ways. First, since most studies on information sensitivity have mainly focused on the measurements and the variations in securities’ information sensitivity [

2,

5,

6,

24], this paper contributes to the existing literature by first empirically examining how issuers manage the information sensitivity of their debts when investors are incentivized to engage in private information production. Second, the use of short-term debts to support long-term assets exposes banks to liquidity risk [

25]. Previous studies demonstrate that shadow banking activities expose banks to greater liquidity risk due to the serious maturity mismatch problem [

26] and the lack of deposit insurance and capital protection [

27]. This paper sheds lights on the measures banks can take to manage liquidity risk in their shadow banking activities based on the information sensitivity theory. Third, given that previous studies have linked the variations in information sensitivity to financial crises [

4,

5], the results of this paper have rich theoretical and practical implications for helping issuers understand and maintain financial stability. This is not just applicable to the Chinese bank WMP markets, but also has profound implications for managers of such quasi-safe assets around the world. Fourth, unlike previous literature that focuses on the pricing of WMPs [

15,

23,

28], to the best of our knowledge, this paper is the first to reveal how banks can adjust other characteristics of the WMPs to help their issuance. Our findings can provide important insights for issuers, investors, and regulators of shadow banking products in China.

The remainder of this paper is organized as follows.

Section 2 presents the background and hypotheses developments.

Section 3 describes the data and methodology.

Section 4 provides empirical results.

Section 5 concludes.

4. Empirical Results

4.1. Descriptive Statistics

Table 1 presents the summary statistics. For the four types of WMP characteristics, the average value of

Maturity_Average is 129.373 days; the average value of

Guarantee is 44%; the average value of

Risk is 8.1%; and the average value of

Institution is 7%. Regarding the explanatory variable, the mean value of

SHIBOR is 2.464%.

Table 2 gives the Pearson correlation results. The results show that there is no serious linear correlation between the variables in the regression model.

4.2. Interbank Offered Rate and the Maturity of WMPs Newly Issued by Banks

We first focus on changes in the maturity of WMPs newly issued by banks when the interbank offered rate rises. The results are reported in

Table 3. The first two columns show the regression results for the overall sample, where no fixed effects are controlled in column (1) and bank and time fixed effects are added in column (2). The results of these two columns maintain good consistency. We find that the regression coefficient of

SHIBOR in column 2 is negative (−2.8180) and significant at the 1% level. This result supports our hypothesis H1 that banks have shortened the maturity of the newly issued WMPs when the interbank offered rate rises. This finding implies that since shorter maturities guarantee the possibility of a future early exit for investors, thus reducing their incentive to engage in private information production, banks manage WMP’s information sensitivity by shortening the maturity of newly issued WMPs. This result is also economically significant. For each standard deviation increase in

SHIBOR, the average maturity of newly issued WMPs decreases by 1.78 (0.63 × 2.8180) days or 1.4% of the average maturity of WMPs (1.78 ÷ 129.379).

The findings regarding the control variables in column (2) are also intuitive. The more competitive the market is (the smaller the HHI), the shorter the average maturity of newly issued WMPs. The positive coefficient of Maturity_Existing indicates that the maturity structure of newly issued WMPs is consistent with the maturity structure of existing WMPs. WMPs issued by large banks have longer maturities since large banks are typically perceived as safer institutions. The greater the refinancing pressure on banks (the larger the WMPdue), the shorter the average maturity of newly issued WMPs.

We then divided the sample into two groups, the largest five state-owned banks (Big5) and the small and medium-sized banks (SMBs). Columns 3 and 4 of

Table 3 report the regression results. As can be seen, the significant effect of

SHIBOR on

Maturity_Average only existed in the sample of SMBs. This result supports hypothesis H5 that large state-owned banks have less need to maintain the information insensitivity of their WMPs by adjusting the WMPs’ characteristics than the small and medium-sized banks. This is because investors perceive that WMPs issued by large state-owned banks are safer and have no incentive to engage in private information production.

We also introduced another variable,

Maturity_Percenti,t, to measure WMPs’ maturity, which represents the proportion of WMPs with maturities over 90 days (the median value of the WMPs’ maturity in our sample is close to 90 days) issued by bank

i in month

t. We rerun the regression and find a quite similar result in column 2 of

Table 4: the regression coefficient of

SHIBOR is negative (−0.0205) and significant at the 1% level, which supports hypothesis H1 that banks issue more WMPs with short maturities to reduce investors’ incentives to engage in private information production and, thus, maintain the information insensitivity of their WMPs when interbank interest rates increase. Correspondingly, the results of the heterogeneity analysis are similar: the significant effect of

SHIBOR on

Maturity_Percent is more pronounced in the sample of SMBs. This result also supports hypothesis H5 that there is less need for large state-owned banks to adjust WMPs’ characteristics since investors perceive that the WMPs issued by them are safer compared to the small and medium-sized banks.

4.3. Interbank Offered Rate and the Proportion of WMPs with Principal Guarantee Newly Issued by Banks

We then investigated the changes in the proportion of WMPs with principal guarantees newly issued by banks when the interbank offered rate rises. The results are shown in

Table 5. The first two columns show the regression results for the overall sample, where no fixed effects are controlled in column (1) and bank and time fixed effects are added in column (2). The results of these two columns maintain good consistency. We can find that the regression coefficient of

SHIBOR in column 2 of

Table 5 is positive (0.0076) and significant at the 1% level. This result supports our hypothesis, H2, that banks provided more guarantees for the newly issued WMPs when the interbank offered rate rose. This result is consistent with the idea that banks maintain the information insensitivity of their WMPs by providing explicit guarantees for WMP, which can reduce the need for investors to engage in private information production. This result is also economically significant. For each standard deviation increase in

SHIBOR, the proportion of WMPs with principal guarantee increases by 0.48% (0.63 × 0.00763), or 1.09%(0.48% ÷ 44%) of the mean value.

As for the control variables in column (2), the coefficient of HHI is not significant. A negative coefficient on LnAssets indicates that large banks are issuing more WMPs without principal guarantees. A positive coefficient on WMPdue indicates that banks that are under greater refinancing pressure have provided more guarantees for newly issued WMPs.

The heterogeneity analysis results in column 3 and 4 of

Table 5 also indicate that the significant effect of

SHIBOR on

Guarantee only existed in the sample of SMBs. This result is consistent with the fact that large state-owned banks have less need to manage their information sensitivity by adjusting their WMPs’ characteristics (providing more principal guarantees) since investors perceive WMPs issued by large state-owned banks to be safer, thus supporting hypothesis H5.

4.4. Interbank Offered Rate and the Proportion of WMPs with High-Risk Underlying Assets Newly Issued by Banks

In this section, we examine the changes in the proportion of WMPs with high-risk underlying assets newly issued by banks when the interbank offered rate rises. In this paper, we define WMPs that invest in stocks, commodities, or currencies as having higher risks.

Table 6 presents the results. The first two columns show the regression results for the overall sample, where no fixed effects are controlled in column (1) and bank and time fixed effects are added in column (2). The results of these two columns maintain good consistency. We can find that the regression coefficient of

SHIBOR in column 2 is negative (−0.0057) and significant at the 5% level. This result supports our hypothesis H3 that banks reduced the risk of the underlying assets for the newly issued WMPs when the interbank offered rate rises. This is because the riskiness of the underlying assets determines the size of the incentive for investors in WMPs to engage in private information production. The less risky the underlying assets, the less incentive for investors to engage in private information production. This result is also economically significant. For each standard deviation increase in

SHIBOR, the proportion of WMPs with high-risk underlying assets decreases by 0.36% (0.63 × 0.00571), or 4.04%(0.36% ÷ 8.9%) of the mean value.

As for the control variables in column 2, the coefficient of HHI is not significant. A positive coefficient on LnAssets indicates that large banks are issuing more WMPs that invest in the underlying assets with high risk. A negative coefficient on WMPdue indicates that banks that are under greater refinancing pressure have reduced the risk of the underlying assets for the newly issued WMP.

The heterogeneity analysis results in columns 3 and 4 of

Table 6 also indicate that the significant effect of

SHIBOR on

Risk only existed in the sample of SMBs. This result supports hypothesis H5 that as investors perceive WMPs issued by Big5 banks as safer, there is less need for Big5 banks to adjust the characteristics of WMPs (reduce the risk of the underlying assets) for maintaining the WMP’s information insensitivity.

4.5. Interbank Offered Rate and the Proportion of WMPs Only Issued to Institutional Investors Newly Issued by Banks

Considering that the previous literature found that institutional investors are more likely to engage in private information production compared to individual investors, we focus on the changes in the proportion of WMPs newly issued by banks to institutional investors when the interbank offered rate rises. As we can see from

Table 7, the first two columns show the regression results for the overall sample, where no fixed effects are controlled in column (1) and the bank and time fixed effects are added in column (2). The results of these two columns maintain good consistency. The regression coefficient of

SHIBOR in column 2 is negative (−0.0069) and significant at the 1% level. This result supports our hypothesis H4 that banks reduced the number of WMPs issued only to institutional investors when the interbank offered rate rises. This finding implies that since institutional investors are more aware of the risks of WMPs and thus have greater incentives to engage in private information production relative to individual investors, banks reduce the number of WMPs issued to institutional investors to maintain the information the insensitivity of WMPs. This result is also economically significant. For each standard deviation increase in SHIBOR, the proportion of WMPs issued for institutional investors only decreases by 0.43% (0.63 × 0.00685), or 6.14% (0.43% ÷ 7%) of the mean value.

As for the control variables in column (2), the coefficient of LnAssets is no longer significant. This result is also intuitive because institutional investors are more aware than individual investors that the WMPs offered by both large and small banks are indeed risky. The more competitive the market (the smaller the HHI) is, the fewer WMPs are issued to institutional investors. A negative coefficient on WMPdue indicates that banks that are under greater refinancing pressure have reduced the number of WMPs issued only to institutional investors.

The results of the heterogeneity analysis are presented in columns 3 and 4. We can see that the coefficient of SHIBOR is significant in both SMB samples and Big5 samples. This result supports our hypothesis, H6, that, unlike individual investors, who perceive WMPs issued by large state-owned banks to be safer relative to those issued by small and medium-sized banks, institutional investors are more aware of the risks of WMPs. Hence, both Big5 banks and SMBs need to adjust the proportion of WMPs only issued to institutional investors newly issued by banks when the interbank offered rate rises.

4.6. Event Study

In this section, we try to figure out how banks adjust the characteristics of their WMPs when the interbank offered rate suddenly rises. We use the money shortage in China’s interbank market in 2013 as an exogenous shock for the event study. Starting on June 6, 2013, the overnight SHIBOR rate soared 495.8 basis points in three days due to rumors that a commercial bank was about to default on its interbank lending. As of June 20, the SHIBOR overnight rate surged 578.4 basis points to 13.44%. There is no evidence that changes in the WMP markets have led to a spike in the overnight SHIBOR rate. We introduce a dummy variable Shock, which equals one for the WMPs that are issued in June 2013 and zero otherwise. We add an interaction term between Shock and SHIBOR to the model.

Table 8 shows the regression results. We find that the coefficients of the interaction term are significant in only two characteristics, i.e., maturity and investor type. These results imply that banks rely more on adjusting maturity and investor type to manage the information sensitivity of WMP when interbank offered rates suddenly increase. These results are consistent with the findings in the previous research that the maturity of financial instruments underwent a significant reduction in the financial crisis [

32,

34,

35] and changes in the information sensitivity of short-term debt are more concentrated in money market funds issued to institutional investors [

3].

4.7. Robustness Check

We still need to consider the possibility that our results can be biased due to endogeneity concerns such as reverse causality, omitted variables, and measurement errors. First, the reverse causality problem is less likely to occur in this paper. This is because the characteristics of WMPs from a single bank are unlikely to affect the overall market rate (

SHIBOR). Nevertheless, we use the lagged term of

SHIBOR. Second, out of concern for omitted variables, we control for the bank and time fixed effects in the paper. Finally, we replace the SHIBOR (Overnight) with SHIBOR (1-week) and re-run the main regressions. The results, shown in

Table 9, remain unchanged.

Furthermore, since the adjustment is unlikely to be instantaneous, we also use the dynamic panel data model by including the lagged dependent variable as the control variable and re-run the regressions. The results shown in

Table 10 remain robust.

Last, considering that the null hypotheses are more likely to be rejected as the sample size increases [

38], we re-examine the difference in the effect of SHIBOR on the characteristics of WMPs by using a dummy variable approach. We can see that the heterogeneity analysis results remain stable in

Table 11.

5. Conclusions

Blocking private information production by issuing information-insensitive assets has been a common practice in money markets. However, changes in the information sensitivity of these assets, such as turning from information-insensitive to information-sensitive, will bring risks to financial institutions and even trigger financial crises. In this paper, we examined how banks manage the information sensitivity of their WMPs by using the WMP data in China. We found that banks manage their WMPs’ information sensitivity by adjusting the structure of four WMP characteristics—maturity, guarantee of the principal, underlying asset risk, and investor types—when investors are motivated to produce private information. By using the interbank offered rate to indicate investors’ incentives for private information production, we found that when the interbank offered rate rises, for the newly issued WMPs, banks have shortened their maturity, provided them with more guarantees, and reduced the risk of the underlying assets they invest in. Moreover, these effects are more pronounced in small and medium-sized banks (SMBs) relative to the five largest state-owned (Big5) banks. Furthermore, we also found that banks reduced the number of WMPs issued to institutional investors when the interbank offered rate rose and this effect existed in both Big5 banks and SMBs.

The findings in this paper imply that banks reduced investors’ incentives to engage in private information production by adjusting the characteristics of newly issued WMPs. Specifically, shorter maturities ensure that investors withdraw in time in case of losses in the future, and providing principal guarantees and reducing the risk of the underlying assets reduces investors’ concerns about future losses. Moreover, as institutional investors are more motivated and capable to engage in private information production, banks reduce the number of WMPs issued to them. In addition, the results of the heterogeneity analysis indicate that since institutional investors are more aware of the WMPs’ risks, all banks have reduced the number of WMPs issued to them.

The findings also provide informative implications for regulators, banks, and WMP investors. First, banks maintain the information insensitivity of WMPs by reducing the maturity of new issues, which will in turn further exacerbate the maturity mismatch problem of WMPs and may increase banks’ liquidity risk [

25,

26]. Second, by providing a principal guarantee for WMPs, banks bear the losses in the event of default of WMPs, thus increasing the risk of the bank itself. In addition, the creditworthiness of small and medium-sized banks is low compared to large banks [

15,

22,

23]. Therefore, providing guarantees may not be a viable option for small and medium-sized banks. Third, banks can reduce the underlying asset risk by investing in safer assets, which will also lead to lower returns. However, lower returns offered by newly issued WMPs are not competitive with other investment opportunities [

22]. Therefore, investors may choose securities other than WMPs, leading to difficulties for banks to refinance. Fourth, the result also indicates that institutional investors are more sophisticated and better understand the effect of the interbank offered rate change on the WMP markets.

Moreover, the results of this paper have profound implications for managers of quasi-safe assets around the world. Since previous studies suggest that financial crises are closely related to variations in the information sensitivity of such quasi-safe financial assets, it is helpful to understand how to manage the information sensitivity of these assets.

Finally, future research may focus on the impact of regulatory policy or public events on the WMP’s information sensitivity and figure out how banks will respond to these shocks. Such as the implementation of new regulations on asset management in China or the COVID-19 shock.

{kind=link}