Do ESG Ratings of Chinese Firms Converge or Diverge? A Comparative Analysis Based on Multiple Domestic and International Ratings

Abstract

:1. Introduction

2. Background and Comparison of ESG Ratings in China

2.1. Background of ESG Ratings in China

2.1.1. Advent and Development of ESG Ratings in China

2.1.2. Application of ESG Ratings in China

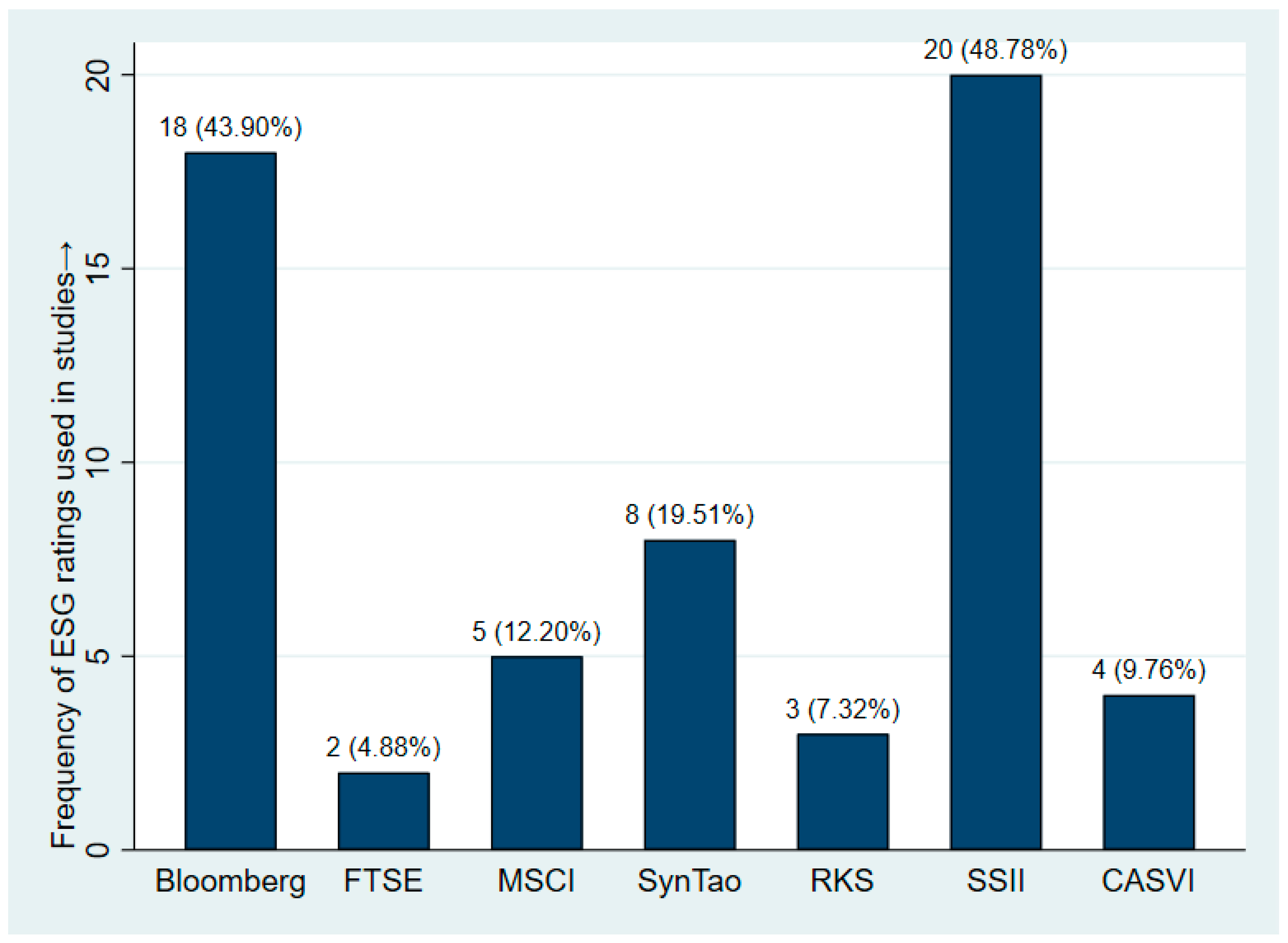

2.2. Comparison of Various ESG Ratings

3. Analysis for the Convergence/Divergence of Chinese ESG Ratings

3.1. Analysis Design

3.2. Sampling Process

3.3. Descriptive Statistics

3.4. Ranking Overlap Analysis

3.5. Correlation Analysis

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Study | Independent Variable | Dependent Variable | ESG Measure | Sampling Period | Obs |

|---|---|---|---|---|---|

| Chang, Cheng, Wang, Liu, and Hu (2023) [23] | ESG performance (+) | Corporate financing efficiency | SSII | 2013–2019 | 2100 |

| Li et al. (2023) [24] | ESG performance (+) | Corporate innovation | SSII (main test), Hexun and Bloomberg (robustness test) | 2009–2020 | 28,636 |

| Feng, Goodell, and Shen (2022) [25] | ESG ratings (-) | Stock price crash risk | SSII | 2009–2020 | 24,193 |

| Li, Zhang, and Zhao (2022) [26] | ESG performance (-) | Firms’ default risk | SSII | 2015–2020 | 185,125 |

| Deng, Li, and Ren (2023) [27] | ESG performance (+) | Total factor productivity (TFP) | SSII (main test) and Bloomberg (robustness test) | 2016–2020 | 11,544 |

| Hu, Zou, and Yin (2023) [28] | ESG performance (+) | Stock price synchronicity | SSII | 2010–2021 | 24,544 |

| Kong (2023) [29] | ESG performance (-) | The cost of debt financing | SSII | 2009–2021 | 16,833 |

| Luo, Wei, and He (2023) [30] | ESG performance (+) | The access to trade credit | SSII (main test) and Hexun (robustness test) | 2011–2019 | 14,201 |

| Lian, Ye, Zhang, and Zhang (2023) [31] | ESG performance (-) | Bond credit spreads | SSII | 2009–2020 | 12,153 |

| Chen, Li, Zeng, and Zhu (2023) [32] | ESG performance (+) | The cost of equity capital | SSII (main test) and Bloomberg (robustness test) | 2010–2020 | 15,633 (main test) 7585 (robustness test) |

| Li, Lian, and Xu (2023) [33] | ESG performance (+) | Peer firms’ green innovation | SSII (main test) Bloomberg (robustness test) | 2012–2020 | 11,259 (main test) 5964 (robustness test) |

| Zeng and Jiang (2023) [34] | ESG performance (+) | Corporate performances | SSII | 2009–2021 | 1247 |

| Tian and Tian (2022) [15] | ESG performance (+) | Corporate trade credit financing | SSII (main test) and Bloomberg (robustness test) | 2009–2020 | 32,534 (main test) 10,188 (robustness test) |

| Zhou, Liu and Luo (2022) [35] | ESG performance (+) | Market value of the firm | SynTao | 2014–2019 | 1002 |

| Broadstock, Chan, Cheng, and Wang (2021) [36] | ESG performance (+) | Financial risk during financial crisis | SynTao | 2015–2020 | 300 |

| Wang, Ma, Dong, and Zhang (2023) [37] | ESG rating (+) | Corporate green innovation | SynTao (main test) and CASVI (robustness test) | 2013–2019 | 18,790 |

| Deng and Cheng (2019) [38] | ESG indices (+) | Stock market performance | SynTao (main test) and CASVI (robustness test) | 2013–2019 | 5864 (main test) 3763 (robustness test) |

| Yang, Du, Zhang, Tong, and Zhou (2021) [39] | ESG disclosure (+) | Corporate bond credit spreads | SynTao | 2015–2020 | 2103 |

| Xu, Liu and Shang (2020) [40] | ESG performance (+) | Green invention | SynTao | 2015–2018 | 739 |

| He, Du, and Yu (2022) [41] | ESG performance (-) | Manager misconduct | Hexun (main test) and RKS (robustness test) | 2010–2020 | 23,741 (main test) 6030 (robustness test) |

| Yu, Liu, Cheng, and Lee (2022) [42] | ESG scores (no link) | Stock returns | RKS | 2020–2021 | 300 |

| Jun, Shiyong, and Yi (2022) [43] | ESG disclosure (non-linear) | Intangible capital | WIND and FTSE | 2017–2020 | 4593 |

| Li, Yin, and Liu (2022) [5] | ESG rating (-) | Stock price crash risk | Bloomberg, FTSE, MSCI, SSII, STGE, and CASVI | 2016–2020 | 13,919 (Only the CASVI sample is 11,765) |

| Zhang, Zhao, and He (2022) [44] | ESG performance (non-linear) | Portfolio excess returns | Bloomberg | 2005–2018 | 10,808 |

| Chen and Xie (2022) [45] | ESG disclosure (+) | Corporate financial performance | Bloomberg | 2011–2020 | 11,382 |

| Yuan, Li, Xu, and Shang (2022) [46] | ESG disclosure (-) | Corporate financial irregularity risks | Bloomberg (main test) and RKS (robustness test) | 2010–2020 | 7123 (main test) 4490 (robustness test) |

| Chen, Khurram, Gao, Abedin, and Lucey (2023) [47] | ESG disclosure (+) | Technological innovation capability | Bloomberg | 2011–2019 | 7146 |

| Ge, Xiao, Li, and Dai (2022) [48] | ESG performance (+) | High-quality development of firms | Bloomberg | 2011–2019 | 4985 |

| Liu, Zhu, Yang, and Chu (2022) [49] | ESG configuration | Corporate financial performance | Bloomberg | 2016–2020 | 210 |

| Zhou and Zhou (2022) [50] | ESG performance (-) | The stock price volatility of firms | MSCI | 2019–2020 | 1021 |

| Cheng, Lee, Li, and Tsang (2023) [51] | ESG proportion (+) and pillar mix efficiency heterogeneity (non-linear) | Financial performance | MSCI | 2015–2019 | 1108 |

| Baker, Boulton, Braga-Alves, and Morey (2021) [52] | ESG government ratings (-) | Firm-level IPO underpricing | MSCI | 2008–2018 | 7446 |

| Mu, Liu, Tao, and Ye (2023) [53] | Digital finance (+) | ESG performance | SSII | 2011–2020 | 26,294 |

| Wang, Lin, Fu, and Chen (2023) [54] | Institutional ownership heterogeneity (+) | ESG performance | SSII (main test) and Refinitiv (robustness test) | 2012–2021 | 23,607 (main test) 1124 (robustness test) |

| Wang, Peng, Tang, and Wu (2022) [55] | The development of fintech (+) | ESG performance | SSII (main test) and CASVI (robustness test) | 2010–2020 | 10,241 |

| Liu, Xiong, Gao, and Zhang (2022) [56] | Institutional shareholdings Heterogeneity (+) | ESG performance | Bloomberg (main test) and MSCI (robustness test) | 2010–2020 | 8421 |

| Meng and Zhu (2023) [57] | Female executives (+) | ESG performance | Bloomberg | 2011–2020 | 10,123 |

| Fang, Nie, and Shen (2023) [58] | Enterprise digitization (+) | ESG performance | Bloomberg (main test), SSII and Hexun (robustness test) | 2012–2020 | 2276 (main test) 2753 and 2036 (robustness test) |

| Yang, Guo, and Fan (2023) [59] | The network centrality of institutional investors (+) | ESG performance | Bloomberg (main test) and SynTao (robustness test) | 2009–2020 | 7562 (main test) 2876 (robustness test) |

| Wang, Sun, Wang, Hua, and Wu (2023) [60] | Environmental uncertainty (-) | ESG performance | Bloomberg (main test) and SSII (robustness test) | 2011–2020 | 5570 |

| Ren, Zeng, and Zhao (2023) [61] | Digital finance (+) | ESG performance | Bloomberg (main test) and SSII (robustness test) | 2011–2020 | 7223 (main test) 6798 (robustness test) |

Appendix B

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | |

| SIZE | 0.075 *** | 0.036 ** | 0.081 *** | 0.015 | 0.066 *** | 0.054 *** | 0.083 *** |

| (4.873) | (2.585) | (5.442) | (0.995) | (5.596) | (3.184) | (6.958) | |

| AGE | −0.090 ** | −0.089 *** | −0.086 ** | −0.068 * | −0.092 *** | 0.019 | −0.004 |

| (−2.459) | (−2.671) | (−2.406) | (−1.898) | (−3.274) | (0.470) | (−0.150) | |

| LEV | −0.145 | 0.038 | −0.158 | −0.117 | −0.121 | −0.194 | −0.204 ** |

| (−1.320) | (0.387) | (−1.489) | (−1.098) | (−1.443) | (−1.607) | (−2.411) | |

| ROE | −0.370 * | −0.476 ** | −0.053 | −0.414 ** | −0.053 | −0.173 | 0.032 |

| (−1.795) | (−2.546) | (−0.265) | (−2.075) | (−0.334) | (−0.759) | (0.203) | |

| Balance | 3.563 * | 4.825 ** | 3.687 * | 2.192 | 2.947 * | 1.614 | 2.169 |

| (1.720) | (2.564) | (1.841) | (1.091) | (1.856) | (0.706) | (1.355) | |

| _cons | −1.167 *** | −0.275 | −1.321 *** | 0.283 | −1.074 *** | −0.681 | −1.334 *** |

| (−3.127) | (−0.812) | (−3.661) | (0.783) | (−3.753) | (−1.651) | (−4.624) | |

| N | 157 | 157 | 157 | 157 | 157 | 157 | 157 |

| r2 | 0.222 | 0.197 | 0.224 | 0.063 | 0.252 | 0.078 | 0.271 |

Appendix C

| Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | |

|---|---|---|---|---|---|---|---|

| Bloomberg | 1 | ||||||

| FTSE | 0.608 *** | 1 | |||||

| MSCI | 0.670 *** | 0.582 *** | 1 | ||||

| SynTao | 0.719 *** | 0.607 *** | 0.571 *** | 1 | |||

| RKS | 0.685 *** | 0.670 *** | 0.629 *** | 0.573 *** | 1 | ||

| SSII | 0.295 *** | 0.116 | 0.227 *** | 0.257 *** | 0.154 ** | 1 | |

| CASVI | 0.441 *** | 0.203 *** | 0.397 *** | 0.275 *** | 0.331 *** | 0.438 *** | 1 |

| Mean of coefficients | 0.570 | 0.464 | 0.513 | 0.500 | 0.507 | 0.248 | 0.348 |

References

- Zhou, Y.; Wang, E. Urban consumers’ attitudes towards the safety of milk powder after the melamine scandal in 2008 and the factors influencing the attitudes. China Agric. Econ. Rev. 2011, 3, 101–111. [Google Scholar] [CrossRef]

- Wang, L. Research on the Environmental Information Disclosure System in Sudden Environmental Pollution Incidents: Taking Zijin Mining Pollution Incident as an Example. In China Green Development Index Report 2011; Li, X., Pan, J., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 449–459. [Google Scholar] [CrossRef]

- Li, R.Y.M.; Li, B.; Zhu, X.; Zhao, J.; Pu, R.; Song, L. Modularity clustering of economic development and ESG attributes in prefabricated building research. Front. Environ. Sci. 2022, 10, 977887. [Google Scholar] [CrossRef]

- Syntao. China Sustainable Investment Review; Syntao: Bejing, China, 2022; 2p. [Google Scholar]

- Li, S.; Yin, P.; Liu, S. Evaluation of ESG Ratings for Chinese Listed Companies From the Perspective of Stock Price Crash Risk. Front. Environ. Sci. 2022, 10, 933639. [Google Scholar] [CrossRef]

- Liu, M. Quantitative ESG disclosure and divergence of ESG ratings. Front. Psychol. 2022, 13, 936798. [Google Scholar] [CrossRef] [PubMed]

- Berg, F.; Kölbel, J.F.; Rigobon, R. Aggregate Confusion: The Divergence of ESG Ratings. Rev. Financ. 2022, 26, 1315–1344. [Google Scholar] [CrossRef]

- Billio, M.; Costola, M.; Hristova, I.; Latino, C.; Pelizzon, L. Inside the ESG ratings: (Dis)agreement and performance. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1426–1445. [Google Scholar] [CrossRef]

- Dimson, E.; Marsh, P.; Staunton, M. Divergent ESG Ratings. J. Portf. Manag. 2020, 47, 75–87. [Google Scholar] [CrossRef]

- Dumrose, M.; Rink, S.; Eckert, J. Disaggregating confusion? The EU Taxonomy and its relation to ESG rating. Financ. Res. Lett. 2022, 48, 102928. [Google Scholar] [CrossRef]

- Gibson Brandon, R.; Krueger, P.; Schmidt, P.S. ESG Rating Disagreement and Stock Returns. Financ. Anal. J. 2021, 77, 104–127. [Google Scholar] [CrossRef]

- Kimbrough, M.D.; Wang, X.F.; Wei, S.; Zhang, J.I. Does Voluntary ESG Reporting Resolve Disagreement among ESG Rating Agencies? Eur. Account. Rev. 2022. ahead-of-print. [Google Scholar] [CrossRef]

- Zumente, I.; Lāce, N. ESG Rating—Necessity for the Investor or the Company? Sustainability 2021, 13, 8940. [Google Scholar] [CrossRef]

- Christensen, D.M.; Serafeim, G.; Sikochi, A. Why is Corporate Virtue in the Eye of The Beholder? The Case of ESG Ratings. Account. Rev. 2022, 97, 147–175. [Google Scholar] [CrossRef]

- Tian, H.; Tian, G. Corporate sustainability and trade credit financing: Evidence from environmental, social, and governance ratings. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1896–1908. [Google Scholar] [CrossRef]

- Chatterji, A.K.; Durand, R.; Levine, D.I.; Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strat. Manag. J. 2016, 37, 1597–1614. [Google Scholar] [CrossRef]

- Zhu, X.; Li, R.Y.M.; Crabbe, M.J.C.; Sukpascharoen, K. Can a chatbot enhance hazard awareness in the construction industry? Front. Public. Health 2022, 10, 993700. [Google Scholar] [CrossRef]

- Cohen, I.; Huang, Y.; Chen, J.; Benesty, J.; Benesty, J.; Chen, J.; Huang, Y.; Cohen, I. Pearson correlation coefficient. In Noise Reduction in Speech Processing; Springer: Berlin/Heidelberg, Germany, 2009; pp. 1–4. [Google Scholar]

- Capizzi, V.; Gioia, E.; Giudici, G.; Tenca, F. The divergence of esg ratings: An analysis of italian listed companies. J. Financ. Manag. Mark. Inst. 2021, 09, 2150006. [Google Scholar] [CrossRef]

- Kotsantonis, S.; Serafeim, G. Four Things No One Will Tell You About ESG Data. J. Appl. Corp. Financ. 2019, 31, 50–58. [Google Scholar] [CrossRef]

- Saadaoui, K.; Soobaroyen, T. An analysis of the methodologies adopted by CSR rating agencies. Sustain. Account. Manag. Policy J. 2018, 9, 43–62. [Google Scholar] [CrossRef]

- White, L.J. Markets: The Credit Rating Agencies. J. Econ. Perspect. 2010, 24, 211–226. [Google Scholar] [CrossRef]

- Chang, K.; Cheng, X.; Wang, Y.; Liu, Q.; Hu, J. The impacts of ESG performance and digital finance on corporate financing efficiency in China. Appl. Econ. Lett. 2023, 30, 516–523. [Google Scholar] [CrossRef]

- Li, C.; Ba, S.; Ma, K.; Xu, Y.; Huang, W.; Huang, N. ESG Rating Events, Financial Investment Behavior and Corporate Innovation. Econ. Anal. Policy 2023, 77, 372–387. [Google Scholar] [CrossRef]

- Feng, J.; Goodell, J.W.; Shen, D. ESG rating and stock price crash risk: Evidence from China. Financ. Res. Lett. 2022, 46, 102476. [Google Scholar] [CrossRef]

- Li, H.; Zhang, X.; Zhao, Y. ESG and Firm’s Default Risk. Financ. Res. Lett. 2022, 47, 102713. [Google Scholar] [CrossRef]

- Deng, X.; Li, W.; Ren, X. More sustainable, more productive: Evidence from ESG ratings and total factor productivity among listed Chinese firms. Financ. Res. Lett. 2023, 51, 103439. [Google Scholar] [CrossRef]

- Hu, J.; Zou, Q.; Yin, Q. Research on the effect of ESG performance on stock price synchronicity: Empirical evidence from China’s capital markets. Financ. Res. Lett. 2023, 103847. [Google Scholar] [CrossRef]

- Kong, W. The impact of ESG performance on debt financing costs: Evidence from Chinese family business. Financ. Res. Lett. 2023, 55, 103949. [Google Scholar] [CrossRef]

- Luo, C.; Wei, D.; He, F. Corporate ESG performance and trade credit financing—Evidence from China. Int. Rev. Econ. Financ. 2023, 85, 337–351. [Google Scholar] [CrossRef]

- Lian, Y.; Ye, T.; Zhang, Y.; Zhang, L. How does corporate ESG performance affect bond credit spreads: Empirical evidence from China. Int. Rev. Econ. Financ. 2023, 85, 352–371. [Google Scholar] [CrossRef]

- Chen, Y.; Li, T.; Zeng, Q.; Zhu, B. Effect of ESG performance on the cost of equity capital: Evidence from China. Int. Rev. Econ. Financ. 2023, 83, 348–364. [Google Scholar] [CrossRef]

- Li, J.; Lian, G.; Xu, A. How do ESG affect the spillover of green innovation among peer firms? Mechanism discussion and performance study. J. Bus. Res. 2023, 158, 113648. [Google Scholar] [CrossRef]

- Zeng, L.; Jiang, X. ESG and Corporate Performance: Evidence from Agriculture and Forestry Listed Companies. Sustainability 2023, 15, 6723. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strat. Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.W.; Wang, X. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 101716. [Google Scholar] [CrossRef] [PubMed]

- Wang, J.; Ma, M.; Dong, T.; Zhang, Z. Do ESG ratings promote corporate green innovation? A quasi-natural experiment based on SynTao Green Finance’s ESG ratings. Int. Rev. Financ. Anal. 2023, 87, 102623. [Google Scholar] [CrossRef]

- Deng, X.; Cheng, X. Can ESG Indices Improve the Enterprises’ Stock Market Performance?—An Empirical Study from China. Sustainability 2019, 11, 4765. [Google Scholar] [CrossRef]

- Yang, Y.; Du, Z.; Zhang, Z.; Tong, G.; Zhou, R. Does ESG Disclosure Affect Corporate-Bond Credit Spreads? Evidence from China. Sustainability 2021, 13, 8500. [Google Scholar] [CrossRef]

- Xu, J.; Liu, F.; Shang, Y. R&D investment, ESG performance and green innovation performance: Evidence from China. Kybernetes 2020, 50, 737–756. [Google Scholar] [CrossRef]

- He, F.; Du, H.; Yu, B. Corporate ESG performance and manager misconduct: Evidence from China. Int. Rev. Financ. Anal. 2022, 82, 102201. [Google Scholar] [CrossRef]

- Yu, G.; Liu, Y.; Cheng, W.; Lee, C. Data Analysis of ESG Stocks in the Chinese Stock Market Based on Machine Learning. In Proceedings of the 2022 2nd International Conference on Consumer Electronics and Computer Engineering (ICCECE), Guangzhou, China, 1 January 2022; IEEE: New York, NY, USA, 2022; pp. 486–493. [Google Scholar] [CrossRef]

- Jun, W.; Shiyong, Z.; Yi, T. Does ESG Disclosure Help Improve Intangible Capital? Evidence From A-Share Listed Companies. Front. Environ. Sci. 2022, 10, 858548. [Google Scholar] [CrossRef]

- Zhang, X.; Zhao, X.; He, Y. Does It Pay to Be Responsible? The Performance of ESG Investing in China. Emerg. Mark. Financ. Trade 2022, 58, 3048–3075. [Google Scholar] [CrossRef]

- Chen, Z.; Xie, G. ESG disclosure and financial performance: Moderating role of ESG investors. Int. Rev. Financ. Anal. 2022, 83, 102291. [Google Scholar] [CrossRef]

- Yuan, X.; Li, Z.; Xu, J.; Shang, L. ESG disclosure and corporate financial irregularities—Evidence from Chinese listed firms. J. Clean. Prod. 2022, 332, 129992. [Google Scholar] [CrossRef]

- Chen, L.; Khurram, M.U.; Gao, Y.; Abedin, M.Z.; Lucey, B. ESG disclosure and technological innovation capabilities of the Chinese listed companies. Res. Int. Bus. Financ. 2023, 65, 101974. [Google Scholar] [CrossRef]

- Ge, G.; Xiao, X.; Li, Z.; Dai, Q. Does ESG Performance Promote High-Quality Development of Enterprises in China? The Mediating Role of Innovation Input. Sustainability 2022, 14, 3843. [Google Scholar] [CrossRef]

- Liu, P.; Zhu, B.; Yang, M.; Chu, X. ESG and financial performance: A qualitative comparative analysis in China’s new energy companies. J. Clean. Prod. 2022, 379, 134721. [Google Scholar] [CrossRef]

- Zhou, D.; Zhou, R. ESG Performance and Stock Price Volatility in Public Health Crisis: Evidence from COVID-19 Pandemic. Int. J. Environ. Res. Pub. Health 2022, 19, 202. [Google Scholar] [CrossRef] [PubMed]

- Cheng, L.T.W.; Lee, S.K.; Li, S.K.; Tsang, C.K. Understanding resource deployment efficiency for ESG and financial performance: A DEA approach. Res. Int. Bus. Financ. 2023, 65, 101941. [Google Scholar] [CrossRef]

- Baker, E.D.; Boulton, T.J.; Braga-Alves, M.V.; Morey, M.R. ESG government risk and international IPO underpricing. J. Corp. Financ. 2021, 67, 101913. [Google Scholar] [CrossRef]

- Mu, W.; Liu, K.; Tao, Y.; Ye, Y. Digital finance and corporate ESG. Financ. Res. Lett. 2023, 51, 103426. [Google Scholar] [CrossRef]

- Wang, Y.; Lin, Y.; Fu, X.; Chen, S. Institutional ownership heterogeneity and ESG performance: Evidence from China. Financ. Res. Lett. 2023, 51, 103448. [Google Scholar] [CrossRef]

- Wang, D.; Peng, K.; Tang, K.; Wu, Y. Does Fintech Development Enhance Corporate ESG Performance? Evidence from an Emerging Market. Sustainability 2022, 14, 16597. [Google Scholar] [CrossRef]

- Liu, J.; Xiong, X.; Gao, Y.; Zhang, J. The impact of institutional investors on ESG: Evidence from China. Account. Financ. 2022, 63, 2801–2826. [Google Scholar] [CrossRef]

- Meng, X.; Zhu, P. Females’ social responsibility: The impact of female executives on ESG performance. Appl. Econ. Lett. 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Fang, M.; Nie, H.; Shen, X. Can enterprise digitization improve ESG performance? Econ. Model. 2023, 118, 106101. [Google Scholar] [CrossRef]

- Yang, B.; Guo, C.; Fan, Y. Institutional Investor Networks and ESG Performance: Evidence from China. Emerg. Mark. Mark. Mark. Mark. Financ. Financ. Financ. Trade 2023. ahead-of-print. [Google Scholar] [CrossRef]

- Wang, W.; Sun, Z.; Wang, W.; Hua, Q.; Wu, F. The impact of environmental uncertainty on ESG performance: Emotional vs. rational. J. Clean. Prod. 2023, 397, 136528. [Google Scholar] [CrossRef]

- Ren, X.; Zeng, G.; Zhao, Y. Digital finance and corporate ESG performance: Empirical evidence from listed companies in China. Pac -Basin Financ. J. 2023, 79, 102019. [Google Scholar] [CrossRef]

| Rating | Category | Start Time | Attributes | Coverage |

|---|---|---|---|---|

| Bloomberg | International | 2006 | Index/data provider | Approximately 860 A-share firms in 2011, over 1200 after 2020 |

| FTSE | International | 2019 | Index/data provider | Covering 30 in 2018, rising to 679 in 2019, and approximately 900 A-share listed firms by the end of 2022 |

| MSCI | International | 2018 | Index/data provider | Covering 5% of A-share listed firms in 2018, raised to 20% in 2019 |

| SynTao | Domestic | 2015 | Consultancy | Hushen 300 (2015), CSI 500 (from 2018), now covering all A-share listed firms |

| RKS | Domestic | 2020 | Consultancy | CSI 800 |

| SSII | Domestic | 2017 | Index/data provider | All A-share listed firms |

| CASVI | Domestic | 2017 | NGO | Hushen 300 |

| Panel A | |||||||||

| Rating Agency | Framework Level | Level-1 Division | Number of Underlying Metrics | ||||||

| Bloomberg | 3 | Environment, social, and corporate governance | 61 | ||||||

| FTSE | 3 | Environment, social, and corporate governance | 300+ | ||||||

| MSCI | 3 | Environment, social, and corporate governance | 37 | ||||||

| SynTao | 3 | Environment, social, and corporate governance | 200+ | ||||||

| RKS | 3 | Environment, social, and corporate governance | 37 | ||||||

| SSII | 3 | Environment, social, and corporate governance | 26 | ||||||

| CASVI | 4 | Objective (driving force), approach (innovation), effectiveness (implementation) | 55 | ||||||

| Panel B | |||||||||

| Dimension | Issue | Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | Frequency |

| Environment | Solid waste discharge | √ | √ | √ | √ | √ | √ | √ | 7 |

| Climate change | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Sewage discharge | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Environmental supply chain | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Exhaust gas emission | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Biodiversity | √ | √ | √ | √ | √ | √ | — | 6 | |

| Water resource management | √ | √ | √ | √ | — | √ | √ | 6 | |

| Negative environmental events | √ | √ | — | √ | √ | √ | √ | 6 | |

| Green purchasing | √ | √ | √ | √ | — | √ | √ | 6 | |

| Energy issues | √ | √ | — | √ | — | √ | √ | 5 | |

| Green products | — | — | √ | √ | √ | √ | — | 4 | |

| Renewable energy management | √ | — | √ | √ | — | √ | — | 4 | |

| Packaging materials | — | — | √ | — | √ | — | — | 2 | |

| Society | Health and safety | √ | √ | √ | √ | √ | √ | √ | 7 |

| Supply chain management | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Product safety | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Employee compensation | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Staff training | √ | — | √ | √ | √ | √ | √ | 6 | |

| Negative events | — | √ | √ | √ | — | √ | √ | 5 | |

| Communities | √ | — | — | √ | √ | √ | √ | 5 | |

| Customer management | √ | √ | — | √ | — | √ | √ | 5 | |

| Corporate donation | — | — | — | √ | √ | √ | √ | 4 | |

| Employee diversity | √ | — | — | √ | √ | — | √ | 4 | |

| Information security | — | — | √ | √ | √ | √ | — | 4 | |

| Human rights | √ | √ | √ | √ | — | — | — | 4 | |

| Inclusive finance | — | — | — | √ | √ | √ | — | 4 | |

| Governance | Fighting corruption | √ | √ | √ | √ | √ | √ | √ | 7 |

| Board structure | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Independent directors | √ | √ | √ | √ | √ | √ | √ | 7 | |

| Audit and supervision | √ | √ | √ | √ | √ | — | √ | 6 | |

| Business ethics | √ | — | √ | √ | √ | √ | √ | 6 | |

| Executive compensation | √ | — | √ | √ | √ | — | — | 4 | |

| Risk management | — | √ | — | — | √ | √ | √ | 4 | |

| Tax transparency | — | √ | √ | √ | — | √ | — | 4 | |

| ESG disclosure | — | √ | — | √ | — | √ | √ | 4 | |

| Debt-paying ability | — | — | — | — | — | √ | √ | 2 | |

| Rating Agency | Information Sources Claimed by the Rating Agency |

|---|---|

| Bloomberg | Public information such as the firm’s sustainability reports, financial statements, website, and press releases. |

| FTSE | Mainly from public information from listed firms, regulators, news media, and other NGOs. |

| MSCI | Public data: government, regulatory, and NGO datasets; firm disclosure documents; 3400 media sources. |

| SynTao | The positive information mainly comes from the independent disclosure of firms, while the negative information comes from the independent disclosure of firms, media reports, announcements of regulatory authorities, and surveys of social organizations. |

| RKS | Mainly comes from the information independently disclosed by the firm, including the firm’s annual report, corporate social responsibility report, and articles of association. |

| SSII | Open data based on a machine learning and text mining algorithm that crawls the website data of the government and relevant regulatory authorities, news media data, etc. |

| CASVI | Public information, including the firm’s annual report, social responsibility report, government departments and third-party announcements, etc. |

| Rating Agency | Review Process |

|---|---|

| Bloomberg | Review the scoring framework internally and establish communication channels with the firm. |

| FTSE | Oversight by external committees set up by businesses, investors, nonprofit organizations, experts, and academics. |

| MSCI | Invite the evaluated firms to review relevant information and data before issuing the final score. |

| SynTao | Conduct cross audits within the organization. |

| RKS | A technical committee composed of experts and scholars from external universities and research institutions can review the rating results. |

| SSII | An ESG expert committee is set up to review the rating results. |

| CASVI | Hire data experts to review and verify information with regulatory authorities and industry associations. |

| Rating Agency | Total Number of Chinese Firms Covered in 2019 | Number of Hushen 300 Firms Covered in 2019 | Number of Hushen 300 Firms Commonly Covered by All Ratings in 2019 |

|---|---|---|---|

| Bloomberg | 1207 | 250 | 195 |

| FTSE | 679 | 255 | 195 |

| MSCI | 580 | 283 | 195 |

| SynTao | 1267 | 279 | 195 |

| RKS | 790 | 294 | 195 |

| SSII | 3775 | 300 | 195 |

| CASVI | 410 | 268 | 195 |

| Panel A (Before 0–1 Standardization) | |||||||||

| Rating Agency | N | Mean | SD | Min | P25 | P50 | P75 | Max | Scoring Range |

| Bloomberg | 195 | 30.55 | 10.52 | 11.98 | 21.49 | 28.93 | 39.26 | 59.92 | 0.1–99 |

| FTSE | 195 | 1.59 | 0.54 | 0.50 | 1.20 | 1.60 | 2.00 | 2.90 | 0–5 |

| MSCI | 195 | 37.71 | 16.29 | 3.17 | 26.53 | 35.16 | 49.58 | 81.02 | 0–100 |

| SynTao | 195 | 52.12 | 6.39 | 39.13 | 47.63 | 51.13 | 56.75 | 71.88 | 0–100 |

| RKS | 195 | 2.97 | 1.45 | 0.76 | 1.85 | 2.69 | 3.84 | 7.00 | 0–7 |

| SSII | 195 | 5.03 | 1.11 | 2.00 | 2.00 | 4.00 | 5.00 | 6.00 | 0–9 |

| CASVI | 195 | 11.97 | 4.01 | 1.00 | 10.00 | 12.00 | 15.00 | 19.00 | 0–20 |

| Panel B (After 0–1 Standardization) | |||||||||

| Rating Agency | N | Mean | SD | Min | P25 | P50 | P75 | Max | Scoring Range |

| Bloomberg | 195 | 0.387 | 0.220 | 0.017 | 0.198 | 0.353 | 0.569 | 0.879 | 0–1 |

| FTSE | 195 | 0.452 | 0.226 | 0.042 | 0.292 | 0.458 | 0.625 | 0.958 | 0–1 |

| MSCI | 195 | 0.444 | 0.209 | 0.005 | 0.300 | 0.411 | 0.596 | 0.952 | 0–1 |

| SynTao | 195 | 0.397 | 0.195 | 0.027 | 0.260 | 0.366 | 0.538 | 0.905 | 0–1 |

| RKS | 195 | 0.354 | 0.232 | 0.010 | 0.175 | 0.309 | 0.494 | 0.952 | 0–1 |

| SSII | 195 | 0.605 | 0.221 | 0.000 | 0.400 | 0.600 | 0.800 | 1.000 | 0–1 |

| CASVI | 195 | 0.610 | 0.223 | 0.000 | 0.500 | 0.611 | 0.778 | 0.944 | 0–1 |

| Panel A (Overlap Frequency of the Top 100 Sample Firms) | |||||||

| Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | |

| (1) Bloomberg | 103 | ||||||

| (2) FTSE | 84 | 107 | |||||

| (3) MSCI | 77 | 78 | 100 | ||||

| (4) SynTao | 81 | 78 | 72 | 100 | |||

| (5) RKS | 82 | 77 | 75 | 74 | 100 | ||

| (6) SSII | 81 | 82 | 77 | 78 | 77 | 133 | |

| (7) CASVI | 75 | 71 | 71 | 69 | 70 | 98 | 119 |

| (8) | Overlap frequency of international ratings: 57 | ||||||

| (9) | Overlap frequency of domestic ratings: 46 | ||||||

| (10) | Overlap frequency of all ratings: 35 | ||||||

| Panel B (Overlap Rate of the Top 100 Sample Firms) | |||||||

| Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | |

| (1) Bloomberg | 100% | ||||||

| (2) FTSE | 81.55% | 100% | |||||

| (3) MSCI | 77.00% | 78.00% | 100% | ||||

| (4) SynTao | 81.00% | 78.00% | 72.00% | 100% | |||

| (5) RKS | 82.00% | 77.00% | 75.00% | 74.00% | 100% | ||

| (6) SSII | 78.64% | 76.64% | 77.00% | 78.00% | 77.00% | 100% | |

| (7) CASVI | 72.82% | 66.36% | 71.00% | 69.00% | 70.00% | 82.35% | 100% |

| (8) | Overlap rate of international ratings: 57% | ||||||

| (9) | Overlap rate of domestic ratings: 46% | ||||||

| (10) | Overlap rate of all ratings: 35% | ||||||

| Bloomberg | FTSE | MSCI | SynTao | RKS | SSII | CASVI | |

|---|---|---|---|---|---|---|---|

| Bloomberg | 1 | ||||||

| FTSE | 0.591 *** | 1 | |||||

| MSCI | 0.682 *** | 0.566 *** | 1 | ||||

| SynTao | 0.736 *** | 0.607 *** | 0.587 *** | 1 | |||

| RKS | 0.621 *** | 0.686 *** | 0.597 *** | 0.550 *** | 1 | ||

| SSII | 0.310 *** | 0.114 | 0.223 *** | 0.274 *** | 0.155 ** | 1 | |

| CASVI | 0.300 *** | 0.057 | 0.261 *** | 0.171 ** | 0.121 * | 0.427 *** | 1 |

| Mean of coefficients | 0.540 (0.658) | 0.437 (0.613) | 0.486 (0.608) | 0.488 (0.620) | 0.455 (0.614) | 0.251 | 0.223 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhu, Y.; Yang, H.; Zhong, M. Do ESG Ratings of Chinese Firms Converge or Diverge? A Comparative Analysis Based on Multiple Domestic and International Ratings. Sustainability 2023, 15, 12573. https://doi.org/10.3390/su151612573

Zhu Y, Yang H, Zhong M. Do ESG Ratings of Chinese Firms Converge or Diverge? A Comparative Analysis Based on Multiple Domestic and International Ratings. Sustainability. 2023; 15(16):12573. https://doi.org/10.3390/su151612573

Chicago/Turabian StyleZhu, Yunfu, Haoling Yang, and Ma Zhong. 2023. "Do ESG Ratings of Chinese Firms Converge or Diverge? A Comparative Analysis Based on Multiple Domestic and International Ratings" Sustainability 15, no. 16: 12573. https://doi.org/10.3390/su151612573