The Effect of Company Ownership on the Environmental Practices in the Supply Chain: An Empirical Approach

Abstract

:1. Introduction

2. Literature Review

2.1. What Is ESG and How Did It Emerge?

2.2. Sustainable Supply Chain Management

2.3. SSCM Challenges in the Current and Global Context

2.4. Importance of the E over the S and the G in ESG

2.5. The Importance of Sustainability

2.6. The Case of Insurers and Pension Funds

2.7. The Case of Hedge Funds

2.8. The Case of Sovereign Wealth Funds

2.9. Individual Investors

3. Materials and Methods

3.1. Methodology and Data

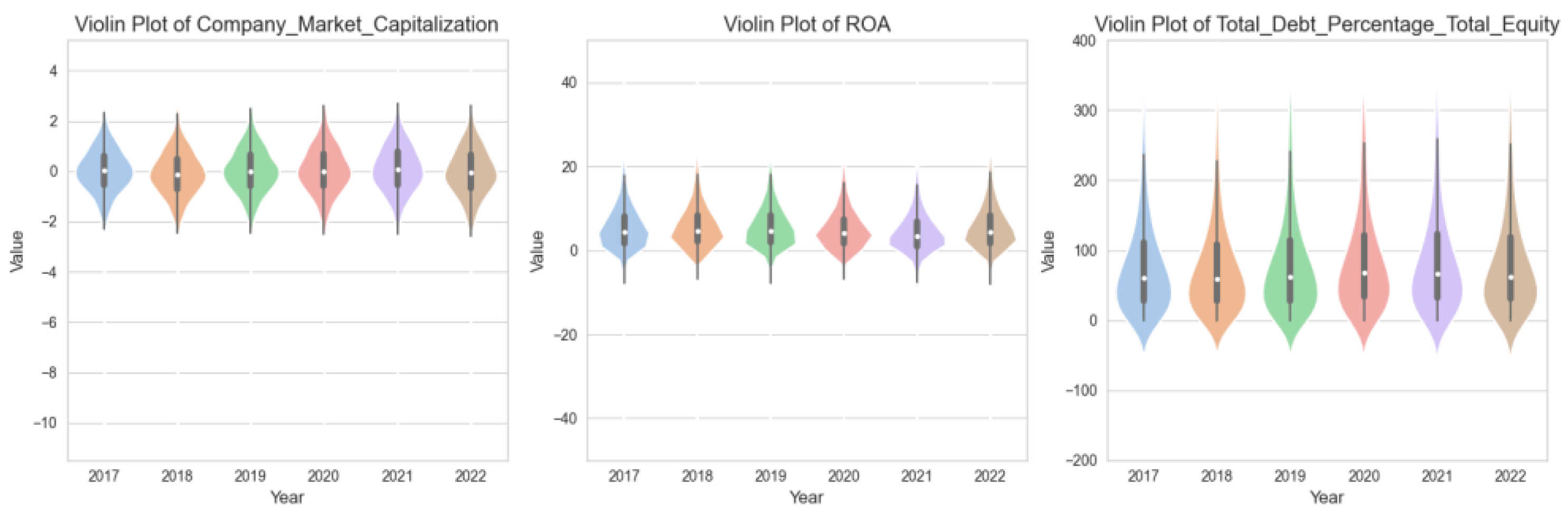

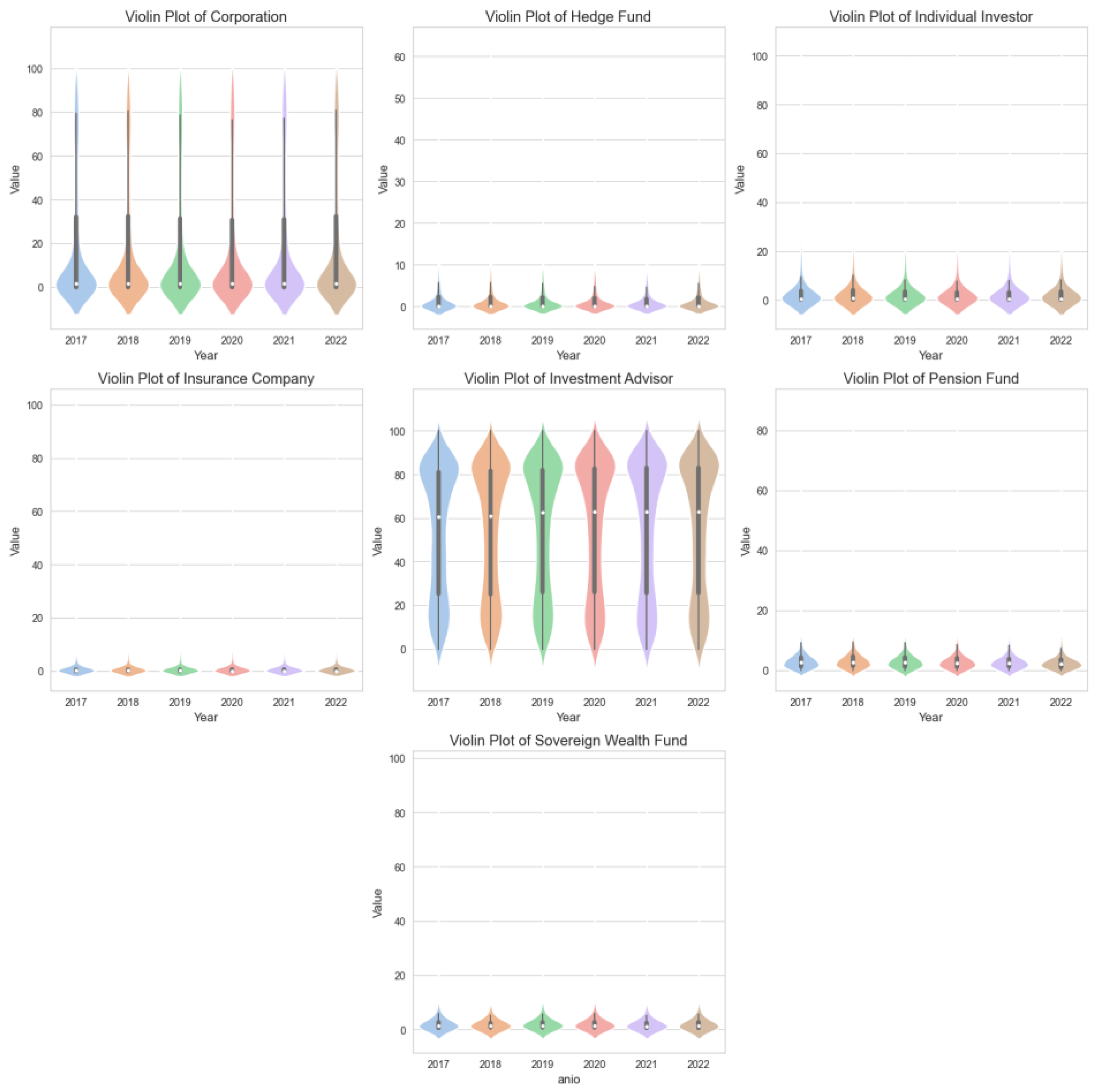

3.2. Variables

3.3. Explanatory and Control Variables

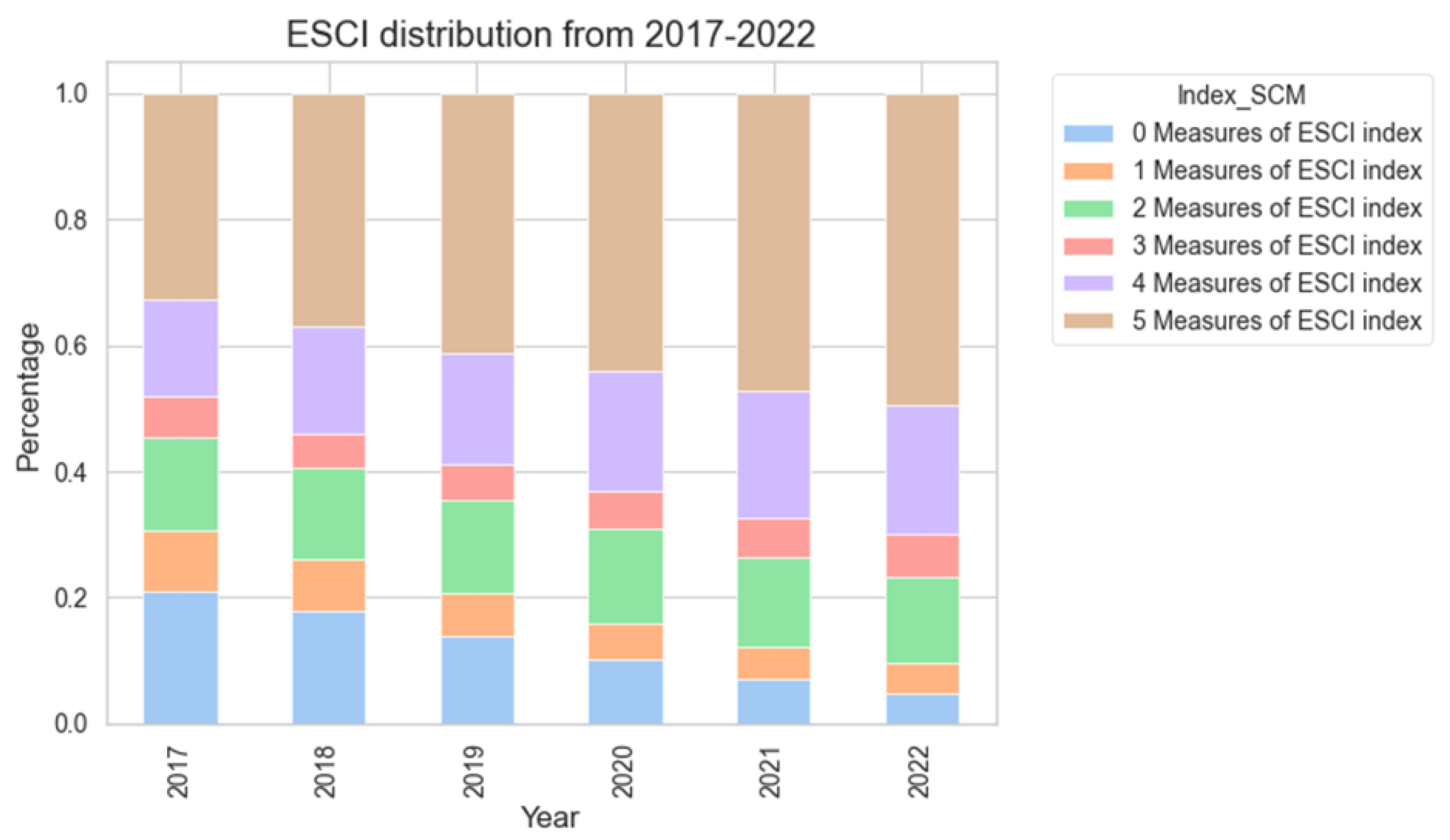

3.4. Environmental Supply Chain Index (ESCI)

3.5. Model

4. Results

4.1. Financial Variables

4.2. Industry Variables

4.3. Ownership Variables

5. Discussion

5.1. Long-Term Horizon Investments Correlate with Greater Use of ESG

5.2. Short-Term Horizon Investments Could Translate into Poor ESG Adoption

5.3. Hedge Funds Case with ESG Adoption

5.4. Policy Implications

6. Conclusions

Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- IPCC. Summary for Policymakers. Climate Change 2022: Impacts, Adaptation, and Vulnerability. In Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Pörtner, H.-O., Ed.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2022; pp. 3–33. [Google Scholar]

- García-Sánchez, I.M.; Aibar-Guzmán, C.; Aibar-Guzmán, B. The effect of institutional ownership and ownership dispersion on eco-innovation. Technol. Forecast. Soc. Change 2020, 158, 120173. [Google Scholar] [CrossRef]

- Wang, Y.; Lin, Y.; Fu, X.; Chen, S. Institutional ownership heterogeneity and ESG performance: Evidence from China. Financ. Res. Lett. 2023, 51, 103448. [Google Scholar] [CrossRef]

- Correll, D.; Betts, K. State of Supply Chain Sustainability 2022. Available online: https://ctl.mit.edu/pub/report/state-supply-chain-sustainability-2022 (accessed on 20 April 2023).

- Wang, Z.; Sarkis, J. Investigating the relationship of sustainable supply chain management with corporate financial performance. Int. J. Product. Perform. Manag. 2013, 62, 871–888. [Google Scholar] [CrossRef]

- Price Waterhouse Coopers (PWC). Accounting Reporting Update. Available online: www.pwc.com (accessed on 2 June 2022).

- Governance & Accountability Institute. 2022. Available online: https://www.ga-institute.com/research/ga-research-directory/sustainability-reporting-trends/2022-sustainability-reporting-in-focus.html (accessed on 20 April 2023).

- Titia Bové, A.; Swartz, S. Starting at the Source: Sustainability in Supply Chains. 2016. McKinsey Sustainability. Available online: https://www.mckinsey.com/capabilities/sustainability/our-insights/starting-at-the-source-sustainability-in-supply-chains (accessed on 20 April 2023).

- Yasar, K. ESG Benefits for Businesses. ESG Strategy and Management: Complete Guide for Businesses. IT Standards and Organizations. TechTarget. 2023. Available online: https://www.techtarget.com/sustainability/feature/ESG-strategy-and-management-Complete-guide-for-businesses (accessed on 8 June 2022).

- Whelan, T.; Atz, U.; Van Holt, T.; Clark, C. ESG and Financial Performance: Uncovering the Relationship by Aggregating Evidence from 1000 Plus Studies Published between 2015–2020; NYU STERN Center for Sustainable Business: New York, NY, USA, 2021. [Google Scholar]

- Luo, X.; Bhattacharya, C.B. Corporate social responsibility, customer satisfaction, and market value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, L.; Luo, S. Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Bus. Strategy Environ. 2022, 31, 3371–3387. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Sirsly, C.A.T.; Lvina, E. From doing good to looking even better: The dynamics of CSR and reputation. Bus. Soc. 2019, 58, 1234–1266. [Google Scholar] [CrossRef]

- Xie, X.; Zhu, Q.; Wang, R. Turning green subsidies into sustainability: How green process innovation improves firms’ green image. Bus. Strategy Environ. 2019, 28, 1416–1433. [Google Scholar] [CrossRef]

- Huang, D.Z. Environmental, social and governance (ESG) activity and firm performance: A review and consolidation. Account. Financ. 2021, 61, 335–360. [Google Scholar] [CrossRef]

- Dyck, A.; Lins, K.V.; Roth, L.; Wagner, H.F. Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 2019, 131, 693–714. [Google Scholar] [CrossRef]

- Earnhart, D.; Lízal, L. Direct and indirect effects of ownership on firm-level environmental performance. East. Eur. Econ. 2007, 45, 66–87. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Aibar-Guzmán, C.; Núñez-Torrado, M.; Aibar-Guzmán, B. Are institutional investors “in love” with the sustainable development goals? Understanding the idyll in the case of governments and pension funds. Sustain. Dev. 2022, 30, 1099–1116. [Google Scholar]

- Aibar-Guzmán, B.; Aibar-Guzmán, C.; Piñeiro-Chousa, J.; Hussain, N.; García-Sánchez, I. The benefits of climate tech: Do institutional investors affect these impacts? Technol. Forecast. Soc. Change 2023, 192, 122536. [Google Scholar] [CrossRef]

- Baid, V.; Jayaraman, V. Amplifying and promoting the “S” in ESG investing: The case for social responsibility in supply chain financing. Manag. Financ. 2022, 48, 1279–1297. [Google Scholar] [CrossRef]

- United Nations Environment Programme, Who Cares Wins—Connecting Financial Markets to a Changing World. 2004. Available online: https://www.unepfi.org/fileadmin/events/2004/stocks/who_cares_wins_global_compact_2004.pdf (accessed on 20 April 2023).

- CFA Institute. Environmental, Social and Governance Issues in Investing: A Guide for Investment Professionals; Center for Financial Analysis: London, UK, 2015. [Google Scholar]

- Kotsantonis, S.; Pinney, C.; Serafeim, G. ESG integration in investment management: Myths and realities. J. Appl. Corp. Financ. 2016, 28, 10–16. [Google Scholar]

- Gold, S.; Seuring, S.; Beske, P. The constructs of sustainable supply chain management: Content analysis based on pu-blished case studies. Prog. Ind. Ecol. Int. J. 2010, 7, 114–137. [Google Scholar] [CrossRef]

- Panigrahi, S.S.; Bahinipati, B. Sustainable supply chain management: A review of literature and implications for future research. Manag. Environ. Qual. Int. J. 2019, 30, 1001–1049. [Google Scholar] [CrossRef]

- Kossmeier, S.; Ariely, D.; Bracha, A. Doing good or doing well? Image motivation and monetary incentives in behaving prosocially. Am. Econ. Rev. 2009, 99, 544–555. [Google Scholar]

- Khodakarami, M.; Shabani, A.; Saen, R.F.; Azadi, M. Developing distinctive two-stage data envelopment analysis models: An application in evaluating the sustainability of supply chain management. Measurement 2015, 70, 62–74. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainable supply chain management: Moving toward new theory. Interna Tional J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

- Pagell, M.; Wu, Z. Building a more complete theory of sustainable supply chain management using case studies of 10 exemplars. J. Supply Chain Manag. 2009, 45, 37–56. [Google Scholar] [CrossRef]

- Tiwari, M.; Tiwari, T.; Sam Santhose, S.; Mishra, L.; Rajeesh, M.R.; Sundararaj, V. Corporate social responsibility and supply chain: A study for evaluating corporate hypocrite with special focus on stakeholders. Int. J. Financ. Econ. 2021, 28, 1391–1403. [Google Scholar] [CrossRef]

- Aras, G.; Crowther, D. The Durable Corporation: Strategies for Sustainable Development; Gower Publishing Limited: Surrey, UK, 2016. [Google Scholar]

- Amel-Zadeh, A.; Serafeim, G. Why and how investors use ESG information: Evidence from a global survey. Financ. A-Nalysts J. 2018, 74, 87–103. [Google Scholar] [CrossRef]

- Epstein, M.J.; Buhovac, A.R.; Yuthas, K. Managing social, environmental and financial performance simultaneously. Long Range Plan. 2015, 48, 35–45. [Google Scholar] [CrossRef]

- Krause, D.R.; Vachon, S.; Klassen, R.D. Special topic forum on sustainable supply chain management: Introduction and reflections on the role of purchasing management. J. Supply Chain Manag. 2009, 45, 18–25. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Geng, Y. Green supply chain management in China: Pressures, practices and performance. Int. J. Oper. Prod. Manag. 2005, 25, 449–468. [Google Scholar] [CrossRef]

- Bevilacqua, M.; Ciarapica, F.E.; Mazzuto, G.; Paciarotti, C. Environmental analysis of a cotton yarn supply chain. J. Clean. Prod. 2014, 82, 154–165. [Google Scholar] [CrossRef]

- Rajak, S.; Vinodh, S. Application of fuzzy logic for social sustainability performance evaluation: A case study of an Indian automotive component manufacturing organization. J. Clean. Prod. 2015, 108, 1184–1192. [Google Scholar] [CrossRef]

- Reinhardt, F.L. Bringing the environment down to earth. Harv. Bus. Rev. 1999, 77, 149–157. [Google Scholar]

- Jeremy, H.; Stelvia, M. Incorporating Impoverished Communities in Sustainable Supply Chains. Int. J. Phys. Distrib. Logist. Manag. 2010, 40, 124–147. [Google Scholar]

- Gold, S.; Hahn, R.; Seuring, S. Sustainable supply chain management in ’Base of the Pyramid’ food projects—A path to triple bottom line approaches for multinationals? Int. Bus. Rev. 2013, 22, 784–799. Available online: https://EconPapers.repec.org/RePEc:eee:iburev:v:22:y:2013:i:5:p:784-799 (accessed on 16 June 2023). [CrossRef]

- Formentini, M.; Taticchi, P. Corporate Sustainability Approaches and Governance Mechanisms in Sustainable Supply Chain Management. J. Clean. Prod. 2016, 112, 1920–1933. [Google Scholar] [CrossRef]

- World Commission on Environment and Development (WCED). Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Liang, H.; Sun, L.; Teo, M. Responsible Hedge Funds. Rev. Financ. 2022, 26, 1585–1633. [Google Scholar] [CrossRef]

- Aldowaish, A.; Kokuryo, J.; Almazyad, O.; Goi, H.C. Environmental, social, and governance integration into the business model: Literature review and research agenda. Sustainability 2022, 14, 2959. [Google Scholar] [CrossRef]

- Liu, Y.; Li, W.; Meng, Q. Influence of distracted mutual fund investors on corporate ESG decoupling: Evidence from China. Sustain. Account. Manag. Policy J. 2023, 14, 184–215. [Google Scholar] [CrossRef]

- CampdenFB. Next Gen Involvement in Impact Investing Prepares Them for Future Family Responsibility. Available online: https://www.campdenfb.com/article/next-gen-involvement-impact-investing-prepares-them-future-family-responsibility (accessed on 25 January 2023).

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research progress and future prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Bellandi, F. Equilibrating financially sustainable growth and environmental, social, and governance sustainable growth. Eur. Manag. Rev. 2023, 12554. [Google Scholar] [CrossRef]

- Gatzert, N.; Reichel, P. Sustainable investing in the US and European insurance industry: A text mining analysis. Geneva Pap. Risk Insur. Issues Pract. 2022, 1–37. [Google Scholar] [CrossRef]

- Aburto Barrera, L.-I.; Wagner, J. A systematic literature review on sustainability issues along the value chain in insurance companies and pension funds. Eur. Actuar. J. 2023, 1–49. [Google Scholar] [CrossRef]

- United Nations Environmental Program (UNEP) Annual Report 2012. Available online: https://reliefweb.int/report/world/unep-annual-report-2012 (accessed on 28 May 2023).

- Boffo, R.; Patalano, R. ESG Investing: Practices, Progress and Challenges. OECD Paris. 2020. Available online: www.oecd.org/finance/ESG-Investing-Practices-Progress-and-Challenges.pdf (accessed on 16 June 2023).

- Meins, P.; Furlan, T.; Shier, P. Pension Fund Environmental, Social and Governance Risk Disclosures: Developing Global Practice; Technical Report; International Actuarial Association: Ottawa, ON, Canada, 2020; Available online: https://www.actuaries.org/IAA/Documents/Publications/Papers/REWG_Pension_Fund_ESG_Risk_Disclosures.pdf (accessed on 17 June 2023).

- Tomassetti, P. Between stakeholders and shareholders: Pension funds and labour solidarity in the age of sustainability. Eur. Labour Law J. 2022, 14, 73–91. [Google Scholar] [CrossRef]

- Liang, H.; Renneboog, L. The global sustainability footprint of sovereign wealth funds. Oxf. Rev. Econ. Policy 2020, 36, 380–426. [Google Scholar] [CrossRef]

- International Forum of Sovereign Wealth Funds (IFSWF). Sovereign Wealth Funds Report 2020. Available online: https://www.ifswf.org/content/2020-annual-report (accessed on 18 June 2003).

- Dai, L.; Song, C.; You, Y.; Zhang, W. Do sovereign wealth funds value ESG engagement? Evidence from target firm’s CSR performance. Financ. Res. Lett. 2022, 50, 103226. [Google Scholar] [CrossRef]

- Sovereign Wealth Research, IE Center for the Governance of Change. Sovereign Wealth Funds 2019. Available online: https://docs.ie.edu/cgc/research/sovereign-wealth/SOVEREIGN-WEALTH-RESEARCH-IE-CGC-REPORT_2019.pdf (accessed on 18 June 2023).

- Hawley, J.P.; Hoepner, A.G.; Johnson, K.L.; Sandberg, J.; Waitzer, E.J. (Eds.) Cambridge Handbook of Institutional Investment and Fiduciary Duty; Cambridge University Press: Cambridge, UK, 2014; pp. 1–6. [Google Scholar]

- Ferrell, A.; Liang, H.; Renneboog, L. Socially Responsible Firms. J. Financ. Econ. 2016, 122, 585–606. [Google Scholar] [CrossRef]

- Mohseni-Cheraghlou, A. Patterns and Trends in Sovereign Wealth Fund Investments: A Postcrisis Descriptive Analysis. Iran. Econ. Rev. 2017, 21, 725–763. [Google Scholar]

- Global Sustainable Investment Alliance. 2021. Available online: https://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf (accessed on 16 June 2023).

- Morgan Stanley. Morgan Stanley Survey Finds Investor Enthusiasm for Sustainable Investing. 2019. Available online: https://www.morganstanley.com/press-releases/morgan-stanley-survey-finds-investor-enthusiasm-for-sustainable- (accessed on 20 April 2023).

- Natixis Investment Managers. 2019 Individual Investor Survey Executive Overview. 2019. Available online: https://www.im.natixis.com/intl/resources/2019-individual-investor-survey-executive-overview (accessed on 20 April 2023).

- Canadian Responsible Investment Association. 2020 RIA Investor Opinion Survey. 2020. Available online: https://www.riacanada.ca/research/2020-ria-investor-opinion-survey/ (accessed on 20 April 2023).

- Ashby, A.; Leat, M.; Hudson-Smith, M. Making connections: A review of supply chain management and sustainability literature. Supply Chain Manag. Int. J. 2012, 17, 497–516. [Google Scholar] [CrossRef]

- Refinitiv. Environmental, Social and Governance Scores from Refinitiv. July 2023. Available online: https://www.refinitiv.com/en/products/refinitiv-workspace/download-workspace (accessed on 21 July 2023).

- Drempetic, S.; Klein, C.; Zwergel, B. The influence of firm size on the ESG score: Corporate Sustainability ratings under review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Dobrick, J.; Klein, C.; Zwergel, B. Size bias in Refinitiv ESG data. Financ. Res. Lett. 2023, 55, 104014. [Google Scholar] [CrossRef]

- Lai, K.H.; Wong, C.W. Green logistics management and performance: Some empirical evidence from Chinese manufacturing exporters. Omega 2012, 40, 267–282. [Google Scholar] [CrossRef]

- Liu, L.; Tang, M.; Xue, F. The impact of manufacturing firms’ green supply chain management on competitive advantage. Adv. Mater. Res. 2012, 472, 3349–3354. [Google Scholar]

- D’Amato, V.; D’Ecclesia, R.; Levantesi, S. fundamental ratios as predictors of ESG scores: A machine learning approach. Decis. Econ. Financ. 2021, 44, 1087–1110. [Google Scholar] [CrossRef]

- Bacharach, S.B. Organizational theories: Some criteria for evaluation. Acad. Manag. Rev. 1989, 14, 496–515. [Google Scholar] [CrossRef]

- Fullerton, A. A conceptual Framework for Ordered Logistic Regression Models. Sociol. Methods Res. 2009, 38, 306–347. [Google Scholar] [CrossRef]

- Zheng, Z.; Liu, Z.; Liu, C.; Shiwakoti, N. Understanding public response to a congestion charge: A random effects ordered logit approach. Transportation research. Part A Policy Pract. 2014, 70, 117–134. [Google Scholar] [CrossRef]

- Williams, R. Understanding and interpreting generalized ordered logit models. J. Math. Sociol. 2016, 40, 7–20. [Google Scholar] [CrossRef]

- Zumente, I.; Bistrova, J. ESG importance for long-term shareholder value creation: Literature vs. practice. J. Open Innov. Technol. Mark. Complex. 2021, 7, 127. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does it Pay to Be Good and Does it Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial Performance. SSRN Electron. J. 2009, ssrn.1866371. [Google Scholar] [CrossRef]

- Hoffmann, B.; Armangue i Jubert, T.; Parrado, E. The Business Case for ESG Investing for Pension and Sovereign Wealth Funds. Inter-American Development Bank. Department of Research. 2020. Available online: https://publications.iadb.org/en/the-business-case-for-esg-investing-for-pension-and-sovereign-wealth-funds (accessed on 22 April 2023).

- Gibson Brandon, R.; Glossner, S.; Krueger, P.; Matos, P.; Steffen, T. Do responsible investors invest responsibly? Rev. Financ. 2022, 26, 1389–1432. [Google Scholar] [CrossRef]

- Raghunandan, A.; Rajgopal, S. Do ESG funds make stakeholder-friendly investments? Rev. Account. Stud. 2022, 27, 822–863. [Google Scholar] [CrossRef]

- Bhagat, S. An Inconvenient Truth About ESG Investing. Harv. Bus. Rev. 2022, 1–3. [Google Scholar]

- Pancholi, D. Hedge Funds: Resolving Myths about ESG Integration. J. Altern. Investig. 2022, 25, 8–13. [Google Scholar] [CrossRef]

- Williamson, C. Hedge funds making progress, but slow to adopt ESG: Despite its popularity, managers say it’s hard to incorporate into strategies. Pensions Investig. 2019, 47, 3. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Measure | Abbreviation | Description |

|---|---|---|

| Environmental Materials Sourcing | EMS | Does the company claim to use environmental criteria (e.g., life cycle assessment) to source or eliminate material? |

| Environmental Supply Chain Management | ESCM | Does the company use environmental criteria (ISO 14000 [69]—energy consumption, etc.) in the selection process for its suppliers or sourcing partners? The data can also be on existing suppliers who were selected using some environmental criteria. |

| Policy Emissions | PE | Does the company have a policy to reduce emissions? This includes land, air, and water emissions stemming from the company’s core activities- processes, mechanisms, or programs in place to reduce emissions in its operations system or a set of formal, documented processes for controlling emissions and driving sustained improvement. |

| Policy Environmental Supply Chain | PESC | Does the company have a policy to include its supply chain in the company’s efforts to lessen its overall environmental impact? This includes legal compliance data on the supply chain to reduce environmental impact is in scope; data on collaboration with suppliers towards reducing their environmental impacts; and data on reducing environmental impacts of the supplier’s operations. |

| Resource Reduction Policy | RRP | Does the company have a policy for reducing the use of natural resources or lessening the environmental impact of its supply chain? |

| Variable | Definition |

|---|---|

| Company Market Capitalization | The market value of outstanding shares |

| Total Debt Percentage to Total Equity | Percentage of debt over equity |

| ROA | Return on assets |

| Corporation | Percentage of shares held by corporations |

| Individual Investor | Percentage of shares held by individual investors |

| Pension Fund | Percentage of shares held by pension funds |

| Sovereign Wealth Fund | Percentage of shares held by sovereign wealth funds |

| Hedge Fund | Percentage of shares held by hedge funds |

| Insurance Company | Percentage of shares held by insurance companies |

| Investment Advisor | Percentage of shares held by investment advisors |

| Industry dummies | For each industry, there exists a binary variable that takes a value of 1 when the company belongs to the industry according to the NAIC classification. The industries considered are the following: finance and insurance; construction; information; quarrying and oil and gas extraction; professional, scientific, and technical services; real estate and rental and leasing; retail trade; transportation and warehousing; and wholesale and utilities. |

| Random Effects Ordered Logistic Regression | ||

|---|---|---|

| Coef. | p > |z| | |

| Company Market Capitalization | 1.416275 | 0.000 *** |

| ROA | −0.0251847 | 0.000 *** |

| Total Debt Percentage to Total Equity | 0.0000531 | 0.000 *** |

| Finance and Insurance | −4.236074 | 0.000 *** |

| Construction | −1.263819 | 0.004 *** |

| Information | −2.832346 | 0.000 *** |

| Quarrying and Oil and Gas Extraction | −2.302227 | 0.000 *** |

| Professional, Scientific, and Technical Services | −2.589448 | 0.000 *** |

| Real Estate, Rental, and Leasing | −2.442437 | 0.000 *** |

| Retail Trade | −1.593914 | 0.000 *** |

| Transportation and Warehousing | −2.36935 | 0.000 *** |

| Utilities | −0.83461 | 0.019 ** |

| Wholesale | −1.987017 | 0.000 *** |

| Corporation | −0.0067893 | 0.132 |

| Individual Investor | −0.0285433 | 0.000 *** |

| Pension Fund | 0.0052381 | 0.649 |

| Sovereign Wealth Fund | 0.0217324 | 0.031 ** |

| Hedge Fund | −0.0542998 | 0.000 *** |

| Insurance Company | 0.0197999 | 0.149 |

| Investment Advisor | −0.0145407 | 0.001 *** |

| sigma2_u | 17.66762 | |

| Category 0 | Category 1 | Category 2 | Category 3 | Category 4 | Category 5 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coef. | p > |z| | Coef. | p > |z| | Coef. | p > |z| | Coef. | p > |z| | Coef. | p > |z| | Coef. | p > |z| | |

| Company Market Capitalization | −0.0532 | 0.000 *** | −0.01707 | 0.000 *** | −0.02624 | 0.000 *** | −0.00775 | 0.000 *** | −0.00458 | 0.000 *** | 0.10892 | 0.000 *** |

| ROA | 0.00094 | 0.000 *** | 0.00030 | 0.000 *** | 0.00046 | 0.000 *** | 0.00013 | 0.000 *** | 0.00008 | 0.004 *** | −0.00193 | 0.000 *** |

| Total Debt Percentage to Total equity | −2.00 × 10−6 | 0.000 *** | −6.41 × 10−7 | 0.000 *** | −9.84 × 10−7 | 0.000 *** | −2.91 × 10−7 | 0.000 *** | −1.72 × 10−7 | 0.022 ** | 4.09 × 10−6 | 0.000 *** |

| Finance and Insurance | 0.15928 | 0.000 *** | 0.05108 | 0.000 *** | 0.07850 | 0.000 *** | 0.02320 | 0.000 *** | 0.01371 | 0.000 *** | −0.32579 | 0.000 *** |

| Construction | 0.04752 | 0.004 *** | 0.01523 | 0.004 *** | 0.02342 | 0.004 *** | 0.0069 | 0.002 *** | 0.00409 | 0.022 ** | −0.09720 | 0.004 *** |

| Information | 0.10650 | 0.000 *** | 0.03415 | 0.000 *** | 0.05249 | 0.000 *** | 0.01551 | 0.000 *** | 0.00917 | 0.000 *** | −0.21783 | 0.000 *** |

| Quarrying and Oil and Gas Extraction | 0.08656 | 0.000 *** | 0.02776 | 0.000 *** | 0.04266 | 0.000 *** | 0.01261 | 0.000 *** | 0.00745 | 0.001 *** | −0.17706 | 0.000 *** |

| Professional, Scientific, and Technical Services | 0.09736 | 0.000 *** | 0.03122 | 0.000 *** | 0.04799 | 0.000 *** | 0.01418 | 0.000 *** | 0.00838 | 0.001 *** | −0.19915 | 0.000 *** |

| Real Estate, Rental, and Leasing | 0.09184 | 0.000 *** | 0.02945 | 0.000 *** | 0.04526 | 0.000 *** | 0.01338 | 0.000 *** | 0.00790 | 0.001 *** | −0.18784 | 0.000 *** |

| Retail Trade | 0.05993 | 0.000 *** | 0.01922 | 0.000 *** | 0.02954 | 0.000 *** | 0.00873 | 0.000 *** | 0.00516 | 0.006 *** | −0.12258 | 0.000 *** |

| Transportation and Warehousing | 0.08909 | 0.000 *** | 0.02857 | 0.000 *** | 0.04391 | 0.000 *** | 0.01297 | 0.000 *** | 0.00767 | 0.001 *** | −0.18222 | 0.000 *** |

| Utilities | 0.03138 | 0.019 ** | 0.01006 | 0.019 ** | 0.01546 | 0.021 ** | 0.00457 | 0.019 ** | 0.00270 | 0.042 ** | −0.06418 | 0.019 ** |

| Wholesale | 0.07471 | 0.000 *** | 0.02396 | 0.000 *** | 0.03682 | 0.000 *** | 0.01088 | 0.000 *** | 0.00643 | 0.003 *** | −0.15282 | 0.000 *** |

| Corporation | 0.00025 | 0.133 | 0.00008 | 0.133 | 0.00012 | 0.134 | 0.00003 | 0.138 | 0.00002 | 0.147 | −0.00052 | 0.133 |

| Individual Investor | 0.00107 | 0.000 *** | 0.00034 | 0.000 *** | 0.00052 | 0.000 *** | 0.00015 | 0.000 *** | 0.00009 | 0.002 *** | −0.00219 | 0.000 *** |

| Pension Fund | −0.0001 | 0.649 | −0.00006 | 0.650 | −0.00009 | 0.650 | −0.00002 | 0.649 | −0.00001 | 0.652 | 0.00040 | 0.649 |

| Sovereign Wealth Fund | −0.0008 | 0.031 ** | −0.00026 | 0.033 ** | −0.00040 | 0.032 ** | −0.00011 | 0.032 ** | −0.00007 | 0.054 * | 0.00167 | 0.031 ** |

| Hedge Fund | 0.00204 | 0.000 *** | 0.00065 | 0.000 *** | 0.00100 | 0.000 *** | 0.00029 | 0.000 *** | 0.00017 | 0.004 *** | −0.00417 | 0.000 *** |

| Insurance Company | −0.0007 | 0.149 | −0.00023 | 0.151 | −0.00036 | 0.150 | −0.00010 | 0.148 | −0.00006 | 0.176 | 0.00152 | 0.149 |

| Investment Advisor | 0.00054 | 0.001 *** | 0.00017 | 0.001 *** | 0.00026 | 0.001 *** | 0.00007 | 0.001 *** | 0.00004 | 0.008 *** | −0.00111 | 0.001 *** |

| Predicted outcomes | Pr (ESCI == 0) (predict, outcome(0)) | Pr (ESCI == 1) (predict, outcome(1)) | Pr (ESCI == 2) (predict, outcome(2)) | Pr (ESCI == 3) (predict, outcome(3)) | Pr (ESCI == 4) (predict, outcome(4)) | Pr (ESCI == 5) (predict, outcome(5)) | ||||||

| 0.1165331 | 0.0583815 | 0.1334956 | 0.0628442 | 0.1968036 | 0.4319419 | |||||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rivera, L.; Ortiz, N.; Moreno, G.; Páez-Gabriunas, I. The Effect of Company Ownership on the Environmental Practices in the Supply Chain: An Empirical Approach. Sustainability 2023, 15, 12450. https://doi.org/10.3390/su151612450

Rivera L, Ortiz N, Moreno G, Páez-Gabriunas I. The Effect of Company Ownership on the Environmental Practices in the Supply Chain: An Empirical Approach. Sustainability. 2023; 15(16):12450. https://doi.org/10.3390/su151612450

Chicago/Turabian StyleRivera, Liliana, Norma Ortiz, Gabriel Moreno, and Iliana Páez-Gabriunas. 2023. "The Effect of Company Ownership on the Environmental Practices in the Supply Chain: An Empirical Approach" Sustainability 15, no. 16: 12450. https://doi.org/10.3390/su151612450