Low-Carbon Manufacturing or Not? Equilibrium Decisions for Capital-Constrained News Vendors with Subsidy and Carbon Tax

Abstract

:1. Introduction

2. Literature Review

2.1. Low-Carbon Supply Chains

2.2. Capital-Constrained Supply Chain

2.3. Governmental Low-Carbon Policy

3. Model Description

3.1. Model Framework

3.2. Demand Setting

3.3. Sequence of the Event

4. Model Analysis

4.1. Equilibrium Decisions

4.2. Price and Quantity Comparison

- (i)

- (), ();

- (ii)

- (), ( and ).

- (i)

- always holds for ;

- (ii)

- for and for .

4.3. Profit Comparison

- (i)

- When , then always holds; therefore, for and for .

- (ii)

- When or and , then holds; therefore, for and otherwise.

- (iii)

- When or and , then holds; therefore, always holds.

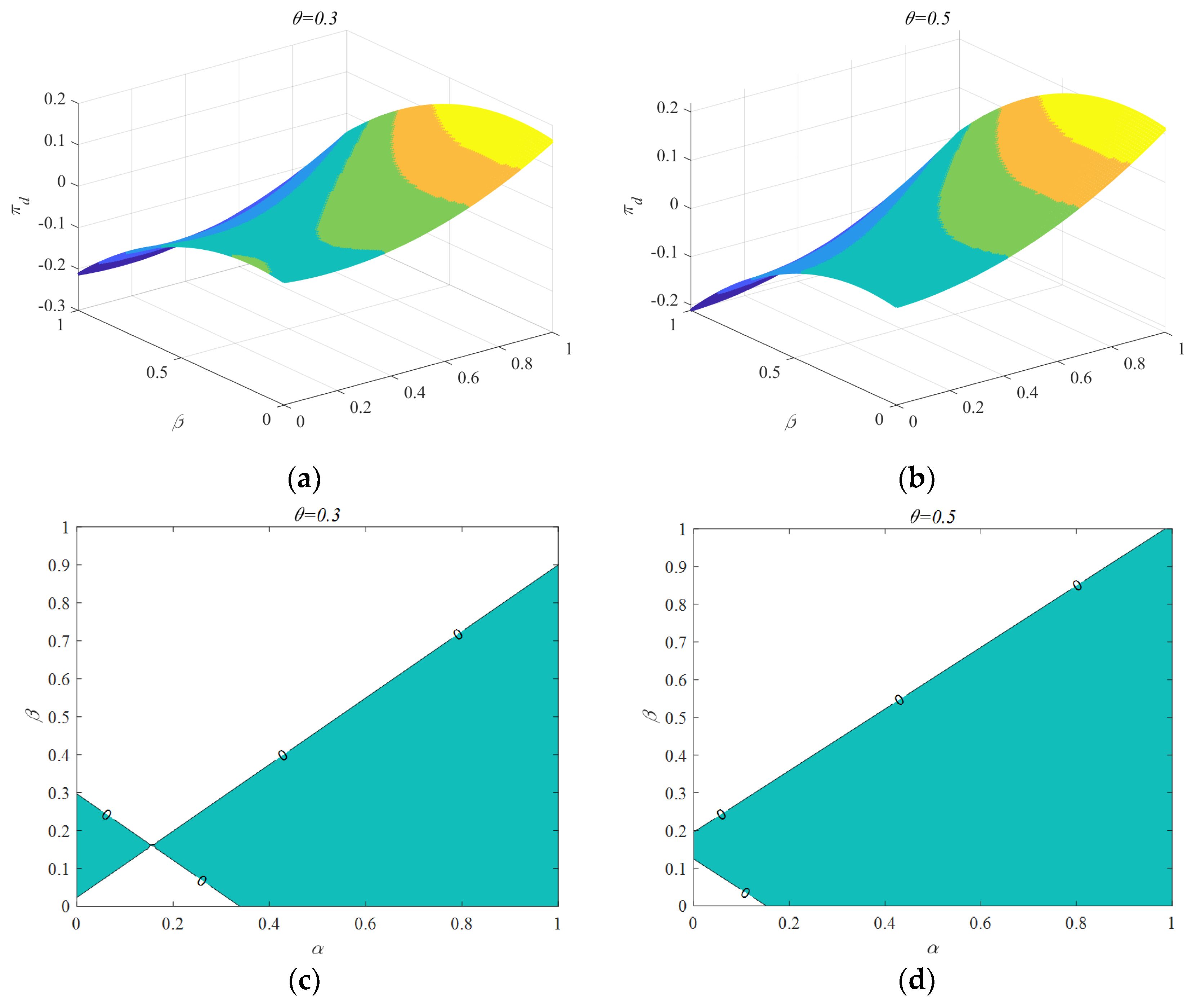

4.4. Social Welfare

5. Sensitivity Analysis

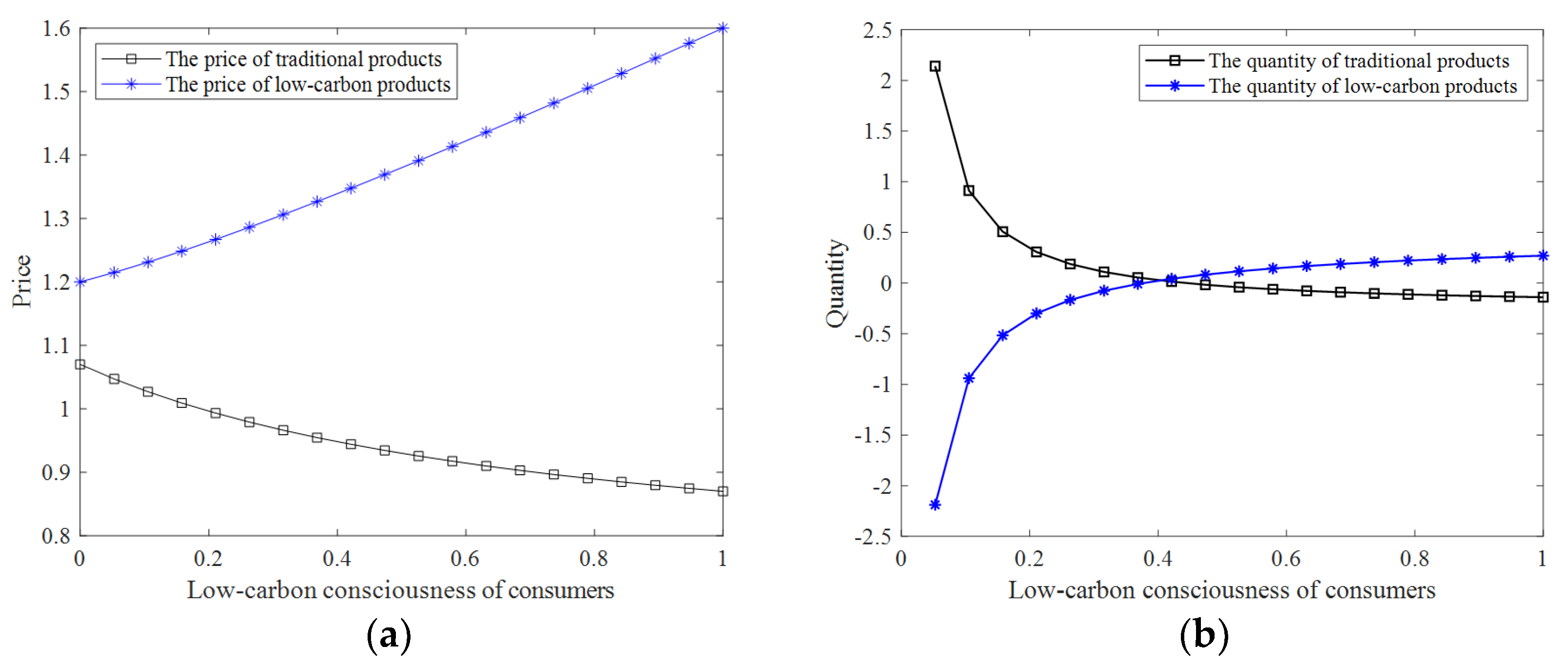

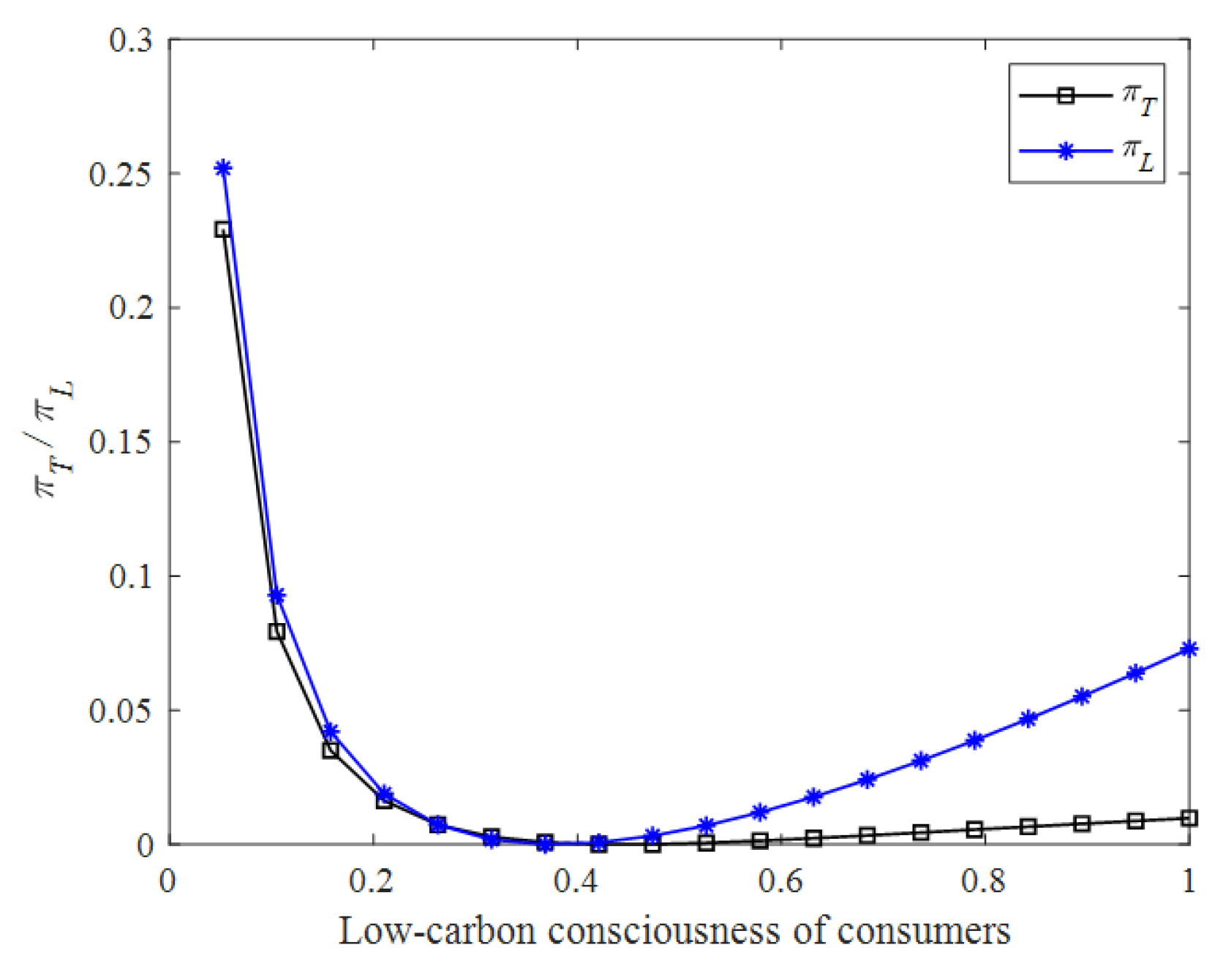

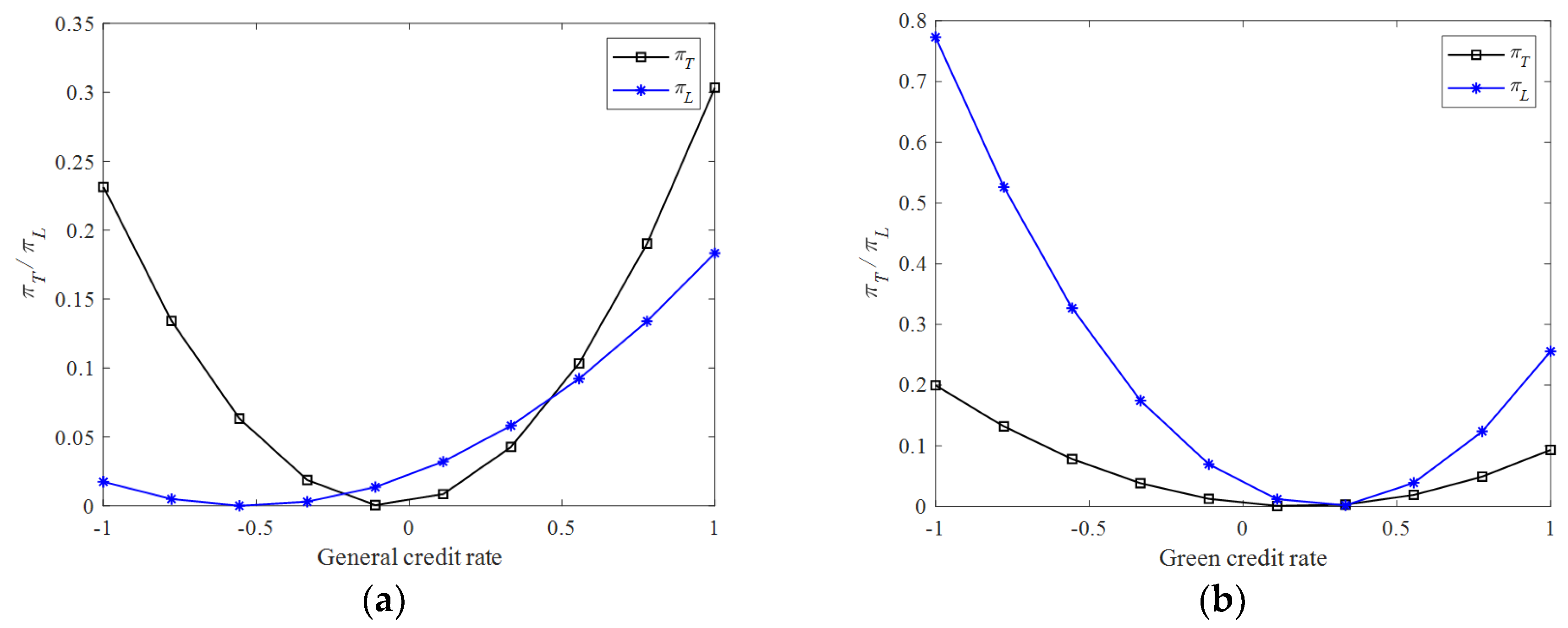

5.1. Effects of Low-Carbon Awareness

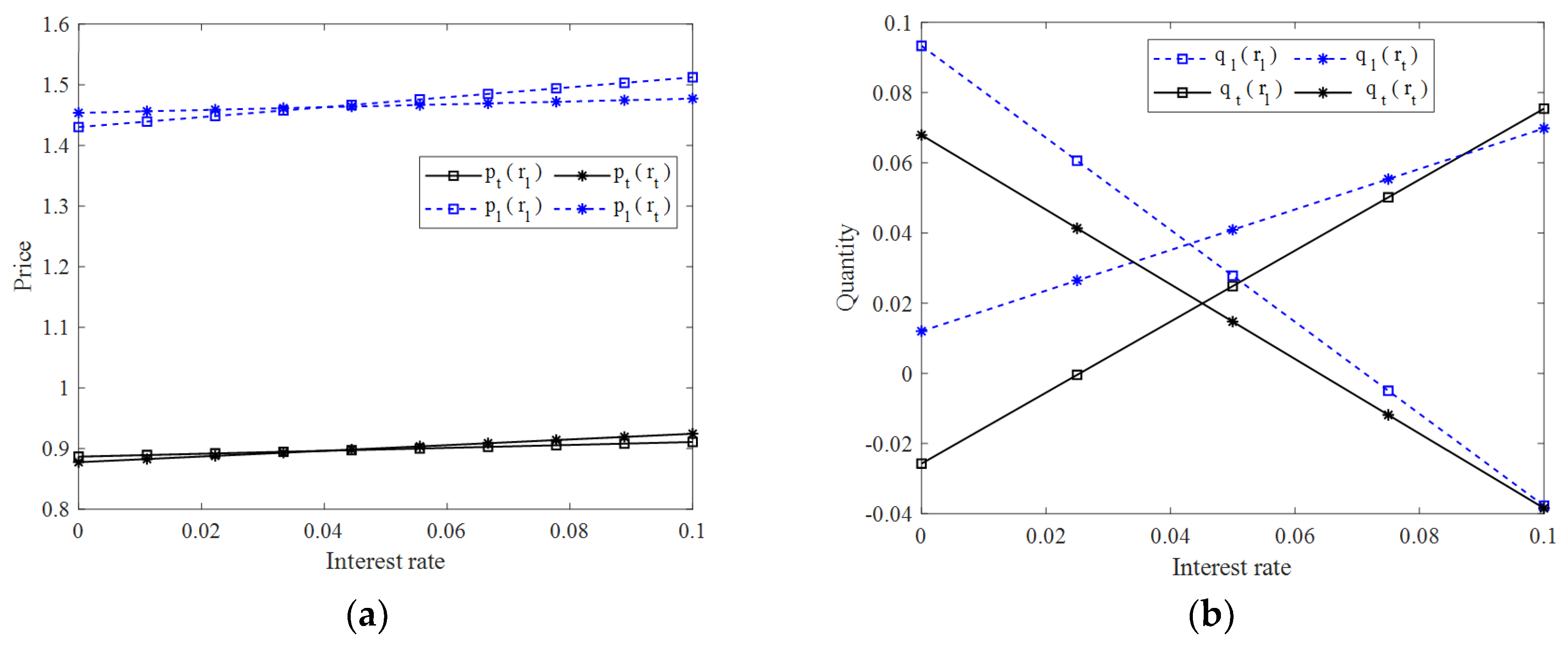

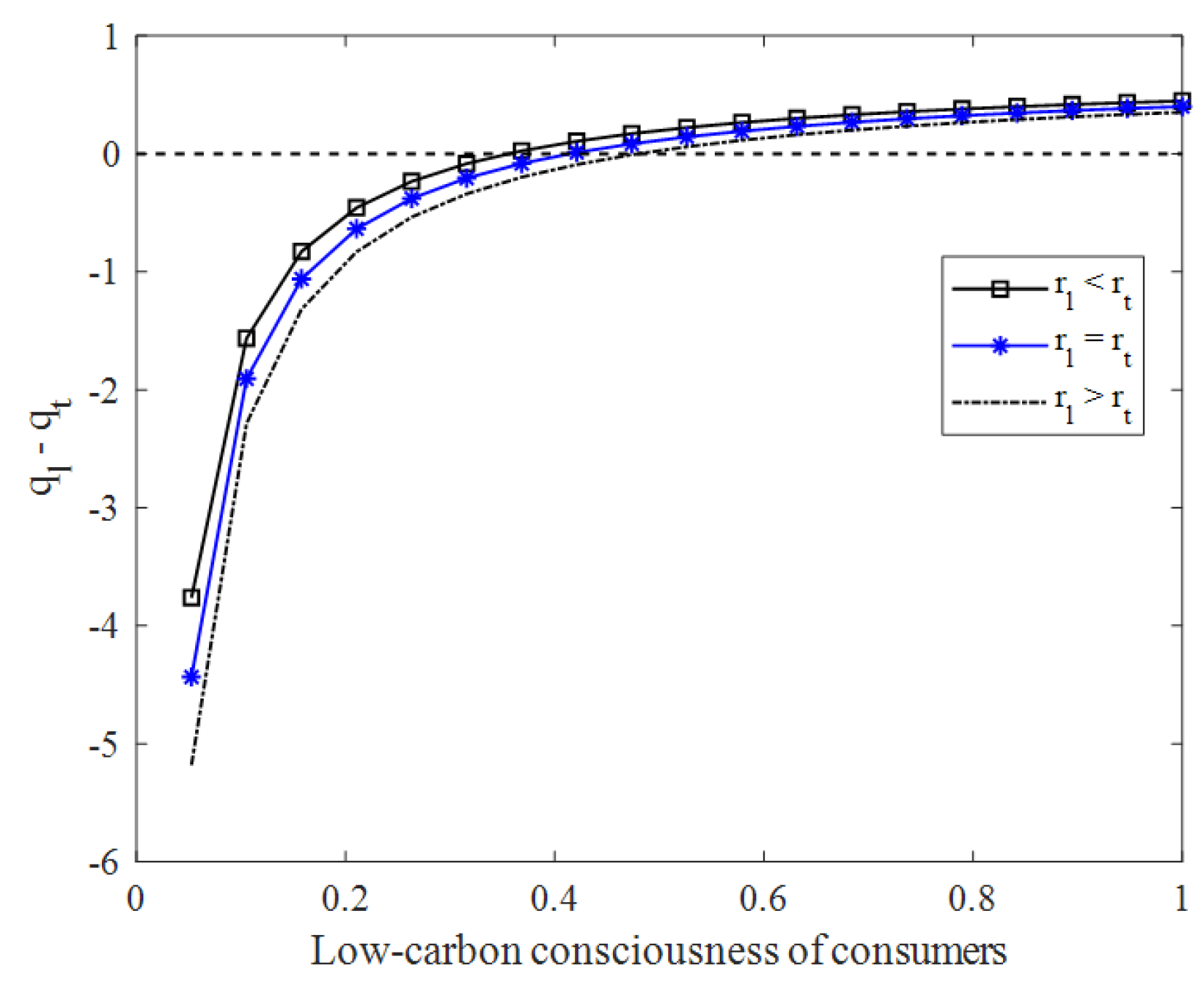

5.2. Effects of Financing Interest Rate

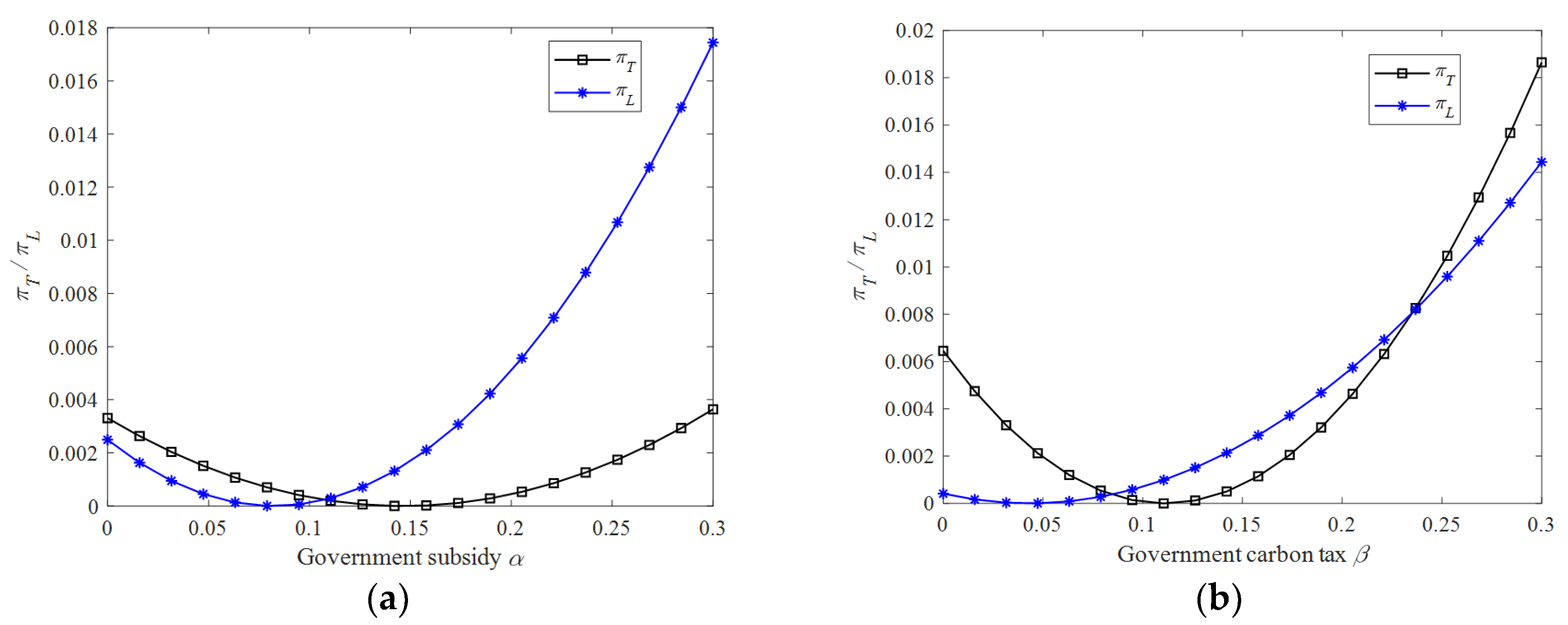

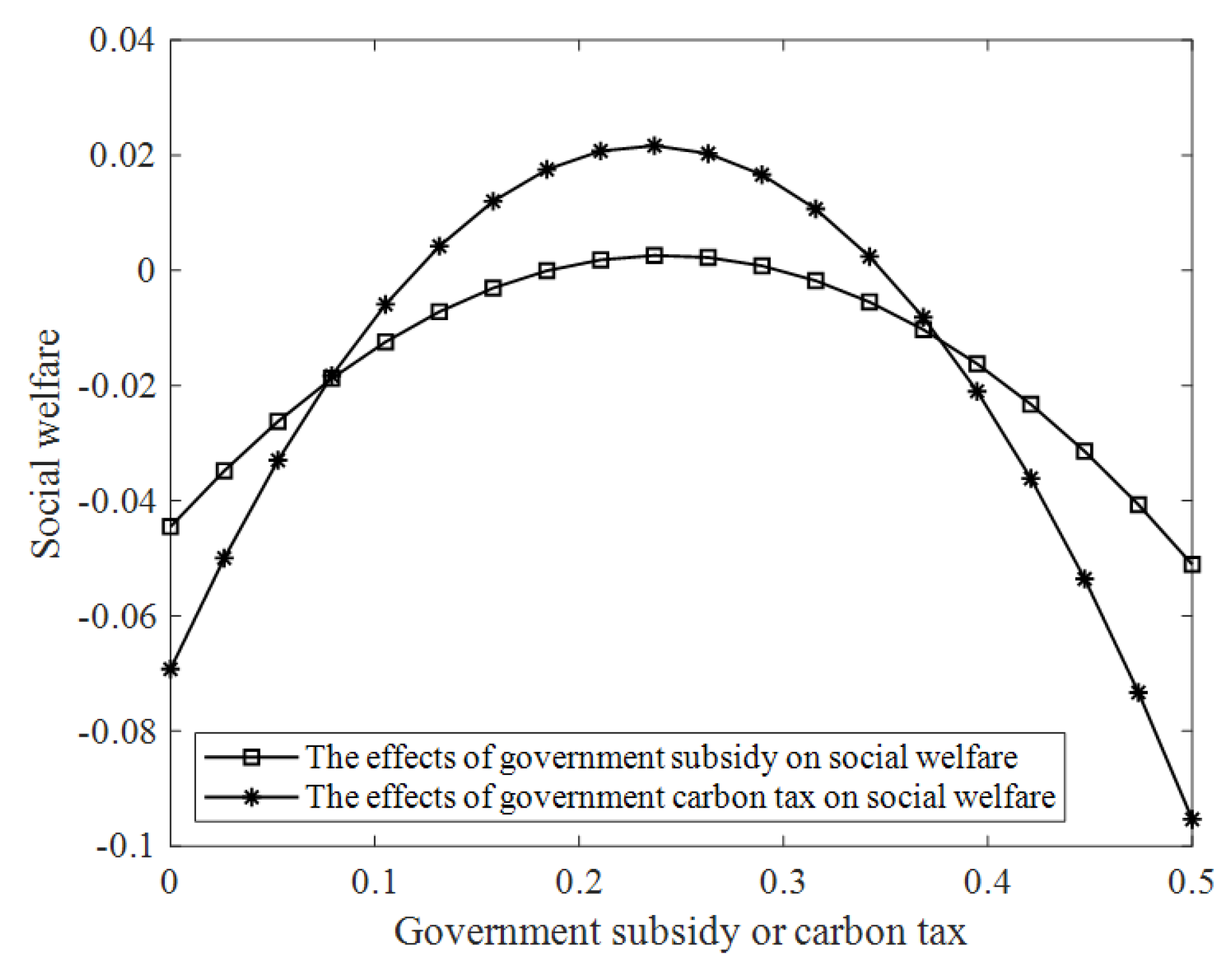

5.3. Effects of the Government Subsidy α and Carbon Tax β

6. Conclusions

6.1. Discussion and Conclusions

6.2. Research Limitation and Future Work

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

- Proof of Proposition 1.

- Proof of Proposition 2.

- (i)

- For , the expression of always holds. The expression of holds for .

- (ii)

- For , the expressions of and always hold.

- (iii)

- For , the expression of holds. The expression of holds for .

- Proof of Proposition 3.

- Proof of Proposition 4.

- Proof of Proposition 5.

- (i)

- When , then always holds. Therefore, for and for .

- (ii)

- When or and , then holds. Therefore, for and otherwise.

- (iii)

- When or and , then holds and always holds.

- Proof of Lemma 1.

References

- Mao, Y.; Wang, J. Is Green Manufacturing Expensive? Empirical Evidence from China. Int. J. Prod. Res. 2019, 57, 7235–7247. [Google Scholar] [CrossRef]

- Aoki, K.; Akai, K. Do Consumers Select Food Products Based on Carbon Dioxide Emissions? In Advances in Production Management Systems. Competitive Manufacturing for Innovative Products and Services: IFIP WG 5.7 International Conference, APMS 2012, Rhodes, Greece, September 24–26, 2012, Revised Selected Papers, Part II; Emmanouilidis, C., Taisch, M., Kiritsis, D., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 345–352. Available online: http://link.springer.com/10.1007/978-3-642-40361-3_44 (accessed on 3 July 2023).

- Benkhodja, M.T.; Ma, X.; Razafindrabe, T. Green Monetary and Fiscal Policies: The Role of Consumer Preferences. Resour. Energy Econ. 2023, 73, 101370. [Google Scholar] [CrossRef]

- Ricky, Y.K.C.; Lau, L.B.Y. Explaining Green Purchasing Behavior. J. Int. Consum. Mark. 2002, 14, 9–40. [Google Scholar]

- Hines, J.M.; Hungerford, H.R.; Tomera, A.N. Analysis and Synthesis of Research on Responsible Environmental Behavior: A Meta-Analysis. J. Environ. Educ. 1987, 18, 1–8. [Google Scholar] [CrossRef]

- Meng, X.; Yao, Z.; Nie, J.; Zhao, Y.; Li, Z. Low-Carbon Product Selection with Carbon Tax and Competition: Effects of the Power Structure. Int. J. Prod. Econ. 2018, 200, 224–230. [Google Scholar] [CrossRef]

- Deng, Z.; Lv, L.; Huang, W.; Wan, L.; Li, S. Modelling of Carbon Utilisation Efficiency and Its Application in Milling Parameters Optimisation. Int. J. Prod. Res. 2020, 58, 2406–2420. [Google Scholar] [CrossRef]

- Wang, Y.; Yu, Z.; Jin, M.; Mao, J. Decisions and Coordination of Retailer-Led Low-Carbon Supply Chain under Altruistic Preference. Eur. J. Oper. Res. 2021, 293, 910–925. [Google Scholar] [CrossRef]

- Lin, J.; Fan, R.; Tan, X.; Zhu, K. Dynamic Decision and Coordination in a Low-Carbon Supply Chain Considering the Retailer’s Social Preference. Socio-Econ. Plan. Sci. 2021, 77, 101010. [Google Scholar] [CrossRef]

- Heydari, J.; Govindan, K.; Basiri, Z. Balancing Price and Green Quality in Presence of Consumer Environmental Awareness: A Green Supply Chain Coordination Approach. Int. J. Prod. Res. 2021, 59, 1957–1975. [Google Scholar] [CrossRef]

- Zhang, Q.; Zhao, Q.; Zhao, X. Manufacturer’s Product Choice in the Presence of Environment-Conscious Consumers: Brown Product or Green Product. Int. J. Prod. Res. 2019, 57, 7423–7438. [Google Scholar] [CrossRef]

- Gao, F.; Souza, G.C. Carbon Offsetting with Eco-Conscious Consumers. Manag. Sci. 2022, 68, 7879–7897. [Google Scholar] [CrossRef]

- Wang, Z.; Wu, Q. Carbon Emission Reduction and Product Collection Decisions in the Closed-Loop Supply Chain with Cap-and-Trade Regulation. Int. J. Prod. Res. 2021, 59, 4359–4383. [Google Scholar] [CrossRef]

- Ji, T.; Xu, X.; Yan, X.; Yu, Y. The Production Decisions and Cap Setting with Wholesale Price and Revenue Sharing Contracts under Cap-and-Trade Regulation. Int. J. Prod. Res. 2020, 58, 128–147. [Google Scholar] [CrossRef]

- Liu, J.; Ke, H. Firms’ Preferences for Retailing Formats Considering One Manufacturer’s Emission Reduction Investment. Int. J. Prod. Res. 2021, 59, 3062–3083. [Google Scholar] [CrossRef]

- Huang, S.; Fan, Z.P.; Wang, N. Green Subsidy Modes and Pricing Strategy in a Capital-Constrained Supply Chain. Transp. Res. Part E Logist. Transp. Rev. 2020, 136, 101885. [Google Scholar] [CrossRef]

- Jing, B.; Chen, X.; Cai, G. Equilibrium Financing in a Distribution Channel with Capital Constraint. Prod. Oper. Manag. 2012, 21, 1090–1101. [Google Scholar] [CrossRef]

- Kouvelis, P.; Zhao, W. Supply Chain Contract Design Under Financial Constraints and Bankruptcy Costs. Manag. Sci. 2016, 62, 2341–2357. [Google Scholar] [CrossRef]

- Whitmore, G.A.; Darkazanli, S. A Linear Risk Constraint in Capital Budgeting. Manag. Sci. 1971, 18, B-155. [Google Scholar] [CrossRef]

- Xu, S.; Fang, L. Partial Credit Guarantee and Trade Credit in an Emission-Dependent Supply Chain with Capital Constraint. Transp. Res. Part E Logist. Transp. Rev. 2020, 135, 101859. [Google Scholar] [CrossRef]

- Wang, Y.; Lv, L.; Shen, L.; Tang, R. Manufacturer’s Decision-Making Model under Carbon Emission Permits Repurchase Strategy and Capital Constraints. Int. J. Prod. Res. 2021, 1–19. [Google Scholar] [CrossRef]

- Cao, E.; Du, L.; Ruan, J. Financing Preferences and Performance for an Emission-Dependent Supply Chain: Supplier vs. Bank. Int. J. Prod. Econ. 2019, 208, 383–399. [Google Scholar] [CrossRef]

- Cao, E.; Yu, M. The Bright Side of Carbon Emission Permits on Supply Chain Financing and Performance. Omega 2019, 88, 24–39. [Google Scholar] [CrossRef]

- Cai, G.; Chen, X.; Xiao, Z. The Roles of Bank and Trade Credits: Theoretical Analysis and Empirical Evidence. Prod. Oper. Manag. 2014, 23, 583–598. [Google Scholar] [CrossRef]

- Deng, S.; Gu, C.; Cai, G.; Li, Y. Financing Multiple Heterogeneous Suppliers in Assembly Systems: Buyer Finance vs. Bank Finance. Manuf. Serv. Oper. Manag. 2018, 20, 53–69. [Google Scholar] [CrossRef]

- Gupta, D.; Chen, Y. Retailer-Direct Financing Contracts Under Consignment. Manuf. Serv. Oper. Manag. 2020, 22, 528–544. [Google Scholar] [CrossRef]

- Kouvelis, P.; Zhao, W. Financing the Newsvendor: Supplier vs. Bank, and the Structure of Optimal Trade Credit Contracts. Oper. Res. 2012, 60, 566–580. [Google Scholar] [CrossRef]

- Kouvelis, P.; Zhao, W. Who Should Finance the Supply Chain? Impact of Credit Ratings on Supply Chain Decisions. Manuf. Serv. Oper. Manag. 2018, 20, 19–35. [Google Scholar] [CrossRef]

- Zhang, Z.C.; Xu, H.Y.; Chen, K.B. Operational Decisions and Financing Strategies in a Capital-Constrained Closed-Loop Supply Chain. Int. J. Prod. Res. 2021, 59, 4690–4710. [Google Scholar] [CrossRef]

- Xia, T.; Wang, Y.; Lv, L.; Shen, L.; Cheng, T.C.E. Financing Decisions of Low-Carbon Supply Chain under Chain-to-Chain Competition. Int. J. Prod. Res. 2022, 61, 6153–6176. [Google Scholar] [CrossRef]

- Cong, J.; Pang, T.; Peng, H. Optimal Strategies for Capital Constrained Low-Carbon Supply Chains under Yield Uncertainty. J. Clean. Prod. 2020, 256, 120339. [Google Scholar] [CrossRef]

- Qin, J.; Han, Y.; Wei, G.; Xia, L. The Value of Advance Payment Financing to Carbon Emission Reduction and Production in a Supply Chain with Game Theory Analysis. Int. J. Prod. Res. 2020, 58, 200–219. [Google Scholar] [CrossRef]

- Shao, L.; Yang, J.; Zhang, M. Subsidy Scheme or Price Discount Scheme? Mass Adoption of Electric Vehicles under Different Market Structures. Eur. J. Oper. Res. 2017, 262, 1181–1195. [Google Scholar] [CrossRef]

- Bao, B.; Ma, J.; Goh, M. Short-and Long-Term Repeated Game Behaviours of Two Parallel Supply Chains Based on Government Subsidy in the Vehicle Market. Int. J. Prod. Res. 2020, 58, 7507–7530. [Google Scholar] [CrossRef]

- Bai, J.; Hu, S.; Gui, L.; So, K.C.; Ma, Z.J. Optimal Subsidy Schemes and Budget Allocations for Government-Subsidized Trade-in Programs. Prod. Oper. Manag. 2021, 30, 2689–2706. [Google Scholar] [CrossRef]

- Luo, R.; Zhou, L.; Song, Y.; Fan, T. Evaluating the Impact of Carbon Tax Policy on Manufacturing and Remanufacturing Decisions in a Closed-Loop Supply Chain. Int. J. Prod. Econ. 2022, 245, 108408. [Google Scholar] [CrossRef]

- Bai, Q.; Xu, J.; Chauhan, S.S. Effects of Sustainability Investment and Risk Aversion on a Two-Stage Supply Chain Coordination under a Carbon Tax Policy. Comput. Ind. Eng. 2020, 142, 106324. [Google Scholar] [CrossRef]

- Sun, H.; Yang, J. Optimal Decisions for Competitive Manufacturers under Carbon Tax and Cap-and-Trade Policies. Comput. Ind. Eng. 2021, 156, 107244. [Google Scholar] [CrossRef]

- Fan, X.; Chen, K.; Chen, Y.J. Is Price Commitment a Better Solution to Control Carbon Emissions and Promote Technology Investment? Manag. Sci. 2023, 69, 325–341. [Google Scholar] [CrossRef]

- Xia, X.; Xu, C. A Comparative Study on the Impact of Government Carbon Tax and Subsidy Policies on Low-Carbon Supply Chains. Oper. Res. Manag. 2020, 29, 112–120. [Google Scholar]

- Bian, J.; Zhao, X. Tax or Subsidy? An Analysis of Environmental Policies in Supply Chains with Retail Competition. Eur. J. Oper. Res. 2020, 283, 901–914. [Google Scholar] [CrossRef]

- Moorthy, K.S. Product and Price Competition in a Duopoly. Mark. Sci. 1988, 7, 141–168. [Google Scholar] [CrossRef] [Green Version]

- Sun, C.; Zhang, X.; Zhou, Y.W.; Cao, B. Pricing, Financing and Channel Structure for Capital-Constrained Dual-Channel Supply Chains with Product Heterogeneity. Int. J. Prod. Econ. 2022, 253, 108591. [Google Scholar] [CrossRef]

- Wu, C.; Li, K.; Shi, T. Supply Chain Coordination with Two-Part Tariffs under Information Asymmetry. Int. J. Prod. Res. 2017, 55, 2575–2589. [Google Scholar] [CrossRef] [Green Version]

- Xu, L.; Wang, C.; Zhao, J. Decision and Coordination in the Dual-Channel Supply Chain Considering Cap-and-Trade Regulation. J. Clean. Prod. 2018, 197, 551–561. [Google Scholar] [CrossRef]

- Yang, H.; Miao, L.; Zhao, C. The Credit Strategy of a Green Supply Chain Based on Capital Constraints. J. Clean. Prod. 2019, 224, 930–939. [Google Scholar] [CrossRef]

- Zhou, Y.; Hu, F.; Zhou, Z. Pricing Decisions and Social Welfare in a Supply Chain with Multiple Competing Retailers and Carbon Tax Policy. J. Clean. Prod. 2018, 190, 752–777. [Google Scholar] [CrossRef]

- Pal, R.; Saha, B. Pollution Tax, Partial Privatization and Environment. Resour. Energy Econ. 2015, 40, 19–35. [Google Scholar] [CrossRef] [Green Version]

- Circular of the Ministry of Finance and the State Administration of Taxation on the Implementation of Coal Resource Tax Reform. Available online: http://www.chinatax.gov.cn/chinatax/n364/c481369/content.html (accessed on 7 July 2023).

- Interpretation of the Circular of the Ministry of Finance, the Ministry of Industry and Information Technology, the Ministry of Science and Technology and the Development and Reform Commission on Further Improving the Financial Subsidy Policy for the Promotion and Application of New Energy Vehicles_Policy Interpretation_Chinese Government Website. Available online: https://www.gov.cn/zhengce/2020-12/31/content_5575908.htm (accessed on 7 July 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Paper | Capital Constraints | Financing Method | Carbon Subsidy Policy | Carbon Tax Policy | Carbon Cap-and-Trade | Research Methodology | |

|---|---|---|---|---|---|---|---|

| Research Theory | Specific Modelling | ||||||

| [21] | ✔ | Carbon Emission Permits Repurchase Strategy (CEPRS) | ✔ | Game theory | Stackelberg game | ||

| [30] | ✔ | bank financing and internal financing | ✔ | Game theory | Stackelberg game, Nash game | ||

| [31] | ✔ | green credit financing | ✔ | Game theory | Stackelberg game | ||

| [32] | ✔ | supplier, platform or hybrid financing models | ✔ | Planning theory | Stochastic Programming | ||

| [38] | ✔ | ✔ | Game theory | Stackelberg game, Nash game | |||

| [39] | ✔ | ✔ | Decision theory | Two-stage optimization | |||

| [40] | ✔ | ✔ | Game theory | Nash game | |||

| This paper | ✔ | general and green bank credit financing | ✔ | ✔ | Game theory | Stackelberg game | |

| + | − | − | |

| + | + | − |

| − | + | + | + | ||

| − | − | + | − | ||

| − | − | + | − | ||

| − | + | + | + | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zheng, Y.; Zhang, J.; Wang, M.; Liu, P.; Shu, T. Low-Carbon Manufacturing or Not? Equilibrium Decisions for Capital-Constrained News Vendors with Subsidy and Carbon Tax. Sustainability 2023, 15, 11779. https://doi.org/10.3390/su151511779

Zheng Y, Zhang J, Wang M, Liu P, Shu T. Low-Carbon Manufacturing or Not? Equilibrium Decisions for Capital-Constrained News Vendors with Subsidy and Carbon Tax. Sustainability. 2023; 15(15):11779. https://doi.org/10.3390/su151511779

Chicago/Turabian StyleZheng, Yanyan, Jin Zhang, Mengyuan Wang, Peng Liu, and Tong Shu. 2023. "Low-Carbon Manufacturing or Not? Equilibrium Decisions for Capital-Constrained News Vendors with Subsidy and Carbon Tax" Sustainability 15, no. 15: 11779. https://doi.org/10.3390/su151511779