1. Introduction

Cross-listing has become a widespread and prevalent strategy with the liberalization of global trade, especially for larger firms focusing on international exposure [

1]. The cross-listing of shares (CLS) refers to listing local shares in the foreign market to access low-price capital for future growth. For instance, the Security and Exchange Commission (SEC) of the U.S. allows foreign companies to raise money in U.S. financial markets under the Level 3 American Depository Receipts (ADR) program (SEC [

2]). More than 2400 non-US firms have been registered on the New York Stock Exchange (NYSE) worldwide [

3]. The motives behind such an increasing trend of CLS are to enhance the shareholder base and information quality as proposed by market segmentation theory and signaling theory, respectively [

4,

5].

Kamarudin et al. [

6] also identified the benefits of cross-listing, such as growing visibility, increasing shareholders’ base, access to the financial markets, improved relationships with the overseas financial community, and increasing demand for shares. CLS is also vital for international investors in diversifying their investment portfolios globally [

7]. Similarly, CLS plays an essential role in developing the home and foreign financial markets [

8].

Various studies have explored the different aspects of cross-listing and narrated the significance of CLS. Dodd [

9] emphasized that the cross-listing of stocks attracts attention due to the decentralization of international capital flows and the internationalization of company shares in the foreign exchange market in the 1980s. Yang and Lai [

10] investigated the impact of cross-listing on the association of Research & Development investment and financial leverage. They found that the advent of cross-listing has significantly increased the firm’s level of financial leverage, leading to an increase in investment in R&D. These findings demonstrate that companies have taken advantage of the rise of cross-listing internationally to enhance their borrowing capacity and further support R&D, which also encourages an intra-industry contagion effect and a possible route to achieve corporate sustainability.

Batra et al. [

11] conducted a detailed bibliometric analysis of cross-listing regarding intellectual structure and revealed the publication trends, journals, and institutions in cross-listing and found that authors from the USA and Canada collaborate well in this area. They pointed out that the existing studies are not sufficient and that more investigations concerning corporate sustainability are needed.

Atuna and Adusei [

12] studied the determinants of the cross-listing of shares in Sub-Saharan Africa (SSA) and identified geography as the key determinant for cross-listing. They also found that business strategy has a vital impact on the cross-listing of shares. Market liquidity is also affected by the cross-listing of shares. This shows that cross-listing is conducted to achieve several objectives and that there are many factors that affect cross-listing decisions.

Chen et al. [

13] found that cross-listing improves corporate governance and results in less tax avoidance, even in the countries with weaker shareholder protection and disclosure requirements. They also found that cross-listing also helps in reducing agency problems in the firms. This shows that the cross-listing of shares results in reducing market deviations and an improved sustainable governance model for the firms.

Oh et al. [

14] examined the impact of cross-listing on firm value through the changes in the composition of corporate boards due to the inclusion of independent directors. They found that cross-listing helps the firms to recruit high-quality foreign independent directors, which subsequently has a positive impact on firm value and rewards the firms with cross-listing premiums. Thus cross-listing improves the sustainability of firms by increasing firm value, encouraging sale growth, and aiding in creating a positive image in the market.

American Depository Receipts (ADRs) and the cross-listing of shares are two mechanisms that can help firms improve their sustainable performance by increasing their access to global capital markets, enhancing transparency and accountability, and increasing their exposure to responsible investors.

Access to Global Capital Markets: Cross-listing and ADRs can help firms expand their investor base and access new sources of capital from around the world. This increased access to capital can allow firms to fund new sustainable initiatives and projects, which can help improve their environmental, social, and governance (ESG) performance.

Enhanced Transparency and Accountability: Firms that cross-list their shares or issue ADRs must comply with the listing rules and disclosure requirements of multiple stock exchanges, which can enhance their transparency and accountability. Increased transparency can help firms build trust with investors and stakeholders, which can lead to better performance based on the environment, sustainability, and governance (ESG) criteria.

Exposure to Responsible Investors: Firms that cross-list their shares or issue ADRs may attract a larger number of responsible investors who prioritize ESG factors in their investment decisions. These investors can help improve a firm’s ESG performance by exerting pressure on the company to improve its sustainability practices.

Exposure to Different Sustainability Standards: Companies that cross-list their shares may be subject to different sustainability standards than they are in their home market. This can expose firms to new ideas and best practices in sustainability and encourage them to adopt more sustainable practices.

Enhanced Reputation: ADRs and the cross-listing of shares can enhance a company’s reputation by demonstrating a commitment to transparency, accountability, and sustainability. This can help attract socially responsible investors who are interested in supporting companies that prioritize sustainability.

Overall, ADRs and the cross-listing of shares can provide firms with valuable opportunities to enhance their ESG performance by expanding their access to capital, improving transparency and accountability, and increasing exposure to responsible investors. A study by Esqueda [

15] found that most firms experience a continuous increase in their value when cross-listed on the U.S. exchange following the implementation of the Sarbanes–Oxley Act in 2002. Firms experienced value growth in the year of cross-listing and typically experience a decline in the post-cross-listing year. Insider-owned firms experience more value growth in their shares than non-insider-owned firms. Visibility and liquidity also increase the value of cross-listing. Perhaps this is why more articles are being published on CLS, particularly in the last two decades.

However, the emerging literature regarding CLS needs to be synthesized to provide a comprehensive view to the practitioners and policymakers to help better inform their decisions and policies. These significant focus points stimulate the researchers to investigate CLS from different perspectives to make policy implications for multinationals, global investors, and the regulators of financial markets. Thus, a systemic and synthesized review of the CLS-based literature is also needed to comprehend its thematic structure and suggest advancements in this budding field of research.

The Research Objective and Questions

The main objective of this study is to systematically explore the main themes embedded in the state-of-the-art research on CLS while responding to the research questions posited in this study. As such, this study aims to answer the following research questions:

RQ1. What is the descriptive bibliometric information available in the publications in the CLS research domain?

RQ2. What are the major themes and practical dimensions emerging from the CLS-based literature?

RQ3. What are the current trends in CLS publications in terms of time, authors, disciplines, journals, institutions, affiliated countries, the study type, and economy?

RQ4. How can we understand the intellectual structure of CLS research and its evolution over multiple years?

RQ5. What are feasible suggestions or future agendas based on the significant research gaps found in the context of research conducted on CLS so far?

The current study identified 315 research articles about CLS that have been published since 1988 in journals from the Web of Science. The present study intends to fill research gaps and better understand the CLS-based literature using bibliometric analysis. Notably, this study explores the influential aspects (i.e., top studies, authors, institutions, and countries) and hidden themes of the CLS-based literature using science mapping (a tool of bibliometric analysis) based on intellectual structure and conceptual structure. Science mapping is a quantitative and systematic approach to exploring a literature review’s hidden themes [

16]. Intellectual and conceptual structure are two frequently used methods to segregate similar articles based on citations and textual analysis [

17,

18]. This research combines intellectual structure and conceptual structure to segregate the CLS-based literature into similar clusters. Such thematic information will help the practitioners and policymakers to understand the width and depth of this field of research. This research also explores desirable future research agendas by including information regarding clustering and the influential aspects mentioned above. Therefore, the outcome of this research is vital for practitioners, policymakers, and researchers. The objectives of the present study are four-fold. Firstly, we aim to explore the current trends in the CLS-based literature in terms of time, authors, disciplines, journals, institutions, affiliated countries, the study type, and economy. Secondly, we intend to determine the major research trends and themes in the domain of CLS research. Thirdly, we aim to understand the intellectual structure of CLS research and its evolution over the course of the past few years. Lastly, we attempt to suggest significant research gaps for future agendas. The remainder of this paper is arranged as follows:

Section 2 describes the methods used;

Section 3 reports the findings and results of the study;

Section 4 discusses the future research agenda; and

Section 5 presents the study’s conclusions.

2. Methods

Zainuldin and Lui [

19] stated that reviewing the existing literature is a common method used to explore concepts from earlier works and convert them into objective and systematic forms to define, specify, map, and assess the contents; however, the intellectual structure of any domain cannot be extracted using conventional review procedures. A traditional approach, such a systematic literature review (SLR), resolves this problem. Jain et al. [

20] have stated that SLR is considered a well-defined technique for scanning various databases using a preset search strategy to improve the research quality by making it more transparent, scientific, and thorough. Under SLR, the bibliometric method involves a quantitative analysis of the contents. For assessing scientific output, newer methodologies have gained acceptance [

21].

Khatib et al. [

22] stated that the bibliometric method is a systematic process that describes published work in terms of top journals, authors from different nations, etc., and is specific to a research area. Scholarly work can be quickly and simply evaluated using a comprehensive approach with the aid of bibliometric analysis. Bibliometric analysis is made up of two key tools: performance analysis and science mapping [

20,

21]. The current study deploys the five-step science mapping clustering approach to identify the themes of the CLS-based literature, as shown in

Figure 1 and proposed by Zupic and Čater [

23].

Science mapping is a quantitative tool of bibliometric analysis that identifies the hidden themes and topics in a literature review [

16]. Since it is a systematic, objective, and quantitative approach that uses classification algorithms and visualization to find an analog of clusters, it provides less biased and rigorous outcomes than narrative literature reviews [

23]. Batra et al. [

11] used the step-by-step process, in which around 600 articles from the Scopus database were identified. To understand the current research environment and identify potential future research orientations regarding CLS, bibliographic coupling and a keyword analysis were used. R Studio and VOS viewer were also employed to analyze and display the data. The current study deploys the five-step science mapping clustering approach to identify themes in the CLS-based literature, as shown in

Figure 1 and proposed by Zupic and Čater [

23]. The first step of this process is to define the research design by specifying the research questions and methods.

The influential aspects refer to the essential articles, authors, journals, institutions, and corresponding countries. In contrast, the hidden themes denote the topics that have been explored in the CLS-based literature. The current study used a combination of intellectual structure and conceptual structure to achieve these research objectives. The intellectual structure is an approach that uses citation information to segregate similar articles. Though various intellectual structure approaches are available, this research applied ‘

bibliometric coupling’. Bibliometric coupling maps the connections between the articles citing similar references [

24]. Under this method, two articles are assumed to be coupled if they contain similar references. The greater the congruency between the two sets of citations the stronger the connection between the two articles. Such an approach is helpful if thematic clustering aims to find the research front, i.e., what is being published (Boyack and Klavans [

25]). Thus, this research segregates the existing literature on CLS by employing bibliometric coupling.

Previously, most studies segregated literature based on a single approach, i.e., intellectual or conceptual structure. In particular, co-citation analysis is one of the most used approaches of intellectual structure in this respect (Díez-Martín, Blanco-González, and Prado-Román [

26]; Randhawa, Wilden and Hohberger [

27]). Co-citation analysis assumes that two articles are similar if they are frequently cited simultaneously. However, co-citation analysis is appropriate when such clustering aims to explore the knowledge base [

28]. Here, bibliometric coupling is a more suitable method, as the objective is to explore the research front rather than the knowledge base. Conversely, the co-word analysis of keywords and the title of each article is also a frequently used method of conceptual structure [

17,

29]. The co-word analysis assumes that two articles are similar if they share identical keywords. However, this research argues that using a combination of intellectual and conceptual structures is more appropriate.

The research of the present study initially involved segregating the CLS-based literature into clusters using bibliometric coupling. Subsequently, each cluster was analyzed using co-word analysis. Such an approach helps to explore the topics covered and the depth of each cluster. Furthermore, influential aspects such as top journals, top authors, and top-cited documents were also analyzed for each cluster. Previously, most bibliometric reviews explored significant elements in the overall literature rather than specific themes. In other words, their flow of work starts with influential aspects and ends with thematic analysis. However, it is argued that exploring the influential aspects of each sub-theme in literature can provide helpful information concerning specific research areas. This argument is particularly valid for emerging themes that have a small number of citations and publications. Therefore, our research started with thematic analysis, and subsequently, the influential aspects were addressed. In this approach, each cluster is defined using bibliometric coupling and analyzed with the consideration of conceptual structure.

The second step of bibliometric analysis is to compile the bibliometric data. This research used the Web of Science database to extract the relevant literature on CLS. The following query was used to search the keywords of “American depository receipt*” or “global depository receipt*” or “depository receipt*” or “cross-listing*” or “cross-listing*” or “foreign stocks listing” in the topic.

TS = (“American depository receipt*” or “global depository receipt*” or “depository receipt*” or “cross listing*” or “cross-listing*” or “foreign stocks listing”)

Refined by: document types: (article) and [excluding] document types: (book chapter or data paper or proceedings paper) indexes = sci-expanded, ssci, at&hci, cpci-s, cpci-ssh, esci timespan = all years

The above search string initially extracted 416 publications after excluding review papers, books, and conference proceedings. Similarly, the abstracts and titles of each article were studied, leading to the selection of 315 publications that focus on CLS. The title, abstract, authors’ detail, author keywords, keyword index, journal, publication year, citations, and references were extracted for all 315 articles. After extracting the data, the clustering algorithm (as alluded to in step 3 of

Figure 1) was applied. Initially, bibliometric coupling was applied using the resolution of 0.9 with 1000 optimization processes in the VOS viewer to identify the clusters based on intellectual structure. The bibliometric coupling segregated the 315 publications into three different clusters. After that, co-occurrence analysis of keywords (both Author and Index keywords) was used to understand the conceptual structure of each cluster using the resolution of 0.9 with 1000 optimization processes in VOS viewer.

However, a thesaurus text file replaced or excluded some of the keywords extracted by the VOS viewer (to clean the data for conceptual structure). The thesaurus file was compiled after a three-step process. Initially, a list of all the keywords was extracted from the co-occurrence analysis in the VOS viewer. In the second stage, concepts with similar keywords which differed due to spellings or acronyms were replaced with identical ones. For instance, “international financial reporting standards” are also written as IFRS. Such keywords were assigned with identical keywords to find their actual impact. In the third stage, irrelevant keywords were excluded to make the analysis more relevant. For instance, “American depository receipts” was the most used keyword. However, including this keyword provides no new information, as all the selected publications are about CLS. Including such keywords to analyze the conceptual structure could lessen the impact of the other important keywords, which could yield meaningful thematic information. Therefore, a thesaurus file was used as a reference library in the co-occurrence analysis of keywords. Similarly, this study employs the R-package of bibliometrics to analyze the influential aspects of each cluster. Top journals, authors, countries, and documents were explored for each cluster. Graphs and tables were used to visualize results related to the influential aspects, while thematic analysis was presented using network graphs. Through this procedure, interpretations and future research directions can be established based on the themes found in the CLS-based literature.

The most prominent journals, authors, countries, articles, and themes were identified using bibliometric analysis, followed by a comprehensive analysis of the content of selected papers in the identified clusters. The three major themes were enumerated, and a conceptual framework was modelled to provide us with the complete picture, after which potential research areas were suggested. This study will help policymakers, regulators, and academic researchers to understand the dynamic aspects of CLS and identify the relevant areas that need investigation. With due regard to the methodological framework dynamics, it is worth noting here that we received a line of direction and appropriate justification of our paper’s format from the empirical articles of, for example, Arslan et al. [

30] and Oliveira et al. [

31].

3. Findings and Results

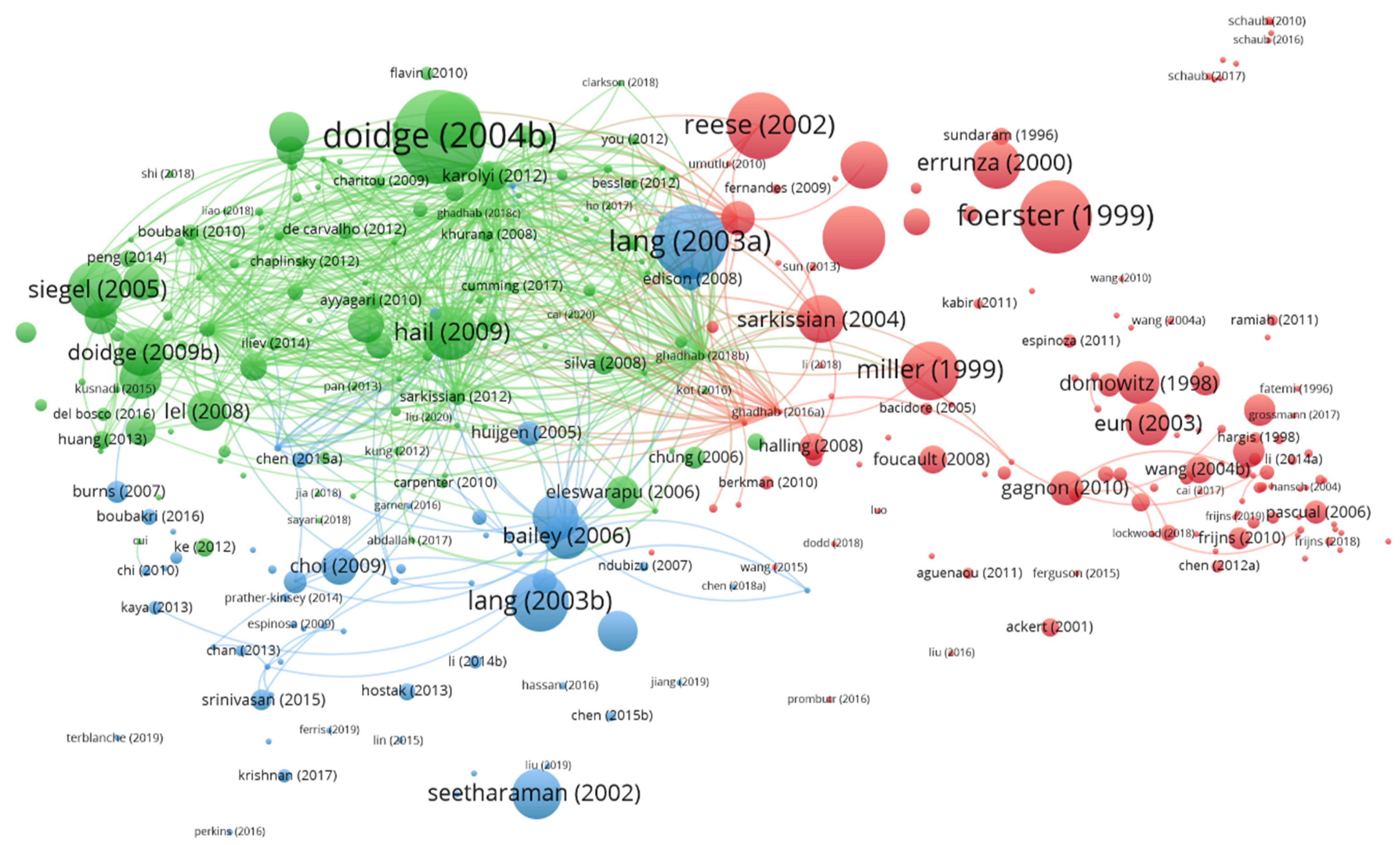

Figure 2 presents bibliometric coupling visualization extracted from the analysis of 315 publications in the VOS viewer. The results showed that CLS literature could be divided into three clusters (represented by green, red, and blue colors). Overall, 130 papers were assigned to the green theme, 123 publications were assigned to the red theme, and 60 were assigned to the blue theme.

Figure 3 presents a word cloud of the top 50 keywords for each theme. The word cloud for the red theme articles shows that liquidity, return, volatility, price discovery, arbitrage, and integration are the most used keywords in this cluster. This indicates that the red theme publications discuss the stock market-related outcomes of cross-listing from the perspective of stock returns, volatility, volume (liquidity), and price discovery mechanism. Therefore, the red cluster is labeled as the Outcome Perspective Theme (OPT) of CLS.

Similarly, the results also show that earnings quality, accounting standards, disclosure, adoption, analysts, information, and audit are the most used keywords in the blue theme publications. These keywords indicate that the blue theme publications discussed the accounting perspectives, such as adopting accounting standards, earnings quality, and analysts’ information quality of CLS. Thus, based on these keywords, the blue cluster is referred to as the Accounting Perspective Theme (APT). Conversely, publications in the third cluster (represented in green in

Figure 2) mainly contained the following keywords: corporate governance, ownership, personal benefits, investor protection, bonding theory, and market segmentation. These keywords indicate that the green theme concerns corporate governance issues, particularly bonding theory, and market segmentation theory. These theoretical perspectives explain the motive for cross-listing. Therefore, the green cluster is categorized as a Motivation Perspective Theme (MPT). The three clusters’ influential aspects and conceptual structure are provided in the following sections.

3.1. Outcome Perspective Theme (OPT)

3.1.1. Influential Aspects of OPT

Figure 4 shows the evolution of the literature on OPT over time, starting from 1993. Since then, researchers have been continuously publishing under this theme, particularly after 2009. Similarly,

Table 1 presents the top journals with OPT publications. Following Bradford’s law, the top five journals are categorized as Zone 1 journals (publishing more than 33% of the articles). Notably, the Journal of Banking and Finance (sixteen articles) and Applied Economics Letters (eleven articles) are the top journals in terms of publication number. Similarly, the Journal of Multinational Financial Management (six articles, starting from 2015) and the International Review of Financial Analysis (four articles, starting from 2011) published the latest OPT articles.

This research also explores the top authors that contribute to this theme, as shown in

Figure 5. Schaub M. is the most prominent author, with nine publications since 2010. Similarly, Ghadhab I., Chen MP., Frijns B., and Tourani-Rad A are other influential authors contributing to OPT literature.

Figure 6 explores the most prominent countries of origin for the corresponding authors, showing that the U.S., China, New Zealand, and the U.K. are the top countries of corresponding authors. One of the reasons behind more research being conducted in these countries could be due to the increasing trend of cross-listing shares in these countries. It is also notable that most of the studies are SCPs (Single-Country Productions), while fewer studies involve collaboration between authors from multiple countries (i.e., MCP—Multi-Country Production).

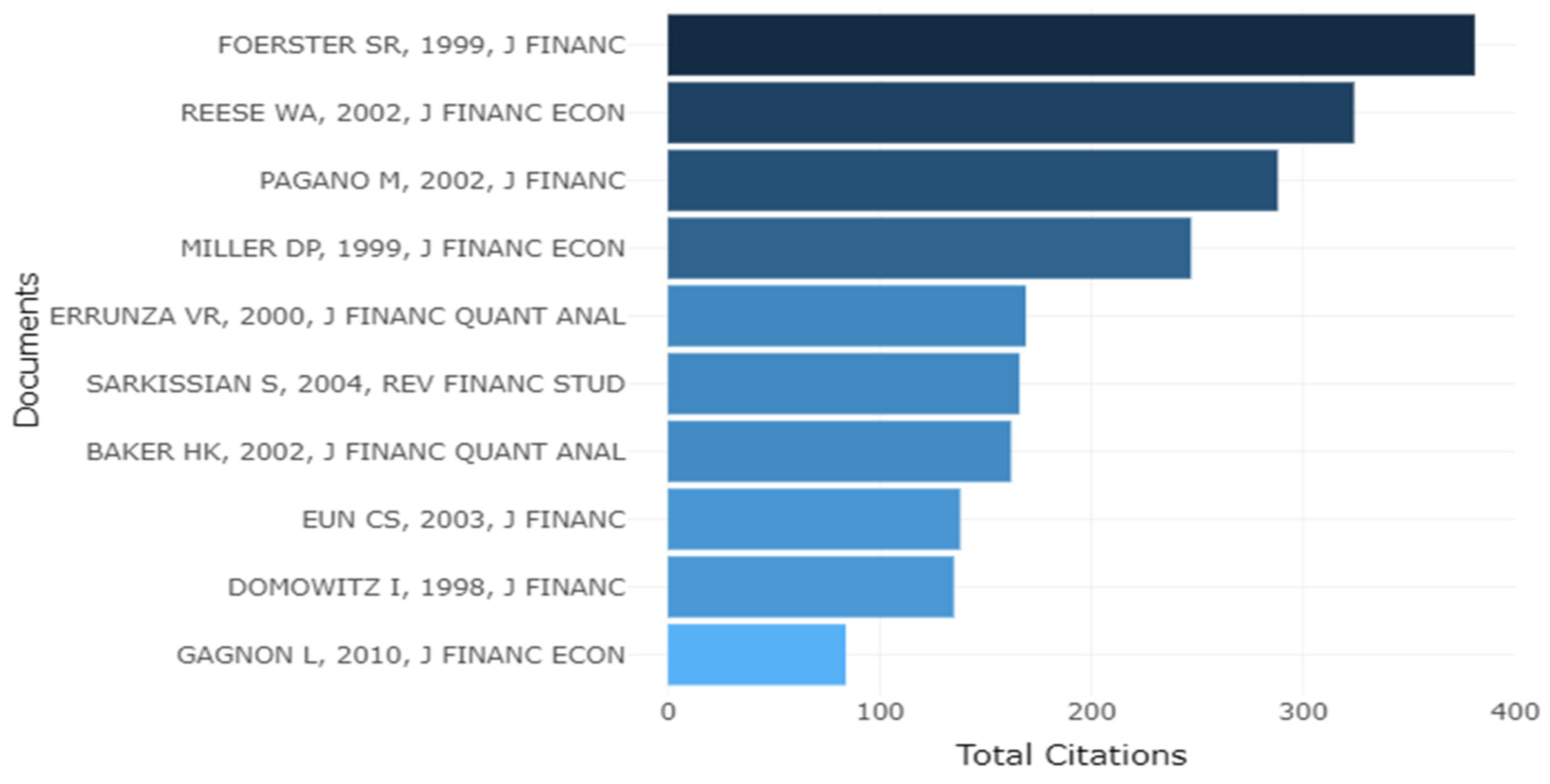

Our study also considered the top 10 publications (based on total citations) related to OPT, as presented in

Figure 7. For instance, a study by Foerster and Karolyi [

32] is the most cited document among OPT publications. They investigated the impact of cross-listing on stock returns. They found that share value changed positively after the event of cross-listing and helped in raising low-cost capital. The second most cited document, authored by Reese and Weisbach [

33], studied investor protection after cross-listing. They examined the hypothesis that cross-listing increases minority shareholders’ protection and enhances managers’ expected cost of removing isolated benefits. Their results reveal that a key motivation for non-US firms to cross-list their shares is to protect minority shareholder interest.

Similarly, Pagano et al. [

34] investigated cross-listing features and post-listing performances while considering location (in terms of European and U.S. cross-listing). Their results revealed that sales revenue increased after the cross-listing of European firms in the U.S. Another influential article from OPT is a study by Miller [

35], which compared the impact of cross-listing on stock performances for developed and developing countries. Miller [

35] also found that the choice of an exchange for cross-listing and the method of new offering (such as public or private offering) are important determinants of price reactions after cross-listing.

Figure 7 shows that Errunza and Miller [

36] also authored one of the top-cited articles. They studied cross-listing in terms of reduced cost of capital. They also contended that such a decrease in the cost of capital is beneficial for the development of financial markets. Sarkissian and Schill [

37] further explored the economic, geographic, cultural, and industrial factors as essential determinants for selecting a cross-listing location. Their results also revealed that the similar proximity limitations that are supposed to lead to “Home Bias” in investment portfolio decisions also impact financing decisions. Another influential study by, this time by Baker, Nofsinger, and Weaver [

38], explored cross-listing benefits with respect to growth visibility. Their results also revealed that cross-listing in the U.S. has more growth visibility and less cost of capital than cross-listing in the U.K.

Eun and Sabherwal [

39] investigated cross-listing with respect to market integration. Their results showed that the U.S. and Canadian exchanges are linked with each other. This cointegration of the two markets affects the price reaction of cross-listing shares. However, Domowitz, Glen, and Madhavan [

40] found that the benefits of inter-market information and the low cost of capital are contingent on shareholders. Different types of shareholders bear a variety of additional costs and benefits of cross-listing in this respect.

The last influential document presented in

Figure 7 is articulated by Gagnon and Andrew Karolyi [

41], who explored the role of quotes and daily prices in creating arbitrage opportunities for cross-listing of shares. In summary, the aforementioned articles primarily discuss price discovery for cross-listing of shares, particularly regarding asymmetric information, home and foreign exchange location, market integration, and investor protections. To further explore the content analysis of OPT, the conceptual structure is analyzed in the subsequent section.

3.1.2. Conceptual Structure of OPT

A co-occurrence network of keywords (VOS Viewer) is presented in

Figure 8 to highlight the conceptual structure of OPT publications. A criterion of minimum link strength of three shows the links between the nodes. Similarly, the size of each node indicates the relative frequency of occurrence. The figure shows that OPT-based literature can be divided into two sub-fields based on its conceptual structure. The top keywords used by the first sub-theme include information, liquidity, price discovery, arbitrage, integration, and cointegration. This means that this domain investigates the liquidity and price discovery of cross-listed stocks, particularly for asymmetric information, arbitrage opportunities, and market integrations between home and foreign markets. This sub-field is named OPT-Info (OPT-Informativeness). For instance, Frijns et al. [

42] studied the impact of home and foreign market integration on the price discovery of cross-listed stocks in New Zealand and Australia. They reported that growth in the Australian market increases its informativeness, ultimately decreasing the bid–ask spread.

Miller [

35] studied the market reaction of cross-listing in the contingency of choice of exchange, location, and capital avenue. Similarly, Kim et al. [

43] investigated the local currency of CLS, exchange rate, and integration of local and foreign markets as determinants of price discovery of CLS. Ghadhab and Hellara [

44] examined the impact of cross-listing on price discovery. Their results revealed that market integration and asymmetric information contribute to price discovery. Similarly, Ghadhab [

45] discussed the arbitrage opportunities using intraday liquidity patterns and found that liquidity increases in the presence of arbitrage opportunities. Such arbitrage opportunities contribute to informed trading and price discrepancies. In short, the central theme of OTP-Info revolves around information asymmetries that lead to arbitrage opportunities and market integration.

Conversely, the second sub-theme pertains to the following top keywords: stock returns, profits (profits), volatility, market efficiency, emerging economies, risk, segmentation, and home bias. This list indicates that such studies focus on stock returns and risk, considering market characteristics, particularly in emerging economies. This sub-field is named OPT-MKT (OPT-Market). For instance, Hargis and Ramanlal [

46] explored the impact of cross-listing on local market development regarding trading volume and liquidity. Errunza and Miller [

36] examined the benefits of financial market liberalization for ADRs, particularly regarding the cost of capital. Foerster and Karolyi [

32] explained the variation in abnormal returns after cross-listing with changing risk exposure, shareholding base, and amount of money raised.

Similarly, Halling et al. [

47] found that the stock return and volatility of ADRs depend on the home country’s location, i.e., whether they are a developed or developing country. Conversely, Chan and Kwok [

48], Li et al. [

49], and Zhang [

50] studied the Chinese stocks listed in Hong Kong with respect to price disparities and stock returns. Hence, the literature on this theme is not limited to ADRs in the U.S. market as it also includes cross-listings in other equity markets.

3.2. Accounting Perspective Theme (APT)

3.2.1. Influential Aspects of APT

The second cluster of bibliometric analysis is represented in blue in

Figure 2. The evolution of the publications of APT over time is provided in

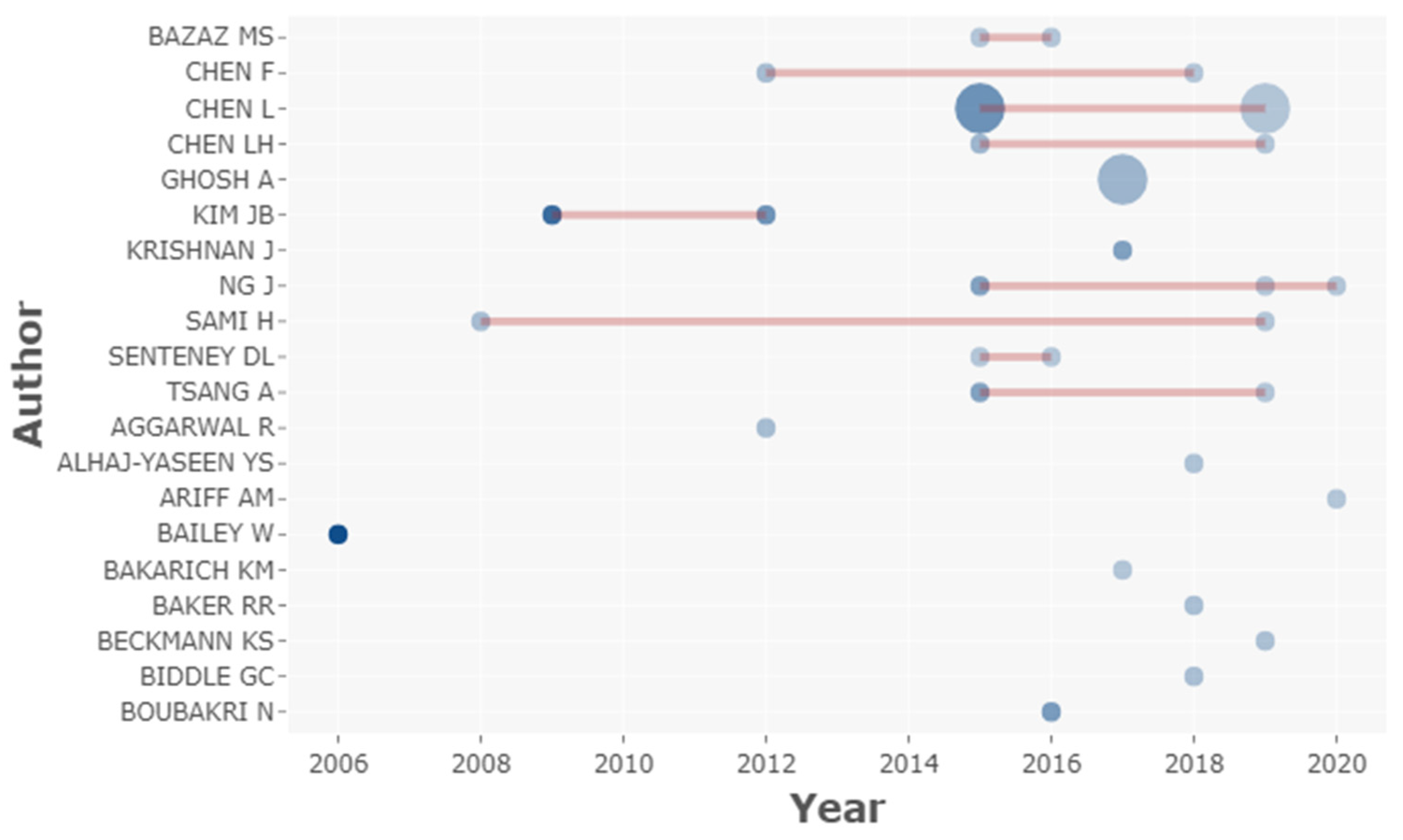

Figure 9. This graph shows a trend in publications in the later years. Notably, in 2015 and 2019, many articles were published regarding accounting standards and earnings quality in the context of CLS research.

Table 2 presents the top journals regarding APT. The results show that Accounting Review and Accounting Horizon are among the most published sources. Notably, the Journal of Contemporary Accounting & Economics has published three recent articles. Similarly, in terms of the total number of citations, the Journal of Accounting Research is the top journal.

Figure 10 presents the list of top authors over time. This figure shows that Chen L is atop the author list with four articles. Similarly, N.G. contributed to three publications. This indicates that the literature on CLS from an accounting perspective is dispersed among different researchers.

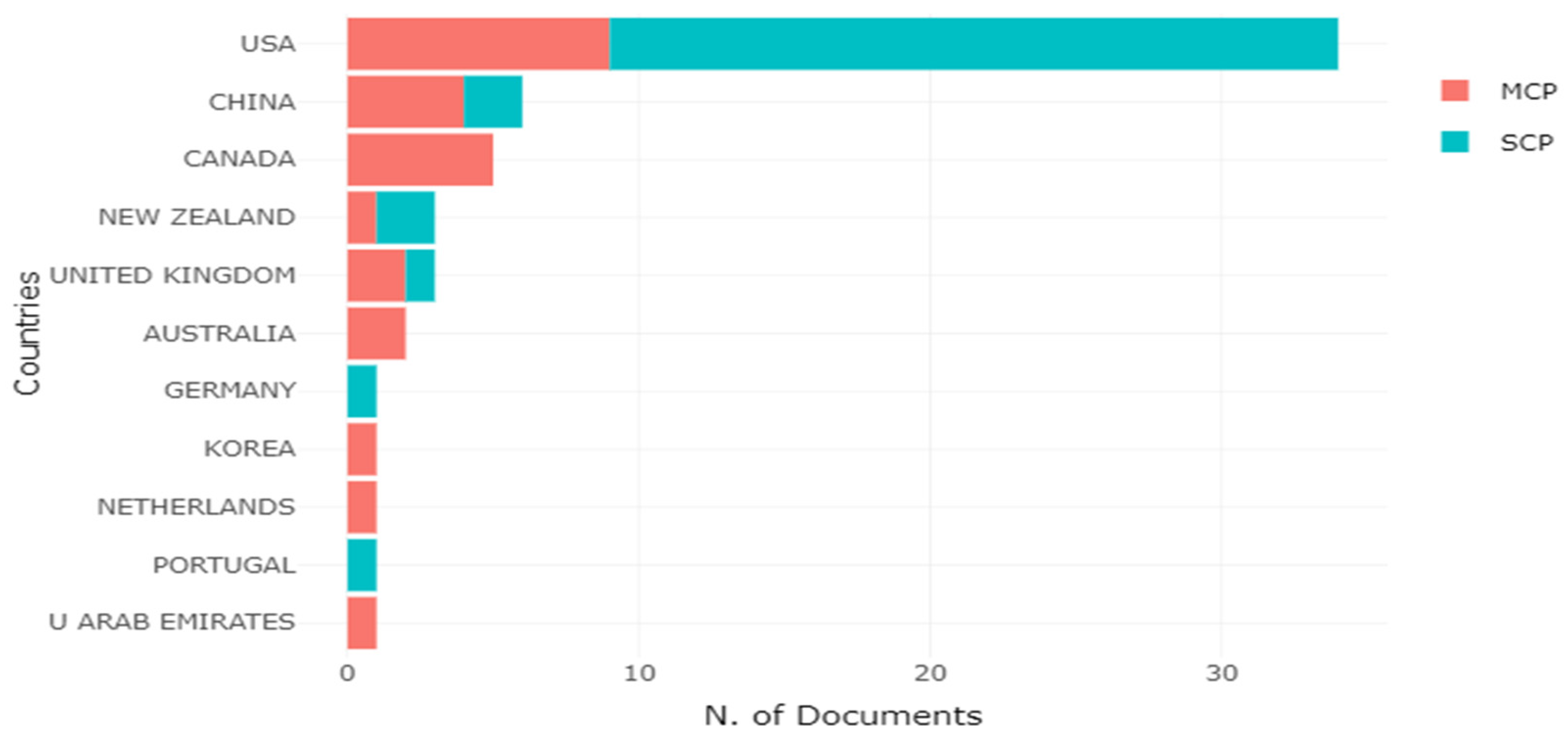

The U.S., China, and Canada are the top countries with respect to publishing APT research, as seen in

Figure 11. Notably, most of the U.S-based literature consists of single-country productions (SCPs). However, most of the overall literature consists of collaborative work as the percentage of multi-country productions (MCPs) are higher, particularly in Canada and China.

Figure 12 explores the top publications regarding APT. The study of Lang, Raedy, and Yetman [

51] is the most cited document. Though

Figure 12 also presents the same reference as the second most cited document, these two articles are the same, differing only due to name discrepancies. Their study compared US GAAP adopted by the U.S. local firms with accounting standards adopted by foreign cross-listed firms. Their results found that cross-listed firms are less hostile in financial reporting and earnings management, and their stock prices adjust to awful news quickly. Our findings are consistent with an empirical study by Leuz et al. [

52], who reported that firms operating under weak investor protection environments tend to engage in earnings management more often than not. This finding is also notable from the perspective of the established notion that the legal and regulatory environment is less stringent for CLFs, and as such, motivations for managing the earnings are more significant. Thus, earnings management is also a severe issue for all such CLFs.

Pincus, Rajgopal, and Venkatachalam [

53] evaluated the accrual anomaly in 20 countries. Their results confirmed the accrual anomalies in four countries, including Australia, Canada, the UK, and the U.S. Furthermore, ADRs documented accrual anomalies even in those that did not demonstrate accrual anomalies. Choi, Kim, Liu, and Simunic [

54] also studied the relationship between cross-listings and audit fees. Huijgen and Lubberink [

55] compared the earnings of U.K.-listed firms and U.K-cross-listed firms. It was noted that U.K-cross-listed firms have excellent earning yields compared to single-listed firms. Auditors charged a higher cost for the cross-listed firms with solid legal systems than for cross-listing firms with weak legal systems. They also suggested that high earnings were a motivator of cross-listing, as some aimed to gain the benefits of earning conservatism.

Kim, Li, and Li [

56] studied the elimination of reconciliation requirements for CLS in the U.S. Their results showed that ease in the reconciliation requirement negatively affected the stock prices and informed trading. They concluded that losing information after such an ease of disclosure requirement was not crucial for the investor. Finally, Shi, Magnan, and Kim [

57] forecasted the disclosure using Agency, institutional, and bonding theories. They found that disclosure likelihood increases with the strength of legal institutions, listing type, ownership structure, and product market. In short, the influential documents regarding APT discuss earnings quality, the adoption of accounting standards, disclosure requirements, and audit premiums for CLS. Seetharaman, Gul, and Lynn [

58] examined the relationship between audit pricing and litigation risk for cross-listed shares. Their results revealed that auditors in the U.K. charge more fees when their clients cross-list in the U.S. financial market due to risk differences across the liability regime. Bailey, Andrew Karolyi, and Salva [

59] investigated the outcomes of increased disclosure requirements for cross-listed firms in the U.S. They found that the earnings announcements of cross-listed firms positively affect their return and volume. They further contended that this positive effect becomes more substantial if the cross-listed firm is from a developing country with strict disclosure requirements. Another frequently cited document by Fernandes and Ferreira [

60] explored whether informativeness is a determinant of price discovery. They found that the coverage of analysts is an essential factor in the price discovery of CLS in emerging markets compared to liquidity, accounting quality, or ownership.

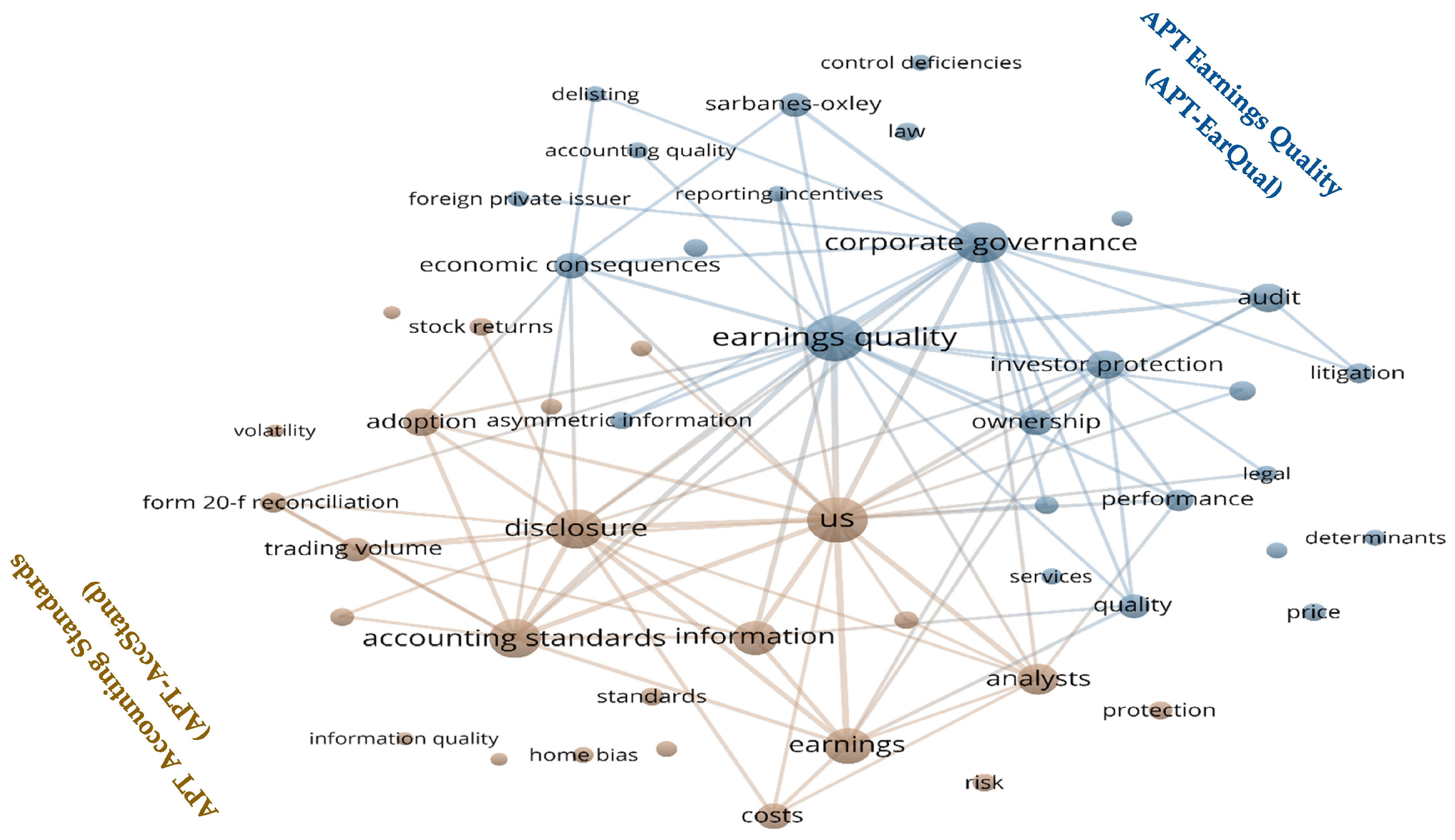

3.2.2. Conceptual Structure of APT

Figure 13 provides the co-occurrence analysis of keywords for APT. According to the co-occurrence analysis, the literature on APT can be segregated into two sub-fields. The top keywords of the first sub-field are earnings quality, corporate governance, ownership, investor protection, and audit. This list shows that this sub-field of APT focuses on earnings quality and corporate governance issues such as ownership structure and investor protection. This sub-field is named APT-EarQual (APT-Earnings Quality). For instance, Huijgen and Lubberink [

55] compared the earnings management of cross-listed stocks with those of single country-listed stores in the U.K. Their results showed more earnings conservatism in cross-listed firms than single-listed firms, particularly in the early years of cross-listing. Choi et al. [

54] also reported that cross-listing results in higher audit fees, especially when a foreign country’s legal regime is stronger than the home country’s legal regime. Similarly, Lin et al. [

61] argued that the listing environment affects the ability of the audit committee to manage their earnings. Conversely, Ndubizu [

62] investigated the benefits of high earnings and profits of cross-listing while comparing IPO and non-IPO listings. Srinivasan et al. [

63] investigated the frequency of restatement mistakes in foreign-listed stocks in the U.S. and found that the restatement frequency of cross-listed stocks is lower than that of local firms. More recently, Kamarudin et al. [

6] studied the impact of cross-listing on the quality of earnings but in the contingency of investor protection. Due to the discussion above, we can conclude that APT-EarQual focuses on the quality of earnings concerning different perspectives and environmental settings.

Conversely, the second sub-field of APT emphasizes disclosure, accounting standards, adoption, information, and analysts’ views, as shown in

Figure 13. This sub-field is named APT-AccStand (APT-Accounting Standards). For instance, Goto et al. [

64] explained the role of strategic disclosures in stock returns and the adoption of IFRS/GAAP for cross-listed firms in the U.S. Similarly, Kaya and Pillhofer [

65] found that, despite having the option of IFRS, most ADRs in the U.S. choose U.S. GAAP. Hong [

66] found that the mandatory adoption of IFRS by cross-listed stocks decreases the voting premium, especially in a robust legal environment. Aggarwal et al. [

67] explored the dividend behaviors of cross-listed stocks while linking the information environment with dividend payments. In short, this sub-field of APT studies the disclosure and accounting standards from various perspectives in CLS. From

Figure 13, it can be safely argued that the cross-listing of shares influences the information environment for CLFs.

Our findings support the proposition made by Fernandes and Ferreira [

60], which suggested that CLS exerts an asymmetric impact on the worldwide informativeness of their prices, and variations in their firm-specific returns support this fact. The price informativeness for the CLS in the developed market is much improved for the relevant firms. Their study also reported the added impact of analyst coverage on the dissemination of market-wide information. Our findings help us to recommend some implications for the regulators of financial markets. The strict disclosure requirements for excessive monitoring and control measures can adversely affect the CLS regime, as has also been reported by Fernandes and Ferreira [

60], that such disclosure requirements ultimately crowd out the dependence upon private information in the context of firms in the emerging markets. Our co-occurrence analysis of the top 50 keywords of articles from APT in

Figure 13, which contained keywords such as accounting standards information, earnings quality, corporate governance, investor protection, disclosure, reporting incentives, trading volume, economic consequences, etc., has prompted us to conclude that accounting and reporting requirements can influence improvements in the information environment in the relevant markets in the context of CLFs. Thus, it can also be safely contended that the information environment can be improved if the market regulators complement the disclosure requirements with adequate incentives and policy initiatives to encourage desirable investment in the information regime at the private level and minimize crowding-out effects, as mentioned above.

3.3. Motivation Perspective Theme (MPT)

3.3.1. Influential Aspects of MPT

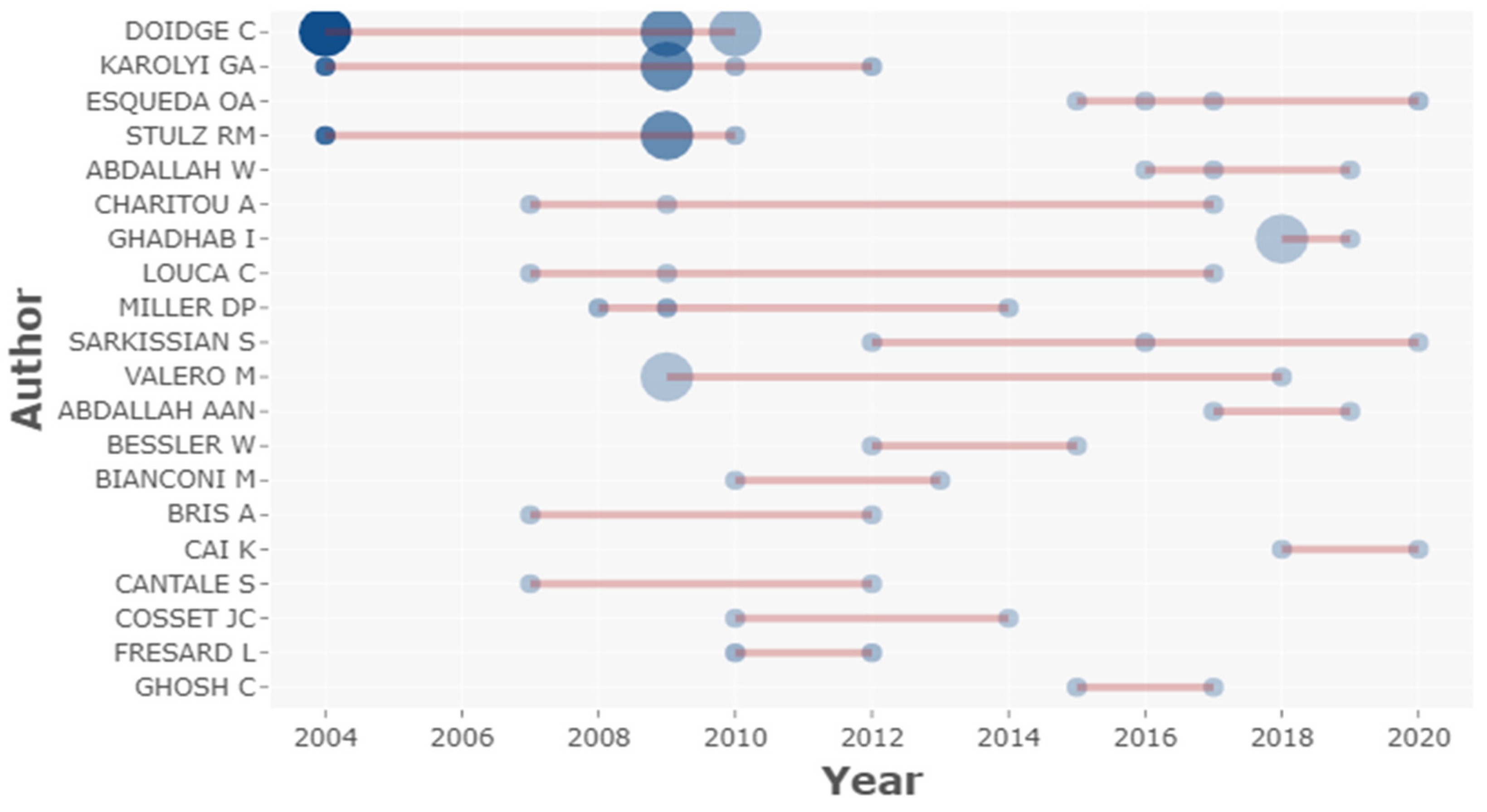

Figure 14 shows that the literature on MPT has generally grown over time, particularly in 2012 and 2018—showing an increasing trend. Such increasing trends may be due to essential corporate governance reforms post-analysis.

Table 3 further presents the top journals regarding the publishing of research on corporate governance and related issues of CLS. Hence, both cluster 1 and cluster 3 share the same leading journal. The Journal of Corporate Finance and the Journal of Financial Economics are other top journals that contain literature on MPT of CLS. However, in terms of the total number of citations, the Journal of Financial Economics is the most influential journal, with 1515 total citations.

Figure 15 shows the top authors with respect to publishing research on MPT. Doidge, C., Karolyi, GA., and Stulz, RM. are the top authors in terms of publications and citations. However, these authors only helped to provide a knowledge base, as their work was published earlier. In contrast, Esqueda, OA. has published four articles since 2015 and is a top author with respect to current research in MPT-based literature. Similarly,

Figure 16 shows that most of the relevant authors belong to the U.S., which is the country that has produced the most articles, both in terms of SCPs and MCPs.

Figure 17 explores the top publications of MPT, wherein it can be seen that Doidge [

68] has the most cited paper. Doidge [

68] suggested that investor protection and cross-listing are influencing factors for growth. They explained that cross-listed shares belonging to a country with weak investor protection experience more growth after being cross-listed. Therefore, such firms are more likely to cross-list shares. Siegel [

69] authored the second most cited paper, in which he identified legal and reputational bonding as success factors of cross-listing and compared their outcomes. Their results showed that reputational bonding is more important in explaining the success of cross-listing than legal bonding in the U.S. Hail and Leuz [

70] also argue that the decreased cost of capital and more growth visibility are the main reasons for cross-listing.

However, Doidge, Karolyi, Lins, Miller, and Stulz [

68] report that firms that have shareholders with private benefits are less likely to cross-list shares in order to safeguard their interests because the decision to cross-list in the U.S. exchange depends on firm-specific variables rather than the benefits of cross-listing. Lins, Strickland, and Zenner [

71] explored the benefits of cross-listing for firms in developing countries. Lel and Miller [

5] attempted to correlate corporate governance performance with weak investor protection and reported that firms with weak investor protection regulations are more likely to remove bad-performing CEOs to improve corporate governance and financial performance. Piotroski and Srinivasan [

72] investigated the impact of the Sarbanes–Oxley Act (SOX) on listing behavior before and after the implementation of SOX in 2002. The results of this study revealed that the frequency of cross-listing among small firms decreased after the implementation of SOX-2000 due to increased governance costs. Last but not the least, Bell, Filatotchev, and Rashesed [

73] explained the problems and prospective solutions relating to cross-listing, thereby concluding that the main issues of information asymmetry, unfamiliarity, cultural differences, and institutional distance in the foreign capital markets can be addressed through organizational isomorphism, reputational endorsements, and signaling.

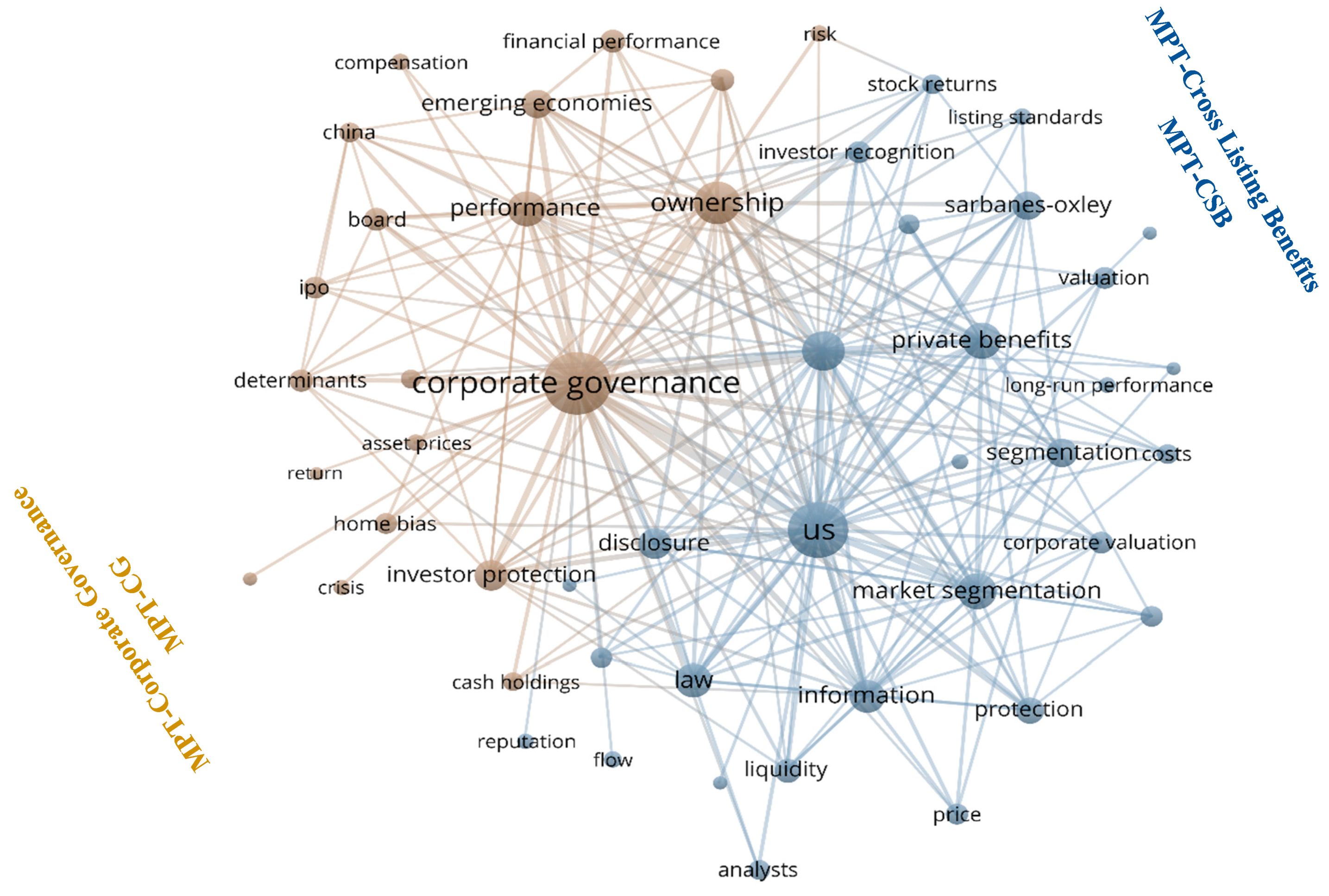

3.3.2. Conceptual Structure of MPT

Figure 18 shows that the MPT-based literature can be segregated into two sub-fields based on their conceptual structure of keywords. One sub-field represents the top keywords of market segmentation, investor protection, bonding theory, private benefits, information, and liquidity. These keywords indicate that this sub-field explains cross-listing benefits using market segmentation, bonding, and liquidity theories. Therefore, this sub-theme is labeled as MPT-CSB (MPT-Cross-listing Benefits). According to market segmentation theory, firms opt to cross-list their shares to make them more accessible, ultimately increasing their value and decreasing the cost of capital. For instance, Lins et al. [

71] argued that foreign stocks listed in the U.S. from developing countries benefit more from greater access to the capital market compared to foreign stocks from developed countries. This is because foreign stocks from developing countries are credit constraints in their local market. You et al. [

74] also identified a strong implication for market segmentation theory and found that cross-listings due to specific needs enjoy the benefits of valuations. Similarly, bonding theory postulates that firms operating in weak governance opt to cross-list their shares to show their intention regarding voluntary adoption of sound corporate governance practices. You et al. [

74] and Ferris et al. [

75] also reported the implications of bonding theory as a motivator of cross-listing. However, Liu et al. [

76] rejected the implications of the bonding theory for Chinese cross-listing stocks, showing that stocks with single-country listings performed better than the cross-listed Chinese stocks even in a better corporate governance environment. Liquidity theory also explains the reason for increased stock liquidity after the cross-listing. You et al. [

74] found weak implications of the liquidity hypothesis regarding CLS. Chung [

77] and Silva and Chávez [

78] also explored the liquidity cost for ADRs, reporting that only large firms enjoyed liquidity benefits in the home market after the cross-listing of their shares.

Dang et al. [

79] revealed that cross-listing has adverse effects on liquidity commonality in the home market. However, in contrast, these effects are positive for foreign listed markets. One sub-field of MPT discusses the motivation of cross-listing from various perspectives. Conversely, another sub-field of MPT explores corporate governance, ownership, investor protection, and performance-related issues. This sub-field focuses on corporate governance issues and investor protection concerning CLS. Therefore, this sub-field is named MPT-CG (MPT-Corporate Governance). For instance, Lel and Miller [

5] found that poorly performing CEOs were at a greater risk of termination in cross-listed firms, especially when the cross-listed firm belonged to a country with weak investor protection regulations. Ayyagari and Doidge [

80] examined cross-listing decisions that influence shareholder ownership structures and controlling rights. Ke et al. [

81] studied the sensitivity of executive compensation and the performances of different Chinese stocks, including h-stock (stocks incorporated in China but listed in Hong Kong).

Esqueda and Jackson [

82] reported that the performance of cross-listed stocks with high inside ownership increases after their cross-listing. Esqueda [

15] examined the change in dividend policy due to corporate governance practices regarding investor protection and reported that, after adopting investor protection measures, the equilibrium points of dividends also changed but in the contingency of locus of control. More recently, Chakraborty et al. [

83] reported the relationship between corporate governance and the risk of cross-listed Canadian stocks, revealing that CEO duality and inside ownership affect the risk of CLS only, while institutional shareholdings and disclosure are more relevant to locally listed stocks. In short, the second sub-field of MPT publications investigated the different aspects of corporate governance for firms with CLS.

5. Conclusions and Implications

This research reviewed the influential aspects, intellectual structure, and conceptual structure of the CLS-based literature using bibliometric analysis in the context of the use of CLS as a tool for targeting sustainable performance. Previously, most bibliometric studies have first explored the principal elements of literature and then divided the literature into clusters through science mapping. However, the present study reversed this order and first divided the literature pertaining to CLS into clusters using bibliometric coupling and then explored each theme’s influential aspects and conceptual structure separately. The results of bibliometric coupling revealed that the CLS literature could be divided into three broad themes: the Outcome Perspective Theme (OPT), which explores the stock market outcomes regarding price discovery and liquidity from different contingency factors; the Accounting Perspective Theme (APT), which investigated the CLS literature for earning quality and adoption of accounting standards; and finally, the Motivation Perspective Theme (MPT), which investigated the benefits of cross-listing that motivate firms to cross-list in different financial markets.

After the identification of the three themes, the influential aspects and conceptual structure of each cluster were examined. This thematic-to-influential aspect approach could provide more relevant information for a specific sub-field. For instance, the analysis showed that each cluster’s top journals and authors differ. This dissimilar information on the influential aspects of each cluster helped us to obtain more relevant information about our area of interest. However, our approach may lead to oversights in the essential aspects of a theme, especially the emerging pieces that have a small number of citations or documents. Overall, researchers can improve their results by using the thematic-to-influential aspect approach rather than the influential aspect-to-thematic flow approach.

This research also studied the conceptual structure of three identified themes using a co-occurrence network of keywords. The analysis showed that OPT discussed the outcomes of cross-listing from two perspectives. The first type primarily focused on asymmetric information (OPT-Info) to explain price discrepancies and market integration. Conversely, other studies related to OPT mainly investigated the risk and returns concerning market efficiencies, particularly in emerging markets (OPT-MKT). Similarly, articles on APT studied the two sub-fields regarding earnings quality (APT-EarQual) and the adoption of accounting standards (APT-Accutane). The articles on MPT also studied cross-listings from two perspectives. The first type focusses on the benefits of cross-listing (MPT-CLB) that motivate firms to cross-list using different theories such as market segmentation, bonding, and liquidity theory. Conversely, the second sub-field from MPT focuses on corporate governance (MPT-CG) issues from different perspectives, such as executive compensation.

Identifying the intellectual structure, influential aspects, and conceptual structure of the CLS-based literature can contribute to the expansion of research strands, as evidenced by the research questions proposed in this study. Moreover, stakeholders of CLFs and firms planning to cross-list can also gain useful insights into the consequences of cross-listing. These distinguishing features make this study a significant contribution to the growing literature on CLS.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}