The Moderating Role of Environmental Information Disclosure on the Impact of Environment Protection Investment on Firm Value

Abstract

:1. Introduction

2. Related Literature and Hypotheses

2.1. Environmental Protection Investment

2.2. Environmental Information Disclosure

3. Data and Methodology

3.1. Model 1: The Impact of Environmental Protection Investment on Firm Value

3.1.1. Sample and Data

3.1.2. Dependent Variables

3.1.3. Explanatory Variables

3.1.4. Control Variables

3.1.5. Descriptive Statistics

3.2. Model 2: The Moderating Effect of Environmental Information Disclosure

3.2.1. Sample and Data

3.2.2. Dependent Variables

3.2.3. Explanatory Variables

3.2.4. Moderating Variables

3.2.5. Control Variables

3.2.6. Descriptive Statistics

4. Empirical Results and Discussion

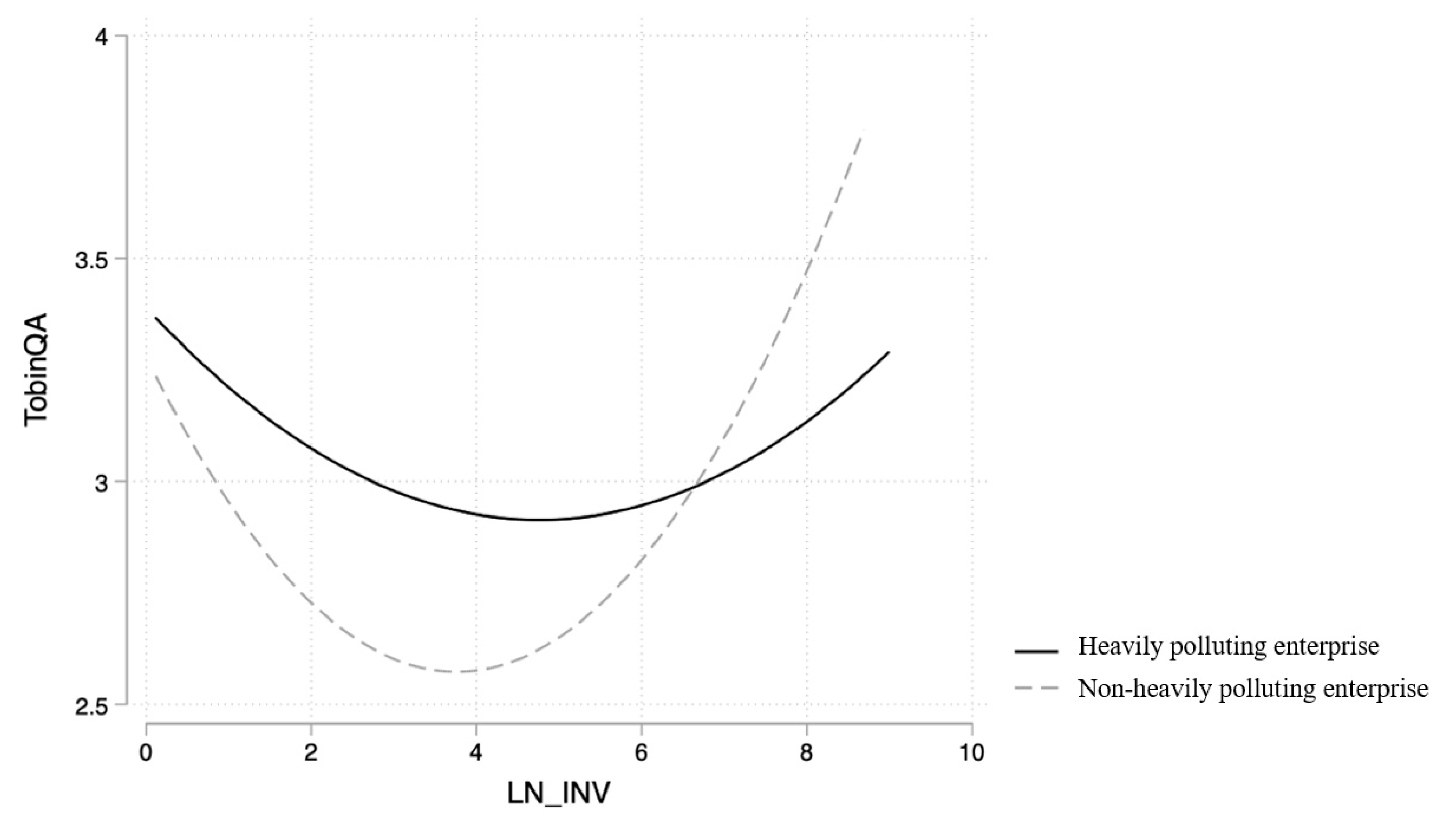

4.1. The Impact of Environmental Protection Investment on Firm Value

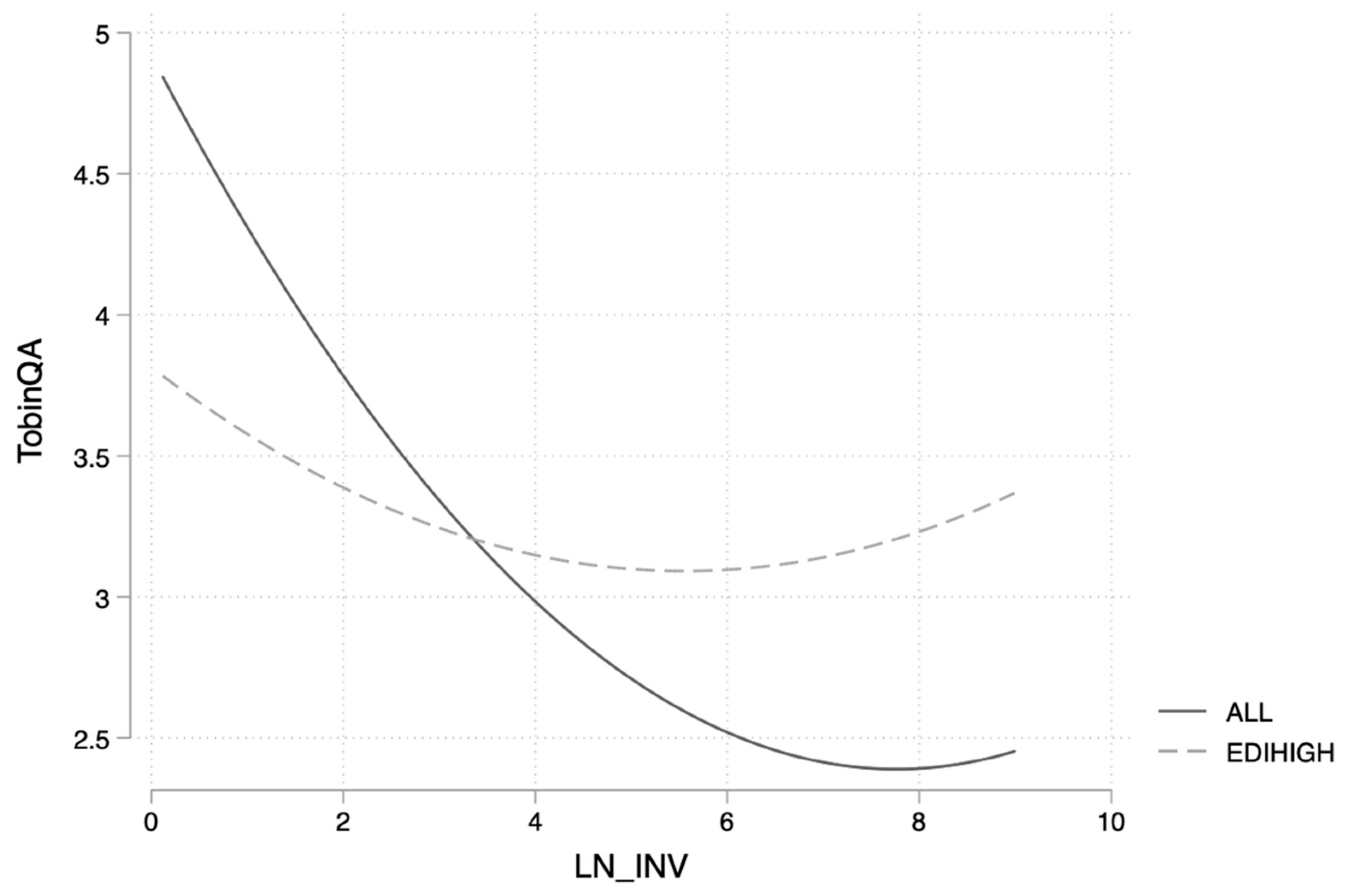

4.2. The Moderating Effect of Environmental Information Disclosure

5. Robustness Tests

6. Conclusions

7. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Heavily Polluting Industry | Non-Heavily Polluting Industry | |||

|---|---|---|---|---|

| (1) Tobin Q | (2) Tobin Q | (3) Tobin Q | (4) Tobin Q | |

| LN_INV | −0.0117 | −0.213 *** | 0.0360 | −0.483 *** |

| (−0.74) | (−3.60) | (1.01) | (−3.40) | |

| 0.0213 *** | 0.0635 *** | |||

| (3.80) | (4.18) | |||

| SIZE | −0.722 *** | −0.745 *** | −0.447 *** | −0.492 *** |

| (−16.10) | (−16.26) | (−4.54) | (−5.13) | |

| LEV | −0.0346 | −0.0186 | −0.0968 | −0.0445 |

| (−0.19) | (−0.10) | (−0.26) | (−0.13) | |

| FIRST | −0.811 *** | −0.836 *** | −0.602 | −0.618 |

| (−4.77) | (−4.90) | (−1.05) | (−1.20) | |

| INS | 2.137 *** | 2.117 *** | 0.634 | 0.710 |

| (13.89) | (13.74) | (1.23) | (1.49) | |

| YEARTURN | 0.0121 * | 0.0115 * | −0.0135 | −0.00869 |

| (1.80) | (1.72) | (−0.72) | (−0.51) | |

| STATE | −0.349 *** | −0.334 *** | −0.405 *** | −0.439 *** |

| (−6.98) | (−6.66) | (−2.78) | (−3.37) | |

| GROW | 0.475 *** | 0.487 *** | 0.0146 | 0.0749 |

| (5.00) | (5.22) | (0.10) | (0.52) | |

| LNG | 0.476 *** | 0.475 *** | 0.357 ** | 0.267 * |

| (8.03) | (8.10) | (2.42) | (1.82) | |

| YEAR | Control | |||

| IND | Control | |||

| cons | 3.386 *** | 3.900 *** | 4.093 *** | 5.518 *** |

| (24.19) | (18.59) | (4.04) | (4.93) | |

| N | 2149 | 2149 | 281 | 281 |

| 0.400 | 0.405 | 0.402 | 0.465 | |

| F | 46.18 | 44.92 | - | - |

| Tobin QA (EDI) | Tobin QA (LD) | Tobin QA (MD) | Tobin QA (SD) | Tobin QA (PD) | |

|---|---|---|---|---|---|

| LN_INV | −0.388 ** | −0.363 *** | −0.355 ** | −0.658 *** | −0.253 |

| (−2.22) | (−2.61) | (−2.44) | (−2.76) | (−1.57) | |

| 0.0241 | 0.0300 ** | 0.0273 ** | 0.0537 *** | 0.0132 | |

| (1.46) | (2.35) | (2.04) | (2.71) | (0.80) | |

| EDI | −6.617 ** | ||||

| (−2.57) | |||||

| LN_INV*EDI | 1.507 ** | ||||

| (2.34) | |||||

| *EDI | −0.0649 | ||||

| (−1.50) | |||||

| LD | −4.768 ** | ||||

| (−2.51) | |||||

| LN_INV*LD | 1.196 ** | ||||

| (2.46) | |||||

| *LD | −0.0614 * | ||||

| (−1.91) | |||||

| MD | −4.010 ** | ||||

| (−2.48) | |||||

| LN_INV*MD | 1.030 ** | ||||

| (2.26) | |||||

| *MD | −0.0538 * | ||||

| (−1.67) | |||||

| SD | −6.787 *** | ||||

| (−2.66) | |||||

| LN_INV*SD | 1.659 ** | ||||

| (2.44) | |||||

| *SD | −0.106 ** | ||||

| (−2.03) | |||||

| PD | −3.877 ** | ||||

| (−2.31) | |||||

| LN_INV*PD | 0.687 * | ||||

| (1.65) | |||||

| *PD | −0.00667 | ||||

| (−0.20) | |||||

| SIZE | −1.257 *** | −1.262 *** | −1.256 *** | −1.261 *** | −1.264 *** |

| (−5.76) | (−5.75) | (−5.72) | (−5.77) | (−5.72) | |

| LEV | 2.228 ** | 2.206 ** | 2.150 ** | 2.154 ** | 2.263 ** |

| (2.20) | (2.19) | (2.19) | (2.20) | (2.20) | |

| FIRST | −1.532 *** | −1.613 *** | −1.478 *** | −1.359 *** | −1.549 *** |

| (−2.87) | (−2.87) | (−2.88) | (−2.85) | (−2.88) | |

| INS | 2.806 *** | 2.833 *** | 2.806 *** | 2.738 *** | 2.798 *** |

| (6.12) | (6.04) | (6.14) | (6.21) | (6.13) | |

| YEARTURN | −0.0118 | −0.0110 | −0.0119 | −0.0173 | −0.0127 |

| (−0.66) | (−0.62) | (−0.66) | (−0.88) | (−0.69) | |

| STATE | −0.455 *** | −0.466 *** | −0.489 *** | −0.497 *** | −0.457 *** |

| (−4.05) | (−4.08) | (−3.96) | (−4.05) | (−4.03) | |

| GROW | 0.270 | 0.285 | 0.283 | 0.279 | 0.274 |

| (1.24) | (1.32) | (1.32) | (1.29) | (1.26) | |

| LNG | 0.564 *** | 0.565 *** | 0.572 *** | 0.590 *** | 0.562 *** |

| (5.11) | (5.10) | (5.22) | (5.50) | (5.12) | |

| YEAR | Control | ||||

| IND | Control | ||||

| cons | 5.743 *** | 5.463 *** | 5.436 *** | 5.506 *** | 5.401 *** |

| (5.53) | (5.90) | (5.88) | (4.87) | (5.70) | |

| N | 1743 | 1743 | 1743 | 1741 | 1743 |

| 0.151 | 0.149 | 0.149 | 0.151 | 0.151 | |

| F | 21.78 | 21.57 | 20.67 | 20.66 | 21.61 |

| One-Period Lag | Two-Period Lag | |||

|---|---|---|---|---|

| Heavily | Non-Heavily | Heavily | Non-Heavily | |

| L.LN_INV | −0.198 *** | −0.454 ** | ||

| (−3.04) | (−2.37) | |||

| L_LN_INV2 | 0.0217 *** | 0.0573 *** | ||

| (3.54) | (2.82) | |||

| L2.LN_INV | −0.0269 | −0.0639 | ||

| (−0.71) | (−0.55) | |||

| L2_LN_INV2 | 0.00424 | 0.0148 | ||

| (1.26) | (1.27) | |||

| avgLN_INV | ||||

| avgLN_INV2 | ||||

| SIZE | −0.678 *** | −0.301 *** | −0.615 *** | −0.288 ** |

| (−14.20) | (−3.24) | (−10.63) | (−2.28) | |

| LEV | −0.00498 | −0.516 *** | −0.232 | −0.382 |

| (−0.03) | (−2.89) | (−1.02) | (−1.61) | |

| FIRST | −0.525 *** | 0.520 | −0.423 * | 1.946 ** |

| (−2.99) | (1.22) | (−1.89) | (2.33) | |

| INS | 1.879 *** | 0.191 | 1.731 *** | −1.014 |

| (11.42) | (0.41) | (8.73) | (−1.02) | |

| YEARTURN | 0.0223 *** | 0.0104 | 0.0262 *** | 0.00377 |

| (2.76) | (0.86) | (2.70) | (0.22) | |

| STATE | −0.288 *** | −0.225 ** | −0.363 *** | −0.226 |

| (−5.90) | (−2.33) | (−6.40) | (−1.63) | |

| GROW | 0.407 *** | 0.115 | 0.530 *** | 0.161 |

| (4.12) | (0.87) | (4.46) | (0.91) | |

| LNG | 0.411 *** | 0.348 *** | 0.392 *** | 0.480 *** |

| (6.93) | (2.97) | (5.28) | (2.76) | |

| YEAR | Control | |||

| IND | Control | |||

| cons | 3.465 *** | 3.142 *** | 3.346 *** | 1.949 ** |

| N | 1603 | 202 | 1176 | 149 |

| N | 0.402 | 0.558 | 0.396 | 0.470 |

| 33.08 | 10.34 | 26.58 | 7.466 | |

References

- Chu, S.; Majumdar, A. Opportunities and challenges for a sustainable energy future. Nature 2012, 488, 294–303. [Google Scholar] [CrossRef] [PubMed]

- Soytas, U.; Sari, R. Energy consumption and GDP: Causality relationship in G-7 countries and emerging markets. Energy Econ. 2003, 25, 33–37. [Google Scholar] [CrossRef]

- Zhang, X.P.; Cheng, X.M. Energy consumption, carbon emissions, and economic growth in China. Ecol. Econ. 2009, 68, 2706–2712. [Google Scholar] [CrossRef]

- Apergis, N.; Payne, J.E. Energy consumption and economic growth in central America: Evidence from a panel cointegration and error correction model. Energy Econ. 2009, 31, 211–216. [Google Scholar] [CrossRef]

- Wu, Q.; Chen, G.; Han, J.; Wu, L. Does corporate ESG performance improve export intensity? evidence from Chinese listed firms. Sustainability 2022, 14, 12981. [Google Scholar] [CrossRef]

- Maqbool, S. An Empirical Examination of the Relationship between Corporate Social Responsibility and Profitability: Evidence from Indian Commercial Banks. Pac. Bus. Rev. Int. 2017, 09, 39–47. [Google Scholar]

- Zhang, F.; Qin, X.; Liu, L. The Interaction Effect between ESG and Green Innovation and Its Impact on Firm Value from the Perspective of Information Disclosure. Sustainability 2020, 12, 1866. [Google Scholar] [CrossRef] [Green Version]

- Yuan, B.; Xiang, Q. Environmental regulation, industrial innovation and green development of Chinese manufacturing: Based on an extended CDM model. J. Clean Prod. 2018, 176, 895–908. [Google Scholar] [CrossRef]

- Zhang, D.; Rong, Z.; Ji, Q. Green innovation and firm performance: Evidence from listed companies in China. Resour. Conserv. Recycl. 2019, 144, 48–55. [Google Scholar] [CrossRef]

- Lv, M.H.; Xu, G.H.; Shen, Y. Monetary Policy and Corporate Environmental Investment: Evidence from the Most Polluting Listed Companies in China. Bus. Manag. J. 2019, 41, 55–71. (In Chinese) [Google Scholar]

- Tang, G.P.; Li, L.H.; Wu, D.J. Environmental Regulation, Industry Attributes and Corporate Environmental Investment. Account. Res. 2013, 06, 83–89. (In Chinese) [Google Scholar]

- Li, Z.; Wang, W.H. Corporate Environmental Responsibility and Bank Credit: Text Analysis of Words and Deeds. J. Financ. Res. 2021, 12, 116–132. (In Chinese) [Google Scholar]

- Bhattacharyya, A.; Rahman, M.L. Mandatory CSR Expenditure and Firm Performance. J. Contemp. Account. Econ. 2019, 15, 100163. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A. Voluntary Non financial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Soc. Sci. Electr. Publ. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Buhr, N.; Freedman, M. Institutional Factors and Differences in Environmental Disclosure Between Canada and the United States. Crit. Perspect. Account. 2001, 12, 293–322. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G. Information Asymmetry, Corporate Disclosure, and the Capital Markets: A Review of The Empirical Disclosure Literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Leiter, A.M.; Parolini, A.; Winner, H. Environmental regulation and investment: Evidence from European industry data. Ecol. Econ. 2011, 70, 759–770. [Google Scholar] [CrossRef]

- Cao, Y.Y.; Yu, L.L. Government Control, Corporate Social Responsibility and Investment Efficiency: Samples of the Listed Companies during 2009~2011. Reform 2013, 7, 127–135. (In Chinese) [Google Scholar]

- Ma, H.; Zhang, J.; Ye, Z.Y. The impact of environmental regulation and property right on corporate environmental investment. J. Arid. L. Resour. Environ. 2016, 30, 47–52. (In Chinese) [Google Scholar]

- Jiang, X.M.; Xu, C.X. Environmental regulation, Corporate governance and environment protection investment. Financ. Account. Mon. 2015, 27, 9–13. (In Chinese) [Google Scholar]

- Tang, G.P.; Zhao, P.Q. Corporate governance and environment protection investment: A literature review. Friends Account. 2021, 13, 77–83. (In Chinese) [Google Scholar]

- Shan, C.X.; Zhong, W.Z. Research on the Influence of Environmental Protection Investment on Core Competitiveness of Coal Enterprises. East China Econ. Manag. 2018, 1, 137–144. (In Chinese) [Google Scholar]

- Tang, Y.J.; Ma, W.C.; Xia, L. Quality of Environmental Information Disclosure, Internal Control “Level” and Enterprise Value——Empirical Evidence from Listed Companies in Heavy Polluting Industries. Account. Res. 2021, 7, 69–84. (In Chinese) [Google Scholar]

- Li, X.T.; Song, C.; Guo, X.M. Enterprise-value Effect of Carbon Disclosure. Manag. Rev. 2017, 12, 175–184. (In Chinese) [Google Scholar]

- Shen, H.; Feng, J. Media Monitoring, Government Supervision, and Corporate Environmental Disclosure. Account. Res. 2012, 2, 72–78. (In Chinese) [Google Scholar]

- Hassel, L.; Nilsson, H.; Nyquist, S. The Value Relevance of Environmental Performance. Eur. Account. Rev. 2005, 14, 41–61. [Google Scholar] [CrossRef]

- Bird, R.; Hall, A.D.; Francesco, M.; Francesco, R. What corporate social responsibility activities are valued by the market? J. Bus. Ethics 2007, 76, 189–206. [Google Scholar] [CrossRef]

- Lioui, A.; Sharma, Z. Environmental Corporate Social Responsibility and Financial Performance: Disentangling Direct and Indirect Effects. Ecol. Econ. 2012, 78, 100–111. [Google Scholar] [CrossRef]

- Chen, L. The Debate of International Strategy and Firm Performance Relationship: A Review of Global Research. Nankai Bus. Rev. 2014, 17, 112–125. (In Chinese) [Google Scholar]

- Zhu, J.F.; Qiao, Y.H. An Empirical Research on the Relationship Between Corporate Profitability and Level of Corporate Environmental Protection Information Disclosure. China Popul. Resour. Environ. 2008, 4, 206–210. (In Chinese) [Google Scholar]

- Peng, F.; Li, B.D. Analysis of Environment Protection Investment. Environ. Sci. Technol. 2005, 3, 72–74. (In Chinese) [Google Scholar]

- Palmer, K.; Oates, W.E.; Portney, P.R. Tightening Environmental Standards: The Benefit-Cost or the No-Cost Paradigm. J. Econ. Perspect. 1995, 9, 119–132. [Google Scholar] [CrossRef]

- Filbeck, G.; Gorman, R.F. The Relationship between the Environmental and Financial Performance of Public Utilities. Environ. Resour. Econ. 2004, 29, 137–157. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E.; Linde, C. Toward a New Conception of The Environment- Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef] [Green Version]

- Konar, S.; Cohen, M. Information as Regulation: The Effect of Community Right to Know Laws on Toxic Emissions. J. Environ. Econ. Manag. 1997, 32, 109–124. [Google Scholar] [CrossRef] [Green Version]

- Cui, X.M.; Wang, J.Y.; Wang, M. Environmental Investment, CEOs with Overseas Experiences and the Value of Enterprises: Increase or Decrease? An Analysis from the Perspective of Imprinting Theory. J. Audit. Econ. 2021, 36, 86–94. (In Chinese) [Google Scholar]

- Zhang, Z.; Duan, Y. Government Supervision, Openness of Economy, and Environmental Information Disclosure: Empirical Analysis of Highly Polluted Industry in China. J. Nanjing Univ. 2019, 1, 78–87. [Google Scholar]

- Zhang, J.Z.; Li, H.Y.; Li, T.; Li, Y. Thoughts on Improving the Environmental Information on Disclosure System of Listed Companies in China. Environ. Prot. 2017, 45, 36–39. (In Chinese) [Google Scholar]

- Wang, L.; Qu, J.; Liu, X.M. Heterogeneous Institutional Investor Portfolio, Environmental Information Disclosure and Corporate Value. J. Manag. Sci. 2019, 32, 31–47. (In Chinese) [Google Scholar]

- Ezzeddine, B.M.; Nassreddine, G.; Kamel, N. Do optimistic managers destroy firm value? J. Behav. Exp. Financ. 2020, 14, 100292. [Google Scholar]

- Lu, Y.T.; Wang, J.N.; Wu, S.Z.; Su, M.; Zhu, J.H. An Analysis on Statistical Indicators and Methodology of Environmental Investments in China. China Popul. Resour. Environ. 2010, 20, 96–99. (In Chinese) [Google Scholar]

- Meng, F.L. Environmental accounting information disclosure and related theoretical issues are discussed. Account. Res. 1999, 4, 17–26. (In Chinese) [Google Scholar]

- Zhang, Q.; Zheng, Y.; Kong, D.M. Local Environmental Governance Pressure, Executive’s Working Experience and Enterprise Investment in Environmental Protection: A Quasi-natural Experiment Based on China’s “Ambient Air Quality Standards 2012”. Econ. Res. J. 2019, 54, 183–198. (In Chinese) [Google Scholar]

- Li, G.R.; Wen, S.H.; Wang, L.N. The Influence of Corporate Environmental Responsibility on Enterprise Value under Different Property Rights. J. Hebei Univ. Econ. Bus. 2019, 40, 92–100. (In Chinese) [Google Scholar]

- Lin, H.; Zeng, S.X.; Ma, H.Y.; Chen, H.Q. How Political Connections Affect Corporate Environmental Performance: The Mediating Role of Green Subsidies. Hum. Ecol. Risk Assess. 2015, 21, 2192–2212. [Google Scholar] [CrossRef]

- Bai, C.N.; Liu, Q.; Lu, Z.; Song, M.; Zhang, J.X. An Empirical Study on Chinese Listed Firms’ Corporate Governance. Econ. Res. J. 2005, 2, 81–91. (In Chinese) [Google Scholar]

- Lu, H.Y.; Deng, T.Q.; Yu, J.L. Can Financial Subsidies Promote the "Greening" of Enterprises? Research on Listed Companies from Heavy Pollution Industry in China. Bus. Manag. J. 2019, 41, 5–22. (In Chinese) [Google Scholar]

- Tang, G.P.; Li, L.H. Corporate information disclosure, Investor confidence and Firm Value: Empirical evidence from listed companies in Hubei Province. J. Zhongnan Univ. Econ. Law 2011, 6, 70–77. (In Chinese) [Google Scholar]

- Wang, J.M. Research on the Correlation among Environmental Information Disclosure, Industry Differences and Supervisory System. Account. Res. 2008, 6, 54–62. (In Chinese) [Google Scholar]

- Clarkson, P.M.; Yue, L.; Richardson, G.D. Revisiting The Relation between Environmental Performance And Environmental Disclosure: An Empirical Analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Wu, H.J. Disclosure of Environmental Information, Environmental Performance and Cost of, Equity Capital. J. Xiamen Univ. (Arts Soc. Sci.) 2014, 3, 129–138. (In Chinese) [Google Scholar]

- Ren, L.; Hong, Z. A Study on The Channel Through Which Environmental Disclosure Influence Firm Value. Bus. Manag. J. 2017, 39, 34–47. (In Chinese) [Google Scholar]

- Law, S.H.; Kutan, A.M.; Naseem, N.M. The Role of Institutions in Finance Curse: Evidence from International Data. J. Comp. Econ. 2018, 46, 174–191. [Google Scholar] [CrossRef]

- Li, H.; Wang, R.K.; Xu, N.N. Research on the Relationship between Management Capability and Corporate Environmental Investment—Based on the Perspective of Moderating Effect of Market Competition and Nature of Property Right. East China Econ. Manag. 2017, 31, 136–143. (In Chinese) [Google Scholar]

- Zhang, X.J.; Xu, J.; Xu, L.B. Can Elite Governance of Senior Executives Improve Performance? Based on the Adjustment Effect of Social Connections. Econ. Res. J. 2015, 50, 100–114. (In Chinese) [Google Scholar]

- Lind, J.T.; Mehlum, H. With or without U? The Appropriate Test for a U-Shaped Relationship. Oxf. Bull. Econ. Stat. 2010, 72, 109–118. [Google Scholar] [CrossRef] [Green Version]

- Zhu, D.; Zhou, S.H. Strategic Change, Internal Control and Firm Performance. J. Cent. Univ. Financ. Econ. 2018, 2, 53–64. (In Chinese) [Google Scholar]

- Dou, X.F. The Lagging Effects of the Influence of Corporate Social Responsibility on Corporate Financial Performance—Empirical Analysis Based on the Panel Data of Chinese Listed Companies. Econ. Res. J. 2015, 3, 74–81. (In Chinese) [Google Scholar]

- Tang, Y.J.; Xia, L. Environmental Investment, Environmental Information Disclosure Quality and Corporate Value. Sci. Technol. Manag. Res. 2019, 39, 256–264. (In Chinese) [Google Scholar]

| Year | Obs. | Proportion of Obs. | Growth Rate |

|---|---|---|---|

| 2010 | 122 | 5.02% | - |

| 2011 | 153 | 6.30% | 25.41% |

| 2012 | 184 | 7.57% | 20.26% |

| 2013 | 188 | 7.74% | 2.17% |

| 2014 | 187 | 7.70% | −0.53% |

| 2015 | 198 | 8.15% | 5.88% |

| 2016 | 211 | 8.68% | 6.57% |

| 2017 | 240 | 9.88% | 13.74% |

| 2018 | 296 | 12.18% | 23.33% |

| 2019 | 315 | 12.96% | 6.42% |

| 2020 | 336 | 13.83% | 6.67% |

| Total | 2430 | 100.00% | - |

| Variable | N | Min | Mean | Median | Max | Std. Dev. |

|---|---|---|---|---|---|---|

| PANEL A: Non-heavily polluting industry | ||||||

| 281 | 0.86 | 1.72 | 1.50 | 7.58 | 0.89 | |

| 281 | 0.12 | 4.46 | 4.62 | 8.69 | 1.76 | |

| 281 | 1.57 | 4.06 | 4.11 | 6.96 | 1.02 | |

| 281 | 0.07 | 0.47 | 0.49 | 0.95 | 0.21 | |

| 281 | 0.08 | 0.39 | 0.40 | 0.75 | 0.16 | |

| 281 | 0.01 | 0.46 | 0.47 | 0.89 | 0.21 | |

| 281 | 0.46 | 4.98 | 3.73 | 23.33 | 4.07 | |

| 281 | 0.00 | 0.59 | 1.00 | 1.00 | 0.49 | |

| 281 | −0.54 | 0.12 | 0.08 | 1.41 | 0.39 | |

| 281 | 0.50 | 1.65 | 1.59 | 2.93 | 0.52 | |

| PANEL B: Heavily polluting industry | ||||||

| 2149 | 0.86 | 1.89 | 1.52 | 7.58 | 1.15 | |

| 2149 | 0.12 | 5.21 | 5.30 | 8.99 | 1.78 | |

| 2149 | 1.57 | 4.00 | 3.88 | 6.96 | 1.23 | |

| 2149 | 0.07 | 0.45 | 0.44 | 0.95 | 0.20 | |

| 2149 | 0.08 | 0.36 | 0.34 | 0.75 | 0.15 | |

| 2149 | 0.00 | 0.43 | 0.44 | 0.89 | 0.23 | |

| 2149 | 0.46 | 5.50 | 4.25 | 23.33 | 4.35 | |

| 2149 | 0.00 | 0.45 | 0.00 | 1.00 | 0.50 | |

| 2149 | −0.54 | 0.13 | 0.09 | 1.41 | 0.29 | |

| 2149 | 0.50 | 1.64 | 1.59 | 3.30 | 0.66 | |

| 2149 | 0.86 | 1.89 | 1.52 | 7.58 | 1.15 | |

| TOTAL | ||||||

| 2430 | 0.86 | 1.87 | 1.52 | 7.58 | 1.12 | |

| 2430 | 0.12 | 5.12 | 5.21 | 8.99 | 1.79 | |

| 2430 | 1.57 | 4.00 | 3.90 | 6.96 | 1.21 | |

| 2430 | 0.07 | 0.45 | 0.44 | 0.95 | 0.20 | |

| 2430 | 0.08 | 0.36 | 0.35 | 0.75 | 0.15 | |

| 2430 | 0.00 | 0.43 | 0.44 | 0.89 | 0.22 | |

| 2430 | 0.46 | 5.44 | 4.21 | 23.33 | 4.32 | |

| 2430 | 0.00 | 0.46 | 0.00 | 1.00 | 0.50 | |

| 2430 | −0.54 | 0.13 | 0.08 | 1.41 | 0.30 | |

| 2430 | 0.50 | 1.64 | 1.59 | 3.30 | 0.64 | |

| Construction | Indicator | Description |

|---|---|---|

| Environmental Management Disclosure (MD) | Environmental Concept | Disclose the company’s environmental protection concept, environmental policy, environmental management structure, whether the economic development is recyclable, green development, etc., with a value of 1, otherwise 0. |

| Environmental Target | Disclose the completion of the company’s existing environmental protection goals and future environmental protection goals, assign a value of 1, otherwise 0. | |

| Environmental Protection Management System | Disclose that the company has established a series of management systems, systems, regulations, responsibilities, and other relevant environmental management systems, with a value of 1, otherwise 0. | |

| Environmental Education and Training | Disclose the company’s participation in environmental-related education and training, assign a value of 1, otherwise 0. | |

| Special Action on Environmental Protection | Disclose the company’s participation in environmental protection special activities, environmental protection, and other social public welfare activities, assign a value of 1, otherwise 0. | |

| Emergency Mechanism for Environmental Events | Disclose the company’s establishment of an emergency mechanism for major environment-related emergencies, the emergency measures taken and the treatment of pollutants, etc., assign a value of 1, otherwise 0. | |

| Environmental Honors or Awards | Disclose the company’s environmental honors or awards with a value of 1, otherwise 0. | |

| “Three Synchronizations” System | Disclose the company’s implementation of the “Three Synchronizations“ System, assign a value of 1, otherwise 0 | |

| Environmental Supervision and Certification Disclosure (SD) | Key Pollution Monitoring Unit | The disclosure company is the key monitoring unit, with a value of 1, otherwise 0. |

| Pollutant Discharge under Certain Standards | The value of the pollutant emission standard is 1, otherwise, it is 0. | |

| Sudden Environmental Accident | If there is a sudden major environmental pollution event, the value is 1, otherwise, it is 0. | |

| Environmental Violations | If environmental violations have occurred, the value is 1, otherwise 0. | |

| Environmental Petition Cases | If there is an environmental petition event, the value is 1, otherwise, it is 0. | |

| Whether it has passed ISO14001 certification | Pass ISO14001, assign a value of 1, otherwise 0. | |

| Whether it has passed ISO9001 certification | Pass ISO19001, assign a value of 1, otherwise 0. | |

| Entry Environmental Liability Disclosure (LD) | Quantity of Wastewater Effluent | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). |

| COD Emissions | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Sulfur Dioxide Emissions | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| CO2 Emissions | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Soot and Dust Emissions | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Production of Industrial Solid Waste | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Environmental Performance and Governance Disclosure (PD) | Treatment of Emission Reduction in Waste Gas | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). |

| Emission Reduction and Treatment of Wastewater | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Dust and Smoke Control Situation | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Utilization and Disposal of Solid Waste | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| Noise, Light Pollution and Radiation Control | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). | |

| The Implementation of Cleaner Production | 0 = no description; 1 = qualitative description; 2 = Quantitative description (monetary/numerical description). |

| Variable | N | Min | Mean | Median | Max | Std. Dev. |

|---|---|---|---|---|---|---|

| Tobin QA | 1848 | 0.87 | 1.88 | 1.51 | 7.61 | 1.13 |

| LN_INV | 1848 | 0.09 | 5.16 | 5.25 | 8.99 | 1.79 |

| DIS | 1848 | 0.00 | 0.94 | 1.00 | 1.00 | 0.23 |

| EDI | 1743 | 0.00 | 0.23 | 0.21 | 0.85 | 0.19 |

| LD | 1743 | 0.00 | 0.18 | 0.08 | 0.92 | 0.22 |

| MD | 1743 | 0.00 | 0.25 | 0.12 | 1.00 | 0.25 |

| SD | 1741 | 0.00 | 0.27 | 0.29 | 0.71 | 0.14 |

| PD | 1743 | 0.00 | 0.25 | 0.25 | 1.00 | 0.25 |

| SIZE | 1848 | 1.55 | 3.97 | 3.86 | 6.84 | 1.22 |

| LEV | 1848 | 0.07 | 0.45 | 0.44 | 0.95 | 0.20 |

| FIRST | 1848 | 0.08 | 0.36 | 0.34 | 0.75 | 0.15 |

| INS | 1848 | 0.00 | 0.42 | 0.44 | 0.88 | 0.22 |

| YEARTURN | 1848 | 0.50 | 5.33 | 4.11 | 23.37 | 4.23 |

| STATE | 1848 | 0.00 | 0.46 | 0.00 | 1.00 | 0.50 |

| GROW | 1848 | −0.52 | 0.14 | 0.09 | 1.47 | 0.29 |

| LNG | 1848 | 0.50 | 1.64 | 1.59 | 3.30 | 0.66 |

| Heavily Polluting Industry | Non-Heavily Polluting Industry | |||

|---|---|---|---|---|

| (1) Tobin Q | (2) Tobin Q | (3) Tobin Q | (4) Tobin Q | |

| LN_INV | −0.005 | −0.200 *** | 0.030 | −0.376 *** |

| (−0.34) | (−3.77) | (1.01) | (−3.15) | |

| 0.021 *** | 0.050 *** | |||

| (4.11) | (3.80) | |||

| SIZE | −0.682 *** | −0.705 *** | −0.325 *** | −0.361 *** |

| (−16.86) | (−17.04) | (−4.26) | (−4.73) | |

| LEV | −0.0263 | −0.0107 | −0.659 *** | −0.619 *** |

| (−0.16) | (−0.07) | (−2.83) | (−3.00) | |

| FIRST | −0.530 *** | −0.554 *** | −0.281 | −0.293 |

| (−3.54) | (−3.69) | (−0.59) | (−0.69) | |

| INS | 1.991 *** | 1.971 *** | 0.495 | 0.554 |

| (14.36) | (14.19) | (1.12) | (1.36) | |

| YEARTURN | 0.010 * | 0.010 | 0.002 | 0.006 |

| (1.69) | (1.61) | (0.16) | (0.53) | |

| STATE | −0.285 *** | −0.270 *** | −0.164 | −0.191 ** |

| (−6.30) | (−5.97) | (−1.59) | (−2.10) | |

| GROW | 0.337 *** | 0.348 *** | −0.005 | 0.042 |

| (3.94) | (4.15) | (−0.04) | (0.35) | |

| LNG | 0.467 *** | 0.466 *** | 0.310 *** | 0.240 ** |

| (8.90) | (8.97) | (2.79) | (2.16) | |

| YEAR | Control | |||

| IND | Control | |||

| cons | 3.453 *** | 3.967 *** | 3.563 *** | 4.545 *** |

| (23.36) | (18.93) | (7.67) | (7.32) | |

| N | 2149 | 2149 | 281 | 281 |

| 0.408 | 0.414 | 0.442 | 0.498 | |

| F | 43.48 | 42.36 | - | - |

| Dependent Variable: Tobin QA | Heavily Polluting | Non-Heavily Polluting | |

|---|---|---|---|

| −0.200 *** | −0.376 *** | ||

| (−3.77) | (−3.15) | ||

| 0.0206 *** | 0.0496 *** | ||

| (4.11) | (3.80) | ||

| slope at | −0.195 | −0.364 | |

| 0.000 | 0.001 | ||

| slope at | 0.0171 | 0.515 | |

| 0.000 | 0.000 | ||

| Extreme point | 4.841 | 3.794 | |

| confidence interval (99%) | [3.533, 5.825] | [1.907, 4.562] | |

| Tobin QA (EDI) | Tobin QA (LD) | Tobin QA (MD) | Tobin QA (SD) | Tobin QA (PD) | |

|---|---|---|---|---|---|

| LN_INV | −0.260 *** | −0.233 *** | −0.232 *** | −0.373 *** | −0.201 ** |

| (−2.77) | (−3.07) | (−2.97) | (−3.18) | (−2.26) | |

| 0.0234 *** | 0.0230 *** | 0.0217 *** | 0.0353 *** | 0.0179 ** | |

| (2.61) | (3.16) | (2.90) | (3.30) | (2.09) | |

| EDI | −2.338 *** | ||||

| (−2.84) | |||||

| LN_INV*EDI | 0.646 ** | ||||

| (2.29) | |||||

| *EDI | −0.0412 * | ||||

| (−1.73) | |||||

| LD | −1.525 ** | ||||

| (−2.28) | |||||

| LN_INV*LD | 0.465 ** | ||||

| (2.05) | |||||

| *LD | −0.0328 * | ||||

| (−1.72) | |||||

| MD | −1.707 *** | ||||

| (−2.64) | |||||

| LN_INV*MD | 0.499 ** | ||||

| (2.29) | |||||

| *MD | −0.0333 * | ||||

| (−1.85) | |||||

| SD | −2.755 *** | ||||

| (−2.78) | |||||

| LN_INV*SD | 0.834 ** | ||||

| (2.37) | |||||

| *SD | −0.0675 ** | ||||

| (−2.22) | |||||

| PD | −1.303 ** | ||||

| (−2.10) | |||||

| LN_INV*PD | 0.306 | ||||

| (1.41) | |||||

| *PD | −0.0141 | ||||

| (−0.75) | |||||

| SIZE | −0.771 *** | −0.773 *** | −0.770 *** | −0.774 *** | −0.773 *** |

| (−17.01) | (−16.93) | (−16.97) | (−17.01) | (−17.01) | |

| LEV | 0.204 | 0.195 | 0.186 | 0.190 | 0.209 |

| (1.18) | (1.13) | (1.08) | (1.11) | (1.20) | |

| FIRST | −0.553 *** | −0.572 *** | −0.540 *** | −0.495 *** | −0.561 *** |

| (−3.61) | (−3.72) | (−3.56) | (−3.26) | (−3.65) | |

| INS | 1.806 *** | 1.813 *** | 1.808 *** | 1.780 *** | 1.802 *** |

| (13.52) | (13.54) | (13.51) | (13.26) | (13.46) | |

| YEARTURN | −0.00156 | −0.00138 | −0.00147 | −0.00349 | −0.00188 |

| (−0.27) | (−0.24) | (−0.25) | (−0.59) | (−0.33) | |

| STATE | −0.204 *** | −0.208 *** | −0.212 *** | −0.217 *** | −0.203 *** |

| (−4.15) | (−4.20) | (−4.34) | (−4.53) | (−4.18) | |

| GROW | 0.238 *** | 0.243 *** | 0.240 *** | 0.239 *** | 0.240 *** |

| (2.77) | (2.82) | (2.81) | (2.81) | (2.79) | |

| LNG | 0.489 *** | 0.490 *** | 0.490 *** | 0.497 *** | 0.488 *** |

| (8.75) | (8.70) | (8.78) | (8.89) | (8.74) | |

| YEAR | Control | ||||

| IND | Control | ||||

| cons | 3.814 *** | 3.689 *** | 3.704 *** | 3.678 *** | 3.678 *** |

| (12.91) | (14.11) | (13.91) | (10.89) | (13.04) | |

| N | 1743 | 1743 | 1743 | 1741 | 1743 |

| 0.470 | 0.468 | 0.469 | 0.471 | 0.470 | |

| F | 34.31 | 33.72 | 33.54 | 33.10 | 34.25 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, K.; Cui, W.; Mei, M.; Lv, B.; Peng, G. The Moderating Role of Environmental Information Disclosure on the Impact of Environment Protection Investment on Firm Value. Sustainability 2023, 15, 9174. https://doi.org/10.3390/su15129174

Wang K, Cui W, Mei M, Lv B, Peng G. The Moderating Role of Environmental Information Disclosure on the Impact of Environment Protection Investment on Firm Value. Sustainability. 2023; 15(12):9174. https://doi.org/10.3390/su15129174

Chicago/Turabian StyleWang, Kedan, Wenjia Cui, Mei Mei, Benfu Lv, and Geng Peng. 2023. "The Moderating Role of Environmental Information Disclosure on the Impact of Environment Protection Investment on Firm Value" Sustainability 15, no. 12: 9174. https://doi.org/10.3390/su15129174