Oil and Non-Oil Determinants of Saudi Arabia’s International Competitiveness: Historical Analysis and Policy Simulations

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Background and Empirical Model of Saudi REER

3.1. Theoretical Background

3.2. Empirical Model of Saudi REER

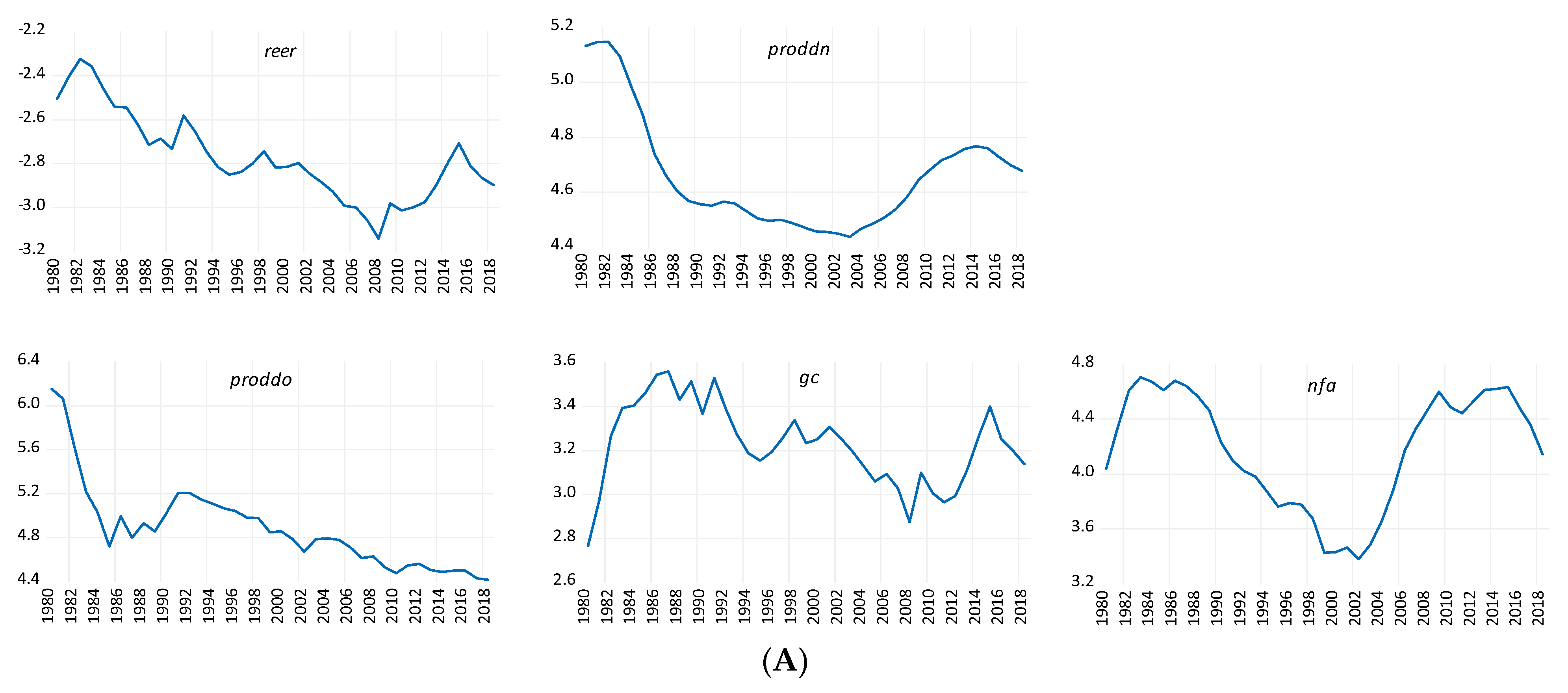

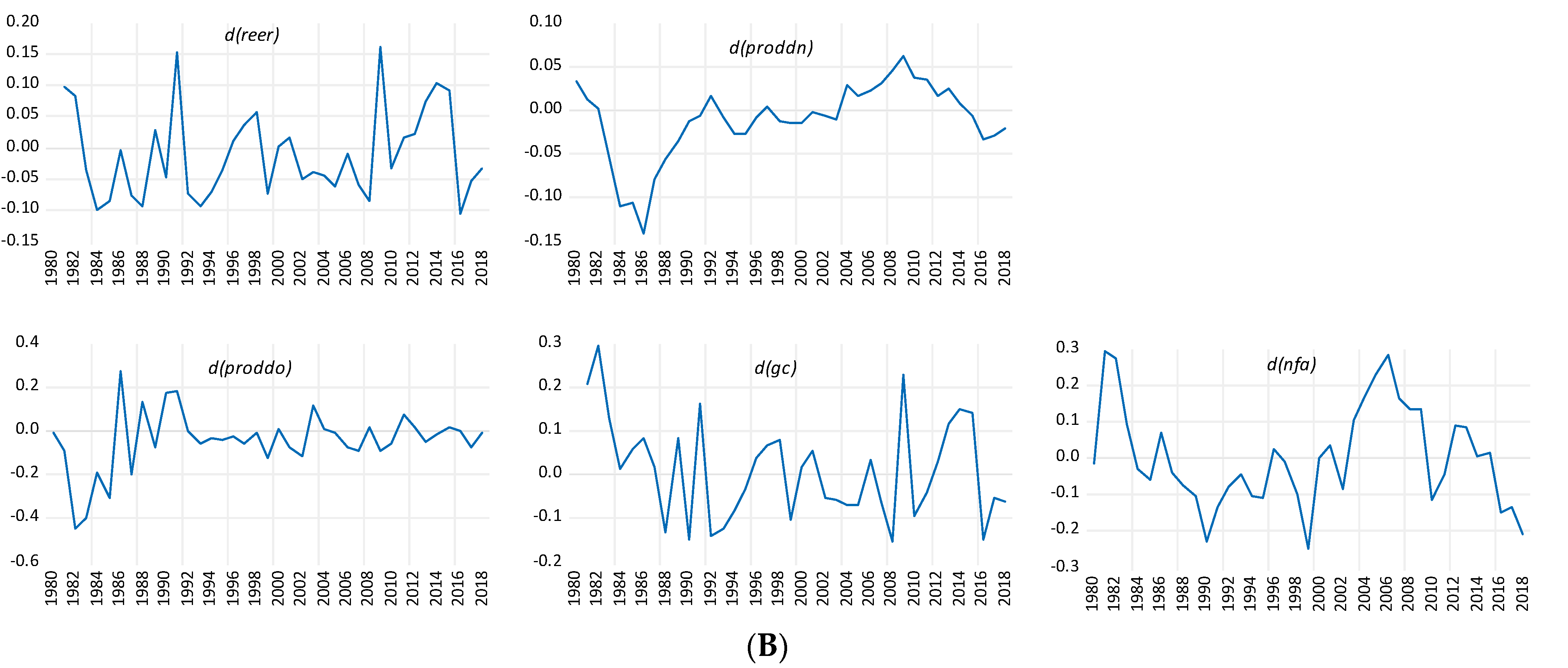

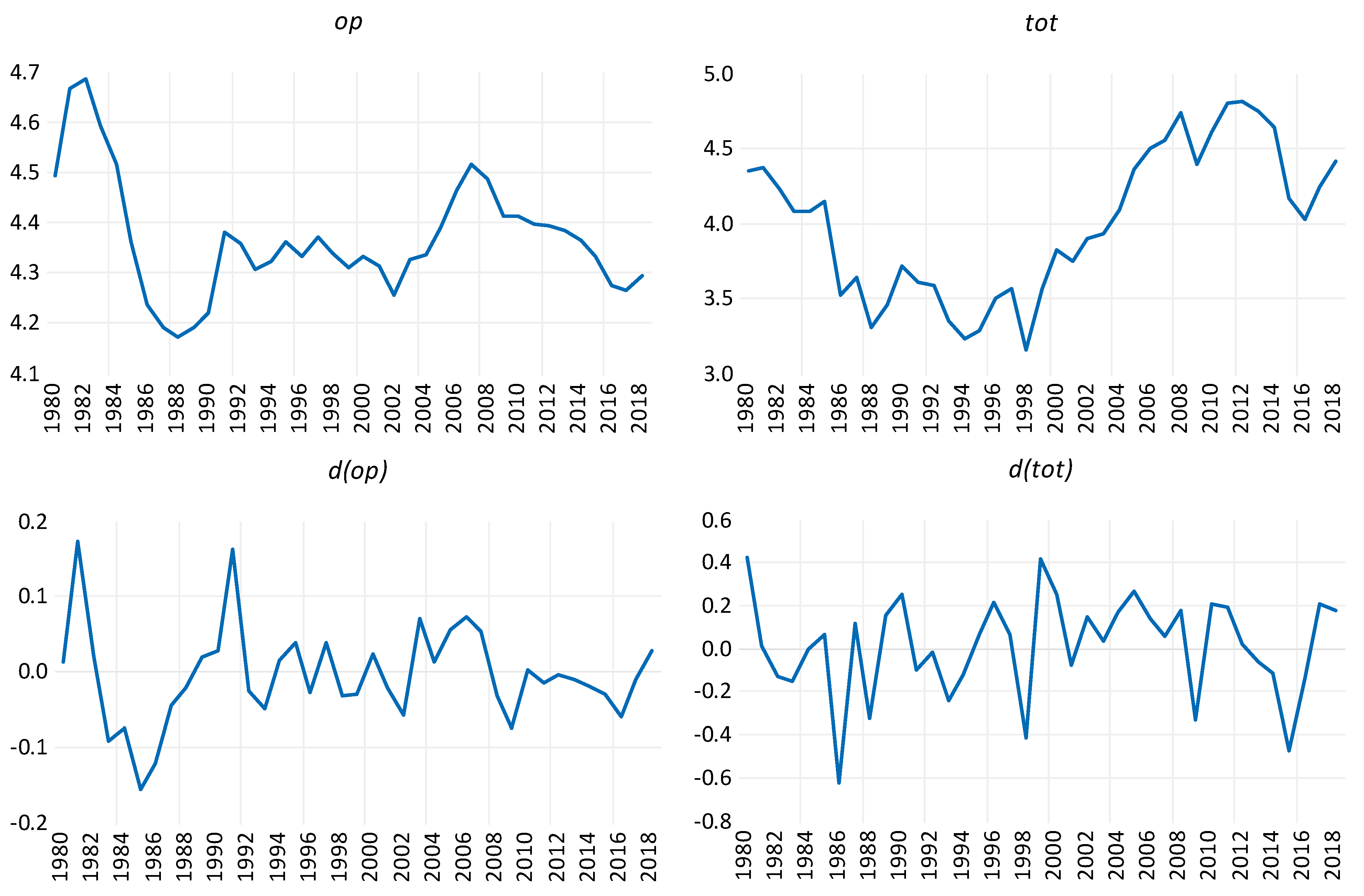

4. Data

5. Econometric Methodology

6. Results of the Empirical Analysis and Robustness Checks

6.1. Unit Root Test Results

6.2. Cointegration Test and Long-Run Estimation Results

6.3. Additional Robustness Checks

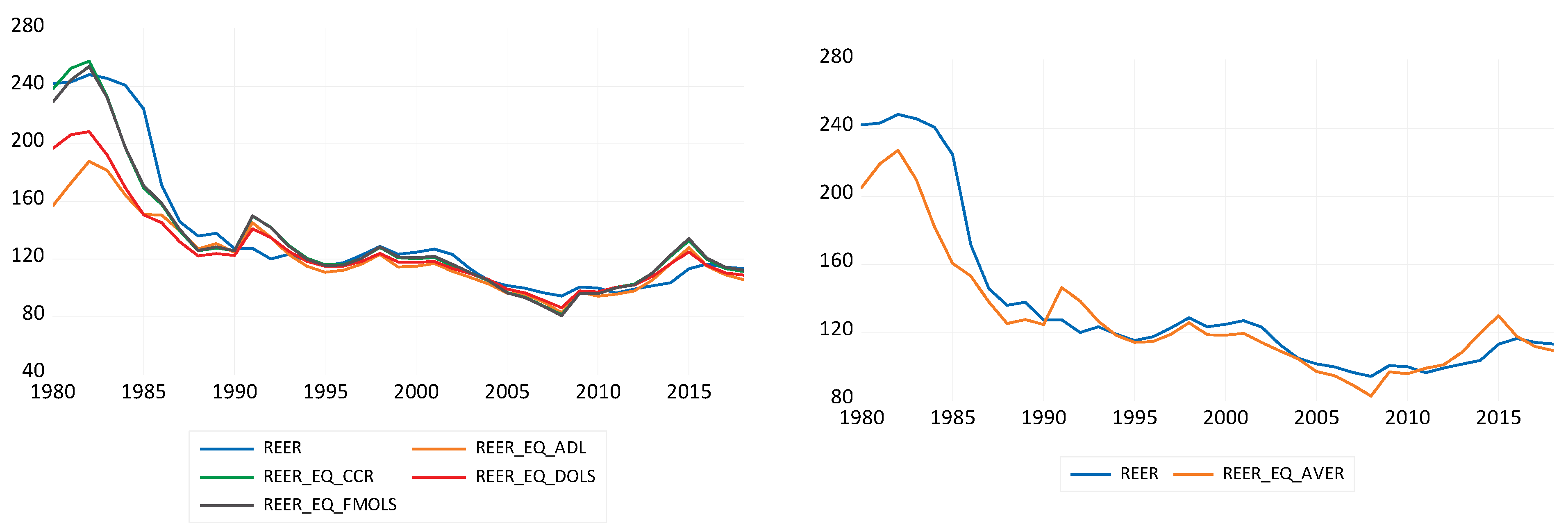

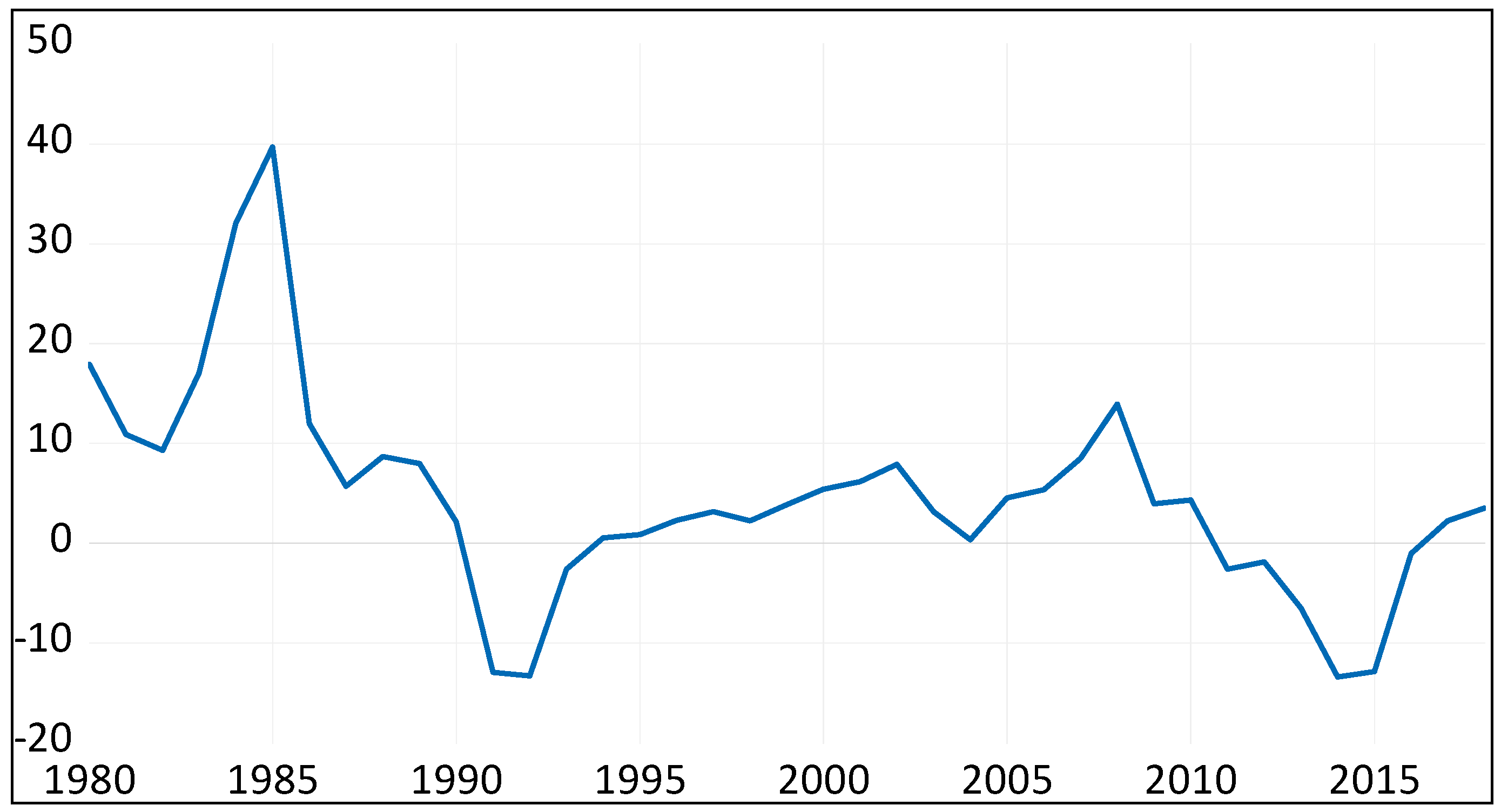

6.4. Equilibrium REER and Currency Misalignment

7. Discussion

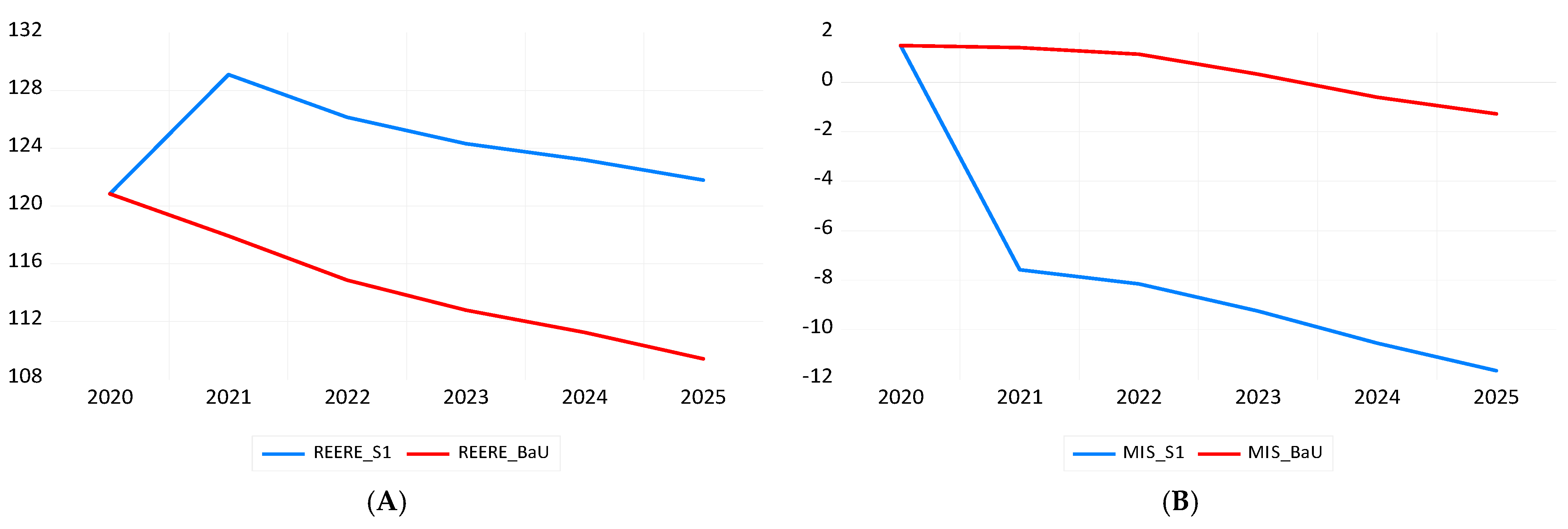

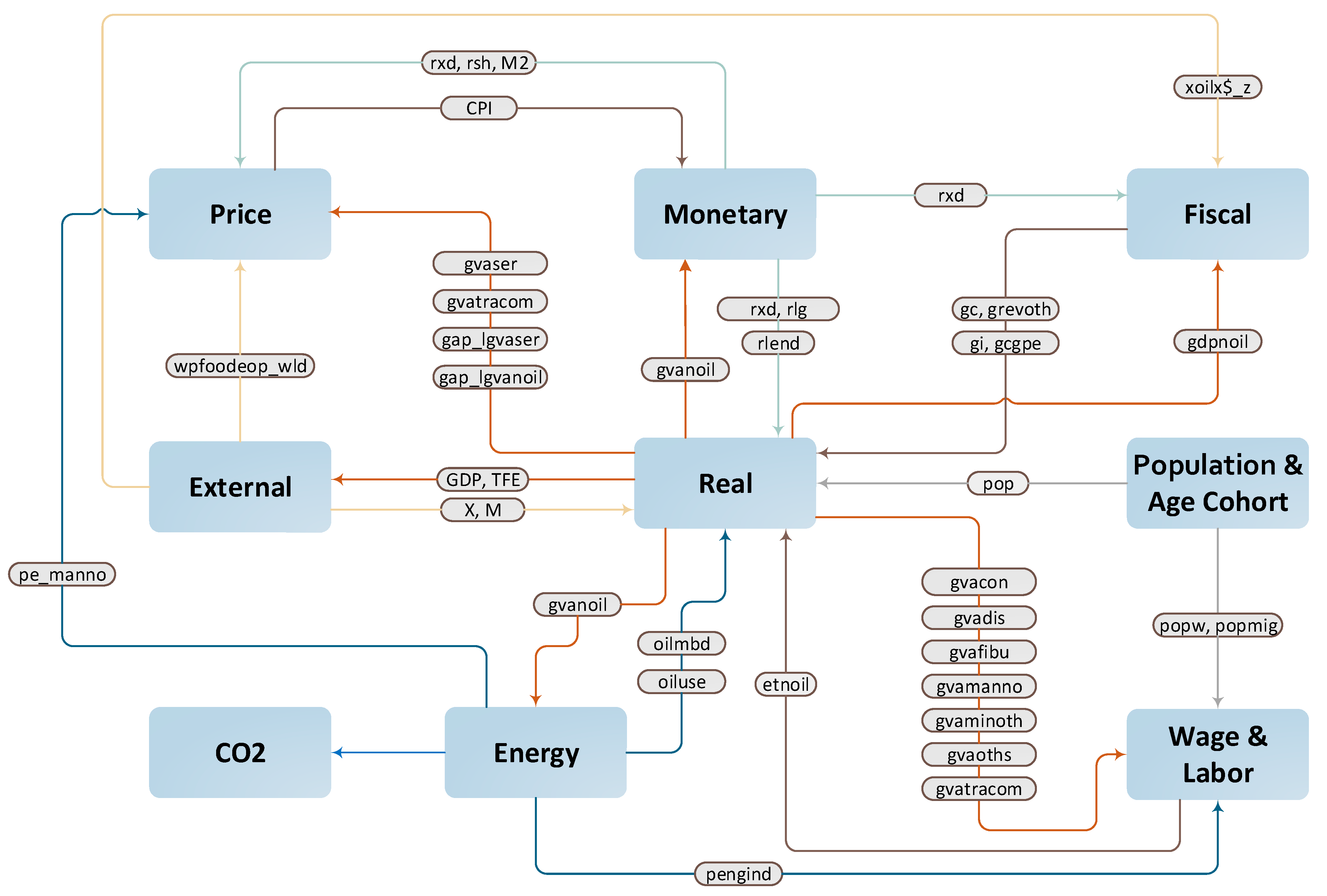

8. Policy Simulation Analysis Using KGEMM

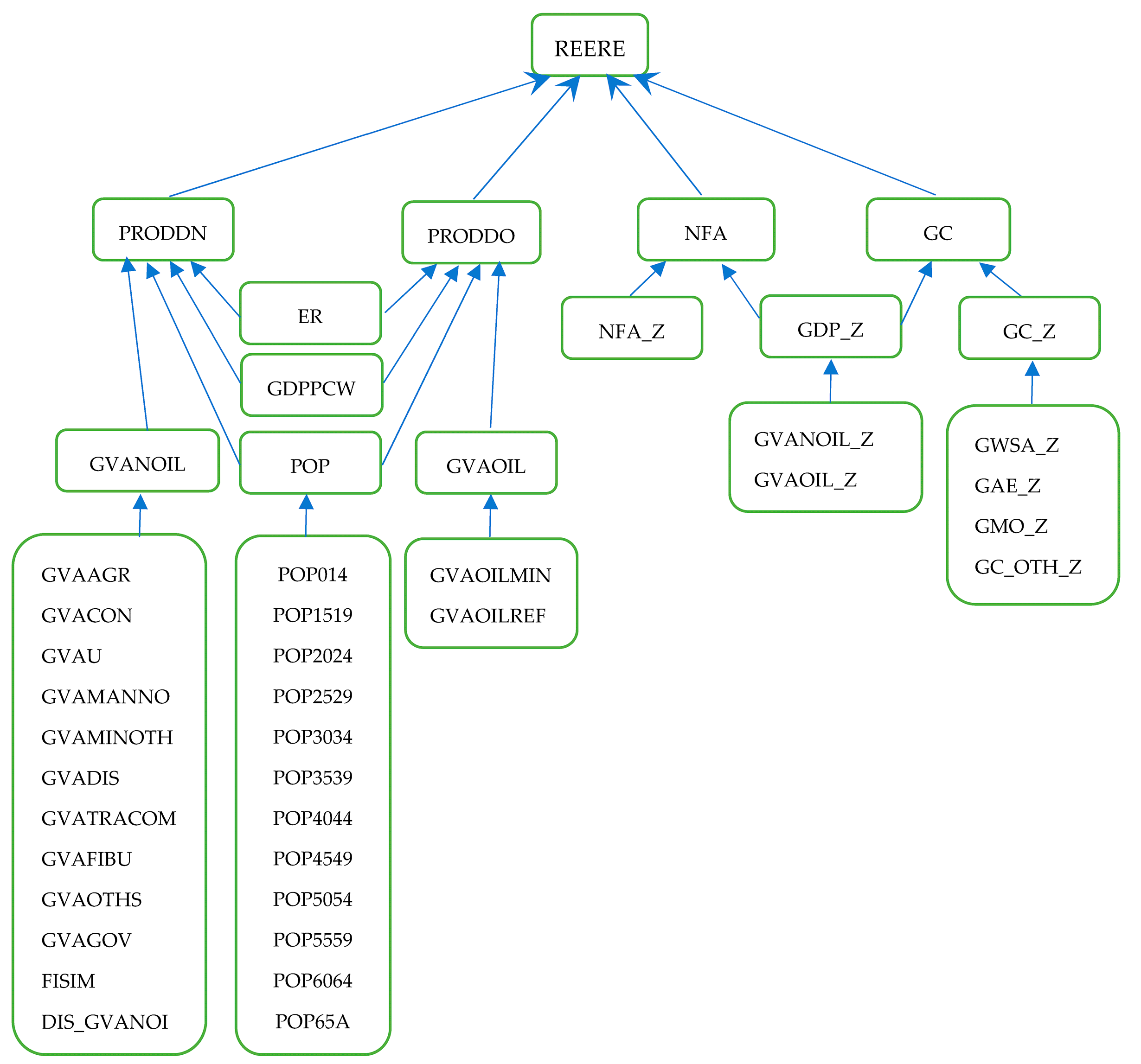

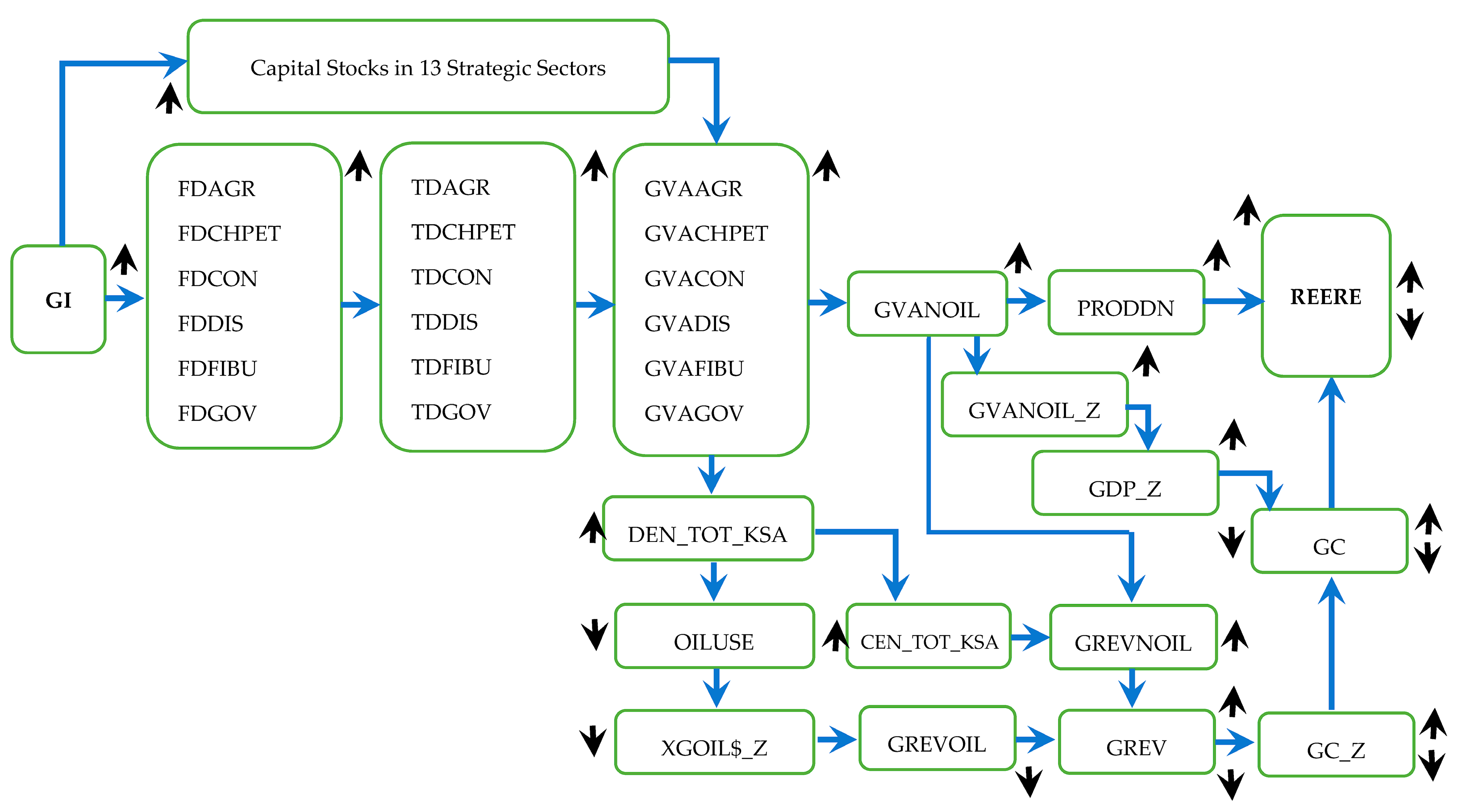

8.1. Brief Overview of the KGEMM and REERE Linkages

8.2. Assumptions for the Simulations and Policy Context

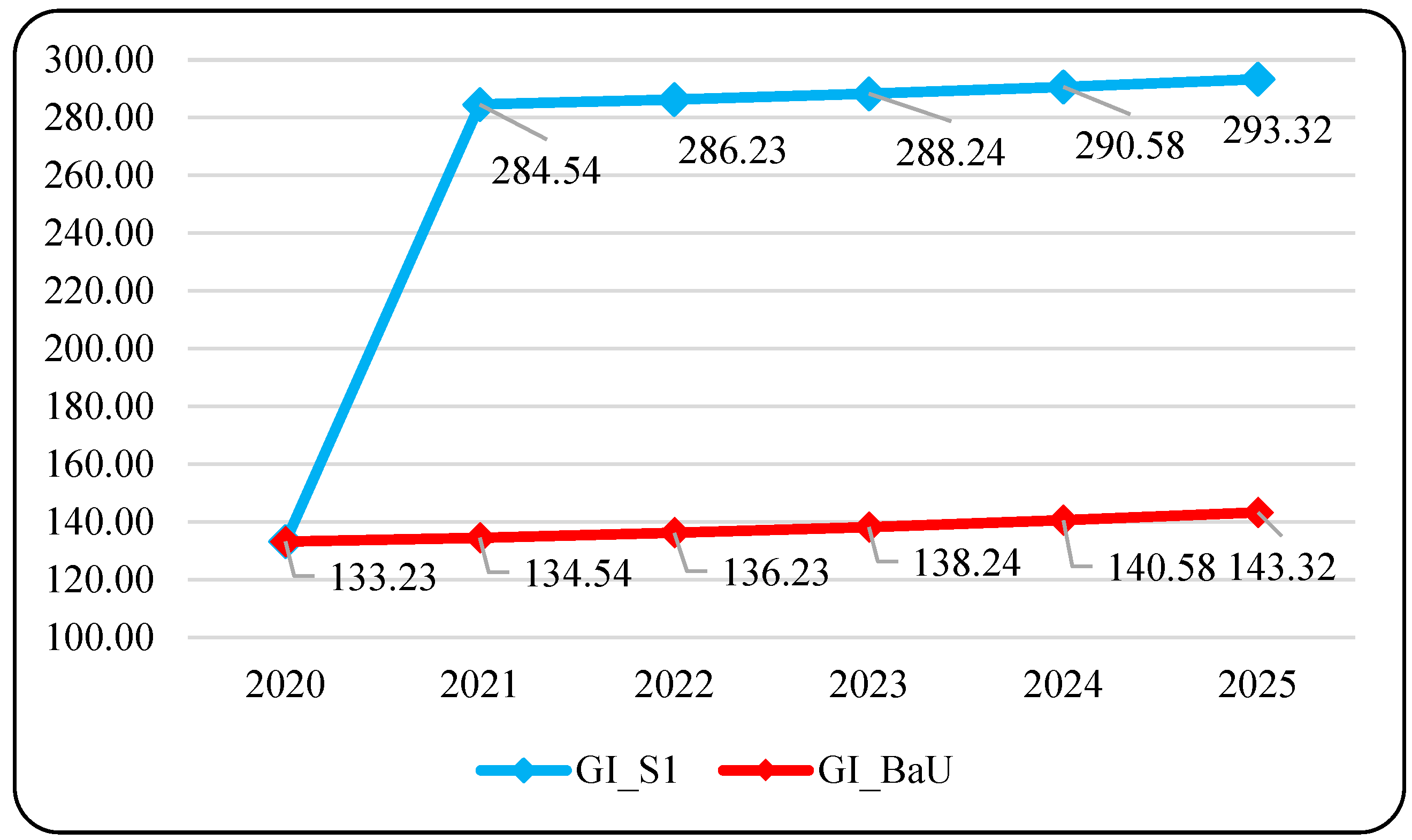

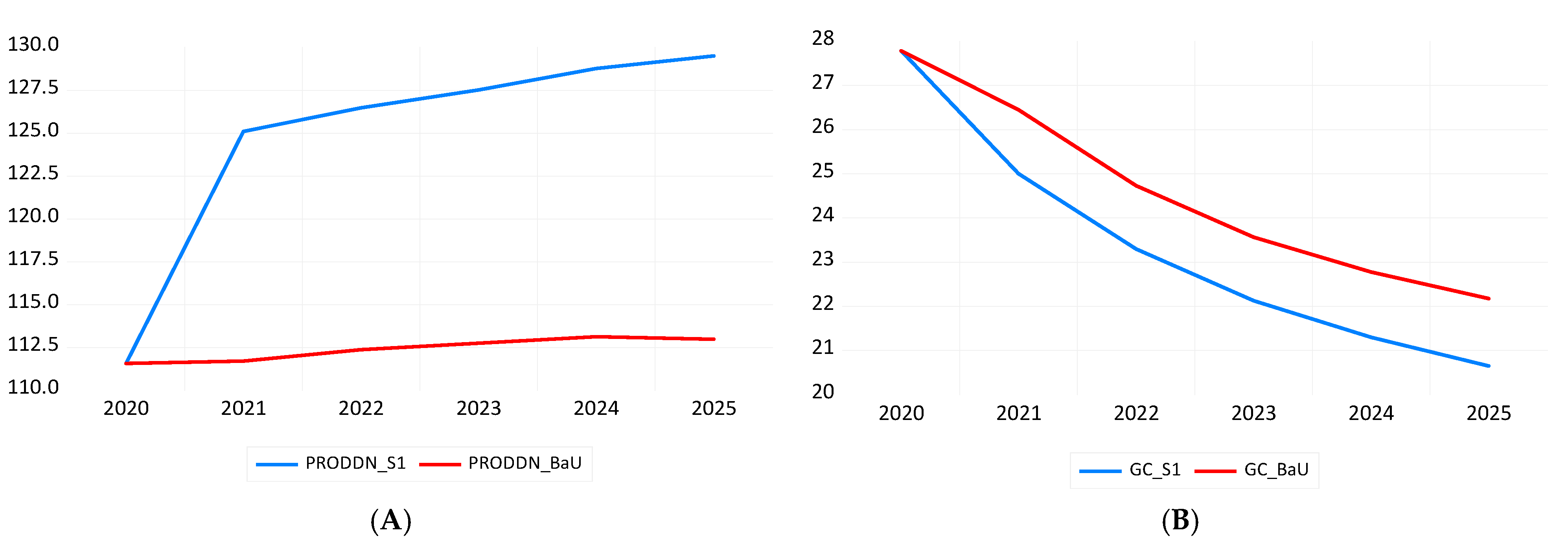

8.3. Results of the Projections

9. Conclusions and Policy Insights

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. A Brief Survey of Panel Studies

Appendix B. Conceptual Framework for Modeling the Saudi REER

Appendix C. Further Explanations for the Estimated Effect of NFA

Appendix D. Description and Test of the Variables Used in the Additional Robustness Checks

Appendix E. Additional Features of the KGEMM

References

- Wysokińska, Z. Competitiveness and its relationships with productivity and sustainable development. Fibres Text. East. Eur. 2003, 11, 42. [Google Scholar]

- Andreoni, V.; Miola, A. Competitiveness and Sustainable Developent Goals; Publications Office of the European Union: Luxembourg, 2016. [Google Scholar]

- Kiseľáková, D.; Šofranková, B.; Čabinová, V.; Onuferová, E. Competitiveness and sustainable growth analysis of the EU countries with the use of Global Indexes’ methodology. Entrep. Sustain. 2018, 5, 581–599. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Krstić, M.; Filipe, J.A.; Chavaglia, J. Higher Education as a Determinant of the Competitiveness and Sustainable Development of an Economy. Sustainability 2020, 12, 6607. [Google Scholar] [CrossRef]

- Suranovic, S. International Trade: Theory and Policy; Saylor Foundation: New York, NY, USA, 2010. [Google Scholar]

- Anyaehie, M.C.; Areji, A.C. Economic diversification for sustainable development n Nigeria. Open J. Political Sci. 2015, 5, 87. [Google Scholar] [CrossRef] [Green Version]

- Krugman, P.R.; Obstfeld, M.; Melitz, M. International Economics: Theory and Policy, 10th ed.; Pearson Series in Economics: London, UK, 2015. [Google Scholar]

- Mania, E.; Rieber, A. Product export diversification and sustainable economic growth in developing countries. Struct. Chang. Econ. Dyn. 2019, 51, 138–151. [Google Scholar] [CrossRef]

- Xu, Z.; Li, Y.; Chau, S.N.; Dietz, T.; Li, C.; Wan, L.; Zhang, J. Impacts of international trade on global sustainable development. Nat. Sustain. 2020, 3, 964–971. [Google Scholar] [CrossRef]

- Beutel, J. Economic diversification and sustainable development of GCC countries. In When Can Oil Economies Be Deemed Sustainable? Palgrave Macmillan: Singapore, 2021; pp. 99–151. [Google Scholar]

- Hasanov, F.; Javid, M.; Joutz, F.L. Saudi Non-oil Exports Before and After COVID-19: Historical Impacts of Determinants and Scenario Analysis. Sustainability 2022, 14, 2379. [Google Scholar] [CrossRef]

- Balassa, B. The Purchasing Power Parity Doctrine: A Reappraisal. J. Political Econ. 1964, 72, 584–596. [Google Scholar] [CrossRef] [Green Version]

- European Commission. Price and Cost Competitiveness: Technical Appendix; Directorate-General for Economic and Financial Affairs: Brussels, Belgium, 2002. [Google Scholar]

- International Monetary Fund (IMF). n.d. What Is Real Effective Exchange Rate (REER)? Available online: http://datahelp.imf.org/knowledgebase/articles/537472-what-is-real-effective-exchange-rate-reer (accessed on 11 March 2023).

- Nagayasu, J. Global and Country-specific Movements in Real Effective Exchange Rates: Implications for External Competitiveness. J. Int. Money Financ. 2017, 76, 88–105. [Google Scholar] [CrossRef]

- Peters, D. Price Competitiveness in Central and Eastern Europe—A Case Study for Transition Economies; IMK Study No. 1/2010; IMK at the Hans Boeckler Foundation, Macroeconomic Policy Institute: Düsseldorf, Germany, 2010. [Google Scholar]

- Samuelson, P.A. Theoretical Notes on Trade Problems. Rev. Econ. Stat. 1964, 46, 145–154. [Google Scholar] [CrossRef]

- United Nations Conference on Trade and Development (UNCTAD). Development and Globalization: Facts and Figures; United Nations Conference on Trade and Development: New York, NY, USA, 2012; Available online: https://unctad.org/system/files/official-document/webgdsdsi2012d2_en.pdf (accessed on 11 March 2023).

- Rodrik, D. The Real Exchange Rate and Economic Growth: Theory and Evidence; Working paper; Harvard University: Cambridge, MA, USA, 2007; Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.554.1195&rep=rep1&type=pdf (accessed on 11 March 2023).

- Alkhareif, R.M.; Barnett, W.A.; Qualls, J.H. Has the Dollar Peg Served the Saudi Economy Well? Int. Financ. Bank. 2017, 4, 145–162. [Google Scholar] [CrossRef] [Green Version]

- Hasanov, F.J.; Al Rasasi, M.H.; Alsayaary, S.S.; Alfawzan, Z. Money demand under a fixed exchange rate regime: The case of Saudi Arabia. J. Appl. Econ. 2022, 25, 385–411. [Google Scholar] [CrossRef]

- Hasanov, F.; Joutz, F.L.; Mikayilov, J.I.; Javid, M. KGEMM: A Macroeconometric Model for Saudi Arabia; KAPSARC Discussion Paper No. KS-2020-DP04; King Abdullah Petroleum Studies and Research Center: Riyadh, Saudi Arabia, 2020. [Google Scholar] [CrossRef] [Green Version]

- Hasanov, F.; Joutz, F.L.; Mikayilov, J.I.; Javid, M. KGEMM: A Macroeconometric Model for Saudi Arabia; Springer: New York, NY, USA, 2023. [Google Scholar]

- Public Investment Fund (PIF). Public Investment Fund Program 2021–2025. 2021. Available online: https://www.pif.gov.sa/VRP%202025%20Downloadables%20EN/PIFStrategy2021-2025-EN.pdf (accessed on 11 March 2023).

- Beenstock, M.; Dalziel, A. The Demand for Energy in the UK: A General Equilibrium Analysis. Energy Econ. 1986, 8, 90–98. [Google Scholar] [CrossRef]

- Bandara, J.S. Computable general equilibrium models for development policy analysis in LDCs. J. Econ. Surv. 1991, 5, 3–69. [Google Scholar] [CrossRef]

- Beck, J.H. Distributive justice and the rules of the corporation: Partial versus general equilibrium analysis. Bus. Ethics Q. 2005, 15, 355–362. [Google Scholar] [CrossRef]

- Thomsen, M.R. An Interactive Text for Food and Agricultural Marketing. 2018. Open Education Resource (OER) LibreTexts Project. Available online: https://LibreTexts.org (accessed on 11 March 2023).

- Cusbert, T.; Kendall, E. Meet MARTIN, the RBA’s New Macroeconomic Model. Aust. Reserve Bank Bull. 2018, 31–44. [Google Scholar]

- Hasanov, F. Theoretical Framework for Industrial Electricity Consumption Revisited: Empirical Analysis and Projections for Saudi Arabia; KAPSARC Discussion Paper No. KS-2019-DP66; King Abdullah Petroleum Studies and Research Center: Riyadh, Saudi Arabia, 2019. [Google Scholar] [CrossRef] [Green Version]

- Ballantyne, A.; Cusbert, T.; Evans, R.; Guttmann, R.; Hambur, J.; Hamilton, A.; Kendall, E.; McCirick, R.; Nodari, G.; Rees, D.M. MARTIN Has Its Place: A Macroeconometric Model of the Australian Economy. Econ. Rec. 2020, 96, 225–251. [Google Scholar] [CrossRef] [Green Version]

- Razek, N.H.A.; McQuinn, B. Saudi Arabia’s Currency Misalignment and International Competitiveness, Accounting for Geopolitical Risks and the Super-contango Oil Market. Resour. Policy 2021, 72, 102057. [Google Scholar] [CrossRef]

- Aleisa, E.A.; Dibooĝlu, S. Sources of Real Exchange Rate Movements in Saudi Arabia. J. Econ. Financ. 2002, 26, 101–110. [Google Scholar] [CrossRef]

- Habib, M.M.; Kalamova, M.M. Are There Oil Currencies? The Real Exchange Rate of Oil Exporting Countries; ECB Working Paper No. 839; European Central Bank: Frankfurt am Main, Germany, 2007. [Google Scholar] [CrossRef]

- Altarturi, B.H.M.; Alshammri, A.A.; Hussin, T.M.T.I.T.; Saiti, B. Oil Price and Exchange Rates: A Wavelet Analysis for OPEC Members. Int. J. Energy Econ. Policy 2016, 6, 421–430. Available online: http://www.econjournals.com/index.php/ijeep/article/view/2253 (accessed on 11 March 2023).

- Suliman, T.H.M.; Abid, M. The Impacts of Oil Price on Exchange Rates: Evidence from Saudi Arabia. Energy Explor. Exploit. 2020, 38, 2037–2058. [Google Scholar] [CrossRef]

- Abdelaziz, M.; Chortareas, G.; Cipollini, A. Stock Prices, Exchange Rates, and Oil: Evidence from Middle East Oil-exporting Countries. Top. Middle East. Afr. Econ. 2008, 10, 1–27. Available online: http://meea.sites.luc.edu/volume10/PDFS/Paper%20by%20Abdelaziz&Chortareas&Cipollini.pdf (accessed on 11 March 2023).

- Coudert, V.; Couharde, C. Currency Misalignments and Exchange Rate Regimes in Emerging and Developing Countries; CEPII Working Paper No. 2008-07; CEPII: Paris, France, 2008; Available online: http://www.cepii.fr/PDF_PUB/wp/2008/wp2008-07.pdf (accessed on 11 March 2023).

- Mozayani, A.H.; Parvizi, S. Exchange Rate Misalignment in Oil Exporting Countries (OPEC): Focusing on Iran. Iran. Econ. Rev. 2016, 20, 261–376. [Google Scholar] [CrossRef]

- Couharde, C.; Delatte, A.L.; Grekou, C.; Mignon, V.; Morvillier, F. EQCHANGE: A World Database on Actual and Equilibrium Effective Exchange Rates. Int. Econ. 2018, 156, 206–230. [Google Scholar] [CrossRef] [Green Version]

- Grekou, C. EQCHANGE Annual Assessment 2018; CEPII Working Paper No. 2018-23; CEPII: Paris, France, 2018; Available online: http://www.cepii.fr/PDF_PUB/wp/2018/wp2018-23.pdf (accessed on 11 March 2023).

- Mahraddika, W. Real exchange rate misalignments in developing countries: The role of exchange rate flexibility and capital account openness. Int. Econ. 2020, 163, 1–24. [Google Scholar] [CrossRef]

- Guillaumin, C.; Boubakri, S.; Silanine, A. Do commodity price volatilities impact currency misalignments in commodity-exporting countries? Econ. Bull. 2020, 40, 1727–1739. [Google Scholar]

- Lemaire, T. Civil Conflicts and Exchange Rate Misalignment: Evidence from MENA and Arab League Members; Economic Research Forum (ERF): Giza, Egypt, 2021. [Google Scholar]

- Aman, Z.; Mallick, S.; Emlioglu, I. Currency regimes and external competitiveness: The role of institutions, trade agreements and monetary rameworks. J. Inst. Econ. 2022, 18, 399–428. [Google Scholar] [CrossRef]

- del Carmen Ramos-Herrera, M.; Sosvilla-Rivero, S. Economic growth and deviations from the equilibrium exchange rate. Int. Rev. Econ. Financ. 2023, 86, 764–786. [Google Scholar] [CrossRef]

- Ugurlu, E.N.; Razmi, A. Political economy of real exchange rate levels. J. Comp. Econ. 2023. [Google Scholar] [CrossRef]

- Elsherif, M.; Mohieldin, M. The Dynamic Interaction of Exchange Rates and International Trade Flows in the MENA Region: GARCH Analysis; Economic Research Forum: Giza, Egypt, 2020. [Google Scholar]

- Kasem, J.; Al-Gasaymeh, A. A Cointegration Analysis for the Validity of Purchasing Power Parity: Evidence from Middle East Countries. Int. J. Technol. Innov. Manag. 2022, 2. [Google Scholar] [CrossRef]

- Leichter, J.; Mocci, C.; Pozzuoli, S. Measuring External Competitiveness: An Overview; Government of the Italian Republic, Ministry of Economy and Finance, Department of the Treasury Working Paper No. 2; Government of the Italian Republic: Rome, Italy, 2010. [CrossRef] [Green Version]

- Comunale, M.; Mongelli, F.P. The Role of Real, Financial, Monetary and Institutional Factors in Tracking Growth. The World Economic Forum. 2020. Available online: https://www.weforum.org/agenda/2020/01/real-financial-monetary-institutional-factors-eu-growth/ (accessed on 11 March 2023).

- Giordano, C. How Frequent a BEER? Assessing the Impact of Data Frequency on Real Exchange Rate Misalignment Estimation; Bank of Italy Occasional Paper 522; Bank of Italy: Rome, Italy, 2019. [Google Scholar]

- Chinn, M.D. A Primer on Real Effective Exchange Rates: Determinants, Overvaluation, Trade Flows and Competitive Devaluation. Open Econ. Rev. 2006, 17, 115–143. [Google Scholar] [CrossRef] [Green Version]

- Baffes, J.; Elbadawi, I.A.; S’ephen, A. O’Connell. Single-equation Estimation of the Equilibrium Real Exchange Rate. In Exchange Rate Misalignment Concepts and Measurement for Developing Countries; Hinkle, L.E., Montiel, P.J., Eds.; Oxford University Press: New York, NY, USA, 1999; pp. 405–466. [Google Scholar]

- Clark, P.B. Concepts of Equilibrium Exchange Rates. In The Globalization of Markets; Stein, J.L., Ed.; Physica: Heidelberg, Germany, 1997; pp. 49–56. [Google Scholar] [CrossRef]

- Clark, P.B.; MacDonald, R. Exchange Rates and Economic Fundamentals: A Methodological Comparison of BEERs and FEERs. In Equilibrium Exchange Rates; MacDonald, R., Stein, J.L., Eds.; Springer: New York, NY, USA, 1999; Volume 69, pp. 285–322. [Google Scholar] [CrossRef] [Green Version]

- Clark, P.B.; MacDonald, R. Filtering the BEER: A Permanent and Transitory Decomposition. Glob. Financ. J. 2004, 15, 29–56. [Google Scholar] [CrossRef]

- Lauro, B.; Schmitz, M. Euro Area Exchange Rate-based Competitiveness Indicators: A Comparison of Methodologies and Empirical Results. In Proceedings of the Sixth IFC Conference on Statistical Issues and Activities in a Changing Environment, Basel, Switzerland, 28–29 August 2012; Volume 36, pp. 325–339. Available online: https://econpapers.repec.org/bookchap/bisbisifc/36-21.htm (accessed on 11 March 2023).

- Fidora, M.; Giordano, C.; Schmitz, M. Real Exchange Rate Misalignments in the Euro Area. Open Econ. Rev. 2021, 32, 71–107. [Google Scholar] [CrossRef]

- Alshehabi, O.H.; Ding, S. Estimating Equilibrium Exchange Rates for Armenia and Georgia; IMF Working Paper No. 08/110; International Monetary Fund: Washington, DC, USA, 2008. [Google Scholar]

- Javed, S.A.; Ali, W.; Ahmed, V. Exchange Rate and External Competitiveness: A Case of Pakistan; SDPI Monetary Policy Brief, Policy Paper No. 41; SDPI: Islamabad, Pakistan, 2016. [Google Scholar] [CrossRef]

- Orszaghova, L.; Savelin, L.; Schudel, W. External Competitiveness of EU Candidate Countries; ECB Occasional Paper No. 141; European Central Bank: Frankfurt am Main, Germany, 2012; Available online: https://www.ecb.europa.eu/pub/pdf/scpops/ecbocp141.pdf (accessed on 11 March 2023).

- Couharde, C.; Delatte, A.-L.; Grekou, C.; Mignon, V.; Morvillier, F. Measuring the Balassa-Samuelson effect: A guidance note on the RPROD database. Int. Econ. 2020, 161, 237–247. [Google Scholar] [CrossRef] [Green Version]

- Couharde, C.; Grekou, C.; Mignon, V. MULTIPRIL, a new database on multilateral price levels and currency misalignments. Int. Econ. 2021, 165, 94–117. [Google Scholar] [CrossRef]

- World Bank. World Development Indicators Database. 2021 Release. [Dataset]. 2021. Available online: https://datatopics.worldbank.org/world-development-indicators/ (accessed on 11 March 2023).

- Chudik, A.; Mongardini, J. Search of Equilibrium: Estimating Equilibrium Real Exchange Rates in Sub-Saharan African Countries; IMF Working Paper No. 07/90; International Monetary Fund: Washington, DC, USA, 2007; ISBN 9781451866544. [Google Scholar]

- Saudi Arabian Monetary Authority (SAMA). Yearly Statistics. Saudi Central Bank. 2018. Available online: https://www.sama.gov.sa/en-US/EconomicReports/Pages/YearlyStatistics.aspx (accessed on 11 March 2023).

- Enders, W. Applied Econometrics Time Series, 5th ed.; Wiley: Hoboken, NJ, USA, 2015. [Google Scholar]

- Pesaran, M.H.; Shin, Y. An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis; Cambridge Working Papers in Economics; Faculty of Economics, University of Cambridge: Cambridge, UK, 1995. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds Testing Approaches to the Analysis of Level Relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Perron, P. Testing for a Unit Root in Time Series Regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Enders, W.; Lee, J. The Flexible Fourier Form and Dickey–Fuller Type Unit Root Tests. Econ. Lett. 2012, 117, 196–199. [Google Scholar] [CrossRef]

- Perron, P. Testing for a Unit Root in a Time Series with a Changing Mean. J. Bus. Econ. Stat. 1990, 8, 153–162. [Google Scholar] [CrossRef]

- Perron, P.; Vogelsang, T.J. Nonstationarity and Level Shifts with an Application to Purchasing Power Parity. J. Bus. Econ. Stat. 1992, 10, 301–320. [Google Scholar] [CrossRef]

- Perron, P.; Vogelsang, T.J. Testing for a Unit Root in a Time Series with a Changing Mean: Corrections and Extensions. J. Bus. Econ. Stat. 1992, 10, 467–470. [Google Scholar] [CrossRef]

- Vogelsang, T.J.; Perron, P. Additional Tests for a Unit Root Allowing for a Break in the Trend Function at an Unknown Time. Int. Econ. Rev. 1998, 39, 1073–1100. [Google Scholar] [CrossRef] [Green Version]

- Enders, W.; Lee, J. A Unit Root Test Using a Fourier Series to Approximate Smooth Breaks. Oxf. Bull. Econ. Stat. 2012, 74, 574–599. [Google Scholar] [CrossRef] [Green Version]

- Badinger, H. Austria’s Demand for International Reserves and Monetary Disequilibrium: The Case of a Small Open Economy with a Fixed Exchange Rate Regime. Economica 2004, 71, 39–55. [Google Scholar] [CrossRef]

- Dibooglu, S.; Enders, W. Multiple Cointegrating Vectors and Structural Economic Models: An Application to the French Franc/US Dollar Exchange Rate. South. Econ. J. 1995, 61, 1098–1116. [Google Scholar] [CrossRef]

- Ericsson, N.R.; MacKinnon, J.G. Distributions of error correction tests for cointegration. Econom. J. 2002, 5, 285–318. [Google Scholar] [CrossRef] [Green Version]

- Johansen, S. Statistical Analysis of Cointegration Vectors. J. Econ. Dyn. Control 1988, 12, 231–254. [Google Scholar] [CrossRef]

- Johansen, S. Cointegration in Partial Systems and the Efficiency of Single-equation Analysis. J. Econom. 1992, 52, 389–402. [Google Scholar] [CrossRef]

- Johansen, S.; Juselius, K. Maximum Likelihood Estimation and Inference on Cointegration—With Applications to the Demand for Money. Oxf. Bull. Econ. Stat. 1990, 52, 169–210. [Google Scholar] [CrossRef]

- Juselius, K. The Cointegrated VAR Methodology. In Oxford Research Encyclopedia of Economics and Finance; Oxford University Press: London, UK, 2006. [Google Scholar] [CrossRef]

- Cheung, Y.-W.; Lai, K.S. Finite-sample Sizes of Johansen’s Likelihood Ratio Tests for Cointegration. Oxf. Bull. Econ. Stat. 1993, 55, 313–328. [Google Scholar] [CrossRef]

- Reimers, H.-E. Comparisons of Tests for Multivariate Cointegration. Stat. Pap. 1992, 33, 335–359. [Google Scholar] [CrossRef]

- Reinsel, G.C.; Ahn, S.K. Vector Autoregressive Models with Unit Roots and Reduced Rank Structure: Estimation, Likelihood Ratio Test, and Forecasting. J. Time Ser. Anal. 1992, 13, 353–375. [Google Scholar] [CrossRef]

- Narayan, P.K. The Saving and Investment Nexus for China: Evidence from Cointegration Tests. Appl. Econ. 2005, 37, 1979–1990. [Google Scholar] [CrossRef]

- MacKinnon, J.G. Numerical distribution functions for unit root and cointegration tests. J. Appl. Econom. 1996, 11, 601–618. [Google Scholar] [CrossRef]

- MacKinnon, J.G.; Haug, A.A.; Michelis, L. Numerical Distribution Functions of Likelihood Ratio Tests for Cointegration. J. Appl. Econom. 1999, 14, 563–577. [Google Scholar] [CrossRef]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill: New York, NY, USA, 2009. [Google Scholar]

- Meshulam, D.; Sanfey, P. The Determinants of Real Exchange Rates in Transition Economies; European Bank for Reconstruction and Development Working Paper Series (No. 228); European Bank for Reconstruction and Development: London, UK, 2019; Available online: https://www.ebrd.com/publications/working-papers/real-exchange-rates (accessed on 11 March 2023).

- International Monetary Fund (IMF). Saudi Arabia: 2011 Article IV Consultation: Staff Report; Public Information Notice on the Executive Board Discussion; IMF Staff Country Reports No. 11/292; International Monetary Fund: Washington, DC, USA, 2011. [Google Scholar] [CrossRef]

- Hasanov, F.J.; Liddle, B.; Mikayilov, J.I.; Bollino, C.A. How Total Factor Productivity Drives Long-run Energy Consumption in Saudi Arabia. In Energy and Environmental Strategies in the Era of Globalization; Shahbaz, M., Balsalobre, D., Eds.; Springer: New York, NY, USA, 2019; pp. 195–220. [Google Scholar]

- Feenstra, R.C.; Inklaar, R.; Timmer, M.P. The Next Generation of the Penn World Table. Am. Econ. Rev. 2015, 105, 3150–3182. [Google Scholar] [CrossRef] [Green Version]

- International Monetary Fund (IMF). Saudi Arabia: 2019 Article IV Consultation—Press Release and Staff Report; IMF Country Report No. 19/290; International Monetary Fund: Washington, DC, USA, 2019. [Google Scholar] [CrossRef] [Green Version]

- Jelić, O.N.; Ravnik, R. Introducing Policy Analysis Croatian MAcroecoNometric Model (PACMAN); Croatian National Bank: Zagreb, Croatia, 2021. [Google Scholar]

- Nikas, A.; Doukas, H.; Papandreou, A. A Detailed Overview and Consistent Classification of Climate-economy Models. In Understanding Risks and Uncertainties in Energy and Climate Policy; Doukas, H., Flamos, A., Lieu, J., Eds.; Springer: New York, NY, USA, 2019; pp. 1–54. [Google Scholar]

- Blanchard, O. On the future of macroeconomic models. Oxf. Rev. Econ. Policy 2018, 34, 43–54. [Google Scholar] [CrossRef]

- Blanchard, O. Do DSGE models have a future. In DSGE Models in the Conduct of Policy: Use as Intended; Gürkaynak, R.S., Tille, C., Eds.; CEPR Press: Brussels, Belgium, 2017; p. 93. [Google Scholar]

- Hendry, D.F. Deciding between Alternative Approaches in Macroeconomics. Int. J. Forecast. 2018, 34, 119–135. [Google Scholar] [CrossRef]

- Hendry, D.F.; Muellbauer, J.N.J. The Future of Macroeconomics: Macro Theory and Models at the Bank of England. Oxf. Rev. Econ. Policy 2018, 34, 287–328. [Google Scholar] [CrossRef] [Green Version]

- Giacomini, R. Economic Theory and Forecasting: Lessons from the Literature. J. Econom. 2015, 18, C22–C41. [Google Scholar] [CrossRef] [Green Version]

- Gürkaynak, R.S.; Tille, C. (Eds.) DSGE Models in the Conduct of Policy: Use as Intended; CEPR Press: Brussels, Belgium, 2017. [Google Scholar]

- Gürkaynak, R.S.; Kısacıkoğlu, B.; Rossi, B. Do DSGE Models Forecast More Accurately Out-Of-Sample than VAR Models? Adv. Econom. 2013, 32, 27–79. [Google Scholar]

- Pesaran, M.H.; Smith, R. Beyond the DSGE Straitjacket; CESifo Working Paper no. 3447; CESifo: Munich, Germany, 2011. [Google Scholar]

- Wickens, M. Real business cycle analysis: A needed revolution in macroeconometrics. Econ. J. 1995, 433, 1637–1648. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Dees, S.; Karadeloglou, P.; Sanchez, M. Does OPEC Matter? An Econometric Analysis of Oil Prices. Energy J. 2004, 25, 67–90. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Bradford, A.; Belanger, L.H.; Mclaughlin, J.P.; Miki, Y. Determinants of OPEC Production: Implications for OPEC Behavior. Energy Econ. 2008, 30, 333–351. [Google Scholar] [CrossRef]

- Wirl, F.; Kujundzic, A. The Impact of OPEC Conference Outcomes on World Oil Prices 1984–2001. Energy J. 2004, 25, 45–62. [Google Scholar] [CrossRef]

- AlGhamdi, A. Saudi Arabia Energy Report; KAPSARC Discussion Paper No. KS–2020–DP25; King Abdullah Petroleum Studies and Research Center: Riyadh, Saudi Arabia, 2020. [Google Scholar]

- Al Moneef, H.E.M.; Hasanov, F.J. Fiscal Multipliers for Saudi Arabia Revisited; KAPSARC Discussion Paper No. KS–2020–DP21; King Abdullah Petroleum Studies and Research Center: Riyadh, Saudi Arabia, 2020. [Google Scholar]

- Musila, J.W. An Econometric Model of the Malawian Economy. Econ. Model. 2002, 19, 295–330. [Google Scholar] [CrossRef]

- International Monetary Fund (IMF). Saudi Arabia: 2018 Article IV Consultation—Press Release and Staff Report; IMF Country Report No. 18/263; International Monetary Fund: Washington, DA, USA, 2018. [Google Scholar] [CrossRef]

- Hasanov, F.J.; AlKathiri, N.; Alshahrani, S.A.; Alyamani, R. The impact of fiscal policy on non-oil GDP in Saudi Arabia. Appl. Econ. 2021, 54, 793–806. [Google Scholar] [CrossRef]

- Al-Hamidy, A. Aspects of Fiscal/Debt Management and Monetary Policy Interaction: The Recent Experience of Saudi Arabia; BIS Paper No. 67v; Bank for International Settlements: Basel, Switzerland, 2012. [Google Scholar] [CrossRef] [Green Version]

- Babetskii, I.; Égert, B. Equilibrium Exchange Rate in the Czech Republic: How Good is the Czech BEER? Czech J. Econ. Financ. 2005, 55, 232–252. [Google Scholar] [CrossRef] [Green Version]

- Brixiova, Z.; Égert, B.; Essid, T.H.A. The Real Exchange Rate and External Competitiveness in Egypt, Morocco and Tunisia. Rev. Middle East Econ. Financ. 2014, 10, 25–51. [Google Scholar] [CrossRef] [Green Version]

- Égert, B.; Lahrèche-Révil, A.; Lommatzsch, K. The Stock-flow Approach to the Real Exchange Rate of CEE Transition Economies; No. 2004-15; CEPII: Paris, France, 2004. [Google Scholar]

- Al-Bassam, K.A. Money Demand and Supply in Saudi Arabia: An Empirical Analysis. Ph.D. Thesis, University of Leicester, Leicester, UK, 1990. [Google Scholar]

- Al Rasasi, M.; Banafea, W. Estimating Money Demand Function in Saudi Arabia: Evidence from Cash in Advance Model; SAMA Working Paper: WP/18/4; Saudi Central Bank: Riyadh, Saudi Arabia, 2018. [Google Scholar]

- Al Rasasi, M.H.; Qualls, J.H. Testing for Causality between Oil Prices and Money Supply in Saudi Arabia; SAMA Working Paper: WP/19/04; Saudi Central Bank: Riyadh, Saudi Arabia, 2019. [Google Scholar]

- Chatah, M.B. A Monetary Framework for the Saudi Arabian Economy. Ph.D. Thesis, University of Texas at Austin, Austin, TX, USA, 1983. [Google Scholar]

- Darrat, A.F. The Money Demand Relationship in Saudi Arabia: An Empirical Investigation. J. Econ. Stud. 1984, 11, 43–50. [Google Scholar] [CrossRef]

- Darrat, A.F. The Demand for Money in Some Major OPEC Members: Regression Estimates and Stability Results. Appl. Econ. 1986, 18, 127–142. [Google Scholar] [CrossRef]

- El Mallakh, R.; El Mallakh, D.H. Saudi Arabia: Energy, Developmental Planning, and Industrialization; Lexington Books: Lexington, MA, USA, 1982. [Google Scholar]

- Al-Yousif, Y.K. Do Government Expenditures Inhibit or Promote Economic Growth: Some Empirical Evidence from Saudi Arabia. Indian Econ. J. 2000, 48, 92–96. [Google Scholar] [CrossRef]

- Fasano, U.; Wang, Q. Fiscal Expenditure Policy and Non-oil Economic Growth: Evidence from GCC Countries; IMF Working Paper No. 2001-195; International Monetary Fund: Washington, DC, USA, 2001. [Google Scholar] [CrossRef]

- Looney, R.E. Saudi Arabia’s Development Strategy: Comparative Advantage vs. Sustainable Growth; Defense Technical Information Center, Accession No. ADA528520; Naval Postgraduate School: Monterey, CA, USA, 1989. [Google Scholar]

- Amano, R.A.; Van Norden, S. Exchange Rates and Oil Prices. Rev. Int. Econ. 1988, 6, 683–694. [Google Scholar] [CrossRef]

- Chen, Y.; Rogoff, K. Commodity Currencies. J. Int. Econ. 2003, 60, 133–160. [Google Scholar] [CrossRef]

- Ferraro, D.; Rogoff, K.; Rossi, B. Can Oil Prices Forecast Exchange Rates? An Empirical Analysis of the Relationship between Commodity Prices and Exchange Rates. J. Int. Money Financ. 2015, 54, 116–141. [Google Scholar] [CrossRef]

- Benigno, G.; Thoenissen, C. Equilibrium Exchange Rates and Supply-side Performance. Econ. J. 2003, 113, C103–C124. [Google Scholar] [CrossRef]

- MacDonald, R.; Ricci, L.A. Purchasing Power Parity and New Trade Theory; IMF Working Paper No. 02/32; International Monetary Fund: Washington, DC, USA, 2002. [Google Scholar] [CrossRef]

- Alberola, E.; Navia, D. Equilibrium Exchange Rates in New EU Members: External Imbalances Versus Real Convergence. Rev. Dev. Econ. 2008, 12, 605–619. [Google Scholar] [CrossRef]

- Alberola, E.; Navia, D. Equilibrium Exchange Rates in New EU Members: External Imbalances v. Real Convergence; Banco de España Working Paper No. 0708; Banco de España: Madrid, Spain, 2007. [Google Scholar]

- Aglietta, M.; Baulant, C.; Coudert, V. Why the Euro Will Be Strong: An Approach Based on Equilibrium Exchange Rates. Rev. Econ. 1998, 49, 721–731. [Google Scholar]

- Comunale, M. Current Account and Real Effective Exchange Rate Misalignments in Central Eastern EU Countries: An Update Using the Macroeconomic Balance Approach. Econ. Syst. 2018, 42, 414–436. [Google Scholar] [CrossRef]

- Lommatzsch, K.; Tober, S. What is Behind the Real Appreciation of the Accession Countries’ Currencies? An Investigation of the PPI-based Real Exchange Rate. Econ. Syst. 2004, 28, 383–403. [Google Scholar] [CrossRef]

- Burgess, R.; Fabrizio, S.; Xiao, Y. Competitiveness in the Baltics in the Run-up to EU Accession; IMF Country Report No. 03/114; International Monetary Fund: Washington, DC, USA, 2003. [Google Scholar]

- Alonso-Gamo, P.; Fabrizio, S.; Kramarenko, V.; Wang, Q. Lithuania: History and Future of the Currency Board Arrangement; IMF Working Paper No. 127; International Monetary Fund: Washington, DC, USA, 2002. [Google Scholar]

- Hemrit, W.; Benlagha, N. The Impact of Government Spending on Non-oil-GDP in Saudi Arabia (Multiplier Analysis). Int. J. Econ. Bus. Res. 2018, 15, 350–372. [Google Scholar] [CrossRef]

- Oxford Economics Group. Oxford Economics Global Economic Model Database. March Release [Dataset]. 2021. Available online: https://www.oxfordeconomics.com/service/subscription-services/macro/global-economic-model/ (accessed on 11 March 2023).

- Weyerstrass, K.; Neck, R.; Blueschke, D.; Majcen, B.; Srakar, A.; Verbič, M. SLOPOL10: A macroeconometric model for Slovenia. Econ. Bus. Rev. 2018, 20, 269–302. [Google Scholar] [CrossRef]

- Khan, M.A.; ud Din, M. A Dynamic Macroeconometric Model of Pakistan’s Economy; Working Papers & Research Reports; Pakistan Institute of Development Economics: Islamabad, Pakistan, 2011. [Google Scholar]

- Weyerstrass, K.; Neck, R. SLOPOL6: A macroeconometric model for Slovenia. Int. Bus. Econ. Res. J. 2007, 6, 81–94. [Google Scholar] [CrossRef]

- Buenafe, S.W.; Reyes, C.M. Alternative Estimation Methodologies for Macro Model: ECM vs. OLS; PIDS Discussion Paper No. 2001-22; Philippine Institute for Development Studies (PIDS): Makati, Philippines, 2001. [Google Scholar]

- Dreger, C.; Marcellino, M. A Macroeconometric Model for the Euro Economy. J. Policy Model. 2007, 29, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Welfe, W. Macroeconometric Models; Springer: New York, NY, USA, 2013. [Google Scholar]

- Fair, R.C. An Analysis of the Accuracy of Four Macroeconometric Models. J. Political Econ. 1979, 87, 701–718. [Google Scholar] [CrossRef] [Green Version]

- Fair, R.C. Testing Macroeconometric Models. Am. Econ. Rev. 1993, 83, 287–293. [Google Scholar]

- Looney, R.E. Pre-revolutionary Iranian Economic Policy Making: An Optimal Control Based Assessment. Econ. Model. 1985, 2, 357–368. [Google Scholar] [CrossRef]

- Looney, R.E. Socio-economic Tradeoffs in Saudi Arabia’s Third Five Year Plan (1980–1985). Socio-Econ. Plan. Sci. 1986, 20, 181–192. [Google Scholar] [CrossRef]

- Looney, R.E. Saudi Arabia’s Fiscal Options: 1986–1992. Socio-Econ. Plan. Sci. 1988, 22, 109–123. [Google Scholar] [CrossRef]

,

,  , and

, and  indicate direction of impact, increase, and decrease, respectively. Source: Authors’ construction.

, , and indicate direction of impact, increase, and decrease, respectively. Source: Authors’ construction.

indicate direction of impact, increase, and decrease, respectively. Source: Authors’ construction.

, , and indicate direction of impact, increase, and decrease, respectively. Source: Authors’ construction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Augmented Dickey–Fuller | Phillips–Perron | |||

|---|---|---|---|---|---|

| Test Value | DC | k | Test Value | DC | |

| −2.55 | c | 1 | −2.28 | c | |

| −2.62 * | c | 1 | −2.05 | c | |

| −3.92 ** | t | 2 | −2.91 | t | |

| −2.84 * | c | 0 | −3.02 ** | c | |

| −2.18 | c | 1 | −1.62 | c | |

| −3.31 *** | n | 0 | −3.31 *** | n | |

| −1.78 * | n | 0 | −1.92 * | n | |

| −5.09 *** | c | 0 | −5.17 *** | c | |

| −5.58 *** | n | 0 | −5.58 *** | n | |

| −3.16 *** | n | 0 | −3.35 *** | n | |

| Panel A: Serial correlation LM test a | Panel E: Johansen cointegration test summary | ||||||

| Lags | LM-statistic | Trend in data: | None | None | Linear | Linear | Quadratic |

| 1 | 29.74 (0.23) | Test type: | (a) No c or t | (b) c | (c) c | (d) c and t | (e) c and t |

| 2 | 26.71 (0.37) | Trace adj: | 1 | 1 | 1 | 1 | 1 |

| 3 | 17.75 (0.85) | Max-eigenvalue adj: | 1 | 1 | 1 | 1 | 1 |

| Panel B: Normality test b | Panel C: Heteroscedasticity test c | Panel D: Stability test d | |||||

| Statistic | Statistic | Modulus | Root | ||||

| Skewness | 1.51 (0.91) | White | 333.20 * (0.09) | 0.93 | 0.93 | ||

| Kurtosis | 1.84 (0.87) | 0.91 | 0.84 – 0.35i | ||||

| Jarque-Bera | 3.35 (0.97) | 0.91 | 0.84 + 0.35i | ||||

| 0.88 | 0.86 – 0.19i | ||||||

| 0.88 | 0.86 + 0.19i | ||||||

| c | ||||

|---|---|---|---|---|

| Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) |

| 0.71 (0.00) | 0.18 (0.00) | 0.67 (0.00) | −0.12 (0.06) | −1.02 (0.16) |

| . [70]’s upper-bound critical values in the case of k = 4 and T = 100 are 4.37, 3.49, and 3.09 at the 1%, 5%, and 10% significance levels, respectively. [89]’s upper-bound critical values in the case of k = 4 and T = 35 are 5.53, 4.09, and 3.46 at the 1%, 5%, and 10% significance levels, respectively. | ||||

| Method | c | ||||

|---|---|---|---|---|---|

| Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | |

| DOLS | 0.89 (0.00) | 0.21 (0.00) | 0.51 (0.00) | −0.18 (0.02) | −1.27 (0.22) |

| FMOLS | 1.24 (0.00) | 0.22 (0.01) | 0.68 (0.00) | −0.25 (0.00) | −3.16 (0.00) |

| CCR | 1.23 (0.00) | 0.24 (0.00) | 0.65 (0.00) | −0.24 (0.00) | −3.15 (0.00) |

| Method | c | ||||||

|---|---|---|---|---|---|---|---|

| Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | Coef. (p-Value) | |

| ADL | 0.70 (0.00) | 0.15 (0.04) | 0.73 (0.00) | −0.12 (0.06) | 0.14 (0.59) | --- | −1.67 (0.24) |

| 1.20 (0.00) | −0.29 (0.19) | 0.66 (0.00) | 0.00 (0.99) | ---- | −0.44 (0.03) | 0.23 (0.81) | |

| DOLS | 0.91 (0.00) | 0.19 (0.01) | 0.62 (0.00) | −0.20 (0.01) | 0.41 (0.15) | --- | −3.25 (0.06) |

| 0.69 (0.04) | 0.28 (0.03) | 0.54 (0.00) | −0.15 (0.04) | ---- | 0.07 (0.56) | −1.17 (0.22) | |

| FMOLS | 1.14 (0.00) | 0.19 (0.05) | 0.79 (0.00) | −0.24 (0.00) | 0.26 (0.39) | --- | −5.51 (0.20) |

| 1.28 (0.00) | 0.20 (0.03) | 0.58 (0.00) | −0.21 (0.00) | ---- | −0.05 (0.53) | −1.20 (0.67) | |

| CCR | 1.12 (0.00) | 0.22 (0.01) | 0.74 (0.00) | −0.23 (0.00) | 0.24 (0.46) | --- | −4.91 (0.23) |

| 1.24 (0.00) | 0.23 (0.02) | 0.58 (0.00) | −0.21 (0.00) | ---- | −0.03 (0.73) | −1.29 (0.67) |

| Year | GI | PRODDN | REERE |

|---|---|---|---|

| 2021 | 111.49 | 11.98 | 9.48 |

| 2022 | 110.11 | 12.54 | 9.84 |

| 2023 | 108.50 | 13.09 | 10.23 |

| 2024 | 106.70 | 13.82 | 10.75 |

| 2025 | 104.66 | 14.62 | 11.33 |

| Average | 108.29 | 13.21 | 10.33 |

| Implied elasticity | 0.10 | 0.12 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hasanov, F.J.; Razek, N. Oil and Non-Oil Determinants of Saudi Arabia’s International Competitiveness: Historical Analysis and Policy Simulations. Sustainability 2023, 15, 9011. https://doi.org/10.3390/su15119011

Hasanov FJ, Razek N. Oil and Non-Oil Determinants of Saudi Arabia’s International Competitiveness: Historical Analysis and Policy Simulations. Sustainability. 2023; 15(11):9011. https://doi.org/10.3390/su15119011

Chicago/Turabian StyleHasanov, Fakhri J., and Noha Razek. 2023. "Oil and Non-Oil Determinants of Saudi Arabia’s International Competitiveness: Historical Analysis and Policy Simulations" Sustainability 15, no. 11: 9011. https://doi.org/10.3390/su15119011