Does Socially Responsible Investing Make a Better Society?—A Micro Perspective through Mutual Funds and Their Investee Companies

Abstract

:1. Introduction

2. Theoretical Analysis

2.1. Literature Review and Hypothesis Development

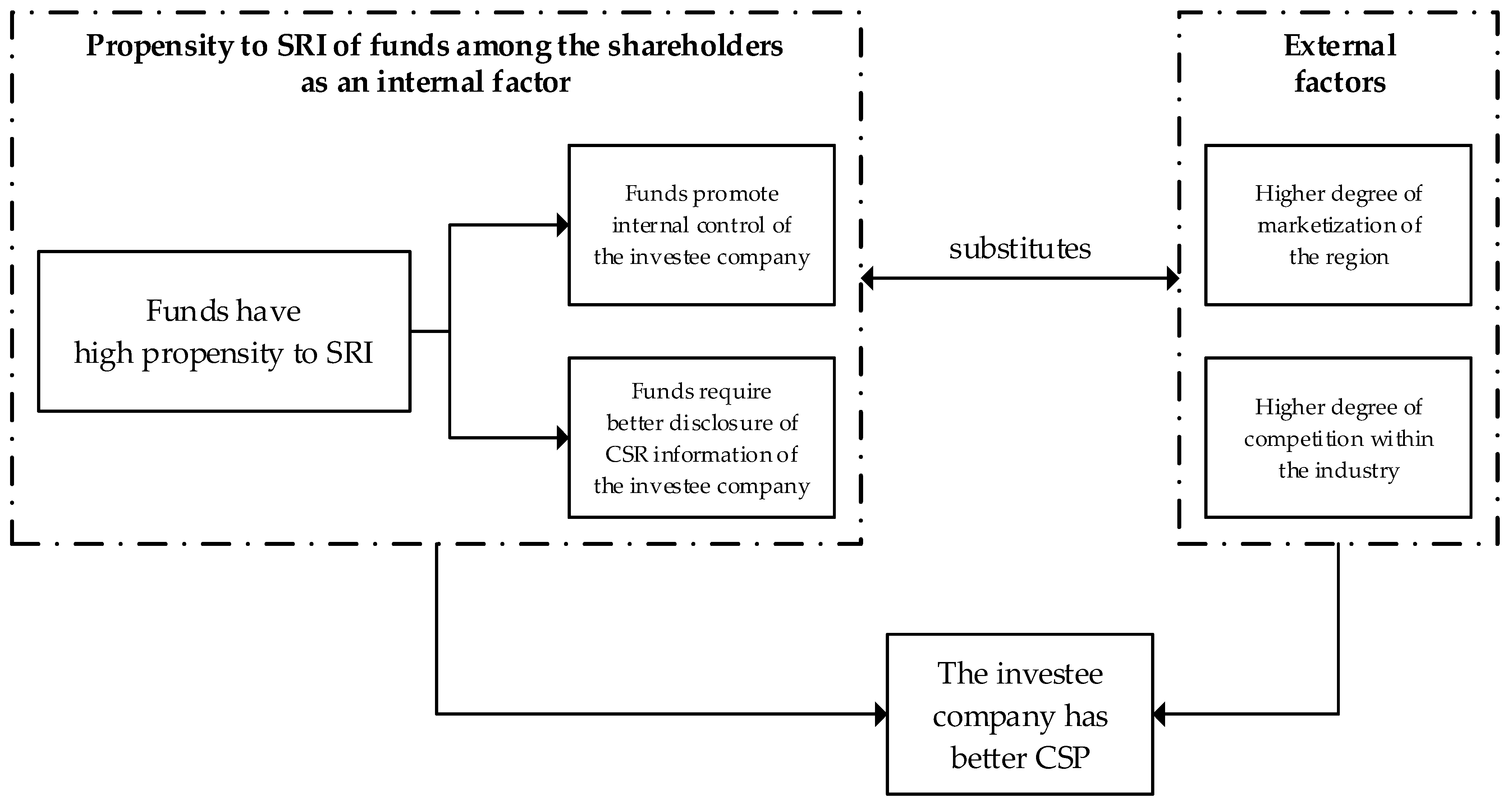

2.2. Research Framework

3. Data

3.1. Sample Source and Data Screening

3.2. Construction of Variables

3.2.1. Dependent Variable

- (1)

- Long coverage time period: Hexun is an early provider of a social responsibility rating product in China. The rating product was launched in September 2013. Upon its release, the social responsibility scores for the years 2010–2012 were announced. Subsequently, every year, Hexun announces the social responsibility scores for the previous year.

- (2)

- Wide coverage of companies: The rating of Hexun covers almost all A-share companies, as Hexun rates the social responsibility of a company based on not only its social responsibility report but also its annual report.

3.2.2. Explanatory Variable

3.2.3. Mechanism Variables

3.2.4. Control Variables

3.3. Data Summary

4. Main Analysis

4.1. Baseline Regression

4.1.1. Model and Method

4.1.2. Results

4.2. Endogeneity Analysis

4.2.1. Lagged Independent Variables

4.2.2. Instrumental Variable Method

4.3. Robustness Tests

5. Mechanism Analysis

5.1. Mechanism of Social Responsibility Information Disclosure

5.2. Mechanism of Internal Control

5.3. Role of External Environment

6. Heterogeneity Analysis and Discussions

6.1. Social Trust Atmosphere

6.2. SOEs vs. Regular Companies

6.3. Discussions

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Renneboog, L.; Ter Horst, J.; Zhang, C. The price of ethics and stakeholder governance: The performance of socially responsible mutual funds. J. Corp. Financ. 2008, 14, 302–322. [Google Scholar] [CrossRef]

- Rivoli, P. Making a difference or making a statement? Finance research and socially responsible investment. Bus. Ethics Q. 2003, 13, 271–287. [Google Scholar] [CrossRef]

- Waring, P.; Lewer, J. The impact of socially responsible investment on human resource management: A conceptual framework. J. Bus. Ethics 2004, 52, 99–108. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Heinkel, R.; Kraus, A.; Zechner, J. The effect of green investment on corporate behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Dam, L.; Heijdra, B.J. The environmental and macroeconomic effects of socially responsible investment. J. Econ. Dyn. Control 2011, 35, 1424–1434. [Google Scholar] [CrossRef]

- Pastor, L.; Stambaugh, R.F.; Taylor, L.A. Sustainable investing in equilibrium. J. Financ. Econ. 2021, 142, 550–571. [Google Scholar] [CrossRef]

- Hwang, C.Y.; Titman, S.; Wang, Y. Investor tastes, corporate behavior, and stock returns: An analysis of corporate social responsibility. Manag. Sci. 2022, 68, 7131–7152. [Google Scholar] [CrossRef]

- Hamilton, S.; Jo, H.; Statman, M. Doing well while doing good? The investment performance of socially responsible mutual funds. Financ. Anal. J. 1993, 49, 62–66. [Google Scholar] [CrossRef]

- Dyck, A.; Lins, K.V.; Roth, L.; Wagner, H.F. Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 2019, 131, 693–714. [Google Scholar] [CrossRef]

- Aggarwal, R.; Erel, I.; Ferreira, M.; Matos, P. Does governance travel around the world? Evidence from institutional investors. J. Financ. Econ. 2011, 100, 154–181. [Google Scholar] [CrossRef]

- Xiang, C.; Chen, F.; Jones, P.; Xia, S. The effect of institutional investors’ distraction on firms’ corporate social responsibility engagement: Evidence from China. Rev. Manag. Sci. 2021, 15, 1645–1681. [Google Scholar] [CrossRef]

- Chen, X.Y.; Wan, P.; Sial, M.S. Institutional investors’ site visits and corporate social responsibility: Implications for the extractive industries. Extr. Ind. Soc. 2021, 8, 374–382. [Google Scholar] [CrossRef]

- Zhou, T.Y.; Gan, J.W. Institutional investors’ site visits and corporate social responsibility: Evidence from China. Econ. Model. 2022, 115, 13. [Google Scholar] [CrossRef]

- Bushee, B.J. The influence of institutional investors on myopic R&D investment behavior. Account. Rev. 1998, 73, 305–333. [Google Scholar] [CrossRef]

- Glossner, S. Investor horizons, long-term blockholders, and corporate social responsibility. J. Bank Financ. 2019, 103, 78–97. [Google Scholar] [CrossRef]

- Kim, H.D.; Kim, T.; Kim, Y.; Park, K. Do long-term institutional investors promote corporate social responsibility activities? J. Bank Financ. 2019, 101, 256–269. [Google Scholar] [CrossRef]

- Oikonomou, I.; Yin, C.; Zhao, L. Investment horizon and corporate social performance: The virtuous circle of long-term institutional ownership and responsible firm conduct. Eur. J. Financ. 2020, 26, 14–40. [Google Scholar] [CrossRef]

- Zhen, H.; Ling, F.; Jing, Y. “Participation in governance” or “selective governance”?—Based on the test of the endogenous relationship between institutional investors and accounting conservatism. Syst. Eng. Theory Pract. 2021, 41, 2198–2217. [Google Scholar] [CrossRef]

- Xiong, W.F.; Dong, M.M.; Xu, C. Institutional investors and corporate social responsibility: Evidence from China. Emerg. Mark. Financ. Trade 2022. [Google Scholar] [CrossRef]

- Dawkins, C.E.; Fraas, J.W. An exploratory analysis of corporate social responsibility and disclosure. Bus. Soc. 2013, 52, 245–281. [Google Scholar] [CrossRef]

- Manning, B.; Braam, G.; Reimsbach, D. Corporate governance and sustainable business conduct-effects of board monitoring effectiveness and stakeholder engagement on corporate sustainability performance and disclosure choices. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 351–366. [Google Scholar] [CrossRef]

- Zhong, P.; Wu, T.; Li, X. An empirical study on the relationship among corporate social responsibility report, social irresponsibility and financial performance of listed companies. Forecasting 2021, 40, 17–23. [Google Scholar] [CrossRef]

- Li, X.; Zheng, C.M.; Liu, G.; Sial, M.S. The effectiveness of internal control and corporate social responsibility: Evidence from Chinese capital market. Sustainability 2018, 10, 4006. [Google Scholar] [CrossRef]

- Huang, R.B.; Huang, Y.B. Does internal control contribute to a firm’s green information disclosure? Evidence from China. Sustainability 2020, 12, 3197. [Google Scholar] [CrossRef]

- Li, X. The effectiveness of internal control and innovation performance: An intermediary effect based on corporate social responsibility. PLoS ONE 2020, 15, 0234506. [Google Scholar] [CrossRef]

- Wang, X.; Zhang, Z.; Chun, D. The influencing mechanism of internal control effectiveness on technological innovation: CSR as a mediator. Sustainability 2021, 13, 13122. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Jing, L. Corporate governance mechanism, marketization process and corporate social responsibility. Stat. Decis. 2020, 36, 168–172. [Google Scholar] [CrossRef]

- Porter, M.E.; Vanderlinde, C. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar] [CrossRef]

- Chang, S.; Jo, H. Employee-friendly practices, product market competition and firm value. J. Bus. Finan. Account. 2019, 46, 200–224. [Google Scholar] [CrossRef]

- Meng, S.; Sima, Y. Foreign competition and corporate social responsibility: The role of the firm-government relationships. Chin. Manag. Stud. 2023, 17, 89–111. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces 2011 Report; Economic Science Press: Beijing, China, 2011. [Google Scholar]

- Fu, L.L.; Pan, L.Y.; Zhao, J.M. Can passive investors improve corporate social responsibility? Evidence from Chinese listed firms. Emerg. Mark. Financ. Trade 2023, 59, 404–419. [Google Scholar] [CrossRef]

- Bai, G.Y.; Li, T.G.; Xu, P. Can analyst coverage enhance corporate innovation legitimacy? -Heterogeneity analysis based on different situational mechanisms. J. Clean Prod. 2023, 405, 13. [Google Scholar] [CrossRef]

- Kempf, A.; Osthoff, P. SRI funds: Nomen est omen. J. Bus. Finan. Account. 2008, 35, 1276–1294. [Google Scholar] [CrossRef]

- Zhang, C.; Zhu, S.; Wu, Y.; Chen, M. Research on behavior and performance of socially responsible investing based on fund holdings. Chin. J. Manag. 2021, 18, 1840–1850. [Google Scholar] [CrossRef]

- Li, Z.F.; Patel, S.; Ramani, S. The role of mutual funds in corporate social responsibility. J. Bus. Ethics 2021, 174, 715–737. [Google Scholar] [CrossRef]

- Shi, Y.; Song, M.; Li, F.; Zhen, H. Share pledge of controlling shareholders and protection of corporate creditors interests: Evidence from China’s bond market. Econ. Res. J. 2021, 56, 109–126. [Google Scholar]

- Lewbel, A. Using heteroscedasticity to identify and estimate mismeasured and endogenous regressor models. J. Bus. Econ. Stat. 2012, 30, 67–80. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. A simple test for heteroscedasticity and random coefficient variation. Econometrica 1979, 47, 1287–1294. [Google Scholar] [CrossRef]

- Baum, C.F.; Lewbel, A. Advice on using heteroskedasticity-based identification. Stata J. 2019, 19, 757–767. [Google Scholar] [CrossRef]

- Hasan, F. Corporate social responsibility and agency cost: Evidence from the UK retail industry. Int. J. Res. Financ. Manag. 2021, 4, 105–115. [Google Scholar] [CrossRef]

- Bernard, J.; Boiral, O.; Guillaumie, L.; Brotherton, M.C. Does proxy voting really promote corporate sustainability? Corp. Gov. 2022, 31, 445–463. [Google Scholar] [CrossRef]

- Baloria, V.P.; Klassen, K.J.; Wiedman, C.I. Shareholder activism and voluntary disclosure initiation: The case of political spending. Contemp. Account. Res. 2019, 36, 904–933. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Definition or Description |

|---|---|

| Dependent | |

| CSP | Social responsibility total score from Hexun. A greater value indicates better corporate social performance. |

| Explanatory | |

| PSRI | Overall propensity for SRI of mutual funds among the shareholders of a company. First, we calculate the weighted average propensity for SRI of mutual funds among the shareholders of a company at the end of each year, then we average the year-end value and the previous-year-end value to proxy the PSRI of the entire year. A larger PSRI indicates greater propensity for SRI. |

| PSRI_A | Firm-level PSRI score adjusted by excluding the data of the indicated firm when calculating the propensity for SRI of mutual funds holding the stock of the indicated firm. A larger PSRI_A indicates greater propensity for SRI. |

| Mechanism | |

| INCTRL | The annual DIB internal control index of the company. A greater value indicates better internal control. |

| DISCL | A dummy variable that equals 1 if the company publishes a social responsibility report separately from the annual report for that year. Such companies are considered to have better disclosure of social responsibility information. |

| EMKT | Provincial Fan et al. [33] marketization index. A greater value indicates better marketization of the region where a company is located. |

| ECOMPE | The opposite number of Herfindahl index of the annual operating income of all companies within an industry. A greater value indicates a higher degree of competition within the industry that a company belongs to. |

| Controls | |

| SIZE | Logarithmic average of year-end and previous-year-end values of total assets of a company. |

| AGE | Average of year-end and previous-year-end values of company age. |

| LEV | Average of year-end and previous-year-end values of asset-liability ratio. |

| BM | Average of year-end and previous-year-end values of B/M ratio. |

| GROWTH | Annual growth rate of the operating income. |

| ROE | Annual return on equity. |

| INS | Average of year-end and previous-year-end percentages of shares held by institutional investors. |

| TOP | Average of year-end and previous-year-end percentages of shares held by the top shareholder. |

| ZINDEX | Average of year-end and previous-year-end Z index. Z index is the ratio of shares held by the top shareholder to the shares held by the second largest shareholder. |

| DUAL | A dummy variable that equals 1 if the CEO also acts as the chairman of the board within the year. |

| INDD | Average of year-end and previous-year-end rates of independent directors. |

| SOE | A dummy variable that equals 1 if the company is a state-owned enterprise. |

| Variable | Obs | Mean | Median | Std | Min | Max |

|---|---|---|---|---|---|---|

| CSP | 11,454 | 27.121 | 22.835 | 17.368 | −1.390 | 75.510 |

| PSRI | 11,454 | 0.373 | 0.360 | 0.088 | 0.224 | 0.594 |

| PSRI_A | 11,454 | 0.373 | 0.361 | 0.088 | 0.224 | 0.595 |

| INCTRL | 11,454 | 658.427 | 671.960 | 96.053 | 0.000 | 849.300 |

| DISCL | 11,454 | 0.303 | 0.000 | 0.460 | 0.000 | 1.000 |

| EMKT | 11,454 | 8.245 | 8.890 | 1.718 | 2.920 | 10.290 |

| ECOMPE | 11,454 | −0.265 | −0.241 | 0.075 | −0.599 | −0.201 |

| SIZE | 11,454 | 22.222 | 22.039 | 1.251 | 19.922 | 26.012 |

| AGE | 11,454 | 17.317 | 16.862 | 5.146 | 4.195 | 32.645 |

| LEV | 11,454 | 0.417 | 0.408 | 0.203 | 0.052 | 0.856 |

| BM | 11,454 | 0.588 | 0.576 | 0.225 | 0.148 | 1.063 |

| GROWTH | 11,454 | 0.182 | 0.111 | 0.395 | −0.490 | 2.573 |

| ROE | 11,454 | 0.072 | 0.068 | 0.077 | −0.244 | 0.300 |

| INS | 11,454 | 0.404 | 0.411 | 0.224 | 0.009 | 0.872 |

| TOP | 11,454 | 0.230 | 0.200 | 0.178 | 0.006 | 0.691 |

| ZINDEX | 11,454 | 10.075 | 3.508 | 16.475 | 1.023 | 103.669 |

| DUAL | 11,454 | 0.284 | 0.000 | 0.451 | 0.000 | 1.000 |

| INDD | 11,454 | 0.373 | 0.354 | 0.050 | 0.333 | 0.571 |

| SOE | 11,454 | 0.373 | 0.000 | 0.484 | 0.000 | 1.000 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| CSP | CSP | CSP | CSP | |

| PSRI | 41.741 *** | 42.010 *** | ||

| (9.59) | (9.74) | |||

| PSRI_A | 33.192 *** | 33.490 *** | ||

| (7.55) | (7.69) | |||

| SIZE | 4.017 *** | 4.124 *** | 4.331 *** | 4.435 *** |

| (12.00) | (12.16) | (12.88) | (13.02) | |

| AGE | 0.052 | 0.057 | 0.054 | 0.059 |

| (1.17) | (1.27) | (1.21) | (1.32) | |

| LEV | −12.303 *** | −12.644 *** | −12.664 *** | −13.002 *** |

| (−9.33) | (−9.56) | (−9.54) | (−9.77) | |

| BM | −4.360 *** | −4.256 *** | −4.910 *** | −4.801 *** |

| (−2.78) | (−2.73) | (−3.11) | (−3.06) | |

| GROWTH | −0.751 *** | −0.736 ** | −0.847 *** | −0.829 *** |

| (−2.58) | (−2.53) | (−2.90) | (−2.84) | |

| ROE | 72.320 *** | 72.394 *** | 72.902 *** | 72.980 *** |

| (28.48) | (28.51) | (28.53) | (28.56) | |

| INS | −1.742 | −1.898 | −1.776 | −1.934 |

| (−1.14) | (−1.23) | (−1.15) | (−1.25) | |

| TOP | 2.411 | 2.655 | 2.323 | 2.568 |

| (1.13) | (1.24) | (1.08) | (1.19) | |

| ZINDEX | 0.000 | 0.001 | 0.001 | 0.002 |

| (0.02) | (0.07) | (0.07) | (0.12) | |

| DUAL | −0.262 | −0.286 | −0.268 | −0.290 |

| (−0.67) | (−0.74) | (−0.68) | (−0.74) | |

| INDD | 0.812 | 0.464 | 0.908 | 0.557 |

| (0.21) | (0.12) | (0.23) | (0.14) | |

| SOE | 2.294 *** | 2.278 *** | 2.360 *** | 2.338 *** |

| (4.17) | (4.04) | (4.26) | (4.11) | |

| Constant | −76.887 *** | −79.224 *** | −80.342 *** | −82.627 *** |

| (−12.44) | (−12.60) | (−12.92) | (−13.05) | |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | NO | YES | NO |

| Industry subcategory FE | NO | YES | NO | YES |

| Adj R2 | 0.348 | 0.350 | 0.345 | 0.347 |

| R2 | 0.352 | 0.355 | 0.348 | 0.352 |

| N | 11,454 | 11,454 | 11,454 | 11,454 |

| Core Explanatory Variable Lagged | All Independent Variables Lagged | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| CSP | CSP | CSP | CSP | F_CSP | F_CSP | F_CSP | F_CSP | |

| PSRI | 28.835 *** | 29.441 *** | ||||||

| (6.36) | (6.60) | |||||||

| PSRI_A | 21.386 *** | 21.999 *** | ||||||

| (4.67) | (4.88) | |||||||

| L_PSRI | 32.992 *** | 33.058 *** | ||||||

| (7.38) | (7.49) | |||||||

| L_PSRI_A | 25.625 *** | 25.718 *** | ||||||

| (5.66) | (5.76) | |||||||

| Constant | −66.346 *** | −68.710 *** | −68.842 *** | −71.172 *** | −73.986 *** | −75.999 *** | −77.175 *** | −79.134 *** |

| (−9.93) | (−10.16) | (−10.24) | (−10.45) | (−11.34) | (−11.48) | (−11.77) | (−11.89) | |

| CVs | YES | YES | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES |

| Industry FE | YES | NO | YES | NO | YES | NO | YES | NO |

| Industry subcategory FE | NO | YES | NO | YES | NO | YES | NO | YES |

| Adj R2 | 0.334 | 0.336 | 0.331 | 0.332 | 0.272 | 0.274 | 0.270 | 0.271 |

| R2 | 0.339 | 0.342 | 0.336 | 0.339 | 0.277 | 0.281 | 0.275 | 0.278 |

| N | 8862 | 8862 | 8853 | 8853 | 9065 | 9065 | 9065 | 9065 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| PSRI | CSP | PSRI_A | CSP | |

| PSRI | 129.295 *** | |||

| (3.99) | ||||

| IV | 0.121 *** | |||

| (7.32) | ||||

| PSRI_A | 129.086 *** | |||

| (3.81) | ||||

| IV _A | 0.118 *** | |||

| (7.15) | ||||

| Constant | −0.381 *** | −48.389 *** | −0.368 *** | −50.172 *** |

| (−21.36) | (−3.18) | (−20.81) | (−3.26) | |

| CVs | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES |

| Adj R2 | 0.788 | 0.305 | 0.787 | 0.293 |

| R2 | 0.789 | 0.309 | 0.788 | 0.297 |

| Kleibergen–Paap | 53.634 | 51.151 | ||

| N | 11,454 | 11,454 | 11,454 | 11,454 |

| OLS | OLS | OLS | OLS | OLogit | OLogit | |

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| CSP_HZ | CSP_HZ | CSP_HZ | CSP_HZ | CSP_HZ | CSP_HZ | |

| PSRI | 18.291 *** | 18.728 *** | 3.883 *** | |||

| (6.46) | (6.63) | (6.72) | ||||

| PSRI_A | 11.644 *** | 12.072 *** | 2.497 *** | |||

| (4.11) | (4.28) | (4.33) | ||||

| Constant | −7.790 * | −8.514 * | −10.302 ** | −10.992 ** | ||

| (−1.77) | (−1.90) | (−2.34) | (−2.45) | |||

| CVs | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Industry FE | YES | NO | YES | NO | NO | NO |

| Industry subcategory FE | NO | YES | NO | YES | NO | NO |

| Adj R2 | 0.262 | 0.268 | 0.260 | 0.265 | ||

| R2 | 0.266 | 0.273 | 0.264 | 0.270 | ||

| Pseudo R2 | 0.113 | 0.111 | ||||

| N | 11,416 | 11,416 | 11,416 | 11,416 | 11,416 | 11,416 |

| Logit | Logit | OLS | OLS | OLS | OLS | |

|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | |

| DISCL | DISCL | DISCL | DISCL | CSP | CSP | |

| PSRI | 5.796 *** | 0.904 *** | 22.792 *** | |||

| (6.06) | (7.19) | (7.70) | ||||

| PSRI_A | 3.360 *** | 0.574 *** | 21.113 *** | |||

| (3.59) | (4.56) | (7.11) | ||||

| DISCL | 20.967 *** | 21.060 *** | ||||

| (55.76) | (56.11) | |||||

| Constant | −26.277 *** | −26.931 *** | −4.013 *** | −4.138 *** | 7.253 * | 6.794 |

| (−15.74) | (−16.04) | (−19.04) | (−19.64) | (1.74) | (1.62) | |

| CVs | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES | YES | YES |

| Pseudo R2 | 0.254 | 0.250 | ||||

| Chi2 | 591.349 | 575.758 | ||||

| Adj R2 | 0.283 | 0.279 | 0.569 | 0.568 | ||

| R2 | 0.287 | 0.283 | 0.571 | 0.571 | ||

| Sobel_z | 10.090 | 6.433 | ||||

| Mediated rate | 0.454 | 0.364 | ||||

| N | 11,401 | 11,401 | 11,454 | 11,454 | 11,454 | 11,454 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| INCTRL | INCTRL | CSP | CSP | |

| PSRI | 44.178 * | 41.443 *** | ||

| (1.95) | (9.53) | |||

| PSRI_A | 43.116 * | 32.898 *** | ||

| (1.90) | (7.50) | |||

| INCTRL | 0.007 *** | 0.007 *** | ||

| (4.00) | (4.05) | |||

| Constant | 397.268 *** | 396.348 *** | −79.560 *** | −83.045 *** |

| (12.46) | (12.45) | (−12.83) | (−13.30) | |

| CVs | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES |

| Adj R2 | 0.169 | 0.169 | 0.349 | 0.346 |

| R2 | 0.174 | 0.174 | 0.353 | 0.349 |

| Sobel_z | 1.983 | 1.952 | ||

| Mediated rate | 0.007 | 0.009 | ||

| N | 11,454 | 11,454 | 11,454 | 11,454 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| CSP | CSP | CSP | CSP | |

| PSRI | 48.513 *** | 48.592 *** | ||

| (4.22) | (4.25) | |||

| PSRI×EMKT | −2.362 ** | −2.363 ** | ||

| (−2.25) | (−2.27) | |||

| PSRI×ECOMPE | −41.759 * | −42.848 * | ||

| (−1.81) | (−1.88) | |||

| PSRI_A | 38.833 *** | 38.970 *** | ||

| (3.36) | (3.39) | |||

| PSRI_A×EMKT | −2.425 ** | −2.426 ** | ||

| (−2.29) | (−2.31) | |||

| PSRI_A×ECOMPE | −47.867 ** | −48.767 ** | ||

| (−2.06) | (−2.14) | |||

| EMKT | 1.086 *** | 1.094 *** | 1.115 *** | 1.124 *** |

| (2.92) | (2.96) | (2.96) | (3.00) | |

| ECOMPE | 24.417 *** | 14.954 * | 26.935 *** | 17.442 * |

| (2.79) | (1.67) | (3.04) | (1.93) | |

| Constant | −79.317 *** | −83.588 *** | −82.278 *** | −86.531 *** |

| (−10.62) | (−11.09) | (−10.90) | (−11.35) | |

| CVs | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | NO | YES | NO |

| Industry subcategory FE | NO | YES | NO | YES |

| Adj R2 | 0.350 | 0.351 | 0.346 | 0.348 |

| R2 | 0.353 | 0.356 | 0.350 | 0.353 |

| N | 11,454 | 11,454 | 11,454 | 11,454 |

| Social Trust | Poor | Good | Poor | Good |

|---|---|---|---|---|

| Atmosphere | (1) | (2) | (3) | (4) |

| CSP | CSP | CSP | CSP | |

| PSRI | 37.678 *** | 46.763 *** | ||

| (6.62) | (8.88) | |||

| PSRI_A | 29.304 *** | 37.942 *** | ||

| (5.09) | (7.20) | |||

| Constant | −76.782 *** | −77.399 *** | −80.211 *** | −80.891 *** |

| (−9.51) | (−10.84) | (−9.88) | (−11.25) | |

| CVs | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES |

| Adj R2 | 0.353 | 0.345 | 0.349 | 0.341 |

| R2 | 0.360 | 0.352 | 0.356 | 0.348 |

| N | 5727 | 5727 | 5727 | 5727 |

| Non-SOE | SOE | Non-SOE | SOE | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| CSP | CSP | CSP | CSP | |

| PSRI | 35.816 *** | 48.520 *** | ||

| (7.08) | (6.07) | |||

| PSRI_A | 27.747 *** | 38.859 *** | ||

| (5.42) | (4.86) | |||

| Constant | −69.841 *** | −68.764 *** | −72.324 *** | −73.252 *** |

| (−8.28) | (−6.84) | (−8.45) | (−7.31) | |

| CVs | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES |

| Industry FE | YES | YES | YES | YES |

| Adj R2 | 0.325 | 0.373 | 0.322 | 0.370 |

| R2 | 0.331 | 0.382 | 0.327 | 0.378 |

| N | 7183 | 4271 | 7183 | 4271 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, W.; Hu, R.; Zhang, C.; Shen, Y. Does Socially Responsible Investing Make a Better Society?—A Micro Perspective through Mutual Funds and Their Investee Companies. Sustainability 2023, 15, 8671. https://doi.org/10.3390/su15118671

Wang W, Hu R, Zhang C, Shen Y. Does Socially Responsible Investing Make a Better Society?—A Micro Perspective through Mutual Funds and Their Investee Companies. Sustainability. 2023; 15(11):8671. https://doi.org/10.3390/su15118671

Chicago/Turabian StyleWang, Wennanxiang, Ridong Hu, Cheng Zhang, and Yang Shen. 2023. "Does Socially Responsible Investing Make a Better Society?—A Micro Perspective through Mutual Funds and Their Investee Companies" Sustainability 15, no. 11: 8671. https://doi.org/10.3390/su15118671