Local Digital Economy and Corporate Social Responsibility

1

School of Economics and Trade, Guangdong University of Foreign Studies, Guangzhou 510006, China

2

Research Institute of International Service Economics, Guangdong University of Foreign Studies, Guangzhou 510006, China

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(11), 8487; https://doi.org/10.3390/su15118487

Submission received: 28 April 2023

/

Revised: 21 May 2023

/

Accepted: 22 May 2023

/

Published: 23 May 2023

(This article belongs to the Special Issue Accounting, Corporate Policies and Sustainability)

Abstract

:Utilizing the entropy evaluation approach to construct a local digital economy index, this paper investigates the influence of digital economy development on corporate social responsibility (CSR) using a sample of Chinese listed firms from 2011 to 2020. Our findings indicate that the development of the digital economy can facilitate enterprise digital transformation, enhance agency efficiency, and increase online media attention, thereby significantly promoting CSR performance for local firms. Further analysis shows that the local digital economy has varying impacts on distinct dimensions of CSR, with more pronounced effects observed among state-owned enterprises, firms in secondary industries, large-scale and non-digital firms. Overall, these findings suggest that the development of the digital economy fosters the willingness of firms to engage in CSR, resulting in a favorable interaction between firms and stakeholders.

1. Introduction

As the extent to which corporates benefit or harm social welfare, Corporate Social Responsibility (CSR) refers broadly to conducting social or environmental behaviors beyond compliance with the law and beyond economic profitability maximization [1]. Given its various potential benefits on corporate value [2], innovation [3], reputational risks [4] and other business activities, an increasing number of enterprises/institutional investors have gradually incorporated CSR into their mainstream business strategy and investment decisions [5], and how to effectively strengthen the willingness or impetus of firms to engage in CSR has aroused heated debate among scholars, business ethicists and regulators [6].

Prior literature has discussed the various factors affecting CSR from the perspectives of both internal and external drivers. The internal driver perspective focuses on variables pertaining to enterprise digitization [7,8], organizational efficiency [9], and corporate governance [10]. While keeping in mind their shared objective of fostering CSR and sustainable development as complementary to traditional hard-law regulations [11], many governments, particularly in Europe, have enacted CSR laws and regulations to shape CSR as a new societal governance [6,12], resulting in a reactive approach to CSR instead of a proactive approach [13], thus external driving forces, such as government initiative [6], social media [14,15] and mandatory disclosure [16] have also become crucial determinants of CSR.

Reviewing the related research of CSR so far however, there is a scant amount of literature paying attention to the impact of the digital economy on CSR performance. As a new economic paradigm grounded in digital technology and information networks, the digital economy fundamentally changes the traditional economic environment and activities [17,18], leading to profound restructuring of corporate business models, organizational structures, and market competition patterns. Especially for CSR strategy decisions, a multi-dimensional enterprise behavior containing shareholders, employees, suppliers, consumers, environment, community and so on, will be deeply involved in the internal and external environment changes created by the deep application of digital technologies. As a result, CSR may become an increasingly important issue for firms operating in the digital economy, and it would be of great interest to investigate whether the development of the digital economy could affect the CSR performance for local firms; and what is the mechanism that brings them to this point.

The digital economy could bring about significant changes in the way businesses operate and interact with their stakeholders. From the corporate governance point of view, the digital economy accelerates the speed of information acquisition, storage, and processing, providing firms with adequate opportunities for digital transformation [19], which enables firms to quickly capture and respond to the CSR proposition of various stakeholders based on digital technologies. On the other hand, the information disclosure system of firms to stakeholders would be comprehensively reshaped in the digital context [20], improving the transparency of accounting information [21,22] and decreasing the agency in organizations with strong socially responsible commitment [23], thereby contributing to the suppression of CSR “Greenwashing” behavior and other opportunist tendencies.

Additionally, in view of stakeholder identification, the digital economy has enabled stakeholders to have greater access to information and communication channels with the rise of digital media and industries such as online chats, short videos and livestreaming platforms. Thus, the CSR engagement will be more easily perceived by stakeholders, which can amplify the financial return from a more effective signaling [24], further enhancing the economic motive for firms to invest in CSR. For example, in the “7·20” heavy rainstorm disaster in Zhengzhou, Henan Province of China in 2021, Hongxing Erke Company (ERKE), as a large sportswear firm, donated 50 million Yuan in goods and materials for post-disaster reconstruction, which was quickly fermented in the online media such as TikTok and Internet We-Media, eventually inducing a huge product publicity effect. According to the report released by JD.com, the sales of ERKE increased 52 times year-on-year on 23 July 2021.

On the basis of the above practical observation and theoretical analysis, this paper attempts to fill the gap in the literature and explore the nexus between the local digital economy and CSR. China, as the largest emerging economy, has become increasingly reliant on the digital economy development model but at the same time is characterized by overall-low CSR performance [25,26], offering a suitable sample to examine empirical evidence on this important yet underexplored issue. Hence, using the data of Chinese A-shared listed companies from 2011 to 2020, we find that the development of digital economy significantly promotes local firms’ CSR performance. Our results are robust on a variety of endogenous and robustness levels, such as alternative measures of core variables, propensity score matching estimation, and instrumental variable estimation. Mechanism tests demonstrate that the digital economy can drive enterprise digital transformation, enhance agency efficiency and increase online media attention, thereby encouraging CSR of local firms. We also find that the impact of the local digital economy on different dimensions of CSR is different, and it is more pronounced among state-owned enterprises, firms in secondary industries, large-scale and non-digital enterprises.

This paper makes the following possible contributions. First, while numerous studies have explored the influencing factors of CSR [6,8,10,27], there is limited research on these in the digital economy context, so we expanded CSR research to new economic scenarios; and particularly based on signaling theory, we demonstrate the prevailing digital/online media in the era of digital economy could be used as an important transmission channel for firms to signal their ethical nature, providing a supplement to the relevant literature that mainly concerns traditional media communication [15,28].

Second, in contrast to previous studies that have focused on the digital economy from a specific perspective, such as artificial intelligence [29], big data [30] and the internet [31], we attempt to construct the digital economy index of prefecture-level cities in China with an entropy approach, which is an objective weighting method aiming to scientifically reflect the contribution of various dimensions of evaluation [30,32].

Third, this paper contributes to literature on the impacts of the digital economy at the micro level. Different to the existing studies that mainly address the digital economy at the city or industry level, including the green economy [17] and urban innovation [33], the firm-level analysis in this study enables exploration of the mechanisms of the digital economy, which is useful for policymakers to build a micro foundation for sustainable economic development.

2. Literature Review and Theoretical Analysis

2.1. Digital Economy and CSR

CSR refers to the obligations that firms have to act in a socially and environmentally responsible manner, which are expected by society and various stakeholders. It has been a subject of interest for academics, business practitioners, and policymakers in recent years. The literature on CSR is extensive and covers a broad range of topics, including the definition and conceptualization of CSR, the benefits and drawbacks of CSR, the measurement and reporting of CSR, and the drivers and motivations for CSR that this paper focuses on. The existing literature identifies various factors for enterprises to engage in CSR activities. These include regulatory pressures [6,16], stakeholder demands [7,8,9,10], reputation management [14,15], and pursuit of competitive advantage [15,34,35]. Due to information asymmetry, stakeholders may not effectively monitor CSR behavior and hold corporates accountable for their actions, thus the extent to which enterprises engage in CSR varies.

In the age of digital economy, the CSR operational decisions may be greatly affected. The digital economy is a relatively new and rapidly evolving area of research that refers to economic activity that is based on digital technologies. Most scholars have focused on various consequences of the digital economy on the traditional economic environment and activities, such as the green economy [17], enterprise sustainable development [18], innovation [19,33], high-quality urban economic development [30], and total factor productivity [32]. However, to the best of our knowledge, there is little literature on the combination of digital and CSR, and this study attempts to fill this gap.

The digital economy offers new opportunities for stakeholders to monitor and hold CSR performance through the use of digital technologies. By leveraging digital technologies, firms can mitigate information asymmetries by facilitating truthful disclosure and improving the equitable allocation of resources and corporate governance [36]. Additionally, online media can provide stakeholders with real-time information about CSR performance, facilitating stakeholder engagement and feedback [15]. Therefore, we identify three paths in which the digital economy may affect CSR performance: enterprise digital transformation, agency efficiency, and online media attention. Accordingly, the following hypotheses are proposed in this paper:

Hypothesis 1.

The development of the local digital economy would significantly promote CSR performance.

2.2. The Mechanism of Enterprise Digital Transformation

The digital economy provides key elements such as digital infrastructure, digital platforms and digital technologies for enterprises, which are required by digital transformation of enterprises. Specifically, the development of the digital economy generally requires local government to improve their network infrastructure, public platforms, and databases, as well as implementation of smart environmental protection, smart payment, and intelligence. These improvements accelerate the speed of information acquisition, storage, and processing, providing firms with adequate opportunities for digital transformation [19], which allows firms to transact and engage with suppliers, customers and others to provide them with real-time information interaction about their CSR performance.

In this way, digital technologies enable firms to quickly capture and respond to the CSR proposition of various stakeholders, including promoting sustainable development, supporting social causes, and improving transparency and accountability. For example, online digital platforms can be used to monitor supply chains, track environmental impacts, and engage with stakeholders in real-time, which can help firms to identify and address social and environmental issues more effectively. Thus, the digital economy contributes to the improvement of information transparency to the stakeholders by driving enterprise digital transformation, and creating new chances for business to engage in CSR activities. In view of the above discuss, we propose the following hypothesis:

Hypothesis 1a.

The development of local digital economy can promote CSR performance by facilitating enterprise digital transformation.

2.3. The Mechanism of Agency Efficiency

Driven the principal–agent problems among shareholders, executives and boards of directors, firms may gain profits at the expense of stakeholders [37,38,39], and through the implementation of “Green Washing” behaviors defraud the support of stakeholders [40]. However, the emergence of the digital economy has facilitated the widespread incorporation of digital technology in corporate governance [36], and it has revolutionized the corporate disclosure and shareholder participation system, thus curbing the opportunity behavior of managers.

Through elevating the quality of corporate disclosure and inducing regulatory intervention that promotes responsible governance of enterprises [41], the digital economy not only enhances transparency in business operation and management but also safeguards the rights and interests of shareholders and external investors, which can greatly suppress the information asymmetry and the earning management motivated by opportunistic management tendencies [42]. Hence, the digital economy has the potential to improve CSR performance by effectively alleviating the principal–agent problem. Given the above discussion, we propose the following hypothesis:

Hypothesis 1b.

The development of the local digital economy can promote CSR performance by enhancing agency efficiency.

2.4. The Mechanism of Online Media Attention

According to the signaling theory, firms could signal their ethical nature by implementing CSR initiatives [24]. Through non-reciprocal transfer or even sacrifice, firms consciously carry out some public welfare or sponsorship activities, that will establish a good reputation and corporate image of responsibility, and which may generate a series of consumption effects such as quality commitment and assurance, advertising and shopping guides, psychological effectiveness, etc. [43]. The boost in benefits from this signaling effect can be amplified in the era of digital economy.

The rapid development of the digital economy has resulted in online media platforms rapidly gaining popularity, which provides new ways for firms to showcase their CSR activities [34]. By sharing updates on their CSR activities through online platforms such as TikTok and Kwai, firms can confirm their commitment to CSR and cultivate a positive image in the minds of stakeholders [35]. Moreover, online media attention can help firms to engage with their customers and receive feedback on their CSR initiatives [15], which can be used to improve their CSR strategies and make a greater impact in the community, as well as to identify new opportunities for CSR initiatives that align with stakeholder needs and expectations. Therefore, with the help of online media, the digital economy can assist businesses in engaging with stakeholders, receiving feedback, and enhancing CSR strategies. Based on the above discussion, we propose the following hypothesis:

Hypothesis 1c.

The development of local digital economy can promote CSR performance by increasing online media attention.

3. Research Design

3.1. Sample Selection

The sample is comprised of all listed companies on the Chinese A-share stock market over the period from 2011 to 2020. Our CSR-scores data are collected manually from the HeXun website, and other firm-level financial data are retrieved from the China Stock Market and Accounting Research Database (CSMAR). Specially, the regional digital economy level is calculated by the entropy method based on prefecture-level city data from the China City Statistics Yearbook and the Institute of Digital Finance Peking University. On the basis of the consolidation of the above databases, this paper performs the following processing on the original data. First, we exclude samples from the financial sector according to the classification of China Securities Regulatory Commission (CSRC) due to their unique regulatory nature and different accounting treatment methods. Second, we exclude firms designated by the stock exchanges as receiving special treatment, namely those marked with “ST” and “*ST”. Third, we exclude observations with missing values in the main variables. The final sample is an unbalanced panel of 23,532 firm-year observations for 3014 listed companies.

3.2. Variable Description

3.2.1. Dependent Variable: CSR Performance

We measure a firm’s CSR performance using a score (CSR_score) that reflects the extent of the firm’s involvement in CSR activities. This score is published regularly by HeXun website based on the professional evaluation system of CSR reports of listed companies, which has been used extensively in prior CSR literature [7]. The HeXun CSR score covers the five pillars of CSR, shareholder (30%), employee (15%), supplier, customer, consumer rights and interests (SCC) (15%), environment (20%) and society (20%), each of which sets up secondary and tertiary indicators, respectively, to comprehensively evaluate CSR performance. The higher the CSR_score, the better the CSR performance of a firm.

In the robustness test, we use the data of ESG ratings (ESG_rating) as an alternative measure for CSR performance. Similar to Fang et al. (2023) [8], we use the data of the HuaZheng ESG rating, which is divided into nine categories: AAA, AA, A, BBB, BB, B, CCC, CC, C. We then define the discrete variable ESG_rating which is assigned values from nine to one, respectively, with the gradual decline of HuaZheng ESG rating.

3.2.2. Core Independent Variable: Local Digital Economy Index

To scientifically examine the impact of the digital economy on CSR, it is crucial to measure the regional digital economy development level (Digital_index). As a brand-new economic form following the agricultural and industrial economies, the digital economy is a series of economic activities based on network information and communication technologies [32], thus it should be a complex covering various aspects such as digital infrastructure, digital technology, digital transaction and so on. Referring to the digital economic index system issued by the China Information and Communication Research Institute, and National Bureau of Statistics, and the empirical practice of previous literature [32], we determined two primary indicators: Internet development and digital financial inclusion, to measure the digital economy development of a prefecture-level city after considering the availability and reliability of relevant data and indicators.

For the measurement of internet development, four secondary indicators are included in this paper: penetration rate of internet, the number of internet-related employees, internet-related output, and mobile phone penetration rate. The actual contents corresponding to the above four indicators are: the number of internet users per 100 people, the proportion of employees in computer services and software industries compared to other urban industries, the total value of telecommunications services per capita and the number of mobile phone users per 100 people.

For the measure of digital finance inclusion, the China Digital Financial Inclusion Index issued by the Institute of Digital Finance Peking University was adopted [44]. It was constructed using three secondary indicators: the breadth of coverage of digital finance, the depth of usage of digital finance, and the level of digitalization in inclusive finance. These indicators comprehensively evaluate the level of popularity, service quality, and financial inclusion provided by digital financial services.

The local digital economy index system was established as shown in Table 1, and the final digital economy index was calculated by the entropy method, which can contribute by dealing with the problem of randomness of subjective assignment and overlapping information among the multiple indicators [30], via determining the indicator weights according to the entropy value.

Specifically, in order to eliminate the comparability bias brought by the large difference in the magnitude and unit of secondary indicators, we standardized the primary data initially, i.e.,

where subscript m and t denote the indicator and year, respectively. is the normalized value, is the raw data, is the minimum value, and is the maximum value. Since the attributes of indicators used in this paper are all positive, the larger the value of , the greater the likelihood that digital economy development will occur. Then,

Determine indicator weights:

Calculate the entropy value of each indicator:

The information utility value of each indicator:

The weight of each indicator:

The weights of various indicators of the digital economy in China’s prefecture-level cities during 2011–2020 are shown in Table 2.

Finally, calculate the composite score of the indicator:

3.2.3. Control Variables

Following the related studies [7,8,45,46], we included a variety of control variables in the regression model as follows: (1) Firm size (), measured as the natural logarithm of number of employees; (2) Cost rate (), measured as the ratio of total cost of operations to total operating income; (3) Economic lever (), measured as the ratio of total assets to total liabilities; (4) Net cash flow from operations (), measured as the ratio of the natural logarithm of net cash flow from operations to total liabilities; (5) Proportion of intangible assets (), measured as the ratio of net intangible assets to total assets; (6) Firm age (), represented as the logarithmic transformation of the difference between the statistical time of the sample and the time when the company went public, plus 1; and (7) Liquidity ratio (), measured as the ratio of current assets to current liabilities. The detailed definitions of the variables used in the analysis are shown in Table 3.

3.3. The Model

In order to examine the correlation between the local digital economy and CSR performance, we have constructed the benchmark regression model in the following manner:

where the subscript , , denotes firm, city and year, respectively. The dependent variable is the CSR performance of the firm, the core independent variable represents the digital economy development level of a city. A series of control variables, denoted by , are included to capture other factors that may affect CSR performance. In addition, we also control for firm fixed effects , city fixed effects and time fixed effects . captures the random disturbance term.

The summary statistics of the main variables are presented in Table 4.

4. Empirical Results

4.1. Baseline Results

In this section, the relation between our main independent variables is examined, the digital economy index (Digital_index) calculated by the regional multiple digital indicators, and CSR performance (CSR_score) of local firms. We report estimation results in Table 5. As shown in Column (1), the coefficient of Digital_index is significantly positive (coefficient = 2.585) at the 5% level when only including the fixed effect. Upon introducing several control variables, the core independent variable in Column (2) continues to exhibit a significantly positive effect at a 5% level of significance. These findings provide confirmation that fostering the development of a city’s digital economy is beneficial for incubating CSR performance among local firms. Thus, the baseline results suggest a positive impact of digital economy on CSR, consistent with our Hypothesis 1.

4.2. Robustness Results

4.2.1. Alternative Measures of CSR

For the baseline regression, the primary dependent variable utilized was the CSR_score derived from the annual CSR report text of the firm, as calculated by the HeXun website. To examine the reliability of the baseline findings, we employed the ESG_rating as an alternative measure of CSR. As studied by Gillan et al. (2021) [47], ESG tends to be a more expansive terminology than CSR, and the main difference between them is that the former includes governance explicitly, whereas the latter includes governance issues indirectly. However, overall, the concept and composition of ESG and CSR has a relatively strong correlation.

As discussed in Section 3.2, we used the data of Huangzhen ESG ratings (ESG_rating) as a proxy variable for CSR. Based on the nine rating categories issued by Huazheng, we assigned different values in turn and finally get the variable ESG_rating which ranges from nine to one. A higher ESG_rating means better CSR/ESG performance. Table 6 presents the results. As shown in Column (1), the coefficient of Digital_index is positive and statistically significant at the 1% level, which is in line with the base results.

4.2.2. Propensity Score Matching Estimation

The main findings prove that the regional digital economy can produce a strong positive effect on firms’ CSR performance. However, there may be some endogenous problems due to omitted variables, that is, some control variables that are difficult to observe but may have impacts on CSR performance. Corresponding with the reality of China’s economic development, different regions or cities have obvious differences in the firm characteristics due to various policies, endowments or business environments. Thus, in order to rule out the possibility that the base results are attributable to unobservable firm-level variables, we conducted a Propensity Score Matching (PSM) estimation method to effectively identify the net effect.

The procedure of PSM estimation is as follows. First, we divided the whole sample into a high-Digital group and a low-Digital group according to the average value of the digital economy index of the location of the firm. We set the dummy variable Digital_dummy equal to one if the digital economy index of firm in year is greater than the average value, which was classified into the high-Digital group; and vice versa, Digital_dummy equals to zero and is regarded as the low-Digital group. Second, we estimated a logit model where the dependent variable is Digital_dummy, which includes all the control variables used in the base regression model that may capture firm characteristics and therefore the likelihood of belonging to the high-Digital group. Eventually, we used nearest neighbor matching to perform a pub-back and year-by-year match for the high-Digital group and low-Digital group based on the estimated propensity score, i.e., .

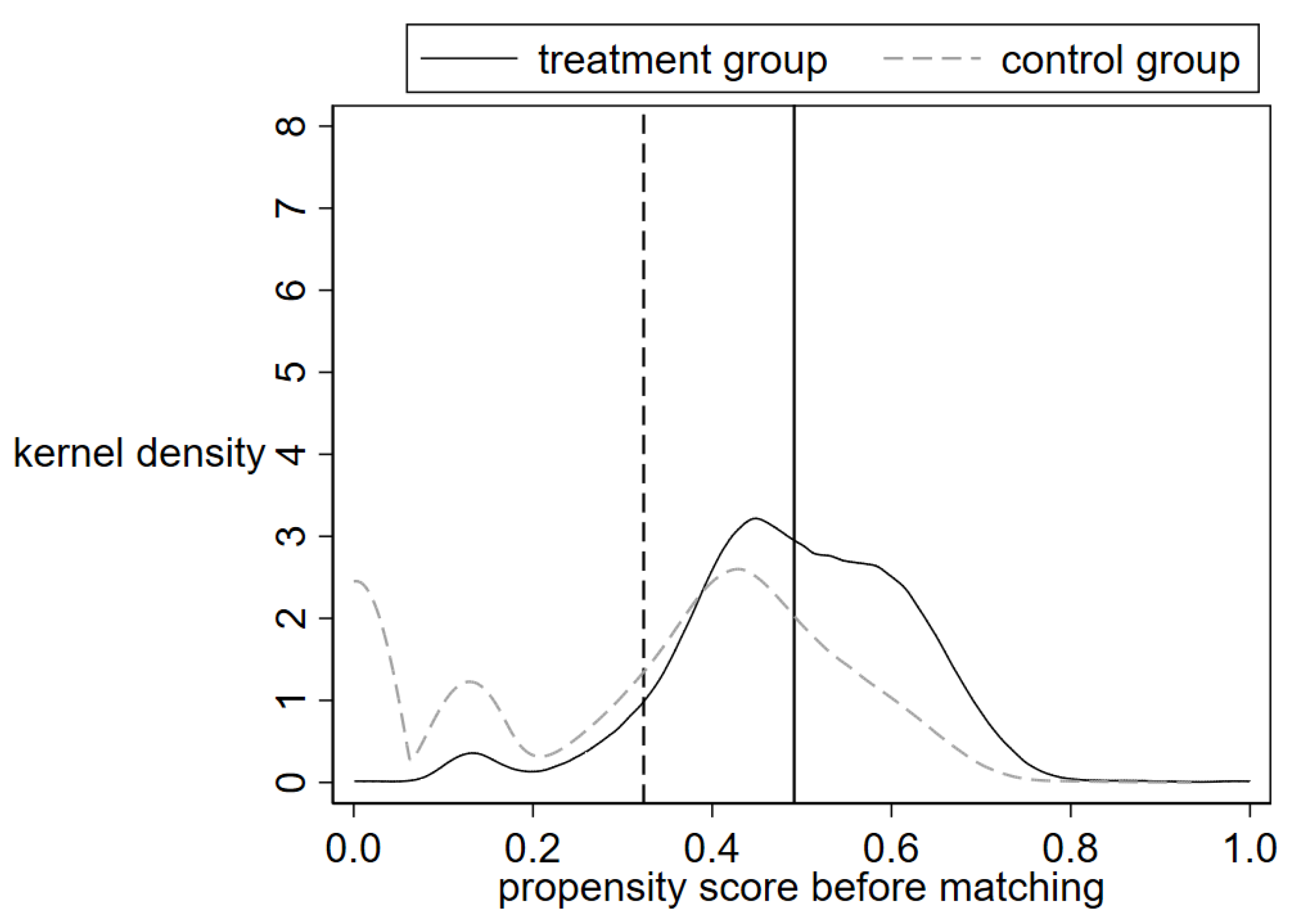

In order to evaluate the validity of the PSM approach, we have presented kernel density diagrams of the propensity scores before and after matching, shown in Figure 1 and Figure 2, respectively. Our findings indicate that the probability density of the PSM scores for the treatment and control groups varies significantly before matching. However, after matching, the probability density of the scores becomes similar, which confirms the validity of the PSM approach.

The above matching ensured that the two groups had comparable characteristics as much as possible, and it provided a better identification of a causal relationship between the regional digital economy development and local firm’s CSR performance. As shown in Column (2) in Table 6, the coefficients of grouping variable Digital_dummy are all significantly positive, indicating the firms in the high-Digital group perform a higher level of CSR compared with those in the low-Digital group. In other words, it is the different development levels of the digital economy that lead to the differences in CSR performance of local firms, which conforms with our main results.

4.2.3. Instrumental Variable Estimation

In addition to omitted variables, there may be some endogenous concerns between regional digital economy development and the CSR performance of local firms due to reverse causality. In this section, we adopt the instrument variable (IV) method to control for possible endogeneity problems.

Reviewing China’s historical development process of information and communication technology (ICT), before the popularization of the network and mobile phones, the fixed telephone penetration usually represents the level of ICT infrastructure of a city. The digital economy as a continuation and upgrading of traditional ICT technology will be affected by the subsequent development and application of the local historical ICT infrastructure based on usage habits, technical level and other factors, satisfying the correlation of instrumental variable selection. Meanwhile, there is no direct relationship between the current firms’ CSR performance and the local historical ICT infrastructure, satisfying the exclusivity of instrumental variable selection as well.

Based on the above logic and referring to previous literature [30], we select the historical data of telecommunication in 1984 as the instrumental variable of the digital economy to re-estimate the base regression model. Due to the original data of the selected instrumental variable beings cross-sectional, it cannot be directly used for the metrological analysis of panel data. Utilizing the framework proposed by Nunn and Qian (2014) [48], we employed the interaction term IV-Digital, which combines the count of international Internet users from the preceding year (time-related) with the number of fixed telephones per million individuals in prefecture-level cities in 1984 (city-related). This amalgamation serves as an instrumental variable in assessing the impact of the digital economy.

Column (3) of Table 6 includes the two-stage least squares (2SLS) regression results using the instrumental variable of IV-Digital. For the validity of the selected instrumental variables, Kleibergen–Paap rk LM statistic rejects the null hypothesis of insufficient recognition at a significance level of 1%, and Kleibergen–Paap rk Wald F statistic (283.96) is greater than the critical value (16.38) at the 10% level of the “Stock–Yogo” weak recognition test, rejecting the null hypothesis of a weak instrumental variable. The coefficient of IV-Digital is still positive and shows a higher statistical significance.

4.2.4. Other Robustness Checks

In order to mitigate the impact of random factors over time within each industry, this study took additional measures to control for industry fixed effects and re-evaluated the baseline regression. Furthermore, considering the potential presence of outliers in the sample, all continuous variables in the base model were trimmed by 1% from both the upper and lower ends before being re-estimated. The outcomes of these adjustments are presented in Columns (4) and (5) of Table 6. Notably, Hypothesis 1 remains valid.

4.3. Underlying Mechanisms

4.3.1. Enterprise Digital Transformation

The digital economy fundamentally changes the traditional economic environment and activities, thus constituting a profound system reform that significantly alters the way we live and how businesses operate. As a result, micro-production units, particularly corporations, must undergo significant restructuring of their business models, organizational structures, and product innovation to promote the digital transformation of internal governance and production processes [19,49]. Additionally, through digital transformation, firms may promote the fulfillment of CSR/ESG by improving the interaction with their stakeholders and other operating conditions [8].

Therefore, we attempt to construct an appropriate variable DCG to measure enterprise digital transformation. Although various aspects such as production processes and internal governance are involved in enterprise digital transformation and it is difficult to measure it precisely, as the major strategy in the digital era, firms will usually disclose relevant digital behaviors in the annual report in order to gain the attention of investors. Hence, we manually collected the frequencies of occurrence of the five characteristic words, including “Artificial intelligence”, “Blockchain”, “Cloud computing”, “Big data” and “Digital technology application” in the annual report, and then take the natural logarithm of the sum of characteristic word frequencies plus one as the proxy index of digital transformation (DCG).

If the DCG mechanism holds, we expected that the regional digital economy would cause a larger increase in CSR performance for local firms with greater digital transformation. We divided our sample into low-DCG and high-DCG samples based on the median of DCG. We re-estimated Equation (1) and present the results in Columns (1) and (2) in Table 7. The findings indicate that the coefficient of Digital_index is more statistically significant in the high-DCG sample, corroborating our Hypothesis 1a.

4.3.2. Agency Efficiency

The digital economy can deal with the information asymmetry under the principal–agent problem and suppress the “Green Washing” behaviors of enterprises that defraud the support of stakeholders. That is, the improvement of agency efficiency would guarantee the fulfillment of CSR to a greater extent. Referring to Singh and Davidson (2003) [50], we used total asset turnover to measure the agency efficiency (AE) of a firm, expressed in the ratio of total operating income to total assets of a firm. Similarly, we divided the sample into low-AE and high-AE groups based on the median of AE. The results presented in Columns (3) and (4) in Table 7 support our expectation, lending support to Hypothesis 1b.

4.3.3. Online Media Attention

From the perspective of public perception, the digital economy makes it easier for stakeholders to access information and communication. Attributed to the rise of digital media and industries such as online chats, short videos and livestreaming platforms, stakeholders can quickly and widely identify the information or news they want to follow. In this way, the CSR behaviors of the local firms will be more easily perceived by the consumers, investors, government and other stakeholders, thereby enhancing a firm’s reputation or goodwill and in turn providing more motivation and willingness for them to engage in CSR initiatives.

Therefore, the external mechanism for the increase in CSR performance is the improvement of online media attention (OMA). Specifically, we use the total amount of online news from firms in the Financial News Database of Chinese Listed Companies (CFND) as a proxy variable for media exposure and divide our sample into low-OMA and high-OMA samples based on the media of OMA. We expect that the effect of the regional digital economy on CSR performance is more prominent among high-OMA local firms. Columns (5) and (6) of Table 7 show the results, indicating that the coefficient of Digital_index is significantly positive for the high-OMA sample but insignificant for the low-OMA firms, which is line with our Hypothesis 1c.

4.4. Heterogeneity Analysis

4.4.1. CSR Dimensions

According to the CSR evaluation system released by the HeXun website, we discuss the impact of the development of the local digital economy on different aspects of CSR in this section. The regression results for each subsample are presented in Columns (1) and (5) of Table 8. It suggests that the digital economy promotes CSR by influencing shareholder responsibility, employee responsibility, social responsibility rather than through supplier, customer and consumer rights (SCC) responsibility and environmental responsibility. The reason behind it may be that the firms tend to be more inclined to invest in CSR activities in the dimensions of shareholder, employees and society (donation-based), because these CSR behaviors are always highly visible and easily attract public attention, which can provide greater operational certainty for bringing economic returns via a reputation or goodwill effect.

4.4.2. Ownership Types

Distinguishing factors exist between state-owned enterprises (SOEs) and non-state-owned enterprises (non-SOEs) concerning their business objectives, external environment, and operational approaches. Due to the special political and social attributes, SOEs are established to provide public goods and services, generate employment opportunities for social welfare, and promote sustainable economic development, whereas non-SOEs are primarily focused on maximizing shareholder profits. Thus, we expect that the impact of the digital economy on CSR is more evident among SOEs than non-SOEs. To test this, we divided the sample into SOEs, private firms, and foreign firms to assess the impact of the digital economy across firms of different ownership types. The results presented in Columns (1)–(3) of Table 9 show that the coefficient of Digital_index is significantly positive only for the sample of SOEs, which is in line with our expectations.

4.4.3. Firm Mode

The impact of the digital economy on CSR may vary depending on whether the firm belongs to a digital industry. Compared with digital firms, non-digital firms have reduced digital technology levels, a lack of digital infrastructure, and shortage of digital talents, and are more vulnerable to the impact of the development of the digital economy, so as to assume more social responsibilities. Therefore, we identified digital firms and non-digital firms according to the CSMAR database and estimated the regression model separately for each group. The results presented in Columns (4) and (5) of Table 9 show that the positive impact of the digital economy on CSR is stronger among non-digital firms.

4.4.4. Operating Industries

The effect of the digital economy on CSR may vary across different industries due to differences in development levels and the impact of information construction. Accordingly, we divide the sample into three categories based on their industry membership, namely agricultural, industrial, and service sectors, and estimate the regression model separately for each group. The results in Columns (1)–(3) of Table 10 show that the coefficient of Digital_index is statistically insignificant for agricultural and service firms, whereas it is significantly positive for industrial firms. This implies that the introduction of the digital economy has resulted in a more pronounced increase in CSR among firms in the secondary industry. The possible reason is that the industrial firms have been hit harder by the digital economy than other firms, and the resulting improvement in digital transformation, agency efficiency and other corporate governance will promote better CSR performance [18].

4.4.5. Firm Size

As firms expand and mature, they may encounter difficulties in adapting to the evolving demands of society and the market, leading to differences in digital adoption and transformation strategies [51]. To examine the impact of digital economy on firms of different size, we divided the sample into large and small firms based on the median age of the sample firms. The regression results for each subsample are presented in Columns (4) and (5) of Table 10. The results show that the coefficient of Digital_index is statistically significant only for large firms. This result shows that larger firms are more socially responsible after being impacted by the digital economy than small firms. The rationale behind this observation may be that large firms on the one hand are better equipped with capital, talent and other digital transformation conditions; on the other hand, large firms have more levels of stakeholders and the principle–agent problem is more complex, so the improvement of their agency efficiency brought by the digital economy is more obvious as well.

5. Discussion of Findings

In the digital era, the application of digital technology in enterprises’ production and management has brought major changes to the development of enterprises. This study focuses on the relationship between local digital economy development and CSR. We find that the development of the local digital economy improves CSR performance by promoting the digital transformation of enterprises, improving agency efficiency, and increasing the attention of online media to enterprises. Moreover, the impact of the local digital economy on enterprises of different dimensions and the nature of CSR is significantly different.

Compared with previous research on the influencing factors of CSR, we explored how the digital development of the external or macro environment affected CSR from the perspective of the local digital economy. Based on signaling theory and “Greenwashing” behavior, we demonstrated the important role played by online media and agency efficiency in the performance of CSR, which provided theoretical guidance for policy formulation and sustainable development of enterprises.

Despite the achievements of this study, there are still shortcomings. On the one hand, as a developing country with rapid economic development and rapid rise of digital economy, the research conclusions may not be applicable to other countries with a rapid digital economy, which makes the research results limited. The follow-up research will focus on the impact on CSR of other countries with rapid digital economy development. On the other hand, during the COVID-19 pandemic, as the virus prevented people from working and consuming, online office and online shopping became mainstream, and these specific behaviors had a significant impact on the production and operations of enterprises [52]. However, due to limited data availability, it is not possible to include the entire sample during the COVID-19 pandemic, and subsequent studies will focus on how the digital economy has impacted CSR during the COVID-19 pandemic.

6. Conclusions

The digital economy has brought about significant changes in the way businesses operate and interact with their stakeholders. As a result, CSR has become an increasingly important issue for companies operating in the digital economy. This paper regards Chinese A-share listed companies during 2011–2020 as a research sample, empirically examined the impact and mechanism of the digital economy on CSR performance. The empirical findings suggested that the digital economy can improve CSR performance through various channels including enterprise digital transformation, agency efficiency and online media attention. The heterogeneity analyses show that the impact of the digital economy on CSR varies according to stakeholder and firm characteristics, namely, the local digital economy would induce somewhat distinct impacts on different dimensions of CSR, and it is more pronounced among state-owned enterprises, firms in secondary industries, large-scale and non-digital firms.

To sum up, this research explores the modern link between local digital economy development and CSR. Due to the recent impact of the COVID-19 pandemic, firms are increasingly affected by the digital economy, online office and online sales enable corporate stakeholders to better supervise CSR behavior, and firms also improve their own value in undertaking CSR. Therefore, policymakers should encourage and support companies to undergo digital transformation by providing incentives, training programs, and financial support [53,54], enable companies to leverage digital technologies to adopt robust governance mechanisms to ensure compliance with CSR objectives and improve their CSR performance. Additionally, governments can collaborate with media organizations and digital platforms to highlight and promote companies that demonstrate exemplary CSR practices. This will encourage companies to prioritize CSR and engage in socially responsible activities, knowing that their efforts will be recognized and rewarded [55]. In addition, investing in capacity building and education programs will enhance CSR knowledge and skills among digital economy professionals, promote the integration of CSR principles and practices into relevant academic curricula and professional development courses. This will contribute to a skilled workforce that understands the importance of CSR and can effectively drive its implementation in the digital economy, promoting CSR performance.

Author Contributions

Conceptualization, Y.H. and Q.L.; methodology, Q.L.; software, Y.H.; writing—original draft preparation, Y.H.; writing—review and editing, Q.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by National Natural Science Foundation of China (72203048) and Guangdong Basic and Applied Basic Research Foundation (2021A1515110226).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Fatima, T.; Elbanna, S. Corporate social responsibility (CSR) implementation: A review and a research agenda towards an integrative framework. J. Bus. Ethics 2023, 183, 105–121. [Google Scholar] [CrossRef] [PubMed]

- Chen, R.C.Y.; Lee, C.-H. Assessing whether corporate social responsibility influence corporate value. Appl. Econ. 2017, 49, 5547–5557. [Google Scholar] [CrossRef]

- Chkir, I.; Hassan, B.E.H.; Rjiba, H.; Saadi, S. Does corporate social responsibility influence corporate innovation? International evidence. Emerg. Mark. Rev. 2021, 46, 100746. [Google Scholar] [CrossRef]

- Karwowski, M.; Raulinajtys-Grzybek, M. The application of corporate social responsibility (CSR) actions for mitigation of environmental, social, corporate governance (ESG) and reputational risk in integrated reports. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1270–1284. [Google Scholar] [CrossRef]

- Yin, J.; Zhang, Y. Institutional dynamics and corporate social responsibility (CSR) in an emerging country context: Evidence from China. J. Bus. Ethics 2012, 111, 301–316. [Google Scholar] [CrossRef]

- Liu, Q.; Wang, L.F.; Chen, C.L. CSR in an oligopoly with foreign competition: Policy and welfare implications. Econ. Model. 2018, 72, 1–7. [Google Scholar] [CrossRef]

- Na, C.; Chen, X.; Li, X.; Li, Y.; Wang, X. Digital transformation of value chains and CSR performance. Sustainability 2022, 14, 10245. [Google Scholar] [CrossRef]

- Fang, M.; Nie, H.; Shen, X. Can enterprise digitization improve ESG performance? Econ. Model. 2023, 118, 106101. [Google Scholar] [CrossRef]

- Filatotchev, I.; Nakajima, C. Corporate governance, responsible managerial behavior, and corporate social responsibility: Organizational efficiency versus organizational legitimacy? Acad. Manag. Perspect. 2014, 28, 289–306. [Google Scholar] [CrossRef]

- Sarhan, A.A.; Al-Najjar, B. The influence of corporate governance and shareholding structure on corporate social responsibility: The key role of executive compensation. Int. J. Financ. Econ. 2022, 7, 1–25. [Google Scholar] [CrossRef]

- Zhou, S. Reporting and Assurance of Climate-Related and Other Sustainability Information: A Review of Research and Practice. Aust. Account. Rev. 2022, 32, 315–333. [Google Scholar] [CrossRef]

- Gatti, L.; Vishwanath, B.; Seele, P.; Cottier, B. Are We Moving Beyond Voluntary CSR? Exploring Theoretical and Managerial Implications of Mandatory CSR Resulting from the New Indian Companies Act. J. Bus. Ethics 2018, 160, 961–972. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. “Implicit” and “explicit” CSR: A conceptual framework for a comparative understanding of corporate social responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Nash, R.; Patel, A. New evidence on the role of the media in corporate social responsibility. J. Bus. Ethics 2019, 154, 1051–1079. [Google Scholar] [CrossRef]

- Pilgrim, K.; Bohnet-Joschko, S. Corporate Social Responsibility on Twitter: A Review of Topics and Digital Communication Strategies’ Success Factors. Sustainability 2022, 14, 16769. [Google Scholar] [CrossRef]

- Ni, X.; Zhang, H. Mandatory corporate social responsibility disclosure and dividend payouts: Evidence from a quasi-natural experiment. Account. Financ. 2019, 58, 1581–1612. [Google Scholar] [CrossRef]

- Zhang, W.; Zhang, S.; Bo, L.; Haque, M.; Liu, E. Does China’s Regional Digital Economy Promote the Development of a Green Economy? Sustainability 2023, 15, 1564. [Google Scholar] [CrossRef]

- Zhou, Z.; Liu, W.; Cheng, P.; Li, Z. The impact of the digital economy on enterprise sustainable development and its spatial-temporal evolution: An empirical analysis based on urban panel data in China. Sustainability 2022, 14, 11948. [Google Scholar] [CrossRef]

- Li, R.; Rao, J.; Wan, L. The digital economy, enterprise digital transformation, and enterprise innovation. Manag. Decis. Econ. 2022, 43, 2875–2886. [Google Scholar] [CrossRef]

- Hinings, B.; Gegenhuber, T.; Greenwood, R. Digital innovation and transformation: An institutional perspective. Inf. Organ. 2018, 28, 52–61. [Google Scholar] [CrossRef]

- Carnegie, G.D.; Ferri, P.; Parker, L.D.; Sidaway, S.I.L.; Tsahuridu, E.E. Accounting as Technical, Social and Moral Practice: The Monetary Valuation of Public Cultural, Heritage and Scientific Collections in Financial Reports. Aust. Account. Rev. 2022, 32, 460–472. [Google Scholar] [CrossRef]

- Gutmayer, T.; Cerbone, D.; Maroun, W. An Evaluation of Business Model Disclosures in Integrated Reports. Aust. Account. Rev. 2022, 32, 220–237. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; Banerjee, S.; García-Sánchez, I.M. Corporate social responsibility as a strategic shield against costs of earnings management practices. J. Bus. Ethics 2016, 133, 305–324. [Google Scholar] [CrossRef]

- Zerbini, F. CSR initiatives as market signals: A review and research agenda. J. Bus. Ethics 2017, 146, 1–23. [Google Scholar] [CrossRef]

- Kuo, L.; Yeh, C.-C.; Yu, H.-C. Disclosure of corporate social responsibility and environmental management: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 273–287. [Google Scholar] [CrossRef]

- Su, R.; Zhong, W. Corporate Communication of CSR in China: Characteristics and Regional Differences. Sustainability 2022, 14, 16303. [Google Scholar] [CrossRef]

- Xu, S.; Wang, F.; Cullinan, C.P.; Dong, N. Corporate Tax Avoidance and Corporate Social Responsibility Disclosure Readability: Evidence from China. Aust. Account. Rev. 2022, 32, 267–289. [Google Scholar] [CrossRef]

- Vogler, D.; Eisenegger, M. CSR communication, corporate reputation, and the role of the news media as an agenda-setter in the digital age. Bus. Soc. 2021, 60, 1957–1986. [Google Scholar] [CrossRef]

- Acemoglu, D.; Restrepo, P. Robots and jobs: Evidence from US labor markets. J. Polit. Econ. 2020, 128, 2188–2244. [Google Scholar] [CrossRef]

- Guo, B.; Wang, Y.; Zhang, H.; Liang, C.; Feng, Y.; Hu, F. Impact of the digital economy on high-quality urban economic development: Evidence from Chinese cities. Econ. Model. 2023, 120, 106194. [Google Scholar] [CrossRef]

- Li, G.; Zhou, X.; Bao, Z. A Win–Win Opportunity: The Industrial Pollution Reduction Effect of Digital Economy Development—A Quasi-Natural Experiment Based on the “Broadband China” Strategy. Sustainability 2022, 14, 5583. [Google Scholar] [CrossRef]

- Pan, W.; Xie, T.; Wang, Z.; Ma, L. Digital economy: An innovation driver for total factor productivity. J. Bus. Res. 2022, 139, 303–311. [Google Scholar] [CrossRef]

- Xu, J.; Li, W. The Impact of the Digital Economy on Innovation: New Evidence from Panel Threshold Model. Sustainability 2022, 14, 15028. [Google Scholar] [CrossRef]

- Edgerly, S.; Thorson, K. Political communication and public opinion: Innovative research for the digital age. Public Opin. Q. 2020, 84, 189–194. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C.; Georgiadis, A.P.; Carroll, C.E.; Siegel, D.S. Does media attention drive corporate social responsibility? J. Bus. Res. 2012, 65, 1622–1627. [Google Scholar] [CrossRef]

- Sama, L.M.; Stefanidis, A.; Casselman, R.M. Rethinking corporate governance in the digital economy: The role of stewardship. Bus. Horiz. 2022, 65, 535–546. [Google Scholar] [CrossRef]

- Nguyen, T.T.M.; Evans, E.; Lu, M. Perceptions of independent directors about their roles of and challenges on corporate boards: Evidence from a survey in Vietnam. Asian Rev. Account. 2019, 27, 69–96. [Google Scholar] [CrossRef]

- Le, C.H.A.; Shan, Y.; Taylor, S. Executive compensation and financial performance measures: Evidence from significant financial institutions. Aust. Account. Rev. 2020, 30, 159–177. [Google Scholar] [CrossRef]

- Hasan, B.T.; Chand, P.; Lu, M. Influence of auditor’s gender, experience, rule observance attitudes and critical thinking disposition on materiality judgements. Int. J. Audit. 2021, 25, 188–205. [Google Scholar] [CrossRef]

- Ioannou, I.; Kassinis, G.; Papagiannakis, G. The impact of perceived greenwashing on customer satisfaction and the contingent role of capability reputation. J. Bus. Ethics 2022. [Google Scholar] [CrossRef]

- An, Y.; Jin, H.; Liu, Q.; Zheng, K. Media attention and agency costs: Evidence from listed companies in China. J. Int. Money Financ. 2022, 124, 102609. [Google Scholar] [CrossRef]

- Kimani, D.; Adams, K.; Attah-Boakye, R.; Ullah, S.; Frecknall-Hughes, J.; Kim, J. Blockchain, business and the fourth industrial revolution: Whence, whither, wherefore and how? Technol. Forecast. Soc. 2020, 161, 120254. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Chen, S.; Zhang, H. Does digital finance promote manufacturing servitization: Micro evidence from China. Int. Rev. Econ. Financ. 2021, 76, 856–869. [Google Scholar] [CrossRef]

- Xu, Z.; Chen, Z.; Deng, L.; Yu, Y. The Impact of Mandatory Deleveraging on Corporate Tax Avoidance: Evidence from a Quasi-experiment in China. Aust. Account. Rev. 2022, 32, 352–366. [Google Scholar] [CrossRef]

- Xiao, H.; Xi, J. The Impact of Institutional Cross-ownership on Corporate Tax Avoidance: Evidence from Chinese Listed Firms. Aust. Account. Rev. 2023, 33, 86–105. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Financ. 2021, 66, 101889. [Google Scholar] [CrossRef]

- Nunn, N.; Qian, N. US Food Aid and Civil Conflict. Am. Econ. Rev. 2014, 104, 1630–1666. [Google Scholar] [CrossRef]

- Peng, Y.; Tao, C. Can digital transformation promote enterprise performance?—From the perspective of public policy and innovation. J. Innov. Knowl. 2022, 7, 100198. [Google Scholar] [CrossRef]

- Singh, M.; Iii, W.N.D. Agency costs, ownership structure and corporate governance mechanisms. J. Bank. Financ. 2003, 27, 793–816. [Google Scholar] [CrossRef]

- McElheran, K. Do Market Leaders Lead in Business Process Innovation? The Case(s) of E-business Adoption. Manag. Sci. 2015, 61, 1197–1216. [Google Scholar] [CrossRef]

- Hao, J.; Pham, V.T. COVID-19 Disclosures and Market Uncertainty: Evidence from 10-Q Filings. Aust. Account. Rev. 2022, 32, 238–266. [Google Scholar] [CrossRef]

- Ryan, J.; Tiller, D. A Recent Survey of GHG Emissions Reporting and Assurance. Aust. Account. Rev. 2022, 32, 181–187. [Google Scholar] [CrossRef]

- Chen, X.; Lu, M.; Shan, Y.; Zhang, Y. Australian evidence on analysts’ cash flow forecasts: Issuance, accuracy and usefulness. Account. Financ. 2021, 61, 3–50. [Google Scholar] [CrossRef]

- Jia, J.; Li, Z. Corporate Environmental Performance and Financial Distress: Evidence from Australia. Aust. Account. Rev. 2022, 32, 188–200. [Google Scholar] [CrossRef]

Figure 1.

The kernel density diagram of propensity score before matching.

Figure 2.

The kernel density diagram of propensity score after matching.

{kind=link}

{kind=link}

Table 1.

Evaluation index system of the local digital economy.

| Primary Indicators | Secondary Indicators | Interpretation | Symbol | Attributes |

|---|---|---|---|---|

| Internet development | Penetration rate of internet | The number of Internet users per 100 people | Z1 | + |

| The number of internet-related employees | The proportion of employees in computer services and the software industry compared to other urban industries | Z2 | + | |

| Internet-related output | The total value of telecommunications services per capita | Z3 | + | |

| The total value of postal services per capita | Z4 | + | ||

| Mobile phone penetration rate | Number of mobile phone users per 100 people | Z5 | + | |

| Digital finance inclusive development | Digital financial inclusion | China Digital Financial Inclusion Index | Z6 | + |

Table 2.

The weights of indicators of the digital economy.

| Indicators | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|

| Z1 | 0.209 | 0.181 | 0.139 | 0.141 | 0.134 | 0.110 | 0.098 | 0.060 | 0.077 | 0.125 |

| Z2 | 0.145 | 0.147 | 0.087 | 0.138 | 0.151 | 0.171 | 0.182 | 0.216 | 0.153 | 0.090 |

| Z3 | 0.140 | 0.164 | 0.138 | 0.142 | 0.165 | 0.174 | 0.146 | 0.242 | 0.314 | 0.324 |

| Z4 | 0.333 | 0.310 | 0.438 | 0.411 | 0.437 | 0.463 | 0.435 | 0.421 | 0.303 | 0.213 |

| Z5 | 0.095 | 0.116 | 0.158 | 0.107 | 0.051 | 0.046 | 0.046 | 0.038 | 0.107 | 0.086 |

| Z6 | 0.077 | 0.082 | 0.039 | 0.060 | 0.061 | 0.036 | 0.093 | 0.022 | 0.046 | 0.163 |

Table 3.

Variable definitions.

| Variables | Variable Name | Definition |

|---|---|---|

| The dependent variable | CSR_score | Corporate social responsibility, measured as the CSR score published by HeXun website |

| ESG_rating | Corporate ESG, measured as the nine grades of AAA-C are assigned to nine to one successively | |

| Core independent variable | Digital_index | Digital economy development level of a city, the weight of internet penetration, number of internet employees, internet-related outputs, mobile phone penetration and China Digital Financial Inclusion Index are calculated by the entropy method to get the comprehensive development level of the digital economy |

| Control variables | Size | Firm size, measured as the natural logarithm of the number of employees |

| Ci | Cost rate, measured as the ratio of total cost of operations to total operating income | |

| Fi | Economic levers, measured as the ratio of total assets to total liabilities | |

| Opncf | Net cash flow from operations, measured as the ratio of the natural logarithm of net cash flow from operations to total liabilities | |

| Ia | Proportion of intangible assets, measured as the ratio of net intangible assets to total assets | |

| Age | Enterprise age, represented as the logarithmic transformation of the difference between the statistical time of the sample and the time when the company went public, plus one | |

| Td | Liquidity ratio, measured as the ratio of current assets to current liabilities | |

| Mechanism variables | DCG | Enterprise digitalization, measured as the natural logarithm of the sum of the occurrences plus one of the “Artificial intelligence technology” “Blockchain technology”, “Cloud computing technology”, “Big data technology” and “Digital technology application” in the financial report |

| OMA | Online media attention, measured by the total number of company news occurrences in the network | |

| AE | Agency efficiency, measured as the ratio of total operating income to total assets |

Table 4.

Summary statistics.

| Variable | Obs | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| CSR_score | 24,532 | 23.981 | 15.316 | −18.450 | 90.870 |

| ESG_rating | 24,532 | 6.520 | 1.117 | 1.000 | 9.000 |

| Digital_index | 24,532 | 0.267 | 0.190 | 0.006 | 0.911 |

| Size | 24,525 | 7.680 | 1.302 | 1.946 | 13.223 |

| Ci | 24,531 | 0.949 | 0.518 | −22.642 | 45.438 |

| Fi | 24,532 | 3.670 | 4.306 | 0.511 | 141.245 |

| Opncf | 24,532 | 0.186 | 0.493 | −25.043 | 23.429 |

| Ia | 24,242 | 0.048 | 0.062 | 0.000 | 0.938 |

| Age | 24,527 | 2.867 | 0.347 | 0.693 | 4.143 |

| Td | 24,532 | 2.705 | 4.188 | 0.026 | 204.742 |

| DCG | 24,532 | 1.308 | 1.387 | 0.000 | 6.282 |

| Online | 24,532 | 333.667 | 896.034 | 1.000 | 49,431.000 |

| Agency | 24,531 | 0.627 | 0.536 | 0.001 | 11.416 |

Table 5.

Local Digital economy and CSR performance: baseline results.

| Variable | (1) | (2) |

|---|---|---|

| CSR_score | CSR_score | |

| Digital_index | 2.585 ** | 2.645 ** |

| (1.101) | (1.090) | |

| Size | 1.772 *** | |

| (0.309) | ||

| Ci | −3.539 * | |

| (1.894) | ||

| Fi | 0.006 | |

| (0.060) | ||

| Opncf | 1.100 *** | |

| (0.311) | ||

| Ia | −13.530 *** | |

| (5.033) | ||

| Age | −0.473 | |

| (2.320) | ||

| Td | −0.031 | |

| (0.056) | ||

| Year FE | Yes | Yes |

| Firm FE | Yes | Yes |

| City FE | Yes | Yes |

| Cons | 23.283 *** | 14.788 ** |

| (0.297) | (7.190) | |

| Observations | 24,088 | 23,784 |

| R-squared | 0.528 | 0.538 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

Table 6.

Robustness test.

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| ESG_rating | PSM | IV-Estimation | Industry Fixed Effect | Winsor 1% | |

| IV-Digital | 59.481 *** | ||||

| (13.738) | |||||

| Digital_index | 0.213 *** | 2.562 ** | 2.070 ** | ||

| (0.077) | (1.078) | (1.025) | |||

| Digital_dummy | 3.443 * | ||||

| (2.039) | |||||

| Size | 0.147 *** | 2.013 *** | 1.760 *** | 1.766 *** | 2.002 *** |

| (0.020) | (0.429) | (0.322) | (0.309) | (0.309) | |

| Ci | −0.035 | −1.917 | −3.549 * | −3.507 * | −35.004 *** |

| (0.036) | (3.091) | (1.833) | (1.883) | (1.250) | |

| Fi | 0.013 *** | −11.532 *** | −0.022 | 0.014 | −0.126 |

| (0.005) | (2.345) | (0.060) | (0.060) | (0.115) | |

| Opncf | 0.004 | −0.016 | 1.254 *** | 1.073 *** | 1.057 ** |

| (0.017) | (0.107) | (0.328) | (0.306) | (0.434) | |

| Ia | −0.426 * | −16.808 *** | −14.708 *** | −12.648 *** | −15.303 *** |

| (0.249) | (6.203) | (5.128) | (4.901) | (4.675) | |

| Age | −0.360 ** | 0.620 * | 1.588 | −0.146 | 2.259 |

| (0.152) | (0.357) | (2.461) | (2.316) | (2.774) | |

| Td | −0.007 * | −0.010 | −0.015 | −0.037 | −0.048 |

| (0.004) | (0.094) | (0.061) | (0.056) | (0.127) | |

| Kleibergen–Paap rk LM statistic | 247.08 *** | ||||

| Kleibergen–Paap rk Wald F statistic | 283.96 | ||||

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Firm FE | Yes | Yes | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | ||||

| Cons | 6.382 *** | 25.140 *** | 13.834 * | 34.774 *** | |

| (0.453) | (9.245) | (7.151) | (8.202) | ||

| Observations | 23,784 | 10,788 | 23,784 | 23,783 | 20,410 |

| R-squared | 0.660 | 0.628 | −0.135 | 0.543 | 0.571 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively. The critical value for the “Stock–Yogo” weak identification test at a significance level of 10% is determined to be 16.38.

Table 7.

Tests of underlying mechanisms.

| Variable | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Low-DCG | High-DCG | Low-AE | High-AE | Low-OMA | High-OMA | |

| Digital_index | 1.955 | 2.578 * | 2.222 | 3.230 ** | 0.485 | 5.377 *** |

| (1.749) | (1.349) | (1.490) | (1.578) | (1.081) | (1.907) | |

| Size | 1.326 *** | 1.608 *** | 1.648 *** | 1.407 *** | 1.181 *** | 2.401 *** |

| (0.426) | (0.483) | (0.384) | (0.491) | (0.381) | (0.448) | |

| Ci | −2.395 * | −10.301 *** | −2.545 * | −50.058 *** | −12.753 *** | −2.055 * |

| (1.304) | (3.895) | (1.352) | (3.614) | (2.481) | (1.230) | |

| Fi | −0.065 | 0.157 | 0.039 | −0.439 ** | 0.114 | −0.025 |

| (0.075) | (0.106) | (0.058) | (0.199) | (0.076) | (0.093) | |

| Opncf | 0.819 *** | 1.089 * | 0.567 * | 0.193 | 0.950 *** | 1.441 ** |

| (0.315) | (0.574) | (0.299) | (0.481) | (0.298) | (0.613) | |

| Ia | −7.727 | −24.892 *** | −13.769 ** | −17.254 ** | −11.220 * | −13.740 ** |

| (5.403) | (8.747) | (5.738) | (8.242) | (6.278) | (6.532) | |

| Age | −3.443 | 2.450 | 2.330 | −0.390 | 0.319 | −1.822 |

| (3.353) | (3.558) | (3.193) | (3.595) | (2.833) | (3.738) | |

| Td | 0.034 | −0.219 ** | −0.063 | 0.278 * | −0.061 | −0.104 |

| (0.066) | (0.087) | (0.051) | (0.164) | (0.064) | (0.072) | |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Firm FE | Yes | Yes | Yes | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Cons | 26.619 *** | 13.471 | 6.688 | 62.317 *** | 23.813 *** | 13.615 |

| (9.926) | (11.302) | (9.549) | (11.117) | (8.754) | (11.220) | |

| Observations | 11,465 | 11,774 | 11,490 | 11,807 | 11,780 | 11,312 |

| R-squared | 0.625 | 0.567 | 0.578 | 0.597 | 0.572 | 0.588 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

Table 8.

Heterogeneity analysis: Different dimensions of CSR.

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Shareholder | Employees | SCC | Environment | Society | |

| Digital_index | 0.910 ** | 0.421 ** | 0.199 | 0.510 | 0.604 * |

| (0.427) | (0.200) | (0.327) | (0.359) | (0.322) | |

| Size | 0.408 *** | 0.259 *** | 0.340 *** | 0.436 *** | 0.329 *** |

| (0.132) | (0.062) | (0.086) | (0.093) | (0.079) | |

| Ci | −2.793 * | 0.017 | −0.008 | 0.016 | −0.771 * |

| (1.490) | (0.030) | (0.034) | (0.049) | (0.462) | |

| Fi | 0.039 | −0.022 * | −0.012 | −0.011 | 0.012 |

| (0.040) | (0.013) | (0.018) | (0.018) | (0.016) | |

| Opncf | 1.134 *** | 0.013 | −0.039 | −0.071 | 0.062 |

| (0.272) | (0.059) | (0.068) | (0.078) | (0.064) | |

| Ia | −9.611 *** | −0.411 | −1.345 | −0.911 | −1.253 |

| (2.197) | (0.825) | (1.322) | (1.531) | (0.970) | |

| Age | −5.079 *** | 1.026 ** | 2.400 *** | 0.923 | 0.256 |

| (0.817) | (0.503) | (0.712) | (0.881) | (0.441) | |

| Td | 0.049 | −0.016 | −0.025 * | −0.034 ** | −0.006 |

| (0.051) | (0.012) | (0.015) | (0.016) | (0.013) | |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Firm FE | Yes | Yes | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes | Yes | Yes |

| Cons | 27.879 *** | −2.410 | −8.025 *** | −4.583 * | 1.926 |

| (2.990) | (1.484) | (2.125) | (2.575) | (1.430) | |

| Observations | 23,784 | 23,784 | 23,784 | 23,784 | 23,784 |

| R-squared | 0.624 | 0.535 | 0.448 | 0.446 | 0.511 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

Table 9.

Heterogeneity analysis: the role of ownership types and firm mode.

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| SOEs | Private | Foreign | Digital | Non-Digital | |

| Digital_index | 4.960 ** | 1.276 | −0.231 | 0.868 | 2.645 ** |

| (2.120) | (1.303) | (5.054) | (2.208) | (1.090) | |

| Size | 1.099 * | 1.595 *** | 2.487 | 2.179 *** | 1.772 *** |

| (0.598) | (0.373) | (1.608) | (0.682) | (0.309) | |

| Ci | −15.364 *** | −2.266 * | −31.777 *** | −11.250 *** | −3.539 * |

| (3.824) | (1.311) | (6.863) | (3.471) | (1.894) | |

| Fi | −0.252 | 0.056 | 0.291 | 0.127 | 0.006 |

| (0.161) | (0.063) | (0.683) | (0.135) | (0.060) | |

| Opncf | 0.656 | 0.944 *** | 2.630 | 0.339 | 1.100 *** |

| (1.128) | (0.278) | (1.921) | (0.541) | (0.311) | |

| Ia | −6.957 | −15.150 *** | −10.378 | −24.945 ** | −13.530 *** |

| (8.608) | (5.192) | (27.754) | (11.579) | (5.033) | |

| Age | −17.595 *** | 2.103 | −14.221 | 8.389 * | −0.473 |

| (5.264) | (2.541) | (11.663) | (4.444) | (2.320) | |

| Td | 0.358 | −0.037 | −0.762 | −0.200 * | −0.031 |

| (0.231) | (0.053) | (0.722) | (0.116) | (0.056) | |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Firm FE | Yes | Yes | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes | Yes | Yes |

| Cons | 83.118 *** | 6.829 | 77.700 ** | −6.048 | 14.788 ** |

| (16.574) | (7.648) | (36.313) | (13.664) | (7.190) | |

| Observations | 8753 | 13,069 | 749 | 3882 | 23,784 |

| R-squared | 0.569 | 0.539 | 0.657 | 0.561 | 0.538 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

Table 10.

Heterogeneity analysis: the role of operating industries and firm size.

| Variable | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Agricultural | Industrial | Service | Large-Scale | Small-Scale | |

| Digital_index | 14.438 | 2.765 ** | 0.681 | 3.382 ** | 1.824 |

| (9.699) | (1.334) | (1.922) | (1.663) | (1.213) | |

| Size | 4.586 | 1.439 *** | 1.988 *** | 0.921 * | 1.025 *** |

| (3.587) | (0.403) | (0.517) | (0.555) | (0.342) | |

| Ci | −15.377 *** | −7.139 *** | −1.855 | −9.597 *** | −2.940 * |

| (5.048) | (2.404) | (1.276) | (3.414) | (1.689) | |

| Fi | 0.059 | 0.042 | −0.063 | 0.210 | 0.058 |

| (0.738) | (0.064) | (0.132) | (0.260) | (0.051) | |

| Opncf | 2.567 * | 1.038 *** | 0.092 | 3.554 *** | 0.613 ** |

| (1.331) | (0.346) | (0.516) | (0.839) | (0.271) | |

| Ia | 23.287 | −16.609 *** | −12.810 | −3.746 | −27.022 *** |

| (40.631) | (5.421) | (8.606) | (7.800) | (5.715) | |

| Age | −28.425 | 3.042 | −6.953 | −3.466 | −3.877 |

| (26.644) | (2.793) | (4.684) | (4.520) | (2.715) | |

| Td | 0.540 | −0.074 | 0.038 | −0.501 *** | −0.011 |

| (0.794) | (0.058) | (0.140) | (0.185) | (0.048) | |

| Year FE | Yes | Yes | Yes | Yes | Yes |

| Firm FE | Yes | Yes | Yes | Yes | Yes |

| City FE | Yes | Yes | Yes | Yes | Yes |

| Cons | 73.627 | 10.103 | 33.654 ** | 37.269 *** | 27.941 *** |

| (79.075) | (8.440) | (14.244) | (14.358) | (8.150) | |

| Observations | 262 | 17,300 | 6123 | 11,941 | 11,572 |

| R-squared | 0.541 | 0.542 | 0.563 | 0.570 | 0.611 |

Note: The standard errors, clustered at the firm level, are presented in parentheses. The significance levels *, **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hu, Y.; Liu, Q. Local Digital Economy and Corporate Social Responsibility. Sustainability 2023, 15, 8487. https://doi.org/10.3390/su15118487

AMA Style

Hu Y, Liu Q. Local Digital Economy and Corporate Social Responsibility. Sustainability. 2023; 15(11):8487. https://doi.org/10.3390/su15118487

Chicago/Turabian StyleHu, Yong, and Qian Liu. 2023. "Local Digital Economy and Corporate Social Responsibility" Sustainability 15, no. 11: 8487. https://doi.org/10.3390/su15118487

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.