1. Introduction

There is an increasing need for investments in sustainable technologies in the construction industry. The construction industry is a heavy user of resources and has a high impact in terms of energy consumption and greenhouse gas emissions [

1]. Investments in technologies might reduce emissions, reduce energy needs, and reduce pollution during manufacture. On the face of it, we might expect to see significant and sustained investments in environmental sustainability technologies [

2]. Yet, there is evidence that firms in the construction industry are hesitant to make investments [

3]. There is limited evidence on how construction firms can best navigate the situation and plan investments that are economically sustainable and provide long-term advantages in the market.

Firms may be inclined to further exploit their current capabilities and undertake incremental improvements in their products and processes. These projects tend to be less risky as they do not push capabilities far. However, they are not able to deliver substantial improvements in sustainability outcomes [

4]. Consequentially, while they have little risk, there is also limited upside return potential. In contrast, a firm might opt for a more radical investment in environmental sustainability initiatives. This may be expected to be more complex, take longer, or require a greater uncertainty in investment amounts [

5]. Given the higher risks and the longer-term investment profiles, the greater levels of uncertainty would normally suggest that the concerns of risk may balance out any perception of greater returns. While Kajander et al. [

6] examined more radical investments in technology in construction, showing a positive stock market reaction to investments, Duong et al. [

7] showed comparable stock market reactions to more incremental investments, suggesting investor concerns not just with potential returns but also the risks that firms take on to gain these returns. This shows that investors value business process improvements that provide contextually sensible risk-return profiles [

8].

Meanwhile, not all firms are equally able to make investments in advancing their environmental sustainability technologies [

9,

10]. For instance, firms that are more highly leveraged or have a reduced current ratio (reflecting higher short-term liabilities compared to assets) may be in a position where taking on more substantial risk is less welcome [

11]. In contrast, firms that are effective managers of their capital, as reflected in measures of turnover of working capital or capital, are likely effectively managed with a higher emphasis placed on risk management and conservative investments and operations.

Despite this research, there is evidence that these investments are beneficial for the construction industry, but little guidance just on how to make the investments profitable [

12]. As a consequence, this research aims to develop a configurational theory of environmentally sustainable investments in construction. The research question that this research aims to address is: what configuration of elements and factors support firms to benefit from environmentally sustainable investments?

To address the question, the research takes a sample of investments and calculates the stock market reaction using the event study method. We then assess the configurations of factors that contribute to positive financial outcomes. This research is important because past studies have taken a regression approach to the study of factors influencing financial outcomes. While our approach is limited as our research finding is formed by taking a configurational approach, this study creates an important contribution by evaluating configurations and developing a new theory.

The rest of the article is structured as follows. We first review the literature relating to innovation management with a focus on incremental vs. radical innovations and the value of developments. We examine the importance of careful management of resources with a focus on financially focused measures that are relevant to risk management and the continued economic vitality of firms. Given the background, we then present the method that we use by explaining the event study method to generate the abnormal returns that are used as a measure of firm performance, before explaining the qualitative comparative analysis (QCA) approach to assess configurations of factors that are associated with positive outcomes. We then discuss the implications for managers and research before concluding.

2. Background and Literature Review

2.1. Innovation and Incremental vs. Radical Initiatives

There have been many discussions about the benefits of radical vs. incremental innovations. Incremental innovations take small progresses, tweaks or modifications, of well-understood products or processes [

13]. In contrast, radical innovations represent a departure from the understood product design or process design. Sustainable innovations are those in products, processes, or services that enhance economic outcomes while reducing environmental burdens or increasing social outcomes [

14]. In the construction industry, business process improvements for environmental outcomes may include new construction processes, enhanced materials, using recycled materials, or innovative designs to reduce energy use.

Radical innovations tend to involve risky and large investments [

15]. They may take time to provide financial payoff or be highly variable in outcomes. They hold the promise of future benefits that can be substantial. In the construction industry, Kajander et al. [

6] showed that announcements of radical innovation business process improvements for sustainable outcomes are associated with positive stock market reactions. In contrast, incremental investments can provide rapid returns on investments that are much smaller. However, they may provide fewer future opportunities and not increase reputational benefits. Duong et al. [

7] demonstrated (over a later time period than Kajander et al.) that investments in incremental innovations also provide positive stock market reactions. Shahin et al. [

16] provided an overview of a method for managers to select and prioritize determinants of eco-innovation for investments. As a consequence, there is a range of related managerial decisions that may influence outcomes from the selection of radical vs. incremental innovations, and there is evidence that either may lead to positive stock market reactions and that the configuration of other factors may also influence the level of stock market reaction.

2.2. Management of Working Capital, Working Capital Turnover, and Security

To take on risky investments, firms need to be careful with their financial investments. They need to ensure that they do not take on too many liabilities in contrast to their ability to service debt. In some cases, extensive or radical innovations may require ongoing investments that occur for longer than expected. As a consequence, additional debt may need to be taken on. Firms with more stable and greater financial security allow them to take on larger risks and maintain their business long enough to benefit from long-term financial benefits.

The current ratio represents the ratio of current or near-term assets to current or near-term liabilities. It represents a measure of whether the company could repay current obligations in the near term if there were business risks or issues. The cash conversion and use of cash for construction companies are critical to financial health. The measure for working capital is the same near-term assets to liabilities of the current ratio. Construction firms often find challenges in the quality of materials, poor management of supply chain factors, and unexpected supply chain costs. Holding more inventory as a buffer, for example, increases working capital requirements and requires higher current ratios [

17].

The working capital turnover measure simply takes the firm’s net annual sales and divides this by the working capital. The measure shows how effective the firm is at creating sales for each dollar of working capital. Higher turnover ratios tend to be better and indicate more ability to generate sales for the capital employed. Working capital turnover is positively associated with the financial health of companies [

18].

However, working capital management focuses on the use of current assets and liabilities to provide sufficient liquidity for ongoing operations [

19]. It is important for firms to have sufficient working capital, as this is associated with enhanced financial and operational performance [

19,

20].

2.3. Growth Prospects

In general, we would expect firms with greater growth prospects to benefit more from business process improvements than firms with lower growth prospects [

21]. Innovations and investments can often be absorbed, and the firm will often be more practiced and able to undertake improvements. Firms that are more known for innovations and growth are more likely to have further innovations rewarded and recognized by investors [

22]. Therefore, firms with better growth prospects are likely to be able to benefit more from investments in business processes and capitalize on the positive outcomes.

2.4. Performance and How to Enhance Performance

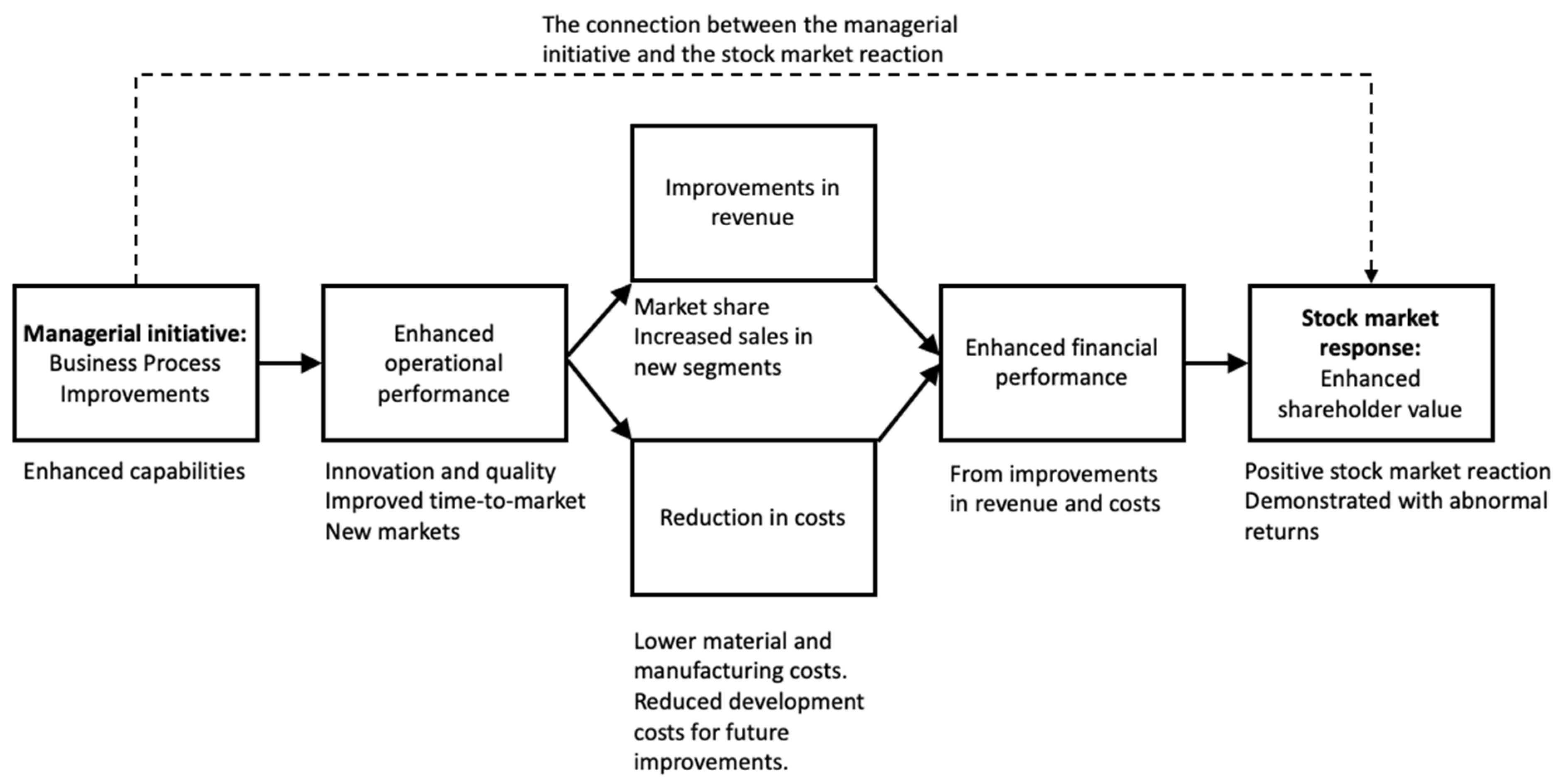

As a measure of performance, we use the abnormal returns (ARs) due to the business process improvement initiative. These ARs are the investors’ unbiased estimates of the overall benefits for the firm, expressed as a change in the current value of the firm shown in the stock market reaction at the time of the announcement.

Figure 1 shows the logic of how managerial initiatives, such as business process improvements for sustainable outcomes, lead to a stock market response that shows a change in shareholder value. The initiatives improve firms’ long-term revenue prospects and reduce costs, resulting in improved financial performance that is expected and then “priced in” to the current stock prices reflecting improved future conditions for the firm. This first phase of this study calculates the stock market reaction to the announcements of business process improvements for sustainable outcomes.

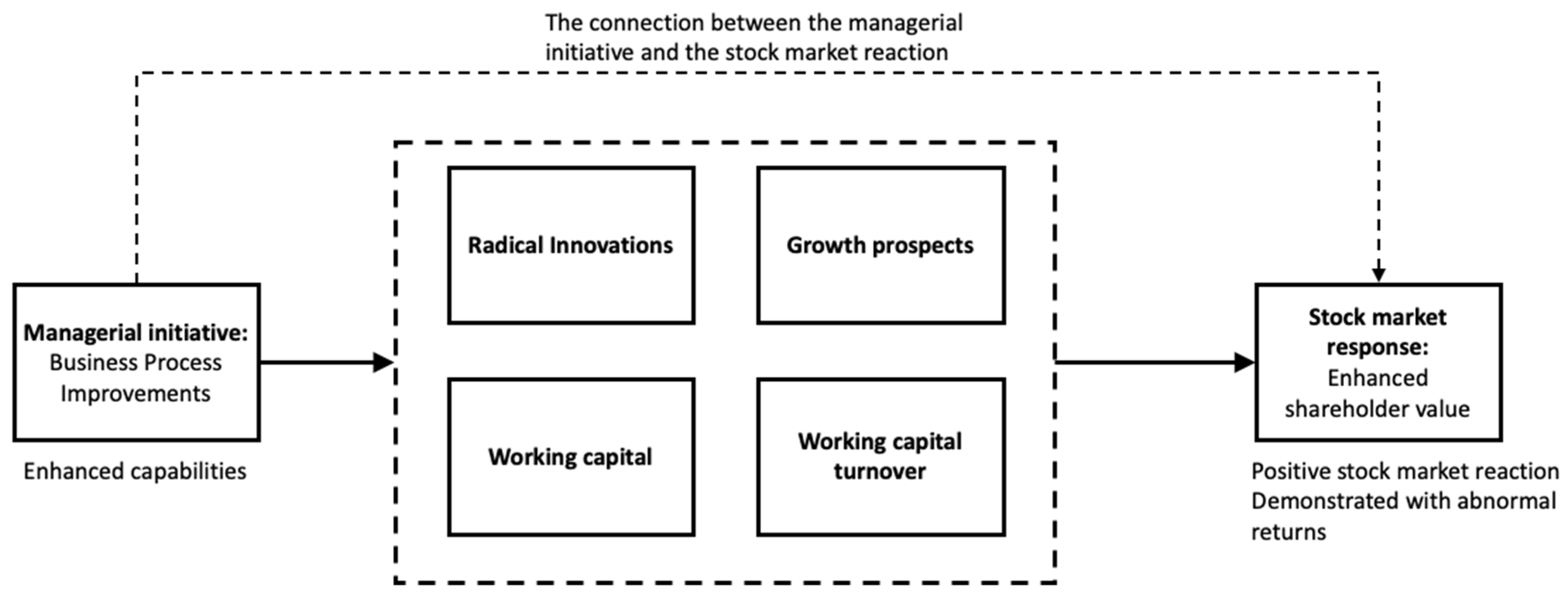

From the discussion of different factors that may influence outcomes, we expect firms with superior current ratios and working capital turnover rates and growth prospects as well as those investing in radical process improvements to enhance their returns from the business process improvements.

Figure 2 builds on the relationship but shows the four factors being studied and how these higher or improved performances are expected to lead to improved stock market responses. The second phase of this study examines the configurations that provide better stock market reactions.

3. Method

To address the research question, we developed a sample, calculated abnormal returns with a standard event study analysis, and then undertook a QCA analysis. Our two-phase approach with distinct analyses (ESA and QCA) provides a novel combination and insights to address the questions. The combination is methodologically novel and is justified, as the ESA generates a performance outcome (the abnormal returns or stock market reaction) that is then subsequently used in the analysis. While many other analyses follow the ESA with a cross-sectional analysis, our use of the QCA approach is justified, as it allows us to identify and evaluate combinations with equifinality in terms of generating the stock market reaction; that is, we are not tied to or connected to generating linear combinations as when using a cross-sectional regression following ESA. This reflects how a range of combinations may result in high or low performance; QCA can analyze the equifinality of combinations in a way that a cross-sectional regression cannot. As past studies, using regression, have often had conflicting results, it may be because of the different possible combinations that may drive performance. ESA followed by QCA allows us to investigate these combinations that lead to higher performance, or which avoid risks. Because of this, it is a superior choice to address the research question which focuses on the configuration and interplay of factors influencing the stock market reaction, rather than a method such as cross-sectional regression that would provide an analysis of how the value of each factor contributes to the stock market reaction.

3.1. Sample

We developed a sample by searching announcements on Factiva from 2011 to 2017. We used a combination of keywords to identify announcements of environmental sustainability initiatives. The combinations included synonyms for developments or innovations that occurred near synonyms for green, such as renewable and environmentally friendly. The research team screened them to manually confirm their relevance and that they were listed companies, leaving a sample of 143 announcements. We then evaluated the data availability for the cases and removed cases without complete data, giving a final sample of 116 cases used in the QCA analysis. The announcements were used to extract details about the nature of the process improvement project; the research team classified them as incremental vs. radical innovations.

3.2. Estimation of Abnormal Returns Using Event Study Analysis (ESA)

To complete the QCA analysis, a measure of performance is required. We evaluated performance by using a standard event study analysis (ESA) to calculate the abnormal return in response to the 116 announcements. The ESA approach relies on the efficient market hypothesis that the firm reacts to new information and incorporates it instantly into the stock prices, reflecting the likely risks and returns expected in the future based on the investors’ estimates of the impact on the firm, discounted to the present value and influencing the stock prices accordingly. This “stock market reaction” to the news can be positive (an abnormal return that is above zero, above, and beyond what we might otherwise expect to see), showing that investors have a bullish and favorable perception that the benefits from this news will outweigh the risks and drawbacks. Conversely, if the news suggests higher levels of risks to the firm relative to potential long-term benefits, the abnormal return will be negative. Risks could include uncertain investments required for an unclear length of time, the possibility of lack of market or customer acceptance, or risks in bringing the product to the market. Benefits might include favorable reputational benefits, new product launches, increased product sales, or entry into new markets or segments.

The approach has been widely used in management to study a range of topics [

23,

24,

25], as well as in management, finance, and construction management research to study innovation [

6,

7,

26].

3.3. Calculating the Abnormal Return

To isolate the event-specific stock returns, we estimated the abnormal returns using the market model, as this is commonly used in similar research and it allows a comparison of a multi-country sample, as we have used, as it relies on the market returns for markets (which are readily available using relevant stock indices) rather than factors identified by Fama, French [

27], and Carhart [

28], which are not available for all markets. We used the Event Study Metrics software and the lmrob R package [

29] for the analysis.

To isolate the stock market reaction to the announcements, we used the market model [

30,

31], as it is frequently used in comparable research [

32] and has good data availability.

We estimated the

ARit for firm

i on day

t as:

where

Rit is the stock returns of firm

i on day

t.

Rmt is the “normal return” calculated with reference to the market on day

t. The market model parameters of

and

were estimated with ordinary least squares (OLS) with a 120-day estimation window that terminated 10 days before the announcement, isolating the estimation of normal returns (in the estimation window) from the estimation of ARs [

6,

24]. Therefore, we estimated the mean abnormal return at day

as:

where

is the number of firms.

We used a short window of two days to capture the stock market reaction. The ARs in the window are cumulative ARs (CAR). The CAR (0,1) of the announcement day and the day after was calculated as:

Because of the international nature of the sample, the two-day window accommodates time-zone differences and announcements made in one region that are outside the trading hours in another region. Such two-day windows are practical [

24,

33].

3.4. Qualitative Comparative Analysis (QCA)

The abnormal returns were used as the performance measure in the QCA analysis approach. The approach provides the opportunity to evaluate a comprehensive perspective on antecedents and configurations of requirements for the business-process innovation investments and how these influence outcomes [

34]. In this phase, we consider the characteristics of the management and use of resources in the firm, the type of projects undertaken, and the overall net impact of these on the performance as measured by the abnormal return. The analysis approach implies that relationships may be asymmetric so that various combinations of the causal conditions and factors can influence the outcome conditions. Consequentially, we highlight the role of these factors using fuzzy QCA (fsQCA) to develop an analysis based on set conditions and consequences. The intermediate solutions are used to demonstrate alternative causal procedures that provide a high level of membership for the outcome conditions of interest. In this study, we examine the configuration of factors that lead to firm performance, as indicated by the presence of the CAR values as well as configurations that lead to the absence of performance. The QCA approach encompasses equifinality and there may be, therefore, a range of configurations unique to the presence or absence of performance.

For each of the cases, we developed a data frame using raw data from COMPUSTAT and the CARs calculated in the previous phase. From this, we then established fuzzy-set scores using the standard calibration method (see

Table 1) [

34]. The calibration rules were established based on the research team’s theoretical evaluation of the importance of the factors. The process enables the transformation of the continuous data (from COMPUSTAT) into set data with fuzzy set values [

35]. It uses three anchor points to define full non-membership, the cross-over point, and full membership. The cross-over point represents that point of maximum ambiguity of the set membership. Manual calibration based on the log-odds method was applied and assessed. Following the calibration, the fsQCA 2.5 software was used for the analysis. The outcome of interest was the performance as measured by the fuzzy set variable created from the cumulative abnormal return (fsCAR) for each case. The other variables were calibrated using the rules defined in

Table 1.

3.5. Analysis of Necessary Conditions

The first step is the analysis of necessary conditions to assess whether any of the variables are

necessary for the outcome if a condition is always present or absent in all cases [

35]. If the consistency score exceeds 0.9, this suggests a high alignment with the particular rule and the condition is regarded as necessary [

36]. The assessment of the fsCAR suggests that the absence of a radical innovation is necessary for a positive outcome (consistency > 0.9).

3.6. Analysis of Sufficient Conditions

There are three primary steps in the analysis of sufficient conditions relating to the truth table algorithm: the construction, preparation, and analysis of the table. We prepared an analysis for both the presence of firm performance as well as the absence.

First, the truth table was constructed. It consisted of the logically possible combination of causal conditions. Each case was evaluated based on the membership scores (

Table 1) and allocated to the appropriate configuration. Each row of the truth table, therefore, consists of a unique combination and the number of cases identified in the dataset. Overall, there is a range of combinations with many, some, few, or no empirically observed cases.

The truth table was then reduced to include only meaningful configurations, based on empirical instances. A frequency threshold of 1 was used so each configuration must have at least a single case with that set of memberships. Next, a minimum acceptable level of consistency was defined for the rows, we used 0.7 for the presence of firm performance and 0.8 for the absence of firm performance to obtain suitable configurational complexity. Finally, the algorithm reduced the logic statements to a set that best describes the underlying causal patterns [

34]. The solution table shows several configurations that can possibly lead to the existence of CAR. The solution coverage explains the number of outcomes covered by the configurations [

37].

There are two measures of “fit” for each configuration. The consistency value measures the extent the configuration matches or corresponds to the outcomes [

34]. The identified configurations exceed the standard cutoff value of 0.75 and are, therefore, considered sufficient for the outcome.

3.7. Variable Construction and Definitions

The measure of working capital is simply the total current assets divided by the current liabilities for the firm, using the most recent financial results. The measure of working capital turnover is the net annual sales divided by the working capital. The measure of incremental vs. radical innovations was evaluated as a binary (or crisp set) where the research team assessed the nature of the innovations. Growth prospects used the book-to-market ratio as a proxy for the growth potential of a firm, using the book value of the equity relative to the market value, as reported in the recent fiscal year. The greater the ratio, the lower the growth prospects.

4. Results

4.1. ESA Results

ESA literature recommends using short and multiple event windows in multiple statistics tests, showing the robustness of the results; the event window should not be longer than a three-day range, i.e., (−1, 1) [

33,

38]. We followed the literature and tested the stock market reaction in multiple event windows, as in

Table 2.

The CAR at the two-day event window of (0, 1) shows the highest statistical significance across multiple tests and event windows. Of note, 59% of the firms showed a positive CAR with the average (median) value being 0.58% (0.43%). Using this two-day event window of CAR allows us to avoid potential bias in the subsequent analysis. We therefore use the individual CAR at (0, 1) as our sample firms’ performance measure in our following QCA tests.

4.2. QCA Results

We first present the results for the evaluation of necessary conditions (

Table A1,

Appendix A). The next step in the analysis was the generation of the truth table (

Appendix A) using fsQCA software. Available online:

https://www.socsci.uci.edu/~cragin/fsQCA/software.shtml (accessed on 1 April 2022) The truth table algorithm uses two steps, and it works to identify possible causal conditions for the outcomes. The software allows the generation of complex, parsimonious, and intermediate solutions. Rihoux and Ragin [

37] suggest that the intermediate solution is interpreted as this provides a superior and most comprehensible and meaningful interpretation.

Table 3 and

Table 4 present the solutions. The intermediate solutions have good consistency with values of 0.79 (

Table 3) and 0.85 (

Table 4), greater than the 0.75 suggested as an acceptable level [

39], with coverage being quite low (0.07 in

Table 3 and 0.13 in

Table 4). This result reflects the conditions present and the difficulty in identifying suitable configurations relevant to stock market reactions. The low coverage may also be related to how a cross-sectional regression using stock market reactions calculated with ESA often produces lower R2 values than seen in other regression models [

39].

5. Discussion

The study has examined the configurations of factors that influence the stock market reaction to the business process improvements for sustainable outcomes in the construction industry. The focus was on the financial capabilities of the firms as well as the type of project and their overall growth prospects and how these influenced stock market reactions.

The study developed a configuration leading to the presence of firm performance, as measured by a positive stock market reaction (

Figure 3):

~cRadical*fsGrowth*~fsWC*fsWCT

The two configurations leading to the absence of positive stock market reactions (

Figure 4) are also important:

cRadical*~fsWC*fsWCT

cRadical*fsWC*~fsWCT

Interpreted together, these factors suggest that the decisions in investments in either radical or incremental innovations are important. While past studies have suggested that both radical [

6] and incremental [

7] projects result in positive stock market reactions, we found no evidence of a stock market reaction significantly different from zero for our study, although we note that the direction and magnitude are comparable to past studies.

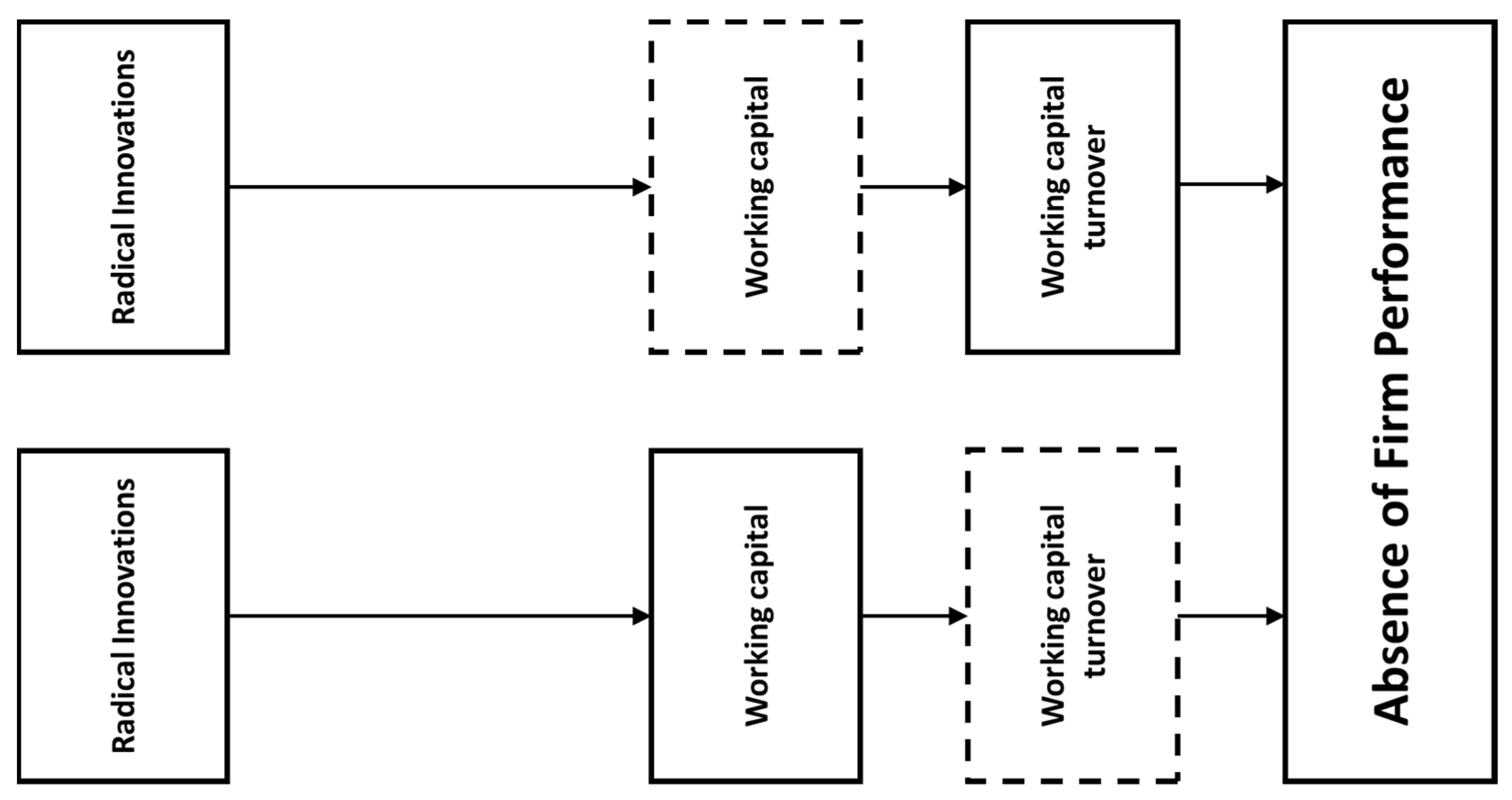

In contrast to past studies, the configurational approach here can provide a more nuanced picture of how construction firms can ensure that they reach a positive firm performance, as measured by the stock market reaction (CAR). One of the most crucial elements was our evaluation of the role of the more conservative approach of using incremental innovations as the business process improvement or a more radical innovation. The results suggest that selecting radical innovations for the construction firms is more likely to lead to negative firm performance;

Figure 4 shows how both these solutions include radical innovations and the absence of performance, while

Figure 3 shows that configurations including incremental solutions generate positive firm performance. This suggests that, similarly to how incremental projects result in positive CARs [

7], a conservative strategy would emphasize the adoption of incremental projects as a method to capture positive performance outcomes and avoid the absence of positive performance. These results reinforce and confirm previous studies that highlight the importance of professional management of construction firms and how effective working capital management is associated with positive health [

17,

18]. Our analysis of the absence of performance hinges partly on both working capital and the working capital turnover, indicating that evaluating one measure alone is insufficient to capture the dynamics of how these factors together interact to produce successful outcomes [

18].

The option of selecting more radical innovations in business process improvements can be associated with the absence of firm performance, representing a loss of shareholder value, coupled with conditions relating to the working capital where the firm either has low working capital and a high turnover (indicating the firm is leveraged and has a higher risk of financial risks) or high working capital and low turnover (indicating greater financial stability and less risk). This result underscores that the more radical the innovation, the higher the risks of undertaking the project and the potential for firms to experience reduced liquidity or risks of insolvency [

19]. Consequently, construction firms should assess their management capabilities and ability to manage working capital effectively prior to committing to radical innovations in business processes [

40].

In contrast, to develop a positive stock market reaction, we find that firms are more likely to develop a configuration of investing in more incremental innovations in business process improvements. In the same type of configuration, with low working capital and a high working capital turnover, the presence of low growth prospects (having a high book-to-market ratio; in our coding, the higher “growth prospect” variable set value is indicative of lower growth prospects) suggests that the construction company has extensive capability to manage the introduction of new processes and innovations and capitalize on the developments. The need for low growth prospects suggests that the greater risks of radical innovations would be compounded, and the firm is more suited to select the incremental innovations in this configuration for the positive outcomes [

41]. From the perspective of firm performance as evaluated by the stock market reaction, these outcomes likely suggest that investors place a high value on the safety and lack of risk from this type of approach, rather than expectations of greater future financial benefits. This outcome contrasts with the common perception of growth prospects [

21]. One interpretation is that the positive performance is connected to the pursuit of incremental innovations by firms with lower growth prospects, suggesting that investors are not rewarding radical innovations, as is often seen [

22], but instead are focused on the minimization of risks and the slow-and-steady benefits that incremental innovations may bring.

The results and specific configurations suggest that investors carefully assess the capabilities of firms [

42]. The risks and the demonstrated management of working capital and the overall growth prospects provide important and meaningful input into the decisions of investors, as they evaluate the likelihood of future benefits and drawbacks from the incremental or radical innovations pursued by construction firms.

Managerial Implications

One of the most important outcomes of this research for managers is the ability to assess their company characteristics (e.g., growth prospects, current ratio) and possible projects with the end stock market reaction in mind. While the stock market reactions are an estimate of outcomes, they can still guide effective management practices. For instance, many construction firms should carefully evaluate radical innovations and may be better off to take incremental innovation projects only, as these tend to have more favorable stock market reactions, and the managers should evaluate projects based on risks due to the company characteristics, management of working capital, and their overall growth prospects.

In contrast, there is a small subset of construction firms, with professional and effective management, that could take on projects with more radical innovations in business processes. While radical innovations might be associated with the absence of performance (

Figure 4), this only occurs in configurations relating to poor management of working capital. Given these circumstances, the firm is more likely to be in a position at the end where they will be able to benefit from the returns from their radical process innovations.

6. Conclusions

This study sought to understand what types of construction industry firms would benefit from process innovations to gain environmental sustainability. To reach this objective, we used a sample of news announcements and then a standard ESA analysis to calculate the abnormal return or stock market reaction to the initiative. In general, despite the positive outcomes from the ESA (i.e., the generally positive abnormal returns), we applied the QCA approach to evaluate possible configurations of characteristics that are more likely to generate positive outcomes. We showed that there is a specific configuration, focusing on incremental innovations, that consistently produces positive firm performance, while two configurations that lead to the absence of performance are associated with radical innovations in firms that struggle to manage their working capital. The novel approach of using the stock market reaction from ESA as a basis for performance in the QCA shows the strengths and benefits of combining these methods, as it allows the evaluation of causal combinations and interplay of factors influencing performance that cannot be identified using cross-sectional analysis.

The research contributes to the sustainability literature by showing the presence of risks and returns, from a financial perspective, and how investors are cautious and risk-averse about the likelihood of positive returns. The analysis can show multiple combinations of factors relating to a weak or strong performance that cannot be identified using a cross-sectional regression, highlighting the value of this novel methodological approach.

This study has several limitations based on the research design decisions employed. First, we studied only firms making business process improvement announcements with a sustainable outcome focus. Therefore, generalizing to other business process improvement announcements in the construction industry, or sustainability-focused announcements outside of the construction industry, should be undertaken with care. Additional research will be required to assess whether these configurations or comparable configurations are valid for other contexts, particularly given the difference in the performance of construction firms relative to those in other industries. The QCA approach is also limited relative to the cross-sectional analysis approach, as we cannot explain how the performance may change in response to the change in one of the input variables; we can only comment on the combinations of factors relating to higher performance but not connect the sensitivity of the performance level to the change in the input variable. Future research may explore the combinations identified here with qualitative or regression-based approaches to provide additional analytical insight into the strength and sensitivity of the relationships.

This study has several limitations. Our measure of firm performance relies on the evaluation of the stock market reaction. There could be other measures of performance used. We also include a limited sample of cases that, while global, is also limited only to the construction industry and features configurations that are relevant to the management of construction firms, such as the emphasis on working capital. Future research should expand this approach to evaluate the importance of business process innovations in other sectors with configurations of factors that may be more relevant to the sectors; for instance, an evaluation in a high-tech sector may include the level of research and development as a factor in the analysis.

Author Contributions

Conceptualization, L.C.W.; methodology, L.C.W., L.N.K.D. and J.X.W.; validation, L.C.W., L.N.K.D. and J.X.W.; formal analysis, L.C.W.; investigation, L.C.W. and L.N.K.D.; resources, L.N.K.D.; data curation, L.C.W., L.N.K.D. and J.X.W.; writing—original draft preparation, L.C.W.; writing—review and editing, L.C.W., L.N.K.D. and J.X.W.; visualization, L.C.W.; project administration, L.C.W. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study did not require ethical approval as it used secondary data from established databases.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data may be obtained from the corresponding author. The data cannot be made publicly available due to database use agreements.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Analysis of the necessary conditions.

Table A1.

Analysis of the necessary conditions.

Outcome Variable: fsCAR

(Presence of Firm Performance) | Outcome Variable: ~fsCAR

(Absence of Firm Performance) |

|---|

| Conditions Tested: | Conditions Tested: |

|---|

| | Consistency | Coverage | | Consistency | Coverage |

|---|

| cRadical | 0.084122 | 0.240588 | cRadical | 0.191600 | 0.759412 |

| ~cRadical | 0.915878 | 0.449798 | ~cRadical | 0.808400 | 0.550202 |

| fsGrowth | 0.357429 | 0.500412 | fsGrowth | 0.340211 | 0.660089 |

| ~fsGrowth | 0.757212 | 0.452992 | ~fsGrowth | 0.742512 | 0.615591 |

| fsWC | 0.56694 | 0.470068 | fsWC | 0.547366 | 0.628951 |

| ~fsWC | 0.552485 | 0.468299 | ~fsWC | 0.538809 | 0.632928 |

| fsWCT | 0.326141 | 0.404992 | fsWCT | 0.392373 | 0.675238 |

| ~fsWCT | 0.738469 | 0.467223 | ~fsWCT | 0.654248 | 0.573655 |

References

- Killip, G.; Owen, A.; Morgan, E.; Topouzi, M. A co-evolutionary approach to understanding construction industry innovation in renovation practices for low-carbon outcomes. Int. J. Entrep. Innov. 2018, 19, 9–20. [Google Scholar] [CrossRef]

- Xue, X.; Zhang, R.; Yang, R.; Dai, J. Innovation in Construction: A Critical Review and Future Research. Int. J. Innov. Sci. 2014, 6, 111–126. [Google Scholar] [CrossRef]

- Meng, X.; Brown, A. Innovation in construction firms of different sizes: Drivers and strategies. Eng. Constr. Arch. Manag. 2018, 25, 1210–1225. [Google Scholar] [CrossRef] [Green Version]

- Brockmann, C.; Brezinski, H.; Erbe, A. Innovation in Construction Megaprojects. J. Constr. Eng. Manag. 2016, 142, 04016059. [Google Scholar] [CrossRef] [Green Version]

- Escrig-Tena, A.B.; Segarra-Ciprés, M.; García-Juan, B. Incremental and radical product innovation capabilities in a quality management context: Exploring the moderating effects of control mechanisms. Int. J. Prod. Econ. 2020, 232, 107994. [Google Scholar] [CrossRef]

- Kajander, J.-K.; Sivunen, M.; Vimpari, J.; Pulkka, L.; Junnila, S. Market value of sustainability business innovations in the construction sector. Build. Res. Inf. 2012, 40, 665–678. [Google Scholar] [CrossRef]

- Duong, L.N.K.; Wang, J.X.; Wood, L.C.; Reiners, T.; Koushan, M. The value of incremental environmental sustainability innovation in the construction industry: An event study. Constr. Manag. Econ. 2021, 39, 398–418. [Google Scholar] [CrossRef]

- Lu, J.-R.; Hwang, C.-C.; Lin, C.-Y. Do shareholders appreciate capital investment policies of corporations? Int. Rev. Econ. Financ. 2016, 43, 344–353. [Google Scholar] [CrossRef]

- Calabrò, A.; Vecchiarini, M.; Gast, J.; Campopiano, G.; De Massis, A.; Kraus, S. Innovation in Family Firms: A Systematic Literature Review and Guidance for Future Research. Int. J. Manag. Rev. 2018, 21, 317–355. [Google Scholar] [CrossRef]

- Foucart, R.; Li, Q.C. The role of technology standards in product innovation: Theory and evidence from UK manufacturing firms. Res. Policy 2020, 50, 104157. [Google Scholar] [CrossRef]

- Pang, C.; Wang, Y. Stock pledge, risk of losing control and corporate innovation. J. Corp. Financ. 2019, 60, 101534. [Google Scholar] [CrossRef]

- Davis, P.; Gajendran, T.; Vaughan, J.; Owi, T. Assessing construction innovation: Theoretical and practical perspectives. Constr. Econ. Build. 2016, 16, 104–115. [Google Scholar] [CrossRef] [Green Version]

- Sivunen, M.; Pulkka, L.; Heinonen, J.; Kajander, J.; Junnila, S. Service-dominant innovation in the built environment. Constr. Innov. 2013, 13, 146–164. [Google Scholar] [CrossRef]

- Kusi-Sarpong, S.; Gupta, H.; Sarkis, J. A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 2018, 57, 1990–2008. [Google Scholar] [CrossRef] [Green Version]

- Bers, J.A.; Dismukes, J.P.; Miller, L.K.; Dubrovensky, A. Accelerated radical innovation: Theory and application. Technol. Forecast. Soc. Chang. 2009, 76, 165–177. [Google Scholar] [CrossRef]

- Shahin, A.; Imanipour, N.; Shahin, A.; Wood, L.C. An integrative approach for structuring and prioritising eco-innovation determinants with a survey in knowledge-based companies. J. Manuf. Technol. Manag. 2020, 31, 799–824. [Google Scholar] [CrossRef]

- Behera, P.; Mohanty, R.; Prakash, A. Understanding Construction Supply Chain Management. Prod. Plan. Control 2015, 26, 1332–1350. [Google Scholar] [CrossRef]

- Yousaf, M.; Bris, P. Assessment of bankruptcy risks in Czech companies using regression analysis. Probl. Perspect. Manag. 2021, 19, 46–55. [Google Scholar] [CrossRef]

- Chamberlain, T.W.; Aucouturier, J. Working Capital Management and Firm Performance: Some Evidence from Europe. Int. Adv. Econ. Res. 2022, 27, 321–323. [Google Scholar] [CrossRef]

- Nguema, J.-N.B.B.; Bi, G.; Akenroye, T.O.; El Baz, J. The effects of supply chain finance on organizational performance: A moderated and mediated model. Supply Chain Manag. Int. J. 2021, 27, 113–127. [Google Scholar] [CrossRef]

- Gregory, A.; Tharyan, R.; Whittaker, J. Corporate Social Responsibility and Firm Value: Disaggregating the Effects on Cash Flow, Risk and Growth. J. Bus. Ethics 2013, 124, 633–657. [Google Scholar] [CrossRef] [Green Version]

- Coad, A.; Segarra, A.; Teruel, M. Innovation and firm growth: Does firm age play a role? Res. Policy 2016, 45, 387–400. [Google Scholar] [CrossRef] [Green Version]

- Jacobs, B.W.; Singhal, V.R. The effect of the Rana Plaza disaster on shareholder wealth of retailers: Implications for sourcing strategies and supply chain governance. J. Oper. Manag. 2017, 49–51, 52–66. [Google Scholar] [CrossRef]

- Wood, L.C.; Wang, J.X.; Olesen, K.; Reiners, T. The effect of slack, diversification, and time to recall on stock market reaction to toy recalls. Int. J. Prod. Econ. 2017, 193, 244–258. [Google Scholar] [CrossRef]

- Wood, L.C.; Wang, J.X.; Duong, L.N.K.; Reiners, T.; Smith, R. Stock Market Reactions to Auto Manufacturers’ Environmental Failures. J. Macromark. 2018, 38, 364–382. [Google Scholar] [CrossRef]

- Yang, M.; He, Y. How does the stock market react to financial innovation regulations? Financ. Res. Lett. 2018, 30, 259–265. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Common risk factors in the returns on stocks and bonds. J. Financ. Econ. 1993, 33, 3–56. [Google Scholar] [CrossRef]

- Carhart, M.M. On Persistence in Mutual Fund Performance. J. Financ. 1997, 52, 57–82. [Google Scholar] [CrossRef]

- Salibian-Barrera, M.; Koller, M. Lmrob. 2020. Available online: https://cran.r-project.org/web/packages/robustbase/robustbase.pdf (accessed on 3 July 2020).

- Brown, S.J.; Warner, J.B. Using daily stock returns: The case of event studies. J. Financ. Econ. 1985, 14, 3–31. [Google Scholar] [CrossRef]

- MacKinlay, A.C. Event studies in economics and finance. J. Econ. Lit. 1997, 35, 13–39. [Google Scholar]

- Wood, L.C.; Wang, J.X. The Event Study Method in Logistics Research. Int. J. Appl. Logist. 2018, 8, 57–79. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Event studies in management research: Theoretical and empirical issues. Acad. Manag. J. 1997, 40, 626–657. [Google Scholar] [CrossRef]

- Ragin, C.C. The Comparative Method: Moving Beyond Qualitative and Quantitative Strategies; University of California Press: Oakland, CA, USA, 2014; Available online: https://www.degruyter.com/document/doi/10.1525/9780520957350/html (accessed on 29 March 2022).

- Ragin, C.C. Redesigning Social Inquiry: Fuzzy Sets and Beyond; University of California Press: Oakland, CA, USA, 2008; Available online: http://ebookcentral.proquest.com/lib/curtin/detail.action?docID=432281 (accessed on 8 March 2022).

- Schneider, C.Q. Set-Theoretic Methods for The Social Sciences: A Guide to Qualitative Comparative Analysis; Cambridge University Press: Oakland, CA, USA, 2012. [Google Scholar]

- Rihoux, B.; Ragin, C. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques; Sage: Thousand Oaks, CA, USA, 2009. [Google Scholar] [CrossRef]

- Kothari, S.; Warner, J.B. Chapter 1—Econometrics of Event Studies. In Handbook of Empirical Corporate Finance; Eckbo, B.E., Ed.; Elsevier: San Diego, CA, USA, 2007; pp. 3–36. [Google Scholar] [CrossRef]

- Tran, P.N.T.; Gorton, M.; Lemke, F. When supplier development initiatives fail: Identifying the causes of opportunism and unexpected outcomes. J. Bus. Res. 2021, 127, 277–289. [Google Scholar] [CrossRef]

- Tripathi, K.K.; Jha, K.N. Determining Success Factors for a Construction Organization: A Structural Equation Modeling Approach. J. Manag. Eng. 2018, 34, 04017050. [Google Scholar] [CrossRef]

- Clifton, N.; Huggins, R.; Pickernell, D.; Prokop, D.; Smith, D.; Thompson, P. Networking and strategic planning to enhance small and medium-sized enterprises growth in a less competitive economy. Strat. Chang. 2020, 29, 699–711. [Google Scholar] [CrossRef]

- Blankespoor, E. Firm communication and investor response: A framework and discussion integrating social media. Account. Organ. Soc. 2018, 68–69, 80–87. [Google Scholar] [CrossRef]

| Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}