CSR and Long-Term Corporate Performance: The Moderating Effects of Government Subsidies and Peer Firm’s CSR

Abstract

:1. Introduction

2. Literature Review and Hypotheses Development

2.1. Corporate Social Responsibility

2.2. Institutional Theory

2.3. CSR and Firm Performance

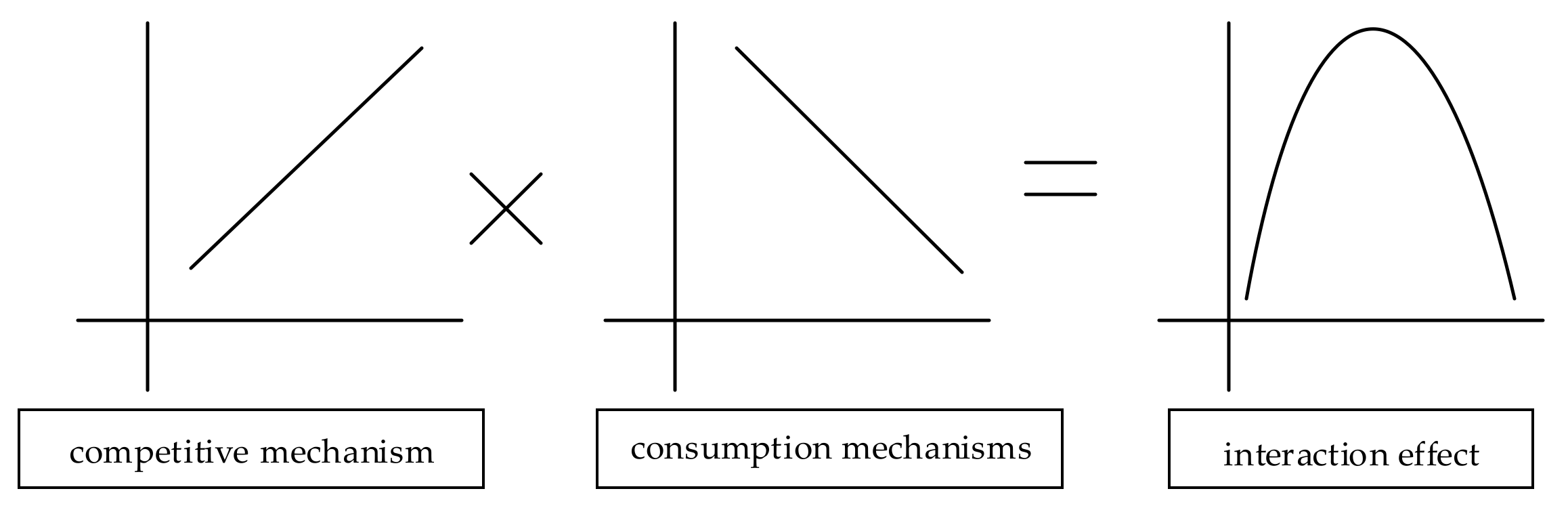

- (1)

- CSR affects the competitive mechanism of enterprises to improve performance.

- (2)

- CSR will consume a lot and have a negative impact on the improvement of enterprise performance.

2.4. The Moderating Role of Peer Firms’ CSR

2.5. The Moderating Role of Government Subsidies

- (1)

- Government subsidies will impact the competition mechanism of firms, thus, affecting firm performance.

- (2)

- Government subsidies affect the consumption mechanism of firms, which impacts firm performance.

3. Methods

3.1. Independent Variables

3.2. Dependent Variables

3.3. Moderators

3.4. Control Variable

4. Analyses

4.1. Analysis and Results

4.2. Robustness Checks

5. Conclusions and Discussion

5.1. Theoretical Implications

5.2. Practical Implications

5.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Park, K.O. How CSV and CSR Affect Organizational Performance: A Productive Behavior Perspective. Int. J. Environ. Res. Public Health 2020, 17, 2556. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Zheng, Q.; Luo, Y.; Maksimov, V. Achieving legitimacy through corporate social responsibility: The case of emerging economy firms. J. World Bus. 2015, 50, 389–403. [Google Scholar] [CrossRef]

- Romero-Castro, N.; López-Cabarcos, M.Á.; Piñeiro-Chousa, J. Uncovering complexity in the economic assessment of derogations from the European industrial emissions directive. J. Innov. Knowl. 2022, 7, 100159. [Google Scholar] [CrossRef]

- Godfrey, P.C. The Relationship between Corporate Philanthropy and Shareholder Wealth: A Risk Management Perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef] [Green Version]

- Tashman, P.; Marano, V.; Kostova, T. Walking the walk or talking the talk? Corporate social responsibility decoupling in emerging market multinationals. J. Int. Bus. Stud. 2019, 50, 153–171. [Google Scholar] [CrossRef]

- Wood, D.J. Measuring Corporate Social Performance: A Review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Park, B.I.; Chidlow, A.; Choi, J. Corporate social responsibility: Stakeholders influence on MNEs’ activities. Int. Bus. Rev. 2014, 23, 966–980. [Google Scholar] [CrossRef]

- Park, B.I.; Ghauri, P.N. Determinants influencing CSR practices in small and medium sized MNE subsidiaries: A stakeholder perspective. J. World Bus. 2015, 50, 192–204. [Google Scholar] [CrossRef]

- Lioui, A.; Sharma, Z. Environmental corporate social responsibility and financial performance: Disentangling direct and indirect effects. Ecol. Econ. 2012, 78, 100–111. [Google Scholar] [CrossRef]

- Pineiro-Chousa, J.; Romero-Castro, N.; Vizcaíno-González, M. Inclusions in and Exclusions from the S&P 500 Environmental and Socially Responsible Index: A Fuzzy-Set Qualitative Comparative Analysis. Sustainability 2019, 11, 1211. [Google Scholar]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How Corporate Social Responsibility Engagement Strategy Moderates the CSR-Financial Performance Relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business is to Increase Its Profits; Corporate ethics and corporate governance; Springer: Berlin/Heidelberg, Germany, 2007; pp. 173–178. [Google Scholar]

- Teoh, S.H.; Welch, I.; Wazzan, C.P. The Effect of Socially Activist Investment Policies on the Financial Markets: Evidence from the South African Boycott. J. Bus. 1999, 72, 35–89. [Google Scholar] [CrossRef] [Green Version]

- Bondy, K.; Starkey, K. The Dilemmas of Internationalization: Corporate Social Responsibility in the Multinational Corporation. Brit. J. Manag. 2014, 25, 4–22. [Google Scholar] [CrossRef] [Green Version]

- Marquina, P.; Morales, C.E. The influence of CSR on purchasing behaviour in Peru and Spain. Int. Market. Rev. 2012, 29, 299–312. [Google Scholar] [CrossRef]

- Polonsky, M.; Jevons, C. Global branding and strategic CSR: An overview of three types of complexity. Int. Market. Rev. 2009, 26, 327–347. [Google Scholar] [CrossRef]

- Zhang, J.; Marquis, C.; Qiao, K. Do political connections buffer firms from or bind firms to the government? A study of corporate charitable donations of Chinese firms. Organ. Sci. 2016, 27, 1307–1324. [Google Scholar] [CrossRef]

- Fabrizi, M.; Mallin, C.; Michelon, G. The Role of CEO’s Personal Incentives in Driving Corporate Social Responsibility. J. Bus. Ethics 2014, 124, 311–326. [Google Scholar] [CrossRef] [Green Version]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Kostova, T.; Beugelsdijk, S.; Scott, W.R.; Kunst, V.E.; Chua, C.H.; van Essen, M. The construct of institutional distance through the lens of different institutional perspectives: Review, analysis, and recommendations. J. Int. Bus. Stud. 2020, 51, 467–497. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Jung, S.; Kim, J.H.; Kang, K.H.; Kim, B. Internationalization and corporate social responsibility in the restaurant industry: Risk perspective. J. Sustain. Tour. 2018, 26, 1105–1123. [Google Scholar] [CrossRef]

- Campbell, J.T.; Eden, L.; Miller, S.R. Multinationals and corporate social responsibility in host countries: Does distance matter? J. Int. Bus. Stud. 2012, 43, 84–106. [Google Scholar] [CrossRef]

- Yin, J.; Zhang, Y. Institutional Dynamics and Corporate Social Responsibility (CSR) in an Emerging Country Context: Evidence from China. J. Bus. Ethics 2012, 111, 301–316. [Google Scholar] [CrossRef]

- Khattak, A.; Yousaf, Z. Digital Social Responsibility towards Corporate Social Responsibility and Strategic Performance of Hi-Tech SMEs: Customer Engagement as a Mediator. Sustainability 2022, 14, 131. [Google Scholar] [CrossRef]

- Fiaschi, D.; Giuliani, E.; Nieri, F. Overcoming the liability of origin by doing no-harm: Emerging country firms’ social irresponsibility as they go global. J. World Bus. 2017, 52, 546–563. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Kramer Strategy and Society: The Link between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2007, 85, 139. [Google Scholar]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate Social Responsibility and Firm Risk: Theory and Empirical Evidence. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef] [Green Version]

- Egri, C.P.; Ralston, D.A. Corporate responsibility: A review of international management research from 1998 to 2007. J. Int. Manag. 2008, 14, 319–339. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized organizations: Formal structure as myth and ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef] [Green Version]

- Goffi, G.; Masiero, L.; Pencarelli, T. Corporate social responsibility and performances of firms operating in the tourism and hospitality industry. TQM J. 2021. [Google Scholar] [CrossRef]

- Campbell, J.L. Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Social Responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Crilly, D.; Ni, N.; Jiang, Y. Do-no-harm versus do-good social responsibility: Attributional thinking and the liability of foreignness. Strateg. Manag. J. 2016, 37, 1316–1329. [Google Scholar] [CrossRef]

- Dahms, S.; Kingkaew, S.; Ng, E.S. The Effects of Top Management Team National Diversity and Institutional Uncertainty on Subsidiary CSR Focus. J. Bus. Ethics 2021, 1–17. [Google Scholar] [CrossRef]

- Okafor, A.; Adeleye, B.N.; Adusei, M. Corporate social responsibility and financial performance: Evidence from U.S tech firms. J. Clean. Prod. 2021, 292, 126078. [Google Scholar] [CrossRef]

- Hadjikhani, A.; Lee, J.W.; Park, S. Corporate social responsibility as a marketing strategy in foreign markets: The case of Korean MNCs in the Chinese electronics market. Int. Mark. Rev. 2016, 33, 530–554. [Google Scholar] [CrossRef]

- Strike, V.M.; Gao, J.; Bansal, P. Being Good While Being Bad: Social Responsibility and the International Diversification of US Firms. J. Int. Bus. Stud. 2006, 37, 850–862. [Google Scholar] [CrossRef]

- Wang, S.L.; Li, D. Responding to public disclosure of corporate social irresponsibility in host countries: Information control and ownership control. J. Int. Bus. Stud. 2019, 50, 1283–1309. [Google Scholar] [CrossRef]

- Mohr, L.A.; Webb, D.J.; Harris, K.E. Do Consumers Expect Companies to be Socially Responsible? The Impact of Corporate Social Responsibility on Buying Behavior. J. Consum. Aff. 2001, 35, 45–72. [Google Scholar] [CrossRef]

- Lichtenstein, D.R.; Drumwright, M.E.; Braig, B.M. The Effect of Corporate Social Responsibility on Customer Donations to Corporate-Supported Nonprofits. J. Mark. 2004, 68, 16–32. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C.B. The Debate over Doing Good: Corporate Social Performance, Strategic Marketing Levers, and Firm-Idiosyncratic Risk. J. Mark. 2009, 73, 198–213. [Google Scholar] [CrossRef] [Green Version]

- Edman, J. Reconciling the advantages and liabilities of foreignness: Towards an identity-based framework. J. Int. Bus. Stud. 2016, 47, 674–694. [Google Scholar] [CrossRef]

- Scott, W.R. Approaching adulthood: The maturing of institutional theory. Theor. Soc. 2008, 37, 427–442. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Corporate Social Responsibility in the Multinational Enterprise: Strategic and Institutional Approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef]

- Orlitzky, M.; Benjamin, J.D. Corporate Social Performance and Firm Risk: A Meta-Analytic Review. Bus. Soc. 2001, 40, 369–396. [Google Scholar] [CrossRef]

- Banerjee, A.V. A Simple Model of Herd Behavior. Q. J. Econ. 1992, 107, 797–817. [Google Scholar] [CrossRef] [Green Version]

- Westphal, J.D.; Khanna, P. Keeping directors in line: Social distancing as a control mechanism in the corporate elite. Admin. Sci. Q. 2003, 48, 361–398. [Google Scholar] [CrossRef] [Green Version]

- Powell, W.W. Inter-organizational collaboration in the biotechnology industry. J. Inst. Theor. Econ. (JITE)/Z. Gesamte Staatswiss. 1996, 152, 197–215. [Google Scholar]

- Cui, P.; Wang, W.; Cai, S.; Zhou, T.; Lai, Y. Close and ordinary social contacts: How important are they in promoting large-scale contagion? Phys. Rev. E 2018, 98, 052311. [Google Scholar] [CrossRef] [Green Version]

- Chen, S.; Chen, Y.; Jebran, K. Trust and corporate social responsibility: From expected utility and social normative perspective. J. Bus. Res. 2021, 134, 518–530. [Google Scholar] [CrossRef]

- Tseng, M.; Chiu, A.S.F.; Tan, R.R.; Siriban-Manalang, A.B. Sustainable consumption and production for Asia: Sustainability through green design and practice. J. Clean. Prod. 2013, 40, 1–5. [Google Scholar] [CrossRef]

- Shamsuddoha, A.K.; Yunus Ali, M.; Oly Ndubisi, N. Impact of government export assistance on internationalization of SMEs from developing nations. J. Enterp. Inf. Manag. 2009, 22, 408–422. [Google Scholar] [CrossRef]

- Falahat, M.; Lee, Y.Y.; Ramayah, T.; Soto-Acosta, P. Modelling the effects of institutional support and international knowledge on competitive capabilities and international performance: Evidence from an emerging economy. J. Int. Manag. 2020, 26, 100779. [Google Scholar] [CrossRef]

- Ying, M.; Tikuye, G.A.; Shan, H. Impacts of Firm Performance on Corporate Social Responsibility Practices: The Mediation Role of Corporate Governance in Ethiopia Corporate Business. Sustainability 2021, 13, 9717. [Google Scholar] [CrossRef]

- Blanes, J.V.; Busom, I. Who participates in R&D subsidy programs? Res. Policy 2004, 33, 1459–1476. [Google Scholar]

- Jourdan, J.; Kivleniece, I. Too Much of a Good Thing? The Dual Effect of Public Sponsorship on Organizational Performance. Acad. Manag. J. 2017, 60, 55–77. [Google Scholar] [CrossRef]

- Takalo, T.; Tanayama, T. Adverse selection and financing of innovation: Is there a need for R&D subsidies? J. Technol. Transf. 2010, 35, 16–41. [Google Scholar]

- Tether, B.S. Who co-operates for innovation, and why: An empirical analysis. Res. Policy 2002, 31, 947–967. [Google Scholar] [CrossRef]

- Tang, P.; Yang, S.; Boehe, D. Ownership and corporate social performance in China: Why geographic remoteness matters. J. Clean. Prod. 2018, 197, 1284–1295. [Google Scholar] [CrossRef]

- Morgan, H.M.; Sui, S.; Malhotra, S. No place like home: The effect of exporting to the country of origin on the financial performance of immigrant-owned SMEs. J. Int. Bus. Stud. 2021, 52, 504–524. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef] [Green Version]

- Haans, R.F.J.; Pieters, C.; He, Z. Thinking about U: Theorizing and testing U- and inverted U-shaped relationships in strategy research. Strateg. Manag. J. 2016, 37, 1177–1195. [Google Scholar] [CrossRef]

- Hu, Q.; Zhu, T.; Lin, C.; Chen, T.; Chin, T. Corporate Social Responsibility and Firm Performance in China’s Manufacturing: A Global Perspective of Business Models. Sustainability 2021, 13, 2388. [Google Scholar] [CrossRef]

- Price, J.M.; Sun, W. Doing good and doing bad: The impact of corporate social responsibility and irresponsibility on firm performance. J. Bus. Res. 2017, 80, 82–97. [Google Scholar] [CrossRef]

- Yang, S.; Ye, H.; Zhu, Q. Do Peer Firms Affect Firm Corporate Social Responsibility? Sustainability 2017, 9, 1967. [Google Scholar] [CrossRef] [Green Version]

- Christakis, N.A.; Fowler, J.H. Social contagion theory: Examining dynamic social networks and human behavior. Stat. Med. 2013, 32, 556–577. [Google Scholar] [CrossRef] [Green Version]

- Li, Y. Research on supply chain CSR management based on differential game. J. Clean. Prod. 2020, 268, 122171. [Google Scholar] [CrossRef]

- Attig, N.; Boubakri, N.; El Ghoul, S.; Guedhami, O. Firm Internationalization and Corporate Social Responsibility. J. Bus. Ethics 2016, 134, 171–197. [Google Scholar] [CrossRef]

- Husted, B.W.; Jamali, D.; Saffar, W. Near and dear? The role of location in CSR engagement. Strateg. Manag. J. 2016, 37, 2050–2070. [Google Scholar] [CrossRef]

- Cuervo-Cazurra, A.; Inkpen, A.; Musacchio, A.; Ramaswamy, K. Governments as owners: State-owned multinational companies. J. Int. Bus. Stud. 2014, 45, 919–942. [Google Scholar] [CrossRef] [Green Version]

- Bryant, S.E. The Role of Transformational and Transactional Leadership in Creating, Sharing and Exploiting Organizational Knowledge. J. Leadersh. Organ. Stud. 2003, 9, 32–44. [Google Scholar] [CrossRef]

- Chen, J.; Heng, C.S.; Tan, B.C.Y.; Lin, Z. The distinct signaling effects of R&D subsidy and non-R&D subsidy on IPO performance of IT entrepreneurial firms in China. Res. Policy 2018, 47, 108–120. [Google Scholar]

- Song, L.; Yan, Y.; Yao, F. Closed-Loop Supply Chain Models Considering Government Subsidy and Corporate Social Responsibility Investment. Sustainability 2020, 12, 2045. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Indicators | Variable Code | Definitions |

|---|---|---|

| Independent variable | ||

| Enterprise performance | roe | Ratio of net income to net assets |

| Dependent variable | ||

| CSR | CSR | The actual score of each company in Hexun |

| Moderator variables | ||

| Peer firms’ CSR | Psrl | Average social responsibility score of all companies in the industry in which the focal company is located in a given year, excluding the focal company |

| Government Subsidy | sub | The total amount of government subsidies actually obtained by enterprises |

| Control variables | ||

| Firm Age | age | the number of years since the company was founded |

| Firm Size | lnsize | Natural logarithm of total corporate assets |

| Firm Nature | state | The value is 1 when the enterprise is a state-owned enterprise, otherwise it is 0 |

| Ownership Concentration | shrcr | Percentage of shares owned by the top 10 shareholders |

| Variable | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. roe | 6.977 | 9.695 | 1 | ||||||||

| 2. state | 0.397 | 0.489 | −0.067 *** | 1 | |||||||

| 3. lnsize | 22.08 | 1.288 | 0.077 *** | 0.391 *** | 1 | ||||||

| 4. lnage | 1.946 | 0.943 | −0.108 *** | 0.470 *** | 0.436 *** | 1 | |||||

| 5. Shrcr | 59.67 | 15.33 | 0.199 *** | −0.100 *** | 0.088 *** | −0.442 *** | 1 | ||||

| 6. slack | 2.903 | 4.946 | 0.038 *** | −0.190 *** | −0.264 *** | −0.292 *** | 0.122 *** | 1 | |||

| 7. CSR | 26.50 | 17.03 | 0.398 *** | 0.140 *** | 0.294 *** | 0.055 *** | 0.122 *** | −0.001 | 1 | ||

| 8. Psrl | 26.09 | 5.987 | 0.087 *** | 0.156 *** | 0.092 *** | 0.080 *** | 0.024 *** | 0.005 | 0.266 *** | 1 | |

| 9. sub | 15.81 | 1.898 | 0.076 *** | 0.173 *** | 0.417 *** | 0.095 *** | 0.056 *** | −0.103 *** | 0.217 *** | 0.125 *** | 1 |

| Variables | M1 | M2 | M3 | M4 | M5 |

|---|---|---|---|---|---|

| CSR | 1.083 *** (0.011) | 1.583 *** (0.047) | 1.496 *** (0.088) | 1.887 *** (0.095) | |

| CSR2 | −0.012 *** (0.000) | −0.019 *** (0.001) | −0.020 *** (0.001) | −0.026 *** (0.001) | |

| Psrl | 0.266 *** (0.028) | 0.025 *** (0.028) | |||

| CSR × Psrl | 0.020 *** (0.002) | −0.019 *** (0.002) | |||

| CSR2 × Psrl | 0.0003 *** (0.000) | 0.0002 *** (0.000) | |||

| sub | 0.401 *** (0.084) | 0.331 *** (0.085) | |||

| CSR × sub | −0.025 *** (0.006) | −0.019 * (0.006) | |||

| CSR2 × sub | 0.001 *** (0.000) | 0.0004 ** (0.0001) | |||

| State | −0.845 *** (0.146) | −0.763 *** (0.116) | −0.767 *** (0.116) | −0.800 *** (0.116) | −0.787 *** (0.116) |

| lnsize | 0.807 *** (0.058) | 0.140 ** (0.047) | 0.149 ** (0.047) | 0.021 (0.050) | −0.021 *** (0.050) |

| lnage | −0.550 *** (0.079) | 0.464 *** (0.063) | 0.043 *** (0.004) | 0.527 *** (0.064) | 0.560 *** (0.064) |

| shrcr | 0.087 *** (0.005) | 0.042 *** (0.004) | 0.043 (0.004) | 0.043 *** (0.004) | 0.044 (0.004) |

| Slack | −0.020 *** (0.006) | −0.049 *** (0.004) | −0.046 *** (0.004) | −0.047 *** (0.004) | −0.045 *** (0.004) |

| N | 18,324 | 18,324 | 18,324 | 18,324 | 18,324 |

| R2 | 0.0535 | 0.4116 | 0.4155 | 0.4144 | 0.4180 |

| Adj R2 | 0.0533 | 0.4114 | 0.4151 | 0.4141 | 0.4176 |

| F | 207.27 | 1830.40 | 1301.55 | 1295.88 | 1011.78 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, W.; Ye, G.; Xu, G.; Liu, C.; Deng, D.; Huang, M. CSR and Long-Term Corporate Performance: The Moderating Effects of Government Subsidies and Peer Firm’s CSR. Sustainability 2022, 14, 5543. https://doi.org/10.3390/su14095543

Zhao W, Ye G, Xu G, Liu C, Deng D, Huang M. CSR and Long-Term Corporate Performance: The Moderating Effects of Government Subsidies and Peer Firm’s CSR. Sustainability. 2022; 14(9):5543. https://doi.org/10.3390/su14095543

Chicago/Turabian StyleZhao, Wenli, Guangyu Ye, Guangyi Xu, Chong Liu, Dandan Deng, and Ming Huang. 2022. "CSR and Long-Term Corporate Performance: The Moderating Effects of Government Subsidies and Peer Firm’s CSR" Sustainability 14, no. 9: 5543. https://doi.org/10.3390/su14095543