Changes in Corporate Responsibility Management during COVID-19 Crisis and Their Effects on Business Resilience: An Empirical Study of Swiss and German Companies

Abstract

:1. Introduction

2. Theoretical Framework, Research Questions, and Hypothesis

2.1. Core Concepts and Theoretical Underpinnings

2.2. Research Questions and Hypothesis

3. Methods and Results of Studies 1 and 2

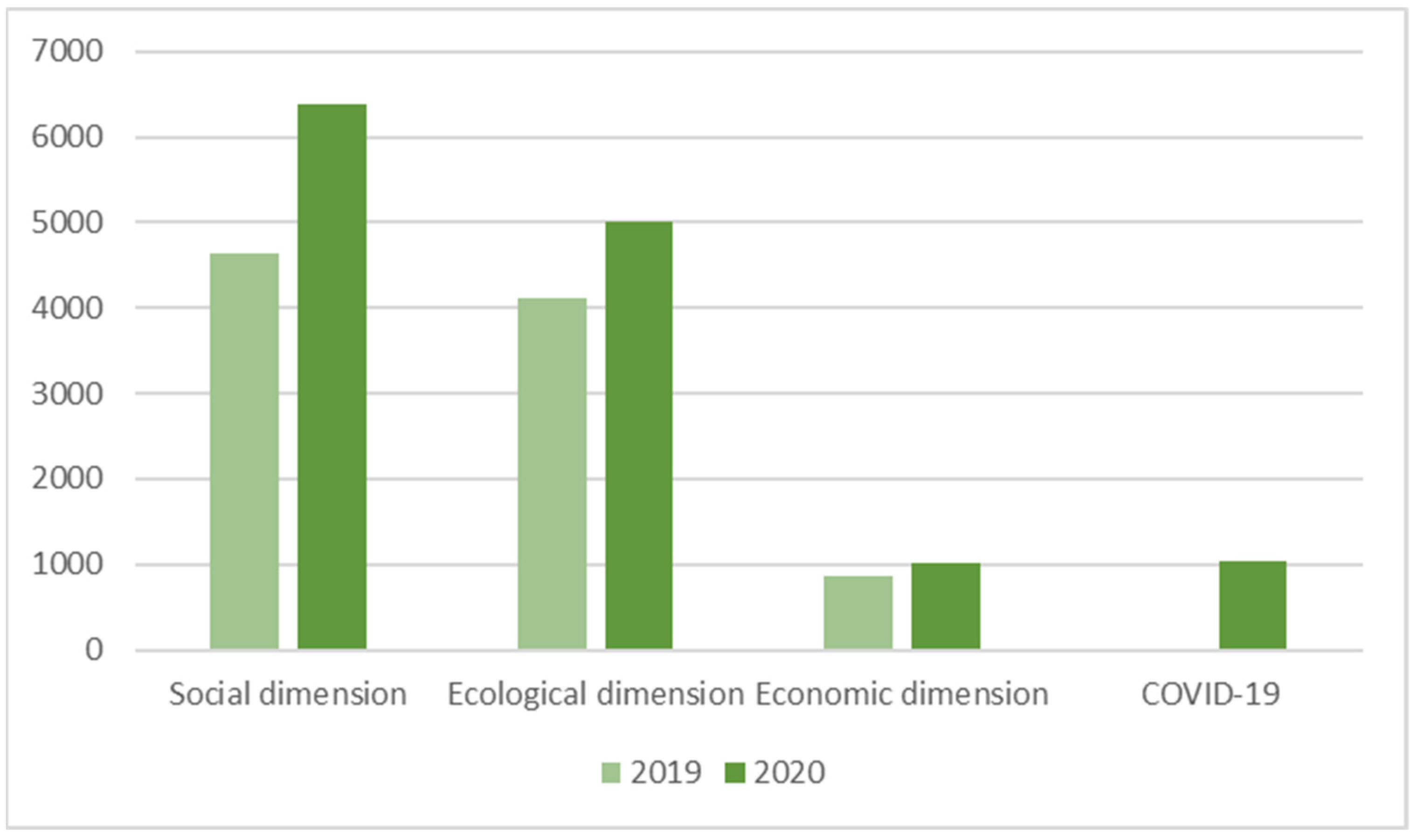

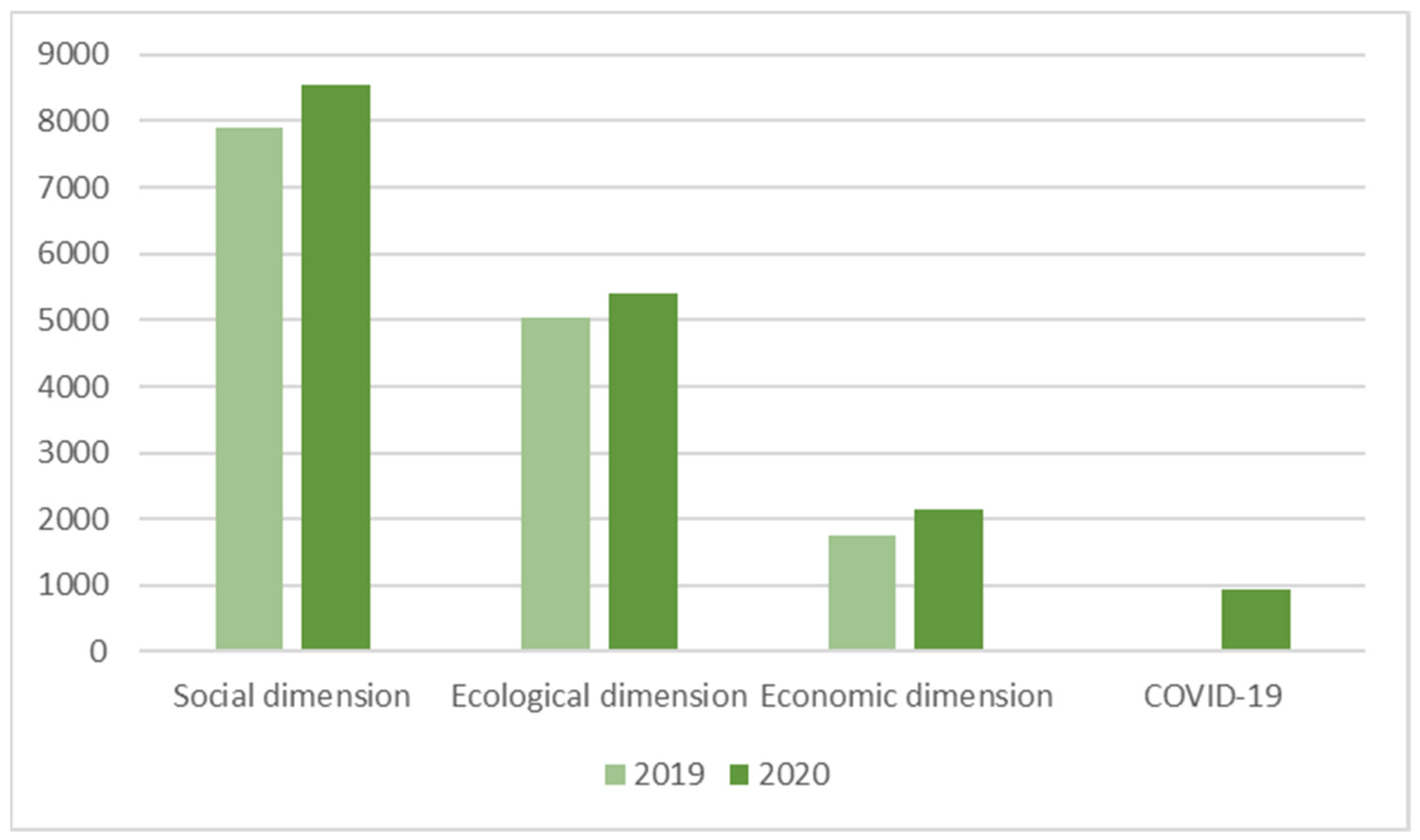

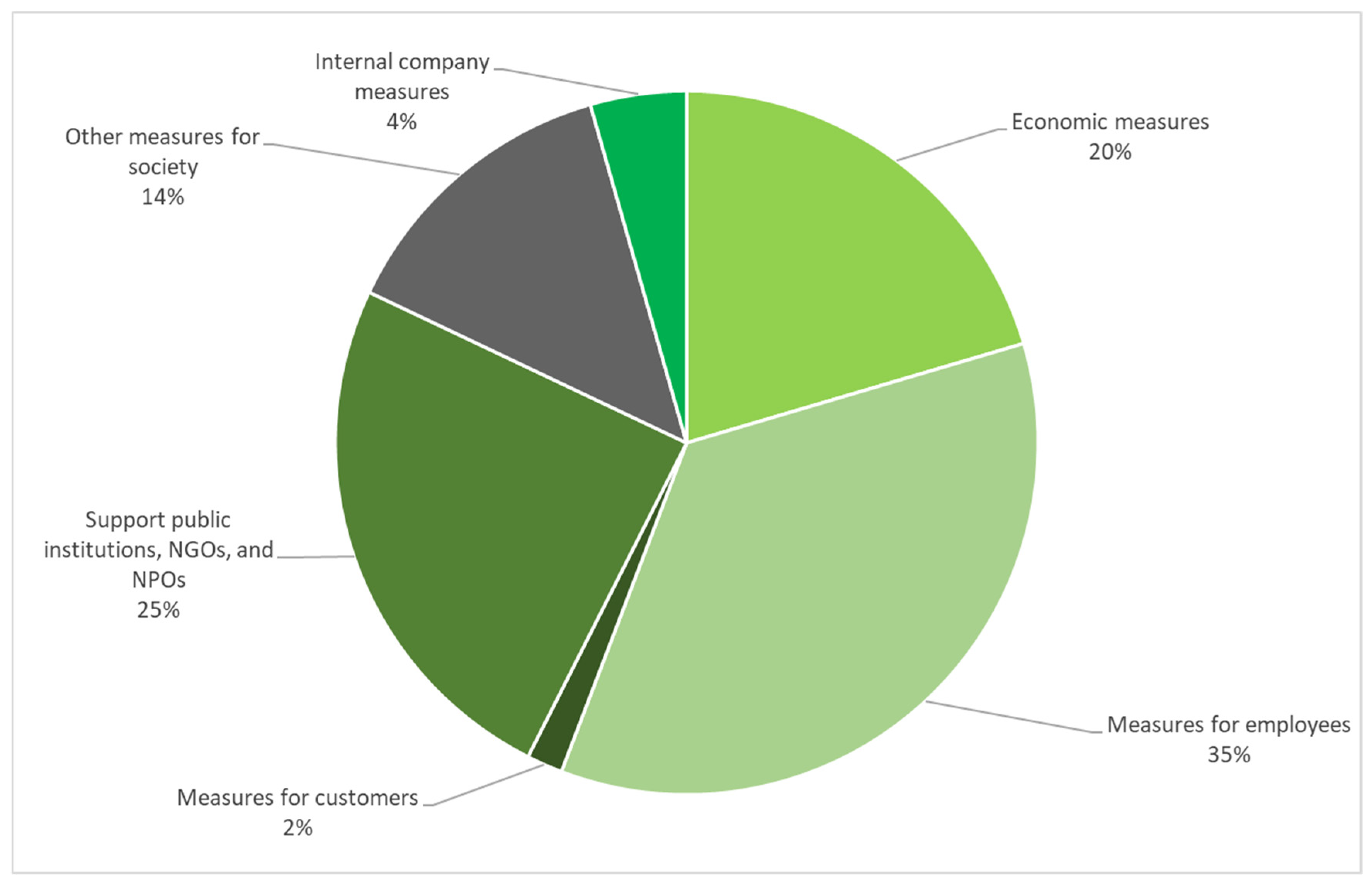

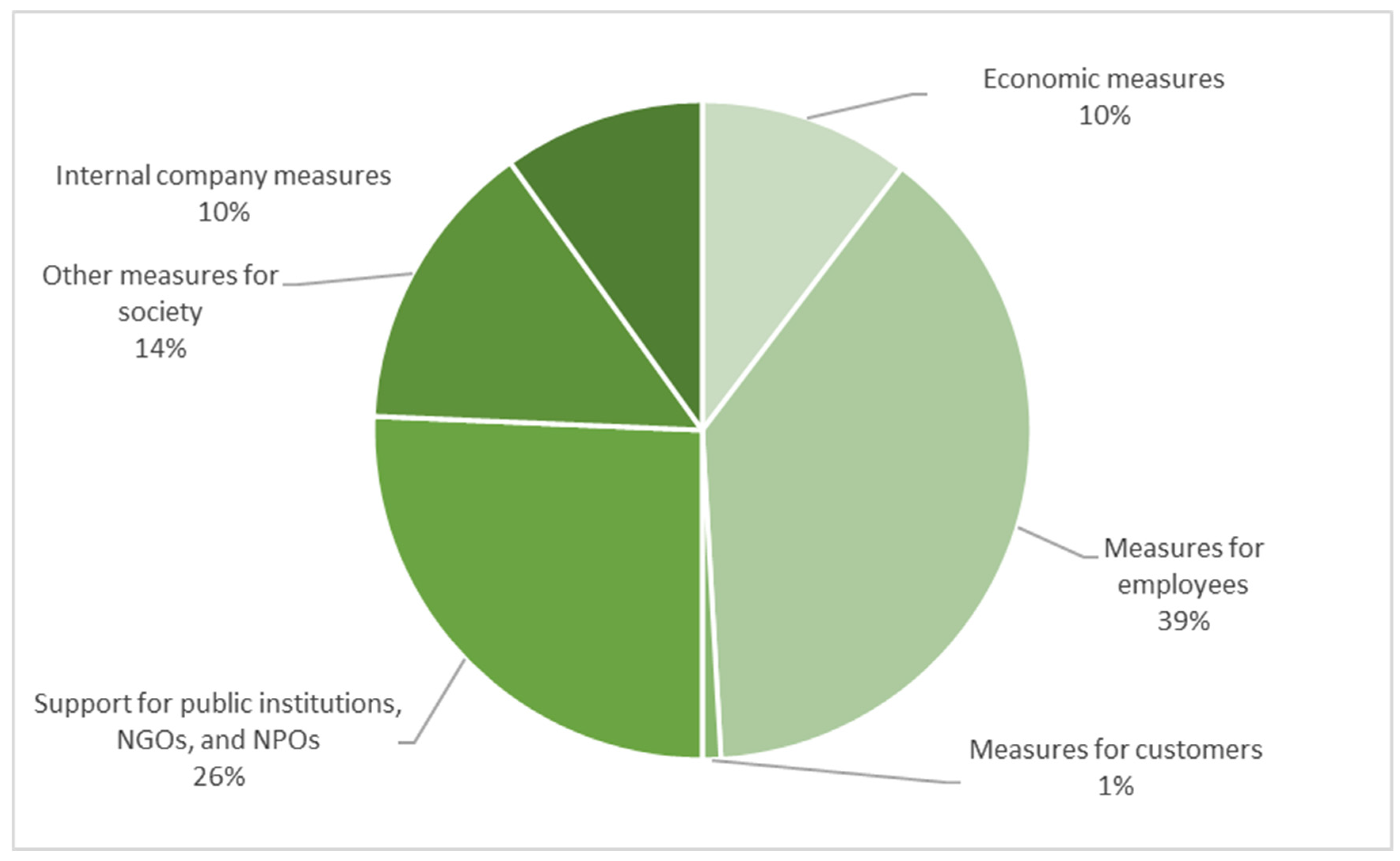

3.1. Methodology of Study 1: Quantitative and Qualitative Content Analysis of Annual Reports

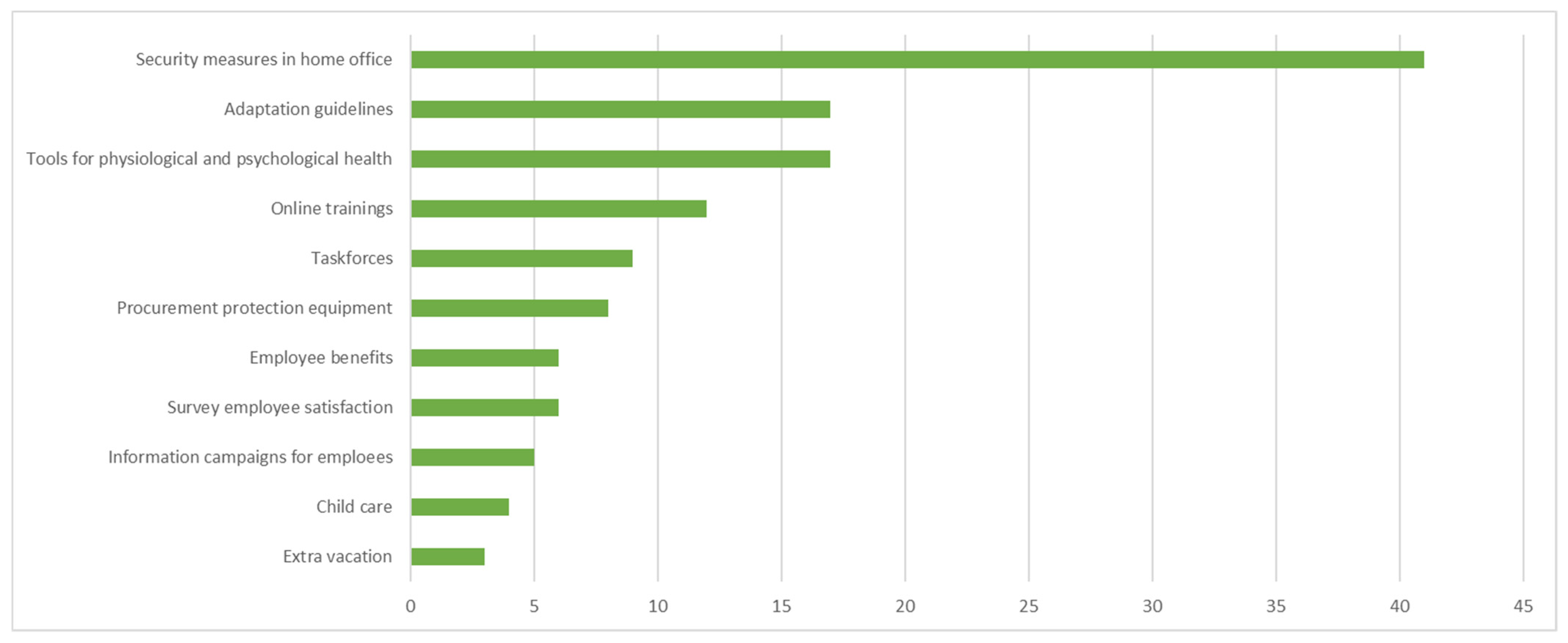

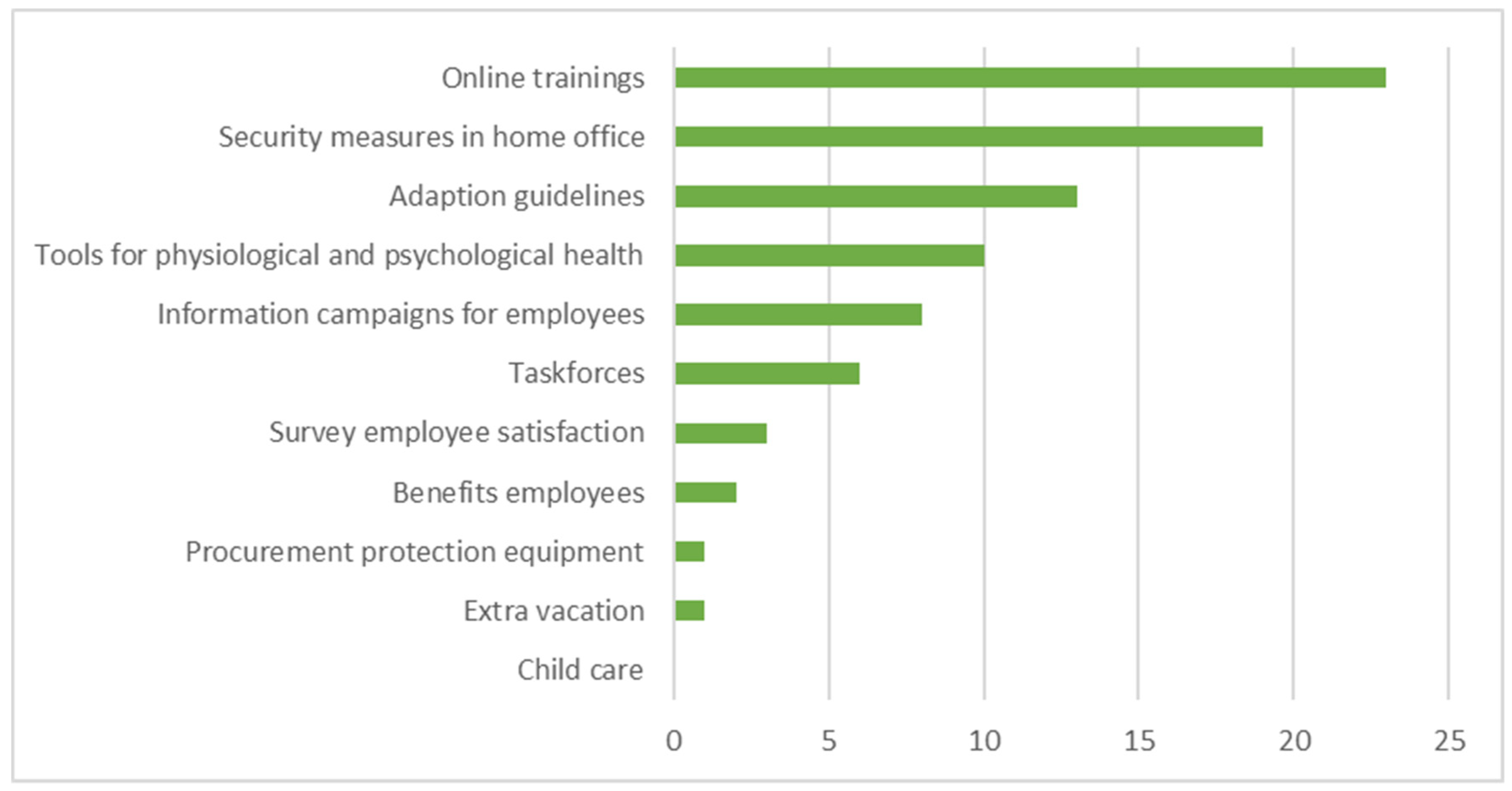

3.2. Results of Study 1: Quantitative and Qualitative Content Analysis of Annual Reports

3.3. Discussion of Study 1 Findings

3.4. Methodology of Study 2: A Quantitative Survey among Swiss Managers

3.4.1. Sample

3.4.2. Dependent Variables

3.4.3. Independent Variable

3.4.4. Control Variables

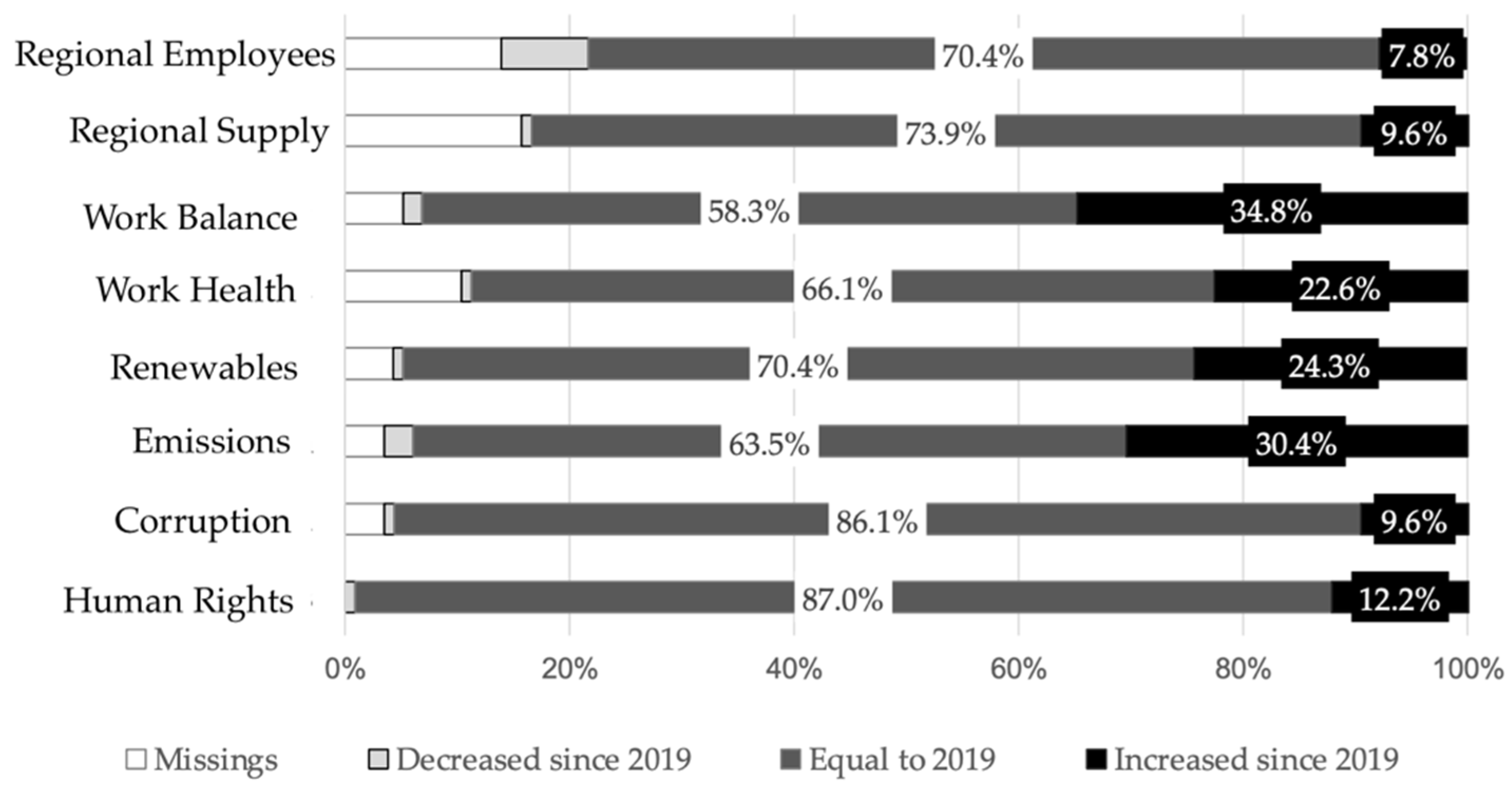

3.5. Results of Study 2

3.5.1. Preliminary Analysis

3.5.2. Corporate-Responsibility-Specific Effects on Expected Business Performance in 2021

3.6. Discussion of Study 2 Findings

4. General Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Carroll, A.B. Corporate social responsibility (CSR) and the COVID-19 pandemic: Organizational and managerial implications. J. Strategy Manag. 2021, 14, 315–330. [Google Scholar] [CrossRef]

- World Bank 2021. Available online: https://www.worldbank.org/en/news/infographic/2021/02/17/how-covid-19is-affecting-companies-around-the-world (accessed on 14 October 2021).

- McKinsey & Company. How Companies Capture the Value of Sustainability: Survey Findings. 2021. Available online: https://www.mckinsey.com/business-functions/sustainability/our-insights/how-companies-capture-the-value-of-sustainability-survey-findings (accessed on 14 October 2021).

- Statista 2021. Available online: https://de.statista.com/themen/6460/auswirkungen-des-coronavirus-covid-19-auf-die-wirtschaft-in-der-schweiz (accessed on 14 October 2021).

- Ioannis, P. Novel CSR & novel coronavirus: Corporate social responsibility inside the frame of coronavirus pandemic in Greece. Int. J. Corp. Soc. Responsib. 2021, 6, 1–12. [Google Scholar]

- Jashim, U.A.; Islam, Q.T.; Ahmed, A.; Faroque, A.R.; Mohammad, J.U. Corporate social responsibility in the wake of COVID-19: Multiple cases of social responsibility as an organizational value. Soc. Bus. Rev. 2021, 16, 496–516. [Google Scholar]

- Koutoupis, A.; Kyriakogkonas, P.; Pazarskis, M.; Davidopoulos, L. Corporate governance and COVID-19: A literature review. Corp. Gov. 2021, 21, 969–982. [Google Scholar] [CrossRef]

- Mahmud, A.; Ding, D.; Hasan, M.M. Corporate Social Responsibility: Business Responses to Coronavirus (COVID-19) Pandemic. SAGE 2021, 11, 2158244020988710. [Google Scholar] [CrossRef]

- Navickas, V.; Kontautiene, R.; Stravinskiene, J.; Bilan, Y. Paradigm shift in the concept of corporate social responsibility: COVID-19. Green Financ. 2021, 3, 138–152. [Google Scholar] [CrossRef]

- Raima, N.; Rella, A.; Vitolla, F.; Sanchez-Vicente, M.-I. Corporate Social Responsibility in the COVID-19 Pandemic Period: A Traditional Way to Address New Social Issues. Sustainability 2021, 13, 6561. [Google Scholar] [CrossRef]

- Rodriguez-Sanchez, A.; Guinot, J.; Chiva, R.; Lopez-Cabrales, A. How to emerge stronger: Antecedents and consequences of organizational resilience. J. Manag. Organ. 2021, 27, 442–459. [Google Scholar] [CrossRef] [Green Version]

- Manuel, T.; Herron, T.L. An ethical perspective of business CSR and the COVID-19 pandemic. Soc. Bus. Rev. 2020, 15, 235–253. [Google Scholar] [CrossRef]

- Qiu, S.; Jiang, J.; Liu, X.; Chen, M.-H.; Yuan, X. Can corporate social responsibility protect firm value during the COVID-19 pandemic? Int. J. Hosp. Manag. 2021, 93, 102759. [Google Scholar] [CrossRef]

- Sajjad, A. The COVID-19 pandemic, social sustainability and global supply chain resilience: A review. Corp. Gov. 2021, 21, 1142–1154. [Google Scholar] [CrossRef]

- Schaltegger, S. Sustainability learnings from the COVID-19 crisis. Opportunities for resilient industry and business development. Sustain. Account. Manag. Policy J. 2021, 12, 889–897. [Google Scholar] [CrossRef]

- Tarigan, Z.J.H.; Siagian, H.; Jie, F. Impact of Internal Integration, Supply Chain Partnership, Supply Chain Agility, and Supply Chain Resilience on Sustainable Advantage. Sustainability 2021, 13, 5460. [Google Scholar] [CrossRef]

- Huang, W.; Chen, S.; Nguyen, L.T. Corporate Social Responsibility and Organizational Resilience to COVID-19 Crisis: An Empirical Study of Chinese Firms. Sustainability 2020, 12, 8970. [Google Scholar] [CrossRef]

- Wendong Lv, Y.W.; Li, X.; Lin, L. What Dimensions of CSR Matters to Organizational Resilience? Evidence from China. Sustainability 2019, 11, 1561. [Google Scholar]

- Carmeli, A.; Dothan, A.; Boojihawon, D.K. Resilience of sustainability-oriented and financially-driven organizations. Bus. Strategy Environ. 2019, 29, 154–169. [Google Scholar] [CrossRef]

- Harwood, I.; Humby, S.; Harwood, A. On the resilience of Corporate Social Responsibility. Eur. Manag. J. 2011, 29, 283–290. [Google Scholar] [CrossRef]

- Arora, S.; Sur, J.K.; Chauhan, Y. Does corporate social responsibility affect shareholder value? Evidence from the COVID-19 crisis. Int. Rev. Financ. 2021, 1–10. Available online: https://onlinelibrary.wiley.com/doi/pdfdirect/10.1111/irfi.12353 (accessed on 23 June 2021). [CrossRef]

- Camilleri, M.A. The employees’ state of mind during COVID-19: A self-determination theory perspective. Sustainability 2021, 13, 3634. [Google Scholar] [CrossRef]

- Godfrey, P. The Relationship between Corporate Philanthropy and Shareholder Wealth: A Risk Management Perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef] [Green Version]

- Fombrun, C.J.; Gardberg, N.A.; Barnett, M.L. Opportunity platforms and safety nets: Corporate citizenship and reputational risk. Bus. Soc. Rev. 2000, 105, 85–106. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility: The centerpiece of competing and complementary frameworks. Organ. Dyn. 2015, 44, 87–96. [Google Scholar] [CrossRef]

- European Commission. Green Paper: Promoting a European Framework for Corporate Responsibility. 2011. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2001:0366:FIN:en:PDF (accessed on 23 June 2021).

- Brand, F.S.; Winistörfer, H. SML-Essentials: Corporate Responsibility Management; Buchzentrum: Hägendorf, Switzerland, 2017. [Google Scholar]

- Brand, F.S.; Jax, K. Focusing the Meaning(s) of Resilience: Resilience as a Descriptive Concept and a Boundary Object. Ecol. Soc. 2007, 12, 23. [Google Scholar] [CrossRef] [Green Version]

- Carpenter, S.; Walker, B.; Anderies, J.M.; Abel, N. From Metaphor to Measurement: Resilience of What to What? Ecosystems 2001, 4, 765–781. [Google Scholar] [CrossRef]

- Fombrun, C.J. Reputation; Harvard Business School Press: Boston, MA, USA, 1996. [Google Scholar]

- Godfrey, P.; Merrill, C.; Hansen, J.M. The Relationship between Corporate Social Responsibility and Shareholder Value: An Empirical Test of the Risk Management Hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Thalmann, G. The Relevance of Sustainability for Investors: Can Socially Responsible Investments Offer Investors Superior Returns or Reduced Volatility? 2019. Available online: https://digitalcollection.zhaw.ch/handle/11475/19093 (accessed on 23 June 2021).

- Rössler, P. Inhaltsanalyse, 3rd ed.; UKV Verlagsgesellschaft mbH.: Konstanz, Germany, 2017; Available online: https://books.google.ch/books/about/Inhaltsanalyse.html (accessed on 23 June 2021).

- Früh, W. Inhaltsanalyse: Theorie und Praxis, 8th ed.; UVK Verlagsgesellschaft mbH.: Konstanz, Germany, 2015. [Google Scholar]

- Mayring, P. Kombination und Integration qualitativer und quantitativer Analyse. Forum Qual. Soz. 2001, 2, 6. [Google Scholar]

- Latif, F.; Pérez, A.; Alam, W.; Saqib, A. Development and validation of a multi-dimensional customer-based scale to measure perceptions of corporate social responsibility (CSR). Soc. Responsib. J. 2019, 15, 492–512. [Google Scholar] [CrossRef] [Green Version]

- Fatma, M.; Rahman, Z.; Khan, I. Multi-item stakeholder based scale to measure CSR in the banking industry. Int. Strateg. Manag. Rev. 2014, 2, 9–20. [Google Scholar] [CrossRef] [Green Version]

- Öberseder, M.; Schlegelmilch, B.B.; Murphy, P.E.; Gruber, V. Consumers’ perceptions of corporate social responsibility: Scale development and validation. J. Bus. Ethics 2014, 124, 101–115. [Google Scholar] [CrossRef] [Green Version]

- Feng, M.; Wang, X.; Kreuze, J.G. Corporate social responsibility and firm financial performance: Comparison analyses across industries and CSR categories. Am. J. Bus. 2017, 32, 106–133. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and Society. The Link Between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Aguinis, H.; Villamor, I.; Gabriel, K.P. Understanding employee responses to COVID-19: A behavioral corporate social responsibility perspective. Manag. Res. J. Iberoam. Acad. Manag. 2020, 18, 421–438. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company | Number of Pages 2020 | Number of Pages 2019 | Change in % |

|---|---|---|---|

| ABB | 133 | 55 | +142 |

| LafargeHolcim | 89 | 93 | −4 |

| Lonza | 68 | 62 | +10 |

| Nestlé | 161 | 58 | +178 |

| Novartis | 94 | 70 | +34 |

| Richemont | 114 | 108 | +6 |

| Roche | 113 | 106 | +7 |

| Sika | 67 | 77 | −13 |

| UBS | 140 | 174 | −20 |

| Zurich Insurance | 73 | 44 | +66 |

| Company | Number of Pages 2020 | Number of Pages 2019 | Change in % |

|---|---|---|---|

| Adidas | 90 | 58 | +32 |

| Allianz | 136 | 102 | +34 |

| BASF | 81 | 65 | +16 |

| Bayer | 96 | 72 | +24 |

| BMW | 128 | 143 | −15 |

| Daimler | 194 | 205 | −11 |

| Deutsche Post | 33 | 59 | −26 |

| Deutsche Telekom | 159 | 113 | +46 |

| SAP SE | 106 | 104 | +2 |

| Siemens | 144 | 64 | +80 |

| Type of Industry | Number of Companies | Frequency |

|---|---|---|

| Machinery, electrical, and metal | 16 | 14.8 |

| Other services | 14 | 13 |

| Construction | 13 | 12 |

| Financial and insurance service providers | 10 | 9.3 |

| Public administration | 6 | 5.6 |

| Retail trade | 4 | 3.7 |

| Energy and water supply | 4 | 3.7 |

| Hospitality and tourism | 4 | 3.7 |

| IT and telecommunications | 4 | 3.7 |

| Food and beverage | 4 | 3.7 |

| Health and welfare | 3 | 2.8 |

| Education and teaching | 2 | 1.9 |

| Wholesale | 2 | 1.9 |

| Transport and delivery | 2 | 1.9 |

| Chemistry and pharmaceuticals | 1 | 1 |

| Art, entertainment, and recreation | 1 | 0.9 |

| Others and missing values | 18 | 16.7 |

| Primary Sector | Secondary Sector | Tertiary Sector | Quaternary Sector | |

|---|---|---|---|---|

| Less than CHF 2 million | 0 | 2 | 11 | 3 |

| CHF 2–10 million | 0 | 6 | 3 | 2 |

| CHF 10–50 million | 0 | 7 | 7 | 4 |

| CHF 50–250 million | 3 | 13 | 5 | 2 |

| CHF 250–1 billion | 2 | 7 | 3 | 0 |

| More than CHF 1 billion | 1 | 11 | 20 | 4 |

| Variable | M | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|---|---|

| 1. Regional suppliers | 2.94 | 1.43 | |||||||

| 2. Regional employees/recruiting | 2.75 | 1.37 | 0.58 ** | ||||||

| [0.44, 0.69] | |||||||||

| 3. Work balance | 3.31 | 1.11 | 0.12 | 0.21 * | |||||

| [−0.07, 0.30] | [0.02, 0.38] | ||||||||

| 4. Occupational health | 2.80 | 1.06 | 0.22 * | 0.32 ** | 0.62 ** | ||||

| [0.03, 0.39] | [0.14, 0.48] | [0.48, 0.72] | |||||||

| 5. Renewables | 3.52 | 1.16 | 0.30 ** | 0.34 ** | 0.34 ** | 0.36 ** | |||

| [0.12, 0.46] | [0.16, 0.49] | [0.16, 0.50] | [0.18, 0.51] | ||||||

| 6. Emissions | 3.32 | 1.28 | 0.29 ** | 0.31 ** | 0.34 ** | 0.34 ** | 0.86 ** | ||

| [0.11, 0.46] | [0.13, 0.47] | [0.16, 0.49] | [0.16, 0.50] | [0.80, 0.90] | |||||

| 7. Human rights | 3.66 | 1.19 | 0.14 | 0.12 | 0.14 | 0.15 | 0.42 ** | 0.48 ** | |

| [−0.05, 0.32] | [−0.07, 0.30] | [−0.05, 0.32] | [−0.04, 0.33] | [0.25, 0.57] | [0.32, 0.62] | ||||

| 8. Corruption | 3.78 | 1.26 | 0.18 | 0.22 * | 0.04 | 0.11 | 0.39 ** | 0.36 ** | 0.68 ** |

| [−0.01, 0.36] | [0.03, 0.39] | [−0.15, 0.22] | [−0.08, 0.30] | [0.22, 0.54] | [0.19, 0.52] | [0.56, 0.77] |

| Dependent Variable | |||

|---|---|---|---|

| Business 2019 | Business 2020 | Business 2021 | |

| (1) | (2) | (3) | |

| Revenue in CHF | 0.13 (0.08) | 0.16 (0.11) | 0.05 (0.11) |

| Delta Region Supply | −0.49 (0.48) | −0.46 (0.67) | −0.72 (0.69) |

| Delta Region Employees | 0.24 (0.38) | 1.68 ** (0.52) | 1.93 *** (0.53) |

| Delta Work Balance | −0.02 (0.30) | 0.13 (0.41) | −0.02 (0.42) |

| Delta Occ. Health | −0.61 (0.34) | 0.04 (0.47) | 0.53 (0.48) |

| Delta Renewables | 0.52 (0.47) | −0.30 (0.66) | 0.35 (0.67) |

| Delta Emissions | −0.05 (0.41) | 0.02 (0.57) | −0.07 (0.59) |

| Delta Corruption | −0.08 (0.54) | 0.28 (0.74) | 0.13 (0.76) |

| Delta Human Rights | −0.34 (0.55) | −0.05 (0.77) | −0.42 (0.78) |

| Constant | 7.38 *** (1.47) | 2.29 (2.05) | 1.76 (2.10) |

| Observations | 73 | 73 | 72 |

| R2 | 0.11 | 0.19 | 0.22 |

| Adjusted R2 | −0.02 | 0.08 | 0.11 |

| Residual Std. Error | 1.09 (df = 63) | 1.52 (df = 63) | 1.55 (df = 62) |

| F Statistic | 0.86 (df = 9; 63) | 1.69 (df = 9; 63) | 1.98 (df = 9; 62) |

| Dependent Variable | |||

|---|---|---|---|

| Business 2021−Business 2019 | Business 2020−Business 2019 | Business 2021−Business 2020 | |

| (4) | (5) | (6) | |

| Revenue in CHF | −0.10 (0.13) | 0.03 (0.13) | −0.10 (0.06) |

| Delta Region Supply | −0.23 (0.79) | 0.03 (0.80) | −0.26 (0.39) |

| Delta Region Employees | 1.69 ** (0.62) | 1.44 * (0.62) | 0.25 (0.30) |

| Delta Work Balance | 0.04 (0.49) | 0.16 (0.49) | −0.16 (0.24) |

| Delta Health | 1.18 * (0.55) | 0.65 (0.56) | 0.49 (0.27) |

| Delta Renewables | −0.18 (0.78) | −0.82 (0.78) | 0.65 (0.38) |

| Delta Emission | 0.02 (0.68) | 0.07 (0.68) | −0.10 (0.33) |

| Delta Corruption | 0.24 (0.88) | 0.36 (0.89) | −0.16 (0.43) |

| Delta Human Rights | −0.07 (0.90) | 0.28 (0.91) | −0.37 (0.44) |

| Constant | −5.89 * (2.42) | −5.09 * (2.44) | −0.49 (1.19) |

| Observations | 72 | 73 | 72 |

| R2 | 0.17 | 0.13 | 0.15 |

| Adjusted R2 | 0.05 | 0.0002 | 0.02 |

| Residual Std. Error | 1.79 (df = 62) | 1.81 (df = 63) | 0.88 (df = 62) |

| F Statistic | 1.43 (df = 9; 62) | 1.00 (df = 9; 63) | 1.18 (df = 9; 62) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Brand, F.S.; Blaese, R.; Weber, G.; Winistoerfer, H. Changes in Corporate Responsibility Management during COVID-19 Crisis and Their Effects on Business Resilience: An Empirical Study of Swiss and German Companies. Sustainability 2022, 14, 4144. https://doi.org/10.3390/su14074144

Brand FS, Blaese R, Weber G, Winistoerfer H. Changes in Corporate Responsibility Management during COVID-19 Crisis and Their Effects on Business Resilience: An Empirical Study of Swiss and German Companies. Sustainability. 2022; 14(7):4144. https://doi.org/10.3390/su14074144

Chicago/Turabian StyleBrand, Fridolin Simon, Richard Blaese, Giulia Weber, and Herbert Winistoerfer. 2022. "Changes in Corporate Responsibility Management during COVID-19 Crisis and Their Effects on Business Resilience: An Empirical Study of Swiss and German Companies" Sustainability 14, no. 7: 4144. https://doi.org/10.3390/su14074144