Environmental, Social, and Governance Integration into the Business Model: Literature Review and Research Agenda

Abstract

:1. Introduction

2. Literature Review

2.1. Socially Responsible Investment

ESG Integration

2.2. Firm Sustainability

ESG Integration into Firms: Sustainable Development

3. Research Methodology

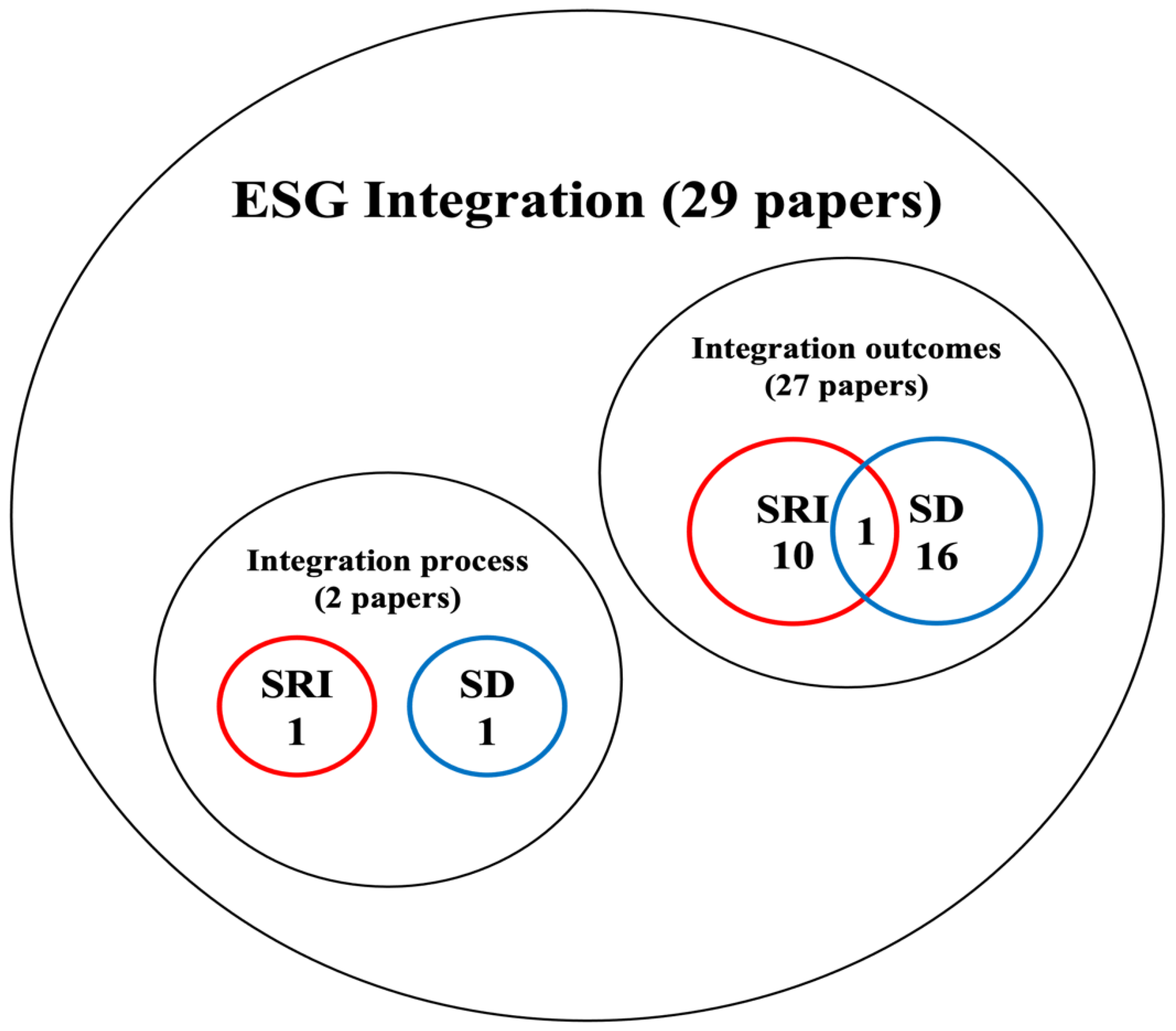

4. Findings

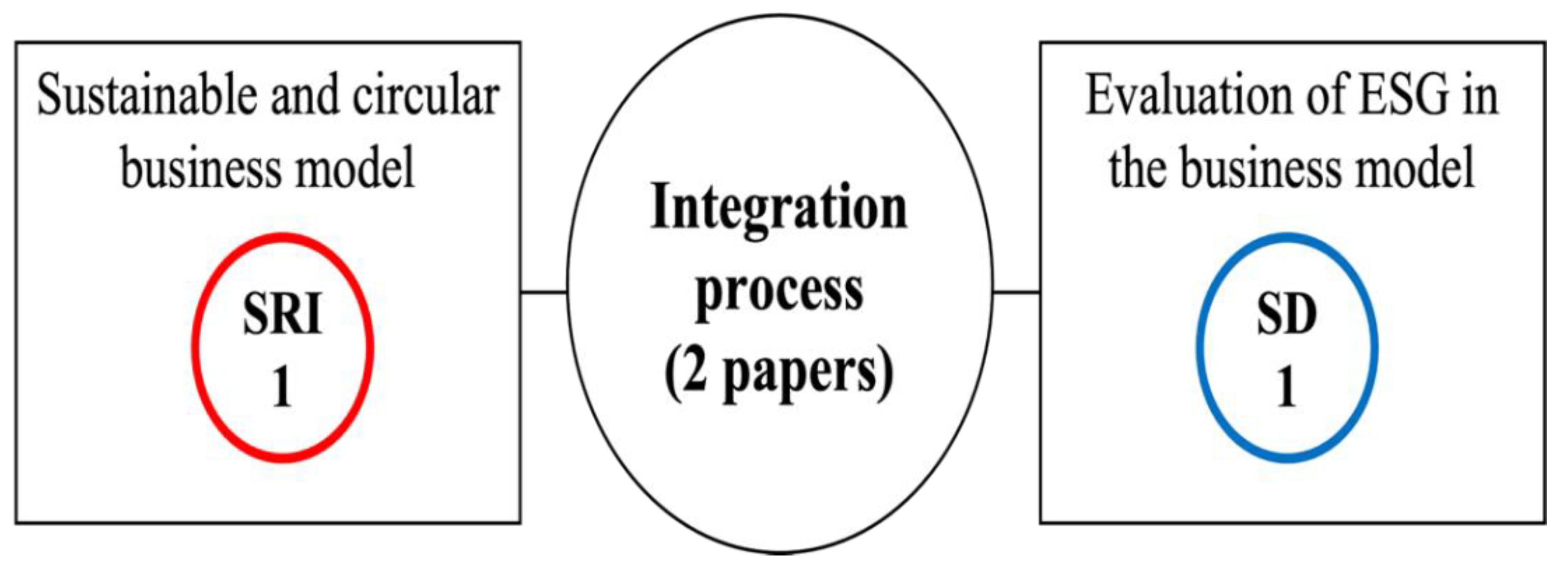

4.1. ESG Integration: The Integration Process

4.2. ESG Integration: Outcomes

4.2.1. Integration Behaviors

4.2.2. Advantages of ESG Integration

4.2.3. Practices

4.2.4. Critical Views

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Eccles, R.; Stroehle, J. Exploring Social Origins in the Construction of ESG Measures; Saïd Business School, University of Oxford: Oxford, UK, 2018. [Google Scholar] [CrossRef]

- Global Sustainable Investment Alliance. Global Sustainable Investment Review; Global Sustainable Investment Alliance: Washington, DC, USA, 2020. [Google Scholar]

- Yu, E.P.Y.; Luu, B.V.; Chen, C.H. Greenwashing in environmental, social and governance disclosures. Res. Int. Bus. Financ. 2020, 52, 101192. [Google Scholar] [CrossRef]

- Sugai, P. The Definition, Identification and Eradication of Value Washing. J. Creat. Value 2021, 7, 165–169. [Google Scholar] [CrossRef]

- Zammit, A. Development at Risk Rethinking UN-Business Partnerships; South Centre: Geneva, Switzerland; UNRISD: Geneva, Switzerland, 2003; pp. 1–277. [Google Scholar]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef] [Green Version]

- Grant, M.; Booth, A. A typology of reviews: An analysis of 14 review types and associated methologies. Health Inf. Libr. J. 2009, 26, 91–108. [Google Scholar] [CrossRef] [PubMed]

- Amir, A.Z.; Serafeim, G. Why and how investors use ESG information: Evidence from a global survey. Financ. Anal. J. 2018, 74, 87–103. [Google Scholar] [CrossRef] [Green Version]

- Sparkes, R. The Ethical Investor; HarperCollins Publishers Inc.: New York, NY, USA, 1995. [Google Scholar]

- Townsend, B. From SRI to ESG: The Origins of Socially Responsible and Sustainable Investing. J. Impact ESG Investig. 2020, 1, 10–25. [Google Scholar] [CrossRef]

- Puaschunder, J.M. The History of Ethical, Environmental, Social, and Governance-Oriented Investments as a Key to Sustainable Prosperity in the Finance World. Public Integr. 2019, 21, 161–181. [Google Scholar] [CrossRef]

- Chang, C.E.; Nelson, W.A.; Doug Witte, H. Do green mutual funds perform well? Manag. Res. Rev. 2012, 35, 693–708. [Google Scholar] [CrossRef]

- Eyraud, L.; Clements, B.; Wane, A. Green investment: Trends and determinants. Energy Policy 2013, 60, 852–865. [Google Scholar] [CrossRef]

- Sandberg, J.; Juravle, C.; Hedesström, T.M.; Hamilton, I. The Heterogeneity of Socially Responsible Investment. J. Bus. Ethics 2009, 87, 519–533. [Google Scholar] [CrossRef]

- von Wallis, M.; Klein, C. Ethical requirement and financial interest: A literature review on socially responsible investing. Bus. Res. 2015, 8, 61–98. [Google Scholar] [CrossRef] [Green Version]

- Barroso, J.S.S.; Araújo, E.A. Socially responsible investments (SRIs)—mapping the research field. Soc. Responsib. J. 2020, 17, 508–523. [Google Scholar] [CrossRef]

- Widyawati, L. A systematic literature review of socially responsible investment and environmental social governance metrics. Bus. Strategy Environ. 2020, 29, 619–637. [Google Scholar] [CrossRef]

- Losse, M.; Geissdoerfer, M. Mapping socially responsible investing: A bibliometric and citation network analysis. J. Clean. Prod. 2021, 296, 126376. [Google Scholar] [CrossRef]

- Chatzitheodorou, K.; Skouloudis, A.; Evangelinos, K.; Nikolaou, I. Exploring socially responsible investment perspectives: A literature mapping and an investor classification. Sustain. Prod. Consum. 2019, 19, 117–129. [Google Scholar] [CrossRef]

- Eccles, N.S.; Viviers, S. The Origins and Meanings of Names Describing Investment Practices that Integrate a Consideration of ESG Issues in the Academic Literature. J. Bus. Ethics 2011, 104, 389–402. [Google Scholar] [CrossRef]

- Nagel, S.; Hiss, S.; Woschnack, D.; Teufel, B. Between Efficiency and Resilience: The Classification of Companies according to their Sustainability Performance. Hist. Soc. Res. 2017, 42, 189–210. [Google Scholar] [CrossRef]

- Robeco. Sustainability Report; Robeco: Rotterdam, The Netherlands, 2020. [Google Scholar]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef] [Green Version]

- Conca, L.; Manta, F.; Morrone, D.; Toma, P. The impact of direct environmental, social, and governance reporting: Empirical evidence in European-listed companies in the agri-food sector. Bus. Strategy Environ. 2021, 30, 1080–1093. [Google Scholar] [CrossRef]

- Brooks, C.; Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. Br. Account. Rev. 2018, 50, 1–15. [Google Scholar] [CrossRef]

- Duque, E.; Caracuel, J. Environmental, Social and Governance (ESG) Scores and Financial Performance of Multilatinas: Moderating Effects of Geographic International Diversification and Financial Slack. J. Bus. Ethics 2021, 168. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R. Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Camilleri, M.A. The market for socially responsible investing: A review of the developments. Soc. Responsib. J. 2021, 17, 412–428. [Google Scholar] [CrossRef]

- Landau, A.; Rochell, J.; Klein, C.; Zwergel, B. Integrated reporting of environmental, social, and governance and financial data: Does the market value integrated reports? Bus. Strategy Environ. 2020, 29, 1750–1763. [Google Scholar] [CrossRef] [Green Version]

- Sultana, S.; Zainal, D.; Zulkifli, N. The influence of environmental, social and governance (ESG) on investment decisions: The Bangladesh perspective. Pertanika J. Soc. Sci. Humanit. 2017, 25, 155–173. [Google Scholar]

- Van Duuren, E.; Plantinga, A.; Scholtens, B. ESG Integration and the Investment Management Process: Fundamental Investing Reinvented. J. Bus. Ethics 2016, 138, 525–533. [Google Scholar] [CrossRef] [Green Version]

- Cappucci, M. The ESG Integration Paradox. SSRN Electron. J. 2018, 30, 22–28. [Google Scholar] [CrossRef]

- Choenmaker, D.; Schramade, W. Investing for long-term value creation. J. Sustain. Financ. Investig. 2019, 9, 356–377. [Google Scholar] [CrossRef] [Green Version]

- Friede, G. Why don’t we see more action? A metasynthesis of the investor impediments to integrate environmental, social, and governance factors. Bus. Strategy Environ. 2019, 28, 1260–1282. [Google Scholar] [CrossRef]

- Sciarelli, M.; Cosimato, S.; Landi, G.; Iandolo, F. Socially responsible investment strategies for the transition towards sustainable development: The importance of integrating and communicating ESG. TQM J. 2021, 33, 39–56. [Google Scholar] [CrossRef]

- Przychodzen, J.; Gómez-Bezares, F.; Przychodzen, W.; Larreina, M. ESG issues among fund managers-factors and motives. Sustainability 2016, 8, 1078. [Google Scholar] [CrossRef] [Green Version]

- Loock, M.; Phillips, D.M. A Firm’s Financial Reputation vs. Sustainability Reputation: Do Consumers Really Care? Sustainability 2020, 12, 10519. [Google Scholar] [CrossRef]

- Jeffrey, S.; Rosenberg, S.; McCabe, B. Corporate social responsibility behaviors and corporate reputation. Soc. Responsib. J. 2019, 15, 395–408. [Google Scholar] [CrossRef]

- Gong, M.; Gao, Y.; Koh, L.; Sutcliffe, C.; Cullen, J. The role of customer awareness in promoting firm sustainability and sustainable supply chain management. Int. J. Prod. Econ. 2019, 217, 88–96. [Google Scholar] [CrossRef]

- Schalock, R.L.; Verdugo, M.; Lee, T. A systematic approach to an organization’s sustainability. Eval. Program Plan. 2016, 56, 56–63. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Bernardo, M.; José de Oliveira, O. Rethinking the way of doing business: A reframe of management structures for developing corporate sustainability. Sustainability 2020, 12, 1177. [Google Scholar] [CrossRef] [Green Version]

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Cavaleri, S.; Shabana, K. Rethinking sustainability strategies. J. Strategy Manag. 2018, 1, 2–18. [Google Scholar] [CrossRef]

- Engert, S.; Baumgartner, R.J. Corporate sustainability strategy—Bridging the gap between formulation and implementation. J. Clean. Prod. 2016, 113, 822–834. [Google Scholar] [CrossRef]

- Nosratabadi, S.; Mosavi, A.; Shamshirband, S.; Zavadskas, E.K.; Rakotonirainy, A.; Chau, K.W. Sustainable business models: A review. Sustainability 2019, 11, 1663. [Google Scholar] [CrossRef] [Green Version]

- Goni, F.A.; Gholamzadeh Chofreh, A.; Estaki Orakani, Z.; Klemeš, J.J.; Davoudi, M.; Mardani, A. Sustainable business model: A review and framework development. Clean Technol. Environ. Policy 2021, 23, 889–897. [Google Scholar] [CrossRef]

- Lozano, R. Sustainable business models: Providing a more holistic perspective. Bus. Strategy Environ. 2018, 27, 1159–1166. [Google Scholar] [CrossRef]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Cosenz, F.; Rodrigues, V.P.; Rosati, F. Dynamic business modeling for sustainability: Exploring a system dynamics perspective to develop sustainable business models. Bus. Strategy Environ. 2020, 29, 651–664. [Google Scholar] [CrossRef]

- Lozano, R. Towards better embedding sustainability into companies’ systems: An analysis of voluntary corporate initiatives. J. Clean. Prod. 2012, 25, 14–26. [Google Scholar] [CrossRef]

- Chevrollier, N.; Zhang, J.; van Leeuwen, T.; Nijhof, A. The predictive value of strategic orientation for ESG performance over time. Corp. Gov. 2019, 20, 123–142. [Google Scholar] [CrossRef]

- Ismail, A.M.; Latiff, I.H.M. Board diversity and corporate sustainability practices: Evidence on environmental, social and governance (ESG) reporting. Int. J. Financ. Res. 2019, 10, 31–50. [Google Scholar] [CrossRef] [Green Version]

- Arayssi, M.; Jizi, M.; Tabaja, H.H. The impact of board composition on the level of ESG disclosures in GCC countries. Sustain. Account. Manag. Policy J. 2020, 11, 137–161. [Google Scholar] [CrossRef]

- Lavin, J.F.; Montecinos-Pearce, A.A. ESG Reporting: Empirical Analysis of the Influence of Board Heterogeneity from an Emerging Market. Sustainability 2021, 13, 3090. [Google Scholar] [CrossRef]

- Wasiuzzaman, S.; Wan Mohammad, W.M. Board gender diversity and transparency of environmental, social and governance disclosure: Evidence from Malaysia. Manag. Decis. Econ. 2020, 41, 145–156. [Google Scholar] [CrossRef]

- Aureli, S.; Del Baldo, M.; Lombardi, R.; Nappo, F. Nonfinancial reporting regulation and challenges in sustainability disclosure and corporate governance practices. Bus. Strategy Environ. 2020, 29, 2392–2403. [Google Scholar] [CrossRef]

- Busch, T.; Bauer, R.; Orlitzky, M. Sustainable Development and Financial Markets: Old Paths and New Avenues. Bus. Soc. 2016, 55, 303–329. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, n71. [Google Scholar] [CrossRef]

- Nazzaro, C.; Uliano, A.; Marotta, G. Drivers and Barriers towards Social Farming: A Systematic Review. Sustainability 2021, 13, 14008. [Google Scholar] [CrossRef]

- Masuwai, A.; Zulkifli, H.; Tamuri, A.H. Systematic Literature Review on Self-Assessment Inventory for Quality Teaching among Islamic Education Teachers. Sustainability 2022, 14, 203. [Google Scholar] [CrossRef]

- Lumpkin, G.T.; Steier, L.; Wright, M. Strategic entrepreneurship in family business. Strateg. Entrep. J. 2011, 5, 285–306. [Google Scholar] [CrossRef]

- Mariani, M.M.; Al-Sultan, K.; De Massis, A. Corporate social responsibility in family firms: A systematic literature review. J. Small Bus. Manag. 2021, 1–55. [Google Scholar] [CrossRef]

- Michael, C.; Gizzi, S.R. The Practice of Qualitative Data Analysis Research Examples Using MAXQDA; MAXQDA Press: Berlin, Germany, 2021. [Google Scholar]

- Kuckartz, U.; Rädiker, S. Analyzing Qualitative Data with MAXQDA: Text., Audio, and Video; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar] [CrossRef]

- Schramade, W. Integrating ESG into valuation models and investment decisions: The value-driver adjustment approach. J. Sustain. Financ. Investig. 2016, 6, 95–111. [Google Scholar] [CrossRef]

- Corral-Marfil, J.A.; Arimany-Serrat, N.; Hitchen, E.L.; Viladecans-Riera, C. Recycling technology innovation as a source of competitive advantage: The sustainable and circular business model of a bicentennial company. Sustainability 2021, 13, 7723. [Google Scholar] [CrossRef]

- Di Tullio, P.; Valentinetti, D.; Nielsen, C.; Rea, M.A. In search of legitimacy: A semiotic analysis of business model disclosure practices. Meditari Account. Res. 2020, 28, 863–887. [Google Scholar] [CrossRef]

- Hill, C.A. Marshalling reputation to minimize problematic business conduct. Boston Univ. Law Rev. 2019, 99, 1193–1228. [Google Scholar]

- La Torre, M.; Leo, S.; Panetta, I.C. Banks and environmental, social and governance drivers: Follow the market or the authorities? Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1620–1634. [Google Scholar] [CrossRef]

- Lee, J.W. Green finance and sustainable development goals: The case of China. J. Asian Financ. Econ. Bus. 2020, 7, 577–586. [Google Scholar] [CrossRef]

- Ziolo, M.; Bak, I.; Cheba, K.; Spoz, A. The relationship between banks and company business models—Sustainability context. Procedia Comput. Sci. 2020, 176, 1507–1516. [Google Scholar] [CrossRef]

- Hoepner, A.G.F.; Schopohl, L. On the Price of Morals in Markets: An Empirical Study of the Swedish AP-Funds and the Norwegian Government Pension Fund. J. Bus. Ethics 2018, 151, 665–692. [Google Scholar] [CrossRef] [Green Version]

- Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M.; Escrig-Olmedo, E. Can environmental, social, and governance rating agencies favor business models that promote a more sustainable development? Corp. Soc. Responsib. Environ. Manag. 2019, 26, 439–452. [Google Scholar] [CrossRef]

- Camilleri, M.A. Theoretical insights on integrated reporting The inclusion of non-financial capitals in corporate disclosures. Corp. Commun. 2018, 23, 567–581. [Google Scholar] [CrossRef]

- Sushchenko, O.; Volkovskyi, I.; Fedosov, V.; Ryazanova, N. Environmental risks and sustainable development indicators: Determinants of impact. Econ. Ann.-XXI 2020, 185, 4–14. [Google Scholar] [CrossRef]

- Herciu, M. Sustainability And profitability can coexist. Improving business models. Fluxos Riscos 2018, 5, 15–33. [Google Scholar] [CrossRef]

- Sabbaghi, O. The behavior of green exchange-traded funds. Manag. Financ. 2011, 37, 426–441. [Google Scholar] [CrossRef]

- Turan, F.M.; Johan, K.; Omar, N.A. Development of hydropower sustainability assessment method in Malaysia context. In Proceedings of the 4th Asia Pacific Conference on Manufacturing Systems and the 3rd International Manufacturing Engineering Conference, Yogyakarta, Indonesia, 7–8 December 2017. [Google Scholar]

- Ashraf, D.; Rizwan, M.S.; L’Huillier, B. Environmental, social, and governance integration: The case of microfinance institutions. Account. Financ. 2021, 62, 837–891. [Google Scholar] [CrossRef]

- Rabaya, A.J.; Saleh, N.M. The moderating effect of IR framework adoption on the relationship between environmental, social, and governance (ESG) disclosure and a firm’s competitive advantage. Environ. Dev. Sustain. 2022, 24, 2037–2055. [Google Scholar] [CrossRef]

- Kluza, K.; Ziolo, M.; Spoz, A. Innovation and environmental, social, and governance factors influencing sustainable business models—Meta-analysis. J. Clean. Prod. 2021, 303, 127015. [Google Scholar] [CrossRef]

- Zubeltzu-Jaka, E.; Andicoechea-Arondo, L.; Alvarez Etxeberria, I. Corporate social responsibility and corporate governance and corporate financial performance: Bridging concepts for a more ethical business model. Bus. Strategy Dev. 2018, 1, 214–222. [Google Scholar] [CrossRef]

- Rezaee, Z.; Tuo, L. Are the Quantity and Quality of Sustainability Disclosures Associated with the Innate and Discretionary Earnings Quality? J. Bus. Ethics 2019, 155, 763–786. [Google Scholar] [CrossRef]

- Cassely, L.; Ben Larbi, S.; Revelli, C.; Lacroux, A. Corporate social performance (CSP) in time of economic crisis. Sustain. Account. Manag. Policy J. 2021, 12, 913–942. [Google Scholar] [CrossRef]

- Eccles, R.G.; Serafeim, G. The Performance Frontier: Innovating for a Sustainable Strategy. Harv. Bus. Rev. 2013, 91, 50–60. [Google Scholar]

- Venanzi, D.; Matteucci, P. The largest cooperative banks in Continental Europe: A sustainable model of banking. Int. J. Sustain. Dev. World Ecol. 2021, 29, 84–97. [Google Scholar] [CrossRef]

- Hizarci-Payne, A.K.; Kirkulak-Uludag, B. Sustainable Business Practices of Turkish Companies Listed on the Borsa Istanbul Sustainability Index. In Sustainable Business Models: Principles, Promise, and Practice; Springer: Berlin/Heidelberg, Germany, 2018; pp. 329–344. [Google Scholar]

- Olatubosun, P.; Charles, E.; Omoyele, T. Rethinking luxury brands and sustainable fashion business models in a risk society. J. Des. Bus. Soc. 2021, 7, 49–81. [Google Scholar] [CrossRef]

- Clegg, J. Innovation in a new normal—How can the upstream industry develop new, fit-for-purpose technology? In Proceedings of the Abu Dhabi International Petroleum Exhibition and Conference, Abu Dhabi, United Arab Emirates, 9–12 November 2020. [Google Scholar]

- Serwinowski, M.A.; Marshall, J. The ROI of social responsibility: Driving sustainability in the oil & gas sector. In Proceedings of the SPE International Conference on Health, Safety and Environment in Oil and Gas Exploration and Production, Rio de Janeiro, Brazil, 12–14 April 2010; pp. 2725–2731. [Google Scholar]

- Jasni, N.S.; Yusoff, H.; Zain, M.M.; Yusoff, N.M.; Shaffee, N.S. Business strategy for environmental social governance practices: Evidence from telecommunication companies in Malaysia. Soc. Responsib. J. 2019, 16, 271–289. [Google Scholar] [CrossRef]

- Isaksson, L.E.; Woodside, A.G. Modeling firm heterogeneity in corporate social performance and financial performance. J. Bus. Res. 2016, 69, 3285–3314. [Google Scholar] [CrossRef]

- Maniora, J. Is Integrated Reporting Really the Superior Mechanism for the Integration of Ethics into the Core Business Model? An Empirical Analysis. J. Bus. Ethics 2017, 140, 755–786. [Google Scholar] [CrossRef]

- Brennan, G.; Tennant, M. Sustainable value and trade-offs: Exploring situational logics and power relations in a UK brewery’s malt supply network business model. Bus. Strategy Environ. 2018, 27, 621–630. [Google Scholar] [CrossRef]

- Esty, D.C. Red Lights to Green Lights: From 20th Century Environmental Regulation to 21st Century Sustainability. Environ. Law 2017, 47, 1–80. [Google Scholar] [CrossRef]

- Moliterni, F. Do Global Financial Markets Capitalise Sustainability? Evidence of a Quick Reversal; Working Paper 025.2018; Fondazione Eni Enrico Mattei: Milan, Italy, 2018; Volume 25. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SALSA Framework | Methods Used |

|---|---|

| Search | ESG and business model literature |

| Appraisal | Quality assessment involves examining claims and generalizability of findings. |

| Synthesis | Thematic synthesis: ESG and business model conceptualization |

| Analysis | ESG and business model analysis: Outcome: The impact of ESG on the business model; concepts. Process: Change, shift or transition in the business model, considering ESG factors in their operation. Using MAXQDA software to analyze ESG and business model discussions: Coding based on how each paper represents ESG and business model. |

| Author | Paper Focus | ESG Integration Type | ESG and BM Concept | Literature Discussion of ESG and BM | Interpretation of the Relationship between ESG and BM | |

|---|---|---|---|---|---|---|

| 1 | (Schramade, 2016) | Integration of ESG into valuation models and investment decisions | SRI | Process | Evaluating firms’ ESG performance by linking ESG to BM | Implementation steps |

| 2 | (Corral-Marfil et al., 2021) | Sustainable and circular business model of a bicentennial company | SD | Process | Impact of recycling on BM components (value proposition, value delivery, value creation and value capture) | Transition process |

| 3 | (Camilleri, 2018) | Theoretical reasoning of ESG disclosure and explanation of integrative reporting purpose | SD | Outcome | Firms are expected to communicate BM in IR reporting | Behavior |

| 4 | (Muñoz-Torres et al., 2019) | Whether the rating agency favors BM that promotes a more sustainable development | SD | Outcome | Rating agencies’ sustainability assessment does not support a sustainable BM (holistic integration of ESG) | Behavior |

| 5 | (Di Tullio et al., 2020) | Impact of the European directive on the BM of 46 European firms | SRI | Outcome | Firms’ behavior in addressing ESG in BM: reluctant acceptance, avoidance, and dismissiveness | Behavior |

| 6 | (Hill, 2019) | Problematic BM | SRI | Outcome | The investor’s role inolves holding firms accountable for their reputations when considering their ESG issues in problematic BM. | Behavior |

| 7 | (Hoepner and Schopohl, 2018) | Analysis of investors’ behavior in excluding firms because of their BM | SRI | Outcome | Investors’ behavior in excluding firms because of their BM | Behavior |

| 8 | (La Torre et al., 2021) | ESG performance and financial performance | SRI | Outcome | Recommendation forcing banks to adopt a new ESG BM | Behavior |

| 9 | (Sushchenko, Volkovskyi, Fedosov, and Ryazanova, 2020) | Impact of environmental risks on SD * conditions through Human Development Index and GDP per capita | SD | Outcome | Regulation impacts adoption | Behavior |

| 10 | (Ziolo, Bak, Cheba, and Spoz, 2020) | Impact of banks on enterprise BM | SRI | Outcome | Banks impact firms with ESG in BM | Behavior |

| 11 | (Lee, 2020) | Exploration of the role of green finance in achieving sustainable development goals in China | SRI | Outcome | The transition occurred due to investors and financial institutions | Behavior |

| 12 | (Rezae and Tuo, 2019) | Relationship between quality and quantity of sustainability disclosure and earning quality of corporate value and culture | SD | Outcome | Earning quality | Advantage |

| 13 | (Zubeltzu-Jaka et al., 2018) | Relationship between CSR * and CG * through ESG indicators | SD | Outcome | Necessity of ESG in BM; ESG positively impacts stakeholders and shareholders by improving the transparency, accountability, compliance, and honesty of firm’s practices. | Advantage |

| 14 | (Kluza et al., 2021) | The role and influence of ESG factors in firms building of sustainable business models | SD | Outcome | A positive relationship between innovation and ESG (SBM *) | Advantage |

| 15 | (Cassely, Ben Larbi, Revelli, and Lacroux, 2021) | Impact of 2008 economic crisis on corporate social performance | SD | Outcome | Economic crises cause firms to change their CSR practices and conceptualize their BM as they consider CSR/ESG in their BM to gain legitimacy | Advantage |

| 16 | (Rabaya & Saleh, 2021) | Effect of IR * adoption on the relationship between ESG and firms’ competitive advantage | SD | Outcome | BM integration into IR, strength as a competitive advantage | Advantage |

| 17 | (Herciu, 2018) | Nature of the relationship between sustainability and profitability in BM | SRI | Outcome | Firms that have BM addressing sustainability and ESG are financially profitable | Advantage |

| 18 | (Ashraf, Rizwan, and L’Huillier, 2021) | Micro-financial institution (MFI) integration of ESG | SD | Outcome | High-leverage MFIs and the presence of women on the board of directors contribute positively to ESG integration in firm operations | Advantage |

| 19 | (Sabbaghi, 2011) | Green traded funding impact on cumulative market-wide return | SRI | Outcome | Green traded funding has a positive cumulative market-wide return, and BM has positive ESG characteristics | Advantage |

| 20 | (Turan, Johan, and Omar, 2018) | Systematic sustainability assessment (SSA) to achieve sustainability | SD | Outcome | Long-term continuity and value creation | Advantage |

| 21 | (R. G. Eccles and Serafeim, 2013) | ESG performance and financial performance | SRI and SD | Outcome | BM innovation leads to high ESG performance and high financial performance | Advantage |

| 22 | (Olatubosun et al., 2021) | Examination of fashion business owners and analysis of policy documents demonstrate implementation of technology to achieve circular BM | SD | Outcome | Examination of how ESG issues affect the luxury fashion business | Practices |

| 23 | (Venanzi and Matteucci, 2021) | Sustainability characteristics of a large European cooperative bank | SRI | Outcome | Situation in Europe (stable business model); cooperative bank BM characteristics | Practices |

| 24 | (Clegg, 2020) | Role of innovation in developing technology strategies | SD | Outcome | Innovation in technology to create new BM to address stakeholder needs on ESG issues. | Practices |

| 25 | (Hizarci-Payne and Kirkulak-Uludag, 2018) | Sustainability practices in Turkey by launching BIST, the first sustainability index | SD | Outcome | Turkish firms are addressing sustainability in their business model based on sector type | Practices |

| 26 | (Serwinowski and Marshall, 2010) | Observation of sustainability in the oil and gas industry | SD | Outcome | Business-case frame: environmental and social integration | Practices |

| 27 | (Jasni et al., 2019) | ESG practices in four telecommunication business strategies | SD | Outcome | BM dynamic in coping with economic activities and delivering ESG issues to stakeholders | Practices |

| 28 | (Maniora, 2017) | Effectiveness of using integrative reporting as a tool to integrate ESG into BM | SD | Outcome | IR * only superior mechanism to integrate ESG into BM when compared with other ESG reporting strategies | Critical view |

| 29 | (Isaksson and Woodside, 2016) | Corporate social performance and financial performance | SRI | Outcome | Negative corporate social performance using ESG and negative CFP * | Critical view |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aldowaish, A.; Kokuryo, J.; Almazyad, O.; Goi, H.C. Environmental, Social, and Governance Integration into the Business Model: Literature Review and Research Agenda. Sustainability 2022, 14, 2959. https://doi.org/10.3390/su14052959

Aldowaish A, Kokuryo J, Almazyad O, Goi HC. Environmental, Social, and Governance Integration into the Business Model: Literature Review and Research Agenda. Sustainability. 2022; 14(5):2959. https://doi.org/10.3390/su14052959

Chicago/Turabian StyleAldowaish, Alaa, Jiro Kokuryo, Othman Almazyad, and Hoe Chin Goi. 2022. "Environmental, Social, and Governance Integration into the Business Model: Literature Review and Research Agenda" Sustainability 14, no. 5: 2959. https://doi.org/10.3390/su14052959