Green Supply Chain Management Efforts of First-Tier Suppliers on Economic and Business Performances in the Electronics Industry

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainable Supplier Management and Tier-Dependenct Characteristics

2.2. Green Supply Chain Management

2.3. Economic and Business Performances

2.4. Internal Environmental Management

2.5. Green Purchasing

2.6. Eco-Design

2.7. Cooperation with Customers

3. Hypotheses Development

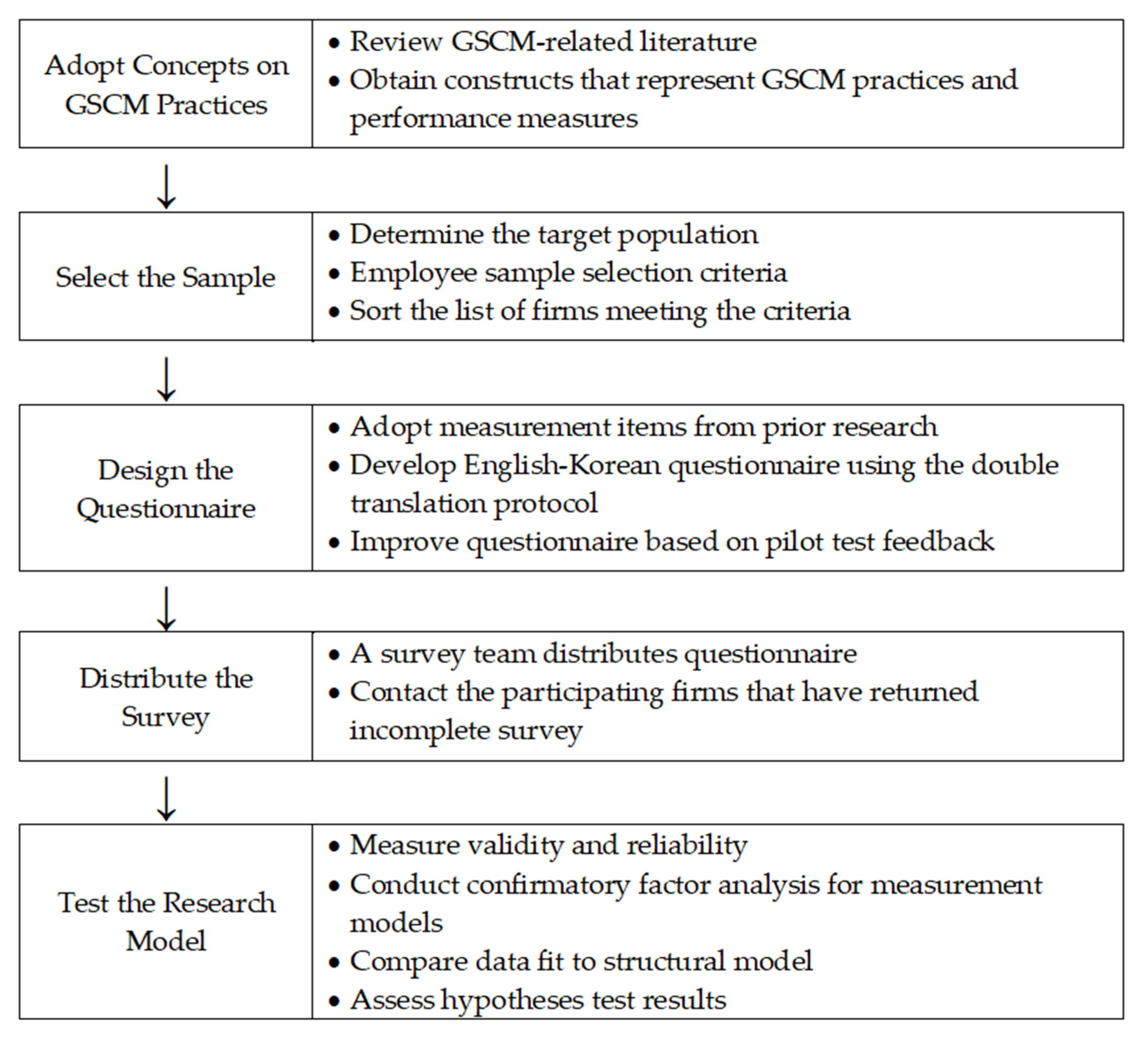

4. Research Methodology

4.1. Description of Data Sources

4.2. Measurement Development

4.3. Data Collection

4.4. Non-Response Bias Analysis

4.5. Measure Assessment

5. Results

5.1. Measurement Model

5.2. Structural Model

6. Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Characteristics | Frequency | % |

|---|---|---|

| A. Respondents’ Job Titles | ||

| Top Executive | 8 | 4.2 |

| Senior Executive | 28 | 14.5 |

| Middle Manager | 138 | 71.5 |

| Employee in Charge | 19 | 9.8 |

| Total | 193 | 100.0 |

| B. Respondents’ Work Experience (years) | ||

| Less than 5 | 50 | 25.9 |

| 5–10 | 76 | 39.4 |

| 11–15 | 52 | 26.9 |

| More than 15 | 15 | 7.8 |

| Total | 193 | 100.0 |

| C. Firm Size (# of employees) | ||

| 50–200 | 118 | 61.1 |

| 201–400 | 49 | 25.4 |

| 401–500 | 26 | 13.5 |

| Total | 193 | 100.0 |

| D. Industry Classification of the Customer Firms (multiple answers) | ||

| Electronics | 193 | |

| Telecommunication | 7 | |

| Automobile | 2 |

References

- Bowcott, H.; Pacthod, D.; Pinner, D. What COP26 Means for Business|McKinsey. Available online: https://www.mckinsey.com/business-functions/sustainability/our-insights/cop26-made-net-zero-a-core-principle-for-business-heres-how-leaders-can-act (accessed on 27 November 2021).

- Aboelmaged, M.; Hashem, G. Absorptive capacity and green innovation adoption in SMEs: The mediating effects of sustainable organisational capabilities. J. Clean. Prod. 2019, 220, 853–863. [Google Scholar] [CrossRef]

- Tuni, A.; Rentizelas, A. An innovative eco-intensity based method for assessing extended supply chain environmental sustainability. Int. J. Prod. Econ. 2019, 217, 126–142. [Google Scholar] [CrossRef] [Green Version]

- Dewan, A.; Cassidy, A.; Formanek, I.; Kottasová, I. COP26 Climate Deal Includes Historic Reference to Fossil Fuels but Doesn’t Meet Urgency of the Crisis. Available online: https://www.cnn.com/2021/11/13/world/cop26-agreement-final-climate-intl/index.html (accessed on 3 December 2021).

- Escaler, G. Council Post: Transforming Sustainability into a Competitive Advantage. Available online: https://www.forbes.com/sites/forbescommunicationscouncil/2020/09/09/transforming-sustainability-into-a-competitive-advantage/ (accessed on 3 December 2021).

- UN Environment Programme. What You Need to Know about the COP26 UN Climate Change Conference. Available online: http://www.unep.org/news-and-stories/story/what-you-need-know-about-cop26-un-climate-change-conference (accessed on 30 November 2021).

- Doshi, S.; Levy, C.; Powis, D.; Stephens, D. Aligning Portfolios with Climate Goals: A New Approach for Financial Institutions|McKinsey. Available online: https://www.mckinsey.com/business-functions/risk-and-resilience/our-insights/aligning-portfolios-with-climate-goals-a-new-approach-for-financial-institutions (accessed on 27 November 2021).

- Broughton, K.; Maurer, M. Companies Push Suppliers to Disclose More Climate Data. Available online: https://www.wsj.com/articles/companies-push-suppliers-to-disclose-more-climate-data-11637145001?page=1 (accessed on 27 November 2021).

- Kim, S.; Foerstl, K.; Schmidt, C.G.; Wagner, S.M. Adoption of green supply chain management practices in multi-tier supply chains: Examining the differences between higher and lower tier firms. Int. J. Prod. Res. 2021, 1–18. [Google Scholar] [CrossRef]

- Liu, J.; Feng, Y.; Zhu, Q. Involving second-tier suppliers in Green supply chain management: Drivers and heterogenous understandings by firms along supply chains. Int. J. Prod. Res. 2021, 1–21. [Google Scholar] [CrossRef]

- Brandenburg, M.; Govindan, K.; Sarkis, J.; Seuring, S. Quantitative models for sustainable supply chain management: Developments and directions. Eur. J. Oper. Res. 2014, 233, 299–312. [Google Scholar] [CrossRef]

- Martin, C.; Dent, M. How Big Business Turns a Profit on Environmentalism. Available online: https://www.fleetowner.com/emissions-efficiency/article/21704282/how-big-business-turns-a-profit-on-environmentalism (accessed on 22 October 2021).

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental Management in SMEs in the UK: Practices, Pressures and Perceived Benefits: Environmental Management in SMEs. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Li, J.J.; Zhou, N.; Su, C. Market orientation, job satisfaction, product quality, and firm performance: Evidence from China. Strat. Manag. J. 2008, 29, 985–1000. [Google Scholar] [CrossRef]

- Berning, A.; Venter, C. Sustainable Supply Chain Engagement in a Retail Environment. Sustainability 2015, 7, 6246–6263. [Google Scholar] [CrossRef] [Green Version]

- Park, S.R.; Jang, J.Y. The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria. Int. J. Financ. Stud. 2021, 9, 48. [Google Scholar] [CrossRef]

- Oh, K.-S.; Han, J.R.; Park, S.R. The Influence of Hotel Employees’ Perception of CSR on Organizational Commitment: The Moderating Role of Job Level. Sustainability 2021, 13, 12625. [Google Scholar] [CrossRef]

- Fathollahi-Fard, A.M.; Dulebenets, M.A.; Hajiaghaei–Keshteli, M.; Tavakkoli-Moghaddam, R.; Safaeian, M.; Mirzahosseinian, H. Two hybrid meta-heuristic algorithms for a dual-channel closed-loop supply chain network design problem in the tire industry under uncertainty. Adv. Eng. Inform. 2021, 50, 101418. [Google Scholar] [CrossRef]

- Fallahpour, A.; Wong, K.Y.; Rajoo, S.; Fathollahi-Fard, A.M.; Antucheviciene, J.; Nayeri, S. An integrated approach for a sustainable supplier selection based on Industry 4.0 concept. Environ. Sci. Pollut. Res. 2021, 1–19. [Google Scholar] [CrossRef]

- Fallahpour, A.; Olugu, E.U.; Musa, S.N.; Khezrimotlagh, D.; Wong, K.Y. An integrated model for green supplier selection under fuzzy environment: Application of data envelopment analysis and genetic programming approach. Neural Comput. Appl. 2016, 27, 707–725. [Google Scholar] [CrossRef]

- Tong, L.Z.; Wang, J.; Pu, Z. Sustainable supplier selection for SMEs based on an extended PROMETHEE II approach. J. Clean. Prod. 2022, 330, 129830. [Google Scholar] [CrossRef]

- Mojtahedi, M.; Fathollahi-Fard, A.M.; Tavakkoli-Moghaddam, R.; Newton, S. Sustainable vehicle routing problem for coordinated solid waste management. J. Ind. Inf. Integr. 2021, 23, 100220. [Google Scholar] [CrossRef]

- Fathollahi-Fard, A.M.; Hajiaghaei-Keshteli, M.; Tavakkoli-Moghaddam, R.; Smith, N.R. Bi-level programming for home health care supply chain considering outsourcing. J. Ind. Inf. Integr. 2022, 25, 100246. [Google Scholar] [CrossRef]

- Awaysheh, A.; Klassen, R.D. The impact of supply chain structure on the use of supplier socially responsible practices. Int. J. Oper. Prod. Manag. 2010, 30, 1246–1268. [Google Scholar] [CrossRef]

- Touboulic, A.; Walker, H. Theories in sustainable supply chain management: A structured literature review. Int. J. Phys. Distrib. Logist. Manag. 2015, 45, 16–42. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainable supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

- Mamic, I. Managing Global Supply Chain: The Sports Footwear, Apparel and Retail Sectors. J. Bus. Ethics 2005, 59, 81–100. [Google Scholar] [CrossRef]

- Ageron, B.; Gunasekaran, A.; Spalanzani, A. Sustainable supply management: An empirical study. Int. J. Prod. Econ. 2012, 140, 168–182. [Google Scholar] [CrossRef]

- Yang, F.; Zhang, X. The impact of sustainable supplier management practices on buyer-supplier performance: An Empirical Study in China. Rev. Int. Bus. Strategy 2017, 27, 112–132. [Google Scholar] [CrossRef]

- Kristal, M.M.; Pagell, M.; Yang, C.; Sheu, C. Are supply chain management theories culturally constrained? An empirical assessment. Oper. Manag. Res. 2011, 4, 61–73. [Google Scholar] [CrossRef]

- Sarkis, J.; Zhu, Q.; Lai, K.-H. An organizational theoretic review of green supply chain management literature. Int. J. Prod. Econ. 2011, 130, 1–15. [Google Scholar] [CrossRef]

- Srivastava, S.K. Green supply-chain management: A state-of-the-art literature review. Int. J. Manag. Rev. 2007, 9, 53–80. [Google Scholar] [CrossRef]

- Petljak, K.; Zulauf, K.; Štulec, I.; Seuring, S.; Wagner, R. Green supply chain management in food retailing: Survey-based evidence in Croatia. Supply Chain Manag. Int. J. 2018, 23, 1–15. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Confirmation of a measurement model for green supply chain management practices implementation. Int. J. Prod. Econ. 2008, 111, 261–273. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between operational practices and performance among early adopters of green supply chain management practices in Chinese manufacturing enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Lee, C.; Lim, S.; Ha, B. Green Supply Chain Management and Its Impact on Consumer Purchase Decision as a Marketing Strategy: Applying the Theory of Planned Behavior. Sustainabilty 2021, 13, 10971. [Google Scholar] [CrossRef]

- Zaid, A.A.; Jaaron, A.A.M.; Bon, A.T. The impact of green human resource management and green supply chain management practices on sustainable performance: An empirical study. J. Clean. Prod. 2018, 204, 965–979. [Google Scholar] [CrossRef]

- Green, K.W., Jr.; Zelbst, P.J.; Meacham, J.; Bhadauria, V.S. Green supply chain management practices: Impact on performance. Supply Chain Manag. Int. J. 2012, 17, 290–305. [Google Scholar] [CrossRef]

- Brynjolfsson, E. The productivity paradox of information technology. Commun. ACM 1993, 36, 66–77. [Google Scholar] [CrossRef]

- Dieppe, A. Global Productivity: Trends, Drivers, and Policies; The World Bank: Washington, DC, USA, 2021; ISBN 978-1-4648-1608-6. [Google Scholar]

- Hervani, A.A.; Helms, M.M.; Sarkis, J. Performance measurement for green supply chain management. Benchmark. Int. J. 2005, 12, 330–353. [Google Scholar] [CrossRef] [Green Version]

- Green, K.W.; Inman, R.A. Using a just-in-time selling strategy to strengthen supply chain linkages. Int. J. Prod. Res. 2005, 43, 3437–3453. [Google Scholar] [CrossRef]

- Richard, P.J.; Devinney, T.M.; Yip, G.S.; Johnson, G. Measuring Organizational Performance: Towards Methodological Best Practice. J. Manag. 2009, 35, 718–804. [Google Scholar] [CrossRef] [Green Version]

- Sharma, E.; Singla, J. Sustainable Supply Chain Practices (SSCPs) and Organizational Performance: A Mediating Role of Functional Constructs. Oper. Supply Chain Manag. Int. J. 2021, 14, 456–466. [Google Scholar] [CrossRef]

- Um, J. The impact of supply chain agility on business performance in a high level customization environment. Oper. Manag. Res. 2017, 10, 10–19. [Google Scholar] [CrossRef]

- Williams, S.; Schaefer, A. Small and Medium-Sized Enterprises and Sustainability: Managers’ Values and Engagement with Environmental and Climate Change Issues: SMEs and Sustainability-Managers’ Values and Engagement. Bus. Strategy Environ. 2013, 22, 173–186. [Google Scholar] [CrossRef] [Green Version]

- del Brío, J.Á.; Junquera, B. A review of the literature on environmental innovation management in SMEs: Implications for public policies. Technovation 2003, 23, 939–948. [Google Scholar] [CrossRef]

- Kim, S.T.; Lee, H.-H.; Lim, S. The Effects of Green SCM Implementation on Business Performance in SMEs: A Longitudinal Study in Electronics Industry. Sustainability 2021, 13, 11874. [Google Scholar] [CrossRef]

- Simpson, M.; Taylor, N.; Barker, K. Environmental responsibility in SMEs: Does it deliver competitive advantage? Bus. Strategy Environ. 2004, 13, 156–171. [Google Scholar] [CrossRef]

- Xu, Y.; Boh, W.F.; Luo, C.; Zheng, H. Leveraging industry standards to improve the environmental sustainability of a supply chain. Electron. Commer. Res. Appl. 2018, 27, 90–105. [Google Scholar] [CrossRef]

- Jolink, A.; Niesten, E. Sustainable Development and Business Models of Entrepreneurs in the Organic Food Industry: Sustainable Development and Business Models of Entrepreneurs. Bus. Strategy Environ. 2015, 24, 386–401. [Google Scholar] [CrossRef]

- Ljungkvist, T.; Andersén, J. A taxonomy of ecopreneurship in small manufacturing firms: A multidimensional cluster analysis. Bus. Strategy Environ. 2021, 30, 1374–1388. [Google Scholar] [CrossRef]

- de Giovanni, P. Do internal and external environmental management contribute to the triple bottom line? Int. J. Oper. Prod. Manag. 2012, 32, 265–290. [Google Scholar] [CrossRef]

- Aslam, M.M.H.; Waseem, M.; Khurram, M. Impact of Green Supply Chain Management Practices on Corporate Image: Mediating Role of Green Communications. Pak. J. Commer. Soc. Sci. 2019, 13, 581–598. [Google Scholar]

- Eva, N.; Newman, A.; Zhou, A.J.; Zhou, S.S. The relationship between ethical leadership and employees’ internal and external community citizenship behaviors: The Mediating Role of Prosocial Motivation. Pers. Rev. 2019, 49, 636–652. [Google Scholar] [CrossRef]

- Schwepker, C.H., Jr. Ethical climate’s relationship to job satisfaction, organizational commitment, and turnover intention in the salesforce. J. Bus. Res. 2001, 54, 39–52. [Google Scholar] [CrossRef]

- Krause, D.R.; Vachon, S.; Klassen, R.D. Special topic forum on sustainable supply chain management: Introduction and reflections on the role of purchasing management. J. Supply Chain Manag. 2009, 45, 18–25. [Google Scholar] [CrossRef]

- Blome, C.; Paulraj, A. Ethical Climate and Purchasing Social Responsibility: A Benevolence Focus. J. Bus. Ethics 2013, 116, 567–585. [Google Scholar] [CrossRef]

- Min, H.; Galle, W.P. Green Purchasing Strategies: Trends and Implications. Int. J. Purch. Mater. Manag. 1997, 33, 10–17. [Google Scholar] [CrossRef]

- Blome, C.; Hollos, D.; Paulraj, A. Green procurement and green supplier development: Antecedents and effects on supplier performance. Int. J. Prod. Res. 2014, 52, 32–49. [Google Scholar] [CrossRef]

- Laari, S.; Töyli, J.; Solakivi, T.; Ojala, L. Firm performance and customer-driven green supply chain management. J. Clean. Prod. 2016, 112, 1960–1970. [Google Scholar] [CrossRef]

- Evans, S.; Partidário, P.J.; Lambert, J. Industrialization as a key element of sustainable product-service solutions. Int. J. Prod. Res. 2007, 45, 4225–4246. [Google Scholar] [CrossRef]

- McDonough, W.; Braungart, M. Cradle to Cradle: Remaking the Way We Make Things, 1st ed.; North Point Press: New York, NY, USA, 2002; ISBN 9780865475878. [Google Scholar]

- McDermaid, D. What Is Design to Cost? An Overview with Examples. Available online: https://www.apriori.com/blog/what-is-design-to-cost-an-overview-with-examples/ (accessed on 29 October 2021).

- Santolaria, M.; Oliver-Solà, J.; Gasol, C.M.; Morales-Pinzón, T.; Rieradevall, J. Eco-design in innovation driven companies: Perception, predictions and the main drivers of integration. The Spanish example. J. Clean. Prod. 2011, 19, 1315–1323. [Google Scholar] [CrossRef]

- Rocha, C.S.; Antunes, P.; Partidário, P. Design for sustainability models: A multiperspective review. J. Clean. Prod. 2019, 234, 1428–1445. [Google Scholar] [CrossRef] [Green Version]

- Martínez-Cámara, E.; Santamaría, J.; Sanz-Adán, F.; Arancón, D. Digital Eco-Design and Life Cycle Assessment—Key Elements in a Circular Economy: A Case Study of a Conventional Desk. Appl. Sci. 2021, 11, 10439. [Google Scholar] [CrossRef]

- Montecchi, T.; Becattini, N. Design for sustainable behavior: Opportunities and challenges of a data-driven approach. In Proceedings of the Design Society: DESIGN Conference; Cambridge University Press: Cambridge, UK, 2020; Volume 1, pp. 2089–2098. [Google Scholar] [CrossRef]

- Balikci, A.; Borgianni, Y.; Maccioni, L.; Nezzi, C. A Framework of Unsustainable Behaviors to Support Product Eco-Design. Sustainability 2021, 13, 11394. [Google Scholar] [CrossRef]

- Bask, A.; Rajahonka, M.; Laari, S.; Solakivi, T.; Töyli, J.; Ojala, L. Environmental sustainability in shipper-LSP relationships. J. Clean. Prod. 2018, 172, 2986–2998. [Google Scholar] [CrossRef]

- Saeed, A.; Jun, Y.; Nubuor, S.A.; Priyankara, H.P.R.; Jayasuriya, M.P.F. Institutional Pressures, Green Supply Chain Management Practices on Environmental and Economic Performance: A Two Theory View. Sustainability 2018, 10, 1517. [Google Scholar] [CrossRef] [Green Version]

- Khan, S.A.R.; Yu, Z. Assessing the eco-environmental performance: An PLS-SEM approach with practice-based view. Int. J. Logist. Res. Appl. 2021, 24, 303–321. [Google Scholar] [CrossRef]

- Saranga, H.; Moser, R. Performance evaluation of purchasing and supply management using value chain DEA approach. Eur. J. Oper. Res. 2010, 207, 197–205. [Google Scholar] [CrossRef]

- Chen, C.-C. Incorporating green purchasing into the frame of ISO 14000. J. Clean. Prod. 2005, 13, 927–933. [Google Scholar] [CrossRef]

- Chien, S.-H.; Chen, J.-J. Supplier involvement and customer involvement effect on new product development success in the financial service industry. Serv. Ind. J. 2010, 30, 185–201. [Google Scholar] [CrossRef]

- Lin, C.-Y.; Lee, A.H.; Kang, H.-Y. An integrated new product development framework–An application on green and low-carbon products. Int. J. Syst. Sci. 2015, 46, 733–753. [Google Scholar] [CrossRef]

- Chan, R.Y.K.; He, H.; Chan, H.K.; Wang, W.Y.C. Environmental orientation and corporate performance: The mediation mechanism of green supply chain management and moderating effect of competitive intensity. Ind. Mark. Manag. 2012, 41, 621–630. [Google Scholar] [CrossRef]

- Luo, J.; Chong, A.Y.-L.; Ngai, E.W.T.; Liu, M.J. Green Supply Chain Collaboration implementation in China: The mediating role of guanxi. Transp. Res. Part E Logist. Transp. Rev. 2014, 71, 98–110. [Google Scholar] [CrossRef]

- Guo, Y.; Yen, D.A.; Geng, R.; Azar, G. Drivers of green cooperation between Chinese manufacturers and their customers: An empirical analysis. Ind. Mark. Manag. 2021, 93, 137–146. [Google Scholar] [CrossRef]

- Theyel, G. Customer and Supplier Relations for Environmental Performance. In Greening the Supply Chain; Sarkis, J., Ed.; Springer: London, UK, 2006; pp. 139–149. ISBN 978-1-84628-298-0. [Google Scholar]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Examining the effects of green supply chain management practices and their mediations on performance improvements. Int. J. Prod. Res. 2012, 50, 1377–1394. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Institutional-based antecedents and performance outcomes of internal and external green supply chain management practices. J. Purch. Supply Manag. 2013, 19, 106–117. [Google Scholar] [CrossRef]

- Melander, L. Customer and Supplier Collaboration in Green Product Innovation: External and Internal Capabilities: Customer and Supplier Collaboration in Green Product Innovation. Bus. Strategy Environ. 2018, 27, 677–693. [Google Scholar] [CrossRef]

- Iranmanesh, M.; Fayezi, S.; Hanim, S.; Hyun, S.S. Drivers and outcomes of eco-design initiatives: A cross-country study of Malaysia and Australia. Rev. Manag. Sci. 2019, 13, 1121–1142. [Google Scholar] [CrossRef]

- Diabat, A.; Khodaverdi, R.; Olfat, L. An exploration of green supply chain practices and performances in an automotive industry. Int. J. Adv. Manuf. Technol. 2013, 68, 949–961. [Google Scholar] [CrossRef]

- Azzaro-Pantel, C.; Madoumier, M.; Gésan-Guiziou, G. Development of an ecodesign framework for food manufacturing including process flowsheeting and multiple-criteria decision-making: Application to milk evaporation. Food Bioprod. Process. 2022, 131, 40–59. [Google Scholar] [CrossRef]

- Chen, J.; Huang, S.; BalaMurugan, S.; Tamizharasi, G.S. Artificial intelligence based e-waste management for environmental planning. Environ. Impact Assess. Rev. 2021, 87, 106498. [Google Scholar] [CrossRef]

- Klos, Z.S.; Kalkowska, J.; Kasprzak, J. Towards a Sustainable Future-Life Cycle Management: Challenges and Prospects, 1st ed.; Springer: Cham, Switzerland, 2021; ISBN 978-3-030-77129-4. [Google Scholar]

- Kondoh, S.; Mishima, N. Proposal of an Integrated Eco-Design Framework of Products and Processes. In Glocalized Solutions for Sustainability in Manufacturing; Hesselbach, J., Herrmann, C., Eds.; Springer: Berlin/Heidelberg, Germany, 2011; pp. 113–117. ISBN 978-3-642-19691-1. [Google Scholar]

- Bae, J.; Insead, M.G. Partner Substitutability, Alliance Network Structure, and Firm Profitability in the Telecommunications Industry. Acad. Manag. J. 2017, 47, 843–859. [Google Scholar] [CrossRef]

- Masa’deh, R.; Alananzeh, O.; Algiatheen, N.; Ryati, R.; Albayyari, R.; Tarhini, A. The impact of employee’s perception of implementing green supply chain management on hotel’s economic and operational performance. J. Hosp. Tour. Technol. 2017, 8, 395–416. [Google Scholar] [CrossRef]

- Shearlock, C.; Hooper, P.; Steve, M. Environmental Improvement in Small and Medium-Sized Enterprises. Greener Manag. Int. 2000, 2000, 50–60. [Google Scholar] [CrossRef]

- Sarkis, J.; Dijkshoorn, J. Relationships between solid waste management performance and environmental practice adoption in Welsh small and medium-sized enterprises (SMEs). Int. J. Prod. Res. 2007, 45, 4989–5015. [Google Scholar] [CrossRef]

- Lee, S.-Y.; Klassen, R.D. Drivers and Enablers That Foster Environmental Management Capabilities in Small- and Medium-Sized Suppliers in Supply Chains. Prod. Oper. Manag. 2008, 17, 573–586. [Google Scholar] [CrossRef]

- Hu, L.-T.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Kline, R.B. Principles and Practice of Structural Equation Modeling, 4th ed.; The Guilford Press: New York, NY, USA, 2015; ISBN 978-1-60623-877-6. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Nunnally, J.C.; Bernstein, I.H. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994; ISBN 9780070478497. [Google Scholar]

- Landy, H. A Wall Street Powerhouse Is Finally Matching Its Climate-Change Rhetoric with Action. Available online: https://qz.com/1784949/blackrock-ceo-larry-finks-2020-letter-backs-up-climate-rhetoric-with-action/ (accessed on 22 October 2021).

- O’Donnell, G. Climate Tech: How ESG Investing Is Evolving into ‘a Profitable Endeavor’. Available online: https://news.yahoo.com/climate-tech-esg-investing-profitable-endeavor-191604271.html (accessed on 22 October 2021).

- Waldman, D.A.; Siegel, D.S.; Javidan, M. Components of CEO Transformational Leadership and Corporate Social Responsibility. J. Manag. Stud. 2006, 43, 1703–1725. [Google Scholar] [CrossRef]

- Velte, P. Does CEO power moderate the link between ESG performance and financial performance?: A Focus on the German Two-Tier System. Manag. Res. Rev. 2019, 43, 497–520. [Google Scholar] [CrossRef]

- Nilashi, M.; Minaei-Bidgoli, B.; Alrizq, M.; Alghamdi, A.; Alsulami, A.A.; Samad, S.; Mohd, S. An analytical approach for big social data analysis for customer decision-making in eco-friendly hotels. Expert Syst. Appl. 2021, 186, 115722. [Google Scholar] [CrossRef]

- Yang, Q.; Yu, S.; Jiang, D. A modular method of developing an eco-product family considering the reusability and recyclability of customer products. J. Clean. Prod. 2014, 64, 254–265. [Google Scholar] [CrossRef]

- Domingo, L.; Buckingham, M.; Dekoninck, E.; Cornwell, H. The importance of understanding the business context when planning eco-design activities. J. Ind. Prod. Eng. 2015, 32, 3–11. [Google Scholar] [CrossRef]

- Li, S.; Ragu-Nathan, B.; Ragu-Nathan, T.; Rao, S.S. The impact of supply chain management practices on competitive advantage and organizational performance. Omega 2006, 34, 107–124. [Google Scholar] [CrossRef]

- Singh, R.K.; Garg, S.K.; Deshmukh, S.G. The competitiveness of SMEs in a globalized economy: Observations from China and India. Manag. Res. Rev. 2009, 33, 54–65. [Google Scholar] [CrossRef]

- Junaid, M.; Zhang, Q.; Syed, M.W. Effects of Sustainable Supply Chain Integration on Green Innovation and Firm Performance. Sustain. Prod. Consum. 2022, 30, 145–157. [Google Scholar] [CrossRef]

- Kim, S.-C.; Kim, H.-Y. A Study of the Impacts of Buyer-Supplier Partnership on the SCM Performance in Electronics Industry. J. Korean Soc. Supply Chain. Manag. 2008, 8, 1–14. [Google Scholar]

| Construct | Operational Definition | References |

|---|---|---|

| Internal Environmental Management (IEM) | A set of management activities involved with evolving environmental sustainability as a fundamental organizational goal through support and commitment of mid-level and senior managers. | Aslam et al. [54] |

| Green Purchasing (GP) | Corporate efforts in minimizing negative externalities impacting environment in the selection and process of acquiring products and services required for the operation of the business. | Min and Galle [59] |

| Cooperation with Customers (CC) | Cooperation with customer requires working with customers to design cleaner production processes that produce environmentally. | Green et al. [38]; Zhu et al. [34] |

| Eco-design (ECO) | Designing of a product so as to minimize the environmental impact of the product during the entire life of the products. | Aslam et al. [54] |

| Economic Performance (EP) | Economic performance related to the manufacturing plant’s ability to reduce costs associated with purchased materials, energy consumption, waste treatment, waste discharge, and fines for environmental accidents. | Green et al. [38]; Zhu et al. [34] |

| Business Performance (BP) | Firm’s financial and marketing performance reflecting the firm’s green practices. | Um [45]; Green and Inman [42] |

| Constructs and Measurement Items | Mean | S.D. | Factor Loading | t-Value | Reliability and Validity | |

|---|---|---|---|---|---|---|

| Internal Environmental Management | α = 0.857; CR = 0.888; | |||||

| IEM1 | In our firm, environmental management systems exist | 4.13 | 0.739 | 0.739 | 18.752 | AVE = 0.541 |

| IEM2 | Our firm keeps environmental compliance and auditing programs | 4.47 | 0.606 | 0.767 | 21.451 | |

| IEM3 | Our firm maintains cross-functional cooperation for environmental improvements | 4.27 | 0.766 | 0.730 | 18.425 | |

| IEM4 | Senior managers show commitment of GSCM | 4.44 | 0.701 | 0.819 | 27.236 | |

| IEM5 | Mid-level managers support GSCM | 4.55 | 0.598 | 0.858 | 29.145 | |

| Green Purchasing | α = 0.882; CR = 0.879; | |||||

| GP1 | Environmental audit for suppliers’ internal management | 4.47 | 0.770 | 0.764 | 21.013 | AVE = 0.647 |

| GP2 | Suppliers’ ISO 14,001 certification | 4.50 | 0.793 | 0.734 | 18.719 | |

| GP3 | Eco-labeling of our products | 4.49 | 0.740 | 0.827 | 28.725 | |

| GP4 | Cooperation with suppliers for environmental objectives | 4.50 | 0.753 | 0.885 | 37.444 | |

| Cooperation with Customers | α = 0.894; CR = 0.909; | |||||

| CC1 | Cooperation with customers for eco-design | 4.45 | 0.831 | 0.716 | 18.720 | AVE = 0.717 |

| CC2 | Cooperation with customers for cleaner production | 4.49 | 0.764 | 0.893 | 45.892 | |

| CC3 | Cooperation with customers for green packaging | 4.51 | 0.782 | 0.869 | 39.752 | |

| CC4 | Cooperation with customers for developing environmental database of products | 4.46 | 0.775 | 0.896 | 47.210 | |

| Eco-design | α = 0.774; CR = 0.857; | |||||

| ECO1 | Design of products for reduced consumption of material/energy is important | 4.54 | 0.847 | 0.755 | 18.815 | AVE = 0.546 |

| ECO2 | Design for Disassembly (DFD) is important | 4.11 | 0.999 | 0.700 | 15.575 | |

| ECO3 | Design of products for reuse/recycle is important | 4.21 | 0.971 | 0.623 | 11.852 | |

| ECO4 | Design of products to avoid use of hazardous products and/or their manufacturing process is important | 4.62 | 0.760 | 0.665 | 13.986 | |

| ECO5 | In the design of products, life cycle assessment (LCA) is important | 4.30 | 0.909 | 0.848 | 25.254 | |

| Economic Performance | α = 0.854; CR = 0.950; | |||||

| ECP1 | Decrease in cost for materials purchasing | 3.79 | 0.946 | 0.838 | 36.938 | AVE = 0.828 |

| ECP2 | Decrease in cost for energy consumption | 4.11 | 0.858 | 0.974 | 154.256 | |

| ECP3 | Decrease in fee for waste treatment | 4.10 | 0.913 | 0.969 | 144.688 | |

| ECP4 | Decrease in fine for environmental accidents | 4.35 | 0.872 | 0.850 | 39.855 | |

| Business Performance | α = 0.921; CR = 0.945; | |||||

| BP1 | Better asset utilization | 4.00 | 0.888 | 0.788 | 26.316 | AVE = 0.699 |

| BP2 | Stronger competitive position | 4.21 | 0.840 | 0.789 | 26.551 | |

| BP3 | Improved profitability | 4.00 | 0.872 | 0.941 | 75.753 | |

| BP4 | Overall improved organizational performance | 4.02 | 0.859 | 0.929 | 68.747 | |

| Construct | IEM | GP | CC | ECO | ECP | BP |

|---|---|---|---|---|---|---|

| IEM | 0.736 | |||||

| GP | 0.335 | 0.804 | ||||

| CC | 0.287 | 0.635 | 0.847 | |||

| ECO | 0.200 | 0.247 | 0.293 | 0.739 | ||

| ECP | 0.230 | 0.243 | 0.316 | 0.330 | 0.910 | |

| BP | 0.360 | 0.480 | 0.363 | 0.338 | 0.710 | 0.836 |

| Construct | IEM | GP | CC | ECO | ECP | BP |

|---|---|---|---|---|---|---|

| IEM1 | 0.665 | 0.064 | −0.002 | 0.078 | 0.192 | 0.078 |

| IEM2 | 0.751 | 0.077 | 0.059 | 0.032 | 0.069 | 0.032 |

| IEM3 | 0.778 | 0.161 | 0.150 | 0.124 | 0.050 | 0.161 |

| IEM4 | 0.819 | 0.196 | −0.028 | 0.050 | 0.132 | 0.197 |

| IEM5 | 0.824 | 0.094 | 0.119 | 0.108 | 0.048 | 0.108 |

| GP1 | 0.380 | 0.717 | 0.104 | 0.169 | 0.039 | 0.104 |

| GP2 | 0.398 | 0.711 | 0.036 | 0.036 | 0.122 | 0.036 |

| GP3 | 0.152 | 0.820 | 0.130 | 0.182 | 0.122 | 0.152 |

| GP4 | 0.284 | 0.814 | 0.114 | 0.194 | 0.100 | 0.115 |

| CC1 | 0.206 | 0.138 | 0.708 | 0.215 | 0.184 | 0.207 |

| CC2 | 0.206 | 0.106 | 0.851 | 0.220 | 0.121 | 0.107 |

| CC3 | 0.122 | 0.077 | 0.806 | 0.370 | 0.038 | 0.077 |

| CC4 | 0.108 | 0.107 | 0.867 | 0.245 | 0.126 | 0.107 |

| ECO1 | 0.106 | 0.003 | 0.049 | 0.804 | 0.048 | 0.106 |

| ECO2 | 0.110 | 0.107 | 0.047 | 0.815 | 0.029 | 0.110 |

| ECO3 | 0.183 | 0.118 | 0.124 | 0.751 | −0.064 | 0.124 |

| ECO4 | 0.119 | −0.026 | 0.119 | 0.699 | 0.170 | 0.120 |

| ECO5 | 0.193 | 0.106 | 0.086 | 0.786 | 0.170 | 0.087 |

| ECP1 | −0.030 | 0.212 | 0.139 | −0.115 | 0.790 | 0.139 |

| ECP2 | 0.058 | 0.137 | 0.074 | 0.106 | 0.836 | 0.074 |

| ECP3 | 0.060 | 0.117 | 0.038 | 0.058 | 0.813 | 0.061 |

| ECP4 | 0.065 | 0.019 | 0.029 | 0.322 | 0.666 | 0.029 |

| BP1 | 0.160 | 0.165 | 0.069 | 0.029 | 0.158 | 0.787 |

| BP2 | 0.261 | 0.019 | 0.186 | 0.174 | 0.019 | 0.711 |

| BP3 | 0.140 | 0.125 | 0.166 | −0.030 | 0.138 | 0.858 |

| BP4 | 0.163 | 0.170 | 0.131 | 0.093 | 0.168 | 0.830 |

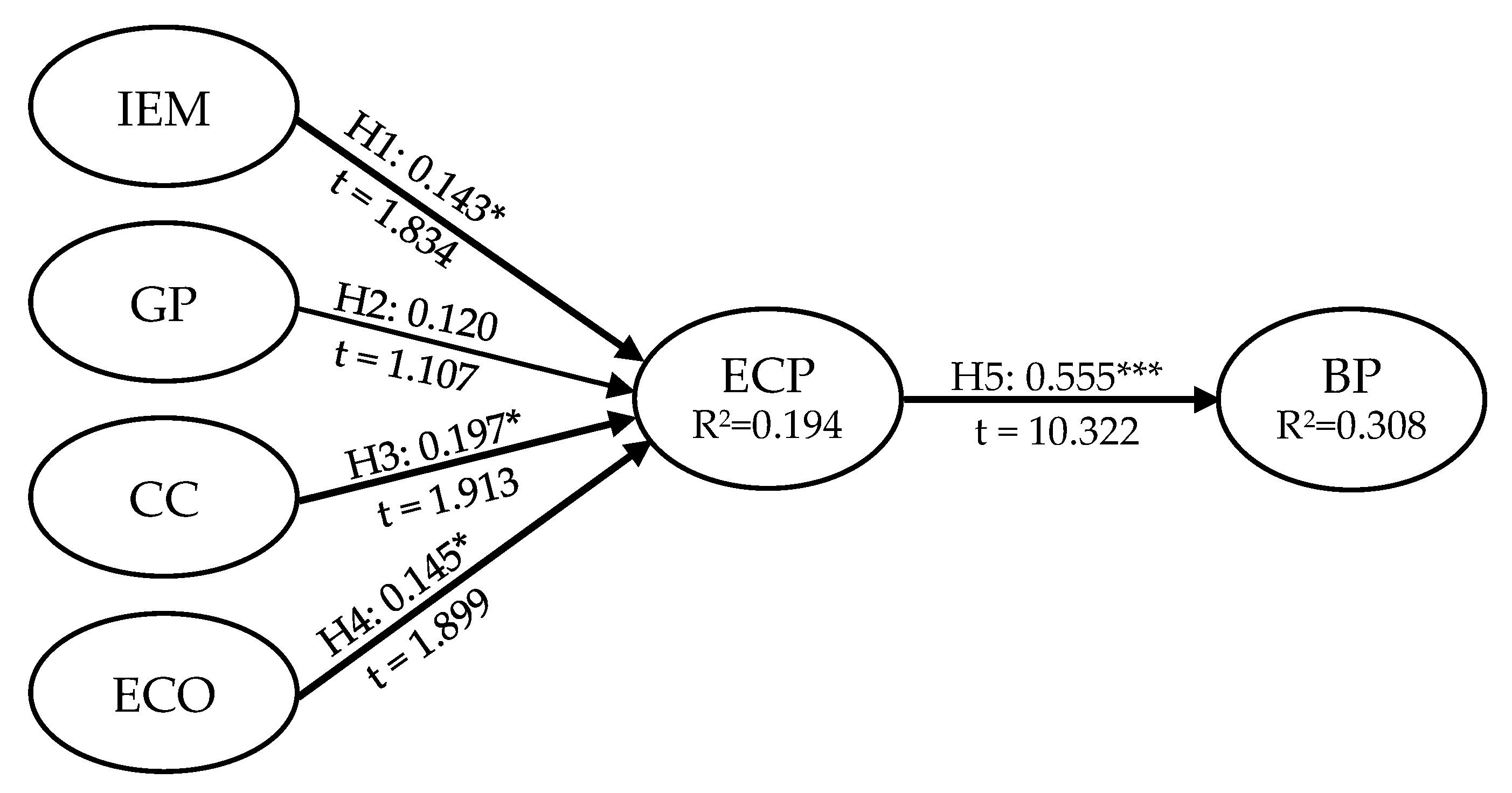

| Hypotheses | Standardized Coefficient (t-Value) | Results | |

|---|---|---|---|

| H1 | Internal Environmental Management → Economic Performance | 0.143 (1.834) * | Supported |

| H2 | Green Purchasing → Economic Performance | 0.120 (1.107) | Not Supported |

| H3 | Cooperation with Customer → Economic Performance | 0.197 (1.913) * | Supported |

| H4 | Eco-design → Economic Performance | 0.145 (1.899) * | Supported |

| H5 | Economic Performance → Business Performance | 0.555 (10.322) *** | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, S.R.; Kim, S.T.; Lee, H.-H. Green Supply Chain Management Efforts of First-Tier Suppliers on Economic and Business Performances in the Electronics Industry. Sustainability 2022, 14, 1836. https://doi.org/10.3390/su14031836

Park SR, Kim ST, Lee H-H. Green Supply Chain Management Efforts of First-Tier Suppliers on Economic and Business Performances in the Electronics Industry. Sustainability. 2022; 14(3):1836. https://doi.org/10.3390/su14031836

Chicago/Turabian StylePark, So Ra, Sung Tae Kim, and Hong-Hee Lee. 2022. "Green Supply Chain Management Efforts of First-Tier Suppliers on Economic and Business Performances in the Electronics Industry" Sustainability 14, no. 3: 1836. https://doi.org/10.3390/su14031836