Value-Added Tax Revenue Transfers and Regional Social Development: Evidence from Nigeria

Department of Accounting, College of Management and Social Sciences, Covenant University, Ota 110001, Ogun State, Nigeria

Sustainability 2022, 14(21), 14343; https://doi.org/10.3390/su142114343

Submission received: 7 September 2022

/

Revised: 25 October 2022

/

Accepted: 27 October 2022

/

Published: 2 November 2022

Abstract

:The gross social underdevelopment in Nigerian communities and villages is the underlying reason for investigating the effectiveness of VAT revenue transfers to states and local governments in providing the necessary social and community development services to meet the needs of the entire populace. This study examined the impact of VAT revenue devolution on social development in Nigeria from 1995 to 2021, with a focus on community welfare, making use of secondary data retrieved from the Central Bank of Nigeria’s statistical archive. In analyzing the data, we used an ex post facto research design and a cross-sectional econometric approach. The study examined the relationship between variables and included a trend analysis, a causality evaluation, and a regression analysis to determine the impact of VAT transfer on social welfare in Nigeria. According to the findings, VAT transfer to states has a positive relationship with social development, and the effect is both significant and beneficial at the 0.01 level. Local governments’ share of VAT collection, on the other hand, has an intangible positive effect on social development at the 0.05 degree of importance. As a result, we concluded that VAT revenue autonomy is now required in Nigeria. The study strongly advocates for the total transfer of revenue receipts to states and local governments for the benefit of society.

1. Introduction

VAT is a tax levied on the worth that the manufacturers or merchants of products or services add to merchandise or services before marketing them. The implementation of VAT in Nigeria was prompted by the need to increase government income from non-oil inputs following oscillations in hydrocarbon income as a result of the global market’s excess supply. VAT was implemented in the 1994 financial year with the enactment of VAT Decree No. 102 of 1993, and it is administrated by the Federal Inland Revenue Service (FIRS). The current VAT rate is 7.5%. The net proceed is divided among the three tiers of government, as follows: federal government—15%; state governments—50%; and municipal councils—35%. The constitutionality of the VAT Act has elicited varying rejoinders from constitutional lawyers; the majority of these political viewpoints center on the ideology behind the VAT Act covering ground that should be governed by state statutes. Thus, VAT is a vestigial issue that falls under the legislative and managerial purview of each region. Approximately 30 states contribute slightly less than 20% of VAT gathering, while Lagos and Rivers State, which are presently in the center of the hurricane, are considered to be responsible for more than 70% of the VAT stream in Nigeria. Lagos, as a place holder, is able to contribute about 55%, because of the large percentage of commercial development in this state as a result of its symbolic significance as Nigeria’s cosmopolitan city, generating a substantial contribution to its economic expansion [1].

VAT revenue collection and devolution have recently become contentious issues in Nigeria. The devolution is such that the states and local governments collect a large chunk of the VAT revenues that have been accrued by the government regardless of the contribution from each state. The federal government collects the lowest sum of VAT as a way of encouraging social development across the regions of the country. The question at hand relates to whether the Federal Government of Nigeria (FGN) has any constitutional authority to collect the VAT accrued from business operations in each state. According to social democrat solicitors, the FGN lacks the power to legislate the VAT Act under the 1999 Constitution [2]. As stated in items 58 and 59 of Part 1 of the Second Schedule to the 1999 Constitution, the appellate court judgment retains that the FG is only authorized to make tax laws and enforce and raise revenue on stamp duties, earnings, company profits, and capital appreciation. The Court also ruled that such clauses should be interpreted to exclude certain forms of tax, such as VAT. The verdicts explicitly indicated that the National Assembly does not have the authority to impose VAT on states [2].

The above analysis has indeed resulted in a situation whereby the states concerned are requesting fairness and justice in the allocation of collected VAT money or asking to be granted the fiscal responsibility to directly collect the VAT accruing from their states. Since many Nigerian jurisdictions clash with the federal government via the FIRS over the gathering of VAT, the biggest problem is that the national government has no legal justification for administering VAT. Thus, the moment has arrived for the Nigerian commonwealth to be restructured from its current command economy. The Rivers State Government has recently gained the opportunity to collect VAT in its region within the Nigerian federation through a High Court decision. Other jurisdictions, including Lagos, Ogun, and Oyo, have decided to join the FG’s Supreme Court petition [2]. Voices in the ongoing dispute keep calling for financial parliamentary sovereignty to be strengthened. To minimize the continuous turbulence in revenue sharing, the federal government must take the initiative in reallocating assets in a just and equitable manner. In our federal structure, as in all others, a financially equitable federal state is advantageous, so that no segment is left behind because it is more impoverished than the rest. Although the government of the Federation of Nigeria has what is called a stabilization fund, which is purely applied to salvaging states that encounter a revenue decline and cannot keep up with their expenditure responsibilities, this fund is derived from the 7.5% special funds and has not been very effective since 2002.

Regardless of the structural asymmetry and security risk to federal systems in Nigeria, of which VAT management is an instance, it is crucial to recognize that Nigeria is a federation made up of the national government, 36 states, a federal capital territory, and 774 municipal councils [3]. Complete decentralization would guarantee the distribution of authority among a variety of self-sufficient regional states. Furthermore, federalism permits the allotment of taxing authority, income, and spending to the various components of the administration in a federal structure so that they may carry out their statutorily designated tasks and duties for their community members [3]. The primary focus of this study was the social impact investments of each of these contentions. Some people define long-term social impact investments as providing social welfare to those who are disadvantaged in a community [4]. Conventional public assistance enterprises are mostly financed by governments, foundation money, or philanthropists, but the value of such financial support is significantly lower than what a community needs to spend on conservative assets, which include specific and financial investments [4]. Notwithstanding, in this study, we argue that social investment is necessary for general social development as well as human capacity building. Government funding for education, technology transfer, infrastructure, electricity, and workforce development—which are the direct consequence of fiscal decentralization—is critical for economic and social development [5]. In Nigeria, social development is linked to socioeconomic indicators such as education level, the availability of healthcare services, the security of lives and properties, job availability, and improvements to the general standard of living.

Following existing debates in the country about VAT revenue and whether states should be given the autonomous right to collect VAT directly from the businesses operating in their region, this study sought to achieve a common goal by determining the impact of VAT revenue transfer or devolution on social and community development in Nigeria. The study’s findings were intended to provide a policy direction for the central administration on the subject at hand. To begin, several studies on the effects of fiscal decentralization and tax revenue on social and economic development were reviewed. Previous studies that have empirically established tax revenue as an economic and social development indicator include [6,7]. Recent studies [8,9,10,11] have provided evidence that fiscal revenue devolution is an agent of social and economic development, particularly in emerging economies, whereas [12,13] argued for the opposite.

The current study, however, focuses on the impact of VAT revenue transfers to states and local governments on social and community development services. There has been no previous study that pursued this goal; thus, this study is organized to fill this existing gap and to boost government decision making at this critical time in Nigeria. The study is divided into five sections: Section 1 highlights the introduction, Section 2 presents the literature review, Section 3 depicts the research methods and properties, Section 4 provides data analysis and discussion of study findings, and Section 5 presents the conclusion.

2. Literature Review

2.1. Conceptual Review

2.1.1. Conceptual Framework

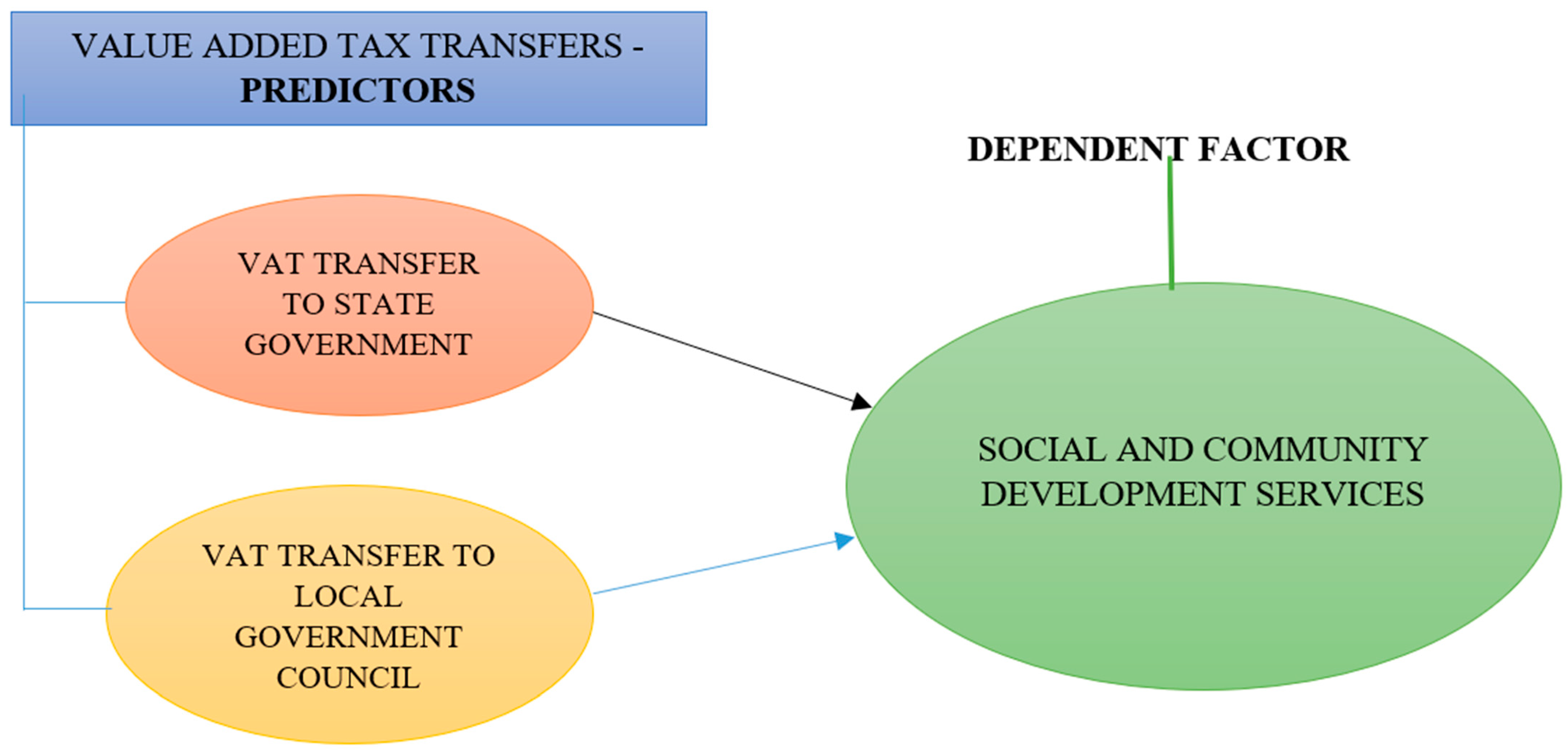

Figure 1 depicts the main goal of this study, which captures how VAT revenue transfers to states and local governments are expected to boost social and community development services in Nigeria. The predictors in this study are VAT revenue transfers to states and local councils, while the dependent factor is social and community development services. This study postulates that VAT devolution should promote social development in areas of public welfare such as education, quality health care services, technological innovations, job creation, social security, and safety in all communities and villages across the country.

2.1.2. Concept of Fiscal Decentralization

Delegation of authority, in a broad sense, refers to the shift of authority or responsibility from the central government to the municipal governments [14,15,16,17]. Financial liberalization is a crucial component of regional autonomy for local authorities. Fiscal liberalization typically entails transferring major spending mandate to local authorities while simultaneously expanding their financial sources and strength [18]. This framework is connected to the subservience of government financial jurisdiction, which includes local council revenue and expenditure [19,20,21]. The deployment of this doctrine is anticipated to enhance the distribution and quality of public good and services provision [15,22]. This efficiency has the potential to drive both local and national economic growth [17]. The connection between revenue mobilization and economic success is not described clearly in traditional budgetary centralist hypothesis [21].

Fiscal outsourcing has the ability to alleviate poverty if it is characterized by greater financial self-governance of municipalities, as well as suitable budgetary allocation, prioritizing, transparency, and sensitivity [23]. Otherwise, devolution risks widening regional imbalances due to local and provincial governments’ lack of expertise in monitoring public assets and services [24]. County council taxation is typically less innovative than state budget taxation [25,26]. According to Wong’s study of the connection between regional economic development and local authority tax strength, high real estate tax money is inversely associated with the capacity of local authorities to earn revenue [26].

Devolution in a specific term facilitates local interconnectivity under high-quality democratic representation but, worryingly, gives rise to broader regional imbalances in improperly managed regions of the world [27]. In contrast, according to [28], huge transfer overdependence might also help homogenize the financial assets available for disadvantaged areas to actually accomplish national standards in the providing of provincial and district commodities and services beneficial to provincial integration. From the standpoint of rational behavior, a central authority does not always reallocate to poorer areas. Wealthier provinces are frequently more powerful dealmakers than poorer ones. As a result, those territories have a greater influence on national government policy instruments, potentially causing a decrease in inter-governmental remittance to impoverished provinces [29]. Bartolini et al. [28], on the other hand, argue that government expenditure on behalf of municipalities should be merged with supplying local authorities with a mainline of their own earnings.

2.1.3. Concept of VAT and Its Devolution Bases in Nigeria

Devolution is characterized by the shift of obligation for making plans, decisions, distribution of resources, or governmental power from the centralized administration to the lower tiers of government [30]. If tax devolution increases the government financial system’s reliance on these mechanisms, the tax overall device multiplier effect usually decreases, thereby triggering greater income disparities to spring up [31]. VAT is a consumption tax that many countries around the world have endorsed and implemented simply because it is challenging to circumvent and relatively simple to conduct. It was initiated by VAT Decree No. 102 of 1993 to substitute the sales tax powered under Decree No.7 of 1986, which was conducted by states and the Federal Capital Territory (FCT) and has since resolved the governmental controversies affecting the formidable nightmare for businesses that operate across the numerous jurisdictions, who were previously subject to distinct sales taxation policies throughout the nation. The tax stayed at 5% before being raised to 7.5% by the Finance Act of 2020. Even though the Federal Inland Revenue Service (FIRS) administers VAT securely, it has always existed mainly for the benefit of Nigeria’s states. The VAT pool is divided as follows: 15% goes to the Federal Government, 50% to states, and 35% to local authorities (with a net of 4 per cent as cost of collection by the FIRS). The proportion of service charges has been raised by the states at Federation Account Allocation Committee (“FAAC”) discussions, but it is still being ignored with great ease.

The concept of determination is recognized in the transfer of VAT among state and local governments, with 20% (20%) of the pool distributed on this basic principle. Under normal circumstances, it is expected that lower-level authorities ought to be capable of covering the majority of their costs through local council taxes and other sources of cash flow [32]. Ordinarily, VAT autonomy is actually one of the measures and income streams available for states and local councils to manage their expenditure responsibilities without too much reliance on the statutory allocation from the central treasury. Furthermore, applying VAT as the primary consumption tax is a government financial measure that minimizes tax fraud because commercial enterprises implement it throughout each phase of manufacture and are only fully responsible for the enhanced value of their merchandise [7]. In terms of societal health and wellbeing, an irreversible mixture of accelerated taxes and government spending would focus on ensuring the transmission of revenue from wealthier to relatively poor localities [7].

2.2. Theoretical Framework

Theory of decentralization. The theory underpinning this work is the theory of decentralization propounded by [33]. The Devolution Syllogism describes a well-known framework by which fiscal decentralization can lead to increased cost productivity, where participants and regional priorities for public amenities and services vary considerably, as demonstrated by this lemma [34]. The amount of social assistance attained by a federal government by delivering homogeneous public resources and services is indeed lower than that attained by supplying public services and products in a federated arrangement that enables the supply of products and services across geographical segments [33]. It is obvious that sub-national authorities are provided with more information about community members’ priorities than the central government. As a result, sub-national governments are always more effective in providing public amenities and services that are specific to the requirements of local people. Correspondingly, financial efficiency may be increased if people are movable enough to relocate to cities and counties that perfectly match their priorities [35].

According to [36], operating costs for community and infrastructural facilities major industries are often more likely to stimulate expansion if conducted by sub-national authorities rather than the centralized administration, which may completely disregard disparities in priority. Rivalry among states is thought to be a crucial pathway for encouraging overall effectiveness in taxes, regulatory frameworks, and the delivery of goods and services [35,37]. Devolution, according to the social representation strategy, may result in contest among municipalities for mobile manufacturing factors. This imposes self-restraint on government servants, who are prone to pursuing their own interests and maximizing their profits. Accordingly, fiscal intensity of rivalry among tiers of government translates to a market-preserving federal structure which mitigates the degree of government involvement, hence trying to maintain economic efficiency [38].

Criticism of theory of decentralization. Over the years, the fiscal devolution theory has suffered some criticisms which includes weak regulation and fiscal control at the local echelons of government. Decentralization supporters argue that municipal authorities have an advantageous position over the centralized administration in the area of getting information regarding the local needs of people. This presumption, nevertheless, can be questioned due to the fact that central governments can designate public officials to regional branches to obtain the requisite information required to improve the social condition of communities. There appears to be no convincing reason to assume that the evidence gathered by these delegates will be less factual than that procured by state municipalities [39]. Likewise, it is found that local governments perceive the desires and requirements of the native community as well as provide public amenities and services appropriately. Tanzi [39] challenges this insinuation, claiming that the native populace may lack the ability to influence the course of action of city governments. As a direct consequence, products and related items may be generated without regard for the desires and requirements of the rural inhabitants. This is due to the fact that local governance is comparatively feeble and unproductive, particularly in emerging economies.

There are issues such as minimal investment in research and development as a result of sub-national policymakers’ constraints, both technologically and financially [40]. Municipal authorities frequently exhibit poor welfare spending managerial systems to support them in their tax and spending plan choices because of the incompetence of local regulatory agencies [30]. A further complicating factor frequently connected with devolution of revenue powers is local councils looting the fiscal resources because of the existence of a soft-budget constrictions. The opposing views hold that sub-national policymakers in decentralization may anticipate the central government to pay for their budget deficits which further reduces the motivation for state authorities to oversee their finances prudently. Delicate budget restraints have a range of causes that are attributed with the predominant current financial organizations, the present political configuration, the vulnerability or even complete lack of numerous significant industries, and, more pertinently, the historical information of redistributive issues throughout the nation [41].

2.3. Empirical Review

Gainsborough [42] reviewed variability in the extent to which states reacted to public assistance provincial autonomy by handing power over welfare system to local governments. The research found that states that decentralized responsibility to lower branches of government actually managed to be states with a higher level of engagement of municipal authorities in social welfare. Joan’s [43] findings indicated that the delegation of authority improved long-term healthcare law and curtailed pre-existing social assistance fracturing in Spain by distributing development framework. Busemeyer [44] examined the effect of revenue mobilization on varying sorts of expenses in OECD nations from 1980 to 2001 using a cross-sectional regression model and an aggregated time series evaluation of schooling, retirement package, social, and total state expenditure. The analysis revealed a strong and positive relationship between fiscal decentralization and overall stages of school funding. Notwithstanding, when glancing at nationwide government policies (for example, retirement plan policies), financial devolution is correlated with lower levels of investment supply. Chu and Zheng [45] used Lucas’ hypothesis of long-run economic growth and Stiglitz’s philosophy of municipal social infrastructure to create an estimation procedure with five algebraic expressions to examine the impact of China’s devolution on regional development. The model is evaluated using two-stage least squares on 31 Chinese provinces from 1996 to 2005. According to the parameter estimates, China’s financial liberalization enhanced local authorities’ public spending on tangible infrastructural development, which ultimately led to rising in specific geographical investment securities, human development levels and general regional economic growth.

Financial liberalization became necessary in Pakistan because of a disparity between overall spending necessities and income generation capabilities. This misalignment usually requires an inter-governmental transfer between the federation and the regions, which is an essential component of the division of power. Based on this premise, ref. [34] tried to investigate the consequences of fiscal regional autonomy on Pakistan’s economy. On the whole, the analysis revealed that cash flow devolution boosted productivity expansion while spending delegation of authority decelerated the process. Soejoto et al. [46] conducted a study on fiscal decentralization as a technique for encouraging human advancement in Indonesia. In broad sense, the analysis revealed that redistributive resources strategies benefited the social evolution of each autonomous community, county, and city. Yushkov [21] investigated the conceptual and empirical implications of revenue mobilization on income progress. Econometric findings of Russian regions from 2005 to 2012 revealed that inordinate expenses devolution within the province was significant and detrimental to regional economic expansion when it was not supplemented by the same rate of income regional autonomy. Provincial reliance on inter-governmental revenue sharing from the national center point, on the other hand, was optimistically linked to increased economic activity.

Setiawan and Aritenang [10] looked into the consequences of fiscal decentralization on Indonesian financial outlook. The study used lag value to evaluate the effects of revenue mobilization and overlooked the presence of geographic interdependence between territories. The analysis indicated that financial liberalization had a considerable influence on financial performance at a three-year latency worth, suggesting that social financial planning will have a major impact on enhancing business success after three years. Furthermore, the paper demonstrated that provinces with related market outcomes were conveniently located, confirming the existence of observed relationships. Utilizing Granger causality evaluation and concentrating on both human development and economic expansion as social assistance ingredients, [7] examined innovative perspectives on the impact of taxes on the social welfare system. The research was based on a comparison of Central and Eastern European countries and the wealthiest European countries between 1995 and 2015. Taxation was represented by various taxes collected to GDP ratios, economic expansion was characterized by gross domestic product and gross national income, and the human development index (HDI) contained in the evaluation was a comprehensive index being used to prioritize states based on their level of social and financial development. The findings confirmed that taxes accelerate economic growth, but they have a constrained influence on human advancement.

Mutiarani and Siswantoro [47] investigated the impact of local authority characteristics on Indonesia’s fulfillment of the Sustainable Development Goals (SDGs). The study’s findings reflected the attributes of municipal administration in terms of territory dimensions, the statistic of provincial workplaces, and the presence of municipal own-source earnings, all of which have an impact on the achievement of the United Nations millennium development goals. According to the findings of this study, local governments will require significant effort and resources to achieve the sustainability goals. Ji and Zhang [13] investigated the fiscal grounds of why land urban development outpaced workforce population growth. They used panel data from 30 Chinese provinces and regional authorities from 2000 to 2012 to examine the effect of transfer payments on urban expansion from four perspectives: fiscal revenue, tax categories, fiscal self-financing rate, and tax shortfalls. Both the municipal tax receipts and the fiscal self-financing rate had a significantly detrimental impact on the gap between land urbanization and the population’s industrialization. The relatively small the disparity, the greater the percentage of corporation tax, and vice versa for value-added tax. The bigger the chasm, the significantly larger the local authorities’ tax decline.

Gemmell et al. [48] used pooled-mean cluster methods to determine if the productivity increases associated with devolution produce greater expansion in more fragmented economic systems, using a large sample of 23 Organization for Economic Cooperation and Development (OECD) regions from 1972 to 2005. The research showed that expenditure devolution was linked to decreased economic progress, whereas revenue devolution was linked to increased rapid expansion. Flaška et al. [49] investigated regional disparities in receipts from local taxation and compared the evolution of local council taxation percentages with randomly chosen metrics in the Slovak Republic’s NUTS III territories. The study summarized regional differences in municipal tax receipts in terms of overall tax collections, own current revenues, and total current outlay in relation to the territories’ levels of socioeconomic status. The findings showed that regional social and economic success has a consequence for local government revenue from taxes.

Galecka et al. [31] used the total order of objects method to determine the impact of government institutions’ spending on an individual’s personal social situation across Poland’s states and local government units. The investigation discovered both the government’s reliance on individual units’ revenue mobilization and its ineffectiveness in completely removing inter-state societal problems. Omodero and Alege [6] examined the impact of crude petroleum products income and tax receipts on Nigerian inclusive growth from 2003 to 2019. The research showed that crude oil income had little influence on social advancement in Nigeria. Similarly, both exchange and inflation rates were having major detrimental effect on the country’s social evolution. Remarkably, tax receipts had a quantitatively beneficial effect on social improvement.

According to Xu and Lin [50], devolution gives local communities more financial independence, which could lead to modifications to healthcare spending; and hence, fiscal decentralization could have an impact on quality of life at the provincial scale. To investigate this claim, they adapted a two-way fixed impact model, as well as maximal hypothesis testing and transitional effect modeling techniques, to panel data from China’s 30 continental counties, as well as four municipal councils and regional authorities, from 2008 to 2019. The study discovered that fiscal decentralization increased public healthcare costs by enhancing local health public utility resources required. Subroto and Baidlowi [11] discussed the policy impact of devolving financing options between national and local government on East Java’s economic progress. A clarification configuration with a deductive methodology was used in the methodological approach. From 2009 to 2018, data panels were harvested from 38 metropolitan areas in East Java and analyzed using the least squares method. The analysis revealed that decentralizing revenue sources could help bolster trade and investment and influence regional development. Steadily increasing business output could significantly improve the economy. Simultaneously, local productivity recovery has the potential to significantly improve the well-being of East Java’s community.

Olaide et al. [12] examined the positive milestones of federal systems in 40 countries between 2006 and 2018. Fiscal decentralization had no considerable influence on the overall community construction, environmental and mineral wealth development indicators, or community welfare benchmark, but it did have a benefit on the economic development indicators. Bui et al. [8] looked into the impact of fiscal decentralization on Vietnamese provinces’ social development. The exploratory work used panel rectified conventional errors assessment and dynamic panel evaluation on revised data set from 63 Vietnamese regions from 2011 to 2019. The research showed that financial liberalization has a beneficial impact on both economic and social development, as well as resource usage reliability for strategic goals. Nguyen and Thanh [9] used panel data from 18 jurisdictions from 2011 to 2017 to investigate the concurrent connection between devolution, wealth creation, and social evolution. The findings revealed a significant relationship between revenue mobilization, productivity expansion, and human evolution from various perspectives. Financial liberalization had a beneficial and detrimental effect on economic growth and social development, respectively. Ma and Mao [51] discovered that economic liberalization changes in China resulted in local economic growth by delegating much tax and expenditure power to local governments. The effect was much stronger in regions with higher immediate macroeconomic stability. According to the findings of Ahmad et al. [52], fiscal decentralization positively affected green building for the appropriate sample metropolitan areas; nevertheless, the effect varied across China. The results also showed that financial devolution increased eco-efficiency in China’s eastern and central regions but had a negative impact in the western part of the country. The findings also demonstrated that irrational use of resources for economic and social development decreased ecosystem preservation. Blane and Smoke [53] stressed the importance for national authorities to diligently analyze the believed arbitrage opportunities in their regional integration structures before attempting to eliminate them. Hang et al. [54] looked into the effect of tax strategy on social evolution in Vietnam. The Distributed Autoregressive technique was employed to study time-series data from 1990 to 2017. The paper was very successful in obtaining the first empirical proof of the long-term hurtful influence of tax plan on joblessness in Vietnam. Furthermore, it discovered a significant statistical effect of household savings and private production on job loss in both the short and long terms. Another study [55] found that regions respond differently to fiscal devolution, with those with macroeconomic issues responding negatively and those with fiscal stability responding positively. In ensuring efficient management of ecosystem, [56] established that fiscal decentralization improves green environment and attracts healthy competition among provinces in China.

3. Methodology

This study looks at the impact of VAT revenue devolution on social and community development in Nigeria from 1995 to 2021. The study employs an ex post facto research design as well as a cross-sectional approach. The ex post facto approach allows researchers to use existing data without modifying it, whereas the cross-sectional system enables the use of appropriate econometric tools such as the Granger causality technique, correlational matrix, and regression technique to drive the study’s objective. Secondary sources are used to gather information for both the dependent and independent variables. The dependent variable is social and community services, and the data are from the Central Bank of Nigeria (CBN) Statistical Bulletin. The independent variables are the VAT revenue allocation to the state governments and the VAT revenue transfer to the local governments. The CBN Statistical Bulletin was used to retrieve all of the data for the predictors. The datasets are collected in national currency, and because there are no differences in their representation, the researchers simply continue with the evaluation without any kind of conversion. The unit root is used to verify the appropriateness and consistency of the dataset in a combine operation, whereas the correlation matrix demonstrates the type of association that exists among the factors used in this study. The data trend for the time frame covered by this study is also shown. The Pairwise Granger Causality Test makes an important contribution to the specific goals of the research by clarifying the causality effect of the variables, whereas the regression analysis provides information on the effects of VAT devolution on social welfare services.

The variable measurements are shown in Table 1:

The specific goals of this study are to assess the impact of VAT allocation to states and local governments in Nigeria on social and community development services. In line with these goals, the study asks whether the current VAT sharing among states and local governments has a meaningful impact on social welfare, particularly in small towns and villages. In order to attempt to answer this research question, the study assumes that Nigeria’s current VAT autonomy has little impact on states and local councils. The following models have been developed to drive this investigation empirically in order to achieve the goal of this study.

3.1. Model Specification

The model engaged for this research is stated as follows:

where

Y = Social and community services;

X = VAT revenue distribution to the state and local governments;

β = Coefficient;

= Error term.

The model shown above can be unambiguously functional to this study as:

where:

SCSV = The cost of social and community services;

SVAT = VAT revenue transfer to the state government;

LVAT = Value-Added Tax income transfer to the Local authorities;

= Constant term

− = intercept

= Error term

On the a priori, we anticipate; β1 > 0, β2 > 0.

3.2. Model for Granger Causality Testing

The model below explains the operation of the Granger causality function applied in this study. The initial assumption is that VAT devolution does have causality effects on social developments (y(t) does not Granger cause x(t)). To test this hypothesis, these equations test to see if y(t) Granger causes x(t):

From Equation (3), we show that Y (Social development) does not Granger cause X (VAT devolution) or that Y does not have causality effect on X.

Similarly, Equation (4) also suggests that X (VAT devolution) does not Granger cause Y (Social development).

4. Data Assessment and Elucidation

This section includes the trend analysis of data, unit root analysis, correlation matrix, Granger causality explanation, and the impact explanation using the regression result.

- Source of data: Central Bank of Nigeria

The graphical output in Figure 2 depicts the dataset’s trend from 1995 to 2021. According to social development, the cost of social and community services in 2020 will be the highest. This is due to the COVID-19 pandemic challenge, which caused the government to spend so much at both the state and community levels due to the large number of victims of the virus and efforts to provide medical facilities to save the lives of citizens under attack. Aside from welfare, the high rate of security challenges in rural areas posed by bandits and herdsmen are also issues that require significant funding to address. As a result, the cost of addressing social challenges in communities and villages was excessive in 2019, 2020, and 2021. The government must identify these challenges and address them appropriately. The year 2021 was projected to have the highest VAT allocation to both states and local governments. This is due to the growing awareness of states’ financial autonomy, as well as the possible increase in the VAT rate from 5% to 7.5%, which went into effect in February 2021.

The unit root result, shown in Table 2, confirms that the datasets used in this study are reliable and do not have the possibility of yielding systematic errors. Levin, Lin & Chut, Im, Pesaran, and Shin W-statistics, Augmented Dickey–Fuller (ADF)-Fisher Chi-square, and Phillip–Peron (PP)-Fisher Chi-square are all unit root corroboration methods. The numerous different unit root mechanism used in this assessment certify that there is no unit root concern with the datasets with a likelihood of 0.00, which is less than 0.05.

The connection between the variables utilized in this research is shown in Table 3. SCSV has a 96.7% correlation with SVAT, indicating a very strong positive correlation. That is, the transfer of VAT to states has a very strong positive relationship with social and community services. The provision of public goods and services across the country is linked to a greater extent with VAT revenue available to states. Similarly, the correlation between local governments and social development is very high (97%). It is important to note that this result supports the decentralization framework provided by [33].

Table 4 shows the extent to which each variable has a connecting effect on the other. At 1% materiality, the test results show that SVAT has a causality effect on social development. In the same order, the allocation of VAT revenue to local governments has a causal influence on social and community services at the 1% significance level. This result supports the result in Table 4 which provides evidence that there is a very strong relationship existing between SCSV and the VAT allocation to both states and local authorities. Additionally, both the state and local authorities VAT transfer do not have causation effect on each other. The obvious reason is that when it comes to revenue sharing in Nigeria, the two levels of government are autonomous. As a result, the fiscal delegation on them is expected to be carried out independently of the other party.

The result in Table 5 provides evidence that the predictors are not interrelated since the VIF is less than the value of 10 [57]. The estimate has a standard error of 0.22, implying that it is at least 78% accurate. The F-statistic also demonstrates that the predictors successfully influence social development, and this evidence is correct because the p-value is 0.00 below the 0.05 threshold. The model is said to be appropriate for the calculation. The predictors are tested independently, and the results show that the state VAT share has a significant positive impact on social welfare.

This discovery gives credibility to the devolution theory [33]. Previous studies have confirmed and agreed with this finding [8,10,11,34,46,51]. This result also contradicts empirical studies of [12,13]. However, the transfer of VAT revenue to municipal governments is insufficient to promote social development. Based on this outcome, and in order to attract even development throughout the country, Nigeria’s devolution strategies should be modified in favor of local councils.

5. Conclusions

Based on the findings of this study, we conclude that VAT revenue transfers to states and local governments should be comprehensive in order for them to effectively carry out their constitutional expenditure responsibility for adequate social welfare. The country’s current VAT revenue sharing formula states that states receive 50% of total VAT receipts, while local government councils receive 35%, leaving the Federal government in charge of the remaining 15%. The argument is that the federal government should allow states and local governments to have autonomy over this type of tax revenue because it does not fall under the category of tax revenues that are solely collected by the federal government. This argument lends credence to the “second-generation theory of fiscal federalism”, which is based on the structure and operation of federal systems [58]. This study objectively examined the current share of VAT for states and local governments, as well as how this current share affects the social and community development services that states and local governments are obviously designed to pursue because they are the government that is relatively close to the people. According to the findings, only the states’ share of the VAT transfer has a tangible impact on social development, while the municipal authorities’ share has no bearing with the development of its communities and suburbs.

As a result of this research, we recommend that states and local governments should be given complete autonomy over VAT collection in Nigeria. In addition, since they have statutory expenditure responsibility to shoulder independently, the sharing should be equitable. The state’s share should not be higher than that of the local authority. In this case, we recommend a sharing formula based on statutory responsibilities for both state and local councils. The main reason is that communities rely on local councils to meet their needs, and because local governments bear a large burden of meeting the social needs of rural residents, it is critical that they build a strong revenue base. Furthermore, because VAT revenue collection is not within the Federal government’s taxing powers, it is expected that this type of tax be delegated to lower-level governments to manage for the benefit of the entire society.

6. Limitations and Further Research

One of the major constraints encountered during this research was a lack of existing literature specifically discussing VAT collection devolution in the country and several other parts of the world. The study relied on other related studies, and it is expected that the current study will improve the literature base in this area of study and assist the government in improving policies of local financial autonomy in the country. There are obvious reasons for further research on VAT devolution in several Sub-Saharan African countries where the central government competes with local authorities for VAT funds meant to boost local investments in social welfare. Following the ongoing disagreements in Nigeria over the local autonomy of VAT revenue, the emergence of more scientific analysis has become critical, serving as a precedent in policies for other emerging economies. As a result, the study suggests that more research be conducted on this topic, particularly in developing economies such as those in Sub-Saharan Africa.

Funding

This research is funded by The Covenant University Centre for Research, Innovation and Discovery (CUCRID).

Institutional Review Board Statement

The originality of this research is confirmed.

Informed Consent Statement

The author has given consent to this publication.

Data Availability Statement

Data provision to anyone is based on request.

Conflicts of Interest

The author expresses an absence of conflict of interest.

References

- Akinyemi, A. VAT Controversy: The Need to Avoid Fiscal Anarchy. Premium Times. 2021. Available online: https://www.premiumtimesng.com/opinion/485019-vat-controversy-the-need-to-avoid-fiscal-anarchy-by-akinyemiashade.html (accessed on 12 August 2022).

- Ogunmupe, B. Why States Should Collect VAT in Nigeria. Guardian. 2021. Available online: https://guardian.ng/opinion/why-states-should-collect-vat-in-nigeria/ (accessed on 10 June 2022).

- Omojoye, S. Staying in the Lane: VAT Dispute Is Constitutional, Not About States’ Capacity to Collect VAT. The Cable. 2021. Available online: https://www.thecable.ng/staying-on-the-lane-vat-dispute-is-constitutional-not-about-states-capacity-to-collect-vat (accessed on 12 December 2021).

- Wong, M.C.S.; Yap, R.C.Y. Social impact investing for marginalized communities in Hong Kong: Cases and Issues. Sustainability 2019, 11, 2831. [Google Scholar] [CrossRef] [Green Version]

- Omodero, C.O. Effect of apportioned federal revenue on economic growth: The Nigerian Experience. Int. J. Financ. Res. 2019, 10, 172–180. [Google Scholar] [CrossRef] [Green Version]

- Omodero, C.O.; Alege, P.O. Crude oil resources, tax revenue and sustainable social Development in Nigeria. Int. J. Energy Econ. Policy 2021, 11, 22–27. [Google Scholar] [CrossRef]

- Vatavu, S.; Lobont, O.-R.; Stefea, P.; Brindescu-Olariu, D. How taxes relate to Potential welfare gain and appreciable economic growth. Sustainability 2019, 11, 4094. [Google Scholar] [CrossRef] [Green Version]

- Bui, M.-T.; Le, T.-H.; Park, D. Impacts of fiscal decentralization on local development In Vietnam: A disaggregated analysis. Econ. Trans. Inst. L Chang. 2022. [Google Scholar] [CrossRef]

- Nguyen, T.H.; Thanh, S.D. Fiscal decentralization, economic growth, and human Development: Empirical evidence. Cogent Econ. Financ. 2022, 10, 1–17. [Google Scholar] [CrossRef]

- Setiawan, F.; Aritenang, A.F. The impact of fiscal decentralization on economic Performance in Indonesia. IOP Conf. Ser. Earth Environ. Sci. 2019, 340, 012021. [Google Scholar] [CrossRef]

- Subroto, W.T.; Baidlowi, I. Does funding decentralization can influence the local Economic growth? Iran. Econ. Rev. 2022, 26, 311–323. [Google Scholar] [CrossRef]

- Olaide, K.; Simo-Kengne, B.D.; Uwilingiye, J. Sustainable Development–Fiscal Federalism Nexus: A “Beyond GDP” Approach. Sustainability 2022, 14, 6267. [Google Scholar] [CrossRef]

- Ji, L.; Zhang, W. Fiscal incentives and sustainable urbanization: Evidence from China. Sustainability 2020, 12, 103. [Google Scholar] [CrossRef]

- Devkota, K.L. Impact of Fiscal Decentralization on Economic Growth in the Districts of Nepal. Int. Cent. Public Policy (ICEPP) Work. Pap. 2014, 12. Available online: https://scholarworks.gsu.edu/icepp/12 (accessed on 20 June 2022).

- Firman, T. Inter-local-government partnership for urban management in decentralizing Indonesia: From below or above? Karmantul (Greater Yogyakarta) and Jabodetabek (Greater Jakarta) compared. Space Polity 2014, 18, 215–232. [Google Scholar] [CrossRef]

- Hammond, G.W.; Tosun, M.S. The Impact of Local Decentralization on Economic Growth: Evidence from U.S Countries. IZA DP No. 4574. 2009. Available online: https://repec.iza.org/dp4574.pdf (accessed on 12 June 2022).

- Baskaran, T.; Feld, L.P. Fiscal Decentralization and Economic Growth in OECD Countries: Is there a Relationship? Public Financ. Rev. 2012, 41. [Google Scholar] [CrossRef]

- Olena, C.; Yuriy, P.; Alina, V.; Anna, V. Assessment of Fiscal Decentralization Influence on Social and Economic Development. Mont. J. Econ. 2018, 14, 69–84. [Google Scholar]

- Zhang, T.; Zou, H.-F. Fiscal decentralization, public spending, and economic Growth in China. J. Public Econ. 1998, 67, 221–240. [Google Scholar] [CrossRef] [Green Version]

- Schneider, A. Who gets what from whom? The impact of decentralization on tax Capacity and pro-poor policy. IDS Work. Pap. 2003, 179. Available online: https://www.ids.ac.uk/download.php?file=files/Wp179.pdf (accessed on 12 June 2022).

- Yushkov, A. Fiscal decentralization and regional economic growth: Theory, empirics, and The Russian experience. Russ. J. Econ. 2015, 1, 404–418. [Google Scholar] [CrossRef] [Green Version]

- Oates, W.E. On the Theory and Practice of Fiscal Decentralization. In IFIR Working Papers; University of Maryland: College Park, MD, USA, 2006. [Google Scholar]

- Agyemang-Duah, W.; Gbedoho, E.K.; Peprah, P.; Arthur, F.; Sobeng, A.K.; Okyere, J.; Dokbila, J.M. Reducing poverty through fiscal decentralization in Ghana and beyond: A review. Cogent Econ. Financ. 2018, 6, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Lessmann, C. Fiscal decentralization and regional disparity: A panel data approach for OECD countries. Ifo Work. Pap. 2006. Available online: https://www.ifo.de/DocDL/IfoWorkingPaper-25.pdf (accessed on 30 August 2022).

- Rubolino, E. The efficiency and distributive effects of local taxes: Evidence from Italian Municipalities. Institute for social and economic research. ISER Work. Pap. Ser. 2019. Available online: http://www.ecineq.org/ecineq_paris19/papers_EcineqPSE/paper_202.pdf (accessed on 20 July 2022).

- Wong, H.K. Induction Programs that Keep New Teachers Teaching and Improving. NASSP Bull. 2004, 88, 41–58. [Google Scholar] [CrossRef]

- Kyriacou, A.P.; Muinelo-Gallo, L.; Roca-Sagales, O. Fiscal decentralization and Regional disparities: The importance of good governance. Reg. Sci. 2015, 94, 89–107. [Google Scholar] [CrossRef]

- Bartolini, D.; Stossberg, S.; Blöchliger, H. Fiscal Decentralization and Regional Disparities. In OECD Economics Department Working Papers; OECD Publishing: Paris, France, 2016. [Google Scholar] [CrossRef]

- Lessmann, C. Regional Inequality and Decentralization: An Empirical Analysis. Environ. Plan. A Econ. Space 2012, 44, 1363–1388. [Google Scholar] [CrossRef] [Green Version]

- Rondinelli, D.A.; Cheema, G.S. Policy implementation in developing countries. In Decentralization and Development; Shabbir, G., Dennis, C., Rondinelli, A., Eds.; Sage: Beverly Hills, CA, USA, 1983. [Google Scholar]

- Gałecka, M.; Patrzalek, L.; Kuropka, I.; Ewa, S.-P. The fiscal capacity of local government versus government expenditure, and its impact on eliminating inter-regional social inequalities in Poland. J. ERSA 2021, 9, 51–67. [Google Scholar] [CrossRef]

- Blöchliger, H.; Bartolini, D.; Stossberg, S. Does Fiscal Decentralization Foster Regional Convergence? In OECD Economic Policy Papers; OECD Publishing: Paris, France, 2016. [Google Scholar] [CrossRef]

- Oates, W.E. Fiscal Federalism; Harcourt Brace Jovanovich: New York, NY, USA, 1972. [Google Scholar]

- Iqbal, N.; Musleh, U.D.; Ghani, E. Fiscal decentralization and economic growth: Role of democratic institutions. PIDE Work. Pap. 2013, 89, 1–26. Available online: https://www.scopus.com/record/display.uri?origin=recordpage&zone=relatedDocuments&eid=2-s2.0-84878869960&noHighlight=false&relpos=0 (accessed on 30 June 2022).

- Tiebout, C.M. A Pure Theory of Local Expenditures. J. Political Econ. 1956, 64, 416–424. [Google Scholar] [CrossRef]

- Oates, W.E. Fiscal Decentralization and Economic Development. Nat. Tax J. 1993, 46, 237–243. [Google Scholar] [CrossRef]

- Brennan, G.; Buchanan, J.M. The Power to Tax—Analytical Foundation of a Fiscal Constitutions; Cambridge University Press: Cambridge, UK, 1980. [Google Scholar]

- Weingast, B.R. The Economic Role of Political Institutions: Market-Preserving Federalism and Economic Development. J. Law Econ. Orgn. 1995, 11, 1–31. [Google Scholar]

- Tanzi, V. Fiscal Federalism and Decentralization: A Review of Some Efficiency and Macroeconomic Aspects. In Annual World Bank Conference on Development Economics; Bruno, M., Pleskovic, B., Eds.; World Bank: Washington, DC, USA, 1996; pp. 295–316. [Google Scholar]

- Prud’homme, R. The Dangers of Decentralization. World Bank Res. Obs. 1995, 10, 201–220. Available online: http://www.jstor.org/stable/3986582 (accessed on 24 December 2021). [CrossRef]

- Rodden, J.; Eskeland, G.S.; Litvack, J. Fiscal Decentralization and the Challenges of Hard Budget Constraints; MIT Press: Cambridge, UK; London, UK, 2003. [Google Scholar]

- Gainsborough, J.F. To devolve or not to devolve? Welfare reform in the States. Political Stud. J. 2003, 31, 603–623. [Google Scholar] [CrossRef]

- Joan, C.-F. Devolution, diversity and welfare reform: Long-term care in the ‘Latin Rim’. Soc. Political Admn. 2010, 44, 481–494. [Google Scholar] [CrossRef]

- Busemeyer, M.R. The impact of fiscal decentralization on education and other types of Spending. Swiss Political Sci. Rev. 2011, 14, 451–481. [Google Scholar] [CrossRef] [Green Version]

- Chu, J.; Zheng, X.-P. China’s fiscal decentralization and regional economic growth. Jpn. Econ. Rev. 2013, 64, 537–549. [Google Scholar] [CrossRef]

- Soejoto, A.; Subroto, W.T.; Suyanto, Y. Fiscal decentralization policy in promoting Indonesia human development. Int. J. Econ. Financ. Iss. 2015, 5, 763–771. Available online: https://dergipark.org.tr/tr/download/article-file/363060 (accessed on 20 September 2022).

- Mutiarani, N.D.; Siswantoro, D. The impact of local government characteristics on the accomplishment of Sustainable Development Goals (SDGs). Cogent Bus. Manag. 2020, 7, 1–11. [Google Scholar] [CrossRef]

- Gemmell, N.; Kneller, R.; Sanz, I. Fiscal decentralization and economic growth: Spending versus revenue decentralization. Econ. Inq. 2021, 51, 1915–1931. [Google Scholar] [CrossRef]

- Flaška, F.; Rigová, Z.; Kološta, S.; Liptáková, K. Regional Differences in Revenues from Local Taxes in Comparison to the Socio-Economic Level of the Regions of the Slovak Republic. DANUBE 2021, 12, 197–211. [Google Scholar] [CrossRef]

- Xu, W.; Lin, J. Fiscal decentralization, public health expenditure and public health evidence from China. Front. Public Health 2022, 10, 1–12. [Google Scholar] [CrossRef]

- Ma, G.; Mao, I. Fiscal decentralization and local economic growth: Evidence from a fiscal reform in China. Fisc. Stud. 2018, 39, 159–187. [Google Scholar] [CrossRef]

- Ahmad, F.; Xu, H.; Draz, M.U.; Ozturk, I.; Chandio, A.A.; Wang, Y.; Zhang, D. The Case of China’s fiscal decentralization and eco-efficiency: Is it worthwhile or just a Bootless errand? Sustain. Prod. Consum. 2020, 26, 89–100. [Google Scholar] [CrossRef]

- Blane, D.L.; Smoke, P. Intergovernmental fiscal transfers and local incentives and responses: The case of Indonesia. Fisc. Stud. 2015, 38, 111–139. [Google Scholar] [CrossRef]

- Hang, N.P.T.; Nguyen, M.-L.T.; Ho, H.T.; Bui, T.N. The impact of tax policy on social development in Vietnam. Manag. Sci. Lett. 2020, 10, 995–1000. [Google Scholar] [CrossRef]

- Yang, Z. Tax reform, fiscal decentralization, and regional economic growth: New evidence From China. Econ. Modl. 2016, 59, 520–528. [Google Scholar] [CrossRef]

- Zhou, M.; Wang, T.; Yan, L.; Xie, X.-B. Has economic competition improved China’s Provincial energy ecological efficiency under fiscal decentralization? Sustainability 2018, 10, 2483. [Google Scholar] [CrossRef] [Green Version]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill Irwin: Boston, MA, USA, 2009. [Google Scholar]

- Oates, W.E. Toward a Second-Generation Theory of Fiscal Federalism. J. Int. Tax Public Financ. 2005, 12, 349–373. [Google Scholar] [CrossRef]

Figure 1.

Diagrammatical depiction of study objective.

Figure 2.

Trend of data used in this research from 1995–2021.

{kind=link}

{kind=link}

Table 1.

Variable dimension and sources.

| VARIABLE CODE | VARIABLE MEANING | VARIABLE MEASUREMENT | SOURCE OF DATA |

|---|---|---|---|

| DEPENDENT VARAIABLE | |||

| SCSV | Social and Community Service Cost | Collected in billions of national currency. | CBN Statistical Bulletin. |

| INDEPENDENT VARIABLES | |||

| SVAT | VAT revenue transfer to the 36 States in Nigeria including the Federal Capital Territory (FCT), Abuja. | Obtained in billions of Naira. | CBN Statistical Bulletin. |

| LVAT | VAT receipts transfer to the 774 local governments in Nigeria. | Gathered in billions of local currency. | CBN Statistical Bulletin. |

Source: Study information, 2022.

Table 2.

Summary of unit root test.

| Series: SCSV, SVAT, LVAT | ||||

| Sample: 1995–2021 | ||||

| Cross- | ||||

| Method | Statistic | Prob. | sections | Obs |

| Null: Unit root (assumes common unit root process) | ||||

| Levin, Lin & Chu t | −4.92 | 0.00 | 3 | 66 |

| Null: Unit root (assumes individual unit root process) | ||||

| ADF-Fisher Chi-square | 27.42 | 0.00 | 3 | 66 |

| PP-Fisher Chi-square | 35.64 | 0.00 | 3 | 72 |

Source: Authors’ research output, 2022.

Table 3.

Correlation analysis.

| Sample: 1995–2021 | |||

| Included observations: 27 | |||

| Correlation | SCSV | SVAT | LVAT |

| SCSV | 1.000000 | ||

| SVAT | 0.967693 | ** 1.000000 | |

| LVAT | 0.969154 | ** 0.999526 | 1.000000 |

** Correlation is significant at the 0.01 level, Source: Authors’ research output, 2022.

Table 4.

Pairwise Granger Causality Tests.

| Sample: 1995–2021 | |||

| Lags: 2 | |||

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| SVAT does not Granger Cause SCSV | 25 | 9.94 | 0.00 *** |

| LVAT does not Granger Cause SCSV | 25 | 8.97 | 0.00 *** |

| LVAT does not Granger Cause SVAT | 25 | 0.88 | 0.43 |

| SVAT does not Granger Cause LVAT | 0.31 | 0.74 | |

Source: Authors’ research output, 2022. *** indicates statistical significance at the 0.01.

Table 5.

Regression outcome.

| Variables Considered | SVAT | LVAT | Other Results |

|---|---|---|---|

| T—Statistic | 5.01 *** | −1.43 | |

| p-value | (0.00) | (0.17) | |

| Multicollinearity test—VIF | 2.12 | 2.05 | |

| CV | (0.01) | (0.02) | |

| Standard Error of the Estimate | 0.22 | ||

| Durbin-Watson | 1.71 | ||

| F—Statistic | 569.82 *** | ||

| (0.00) | |||

| Constant | 0.20 |

*** means 0.01 level of significance. VIF—Variance Inflation Factor; CV—Coefficient Variance, Source: Author’s statistical information, 2022.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Omodero, C.O. Value-Added Tax Revenue Transfers and Regional Social Development: Evidence from Nigeria. Sustainability 2022, 14, 14343. https://doi.org/10.3390/su142114343

AMA Style

Omodero CO. Value-Added Tax Revenue Transfers and Regional Social Development: Evidence from Nigeria. Sustainability. 2022; 14(21):14343. https://doi.org/10.3390/su142114343

Chicago/Turabian StyleOmodero, Cordelia Onyinyechi. 2022. "Value-Added Tax Revenue Transfers and Regional Social Development: Evidence from Nigeria" Sustainability 14, no. 21: 14343. https://doi.org/10.3390/su142114343

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.