2. Terminology

Generally speaking, technical objects are the focus of involved in two different activities (phases): use—involving their production—and maintenance—oriented to their repair, inspection, service [

1]. Generally, use refers to any handling of a technical object when it is in an optimal operational condition. Therefore, use regards both when the machine is performing its functions and when, due to various circumstances (lack of production orders, waiting for raw material, retooling), it is not working [

2]. Maintenance, in turn, concerns dealing with unfit objects and includes not only the time spent on direct servicing and repair, but also that spent waiting for servicing or identifying the location of damage. The phase of use is therefore directly related to the performance of a production task, while maintenance is treated as an auxiliary process, which often means “I use the machine (I earn, produce), and you repair it (which will be costly)”. The result is a willingness to earn more (use, operate) income with less (maintenance) maintenance cost. It is of course possible (to some extent) to optimize the operation and maintenance, through activities based on the concepts of TPM (Total Productive Maintenance) and Lean Maintenance. A model that provides information for an effective implementation of TPM is reported in [

3]. This model considers different influences of Maintenance Prevention and Preventive Maintenance on the (OEE) Overall Equipment Effectiveness as the central performance measure of a maintenance system. Reference [

4] provides practical guidance on the type of TPM process which is suitable for different circumstances and in relation to specific strategic company objectives. A review of the literature on TPM and an overview of TPM implementation practices adopted by manufacturing organizations are presented in [

5]. There are also studies in which the authors try to assess the effectiveness of the implemented operation and maintenance solutions on the basis of dedicated maturity models [

6] and their improvement by implementing 5S or Lean Management [

7,

8,

9]. The importance of an efficient communication between processes implemented in an enterprise is also noticed. For example, Reference [

10] identifies and proposes a way of eliminating waste in information management processes through a value stream mapping (VSM)-based method.

Nevertheless, both of these activities mentioned above (operation and maintenance) are necessary and closely related not only to each other but also to other business processes, such as quality, logistics, SHE (Safety, Health, Environment), etc., as indicated below:

| [11] | Integrated strategies joining maintenance and quality. |

| [12] | Spare parts management as a function of maintenance management that aims to support maintenance activities, providing real-time information on the available quantities of each spare part and adopting the inventory policies that ensure their availability when required, minimizing costs. |

| [13] | Impacts and contributions of best practice maintenance toward sustainable manufacturing operations. |

| [14] | Model for supporting the design and assessment of business models with a sustainable perspective, by integrating a new business model canvas for sustainability (BMCS) and an evaluation method to assess it. |

| [15] | Joint production, maintenance, and dynamic sampling inspection control policy, for failure-prone manufacturing systems. |

This proves that the processes of using and maintaining technical objects are broad concepts and, in addition to technical activities, also include economic and organizational activities [

16,

17], which affect the financial, environmental and social perception of the company by stakeholders [

18,

19,

20].

According to Polish terminology, both academic and industrial, the combined processes of using and maintaining technical facilities are called the exploitation of technical objects and are defined as “a set of purposeful organizational, technical and economic activities of people regarding technical devices and the mutual relations between them from the moment of taking over some equipment for use as intended until its disposal after liquidation ”. The concept, therefore, refers to a wide range of actions at a certain stage in the life of a technical object (

Figure 1).

The word “exploitation” in English has rather different associations than in the described context of the Polish Standard. It is used rather in other contexts such as “exploitation of coal deposits, exploitation of natural resources”, and the term “operation” is used to describe the Polish meaning of the word “exploitation”. In fact, the Polish meaning of the word exploitation is wider and, in addition to “operation”, also includes “maintenance” and other activities (as the term terotechnology).

In the Polish nomenclature, exploitation is also defined as a science whose subject of research is the rational use of machines by man, while rational use is understood as effective and efficient. Effective—production processes effectively achieve the goals set for them—widely understood stakeholders are satisfied with the degree these processes meet their requirements and expectations.

In turn, the Anglo-Saxon nomenclature defines the concept of terotechnology as “a combination of management, finance, engineering and other practices applicable to physical assets in order to optimize their life cycle costs; deals with the design and construction of these assets to ensure their reliability and serviceability at the plant, machine, building equipment level at every life stage—installation, commissioning, use, maintenance, modification and replacement with performance and cost feedback”(BS 3811 “Glossary of maintenance management terms in terotechnology”). Also this definition—albeit more focused on the phases of constructing and designing objects—expresses the multidisciplinary physical asset management, which includes both technical administration and management aspects, referring to the assets itself and to all stakeholders and resources engaged into maintenance processes.

Of course, it is sometimes difficult to unequivocally qualify an action as purely technical or purely economic. An example may be the implementation of a strategy according to the technical condition that requires—in addition to conducting an economic profitability analysis—a number of technical activities (e.g., installation of measuring equipment on a machine) and organizational activities such as the employment of competent personnel (

Table 1).

Taking management decisions in a company, including those related to the operation and maintenance processes, is most often based on the management accounting system and a market data analysis [

21,

22,

23,

24].

According to the Institute of Management Accountants (2008) [

25], “Management Accounting is a profession that involves partnering in management decision making, devising planning and performance management systems, and providing expertise in financial reporting and control to assist management in the formulation and implementation of an organization’s strategy”. This definition indicates that the essence of these activities is rooted in two areas. On the one hand, it is about providing more predictive information, and on the other hand, it directs decision-makers towards a higher value.

Since all organizations face various resource and capacity constraints, all the activities that they perform have to be justified by clearly adding value [

26,

27,

28]. Most organizations of any significant size have a management accounting function, management accountants and management accounting tools [

25].

Issues in process approach issues regarding management accounting are not a new topic. An example is the Activity-Based Costing (ABC) method, which [

29] is presented as a tool, used for decades, that allows control in the production process through the location of indirect costs and cost drivers, which generate the cost of the product. A study [

30] describes the different product cost calculation models—as mentioned above, ABC, Time-Driven Activity-Based Costing (TDABC), Service-Based Costing (S-BC), Duration-Based Costing (DBC) and LEAN accounting. The authors of this publication conclude that the ABC model methodically justifies the allocation of indirect costs for each produced product but does not allocate them according to their relationship with production, sales, and administrative processes. LEAN does not focus on allocating indirect costs but requires adapting all corporate processes to the customer’s needs. S-BC responds to this LEAN principle.

There is no doubt, however, that the use of these methods is beneficial for enterprises. A study [

31] based on research in 339 SMEs showed a strong, statistical relationship between the performance of these enterprises and the management accounting information used.

Management accounting, as opposed to the more formalized financial accounting, was created for the internal purposes of an enterprise, and its purpose is to collect and analyze information allowing the management boards of this enterprise to make current and strategic decisions by (

Table 2).

According to [

33], the information provided through management accounting is necessary to achieve all managerial functions, providing the necessary data and information, including advice and recommendations.

The possibilities of using management accounting in the operation of machines and devices were presented in [

34]. In this study, the authors proposed a method of managing the maintenance of technical objects in a condition of serviceability by means of cost accounting, as well as a method of analyzing these costs. They also drew attention to the relationship between the unit costs of operation and the physical processes of wear taking place in the objects—expressed as the intensity of damage. Undoubtedly, there is close feedback between the operation of the operation system in the enterprise and management accounting—i.e., data from the operation system are one of the foundations of management accounting and decision making, which in turn determine the effectiveness and efficiency of the operation system [

35]. For example, an increase in the operating costs of an “old” technical facility may result in a decision to withdraw it from the system and replace it with a new one (or subject it to modernization). This, in turn, will reduce the operating costs and increase the operating efficiency.

3. Formulation of the Problem and Concept

Bearing in mind the definition of exploitation as a series of activities, not only technical, but also organizational and economic, one can ask whether information from the operation of the exploitation system can be one of the pillars of decision making concerning the entire enterprise. It is important that, at the moment “pure” maintenance, indicators such as those included in the standard EN 15341:2019, Maintenance—Maintenance Key Performance Indicators—are not considered [

36]. In other words, is it possible to propose such an architecture of the exploitation system and its effectiveness and efficiency indicators that will convey information not only about this process [

37], but also about other business processes carried out by the enterprise? Can the concepts of internal stakeholders of the exploitation system, i.e., other business processes implemented in enterprises, such as logistics, marketing, or human resource management, be proposed?

To solve the problem, the formal definition of the machine exploitation system (MES) was used, which is described by the formula:

where:

E—set of operating states (e) of the machine (the so-called exploitation repertoire),

D—set of machine exploitation locations (d) (exploitation base),

R—exploitation distribution,

G—exploitation graph (relations defined by E × E or D × D),

H—operational order.

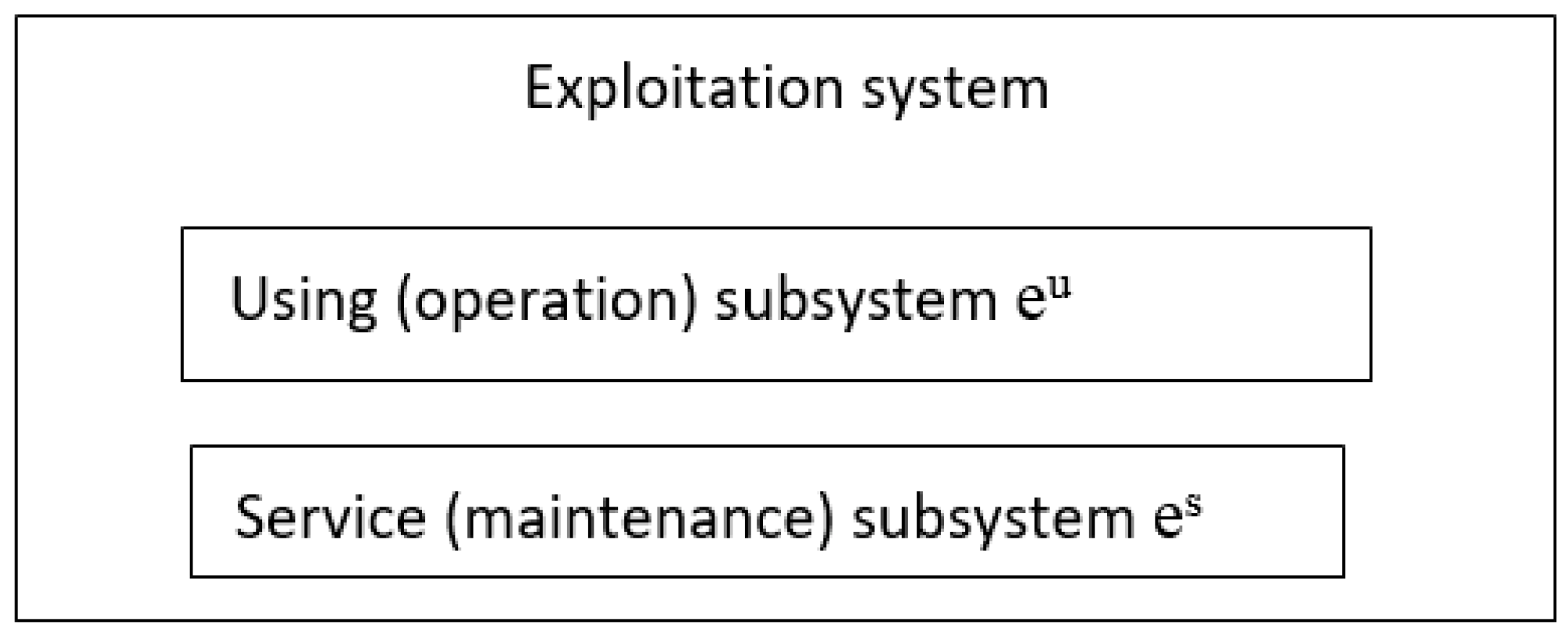

The operating state (e) is the state of an object defined by a set of values of its technical and/or economic characteristics, determined for an object at a given moment or in a specific period of time [

38]. The set of operating states (exploitation repertoire) includes—in the simplest case—two elements: state of use (e

u) and state of servicing (e

s) (

Figure 2).

where:

The exploitation system can also be considered as a territorial model, including elements of the exploitation base (D) spread over an area, for instance, d

1—workshop, d

2—production area, d

3—parking. Exploitation distribution (R) is a relation defined by the Cartesian product E × D as a set of exploitation chains), as shown in

Table 3.

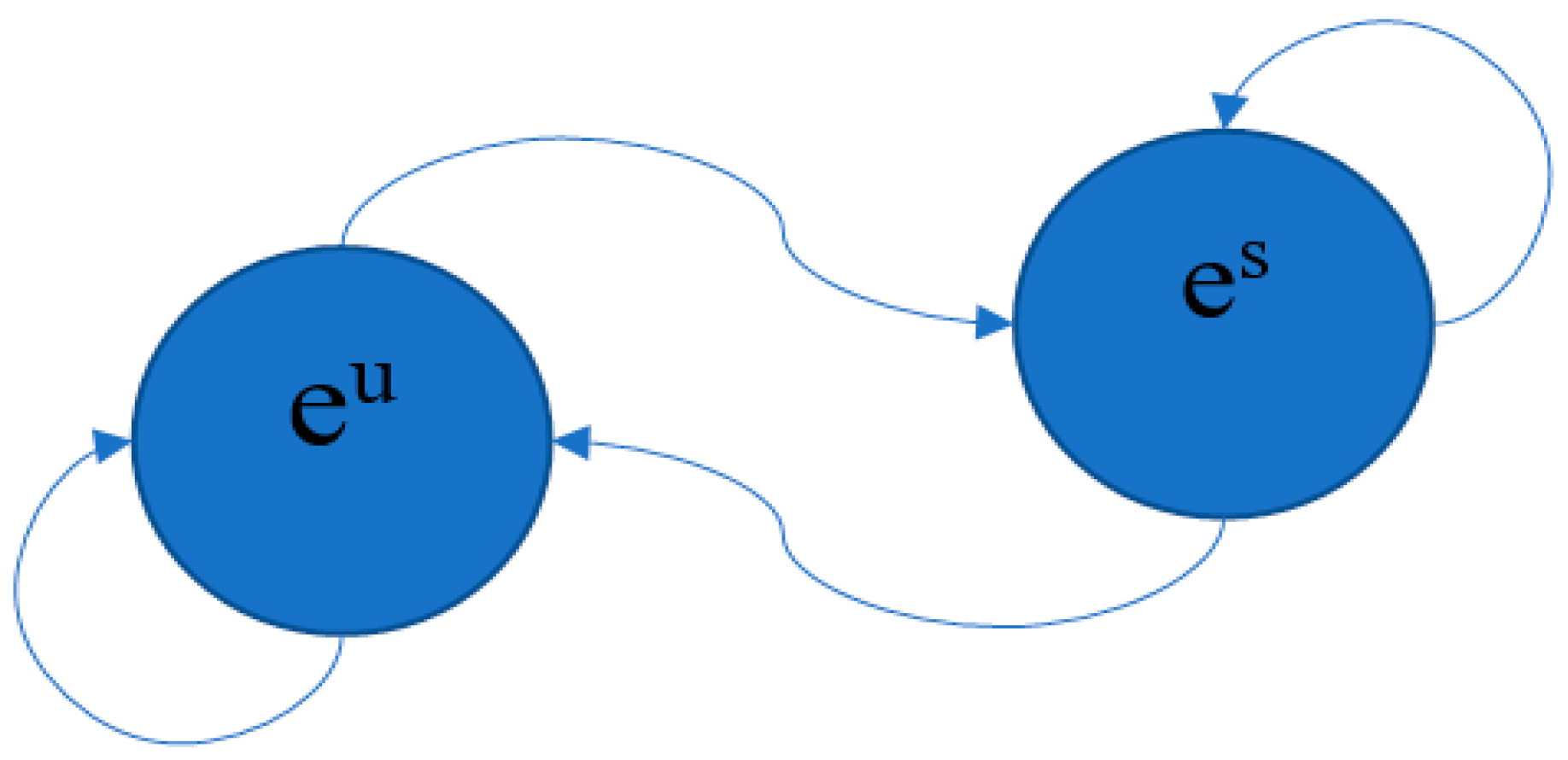

The exploitation graph (G) describes relations defined by E × E or D × D; it is a directed graph in which the nodes are exploitation states (or locations), and the arcs are possible transitions between states (or locations),

Figure 3.

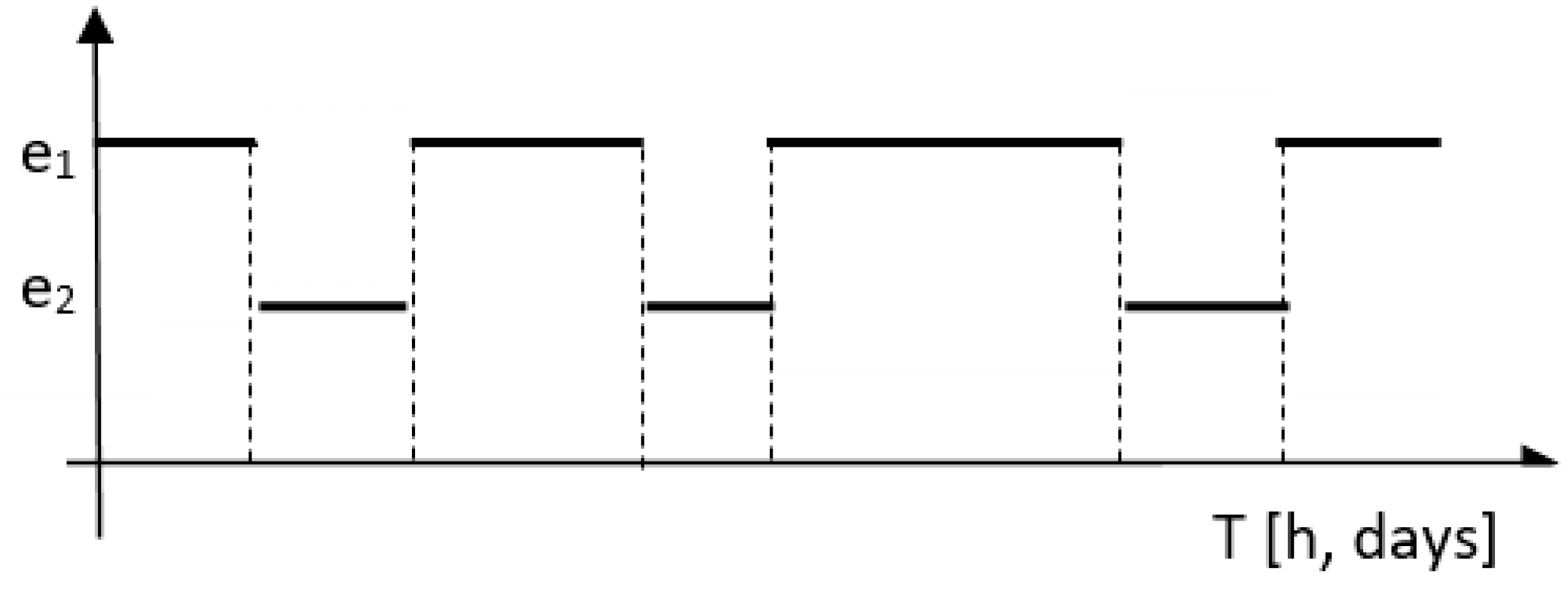

The operational order H describes relations establishing the sequence during the exploitation of a machine, as shown in

Figure 4.

Assuming the simplest, two-elements model of the exploitation system, it is possible to analyze the times (or related costs) the technical objects remain in the two subsystems. However, the number of indicators available is limited in this case. The two-state (use and maintenance) operation model is characterized by a clear division of the operating time into use and service time. It is relatively easy to determine the time T

u(t) the object stays in the operational state and the time T

0(t) it is in the service state for such a model. In practice, it is possible to determine various measures constructed using the functions T

u(t) and T

o(t), the most important of which are the availability index k

g expressed by the formula:

which is a measure of the availability of the object to meet the required functions, and the downtime indicator k

p, a measure of the lack of availability, expressed by formula:

These are undoubtedly important indicators from the technical point of view, as they inform about the “quality” of the technical condition of the object. From the economic point of view, however, this is only partial information, not saying anything, for example, about the rationality of purchasing and using this device. Therefore, such a simplified approach does not allow for deeper analyses, and the conclusions formulated on this basis may be even erroneous or at least ambiguous [

39]. If, for example, we compare the times the object remains in each of these states, and the result indicates an excessively long time of the object in the service system, the conclusion may concern both the failure rate of the object (technical aspect) and an improper organization of the service system (organizational aspect). However, by properly identifying the operational repertoire, the analyses can be more comprehensive and valuable.

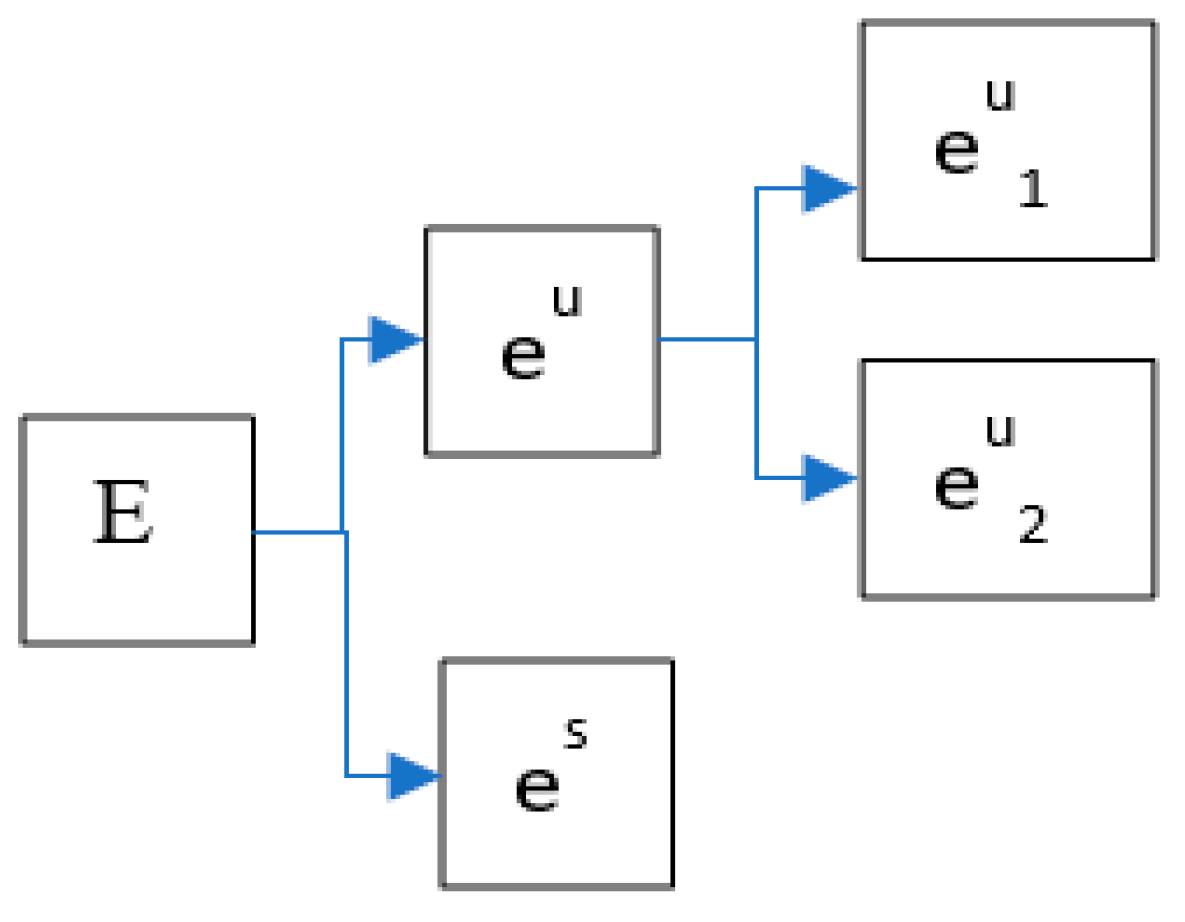

Let assume that the repertoire E of the exploitation system consists of three exploitation states (

Figure 5):

For such a three-state exploitation system, the following times can be specified:

Tu(t)—time of use of the object (operational state),

Tp(t)—downtime of the object (operational state),

To(t)—total service time of the object (maintenance state).

Apart from the availability ratio k

g (as for a two-state system), it is possible to determine the availability ratio k

g1, which takes into account the downtime of the object in the operational state:

and, additionally, the standstill indicator k

pt (object in the operational state):

or the indicator k

w:

which, from an economic point of view, determine the actual use of the given object, and therefore—in some way—the reason of its purchase and use.

If, in turn, it is assumed that the repertoire E of the exploitation system consists of five operational states:

where

—the object performs its functions,

—downtime—the object is waiting for use,

—downtime—the object (out of order) is serviced/under repair,

—downtime—the object (out of order) is waiting for service,

—downtime—object (out of order) is waiting for service–fault location,

it is possible to define the following times: T

oo(t)—waiting time for service, and T

lu(t)—fault localization time. Then, by defining and analyzing subsequent indicators, for example, the failure localization time indicator k

lk:

and the indicator of waiting time for service, k

oo:

more specific conclusions can be drawn. For example, a high value of the k

lk index may indicate a lack of competences of the workshop employees or a lack of appropriate equipment. In turn, a high value of the index k

oo may indicate a necessity to increase the number of service stations.

The conclusion is that management information concerning not only technical activities but also organizational and economic ones, can be obtained from an appropriately designed and implemented operating system, i.e., a system for which its repertoire is reasonably determined and for which appropriate time (or costs) measurements are made regarding the presence of the object in particular operating states.

4. An Example of Using Data from the Exploitation System to Make Management Decisions

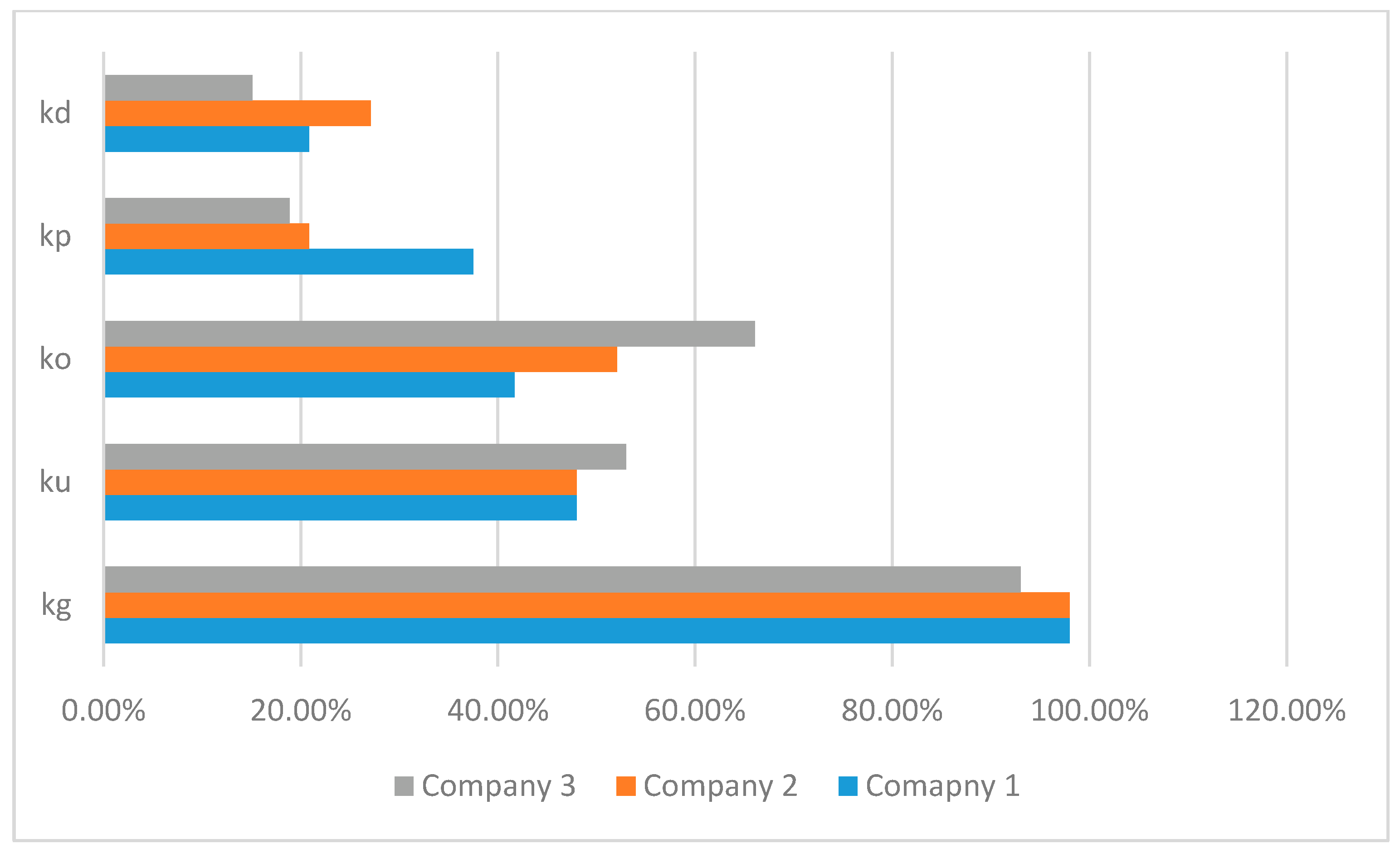

Three local taxi companies were offered the implementation of a virtual model of a five-state exploitation system:

where:

e1—driving with a client,

e2—driving after leaving the client,

e3—waiting for the client,

e4—driver’s rest,

e5—workshop service.

In each company, 15 drivers determined the (estimated) percentage share of the time their vehicles stayed in individual exploitation states (total 24 h). The research was conducted in the form of a questionnaire. The averaged results are presented in

Table 4.

The indicators of availability k

g (13), of use k

u (14), of waiting time k

o (15), of efficient work k

p (16) and of driving after leaving the client k

d (17) are defined as:

The comments of the owners of the surveyed enterprises and their suggestions for further actions are presented below.

Taxi Company 1 is a relatively new, but very buoyant corporation with a large marketing budget, a competitive pricing, and a relatively new fleet of vehicles. It is popular with the locals, because it offers short waiting times for the client and relatively more courses. Due to the technical condition of vehicles, the service in the workshop applies only to inspections and warranty services. A good navigation system, constantly updated maps and effective tools for assigning and planning the courses mean that the travel times to the customers are not long. The owner of this company is worried about the long idle time of his taxis due to the rest of the drivers.

Taxi company 2 is less competitive than company 1 in terms of price, the waiting times for the customers are longer and—as a consequence—the driving times with the customers are shorter. Due to the good technical condition of its vehicles, visits to the garage are also not very frequent. The owner of this company is worried about the fact that his taxis may not be in use for a long time, and the drivers will thus have a leisure time.

The taxi company 3 employs, in principle, drivers who earn extra money for their retirement with their not newest cars. Hence, this implies both shorter rest times and relatively long residence times in the subsystems. Due to the prices and technical condition of the vehicles, customers choose this corporation less often (hence, the relatively long waiting times). The short travel times to the customer are due to the fact that both the dispatcher and the drivers know the city’s transport schedule perfectly, and good relations between drivers (they do not compete with each other, as is the case in other companies) make them warn each other about obstructions on the road.

Table 6 shows the technical, economic and organizational factors affecting the efficiency of the operation of taxi companies, assuming the above-mentioned operation model.

As a result of the analysis of data obtained from the exploitation system, the entrepreneurs planned corrective actions. In company 1, it was decided to consider the joint use of a car by two drivers. Owner 2 also took this into account and also decided to perform intensive advertising and marketing and a review of the software (GPS, maps) and to carry out training on the topography and customer communication. Only in company 3 no activities were planned.

Similar studies were carried out in enterprises dealing with vehicle repair. For these companies, a three-state model of the exploitation system was proposed:

where:

ew1—repair,

ew2—diagnostics,

ew3—waiting for repair.

In this case, a questionnaire survey was also carried out, but this time among the companies’ owners, who determined the percentage share of the time spent by their customers’ vehicles in particular states (

Table 7).

The indicators of repair time k

n (19), diagnostic time k

d (20) and repair waiting time k

on (21) were defined:

The calculated values of the ratios are summarized in

Table 8.

The results of the research were presented to the owners of the individual companies on the basis of benchmarking indicators, i.e., they did not know the names of the other companies participating in the research.

Workshop 1—small (only one service station), but with a very competent mechanic-diagnostician. Due to its reliability and prices, its customers agree to longer waiting times for repairs.

Workshop 2—larger than the previous one, two service stations with more staff. The owner knows that the competences of the employees are not high, hence the long waiting times for diagnostics and fault location.

Table 9 presents the technical, economic and organizational factors influencing the effectiveness of the garage exploitation, assuming the above-mentioned operation model.

As a result of the analysis of data obtained from the system, the owner of workshop 1 decided to expand the company and hire a young worker to help an experienced mechanic. Workshops for employees were planned in workshop 2.

The presented research shows that properly collected information from the system of operation of technical facilities can be the basis for making decisions regarding the operation of the entire enterprise. However, this requires the design and implementation of an appropriate exploitation system with correctly identified exploitation states.

5. Conclusions

This paper shows that a properly designed exploitation system for technical objects can be a source of valuable data allowing for making management decisions of not only technical, but also organizational and economic nature. For this purpose, it is necessary to divide the exploitation system into a certain number of subsystems (exploitation states) and implement appropriate measurement of times, costs or other parameters related to the presence of a technical object in a given subsystem.

It has been shown that the simplest, two-state model of the exploitation system (operation and maintenance) limits the number of data that can be obtained, basically providing only information on the quality of the technical condition of the operated devices. Extending the model by introducing new states enables the acquisition of economic, organizational and even social data. However, it should be remembered that the more operating states are considered, the more data must be reliably collected and analyzed.

According to the authors, a novelty in this article is the presentation of the concept in which “non-technical” business processes (e.g., procurement, HR, marketing, training processes) are treated as stakeholders of technical processes (production and maintenance), and the effectiveness and efficiency of all processes can be assessed by analyzing the system of exploitation of technical objects. Putting the concept into practice is quite easy and intuitive. The managers of companies know perfectly well the exploitation states of their objects. Collecting data on the time or costs of their stay in given states is relatively easy and does not require deep economic knowledge, as in the ABC or Lean systems. Restrictions apply to the use of such a tool, which is generally applicable only to production and service companies and whose functioning is essentially based on the operation of technical facilities. Further research should concern two aspects:

- -

a direct comparison of the proposed method with classic tools (such as the aforementioned ABC), in terms of both labor intensity/implementation costs and operational efficiency;

- -

the implementation of the method in enterprises with a more complex organizational and process structure.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}