The Effect of Apparent and Intellectual Sustainability Independence on the Credibility Gap of the Accounting Information

, , and

, , and

Abstract

:1. Introduction

- Does the auditor’s apparent independence effect the credibility gap of information?

- Does the auditor’s intellectual independence affect the credibility gap of information?

2. Literature Review and Hypotheses Development

2.1. Credibility Gap of Information

2.2. Auditors’ Sustainable Independence

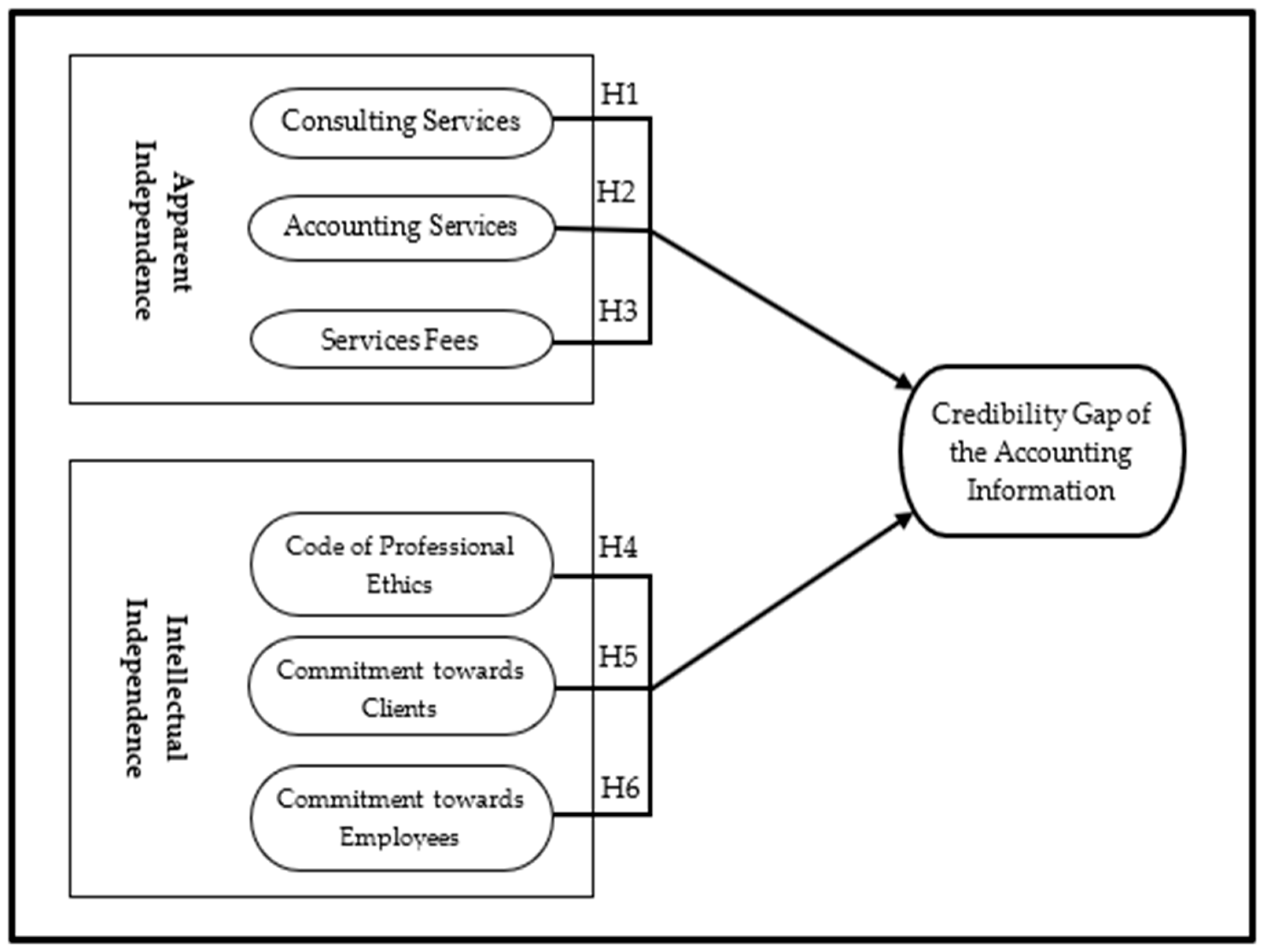

2.2.1. Apparent Independence

Consulting Services

Accounting Services

Services Fees

2.2.2. The Intellectual Independence

Code of Professional Ethics

Commitment toward Clients

Commitment toward Employees

3. Research Methodology

3.1. Study Tool, Design and Sections

3.2. Statistical Descriptive

4. Research Analysis

- Constant predictors: apparent independence and intellectual independence.

- Dependent variable: credibility gap of information.

4.1. Apparent Independence

4.2. Intellectual Independence

5. Research Discussion

6. Research Limitations

7. Research Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Variables and Their Related Measurement Items

| No. | Independent Variables (Apparent Independence) | Mean | SD | Level |

|---|---|---|---|---|

| Consulting Services | ||||

| 1 | Auditing office offers consulting and managerial services if there are common interests with the company’s management. | 3.76 | 1.94 | High |

| 2 | Auditing office offers consulting and managerial services if there are personal relations with the client. | 3.54 | 1.88 | Medium |

| 3 | Auditing office offers consulting and managerial services for the same company whose its accounts it audits. | 3.67 | 1.92 | Medium |

| 4 | Auditing office offers the client a tax return provided that the office obtains a percentage of tax savings. | 4.11 | 2.03 | High |

| 5 | The auditor invests in the shares of the company whose accounts she/he audits. | 4.01 | 2.00 | High |

| 6 | Having a financial relation between auditing office members of his/her household and the client affects the auditor’s sustainable independence. | 4.04 | 2.01 | High |

| 7 | Clients, who promote some auditing offices and services they offer, affect the auditor’s sustainable independence. | 3.54 | 1.88 | Medium |

| 8 | Competition between auditing offices in offering consulting and managerial services affects the auditor’s sustainable independence. | 3.76 | 1.94 | High |

| Total | 3.80 | 1.95 | High | |

| Accounting Services | ||||

| 9 | The acquaintance of the external auditor with international accounting and auditing standards and the code of professional ethics affects the auditor’s sustainable independence and neutrality. | 3.49 | 1.87 | Medium |

| 10 | The ambition of the external auditor in conducting auditing assignments for the same companies annually affects his/her sustainable independence. | 3.07 | 1.75 | Medium |

| 11 | The external auditor’s auditing of financial lists for several subsequent years leads to acquiring new abilities and skills that strengthen his/her sustainable independence and neutrality. | 4.19 | 2.05 | High |

| 12 | The external auditor’s auditing of financial lists for several subsequent years leads to lowering auditing fees which strengthen his/her sustainable independence. | 3.25 | 1.80 | Medium |

| 13 | Devoting of the external auditor to the profession of auditing leads to promoting his/her success, sustainable independence and neutrality. | 3.41 | 1.85 | Medium |

| 14 | Sufficient and specialized knowledge of the external auditor in the fields of accounting and auditing leads to practicing it in all cases and circumstances. | 2.8 | 1.67 | Medium |

| 15 | Both dependence and incompetence of the external auditor affect negatively the opinion that he/she will express in his/her report. | 4.38 | 2.09 | High |

| Total | 3.51 | 1.87 | Medium | |

| Service Fees | ||||

| 16 | Competition between auditing offices affects selecting services fees. | 4.31 | 2.08 | High |

| 17 | There is an objectively fair base for selecting auditing fees in the companies. | 4.30 | 2.08 | High |

| 18 | Selecting auditing fees affects the auditor’s behavior, proficiency and sustainable independence. | 4.19 | 2.05 | High |

| 19 | Reputation and size of the auditing office affects selecting auditing fees. | 3.41 | 1.85 | Medium |

| 20 | The difficulty of auditing and the degree of complexity affect the required fees. | 3.1 | 1.76 | Medium |

| 21 | Using technology in companies affects the required fees. | 4.24 | 2.06 | High |

| 22 | The integrity of the internal observation system in companies affects the required fees. | 4.1 | 2.02 | High |

| 23 | The time of auditing affects the required fees. | 3.78 | 1.94 | High |

| 24 | The quality of the report issued from the auditing office affects selecting the required fees. | 3.69 | 1.92 | High |

| Total | 3.90 | 1.97 | High | |

| No. | Independent Variables (Intellectual Independence) | Mean | SD | Level |

| 25 | The ethics of the profession affects the auditor’s treatment of colleagues, clients and employees. | 3.65 | 1.91 | Medium |

| 26 | The CPA accepts presents and gifts before, during and after auditing to the company of auditing. | 3.06 | 1.75 | Medium |

| 27 | The deterrent procedures imposed on the auditors who violate the ethical standards of the profession affect their sustainable independence. | 3.95 | 1.99 | High |

| 28 | In the law of practicing the profession, there is nothing that prevents implementing the system of selecting conditioned fees. | 2.66 | 1.63 | Medium |

| 29 | In the law of practicing the profession, there is no clause which prevents implementing the system of revising the opposite, (an auditor who checks his colleague’s commitments and auditing works). | 3.17 | 1.78 | Medium |

| 30 | The size of the auditing office affects its auditors’ proficiency and their commitment to the work behavior. | 3.14 | 1.77 | Medium |

| 31 | The size of the auditing office affects its auditors’ proficiency and their capability of resisting work pressures. | 2.69 | 1.64 | Medium |

| Total | 3.18 | 1.78 | Medium | |

| Commitment toward Clients | ||||

| 32 | When accepting auditing, there should not be any relatives of the auditor in the company under auditing. | 3.69 | 1.92 | High |

| 33 | When working on auditing, having impartiality at the auditing office leads to promoting the auditor’s sustainable independence. | 3.84 | 1.96 | High |

| 34 | When working on auditing, having impartiality at the auditing office leads to promoting the auditor’s sustainable independence. | 4.33 | 2.08 | High |

| 35 | When working on auditing, having credibility at the auditing office leads to promoting the auditor’s sustainable independence. | 4.6 | 2.14 | High |

| 36 | When working on auditing, having objectivity in the decisions made at the auditing office leads to promoting the auditor’s sustainable independence. | 4.53 | 2.13 | High |

| 37 | When working on auditing, the auditing office takes personal precautions to guarantee sustainable independence. | 4.48 | 2.12 | High |

| 38 | Although there are many pressures, the auditing office is able to make its decisions. | 4.61 | 2.15 | High |

| 39 | The auditor doubts the financial data under auditing till the opposite emerges. | 4.4 | 2.09 | High |

| 40 | It is not preferable for the auditor to build relationships with the clients. | 4.45 | 2.11 | High |

| Total | 4.32 | 2.08 | High | |

| Commitment toward employees | ||||

| 41 | The relationship between the auditor and employees is characterized by equality and fairness. | 4.15 | 2.04 | High |

| 42 | The auditor deals clearly in terms of providing employees with their salaries and rewards that suit their work. | 3.77 | 1.94 | High |

| 43 | The auditor deals honestly with employees regarding the company’s operations and financial situation. | 4.27 | 2.07 | High |

| 44 | The auditor allows the employees to criticize the company’s management without being afraid of Punishment. | 4.1 | 2.02 | High |

| 45 | The auditor ensures that companies offer health care services to its employees in accordance with the law. | 4.18 | 2.04 | High |

| 46 | The auditor ensures that companies offer services of insurance and retirement to its employees in accordance with the law. | 3.79 | 1.95 | High |

| 47 | The auditor ensures that companies offer services and courses related to technology to its employees. | 3.68 | 1.92 | High |

| Total | 3.99 | 1.99 | High | |

| No. | Dependent Variables (Credibility Gap) | Mean | SD | Level |

| 48 | Inadequacy of information in the financial lists to meet the needs of its users. | 4.14 | 2.03 | High |

| 49 | Lack of disclosing information to the decision makers in the suitable time. | 3.18 | 1.78 | Medium |

| 50 | Lack of submitting information, which is credible, neutral and free from bias. | 4.21 | 2.05 | High |

| 51 | Incapability of ascertaining the information that can be depended on. | 4.07 | 2.02 | High |

| 52 | Lack of true representation of the reported phenomena and information. | 4.07 | 2.02 | High |

| 53 | Unavailability of feedback which contributes to improving and developing the quality of information submitted to the decision makers. | 3.94 | 1.98 | High |

| 54 | Incredibility of the submitted information. | 4.05 | 2.01 | High |

| 55 | Incapability of predicting the future and recognizing deviations, its places and its reasons and treating them. | 3.95 | 1.99 | High |

| 56 | Not having the characteristic of the appropriate time in the submitted information. | 3.98 | 1.99 | High |

| 57 | Not having the features of competence, efficiency and comprehensiveness in the information submitted by the CPA. | 3.93 | 1.98 | High |

| 58 | Reducing opportunities to make mistakes and cheating in the data submitted by the CPA. | 4.05 | 2.01 | High |

| 59 | Inadequacy in allowing the horizons of observation on the operations and providing information to support decision making. | 3.95 | 1.99 | High |

| Total | 3.68 | 1.92 | High | |

References

- Al-Okaily, M. Assessing the effectiveness of accounting information systems in the era of COVID-19 pandemic. VINE J. Inf. Knowl. Manag. Syst. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Roussy, M.; Barbe, O.; Raimbault, S. Internal audit: From effectiveness to organizational significance. Manag. Audit. J. 2020, 35, 322–342. [Google Scholar] [CrossRef]

- Aws, A.L.; Ping, T.A.; Al-Okaily, M. Towards business intelligence success measurement in an organization: A conceptual study. J. Syst. Manag. Sci. 2021, 11, 155–170. [Google Scholar]

- Argento, D.; Umans, T.; Håkansson, P.; Johansson, A. Reliance on the internal auditors’ work: Experiences of Swedish external auditors. J. Manag. Control 2018, 29, 295–325. [Google Scholar] [CrossRef] [Green Version]

- Alsmadi, A.A.; Shuhaiber, A.; Alhawamdeh, L.N.; Alghazzawi, R.; Al-Okaily, M. Twenty Years of Mobile Banking Services Development and Sustainability: A Bibliometric Analysis Overview (2000–2020). Sustainability 2022, 14, 10630. [Google Scholar] [CrossRef]

- Price Waterhouse Coopers. Global Economic Crime Survey 2011. Available online: Pwc.com/us/en/forensic-services/publications/global-economic-crime-survey-2011.jhtml (accessed on 15 December 2021).

- AL-Khatib, A.W. Can Big Data Analytics Capabilities Promote a Competitive Advantage? Green Radical Innovation, Green Incremental Innovation and Data-Driven Culture in a Moderated Mediation Model. Bus. Process Manag. J. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Al-Omoush, K.S.; Al Attar, M.K.; Saleh, I.H.; Alsmadi, A.A. The drivers of E-banking entrepreneurship: An empirical study. Int. J. Bank Mark. 2019, 38, 485–500. [Google Scholar] [CrossRef]

- Sweeney, B.; Pierce, B. Management control in audit firms: A qualitative examination. Account. Audit. Account. J. 2004, 17, 779–812. [Google Scholar] [CrossRef]

- Jelinek, R.; Jelinek, K. Auditors gone wild: The ‘other’ problem in public accounting. Bus. Horiz. 2008, 51, 223–233. [Google Scholar] [CrossRef]

- Knechel, R. The business risk audit: Origins, obstacles and opportunities. Account. Organ. Soc. 2007, 32, 383–408. [Google Scholar] [CrossRef]

- Chen, Q.; Kelly, K.; Salterio, S.E. Do changes in audit actions and attitudes consistent with increased auditor skepticism deter aggressive earnings management? An experimental investigation. Account. Organ. Soc. 2012, 37, 95–115. [Google Scholar] [CrossRef]

- Wainberg, J.S.; Kida, T.; Piercey, M.D.; Smith, J.F. The impact of anecdotal data in regulatory audit firm inspection reports. Account. Organ. Soc. 2013, 38, 621–636. [Google Scholar] [CrossRef]

- Bennett, G.B.; Hatfield, R.C. Staff auditors’ proclivity for computer-mediated communication with clients and its effect on skeptical behavior. Account. Organ. Soc. 2018, 68, 42–57. [Google Scholar] [CrossRef]

- Amiruddin, A. Mediating effect of work stress on the influence of time pressure, work–family conflict and role ambiguity on audit quality reduction behavior. Int. J. Law Manag. 2019, 61, 434–454. [Google Scholar] [CrossRef]

- Al-Okaily, A.; Al-Okaily, M.; Teoh, A.P. Evaluating ERP systems success: Evidence from Jordanian firms in the age of the digital business. VINE J. Inf. Knowl. Manag. Syst. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Paino, H.; Smith, M.; Ismail, Z. Auditor acceptance of dysfunctional behaviour. J. Appl. Account. Res. 2012, 13, 37–55. [Google Scholar] [CrossRef]

- Daoust, L.; Malsch, B. How ex-auditors remember their past: The transformation of audit experience into cultural memory. Account. Organ. Soc. 2019, 77, 101050. [Google Scholar] [CrossRef]

- Ikpor, I.M.; Bracci, E.; Kanu, C.I.; Ievoli, R.; Okezie, B.; Mlanga, S.; Ogbaekirigwe, C. Drivers of Sustainability Accounting and Reporting in Emerging Economies: Evidence from Nigeria. Sustainability 2022, 14, 3780. [Google Scholar] [CrossRef]

- Kwakye, T.O.; Welbeck, E.E.; Owusu, G.M.Y.; Anokye, F.K. Determinants of intention to engage in Sustainability Accounting & Reporting (SAR): The perspective of professional accountants. Int. J. Corp. Soc. Responsib. 2018, 3, 11. [Google Scholar]

- Al-Okaily, M.; Al-Okaily, A. An Empirical Assessment of Enterprise Information Systems Success in a Developing Country: The Jordanian Experience. TQM J. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Nehme, R. Performance evaluation of auditors: A constructive or a destructive tool of audit output. Manag. Audit. J. 2017, 32, 215–231. [Google Scholar] [CrossRef]

- Hatfield, R.C.; Mullis, C. Negotiations between auditors and their clients regarding adjustments to the financial statements. Bus. Horiz. 2015, 58, 203–208. [Google Scholar] [CrossRef]

- Engelbrecht, L.; Yasseen, Y.; Omarjee, I. The role of the internal audit function in integrated reporting: A developing economy perspective. Meditari Account. Res. 2018, 26, 657–674. [Google Scholar] [CrossRef]

- Abdelhak, E.E.; Elamer, A.A.; AlHares, A.; McLaughlin, C. Auditors’ ethical reasoning in developing countries: The case of Egypt. Int. J. Ethics Syst. 2019, 35, 558–583. [Google Scholar] [CrossRef]

- Astami, E.W.; Rusmin, R.; Hartadi, B.; Evans, J. The role of audit quality and culture influence on earnings management in companies with excessive free cash flow: Evidence from the Asia-Pacific region. Int. J. Account. Inf. Manag. 2017, 25, 21–42. [Google Scholar] [CrossRef]

- Fossung, M.F.; Mukah, S.T.; Berthelo, K.W.; Nsai, M.E. The Demand for External Audit Quality: The Contribution of Agency Theory in the Context of Cameroon. Account. Finance Res. 2022, 11, 1–13. [Google Scholar] [CrossRef]

- Pham, A.V.; Pham, M.H.; Truong, C. Audit Quality: An Analysis of Audit Partner Cultural Proximity to Client Executives. Eur. Account. Rev. 2022, 1–33. [Google Scholar] [CrossRef]

- Toumeh, A.A.; Yahya, S.; Siam, W.Z. Expectations gap between auditors and user of financial statements in the audit process: An auditors’ perspective. Asia-Pac. Manag. Account. J. 2018, 13, 79–107. [Google Scholar]

- Al-Qudah, A.A.; Hamdan, A.; Al-Okaily, M.; Alhaddad, L. The impact of green lending on credit risk: Evidence from UAE’s banks. Environ. Sci. Pollut. Res. 2022. [Google Scholar] [CrossRef]

- Mahdavi, G.; Daryaei, A.A. Attitude toward auditing, marketing and corporate governance (An examination based in Parsons’ social action theory). Int. J. Corp. Soc. Responsib. 2016, 1, 7. [Google Scholar] [CrossRef] [Green Version]

- Waples, E.; Shaub, M.K. Establishing an ethic of accounting: A response to Westra’s call for government employment of auditors. J. Bus. Ethics 1991, 10, 385–393. [Google Scholar] [CrossRef]

- Keeffe, A.J. When Accountants Fall into the Credibility Gap. Am. Bar Assoc. J. 1975, 61, 993–994. [Google Scholar]

- Saudagaran, S.M. International Accounting: A User Perspective; CCH: Chicago, IL, USA, 2009. [Google Scholar]

- Shahzad, F.; Rehman, I.U.; Hanif, W.; Asim, G.A.; Baig, M.H. The influence of financial reporting quality and audit quality on investment efficiency: Evidence from Pakistan. Int. J. Account. Inf. Manag. 2019, 27, 600–614. [Google Scholar] [CrossRef]

- Hsueh, J.W.J. Governance structure and the credibility gap: Experimental evidence on family businesses’ sustainability reporting. J. Bus. Ethics 2018, 153, 547–568. [Google Scholar] [CrossRef]

- Norman, C.S.; Rose, J.M.; Suh, I.S. The effects of disclosure type and audit committee expertise on chief audit executives’ tolerance for financial misstatements. Account. Organ. Soc. 2011, 36, 102–108. [Google Scholar] [CrossRef]

- Ariail, D.L.; Smith, K.T.; Smith, L.M. Do United States accountants’ personal values match the profession’s values (ethics code)? Account. Audit. Account. J. 2020, 33, 1047–1075. [Google Scholar] [CrossRef]

- Emett, S.A.; Libby, R.; Nelson, M.W. PCAOB guidance and audits of fair values for Level 2 investments. Account. Organ. Soc. 2018, 71, 57–72. [Google Scholar] [CrossRef]

- Arar, S.H. To What Extent Do External Auditors in Jordan Comply with Tests and Procedures in Evaluating Risks of Fundamental Errors in Auditing Financial Statements. Master’s Thesis, MEU, Amman, Jordan, 2009. [Google Scholar]

- May-Amy, Y.C.; Han-Rashwin, L.Y.; Carter, S. Antecedents of company secretaries’ behaviour and their relationship and effect on intended whistleblowing. Corp. Gov. Int. J. Bus. Soc. 2020, 20, 837–861. [Google Scholar] [CrossRef]

- Svanberg, J.; Öhman, P. Auditors’ time pressure: Does ethical culture support audit quality? Manag. Audit. J. 2013, 28, 572–591. [Google Scholar] [CrossRef]

- Lindberg, D.L.; Beck, F.D. Before and after Enron: CPAs’ views on auditor independence. CPA J. 2004, 74, 36. [Google Scholar]

- Khalil, M.; Ozkanc, A.; Yildiz, Y. Foreign institutional ownership and demand for accounting conservatism: Evidence from an emerging market. Rev. Quant. Finance Account. 2019, 55, 1–27. [Google Scholar] [CrossRef] [Green Version]

- Fontaine, R.; Khemakhem, H.; Herda, D.N. Audit committee perspectives on mandatory audit firm rotation: Evidence from Canada. J. Manag. Gov. 2016, 20, 485–502. [Google Scholar] [CrossRef]

- Al-Khadash, H.A.; Khasawneh, A.Y. The effects of the fair value Option under IAS 40 on the volatility of earnings. J. Appl. Finance Bank. 2014, 4, 95. [Google Scholar]

- Al-Khatib, A.W.; Al-ghanem, E.M. Radical innovation, incremental innovation, and competitive advantage, the moderating role of technological intensity: Evidence from the manufacturing sector in Jordan. Eur. Bus. Rev. 2022, 34, 344–369. [Google Scholar] [CrossRef]

- Abdul, W.E.A.; Majid, W.Z.N.A.; Harymawan, I.; Agustia, D. Characteristics of auditors’ non-audit services and accruals quality in Malaysia. Pac. Account. Rev. 2020, 32, 147–175. [Google Scholar] [CrossRef]

- Bala, H.; Amran, N.A.; Shaari, H. Audit committee attributes and cosmetic accounting in Nigeria. Manag. Audit. J. 2019, 35, 177–206. [Google Scholar] [CrossRef]

- Chen, K.Y.; Elder, R.J.; Liu, J.L. Auditor independence, audit quality and auditor-client negotiation outcomes: Some evidence from Taiwan. J. Contemp. Account. Econ. 2005, 1, 119–146. [Google Scholar] [CrossRef]

- Mertzanis, C.; Balntas, V.; Pantazopoulos, T. Internal auditor perceptions of corporate governance in Greece after the crisis. Qual. Res. Account. Manag. 2019, 17, 201–227. [Google Scholar] [CrossRef]

- Steinbart, P.J.; Raschke, R.L.; Gal, G.; Dilla, W.N. The influence of a good relationship between the internal audit and information security functions on information security outcomes. Account. Organ. Soc. 2018, 71, 15–29. [Google Scholar] [CrossRef] [Green Version]

- Hamdallah, M. The reliance of external auditors on the work performed by internal auditors and its impact on audit on banks: A case of the first Abu Dhabi Bank, UAE. Икoнoмикa и Уnpaвлeниe 2020, 17, 68–80. [Google Scholar]

- Hoopes, J.L.; Merkley, K.J.; Pacelli, J.; Schroeder, J.H. Audit personnel salaries and audit quality. Rev. Account. Stud. 2018, 23, 1096–1136. [Google Scholar] [CrossRef]

- Hammami, A.; Moldovan, R.; Peltier, E. Salary perception and career prospects in audit firms. Manag. Audit. J. 2020, 35, 759–793. [Google Scholar] [CrossRef]

- Schneider, A. Is investment decision-making influenced by perceptions relating to auditors’ client dependence and amount of audit fees? Adv. Account. 2011, 27, 75–80. [Google Scholar] [CrossRef]

- Mao, J.; Ettredge, M.; Stone, M. Group audits: Are audit quality and price associated with the Lead auditor’s decision to accept responsibility? J. Account. Public Policy 2020, 39, 106718. [Google Scholar] [CrossRef]

- Chang, Y.T.; Stone, D.N. Proposal readability, audit firm size and engagement success. Manag. Audit. J. 2019, 34, 871–894. [Google Scholar] [CrossRef]

- Nehme, R.; AlKhoury, C.; Al Mutawa, A. Evaluating the performance of auditors: A driver or a stabilizer of auditors’ behaviour. Int. J. Product. Perform. Manag. 2019, 69, 1999–2019. [Google Scholar] [CrossRef]

- Al-Khadash, H.E.; Al-Sartawi, M.S. The Capability of Sarbanes-Oxley Act in Enhancing the Independence of the Jordanian Certified Public Accountant and its Impact on Reducing the Audit Expectation Gap—An Empirical Investigation from the Perspectives of Auditors and Institutional Investors. Jordanian J. Bus. Adm. 2010, 6, 294–316. [Google Scholar]

- Olojede, P.; Erin, O.; Asiriuwa, O.; Usman, M. Audit expectation gap: An empirical analysis. Future Bus. J. 2020, 6, 10. [Google Scholar] [CrossRef]

- Srouji, A.F.; Ab Halim, M.S.; Lubis, Z.; Hamdallah, M.E. International standards as corporate governance mechanisms and credibility gap in Jordan: Financial managers’ point of view. Int. Bus. Manag. 2016, 10, 751–758. [Google Scholar]

- IFAC. Code of Ethics. Available online: https://www.ifac.org/system/files/publications/files/ifac-code-of-ethics-for.pdf (accessed on 24 July 2022).

- Saiewitz, A.; Kida, T. The effects of an auditor’s communication mode and professional tone on client responses to audit inquiries. Account. Organ. Soc. 2018, 65, 33–43. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, M. The impact of ex-auditors’ employment with audit clients on perceptions of auditor independence. Procedia-Soc. Behav. Sci. 2015, 172, 479–486. [Google Scholar] [CrossRef] [Green Version]

- Yang, L.; Ruan, L.; Tang, F. The impact of disclosure level and client incentive on auditors’ judgments of related party transactions. Int. J. Account. Inf. Manag. 2020, 28, 717–737. [Google Scholar] [CrossRef]

- Maresch, D.; Aschauer, E.; Fink, M. Competence trust, goodwill trust and negotiation power in auditor-client relationships. Account. Audit. Account. J. 2019, 33, 335–355. [Google Scholar] [CrossRef]

- Loke, C.H.; Ismail, S.; Fatima, A.H. Validation of Arnaud’s ethical climate index by public sector auditors in Malaysia. Int. J. Ethics Syst. 2019, 35, 345–358. [Google Scholar] [CrossRef]

- Srouji, A.F.; Abed, S.R.; Hamdallah, M.E. Banks performance and customers’ satisfaction in relation to corporate social responsibility: Mediating customer trust and spiritual leadership: What counts! Int. J. Bus. Innov. Res. 2019, 19, 358–384. [Google Scholar] [CrossRef]

- Hamdallah, M.E.; Srouji, A.F.; Abed, S.R. The Nexus between Reducing Audit Report Lags and Divining Integrated Financial Report Governance Disclosures: Should ASE Directives be More Conspicuous? Afro-Asian J. Financ. Account. 2021, 11, 81–103. [Google Scholar] [CrossRef]

- Taamneh, A.M.; Taamneh, M.; Alsaad, A.; Al-Okaily, M. Talent management and academic context: A comparative study of public and private universities. EuroMed J. Bus. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Perreault, S.; Kida, T. The relative effectiveness of persuasion tactics in auditor–client negotiations. Account. Organ. Soc. 2011, 36, 534–547. [Google Scholar] [CrossRef]

- Bitbol-Saba, N.; Dambrin, C. It’s not often we get a visit from a beautiful woman! The body in client-auditor interactions and the masculinity of accountancy. Crit. Perspect. Account. 2019, 64, 102068. [Google Scholar] [CrossRef]

- Knechel, W.R.; Thomas, E.; Driskill, M. Understanding financial auditing from a service perspective. Account. Organ. Soc. 2020, 81, 101080. [Google Scholar] [CrossRef]

- Available online: https://www.jiec.com/en (accessed on 12 January 2022).

- Nabil, B.; Srouji, A.; Abu Zer, A. Gender stereotyping in accounting education, why few female students choose accounting. J. Educ. Bus. 2021, 97, 542–554. [Google Scholar] [CrossRef]

- Mahadin, B.K.; Akroush, M.N. A study of factors affecting word of mouth (WOM) towards Islamic banking (IB) in Jordan. Int. J. Emerg. Mark. 2019, 14, 639–667. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Bougie, R.; Sekaran, U. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2019. [Google Scholar]

- He, L.J.; Chen, J. Does Mandatory Audit Partner Rotation Influence Auditor Selection Strategies? Sustainability 2021, 13, 2058. [Google Scholar] [CrossRef]

- Al-Thunaibat, A.A. Auditing of Accounts in the Light of International Auditing Standards and Local Laws and Regulations: Theory and Practice, 6th ed.; Wael for Printing, Publishing and Distribution: Cairo, Egypt, 2017. [Google Scholar]

- Bhandari, A.; Golden, J.; Thevenot, M. CEO political ideologies and auditor-client contracting. J. Account. Public Policy 2020, 39, 106755. [Google Scholar] [CrossRef]

- Ettredge, M.; Fuerherm, E.E.; Li, C. Fee pressure and audit quality. Account. Organ. Soc. 2014, 39, 247–263. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Alghazzawi, R.; Alkhwaldi, A.F.; Al-Okaily, A. The effect of digital accounting systems on the decision-making quality in the banking industry sector: A mediated-moderated model. Glob. Knowl. Mem. Commun. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Bills, K.L.; Cobabe, M.; Pittman, J.; Stein, S.E. To share or not to share: The importance of peer firm similarity to auditor choice. Account. Organ. Soc. 2020, 83, 101115. [Google Scholar] [CrossRef]

- Koh, K.; Rajgopal, S.; Srinivasan, S. Non-audit services and financial reporting quality: Evidence from 1978 to 1980. Rev. Account. Stud. 2013, 18, 1–33. [Google Scholar] [CrossRef]

- Mande, V.; Son, M. How do auditor fees affect accruals quality? Additional evidence. Int. J. Audit. 2015, 19, 238–251. [Google Scholar] [CrossRef]

- Lim, C.; Ding, D.; Charoenwong, C. Non-audit fees, institutional monitoring, and audit quality. Rev. Quant. Finance Account. 2013, 41, 343–384. [Google Scholar] [CrossRef]

- Yamada, A.; Fujita, K. Impact of Parent Companies and Multiple Large Shareholders on Audit Fees in Stakeholder-Oriented Corporate Governance. Sustainability 2022, 14, 5534. [Google Scholar] [CrossRef]

- Xin, C.; Hao, X.; Cheng, L. Do Environmental Administrative Penalties Affect Audit Fees? Results from Multiple Econometric Models. Sustainability 2022, 14, 4268. [Google Scholar] [CrossRef]

- Svanberg, J.; Öhman, P. Auditors’ identification with their clients: Effects on audit quality. Br. Account. Rev. 2015, 47, 395–408. [Google Scholar] [CrossRef]

- Chang, W.C.; Chen, J.P. Auditor sanction and reputation damage: Evidence from changes in non-client-company directorships. Br. Account. Rev. 2020, 52, 100894. [Google Scholar] [CrossRef]

- Booker, K. Can clients of economically dependent auditors benefit from voluntary audit firm rotation? An experiment with lenders. Res. Account. Regul. 2018, 30, 63–67. [Google Scholar] [CrossRef]

- Chen, Y.; Gul, F.A.; Truong, C.; Veeraraghavan, M. Auditor client specific knowledge and internal control weakness: Some evidence on the role of auditor tenure and geographic distance. J. Contemp. Account. Econ. 2016, 12, 121–140. [Google Scholar] [CrossRef]

- Liu, A.A. Trainee auditors’ perception of ethical climate and workplace bullying in Chinese audit firms. Asian J. Account. Res. 2020, 5, 63–79. [Google Scholar] [CrossRef]

- Al-Bashayreh, M.; Almajali, D.; Altamimi, A.; Masa’deh, R.E.; Al-Okaily, M. An Empirical Investigation of Reasons Influencing Student Acceptance and Rejection of Mobile Learning Apps Usage. Sustainability 2022, 14, 4325. [Google Scholar] [CrossRef]

- Sian, S.; Agrizzi, D.; Wright, T.; Alsalloom, A. Negotiating constraints in international audit firms in Saudi Arabia: Exploring the interaction of gender, politics and religion. Account. Organ. Soc. 2020, 84, 101103. [Google Scholar] [CrossRef]

- Carp, M.; Istrate, C. Audit Quality under Influences of Audit Firm and Auditee Characteristics: Evidence from the Romanian Regulated Market. Sustainability 2021, 13, 6924. [Google Scholar] [CrossRef]

- Crucean, A.C.; Hategan, C.D. The Determinants Factors on Audit Quality: A Theoretical Approach. Ovidius Univ. Ann. Econ. Sci. Ser. 2019, 19, 702–710. [Google Scholar]

- Read, W.J.; Yezegel, A. Going-concern opinion decisions on bankrupt clients: Evidence of long-lasting auditor conservatism? Adv. Account. 2018, 40, 20–26. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Independent Variable | Type of Independent Variable | Value | Percentage |

|---|---|---|---|

| Gender | Male | 89 | 95.6% |

| Female | 4 | 4.4 | |

| Age | 30 and younger | 7 | 7.5 |

| 31–40 | 22 | 23.7 | |

| 41–50 | 30 | 32.3 | |

| Older than 50 | 34 | 36.5 | |

| Education | Diploma | 6 | 6.5 |

| Bachelor’s | 44 | 47.3 | |

| High Diploma | 16 | 17.2 | |

| Master’s | 15 | 16.1 | |

| Doctorate | 12 | 12.9 | |

| Experience | Less than 5 years | 5 | 5.4 |

| 5–9 | 18 | 19.4 | |

| 10–14 | 44 | 47.3 | |

| More than 15 | 26 | 27.9 |

| No. | Constructs | No. of Items | Cronbach Alpha | Results |

|---|---|---|---|---|

| 1 | Consulting Services | 8 | 70.1% | Acceptable |

| 2 | Accounting Services | 7 | 66.3% | Acceptable |

| 3 | Services Fees | 9 | 73.1% | Acceptable |

| 4 | Code of Professional Ethics | 7 | 69.5% | Acceptable |

| 5 | Commitment towards Clients | 9 | 67.8% | Acceptable |

| 6 | Commitment towards Employees | 7 | 82.6% | Acceptable |

| 7 | Credibility Gap of the Accounting Information | 12 | 88.2% | Acceptable |

| Total | 59 | 76.7% | Acceptable |

| Model | R | R Square | Adjusted R Square | Std Error of the Estimate |

|---|---|---|---|---|

| 1 | 0.26 | 0.51 | 0.22 | 1.65 |

| Hypotheses | B Values | Beta Coefficient | T Value | p Value | Decision |

|---|---|---|---|---|---|

| Consulting Services → Credibility Gap | 0.012 | 0.013 | 0.141 | 0.088 | Accepted |

| Accounting Services → Credibility Gap | 0.090 | 0.021 | 0.171 | 0.188 | Accepted |

| Services Fees → Credibility Gap | 0.240 | 0.237 | 2.002 | 0.048 | Rejected |

| Code of Professional Ethics → Credibility Gap | 0.220 | 0.212 | 1.993 | 0.049 | Rejected |

| Commitment towards Clients → Credibility Gap | 0.469 | 0.542 | 5.051 | 0.000 | Rejected |

| Commitment towards Employees → Credibility Gap | 0.007 | 0.0081 | 0.0753 | 0.940 | Accepted |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hamdallah, M.E.; Al-N’eimat, S.; Srouji, A.F.; Al-Okaily, M.; Albitar, K. The Effect of Apparent and Intellectual Sustainability Independence on the Credibility Gap of the Accounting Information. Sustainability 2022, 14, 14259. https://doi.org/10.3390/su142114259

Hamdallah ME, Al-N’eimat S, Srouji AF, Al-Okaily M, Albitar K. The Effect of Apparent and Intellectual Sustainability Independence on the Credibility Gap of the Accounting Information. Sustainability. 2022; 14(21):14259. https://doi.org/10.3390/su142114259

Chicago/Turabian StyleHamdallah, Madher E., Salem Al-N’eimat, Anan F. Srouji, Manaf Al-Okaily, and Khaldoon Albitar. 2022. "The Effect of Apparent and Intellectual Sustainability Independence on the Credibility Gap of the Accounting Information" Sustainability 14, no. 21: 14259. https://doi.org/10.3390/su142114259