1. Introduction

Recent decades have seen a dynamic rise in economic and industrial development across the globe. The collective activities of human beings have altered and are threatening the Earth’s fragile ecosystems and the possibilities of reversing the damage are diminishing. The financial sector also plays a significant role in shaping and transforming the economy along sustainable principals. Younger generations have demonstrated a concern for the well-being of the planet and their behavior, decisions, and choices are making an impact on economic and sustainable finance development.

The definitions of sustainability and sustainability literacy are relatively new both in the academic literature and in practical activities and are constantly changing due to rapid environmental, economic, and social development. In 1987, the United Nations Brundtland Commission defined sustainability as “meeting the needs of the present without compromising the ability of future generations to meet their own needs” [

1]. Ruggerio [

2] proposes that a definition or conceptual model of sustainability complies with the following criteria: (a) account for the complexity of socio-ecological sustainability by encompassing economic, ecological, social, and political factors; (b) account for intergenerational and intragenerational equity; and (c) address the hierarchical organization of nature, that is, acknowledge the feedback between socio-ecological sustainability and its surroundings. The United Nations Sustainable Development Goals (17 themes) have become the strongest directive for sustainability education policy and practice [

3]. Moreover, the United Nations [

4] is actively raising awareness of the importance of sustainability literacy. Sustainability literacy is defined as “the knowledge, skills and mindsets that allow individuals to become deeply committed to building a sustainable future and assisting in making informed and effective decisions to this end” [

5]. Diamond and Irwin [

6] defined sustainability literacy as “having the understanding, skills, attitudes and attributes to take informed action for the benefit of oneself and others, now and into a long-term future”.

Many researchers have conducted analyses of financial literacy as an important instrument for society’s development. Financial literacy is a specific component of human capital, which allows an individual to deal with fundamental financial issues to make adequate financial decisions. A financially literate individual, therefore, has the capacity to acquire financial skills and capabilities and is motivated to critically reflect on what influences their financial decision-making before applying their financial skills and capabilities to the financial dilemmas they face. Financial literacy education is about the teaching of personal financial skills and capabilities, with the direct intention of increasing an individual’s financial literacy through the acquisition of skills and capabilities. The terms financial literacy, financial knowledge, and financial education are often used interchangeably in the literature and popular media [

7]. As the background for our research, we use the financial literacy definition provided by the Organisation for Economic Co-operation and Development (OECD). Financial literacy is defined as the knowledge of financial products, skills, attitudes, and behaviors needed to make rational decisions and achieve individual financial well-being [

8].

Sustainability literacy and financial literacy have been combined to form the new concept of “sustainable financial literacy”. In the literature, sustainable finance has increasingly become the focus of empirical studies that seek to establish definitions, identify and analyze factors, and describe instruments. In some cases, climate finance, green finance, environmental finance, and sustainable finance are used interchangeably, with some small differences, with the common focus being to contribute to changing the world’s economy for a sustainable future. The notion of sustainable finance literacy includes the elements that form traditional finance literacy, such as budgeting, saving, borrowing, investing and an awareness of sustainable financial products, sustainable investments, etc.

The aim of our research was to analyze and assess the sustainability literacy and financial literacy of young people in the Baltic States and to provide some insights and recommendations on how to improve the levels of sustainability literacy, financial literacy, and sustainable financial literacy in these states. To achieve this goal, the following objectives were set:

- -

To examine the scientific literature on sustainability literacy and financial literacy.

- -

To conduct a study in the Baltic States to investigate the level of sustainability literacy and financial literacy among young people aged 15–30 years in the Baltic states.

The authors carried out a scientific analysis of the literature and comparative analysis of statistical data from the conducted surveys for the last few decades.

2. Literature Review

2.1. Financial Literacy

The term financial literacy originated in the United States around 1990. The term became particularly popular after 2000, when major programs to improve financial literacy were launched. At the international level, the term became generally accepted when the OECD published a definition of the concept as a process that helps to improve the understanding of financial products and concepts, develops the ability to assess financial risks and opportunities, and helps to make the most beneficial financial decision (OECD 2005).

Table 1 below highlights the most prominent definitions.

One of the first benchmark studies in financial literacy was the U.S. 2004 Health and Retirement Study (HRS), which included questions on this subject. It established the basis of a model for conducting studies in the financial field called the Big Three, which is based on three concepts: compound interest, inflation, and risk diversification indicate, where respondents command key economic concepts fundamental to savings and knowledge of risk diversification, crucial to informed investment decisions [

20]. The basis of this methodology was proposed by OECD and its International Network on Financial Education (INFE), who developed a core questionnaire in 2011 [

21]. The questions addressed a range of financial topics, including debt, insurance, spending, budgeting, inflation, investments, and saving for retirement. The methods used to measure financial literacy vary quite substantially according to the different conceptual definitions adopted. Across studies, both performance tests (usually multiple-choice questionnaires) and self-report methods have been employed to measure financial literacy [

17]. The number of questions used to assess financial literacy levels also vary, ranging from 3 to 45 items.

Financial literacy can often be associated with successful stock investing, high investment returns, low interest rates, and balanced lending and retirement planning. In contrast, in a study in Japan, Kawamura et al. [

22] showed that high financial literacy was often associated with speculative investing, over-borrowing, unbalanced and risky investment portfolios, and naïve financial decision-making. The authors concluded that the acquisition of financial knowledge can lead people to overestimate their financial knowledge and thus lead them to make irresponsible financial decisions.

Studies of the financial literacy among young people have identified a range of issues that merit attention from the analysis of external factors such as cultural differences, the level of a country’s development, and internal factors (such as gender, family wealth, or knowledge of mathematics). Moreno-Herrero et al. [

23] identified three main factors influencing a young person’s level of financial literacy: children’s communication with their parents about financial management, young people’s understanding of the importance of saving, and students’ use of financial products. Recommendations regarding what governments should do to strengthen financial literacy at the national level include: improving young people’s knowledge of mathematics; providing equal access to financial management education for both boys and girls; giving more attention to underachieving and vulnerable groups who may find it more difficult to educate or enlighten their children about financial management; and introducing financial management training initiatives not only for children but also parents, who can interact with their children to teach them how to make the right financial decisions.

According to the 2012 OECD’s Program for International Student Assessment (PISA) study, the use of financial literacy knowledge correlates with a person’s mathematics knowledge [

24]. A survey was conducted in the Netherlands to find out what factors influence the level of financial literacy among 15-year-old students [

25]. The results of the survey showed that, in addition to being from an immigrant background, their mothers’ education, or talking to their families about financial management, school performance had a significant influence. It was observed that students with better than average grades responded better to the survey questions. Muñoz-Céspedes et al. [

26] suggested the inclusion of the findings of psychological science and presented the combination of awareness, knowledge, skills, attitudes, and behaviors that help people make informed financial decisions that ensure their present and future financial well-being.

The concept ‘financial literacy’ now includes not only the knowledge of math, attitudes, and behavior of financial well-being but also positive impacts on environmental and social development. The concept ‘sustainable finance literacy’ can be presented like the updated concept of financial literacy, incorporating the knowledge of sustainability in making financial decisions. The importance of such new concept development has been raised by OECD. The combination of two concepts was discussed on 18 May 2018 at the 5th OECD-GFLEC global policy research symposium, where the key role of financial education in supporting sustainable and inclusive growth, and the relationship between financial education policies and broader economic, financial, and social outcomes were analyzed (OECD, 2018). The practitioners have suggested the definition ‘sustainable finance literacy’, meaning an understanding of sustainable financial products and their use for promoting sustainable development goals, plays a key role in the integration of ESG factors into financial decisions [

27]. Filippini et al. [

28] conducted research with Swiss households and measured the sustainable financial literacy using two complementary approaches (traditional multiple-choice questions and based on open-ended questions). The results revealed that Swiss households exhibited a low level of sustainable finance literacy. The authors presented the concept of sustainable finance literacy as the retail investors’ knowledge of regulations, norms, and standards for financial products with sustainable characteristics [

28]. Therefore, this article analyzes these two concepts separately as a mandatory part of education in modern society. In analyzing financial literacy, the authors are in line with the definition of Corsini and Giannelli [

19] by supplementing the definition of the importance of understanding sustainable financial products. This article contributes to the new direction of financial literacy, where the importance of sustainability knowledge is equally valued.

2.2. Sustainability Literacy

Sustainability literacy is a separate stream that has been developing very rapidly since the Sulitest (Sustainability Literacy Tools & Community) was created following the Rio+20 Conference as an easy to use, online, multiple-choice assessment platform, consisting of a set of questions identical for all users throughout the world, and other specialized modules that consider national, regional, and cultural realities [

4]. The proposed Sustainability Literacy Test by UN is an open online training and assessment tool, which is dedicated to educating a large part of society. The most common instrument employed to test sustainability knowledge is in the form of a quiz and focuses on knowledge. Relatedly, Zwickle et al. [

29] assessed the sustainability literacy of undergraduate students at the Ohio State University (1000 students) using a web-based and campus-wide survey, which featured 16 multiple-choice questions. This study discovered that an average of 69% of the students answered the questions correctly. A surprising finding was that aeronautical engineering students performed better than the rest of the students [

29]. Décamps et al. [

30] clarified the definition of ‘sustainability literacy’, which can be defined as the knowledge, skills, and mindsets that help compel an individual to become deeply committed to building a sustainable future and allow him or her to make informed and effective decisions to this end. The authors presented the tool’s structure and the contribution of measuring sustainability literacy globally and recommended it for educational institutions. Akeel et al. [

31] assessed the sustainability literacy of the Nigerian engineering community based on three criteria: level of awareness of the UN program for SD in Africa, performance on sustainability literacy tests, and self-assessment of sustainability knowledge. The results revealed that a low level of sustainability knowledge and the Nigerian engineering community were more familiar with economic topics [

31]. Following the same methodology used by Akeel et al. [

31], the authors surveyed the research of future managers with a Post Graduate Diploma in Management and Master of Business Administration in India for sustainability literacy. The findings revealed that students were more familiar with social and economic sustainability and had less awareness of environmental issues [

32].

We suggest the term ‘sustainable literacy’ as knowledge of sustainable development goals presented by UN, especially stressing the importance of environmental issues. Theoretical analysis shows that financial literacy and, especially, sustainability literacy should be taught as soon as young people begin to make simple financial decisions independently. For this reason, a study on sustainable financial literacy of young people was carried out in Lithuania, Latvia, and Estonia to compare the level of sustainability literacy and financial literacy. The findings expanded the group of articles analyzing different levels of financial and sustainability literacy in different countries. From our knowledge, there is no research assessing both sustainability literacy and financial literacy in the Baltic countries.

3. Materials and Methods

According to the Data of Statistics Lithuania, 500,933 persons aged 15–30 years lived in Lithuania in 2021; according to the data of Statistics Latvia, there were 305,979 people aged 15–30 in 2021; and according to the Estonian Department of Statistics, there were 222,521 people aged 15–30 in Estonia in 2021. The number of surveys completed in the three states were as follows: 387 questionnaires in Lithuania, 392 questionnaires in Latvia, and 400 questionnaires in Estonia. The survey was completed in the second half of 2021, starting in Lithuania and then Latvia and Estonia. The survey was translated into Lithuanian whereas in Latvia and Estonia, the survey was administered in English.

The questionnaire (see

Appendix A for details) had the following structure:

Four questions (No. 2, 4, 12, 13) that help assess the sustainability and financial knowledge of respondents.

Four questions (No 11, 14, 15, 16) that help to measure the financial knowledge of young people.

Two questions (No 10, 17) that help assess sustainability-related knowledge.

Three questions (No 1, 3, 7) that help to understand young people’s behavior when making financial decisions.

Four questions (No 5, 6, 8, 9) that help measure people’s behavior in making sustainable finance decisions.

Four questions (18, 19, 20, 21) that help to determine the demographics of the surveyed persons.

4. Results

The first block of questions sought to clarify the level of knowledge respondents had about sustainability.

Figure 1 shows respondents’ answers to the question “

In your opinion, what would be the expected return on investment when investing in sustainable financial instruments (stocks, bonds, etc.)?”

The results in

Figure 1 suggest that young people in all three Baltic countries lack an understanding of the value created by sustainable investment as almost half of the respondents identified themselves as “not competent “or assumed that the investment return from sustainable financial instruments would be below average.

More thorough investigation extends the above conclusion for the entire population of the three countries with the above characteristics. The level of significance was chosen as . The sum of responses in all three countries was and served as the statistics of the test of the following hypothesis. The average percentage of the ones who stated that they are not competent (32% = 337/1179) was used for estimation of the variance of the binomial distribution. Based on the special case of the central limit theorem related to the binomial distribution, the test of the following hypotheses can be performed.

Hypothesis 0 (H0). Half of respondents identified themselves as being competent to answer the question “In your opinion, what would be the expected return on investment when investing in sustainable financial instruments (stocks, bonds, etc.)?”

Hypothesis 1 (H1). Less than half of the respondents identified themselves as being competent to answer the above question.

The following appropriate test statistics formula was applied for the binomial distribution:

For , , the size of the population (the number of responses obtained in all the three countries in question), we obtain the realization of the test statistics , which is less than the threshold for the standard normal distribution for the chosen level of significance −1.645. Therefore, with the stated level of significance, we can choose to accept the alternative hypothesis H1.

The results of the academic study (Unruh et al. [

33]) and practical research (Morningstar [

34]), showing that sustainable instruments create value and that their return on investment is higher than traditional investments, should be more effectively communicated to a larger younger population.

Further clarification on the level of respondents’ knowledge about sustainability was requested using the concept of green economy (

Figure 2). The term was defined in the questionnaire: “

A term used to describe the pursuit of human well-being in an effort to minimize the adverse effects on nature by reducing greenhouse gas emissions and making the most efficient use of non-renewable resources.”

The results presented in

Figure 2 show that a large proportion of young people in the Baltic States are aware of green economy policies aimed at reducing environmental pollution. Latvians and Estonians appeared to be more knowledgeable than Lithuanians in this regard. The difference between Lithuania and Latvia was statistically significant, in contrast to other pairs. In fact, the standard deviation of the corresponding normal distribution for the estimation of the differences of proportions in all three pairs of countries ranges from 6.32 to 6.64 while the differences of proportions appear to be considerable only between Lithuania and Latvia, with the corresponding

p value 0.039, which relates to the calculated

Z value:

where

is the average proportion of positive answers between respondents in the two countries in question. Thus, as Lithuania was distinguished in this regard with the chosen level of significance

, we believe that such a bias can be mitigated by explaining and promoting to the public various programs, such as European Green Deal or similar.

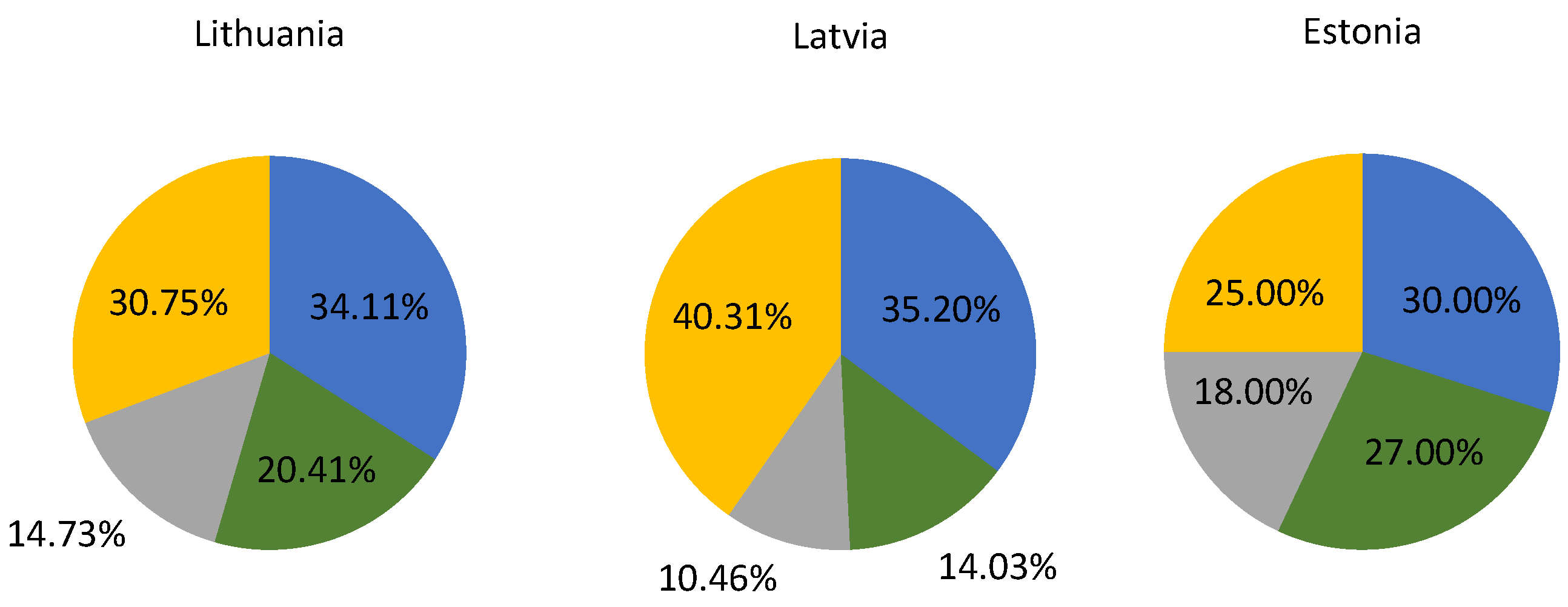

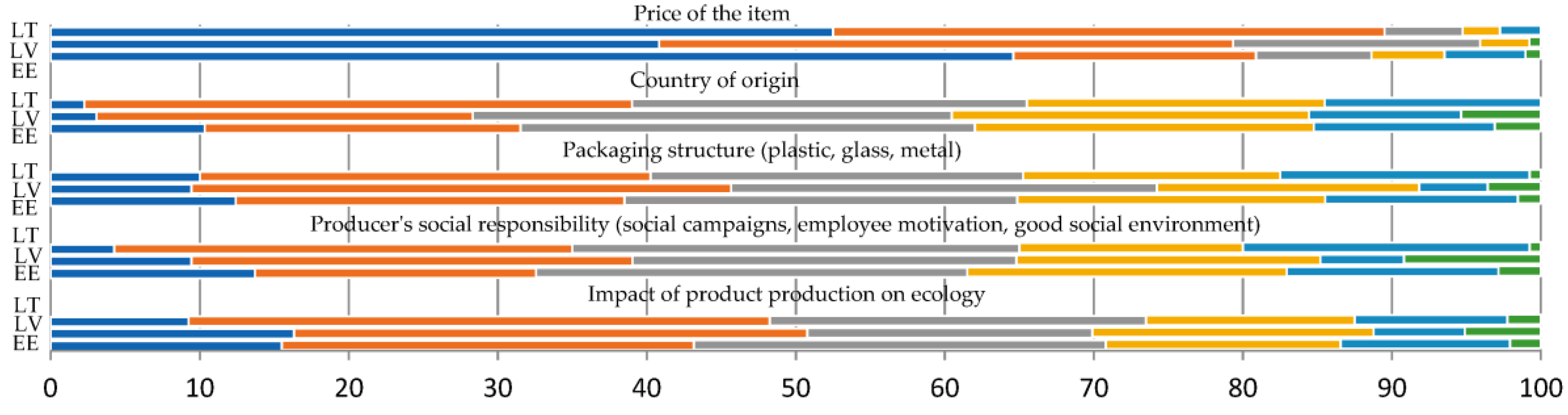

When it comes to behaviors related to making sustainable decisions, the results show that the price of a product is still more important for young people than a producer’s social responsibility, product packaging structure, or the impact of production on the environment (

Figure 3).

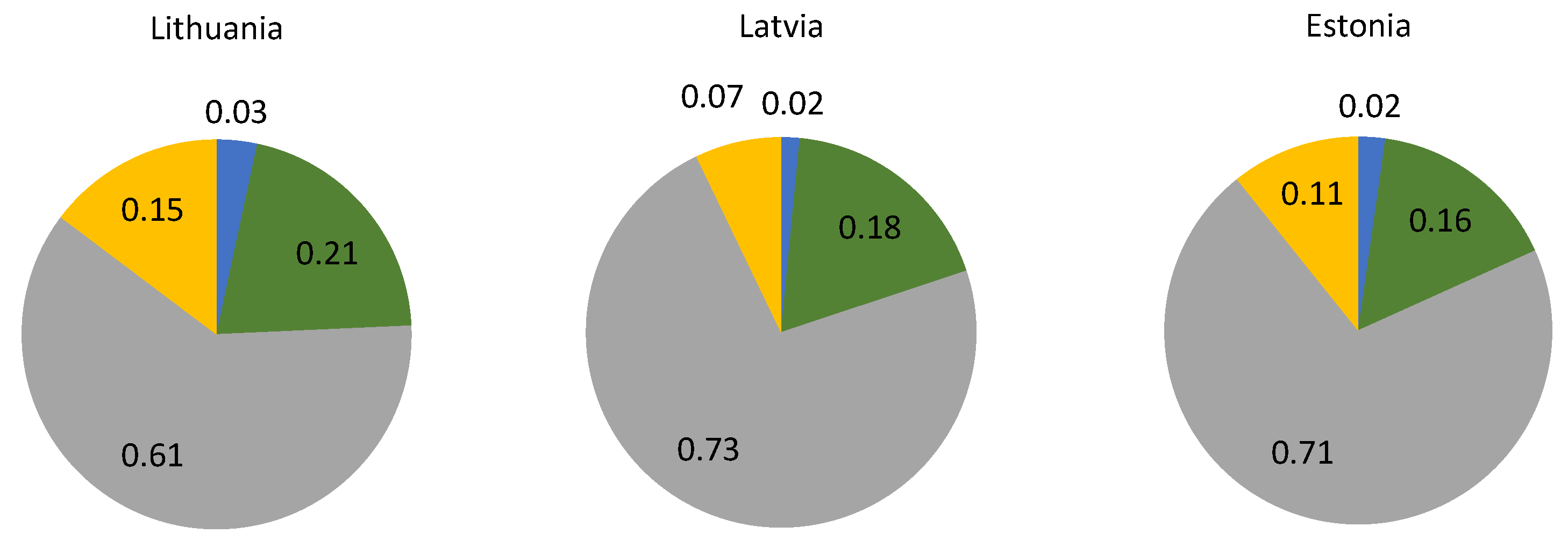

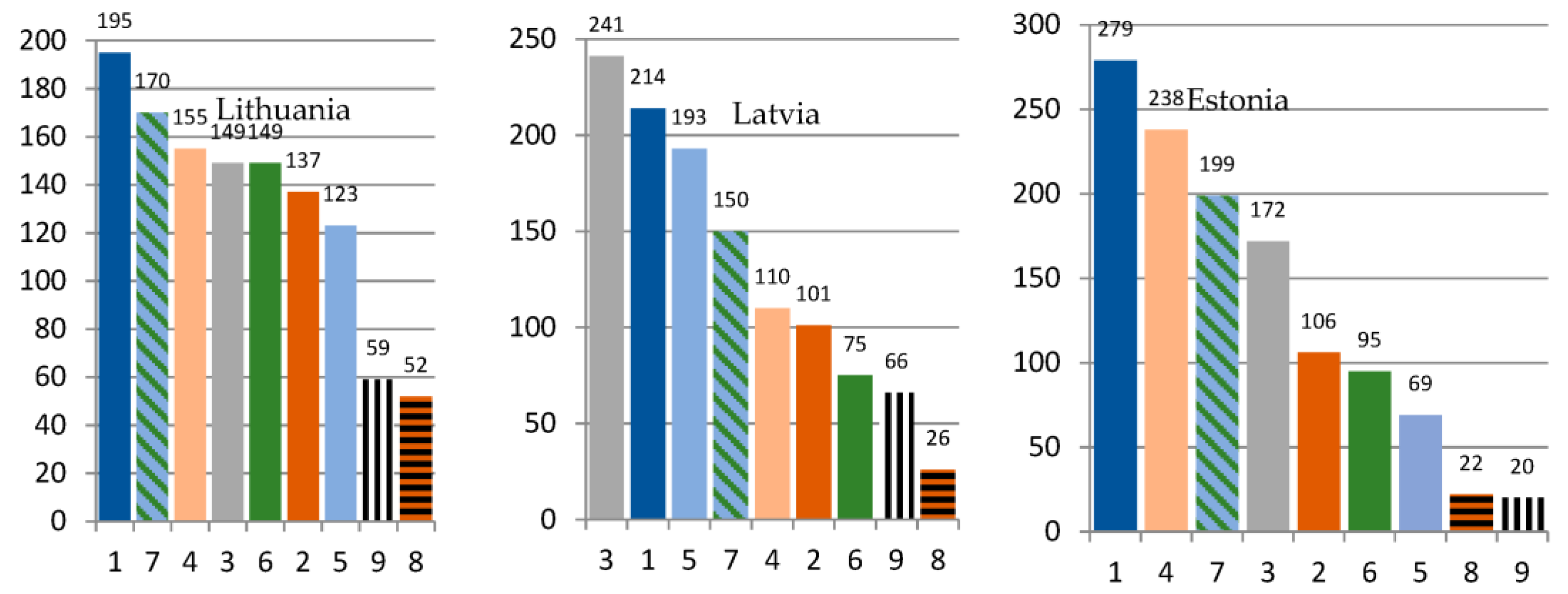

When it comes to UN Sustainable Development Goals (SDGs) and the environmental, social, and governance (ESG) perspective, the survey showed that the most important factors for young people in the Baltic states are social factors such as workers’ rights, human rights, and governance issues such as preventing corruption, rather than environmental issues such as climate change or air and water pollution (

Figure 4). The respondents were asked the question “

Imagine that you have inherited a controlling stake in an international company and you have to make the most important decisions for the company. Which of the following global and local issues would your company prioritize? (select only 3 options)”.

The second block of questions sought to clarify the level of knowledge of respondents’ financial literacy and personal finance management. The two questions were adopted from Lusardi et al. [

35]: (1) the inflation effect on savings: “

Imagine you are making a deposit with an interest rate of 1% per year and inflation of 2% in the same year. How many of the same goods and services will you be able to buy with the amount of money available in one year?”; and (2) diversification of investments: “

By investing in the stock market, the risks of the investment can be reduced by investing in a wide range of shares of different companies”. The results show that in both cases, young people in Estonia have higher financial literacy knowledge compared to young people in Latvia and Lithuania.

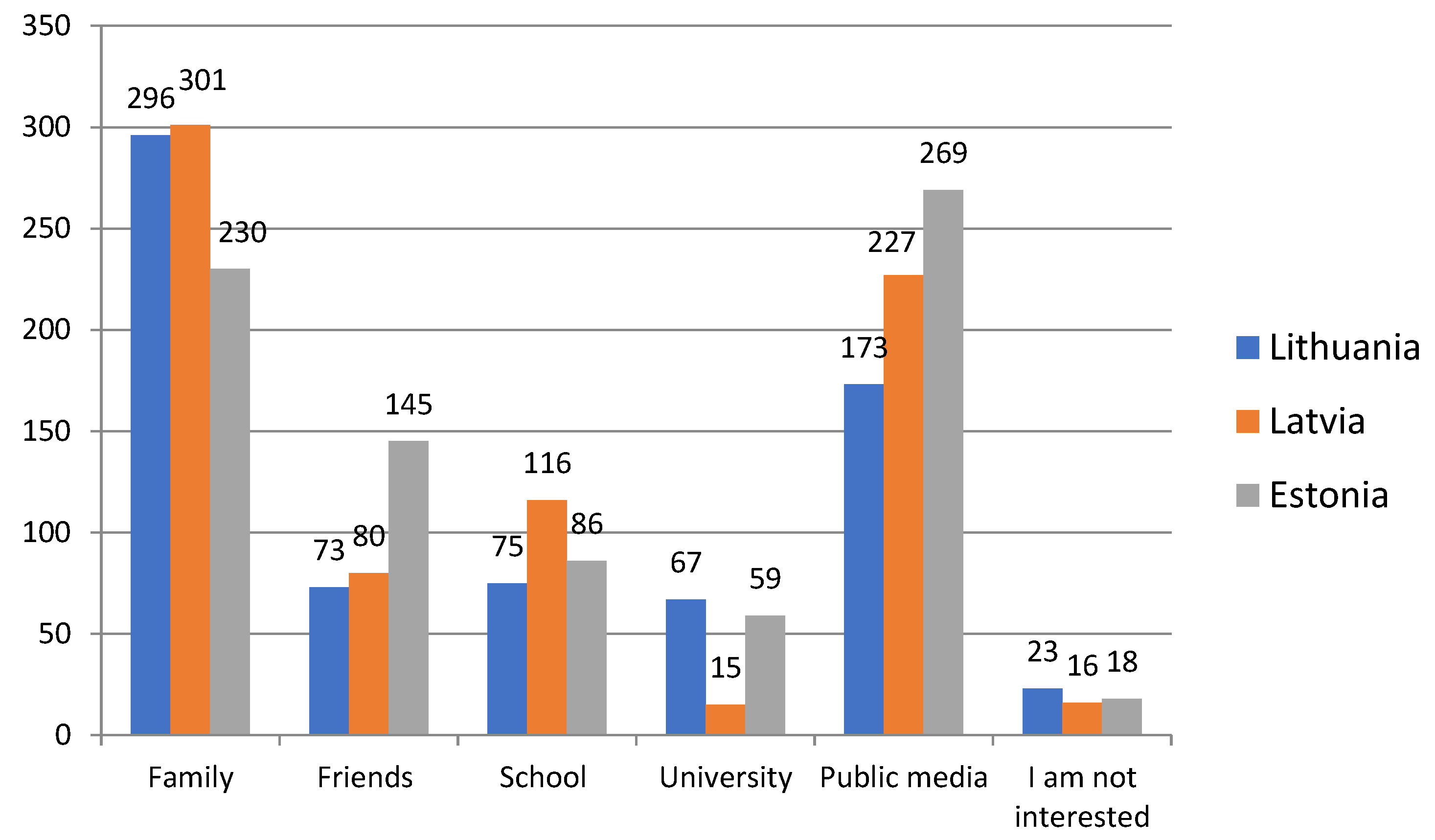

This research also aimed to identify the channels through which young people in the Baltic States acquire financial literacy knowledge and learn to manage their personal finances. The results show that parents and media are the mains sources of information and knowledge (

Figure 5).

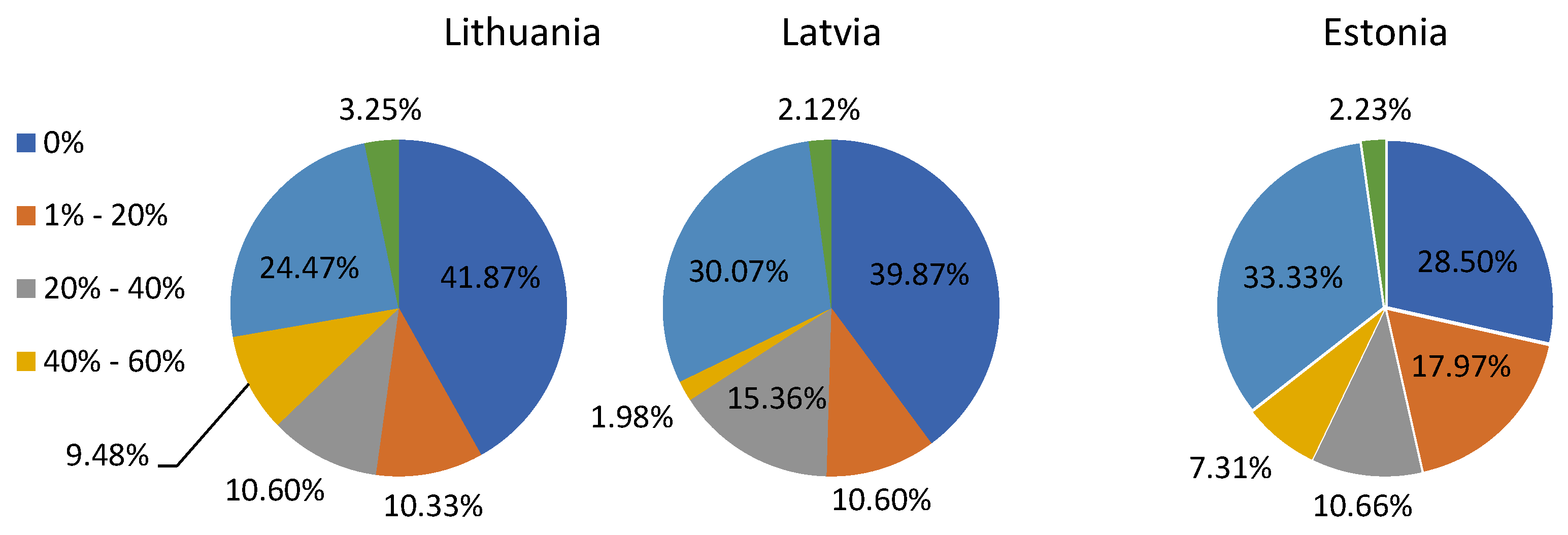

Finally, the survey sought to compare how young people in the Baltic States put financial literacy knowledge into practice. The effective use of financial literacy knowledge is often associated with investment, so in our research, we also tried to find out what proportion of young people’s income is a return on investment (

Figure 6).

The results show that over half of the young people in Lithuania do not invest or do not benefit financially from their investments. In Latvia, about half are investment-averse, and in Estonia, more than half receive at least some financial benefit from their investments. The first and the last statements can be verified by statistical means. In fact, the difference between half of the responses and the actual realization is 49.5 votes for Lithuania and −27 for Estonia, which produces a Z score of 5.03 and −2.7, respectively. Both obviously confirm the conclusion of a considerable difference with half of the population, with the chosen level of significance corresponding to left- and right-hand 5% probability thresholds of +1.645 and −1.645 of the standard normal distribution, respectively.

It can be noted that when assessing financial knowledge, Estonians proved to be better informed than Lithuanians and Latvians. On the other hand, Latvians received a higher financial return than Lithuanians or Estonians, which shows that the level of financial literacy does not necessarily correlate with the financial behavior of young people and the return on investment in financial decisions made. A large proportion of young people do not obtain any financial returns, but a significant proportion do try or have tried to invest to improve their financial situation. It is quite interesting to note that in Lithuania and Estonia, men invest more and obtain a greater return on their investment, but in Latvia, the numbers of men and women are similar.

5. Discussion

This paper adds to existing research and knowledge by analyzing what young people know (and do not know) about sustainability and financial literacy using a set of simple questions. The results of our study reveal that young people have different levels of financial and sustainability literacy in the Baltic States despite Estonia, Latvia, and Lithuania being neighboring countries and having a similar level of economic and social development. Comparing the results of the financial literacy of young people with other similar studies, it can be noted that the financial literacy level is quite high in Baltic countries. The study by Lusardi et al. (2010) [

35] revealed that only 27% of young US citizens knew about inflation and risk diversification and could perform simple interest rate calculations while our research results show that more than half of young people knew about inflation and risk diversification in Estonia, Latvia, and Lithuania. We cannot exclude the possibility that during the decade, the general level and understanding of young people has increased and it might be a confusing comparison.

It is more difficult to assess sustainability literacy results and their context, as our study is one of the first in the field of sustainable literacy and sustainable financial literacy. The results of this study reveal that young residents in Baltic countries have sufficient knowledge about sustainability and the green economy. However, their behavior discloses the opposite results. When young people buy an item, the price becomes the most important criteria, and an item’s impact on ecology Nd an item’s producers’ social responsibility are rather unimportant criteria. We did not detail the sectors of items in our study. Filippini et al.’s (2021) results show that specifically for owning sustainable finance products, the level of sustainable finance literacy is an important determinant, but both financial literacy and sustainability literacy do not have a statistically significant effect on holding sustainable assets for Swiss households.

Finally, this study’s results show that for young people in the Baltics, social aspects are the most important from an ESG perspective. Fighting for workers’ rights, preserving jobs, and supporting the fight for humans’ rights was more important than promoting gender equality or reducing air and water pollution. We cannot exclude the possibility, that this is due to the constraints of the designed test, where answers related to social aspects were listed at the beginning, and environmental aspects were listed at the end. While we believe these limitations did not impact the primary outcome of this study, future research could seek to include additional questions to find out the importance of environmental, social, and governance factors (ESG) in relation to each other.

6. Conclusions

The results of this study suggest that the level of financial literacy among young people in the Baltic States is the highest in Estonia, followed by Lithuania and Latvia. A possible connection was observed between the level of financial literacy of young people and the sources of information young people use when learning how to manage their finances. Estonians’ main source of financial management is public information in the media, whereas young people in Lithuania and Latvia learn from their parents. Lithuanians seem to be the most likely to save as the proportion of young people in Lithuania was the highest in terms of how many respondents had set savings goals.

Some connection was observed between the financial literacy of young people and sustainable financial behavior. The Estonian respondents had the best financial literacy knowledge and made the best sustainable financial decisions of the three Baltic States, even though they applied this knowledge quite poorly when making financial decisions. This connection does not seem to apply to the financial literacy among the Latvian respondents as their knowledge was limited compared to the Lithuanian respondents yet their sustainable financial behavior was better than that of young respondents in Lithuania. Shopping behaviors were more sustainable among Latvia’s respondents than among Estonians, which also undermines this connection, as Latvian respondents’ financial literacy was much lower than the Estonian financial literacy.

While the levels of financial literacy differed across the three states, the levels of knowledge about sustainability were quite similar.

With regards to developing sustainable literacy, financial literacy and sustainable finance recommendations vary as to when, where, and how such learning should take place. There are a range of ideas about introducing this topic at different points, through different types and lengths of education and in both formal and non-formal settings. Specific suggestions include elective courses in higher education and workshops for those who do not attend high education. What most researchers do agree upon is that the levels of financial literacy and sustainability literacy are too low and that measures need to be taken to improve this situation, considering culture, age, gender, and other social and demographic aspects.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}