Environmental Economics and the SDGs: A Review of Their Relationships and Barriers

,

,  ,

,

Abstract

:1. Introduction

2. Literature Review

2.1. Environmental Economics

2.1.1. The Inclusion of Natural Capital in the System of National Accounts (SEEA)

2.1.2. Green Consumerism

2.1.3. Fiscal Policy

2.1.4. De-Growth Economic Model

2.2. The Sustainable Development Goals (SDGs)

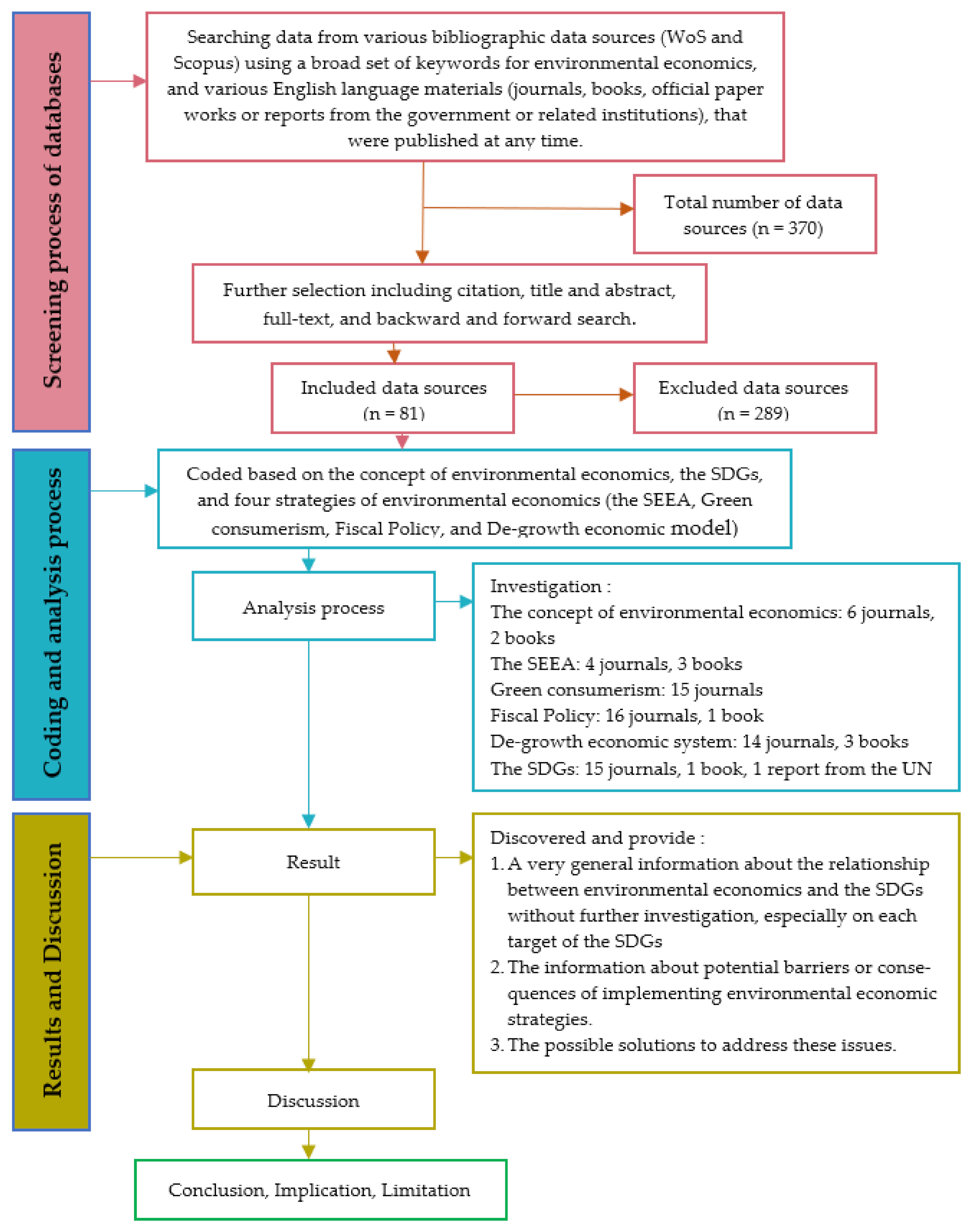

3. Methodology

3.1. The First Step: Screening Process of Databases

3.2. The Second Step: Coding and Analysis Process

3.3. The Third Step: Results and Discussion

4. Findings

4.1. The Relationship between the Inclusion of Natural Capital in the SNA (SEEA) and the SDGs

4.2. The Relationship between “Green Consumerism” and the SDGs

4.3. The Relationship between Fiscal Policy and the SDGs

4.4. The Relationship between the De-Growth Economic Model and the SDGs

4.5. The Possible Barriers or Consequences of Implementing Environmental Economics

5. Discussion

6. Conclusions, Implications, and Limitations

6.1. Conclusions

6.2. Implication

6.3. Limitation

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Huynh, C.M. Shadow economy and air pollution in developing Asia: What is the role of fiscal policy? Environ. Econ. Policy Stud. 2020, 22, 357–381. [Google Scholar] [CrossRef]

- Biswas, A.K.; Farzanegan, M.R.; Thum, M. Pollution, shadow economy and corruption: Theory and evidence. Ecol. Econ. 2012, 75, 114–125. [Google Scholar] [CrossRef] [Green Version]

- Pirmana, V.; Alisjahbana, A.S.; Yusuf, A.A.; Hoekstra, R.; Tukker, A. Environmental costs assessment for improved environmental-economic account for Indonesia. J. Clean. Prod. 2020, 280, 124521. [Google Scholar] [CrossRef]

- Obst, C.; Vardon, M. Recording environmental assets in the national accounts. Oxf. Rev. Econ. Policy 2014, 30, 126–144. [Google Scholar] [CrossRef]

- Sachs, J.D. From Millennium Development Goals to Sustainable Development Goals. Lancet 2012, 379, 2206–2211. [Google Scholar] [CrossRef]

- Mio, C.; Panfilo, S.; Blundo, B. Sustainable development goals and the strategic role of business: A systematic literature review. Bus. Strat. Environ. 2020, 29, 3220–3245. [Google Scholar] [CrossRef]

- Beder, S. Environmental economics and ecological economics: The contribution of interdisciplinarity to understanding, influence and effectiveness. Environ. Conserv. 2011, 38, 140–150. [Google Scholar] [CrossRef] [Green Version]

- Medina, L.; Schneider, F. Shadow Economies Around the World: What Did We Learn Over the Last 20 Years? IMF Working Papers; International Monetary Fund: Washington, DC, USA, 2018; Volume 18. [Google Scholar] [CrossRef]

- Ambec, S.; De Donder, P. Environmental policy with green consumerism. J. Environ. Econ. Manag. 2021, 111, 102584. [Google Scholar] [CrossRef]

- Ulph, A.; Ulph, D. Environmental policy when consumers value conformity. J. Environ. Econ. Manag. 2018, 109, 102172. [Google Scholar] [CrossRef] [Green Version]

- Field, B.C.; Field, M.K. Environmental Economics-An Introduction, 7th ed.; McGraw-Hill Education: New York, NY, USA, 2017. [Google Scholar]

- Pearce, D. An Intellectual History of Environmental Economics. Annu. Rev. Energy Environ. 2002, 27, 57–81. [Google Scholar] [CrossRef]

- Sagoff, M. Environmental Economics. Encycl. Appl. Ethics 2012, 97–104. [Google Scholar] [CrossRef]

- Nadeau, R.L. The unfinished journey of ecological economics. Ecol. Econ. 2015, 109, 101–108. [Google Scholar] [CrossRef]

- Lélé, S.M. Sustainable development: A critical review. World Dev. 1991, 19, 607–621. [Google Scholar] [CrossRef]

- Venkatachalam, L. Environmental economics and ecological economics: Where they can converge? Ecol. Econ. 2007, 61, 550–558. [Google Scholar] [CrossRef]

- Kahneman, D.; Knetsch, J.L. Valuing public goods: The purchase of moral satisfaction. J. Environ. Econ. Manag. 1992, 22, 57–70. [Google Scholar] [CrossRef]

- Beder, S. Charging the earth: The promotion of price-based measures for pollution control. Ecol. Econ. 1996, 16, 51–63. [Google Scholar] [CrossRef]

- Johnson, M. ‘Fiscal Policy’ Before Keynes’ General Theory. SSRN Electron. J. 2018. [Google Scholar] [CrossRef]

- Plaza-Úbeda, J.A.; Pérez-Valls, M.; Cespedes-Lorente, J.; Payán-Sánchez, B. The contribution of systems theory to sustainability in degrowth contexts: The role of subsystems. Syst. Res. Behav. Sci. 2019, 37, 68–81. [Google Scholar] [CrossRef] [Green Version]

- Jakob, M.; Edenhofer, O. Green growth, degrowth, and the commons. Oxf. Rev. Econ. Policy 2014, 30, 447–468. [Google Scholar] [CrossRef]

- Vardon, M.; Castaneda, J.-P.; Nagy, M.; Schenau, S. How the System of Environmental-Economic Accounting can improve environmental information systems and data quality for decision making. Environ. Sci. Policy 2018, 89, 83–92. [Google Scholar] [CrossRef]

- System of National Accounts. European Communities, International Monetary Fund, Organisation for Economic Co-operation and Development, United Nations, and World Bank Papers; United Nations: New York, NY, USA, 2009. [Google Scholar]

- United Nations; Ecosystem Accounting. System of Environmental-Economic Accounting—Ecosystem Accounting; United Nations: San Francisco, CA, USA, 2021. [Google Scholar]

- United Nations; European Commission; International Monetary Fund; World Bank. Integrated Environmental and Economic Accounting; United Nations: San Francisco, CA, USA, 2003. [Google Scholar]

- Dagher, G.K.; Itani, O. Factors influencing green purchasing behaviour: Empirical evidence from the Lebanese consumers. J. Consum. Behav. 2014, 13, 188–195. [Google Scholar] [CrossRef] [Green Version]

- Tseng, C.-H. The effect of price discounts on green consumerism behavioral intentions. J. Consum. Behav. 2016, 15, 325–334. [Google Scholar] [CrossRef]

- Paetz, A.-G.; Dütschke, E.; Fichtner, W. Smart Homes as a Means to Sustainable Energy Consumption: A Study of Consumer Perceptions. J. Consum. Policy 2011, 35, 23–41. [Google Scholar] [CrossRef]

- Haytko, D.L.; Matulich, E. Green advertising and environmentally responsible consumer behaviors: Linkages examined. J. Manag. Mark. Res. 2008, 1, 2–11. Available online: http://search.proquest.com/abiglobal/docview/759652267?accountid=14681%5Cnhttp://media.proquest.com/media/pq/classic/doc/2170766611/fmt/pi/rep/NONE?hl=&cit:auth=Haytko,+Diana+L;Matulich,+Erika&cit:title=Green+Advertising+and+Environmentally+Responsible+Co (accessed on 3 January 2022).

- Wiedenhofer, D.; Guan, D.; Liu, Z.; Meng, J.; Zhang, N.; Wei, Y.-M. Unequal household carbon footprints in China. Nat. Clim. Chang. 2016, 7, 75–80. [Google Scholar] [CrossRef] [Green Version]

- Han, H.; Hsu, L.-T.J.; Lee, J.-S. Empirical investigation of the roles of attitudes toward green behaviors, overall image, gender, and age in hotel customers’ eco-friendly decision-making process. Int. J. Hosp. Manag. 2009, 28, 519–528. [Google Scholar] [CrossRef]

- Laroche, M.; Bergeron, J.; Barbaro-Forleo, G. Targeting consumers who are willing to pay more for environmentally friendly products. J. Consum. Mark. 2001, 18, 503–520. [Google Scholar] [CrossRef] [Green Version]

- Mostafa, M.M. Gender differences in Egyptian consumers? green purchase behaviour: The effects of environmental knowledge, concern and attitude. Int. J. Consum. Stud. 2007, 31, 220–229. [Google Scholar] [CrossRef]

- Stern, P.C. Toward a coherent theory of environmentally significant behavior. J. Soc. Issues 2000, 56, 407–424. [Google Scholar] [CrossRef]

- Elsantil, Y. Antecedents of Green Purchasing Behavior in the Arabic Gulf. Soc. Mark. Q. 2021, 27, 133–149. [Google Scholar] [CrossRef]

- Paul, J.; Modi, A.; Patel, J. Predicting green product consumption using theory of planned behavior and reasoned action. J. Retail. Consum. Serv. 2016, 29, 123–134. [Google Scholar] [CrossRef]

- Pearce, D.W.; Atkinson, G.D. Capital theory and the measurement of sustainable development: An indicator of ‘weak’ sustainability. Sustainability 2017, 8, 397–402. [Google Scholar] [CrossRef]

- Battaglini, M.; Coate, S. A Political economy theory of fiscal policy and unemployment. J. Eur. Econ. Assoc. 2015, 14, 303–337. [Google Scholar] [CrossRef]

- López, R.; Galinato, G.I.; Islam, A. Fiscal spending and the environment: Theory and empirics. J. Environ. Econ. Manag. 2011, 62, 180–198. [Google Scholar] [CrossRef]

- Huynh, C.M.; Nguyen, T.L. Fiscal policy and shadow economy in Asian developing countries: Does corruption matter? Empir. Econ. 2019, 59, 1745–1761. [Google Scholar] [CrossRef]

- Antweiler, W.; Copeland, B.R.; Taylor, M.S. Is Free Trade Good for the Environment? Am. Econ. Rev. 2001, 91, 877–908. [Google Scholar] [CrossRef] [Green Version]

- Mani, M.; Wheeler, D. In Search of Pollution Havens? Dirty Industry in the World Economy, 1960 to 1995. J. Environ. Dev. 1998, 7, 215–247. [Google Scholar] [CrossRef]

- Vazquez-Brust, D.; Plaza-Úbeda, J. Green Growth Policy, De-Growth, and Sustainability: The Alternative Solution for Achieving the Balance between Both the Natural and the Economic System. Sustainability 2021, 13, 4610. [Google Scholar] [CrossRef]

- Win, T.; Paradigm, W. The Win-Win Paradigm and Stakeholder Integration. Bus. Strat. Environ. 2009, 499, 487–499. [Google Scholar]

- Sorman, A.H.; Giampietro, M. The energetic metabolism of societies and the degrowth paradigm: Analyzing biophysical constraints and realities. J. Clean. Prod. 2013, 38, 80–93. [Google Scholar] [CrossRef]

- Corbett, L.M. Sustainable operations management: A typological approach. J. Ind. Eng. Manag. 2009, 2, 10–30. [Google Scholar] [CrossRef]

- Latouche, S. Farewell To Growth, 1st ed.; Polity Press: Cambridge, UK, 2009. [Google Scholar]

- Felber, C. Change Everything–The Economy for the Common Good, 1st ed.; Zed Books, Ltd.: London, UK, 2015. [Google Scholar]

- Lorek, S.; Fuchs, D. Strong sustainable consumption governance—Precondition for a degrowth path? J. Clean. Prod. 2013, 38, 36–43. [Google Scholar] [CrossRef] [Green Version]

- Gomez-Mejia, L.R.; Balkin, D.B.; Cardy, R.L. Manging Human Resources; Prentice Hall: Hoboken, NJ, USA, 2012. [Google Scholar]

- Alcott, B. Should degrowth embrace the Job Guarantee? J. Clean. Prod. 2011, 38, 56–60. [Google Scholar] [CrossRef]

- United Nations. Global Indicator Framework for the Sustainable Development Goals and Targets of the 2030 Agenda for Sustainable Development; United Nations: New York, NY, USA, 2018; pp. 1–21. Available online: https://unstats.un.org/sdgs/indicators/Global Indicator Framework after refinement_Eng.pdf (accessed on 15 January 2022).

- United Nations. The 17 Goals of Sustainable Development Goals; United Nations: New York, NY, USA, 2015; Available online: https://sdgs.un.org/goals (accessed on 15 January 2022).

- Hutton, C.W.; Nicholls, R.J.; Lázár, A.N.; Chapman, A.; Schaafsma, M.; Salehin, M. Potential Trade-Offs between the Sustainable Development Goals in Coastal Bangladesh. Sustainability 2018, 10, 1108. [Google Scholar] [CrossRef] [Green Version]

- Bennich, T.; Weitz, N.; Carlsen, H. Deciphering the scientific literature on SDG interactions: A review and reading guide. Sci. Total Environ. 2020, 728, 138405. [Google Scholar] [CrossRef] [PubMed]

- Cordova, M.F.; Celone, A. SDGs and Innovation in the Business Context Literature Review. Sustainability 2019, 11, 7043. [Google Scholar] [CrossRef] [Green Version]

- Nerini, F.F.; Sovacool, B.; Hughes, N.; Cozzi, L.; Cosgrave, E.; Howells, M.; Tavoni, M.; Tomei, J.; Zerriffi, H.; Milligan, B. Connecting climate action with other Sustainable Development Goals. Nat. Sustain. 2019, 2, 674–680. [Google Scholar] [CrossRef]

- Muff, K.; Kapalka, A.; Dyllick, T. The Gap Frame-Translating the SDGs into relevant national grand challenges for strategic business opportunities. Int. J. Manag. Educ. 2017, 15, 363–383. [Google Scholar] [CrossRef]

- Walz, R.; Pfaff, M.; Marscheider-Weidemann, F.; Glöser-Chahoud, S. Innovations for reaching the green sustainable development goals–Where will they come from? Int. Econ. Econ. Policy 2017, 14, 449–480. [Google Scholar] [CrossRef]

- Pedersen, C.S. The UN Sustainable Development Goals (SDGs) are a Great Gift to Business! Procedia Cirp 2018, 69, 21–24. [Google Scholar] [CrossRef]

- Zhang, Q.; Prouty, C.; Zimmerman, J.B.; Mihelcic, J.R. More than Target 6.3: A Systems Approach to Rethinking Sustainable Development Goals in a Resource-Scarce World. Engineering 2016, 2, 481–489. [Google Scholar] [CrossRef]

- Xue, S.; Zhang, B.; Zhao, X. Brain drain: The impact of air pollution on firm performance. J. Environ. Econ. Manag. 2021, 110, 102546. [Google Scholar] [CrossRef]

- Chay, K.Y.; Greenstone, M. Does Air Quality Matter? Evidence from the Housing Market. J. Political Econ. 2005, 113, 376–424. [Google Scholar] [CrossRef] [Green Version]

- Arntz, M. What Attracts Human Capital? Understanding the Skill Composition of Interregional Job Matches in Germany. Reg. Stud. 2009, 44, 423–441. [Google Scholar] [CrossRef]

- Wang, J.; Nguyen, N.; Bu, X. Exploring the Roles of Green Food Consumption and Social Trust in the Relationship between Perceived Consumer Effectiveness and Psychological Wellbeing. Int. J. Environ. Res. Public Health 2020, 17, 4676. [Google Scholar] [CrossRef]

- Allen, M.W.; Craig, C.A. Rethinking corporate social responsibility in the age of climate change: A communication perspective. Int. J. Corp. Soc. Responsib. 2016, 1, 1. [Google Scholar] [CrossRef] [Green Version]

- Gerlagh, R.; Bijgaart, I.V.D.; Nijland, H.; Michielsen, T. Fiscal Policy and CO2 Emissions of New Passenger Cars in the EU. Environ. Resour. Econ. 2016, 69, 103–134. [Google Scholar] [CrossRef] [Green Version]

- Pereira, R.M.; Pereira, A.M. The Economic and Budgetary Impact of Climate Policy in Portugal: Carbon Taxation in a Dynamic General Equilibrium Model with Endogenous Public Sector Behavior. Environ. Resour. Econ. 2016, 67, 231–259. [Google Scholar] [CrossRef]

- Schneider, F.; Kallis, G.; Martinez-Alier, J. Crisis or opportunity? Economic degrowth for social equity and ecological sustainability. Introduction to this special issue. J. Clean. Prod. 2010, 18, 511–518. [Google Scholar] [CrossRef]

- Infante-Amate, J.; de Molina, M.G. ‘Sustainable de-growth’ in agriculture and food: An agro-ecological perspective on Spain’s agri-food system (year 2000). J. Clean. Prod. 2013, 38, 27–35. [Google Scholar] [CrossRef]

- Pirmana, V.; Alisjahbana, A.S.; Hoekstra, R.; Tukker, A. Implementation Barriers for a System of Environmental-Economic Accounting in Developing Countries and Its Implications for Monitoring Sustainable Development Goals. Sustainability 2019, 11, 6417. [Google Scholar] [CrossRef] [Green Version]

- Jackson, S.E.; Ones, D.S.; Dilchert, S. Managing Human Resource for Environmental Sustainability; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Pearson, J. Turning Point. Are We Doing the Right Thing? Leadership and Prioritisation for Public Benefit. J. Corp. Citizsh. 2010, 2010, 37–40. [Google Scholar] [CrossRef]

- Nyilasy, G.; Gangadharbatla, H.; Paladino, A. Perceived Greenwashing: The Interactive Effects of Green Advertising and Corporate Environmental Performance on Consumer Reactions. J. Bus. Ethics 2013, 125, 693–707. [Google Scholar] [CrossRef]

- Delmas, M.A.; Burbano, V.C. The Drivers of Greenwashing. Calif. Manag. Rev. 2011, 54, 64–87. [Google Scholar] [CrossRef] [Green Version]

- Fredriksson, P.G. How Pollution Taxes may Increase Pollution and Reduce Net Revenues. Public Choice 2001, 107, 65–85. [Google Scholar] [CrossRef]

- Schneider, F. The Influence of Public Institutions on the Shadow Economy: An Empirical Investigation for OECD Countries. Rev. Law Econ. 2010, 6, 441–468. [Google Scholar] [CrossRef]

- Singh, N.M. Environmental justice, degrowth and post-capitalist futures. Ecol. Econ. 2019, 163, 138–142. [Google Scholar] [CrossRef]

- Cosme, I.; Santos, R.; O’Neill, D. Assessing the degrowth discourse: A review and analysis of academic degrowth policy proposals. J. Clean. Prod. 2017, 149, 321–334. [Google Scholar] [CrossRef] [Green Version]

- Pellegrini, L.; Gerlagh, R. An Empirical Contribution to the Debate. Environ. Dev. 2006, 15, 332–354. [Google Scholar] [CrossRef]

- Ossewaarde, M.; Ossewaarde-Lowtoo, R. The EU’s Green Deal: A Third Alternative to Green Growth and Degrowth? Sustainability 2020, 12, 9825. [Google Scholar] [CrossRef]

- Milanovic, B. Global Inequality: A New Approach for the Age of Globalization, 1st ed.; Belknap Press: London, UK, 2016. [Google Scholar]

- Blažej, A.; Ambrozy, M. Some aspects of the problems of keeping sustainable development in the philosophy of Martin Heidegger. Int. J. Multidiscip. Thought 2013, 3, 385–391. [Google Scholar]

- Vargas-Hernández, J.G. Bio-Economy at the Crossroads of Sustainable Development. In Advanced Integrated Approaches to Environmental Economics and Policy: Emerging Research and Opportunities; IGI Global: Hershey, PA, USA, 2019; pp. 23–48. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Item | Description |

|---|---|

| Source | Journals, books, paper works or reports |

| Query | Topic: “environmental economics” AND ”environmental problems” AND “environmental-accounting system” OR ”the SEEA” OR “national accounts ”AND “green consumerism” AND “fiscal policy” AND “De-growth” AND “sustainability” OR “sustainable development goals” OR “sustainable economy” Refined by: Languages—(English), Subject area—Environmental economics and sustainability, Source type—Articles, books, official papers, works or reports from governments or related institutions. |

| Hits | 370 |

| Papers retained after: | |

| - Cite selection; | 200 |

| - Title and abstract selection; | 130 |

| - Full-text selection; | 90 |

| - Backward and forward search. | 81 |

| Article | Year | Source Type | Environmental Economics | The Sustainable Development Goals (SDGs) | ||||

|---|---|---|---|---|---|---|---|---|

| The Concept | Environmental–Economics Accounting System | Green Consumerism | Fiscal Policy | De-Growth | ||||

| Huyhn, C.M. | 2020 | Journal | ✓ | |||||

| Biswas et al. | 2012 | Journal | ✓ | |||||

| Pirmana | 2020 | Journal | ✓ | |||||

| Obst and Vardon | 2014 | Journal | ✓ | |||||

| Sachs, J.D. | 2012 | Journal | ✓ | |||||

| Mio et al. | 2020 | Journal | ✓ | |||||

| The United Nations | 015 | Report | ✓ | |||||

| Beder | 2011 | Journal | ✓ | |||||

| Medina and Schneider | 2018 | Journal | ✓ | |||||

| Ambec and Donder | 2022 | Journal | ✓ | |||||

| Ulph and Ulph | 2021 | Journal | ✓ | |||||

| Barry Field | 2017 | Book | ✓ | |||||

| Pearce | 2002 | Book | ✓ | |||||

| Sagoff | 2012 | Journal | ✓ | |||||

| Nadeau | 2015 | Journal | ✓ | |||||

| Lele | 1991 | Journal | ✓ | |||||

| Venkatachalam | 2006 | Journal | ✓ | |||||

| Kahneman and Knetsch | 1992 | Journal | ✓ | |||||

| Beder | 1996 | Journal | ✓ | |||||

| Johnson | 1996 | Book | ✓ | |||||

| Ubeda et al. | 2020 | Journal | ✓ | |||||

| Jakob and Edenhofer | 2014 | Journal | ✓ | ✓ | ||||

| Vardon et al. | 2018 | Journal | ✓ | |||||

| Bwanakare | 2019 | Book | ✓ | |||||

| The UN and Eaccounting | 2010 | Book | ✓ | |||||

| The UN | 2003 | Book | ✓ | |||||

| Dagher | 2014 | Journal | ✓ | |||||

| Tseng | 2016 | Journal | ✓ | |||||

| Paetz et al. | 2012 | Journal | ✓ | |||||

| Haytko and Matulich | 2008 | Journal | ✓ | |||||

| Wiedenhofer et al. | 2017 | Journal | ✓ | |||||

| Han et al. | 2009 | Journal | ✓ | |||||

| Laroche et al. | 2001 | Journal | ✓ | |||||

| Mostafa | 2007 | Journal | ✓ | |||||

| Stern | 2000 | Journal | ✓ | |||||

| Elsantil | 2021 | Journal | ✓ | |||||

| Paul et al. | 2016 | Journal | ✓ | |||||

| Pearce and Atkinson | 2017 | Journal | ✓ | |||||

| Battaglini and Coate | 2016 | Journal | ✓ | |||||

| Galinato and Islam | 2014 | Journal | ✓ | |||||

| Hyunh et al. | 2019 | Journal | ✓ | |||||

| Antweiler et al. | 2001 | Journal | ✓ | |||||

| Mani and Wheeler | 1998 | Journal | ✓ | |||||

| Vazquez and Ubeda | 2021 | Journal | ✓ | |||||

| Win and Paradigm | 2009 | Journal | ✓ | |||||

| Sorman and Giampietro | 2013 | Journal | ✓ | |||||

| Corbett | 2009 | Journal | ✓ | |||||

| Latouche | 2009 | Book | ✓ | |||||

| Felber | 2015 | Book | ✓ | |||||

| Lorek andand Fuchs | 2013 | Journal | ✓ | |||||

| Gomes et al. | 2012 | Book | ✓ | |||||

| Alcott | 2011 | Journal | ✓ | |||||

| The United Nations | 2018 | Report | ✓ | |||||

| Hutton et al. | 2018 | Journal | ✓ | |||||

| Bennich et al. | 2020 | Journal | ✓ | |||||

| Cordova andand Celone | 2019 | Journal | ✓ | |||||

| Fuso Nerini | 2019 | Journal | ✓ | |||||

| Muff et al. | 2017 | Journal | ✓ | |||||

| Walz et al. | 2017 | Journal | ✓ | |||||

| Pedersen | 2018 | Journal | ✓ | |||||

| Zhang et al. | 2016 | Journal | ✓ | |||||

| Xue et al. | 2021 | Journal | ✓ | |||||

| Chay et al. | 2015 | Journal | ✓ | |||||

| Arnzt | 2012 | Journal | ✓ | |||||

| Wang et al. | 2020 | Journal | ✓ | |||||

| Christopher | 2016 | Journal | ✓ | |||||

| Gerlagh et al. | 2018 | Journal | ✓ | |||||

| Pereira | 2017 | Journal | ✓ | |||||

| Schneider et al. | 2010 | Journal | ✓ | |||||

| Infante et al. | 2011 | Journal | ✓ | |||||

| Pirmana et al. | 2019 | Journal | ✓ | |||||

| Jackson et al. | 2012 | Book | ✓ | |||||

| Fredriksson | 2001 | Journal | ✓ | |||||

| G. Nyilasi, H. et al. | 2014 | Journal | ✓ | |||||

| Magali, A. et al. | 2011 | Journal | ✓ | |||||

| Schneider | 2010 | Journal | ✓ | |||||

| Singh | 2019 | Journal | ✓ | |||||

| Cosme et al. | 2017 | Journal | ✓ | |||||

| Pellgrini and Gerlagh | 2006 | Journal | ✓ | |||||

| Ossewaarde | 2020 | Journal | ✓ | |||||

| Milanovic | 2016 | Journal | ✓ | |||||

| Environmental Economics | |||||

|---|---|---|---|---|---|

| Environmental–Economics Accounting System | Green Consumerism | Fiscal Policy | De-Growth | ||

| The Sustainable Development Goals (SDGs) |  | ✓ | ✓ | ✓ | |

| |||||

| ✓ | ✓ | ✓ | ||

| |||||

| |||||

| ✓ | ||||

| ✓ | ||||

| |||||

| ✓ | ||||

| |||||

| ✓ | ||||

| ✓ | ✓ | ✓ | ||

| ✓ | ✓ | ✓ | ||

| ✓ | ||||

| ✓ | ✓ | |||

| |||||

| |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Setioningtyas, W.P.; Illés, C.B.; Dunay, A.; Hadi, A.; Wibowo, T.S. Environmental Economics and the SDGs: A Review of Their Relationships and Barriers. Sustainability 2022, 14, 7513. https://doi.org/10.3390/su14127513

Setioningtyas WP, Illés CB, Dunay A, Hadi A, Wibowo TS. Environmental Economics and the SDGs: A Review of Their Relationships and Barriers. Sustainability. 2022; 14(12):7513. https://doi.org/10.3390/su14127513

Chicago/Turabian StyleSetioningtyas, Widhayani Puri, Csaba Bálint Illés, Anna Dunay, Abdul Hadi, and Tony Susilo Wibowo. 2022. "Environmental Economics and the SDGs: A Review of Their Relationships and Barriers" Sustainability 14, no. 12: 7513. https://doi.org/10.3390/su14127513