With the increasingly strict background of China’s environmental regulation and the increasingly significant trend of the impact of environmental policies on the development of enterprises, based on environmental regulation policy produced by the externality theory, this study takes the listed manufacturing enterprises in the Beijing–Tianjin–Hebei region as the research sample to discuss the economic impact of environmental regulation on the manufacturing enterprises in this region and its impact mechanism.

For the first research question of this paper, the difference between this paper and some analyzed literature is that they have studied the impact of environmental regulation on enterprises from many other aspects. For example, Sharma (2000) [

16] focuses the impact of environmental regulation on the strategic planning of enterprises and some analyzed literature focus more on the impact of environmental regulation on the quantity of enterprise investment (Zhang, J., 2016 [

26]; Yuan, Y.J. and Xie, R.H., 2016; Zhou, H.N., 2019 [

34]) or the overall production efficiency of enterprises (Isabelle Piot–Lepetit, 2007 [

18]; Chintrakam, 2008), while this paper focuses on the impact of environmental regulation on the investment quality, i.e., investment efficiency. For the verification of “Porter Hypothesis”, some analyzed literature focused more on the positive impact of enterprise innovation caused by environmental regulation on enterprise research and development, governance cost, productivity, and technological development (Jaffe and Palmer, 1997 [

29]; Brunnermeier and Cohen, 2003 [

30]; Hamamoto, 2006 [

31]; Ramanathan, R. et al., 2017 [

22]; Garcia-Quevedo, 2021 [

24]; Yang, Y.L., 2020 [

33]). Other analyzed researchers also believe that environmental regulation improves the private investment efficiency of enterprises and reduces the investment opportunities of enterprises (Yao Du et al., 2018 [

27]; Z. Feng et al., 2018 [

28]), that appropriate environmental management and investment strategies enable enterprises to reduce costs and risks so as to improve energy efficiency and achieve sustainable development (Song, H.X., 2016 [

23]; Xiong, F.P. and Bo, W.A. et al., 2019), and that only when enterprises overinvest can environmental regulation policies improve enterprise investment efficiency (Li, T., 2021 [

36]). However, some analyzed literature included the use of the data of their country to conclude that there is no obvious relationship between environmental regulation and enterprise performance (Stoeve, J., 2018 [

20]) and that environmental regulation policies have an inhibitory effect on enterprise investment efficiency (Paulsson, 2004 [

17]; Zhou, H.N., 2019 [

34]; Wang, X.H., 2020 [

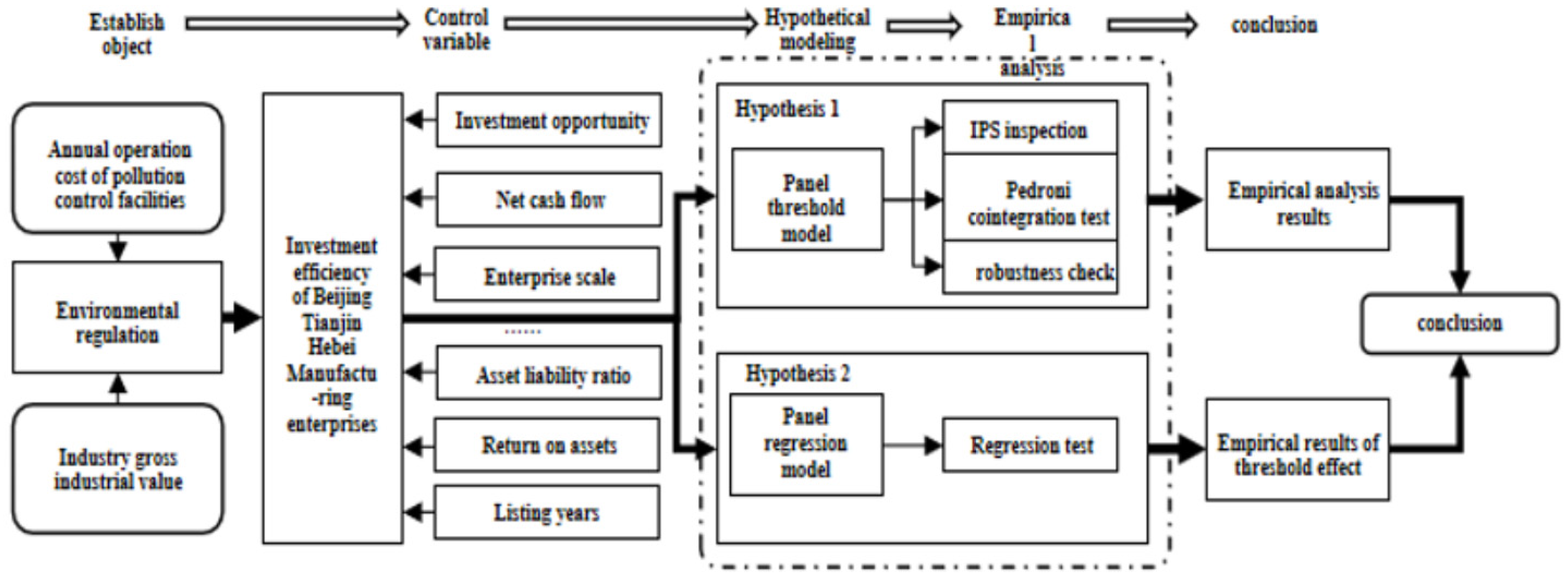

35]). Therefore, at present, scholars have yet to reach a consensus on the impact of environmental regulation on enterprise investment efficiency. In this paper, through the analysis of the industrial characteristics of manufacturing enterprises and the characteristics of environmental regulation policies in the Beijing–Tianjin–Hebei region, the Hypothesis 1 is put forward that environmental regulation does not significantly promote the investment efficiency of enterprises in the Beijing–Tianjin–Hebei region. The research results show that the impact of environmental regulation intensity on enterprise investment efficiency is negative, which responds to the first research question proposed in this paper and is also the same as some experts’ research views on the inhibitory effect of environmental regulation policies on enterprise investment efficiency, which reflects the fact that manufacturing in the Beijing–Tianjin–Hebei region is mainly the traditional resource- and labor-intensive manufacturing industry and its technological innovation ability is not strong on the whole. The contribution is to take a national key development area as the research scope to explore the impact of environmental regulation on investment efficiency and explain that due to the existence of inducing factors of environmental regulation, manufacturing enterprises face more stringent internal and external management systems and stronger financing constraints limiting the occurrence of investment behavior. From the perspective of empirical analysis, this paper extends the research on the relationship between environmental regulation and manufacturing investment efficiency, and the research results have reference value for regional coordinated development.

For the second research question of this paper, the impact mechanism of environmental regulation on investment efficiency in the Beijing–Tianjin–Hebei region, some analyzed literature have found that different environmental policies and measures have a threshold effect on technological innovation (Shen, N., 2012 [

37]) and in promoting the upgrading of industrial structure (Song, W.X., Han, W.H., 2021 [

42]). Due to the regional gap, time gap and industrial gap in the economic effects of environmental regulation, it is difficult to determine the size of “compliance cost” and “innovation compensation” and the economic effects of environmental regulation are nonlinear (Conrad and Wastl, 1995 [

39]; Lanoie et al., 2008 [

40]). Some other analyzed literature focus on the impact of environmental regulation on enterprise innovation, which showed that when the intensity of environmental regulation exceeds a specific “threshold”, the existence of environmental regulation will bring opportunities for innovative production (Su, H., 2018 [

38]; Pang, M.C. and Ning F.X., 2022 [

41]). Based on them, the Hypothesis 2 is put forward that there is a nonlinear threshold effect in the impact of environmental regulation intensity on enterprise investment efficiency. Different from the analyzed literature, this paper answers the problem of the impact mechanism of regional environmental regulation on investment efficiency in a coordinated development region. Similar to the analyzed literature, the existence of threshold effect is verified. The panel threshold model is constructed to verify the existence of threshold effect in this paper. The results of this study clearly show that when the intensity of environmental regulation exceeds the threshold value of 2.2358, it has a significant negative impact on the investment efficiency of enterprises, which shows that environmental regulation tends to make the internal management system of enterprises more strictly. Once it exceeds a certain critical point, it will inhibit investment behavior. The contribution of this study is that in the face of more and more strict environmental regulation in regions with rapid collaborative development, such as the environmental regulation policy in the Beijing–Tianjin–Hebei region, when making policy in the face of manufacturing industry, we need to consider the threshold and make targeted adjustment to achieve a win-win situation of environmental protection and investment growth. The research conclusion has certain practical value for the coordinated development region to coordinate the unbalanced relationship between environment and economy and realize the healthy and benign development of both on the basis of reasonable responses to environmental regulation and improving pollution prevention and control.

{kind=link}