Corruption and FDI in Brazil: Contesting the “Sand” or “Grease” Hypotheses

, ,

, ,

Abstract

:1. Introduction

2. Literature Review

2.1. FDI and Corruption in Emerging Economies

2.2. FDI and Corruption—The “Sand or Grease” Theory

3. Methods

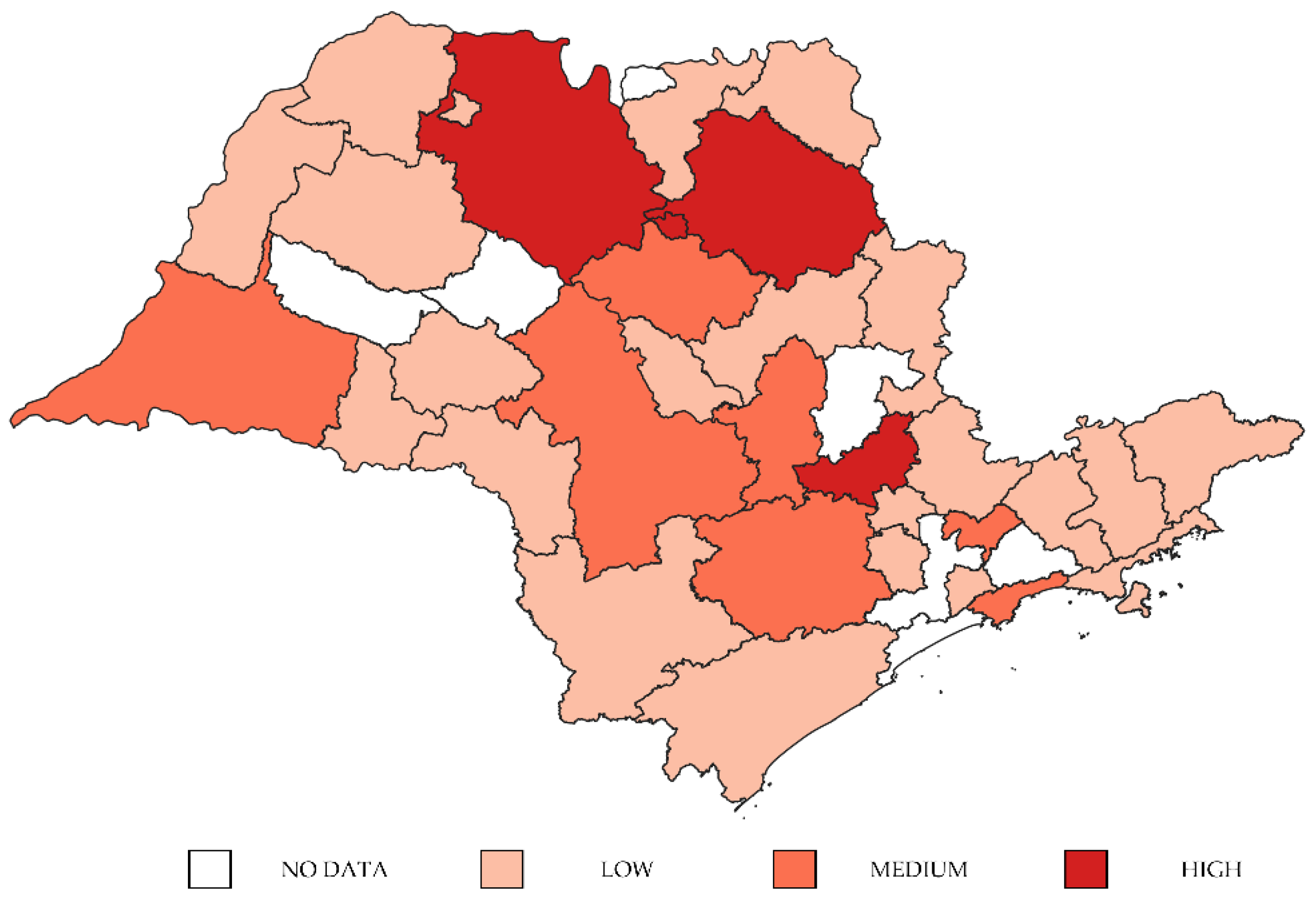

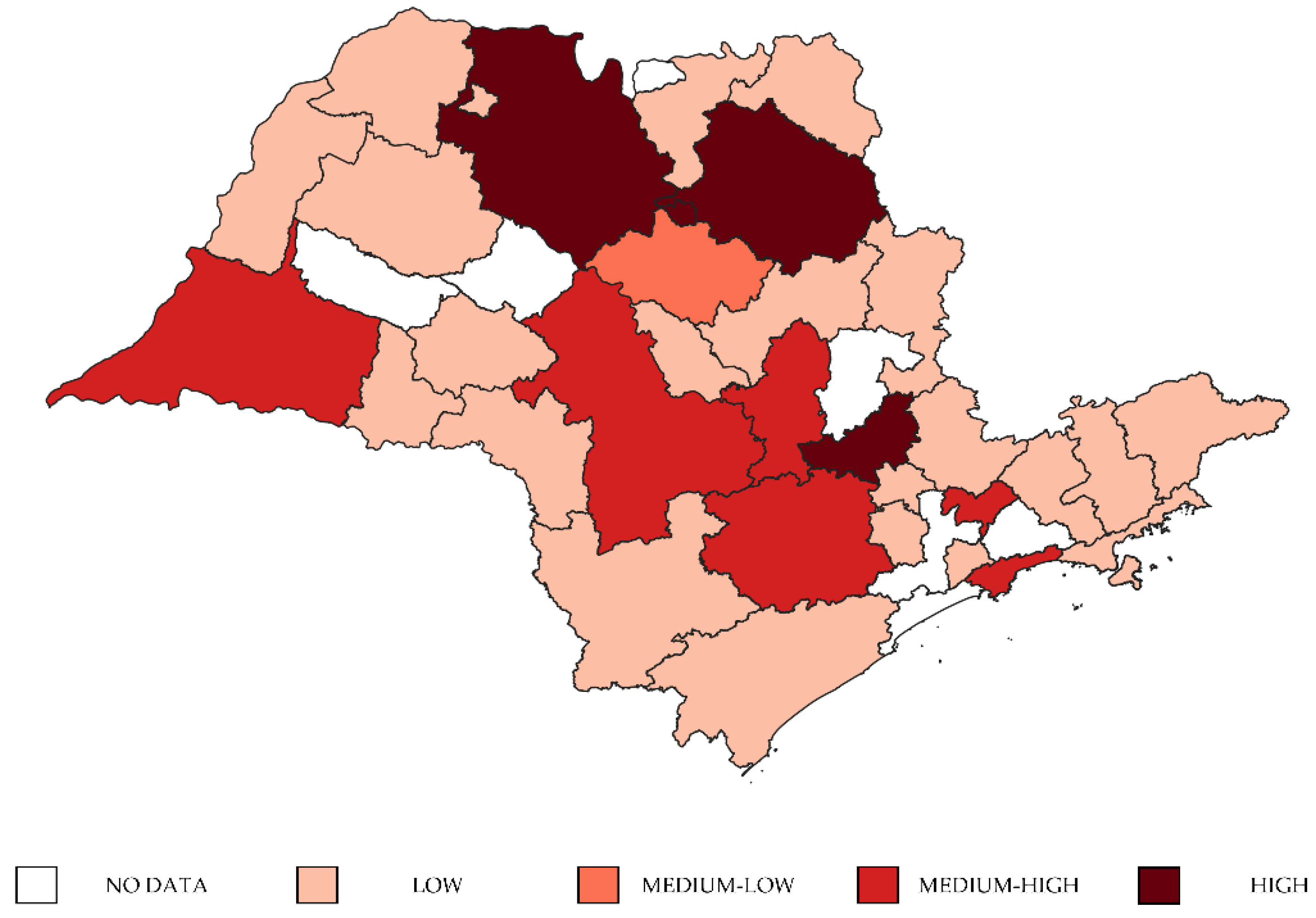

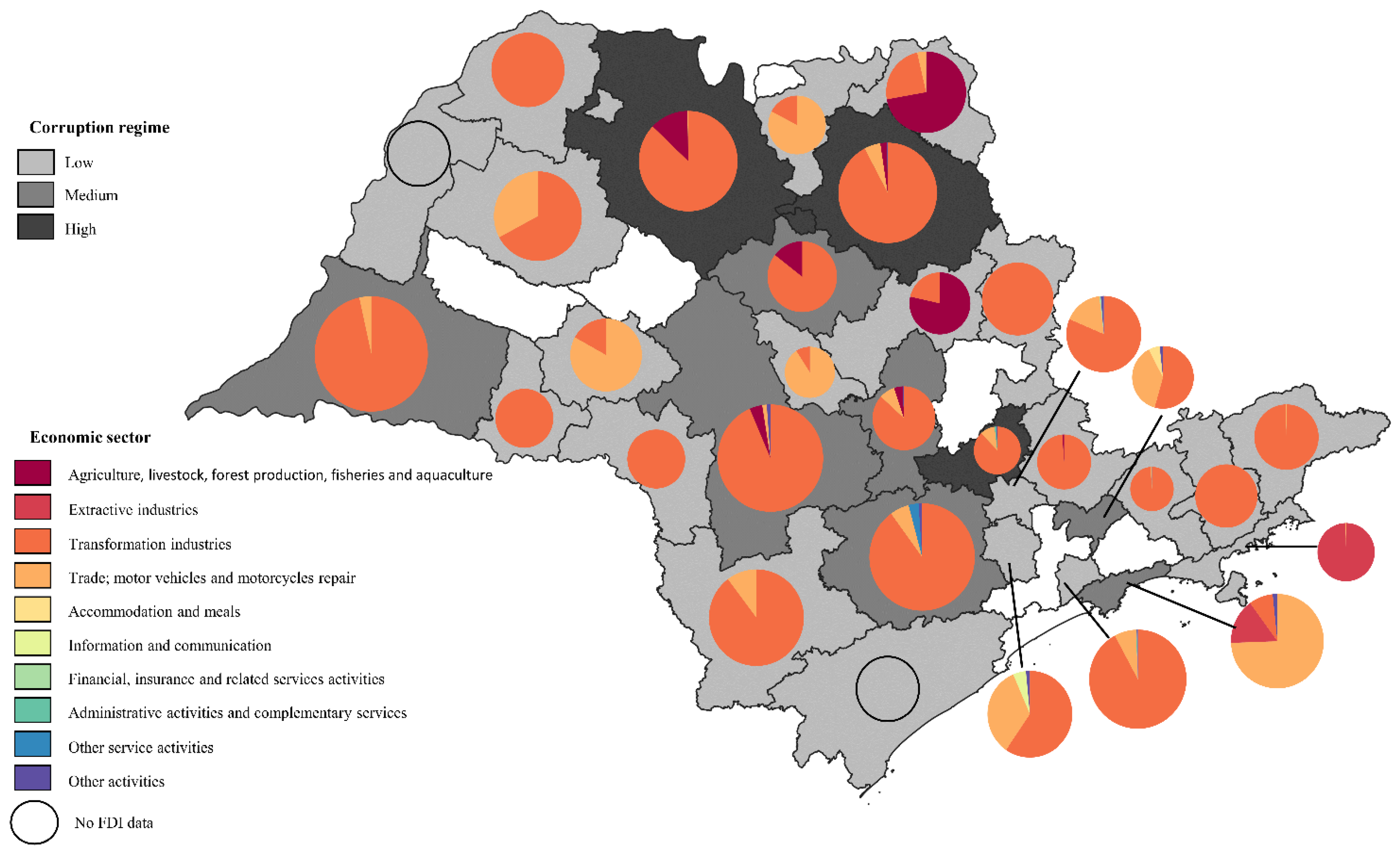

3.1. Data Sources and Variables

- MNC is the number of exporting multinational companies in the region “j”;

- T is the regional whole population of exporting companies (domestic and foreign) in the region j;

- W is the adjustment weight (based on its exporting value) for each company “i”;

- k is the total number of companies in each region;

- s represents each of the 31 regions Judicial Subsections of the São Paulo state.

3.2. Econometric Model and Estimation Strategy

- FDI: Foreign direct investment;

- X: Regional-level controls;

- C: Corruption proxy;

- I(.): Is an indicator function;

- ai: Regional time-invariant characteristics (Fixed Effects);

- γi: Thresholds to be estimated;

- ε: Stochastic disturbance.

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dhahri, S.; Omri, A. Foreign Capital towards SDGs 1 & 2—Ending Poverty and Hunger: The Role of Agricultural Production. Struct. Change Econ. Dyn. 2020, 53, 208–221. [Google Scholar] [CrossRef]

- Gherghina, Ş.C.; Simionescu, L.N.; Hudea, O.S. Exploring Foreign Direct Investment-Economic Growth Nexus-Empirical Evidence from Central and Eastern European Countries. Sustainability 2019, 11, 5421. [Google Scholar] [CrossRef] [Green Version]

- Rjou, H.; Abu Alrub, A.; Soyer, K.; Hamdan, S. The Syndrome of FDI and Economic Growth: Evidence from Latin American Countries. J. Financ. Stud. Res. 2016, 2016, 1–8. [Google Scholar] [CrossRef] [Green Version]

- Uttama, N.P. Foreign Direct Investment and the Poverty Reduction Nexus in Southeast Asia. In Economic Studies in Inequality, Social Exclusion and Well-Being; Springer: Singapore, 2015; pp. 281–298. ISBN 9789812874207. [Google Scholar]

- Aust, V.; Morais, A.I.; Pinto, I. How Does Foreign Direct Investment Contribute to Sustainable Development Goals? Evidence from African Countries. J. Clean. Prod. 2020, 245, 118823. [Google Scholar] [CrossRef]

- Barassi, M.R.; Zhou, Y. The Effect of Corruption on FDI: A Parametric and Non-Parametric Analysis. Eur. J. Political Econ. 2012, 28, 302–312. [Google Scholar] [CrossRef] [Green Version]

- Meyer, K.E.; Nguyen, H.V. Foreign Investment Strategies and Sub-National Institutions in Emerging Markets: Evidence from Vietnam. J. Manag. Stud. 2005, 42, 63–93. [Google Scholar] [CrossRef]

- Freckleton, M.; Wright, A.; Craigwell, R. Economic Growth, Foreign Direct Investment and Corruption in Developed and Developing Countries. J. Econ. Stud. 2012, 39, 639–652. [Google Scholar] [CrossRef]

- Wei, S.-J. How Taxing Is Corruption on International Investors? Rev. Econ. Stat. 2000, 82, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Kaufmann, D. Corruption: The Facts. Foreign Policy 1997, 107, 114–131. [Google Scholar] [CrossRef]

- Urbina, D.A. The Consequences of a Grabbing Hand: Five Selected Ways in Which Corruption Affects the Economy. Economía 2020, 43, 65–88. [Google Scholar] [CrossRef]

- Bardhan, P.; Berthelemy, C.; Goudie, A.; Olson, M.; Rodrik, D.; Rose-Ackermnan, S.; Shleifer, A. Corruption and Development: A Review of Issues. J. Econ. Lit. 1997, 35, 1320–1346. [Google Scholar]

- Driffield, N.; Jones, C.; Kim, J.Y.; Temouri, Y. FDI Motives and the Use of Tax Havens: Evidence from South Korea. J. Bus. Res. 2021, 135, 644–662. [Google Scholar] [CrossRef]

- Polloni-Silva, E.; Moralles, H.F.; Rebelatto, D.A.d.N.; Hartmann, D. Are Foreign Companies a Blessing or a Curse for Local Development in Brazil? It Depends on the Home Country and Host Region’s Institutions. Growth Change 2021, 52, 933–962. [Google Scholar] [CrossRef]

- Moralles, H.F.; Moreno, R. FDI Productivity Spillovers and Absorptive Capacity in Brazilian Firms: A Threshold Regression Analysis. Int. Rev. Econ. Financ. 2020, 70, 257–272. [Google Scholar] [CrossRef]

- Kaulihowa, T.; Adjasi, C. FDI and Welfare Dynamics in Africa. Thunderbird Int. Bus. Rev. 2018, 60, 313–328. [Google Scholar] [CrossRef]

- Sunde, T. Foreign Direct Investment, Exports and Economic Growth: ADRL and Causality Analysis for South Africa. Res. Int. Bus. Financ. 2017, 41, 434–444. [Google Scholar] [CrossRef]

- Akhmetzaki, Y.Z.; Mukhamediyev, B.M. Fdi Determinants in the Eurasian Economic Union Countries and Eurasian Economic Integration Effect on Fdi Inflows. Econ. Reg. 2017, 13, 959–970. [Google Scholar] [CrossRef]

- Ashurov, S.; Abdullah Othman, A.H.; bin Rosman, R.; bin Haron, R. The Determinants of Foreign Direct Investment in Central Asian Region: A Case Study of Tajikistan, Kazakhstan, Kyrgyzstan, Turkmenistan and Uzbekistan (A Quantitative Analysis Using GMM). Russ. J. Econ. 2020, 6, 162–176. [Google Scholar] [CrossRef]

- Dhrifi, A.; Jaziri, R.; Alnahdi, S. Does Foreign Direct Investment and Environmental Degradation Matter for Poverty? Evidence from Developing Countries. Struct. Change Econ. Dyn. 2020, 52, 13–21. [Google Scholar] [CrossRef]

- Lin, M.; Kwan, Y.K. FDI Technology Spillovers, Geography, and Spatial Diffusion. Int. Rev. Econ. Financ. 2016, 43, 257–274. [Google Scholar] [CrossRef] [Green Version]

- Lee, J.W. The Contribution of Foreign Direct Investment to Clean Energy Use, Carbon Emissions and Economic Growth. Energy Policy 2013, 55, 483–489. [Google Scholar] [CrossRef]

- Agarwal, M.; Atri, P.; Kundu, S. Foreign Direct Investment and Poverty Reduction: India in Regional Context. South Asia Econ. J. 2017, 18, 135–157. [Google Scholar] [CrossRef]

- Soumaré, I. Does FDI Improve Economic Development in North African Countries? Appl. Econ. 2015, 47, 5510–5533. [Google Scholar] [CrossRef]

- Polloni-Silva, E.; Roiz, G.A.; Mariano, E.B.; Moralles, H.F.; Rebelatto, D.A.N. The Environmental Cost of Attracting FDI: An Empirical Investigation in Brazil. Sustainability 2022, 14, 4490. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R. Oil Abundance and Economic Growth; Logos: Berlin, Germany, 2016; ISBN 9783832543426. [Google Scholar]

- Magombeyi, M.T.; Odhiambo, N.M. FDI Inflows and Poverty Reduction in Botswana: An Empirical Investigation. Cogent Econ. Financ. 2018, 6, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Ganić, M. Does Foreign Direct Investment (FDI) Contribute to Poverty Reduction? Empirical Evidence from Central European and Western Balkan Countries. Sci. Ann. Econ. Bus. 2019, 66, 15–27. [Google Scholar] [CrossRef] [Green Version]

- Cheung, Y.W.; Qian, X. Empirics of China’s Outward Direct Investment. Pac. Econ. Rev. 2009, 14, 312–341. [Google Scholar] [CrossRef] [Green Version]

- Kolstad, I.; Wiig, A. What Determines Chinese Outward FDI? J. World Bus. 2012, 47, 26–34. [Google Scholar] [CrossRef]

- Rogmans, T.; Ebbers, H. The Determinants of Foreign Direct Investment in the Middle East North Africa Region. Int. J. Emerg. Mark. 2013, 8, 240–257. [Google Scholar] [CrossRef] [Green Version]

- Puatwoe, J.T.; Piabuo, S.M. Financial Sector Development and Economic Growth: Evidence from Cameroon. Financ. Innov. 2017, 3, 25. [Google Scholar] [CrossRef]

- Safaee, M.; Gerayli, M.S. Family Control and Corporate Social Responsibility: Evidence from Iranian Companies. Int. J. Financ. Eng. 2017, 4, 1750046. [Google Scholar] [CrossRef]

- Hoang, H.H.; Huynh, C.M.; Duong, N.M.H.; Chau, N.H. Determinants of Foreign Direct Investment in Southern Central Coast of Vietnam: A Spatial Econometric Analysis. Econ. Change Restruct. 2022, 55, 285–310. [Google Scholar] [CrossRef]

- William, P. Wan Country Resource Environments, Firm Capabilities, and Corporate Diversification Strategies. J. Manag. Stud. 2005, 42, 161–181. [Google Scholar]

- Charpin, R.; Powell, E.E.; Roth, A.V. The Influence of Perceived Host Country Political Risk on Foreign Subunits’ Supplier Development Strategies. J. Oper. Manag. 2021, 67, 329–359. [Google Scholar] [CrossRef]

- Ketteni, E.; Kottaridi, C. The Impact of Regulations on the FDI-Growth Nexus within the Institution-Based View: A Nonlinear Specification with Varying Coefficients. Int. Bus. Rev. 2019, 28, 415–427. [Google Scholar] [CrossRef]

- Chaudhry, I.S.; Yin, W.; Ali, S.A.; Faheem, M.; Abbas, Q.; Farooq, F.; Ur Rahman, S. Moderating Role of Institutional Quality in Validation of Pollution Haven Hypothesis in BRICS: A New Evidence by Using DCCE Approach. Environ. Sci. Pollut. Res. 2022, 29, 9193–9202. [Google Scholar] [CrossRef]

- Slesman, L.; Abubakar, Y.A.; Mitra, J. Foreign Direct Investment and Entrepreneurship: Does the Role of Institutions Matter? Int. Bus. Rev. 2021, 30, 101774. [Google Scholar] [CrossRef]

- Chih, Y.Y.; Kishan, R.P.; Ojede, A. Be Good to Thy Neighbours: A Spatial Analysis of Foreign Direct Investment and Economic Growth in Sub-Saharan Africa. World Econ. 2022, 45, 657–701. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R.; Löwenstein, W.; Ferrari, M. International Journal of Energy Economics and Policy Privatization and the Role of Sub-National Governments in the Latin American Power Sector: A Plea for Less Subsidiarity? Int. J. Energy Econ. Policy 2018, 8, 95–103. [Google Scholar]

- Krammer, S.M.S. Greasing the Wheels of Change: Bribery, Institutions, and New Product Introductions in Emerging Markets. J. Manag. 2017, 45, 1889–1926. [Google Scholar] [CrossRef] [Green Version]

- Wellalage, N.; Thrikawala, S. Does Bribery Sand or Grease the Wheels of Firm Level Innovation: Evidence from Latin American Countries. J. Evol. Econ. 2021, 31, 891–929. [Google Scholar] [CrossRef]

- Tanzi, V.; Davoodi, H. Corruption, Public Investment and Growth; International Monetary Fund: Washington, DC, USA, 1997; Volume 97. [Google Scholar]

- Svensson, J. Eight Questions about Corruption. J. Econ. Perspect. 2005, 19, 19–42. [Google Scholar] [CrossRef] [Green Version]

- Uhlenbruck, K.; Rodriguez, P.; Doh, J.; Eden, L. The Impact of Corruption on Entry Strategy: Evidence from Telecommunication Projects in Emerging Economies. Organ. Sci. 2006, 17, 402–414. [Google Scholar] [CrossRef] [Green Version]

- Martin, K.D.; Johnson, J.L.; Cullen, J.B. Organizational Change, Normative Control Deinstitutionalization, and Corruption. Bus. Ethics Q. 2009, 19, 105–130. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C.; Fleming, P.J.; Rothenberg, S. Rationalization, Overcompensation and the Escalation of Corruption in Organizations. J. Bus. Ethics 2009, 84, 65–73. [Google Scholar] [CrossRef]

- Torsello, D.; Venard, B. The Anthropology of Corruption. J. Manag. Inq. 2016, 25, 34–54. [Google Scholar] [CrossRef]

- Zyglidopoulos, S.C.; Fleming, P.J. Ethical Distance in Corrupt Firms: How Do Innocent Bystanders Become Guilty Perpetrators? J. Bus. Ethics 2008, 78, 265–274. [Google Scholar] [CrossRef]

- Svensson, J. Who Must Pay Bribes and How Much? Evidence from a Cross Section of Firms. Q. J. Econ. 2003, 118, 207–230. [Google Scholar] [CrossRef] [Green Version]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. Governance Matters VII: Aggregate and Individual Governance Indicators 1996–2007. In Non-State Actors as Standard Setters; Cambridge University Press: Cambridge, UK, 2009; pp. 146–188. [Google Scholar] [CrossRef] [Green Version]

- Transparency International Corruption Perceptions. Available online: http://cpi.transparency.org/cpi2013/results/ (accessed on 19 February 2022).

- Kotabe, M.; Jiang, C.X.; Murray, J.Y. Examining the Complementary Effect of Political Networking Capability with Absorptive Capacity on the Innovative Performance of Emerging-Market Firms. J. Manag. 2017, 43, 1131–1156. [Google Scholar] [CrossRef]

- Habiyaremye, A.; Raymond, W. Working Paper Series Transnational Corruption and Innovation in Transition Economies; United Nations University—Maastricht Economic and Social Research Institute on Innovation and Technology (MERIT): Maastricht, The Netherlands, 2013. [Google Scholar]

- Habiyaremye, A.; Raymond, W. How Do Foreign Firms’ Corruption Practices Affect Innovation Performance in Host Countries? Industry-Level Evidence from Transition Economies. Innovation 2018, 20, 18–41. [Google Scholar] [CrossRef]

- Ojide, M.G.; Agu, C.O.; Ohalete, P.; Chinanuife, E. Nigerian Economic Policy Response to COVID-19: An Evaluation of Policy Actors’ Views. Poverty Public Policy 2022, 14, 69–85. [Google Scholar] [CrossRef] [PubMed]

- Soh, W.N.; Muhamad, H.; San, O.T. The Impact of Government Efficiency, Corruption, and Inflation on Public Debt: Empirical Evidence from Advanced and Emerging Economies. Pertanika J. Soc. Sci. Humanit. 2021, 29, 1551–1570. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R.; Gatto, A.; Niftiyev, I. E-Government and Petty Corruption in Public Sector Service Delivery. Technol. Anal. Strateg. Manag. 2022. [Google Scholar] [CrossRef]

- Bouzahzah, M. Pollution Haven Hypothesis in Africa: Does the Quality of Institutions Matter? Int. J. Energy Econ. Policy 2022, 12, 101–109. [Google Scholar] [CrossRef]

- Fungáčová, Z.; Kochanova, A.; Weill, L. Does Money Buy Credit? Firm-Level Evidence on Bribery and Bank Debt. World Dev. 2015, 68, 308–322. [Google Scholar] [CrossRef] [Green Version]

- Chewaka, D.B.; Zhang, C. Multinational Firm Growth and Sustainability Responses to Dynamics of Business Regulations in Host Market. Sustainability 2021, 13, 13945. [Google Scholar] [CrossRef]

- Ghosh, C.; Narayan, P.C.; Prasadh, R.S.; Thenmozhi, M. Does Corruption Distance Affect Cross-Border Acquisitions? Different Tales from Developed and Emerging Markets. Eur. Financ. Manag. 2022, 28, 345–402. [Google Scholar] [CrossRef]

- Fisman, R.; Svensson, J. Are Corruption and Taxation Really Harmful to Growth? Firm Level Evidence. J. Dev. Econ. 2007, 83, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Mauro, P. Corruption and Growth. Q. J. Econ. 1995, 110, 681–712. [Google Scholar] [CrossRef]

- Reinikka, R.; Svensson, J. Fighting Corruption to Improve Schooling: Evidence from a Newspaper Campaign in Uganda. J. Eur. Econ. Assoc. 2005, 3, 259–267. [Google Scholar] [CrossRef]

- Glaeser, E.L.; Kallal, H.D.; Scheinkman, J.A.; Shleifer, A. Growth in Cities. J. Political Econ. 1992, 100, 1126–1152. [Google Scholar] [CrossRef]

- Sartor, M.A.; Beamish, P.W. Host Market Government Corruption and the Equity-Based Foreign Entry Strategies of Multinational Enterprises. J. Int. Bus. Stud. 2018, 49, 346–370. [Google Scholar] [CrossRef]

- Cuervo-Cazurra, A. Who Cares about Corruption? J. Int. Bus. Stud. 2006, 37, 807–822. [Google Scholar] [CrossRef]

- Jadhav, P.; Katti, V. Institutional and Political Determinants of Foreign Direct Investment: Evidence from BRICS Economies. Poverty Public Policy 2012, 4, 49–57. [Google Scholar] [CrossRef]

- Qian, X.; Sandoval-Hernandez, J. Corruption Distance and Foreign Direct Investment. Emerg. Mark. Financ. Trade 2016, 52, 400–419. [Google Scholar] [CrossRef] [Green Version]

- Hakimi, A.; Hamdi, H. Does Corruption Limit FDI and Economic Growth? Evidence from MENA Countries. Int. J. Emerg. Mark. 2017, 12, 550–571. [Google Scholar] [CrossRef]

- Goedhuys, M.; Mohnen, P.; Taha, T. Corruption, Innovation and Firm Growth: Firm-Level Evidence from Egypt and Tunisia. Eurasian Bus. Rev. 2016, 6, 299–322. [Google Scholar] [CrossRef] [Green Version]

- Karaman Kabadurmuş, F.N. Corruption and Innovation: The Case of EECA Countries. J. Entrep. Innov. Manag. 2017, 6, 51–71. [Google Scholar]

- Bertrand, M.; Djankov, S.; Hanna, R.; Mullainathan, S. Obtaining a Driver’s License in India: An Experimental Approach to Studying Corruption. Q. J. Econ. 2007, 122, 1639–1676. [Google Scholar] [CrossRef]

- Krastanova, P. Greasing the Wheels of Innovation: How Corruption and Informal Practices of Firms Impact the Level of Innovation in Bulgaria Central European University. Master’s Thesis, Central European University, Budapest, Hungary, 2014. [Google Scholar]

- Sidki Darendeli, I.; Hill, T.L. Uncovering the Complex Relationships between Political Risk and MNE Firm Legitimacy: Insights from Libya. J. Int. Bus. Stud. 2016, 47, 68–92. [Google Scholar] [CrossRef]

- Helmy, H.E. The Impact of Corruption on FDI: Is MENA an Exception? Int. Rev. Appl. Econ. 2013, 27, 491–514. [Google Scholar] [CrossRef]

- Galang, R.M.N. Victim or Victimizer: Firm Responses to Government Corruption. J. Manag. Stud. 2012, 49, 429–462. [Google Scholar] [CrossRef]

- Zhu, J.; Wu, Y. Who Pays More “Tributes” to the Government? Sectoral Corruption of China’s Private Enterprises. Crime Law Soc. Change 2014, 61, 309–333. [Google Scholar] [CrossRef]

- Phan, N.H.; Nguyen, L.Q.T. FDI, Corruption and Development of Public Service Sectors in ASEAN Countries. J. Asian Financ. Econ. Bus. 2020, 7, 241–249. [Google Scholar] [CrossRef]

- Rygh, A.; Torgersen, K.; Benito, G.R.G. Institutions and Inward Foreign Direct Investment in the Primary Sectors. Rev. Int. Bus. Strategy, 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Nguyen, B.N.; Boruff, B.; Tonts, M. Looking through a Crystal Ball: Understanding the Future of Vietnam’s Minerals and Mining Industry. Extr. Ind. Soc. 2021, 8, 100907. [Google Scholar] [CrossRef]

- Berdiev, A.N.; Saunoris, J.W. Corruption and Entrepreneurship: Cross-Country Evidence from Formal and Informal Sectors. South. Econ. J. 2018, 84, 831–848. [Google Scholar] [CrossRef]

- Gao, Y. Mimetic Isomorphism, Market Competition, Perceived Benefit and Bribery of Firms in Transitional China. Aust. J. Manag. 2010, 35, 203–222. [Google Scholar] [CrossRef]

- Kouneva-Loewenthal, N.; Vojvodic, G. Corruption and Its Effect on Foreign Direct Investment in the Energy Sector of Emerging and Developing Economies. Prog. Int. Bus. Res. 2012, 7, 339–363. [Google Scholar] [CrossRef]

- Fredriksson, P.G.; List, J.A.; Millimet, D.L. Bureaucratic Corruption, Environmental Policy and Inbound US FDI: Theory and Evidence. J. Public Econ. 2003, 87, 1407–1430. [Google Scholar] [CrossRef] [Green Version]

- Cole, M.A.; Elliott, R.J.R.; Zhang, J. Corruption, Governance and FDI Location in China: A Province-Level Analysis. J. Dev. Stud. 2009, 45, 1494–1512. [Google Scholar] [CrossRef]

- Polloni-Silva, E.; Silveira, N.; Ferraz, D.; de Mello, D.S.; Moralles, H.F. The Drivers of Energy-Related CO2 Emissions in Brazil: A Regional Application of the STIRPAT Model. Environ. Sci. Pollut. Res. 2021, 28, 51745–51762. [Google Scholar] [CrossRef] [PubMed]

- Driscoll, J.C.; Kraay, A.C. Consistent Covariance Matrix Estimation with Spatially Dependent Panel Data. Rev. Econ. Stat. 1998, 80, 549–559. [Google Scholar] [CrossRef]

- Williams, R. Panel Data 4: Fixed Effects vs. Random Effects Models; University of Notre Dame: Paris, France, 2018. [Google Scholar]

- Croissant, Y.; Millo, G. Panel Data Econometrics in R: The Plm Package. J. Stat. Softw. 2008, 27, 1–43. [Google Scholar] [CrossRef] [Green Version]

- Wooldridge, J.M. Econometric Analysis of Cross Section and Panel Data; The MIT Press: Cambridge, MA, USA, 2010; ISBN 0262232588/780262232586. [Google Scholar]

- Beck, N.; Katz, J.N. What To Do (and Not to Do) with Time-Series Cross-Section Data. Am. Political Sci. Rev. 1995, 89, 634–647. [Google Scholar] [CrossRef]

- Hansen, B.E. Sample Splitting and Threshold Estimation. Econometrica 2000, 68, 575–603. [Google Scholar] [CrossRef] [Green Version]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef] [Green Version]

- Mark, E.S. XTIVREG2: Stata Module to Perform Extended IV/2SLS, GMM and AC/HAC, LIML and k- Class Regression for Panel Data Models (Version S456501); Boston College Department of Economics: Boston, MA, USA, 2005. [Google Scholar]

- Razzaq, A.; An, H.; Delpachitra, S. Does Technology Gap Increase FDI Spillovers on Productivity Growth? Evidence from Chinese Outward FDI in Belt and Road Host Countries. Technol. Forecast. Soc. Change 2021, 172, 121050. [Google Scholar] [CrossRef]

- Ashraf, A.; Herzer, D.; Nunnenkamp, P. The Effects of Greenfield FDI and Cross-Border M&As on Total Factor Productivity. World Econ. 2016, 39, 1728–1755. [Google Scholar] [CrossRef] [Green Version]

- Wang, D.T.; Gu, F.F.; Tse, D.K.; Yim, C.K.B. When Does FDI Matter? The Roles of Local Institutions and Ethnic Origins of FDI. Int. Bus. Rev. 2013, 22, 450–465. [Google Scholar] [CrossRef]

- Armijo, L.E.; Rhodes, S.D. Explaining Infrastructure Underperformance in Brazil: Cash, Political Institutions, Corruption, and Policy Gestalts. Policy Stud. 2017, 38, 231–247. [Google Scholar] [CrossRef]

- Lakshmi, G.; Saha, S.; Bhattarai, K. Does Corruption Matter for Stock Markets? The Role of Heterogeneous Institutions. Econ. Model. 2021, 94, 386–400. [Google Scholar] [CrossRef] [PubMed]

- Sabir, S.; Rafique, A.; Abbas, K. Institutions and FDI: Evidence from Developed and Developing Countries. Financ. Innov. 2019, 5, 8. [Google Scholar] [CrossRef] [Green Version]

- Erdogan, M.; Unver, M. Determinants of Foreign Direct Investments: Dynamic Panel Data Evidence. Int. J. Econ. Financ. 2015, 7, 82–95. [Google Scholar] [CrossRef] [Green Version]

- Tan, S.W.; Tran, T.T. The Effect of Local Governance on Firm Productivity and Resource Allocation: Evidence from Vietnam; World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Zhou, K.Z.; Xu, D. How Foreign Firms Curtail Local Supplier Opportunism in China: Detailed Contracts, Centralized Control, and Relational Governance. J. Int. Bus. Stud. 2012, 43, 677–692. [Google Scholar] [CrossRef]

- Delgado, M.S.; McCloud, N.; Kumbhakar, S.C. A Generalized Empirical Model of Corruption, Foreign Direct Investment, and Growth. J. Macroecon. 2014, 42, 298–316. [Google Scholar] [CrossRef]

- Di Vita, G. Political Corruption and Legislative Complexity: Two Sides of Same Coin? Struct. Change Econ. Dyn. 2021, 57, 136–147. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| FDI | 155 | 315.96 | 468.65 | 0.00 | 2339.33 |

| Corruption | 155 | 32.42 | 26.72 | 2.00 | 146.00 |

| GDP PC | 155 | 373.38 | 254.33 | 103.52 | 1574.48 |

| Urbanization | 155 | 1583.22 | 1139.27 | 391.76 | 6181.65 |

| Industry GDP | 155 | 794.68 × 104 | 812.80 × 104 | 109.17 × 104 | 4871.08 × 104 |

| Agriculture GDP | 155 | 80.23 × 104 | 70.27 × 104 | 0.75 × 104 | 369.71 × 104 |

| Service GDP | 155 | 1775.28 × 104 | 2115.03 × 104 | 229.08 × 104 | 11,325.44 × 104 |

| Education H/P | 155 | 0.89 | 0.62 | 0.09 | 4.97 |

| IFGF | 155 | 5.87 | 7.06 | 0.00 | 36.65 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Variables | FE | RE | DK FE | DK RE | FGLS | FEGLS | PCSE |

| Corruption | 0.0914 *** | 0.122 ** | 0.0914 ** | 0.122 ** | 0.172 *** | 0.0403 *** | 0.249 *** |

| (0.0309) | (0.0479) | (0.0191) | (0.0311) | (0.0277) | (0.0132) | (0.0660) | |

| GDP PC | 0.345 | 0.342 | 0.345 ** | 0.342 ** | 0.161 * | 0.159 *** | 0.0808 |

| (0.227) | (0.251) | (0.0665) | (0.0834) | (0.0950) | (0.0587) | (0.188) | |

| Urbanization | 0.0229 | −0.514 *** | 0.0229 | −0.514 ** | −0.524 *** | −0.903 | −0.852 *** |

| (2.509) | (0.196) | (1.118) | (0.135) | (0.0773) | (0.656) | (0.184) | |

| Industry GDP | −0.127 | 0.0822 | −0.127 ** | 0.0822 | 0.253 *** | −0.106 *** | 0.638 *** |

| (0.139) | (0.165) | (0.0229) | (0.0771) | (0.0773) | (0.0337) | (0.226) | |

| Agriculture GDP | −0.344 *** | 0.0296 | −0.344 *** | 0.0296 | 0.574 *** | −0.289 *** | 0.570 *** |

| (0.0959) | (0.183) | (0.0430) | (0.0248) | (0.0633) | (0.0494) | (0.0872) | |

| Service GDP | −0.0406 | −0.0149 | −0.0406 | −0.0149 | 0.116 *** | 0.0219 | 0.107 |

| (0.148) | (0.0870) | (0.0712) | (0.0765) | (0.0351) | (0.0640) | (0.0946) | |

| Education H/P | 0.000629 | −9.62 × 10−5 | 0.000629 | −9.62 × 10−5 | 6.95 × 10−6 | 0.000160 | −0.00157 |

| (0.000537) | (0.00152) | (0.000372) | (0.000861) | (0.00238) | (0.000343) | (0.00525) | |

| IFGF | 0.0228 | 0.0489 *** | 0.0228 ** | 0.0489 *** | 0.0446 *** | 0.00234 | 0.0794 * |

| (0.0233) | (0.0161) | (0.00543) | (0.00530) | (0.0135) | (0.00546) | (0.0455) | |

| Constant | 0.0939 | 0.124 *** | 0.0939 | 0.124 ** | −0.00979 | −0.000888 | −0.000783 |

| (0.522) | (0.0413) | (0.223) | (0.0366) | (0.00788) | (0.000732) | (0.0198) | |

| Observations | 112 | 112 | 112 | 112 | 111 | 111 | 112 |

| R-squared | 0.206 | 0.671 | |||||

| Number of id | 31 | 31 | 31 | 31 | 30 | 30 |

| Variables | FE Panel Threshold |

|---|---|

| Low corruption | −0.0995 |

| (0.111) | |

| Medium–low corruption | 0.305 *** |

| (0.106) | |

| Medium–high corruption | 0.0456 |

| (0.0529) | |

| High corruption | −0.0731 |

| (0.0803) | |

| GDP PC | 0.447 |

| (0.278) | |

| Urbanization | −0.903 |

| (3.394) | |

| Industry GDP | −0.120 |

| (0.167) | |

| Agriculture GDP | −0.354 *** |

| (0.0793) | |

| Service GDP | −0.253 |

| (0.300) | |

| Education H/P | 0.000392 |

| (0.000634) | |

| IFGF | −0.0136 |

| (0.0371) | |

| Constant | 0.365 |

| (0.652) | |

| Threshold 1 (λ1) | 0.298 * |

| Threshold 2 (λ2) | 0.305 |

| Threshold 3 (λ3) | 0.597 *** |

| Observations | 124 |

| Number of id | 31 |

| R-squared | 0.431 |

| Sector | Activity |

|---|---|

| A | Agriculture, livestock, forest production, fisheries, and aquaculture |

| B | Extractive industries |

| C | Transformation industries |

| D | Electricity and gas |

| E | Water, sanitation, waste management and decontamination activities |

| F | Construction |

| G | Trade; repair of motor vehicles and motorcycles |

| H | Transport, storage, and mail |

| I | Accommodation and meals |

| J | Information and communication |

| K | Financial, insurance, and related services activities |

| L | Real estate activities |

| M | Professional, scientific, and technical activities |

| N | Administrative activities and complementary services |

| O | Public administration, defense, and social security |

| P | Education |

| Q | Human health and social services |

| R | Arts, culture, sports, and recreation |

| S | Other service activities |

| T | Domestic services |

| U | International organizations and other extraterritorial institutions |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Variables | FE | RE | DK FE | DK RE | FGLS | FEGLS | PCSE |

| Corruption | 0.0454 ** | −0.000530 | 0.0454 ** | −0.000530 | 0.0145 *** | 0.00665 * | −0.0422 |

| (0.0170) | (0.0423) | (0.00960) | (0.0256) | (0.00461) | (0.00356) | (0.0446) | |

| GDP PC | 0.260 * | −0.171 | 0.260 ** | −0.171 | 0.0291 *** | 0.0218 | −0.259 ** |

| (0.129) | (0.187) | (0.0739) | (0.110) | (0.0112) | (0.0156) | (0.101) | |

| Urbanization | −0.382 | 0.0896 | −0.382 | 0.0896 | −0.0343 *** | 0.0431 | 0.130 |

| (0.900) | (0.151) | (0.377) | (0.0778) | (0.0108) | (0.155) | (0.110) | |

| Industry GDP | −0.107 | 0.0457 | −0.107 * | 0.0457 | 0.0112 | −0.00716 | 0.0848 |

| (0.0887) | (0.0746) | (0.0416) | (0.0417) | (0.00943) | (0.0135) | (0.115) | |

| Agriculture GDP | −0.156 ** | 0.142 | −0.156 ** | 0.142 ** | 0.0328 *** | −0.0721 *** | 0.185 *** |

| (0.0636) | (0.127) | (0.0351) | (0.0260) | (0.00535) | (0.0241) | (0.0438) | |

| Service GDP | 0.0427 | 0.0182 | 0.0427 | 0.0182 | 0.00712 | 0.0117 | 0.0204 |

| (0.0785) | (0.0240) | (0.0319) | (0.00809) | (0.00469) | (0.0221) | (0.0447) | |

| Education H/P | 0.000463 * | 0.00212 | 0.000463 ** | 0.00212 * | 0.000351 | 7.33 × 10−5 | 0.00211 |

| (0.000252) | (0.00204) | (9.71 × 10−5) | (0.000872) | (0.000285) | (0.000224) | (0.00262) | |

| IFGF | 0.0106 | −0.00689 | 0.0106 *** | −0.00689 | 0.00504 *** | 0.00143 | −0.00700 |

| (0.00900) | (0.0161) | (0.00134) | (0.00948) | (0.00183) | (0.00286) | (0.0231) | |

| FDI Sector A | 0.143 *** | 0.130 *** | 0.143 *** | 0.130 *** | 0.134 *** | 0.152 *** | 0.125 *** |

| (0.00410) | (0.00542) | (0.00597) | (0.00523) | (0.00271) | (0.0108) | (0.0189) | |

| FDI Sector B | 0.157 *** | 0.186 *** | 0.157 *** | 0.186 *** | 0.175 *** | 0.182 *** | 0.206 *** |

| (0.0483) | (0.0309) | (0.0134) | (0.0201) | (0.0110) | (0.0220) | (0.0261) | |

| FDI Sector C | 0.120 *** | 0.143 *** | 0.120 *** | 0.143 *** | 0.141 *** | 0.129 *** | 0.148 *** |

| (0.00868) | (0.0128) | (0.00627) | (0.00962) | (0.00213) | (0.00400) | (0.00688) | |

| FDI Sector D | - | - | - | - | - | - | - |

| FDI Sector E | - | −2.756 | - | −2.756 | −0.307 | 13.40 *** | −5.328 |

| (4.050) | (1.579) | (0.700) | (1.469) | (3.334) | |||

| FDI Sector F | - | - | - | - | - | - | - |

| FDI Sector G | 0.0202 | 0.0651 ** | 0.0202 | 0.0651 ** | 0.0886 *** | 0.0739 *** | 0.0692 *** |

| (0.0608) | (0.0314) | (0.0347) | (0.0145) | (0.00426) | (0.0151) | (0.0229) | |

| FDI Sector H | 0.877 *** | 0.407 | 0.877 ** | 0.407 | 0.627 | 0.840 | 1.451 |

| (0.312) | (1.226) | (0.167) | (0.684) | (0.440) | (0.559) | (2.120) | |

| FDI Sector I | 0.368 ** | 0.0690 | 0.368 ** | 0.0690 | 0.455 *** | 0.0937 | −0.0155 |

| (0.137) | (0.403) | (0.0767) | (0.140) | (0.0552) | (0.125) | (0.422) | |

| FDI Sector J | −0.0250 | −0.815 | −0.0250 | −0.815 | −0.0884 | −0.0261 | −1.224 ** |

| (0.263) | (1.093) | (0.0470) | (0.443) | (0.0785) | (0.114) | (0.489) | |

| FDI Sector K | 0.171 | −0.699 | 0.171 ** | −0.699 | 0.287 | −0.323 | −0.271 |

| (0.197) | (1.967) | (0.0484) | (1.194) | (0.388) | (0.298) | (1.907) | |

| FDI Sector L | - | - | - | - | - | - | - |

| FDI Sector M | 0.894 | 2.952 * | 0.894 *** | 2.952 | 2.494 *** | 1.090 *** | 4.052 *** |

| (0.580) | (1.722) | (0.0261) | (1.306) | (0.412) | (0.243) | (1.184) | |

| FDI Sector N | 0.184 *** | 0.0774 | 0.184 *** | 0.0774 | −0.582 *** | 0.219 *** | 0.336 |

| (0.0475) | (0.510) | (0.0216) | (0.591) | (0.0747) | (0.0276) | (0.315) | |

| FDI Sector O | - | - | - | - | - | - | - |

| FDI Sector P | - | - | - | - | - | - | - |

| FDI Sector Q | - | - | - | - | - | - | - |

| FDI Sector R | −7.081 ** | 9.323 | −7.081 ** | 9.323 | 1.887 | 0.545 | 5.584 |

| (3.068) | (13.75) | (2.190) | (5.633) | (2.956) | (3.907) | (16.07) | |

| FDI Sector S | −0.0430 | 0.381 | −0.0430 | 0.381 ** | 0.132 | 0.106 | 0.731 |

| (0.0395) | (0.407) | (0.0860) | (0.0872) | (0.0890) | (0.0836) | (0.465) | |

| FDI Sector T | - | - | - | - | - | - | - |

| FDI Sector U | - | - | - | - | - | - | - |

| Constant | 0.0824 | −0.00758 | 0.0824 | −0.00758 ** | −0.00331 *** | −0.000190 | - |

| (0.189) | (0.00616) | (0.0737) | (0.00151) | (0.000895) | (0.000260) | ||

| Observations | 112 | 112 | 112 | 112 | 111 | 111 | 112 |

| R-squared | 0.914 | 0.962 | |||||

| Number of id | 31 | 31 | 31 | 31 | 30 | 30 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Onody, V.d.S.M.; Gandra de Carvalho, A.C.; Polloni-Silva, E.; Roiz, G.A.; Mariano, E.B.; Rebelatto, D.A.N.; Moralles, H.F. Corruption and FDI in Brazil: Contesting the “Sand” or “Grease” Hypotheses. Sustainability 2022, 14, 6288. https://doi.org/10.3390/su14106288

Onody VdSM, Gandra de Carvalho AC, Polloni-Silva E, Roiz GA, Mariano EB, Rebelatto DAN, Moralles HF. Corruption and FDI in Brazil: Contesting the “Sand” or “Grease” Hypotheses. Sustainability. 2022; 14(10):6288. https://doi.org/10.3390/su14106288

Chicago/Turabian StyleOnody, Vanessa da Silva Mariotto, Ana Catarina Gandra de Carvalho, Eduardo Polloni-Silva, Guilherme Augusto Roiz, Enzo Barberio Mariano, Daisy Aparecida Nascimento Rebelatto, and Herick Fernando Moralles. 2022. "Corruption and FDI in Brazil: Contesting the “Sand” or “Grease” Hypotheses" Sustainability 14, no. 10: 6288. https://doi.org/10.3390/su14106288