Emotional Artificial Neural Networks and Gaussian Process-Regression-Based Hybrid Machine-Learning Model for Prediction of Security and Privacy Effects on M-Banking Attractiveness

,

,  ,

,

Abstract

:1. Introduction

2. Materials and Methods

2.1. Technology Acceptance Models

2.2. Mobile Banking System Features, and Challenges

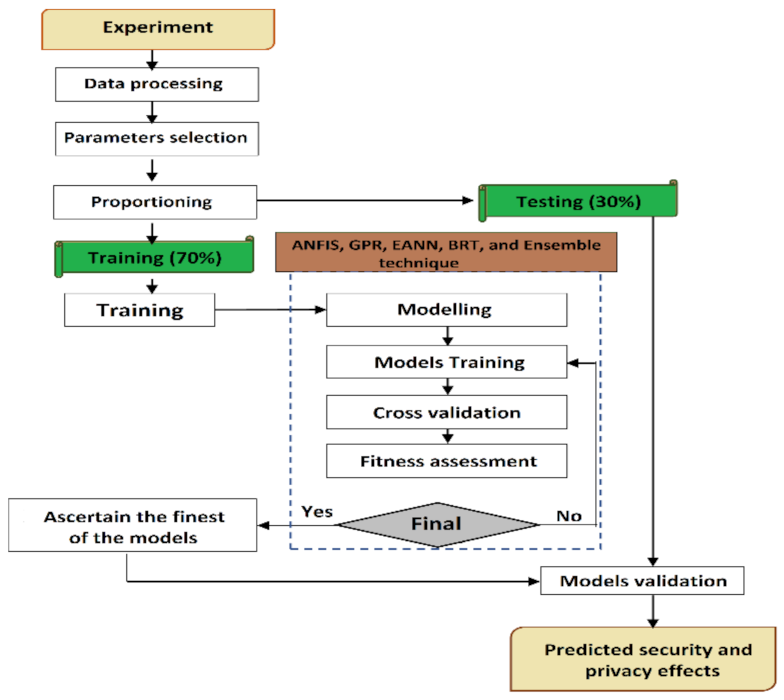

2.3. Method

2.3.1. Study Design and Measurement Scales

2.3.2. Data Collection and Sampling Techniques

2.3.3. Data Examination Techniques

2.4. Artificial Intelligence Techniques

2.5. Ensemble Techniques

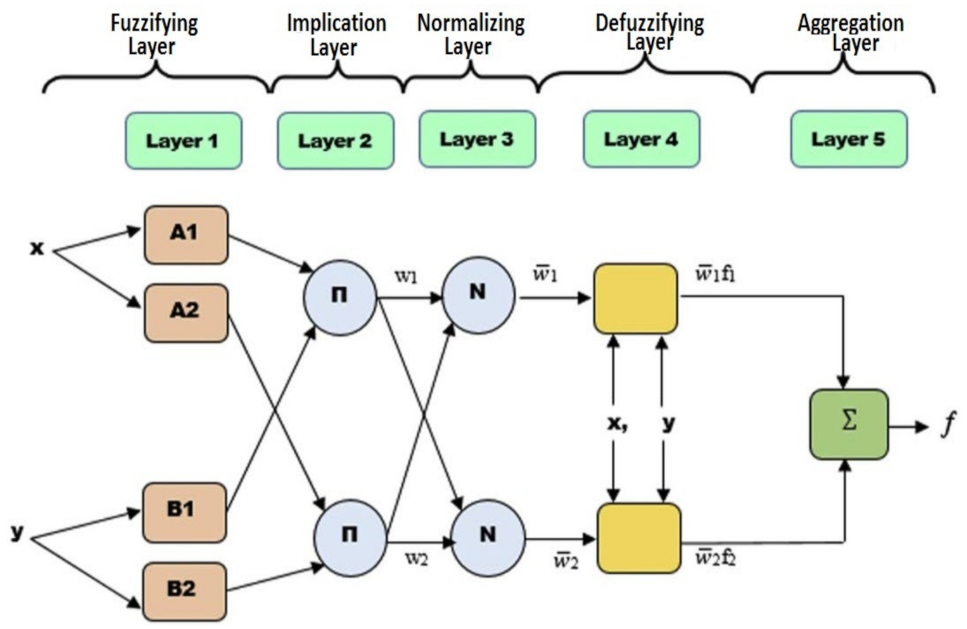

2.5.1. ANFIS Model

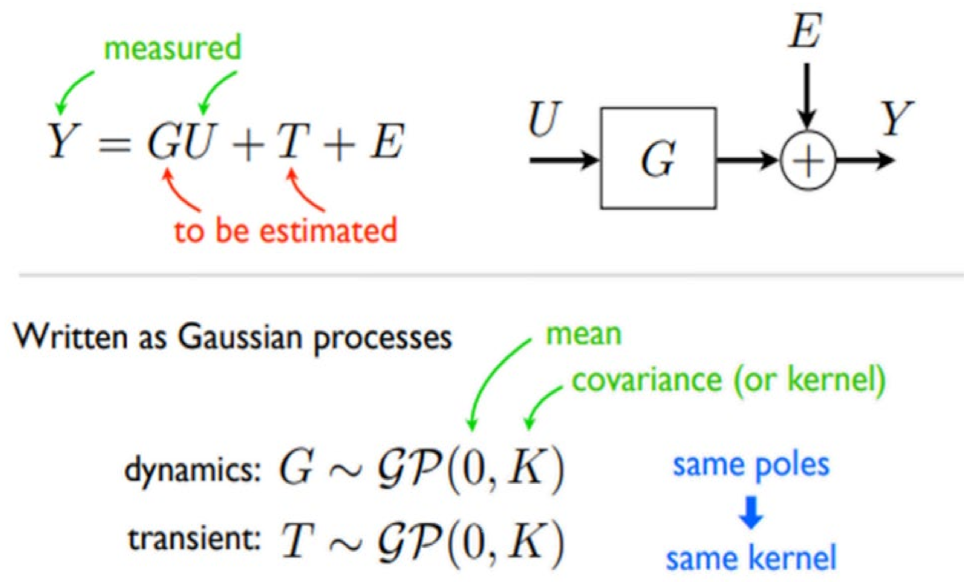

2.5.2. GPR Model

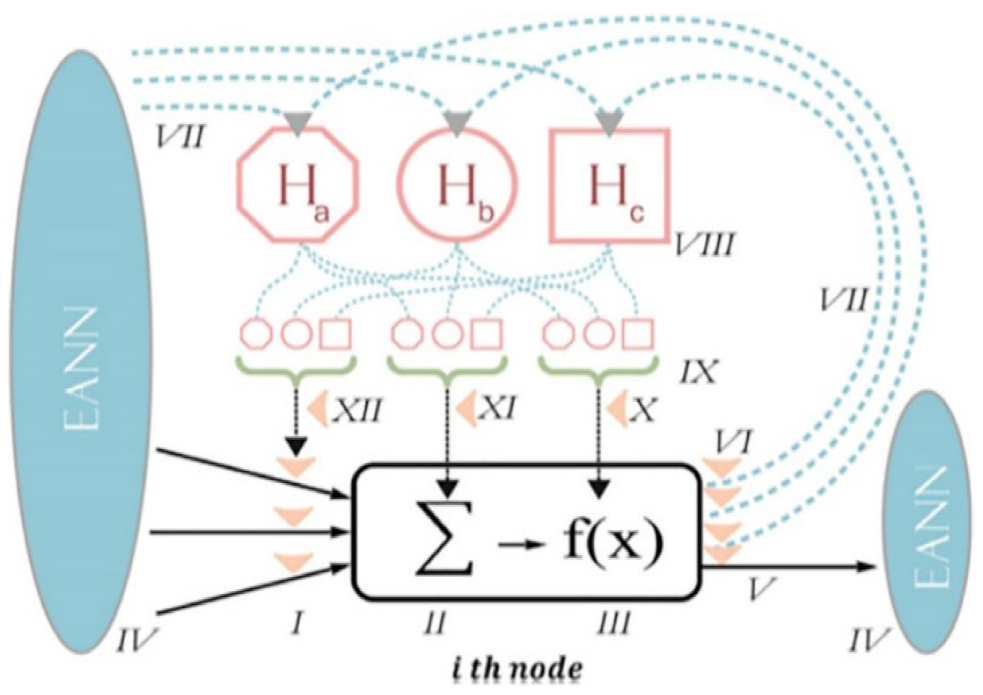

2.5.3. EANN Model

2.5.4. BRT Model

2.6. Data Normalization, Models Validation and Performance Comparisons

2.6.1. Data Normalization

2.6.2. Models’ Validation, and Performance Comparisons

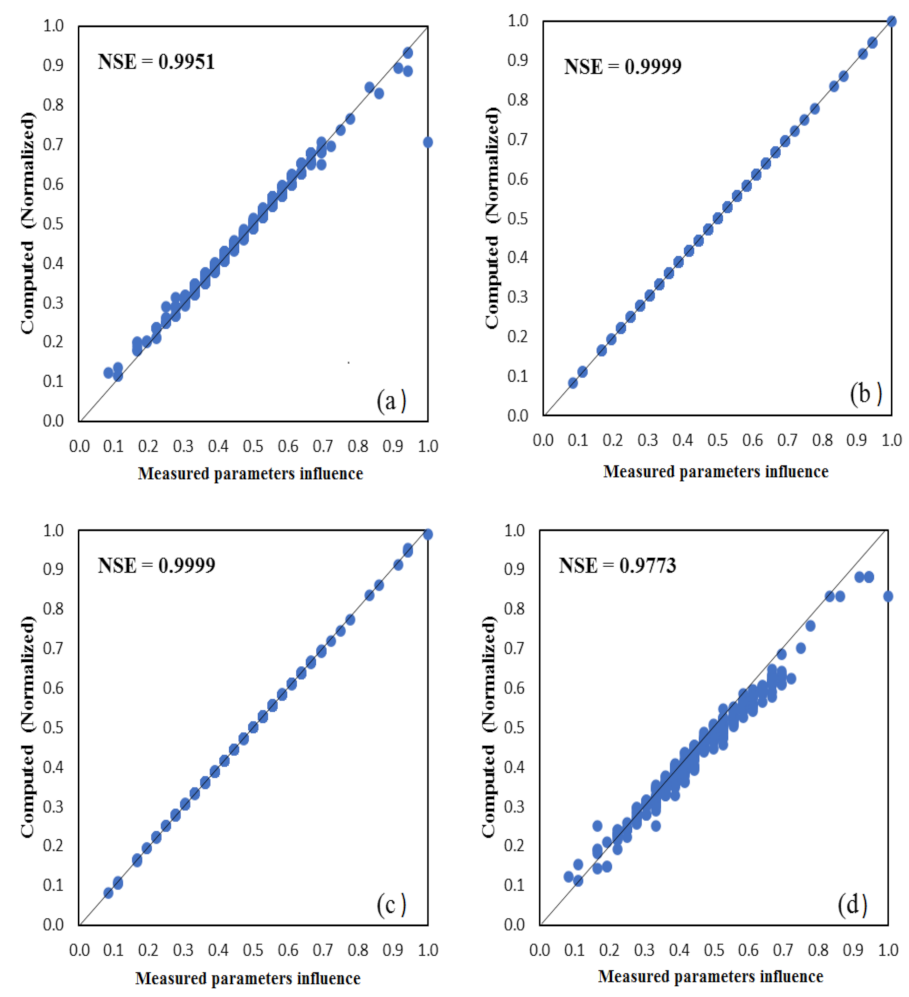

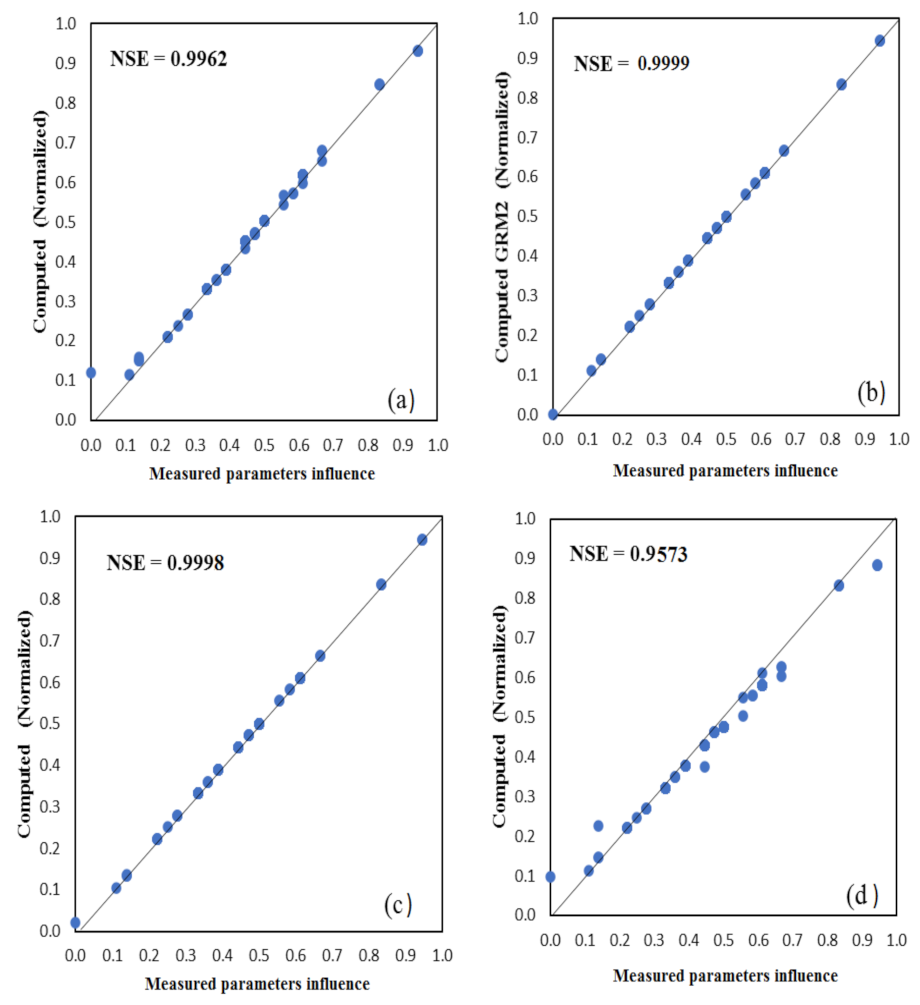

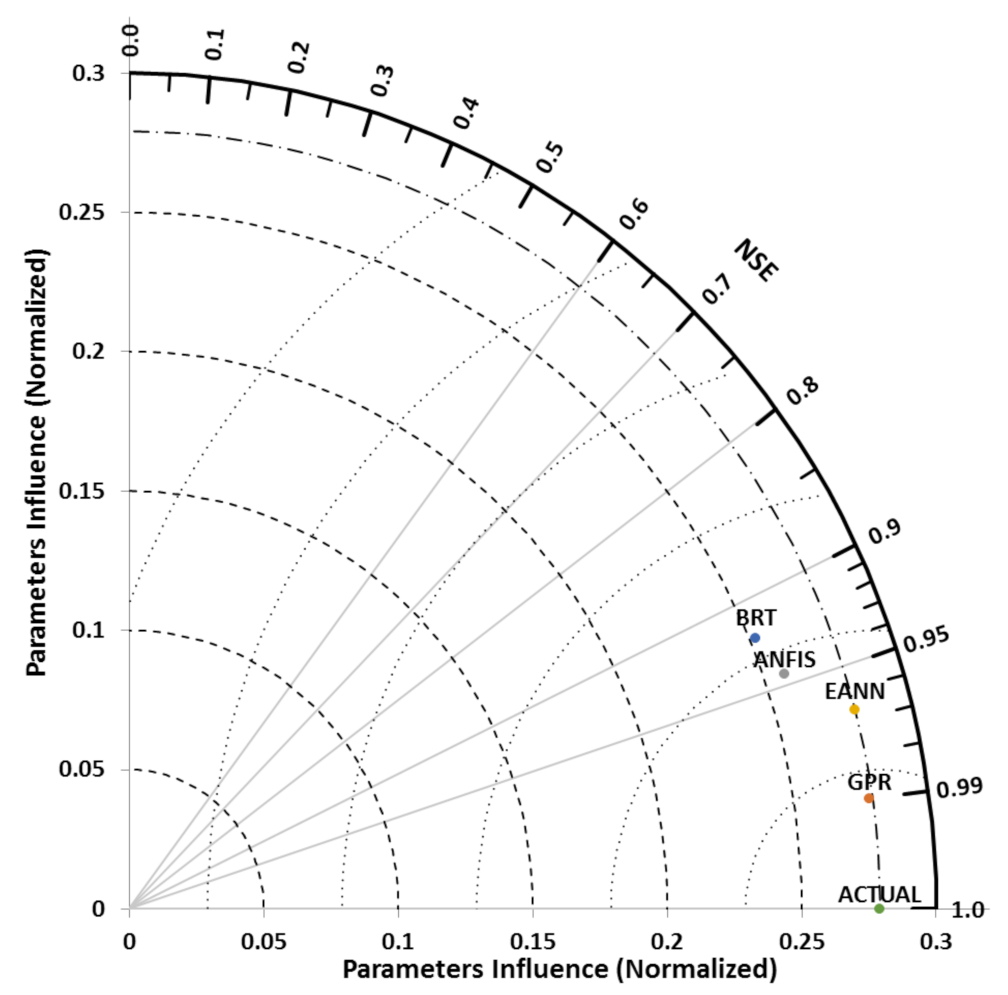

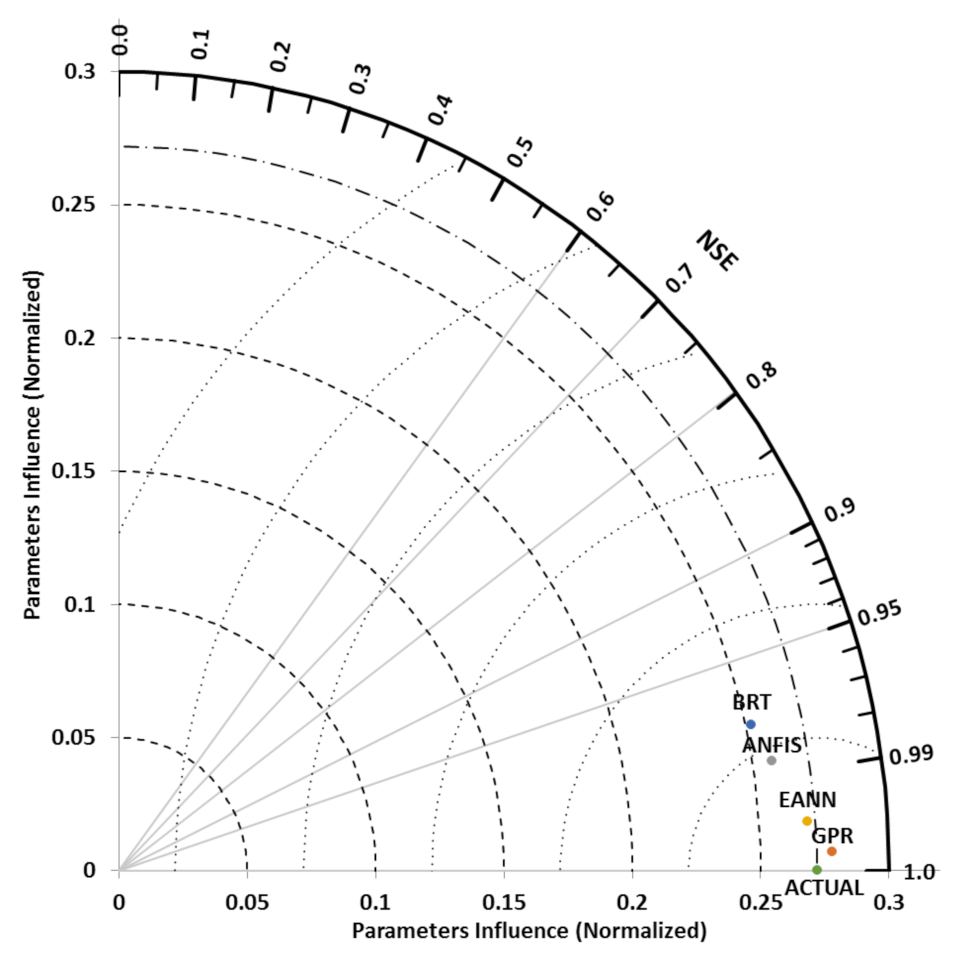

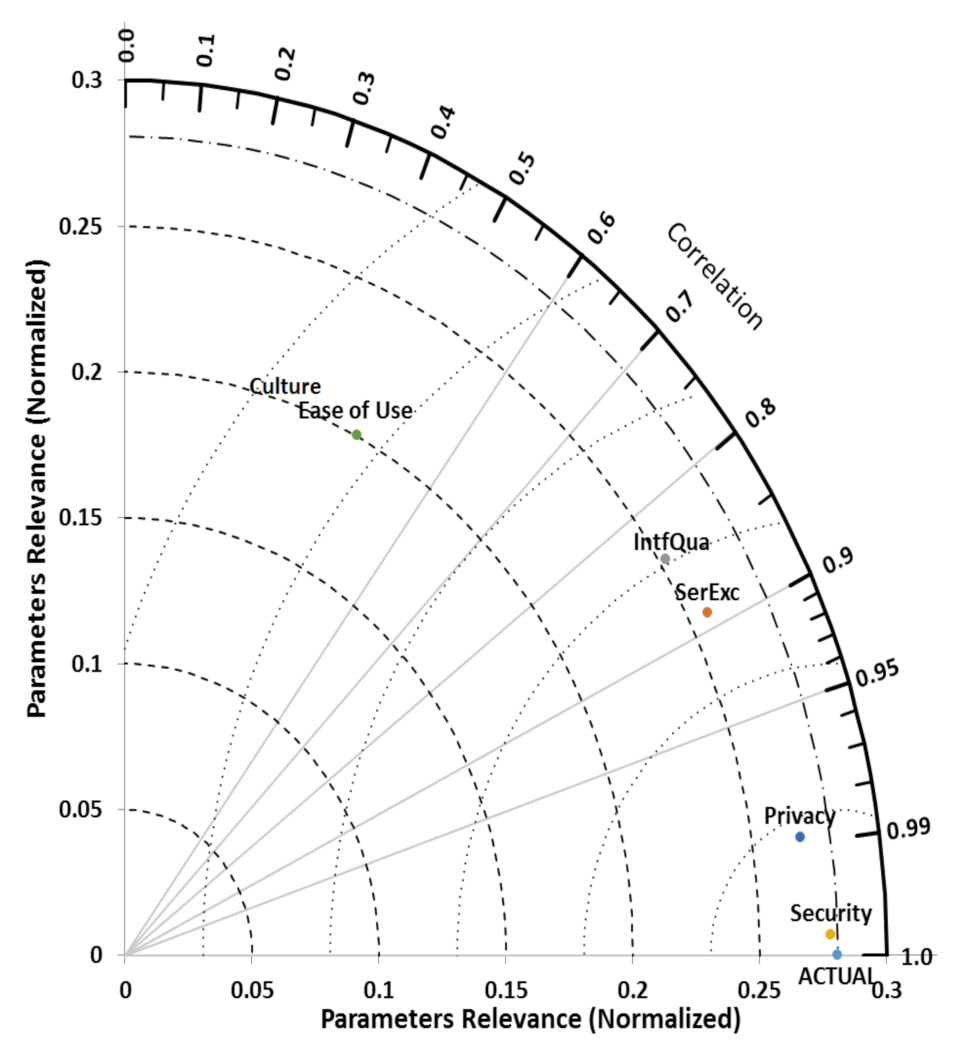

3. Results and Discussion

3.1. Sensitivity Examination Results

3.2. AI Models Results and Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1. Gender | ( ) Male | ( ) Female | ||

| 2. Age group | ( ) 18–25 | ( ) 26–35 | ( ) 36 and above | |

| 3. Education level | ( ) SSCE | ( ) ND | ( ) Barchelor/HND | 3. Education level |

| 4. Employment Status | ( ) Academics | ( ) Students | ( ) Banking Staff | ( ) Security expert |

| 5. Nationality | ( ) Nigeria | ( ) Cyprus |

| Items | Sd | D | N | A | Sa | |

|---|---|---|---|---|---|---|

| H1 | Ease of use (Lewis, 2006) | |||||

| EoU1 | “Overall, I am satisfied with how easy it is to use this System” | |||||

| EoU2 | “It was simple to use this system” | |||||

| EoU3 | “I was able to complete the tasks and scenarios quicklyusing this system” | |||||

| EoU4 | “I felt comfortable using this system” | |||||

| EoUe5 | “It was easy to learn to use this system”. | |||||

| EoU6 | “I believe I could be protected using this System” | |||||

| H2 | Privacy (Authors of this study) | |||||

| Priv1 | “I fear that while I am paying a bill by mobile phone, I might make mistakes since the correctness of the inputted information is difficult to check from the screen” | |||||

| Priv2 | “I fear that while I am using mobile banking services, the Government can intercept my personal information” | |||||

| Priv3 | “I fear that while I am using mobile banking services, third parties can access my account or see my account information” | |||||

| Priv4 | “I fear that the list of PIN codes may be lost and end up in the wrong hands” | |||||

| Priv5 | “Generally, I fear that my personal information can be accessed through m-banking platform” | |||||

| H3 | Interface quality (Shama, 2019; Lewis, 2006) | |||||

| IntQual1 | “The interface of this system was pleasant”. | |||||

| IntQual2 | “I liked using the interface of this system”. | |||||

| IntQual3 | “This system has all of the functions and capabilities I expect it to have” | |||||

| IntQual4 | “Overall, I am satisfied with this system” | |||||

| H4 | System Security (Authors of this study) | |||||

| SysSq1 | “The security features of the system are pleasant to me” | |||||

| SysSq2 | “Velocity anomalies during login can be handle by the system” | |||||

| SysSq3 | “The authentication process provided in the system is more reliable, robust, and can help safeguard customers funds” | |||||

| SysSq4 | “The system is capable of handling DDoS attacks” | |||||

| SysSq5 | “In general, I am satisfied with the level of security provided in the systems” | |||||

| H5 | Service quality (Shama, 2019; Lewis, 2006) | |||||

| SQ1 | “The call centre representatives always help me when I need support with m-banking” | |||||

| SQ2 | “The call centre representatives always pay personal attention when I experience problems with m-banking” | |||||

| SQ3 | “The call centre representatives have adequate knowledge to answer my queries related to m-banking” | |||||

| H6 | Cultural values (Shama, 2019) | |||||

| CV1 | “People who are important to me think that I should use Mobile banking apps” | |||||

| CV2 | “People who influence my behaviour think that I should use Mobile banking apps” | |||||

| CV3 | “People whose opinions that I value prefer that I use Mobile Banking” | |||||

| CV4 | “Generally, my culture encourages the use of m-banking services” |

Appendix B

| Demographic Variable | Frequencies | Percentage |

|---|---|---|

| Nationality | ||

| Nigeria | 427 | 57.3 |

| Cyprus | 318 | 42.7 |

| Gender | ||

| Male | 411 | 55.2 |

| Female | 334 | 44.8 |

| Age group | ||

| 18–25 | 241 | 32.3 |

| 26–35 | 381 | 51.2 |

| 36 and above | 123 | 16.5 |

| Educational qualification | ||

| SSCE | 73 | 9.8 |

| ND | 110 | 14.8 |

| Bachelor/HND | 397 | 53.3 |

| Masters or higher | 165 | 22.1 |

| Employment status | ||

| Academics | 173 | 23.2 |

| Students | 368 | 49.4 |

| Other civil servants | 89 | 11.9 |

| Business | 107 | 14.4 |

| Security experts | 8 | 1.1 |

References

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Park, J.; Amendah, E.; Lee, Y.; Hyun, H. M-payment service: Interplay of perceived risk, benefit, and trust in service adoption. Hum. Factors Ergon. Manuf. Serv. Ind. 2019, 29, 31–43. [Google Scholar] [CrossRef]

- Cavus, N.; Mohammed, Y.B.; Yakubu, M.N. An Artificial Intelligence-Based Model for Prediction of Parameters Affecting Sustainable Growth of Mobile Banking Apps. Sustainability 2021, 13, 6206. [Google Scholar] [CrossRef]

- Zhou, L.; Gozgor, G.; Huang, M.; Lau, M.C.K. The impact of geopolitical risks on financial development: Evidence from emerging markets. J. Compet. 2020, 12, 93. [Google Scholar] [CrossRef]

- Moghavvemi, S.; Mei, T.X.; Phoong, S.W.; Phoong, S.Y. Drivers and barriers of mobile payment adoption: Malaysian merchants’ perspective. J. Retail. Consum. Serv. 2021, 59, 102364. [Google Scholar] [CrossRef]

- Lee, S.-J.; Rho, M.J.; Yook, I.H.; Park, S.-H.; Jang, K.-S.; Park, B.-J.; Lee, O.; Lee, D.K.; Kim, D.-J.; Choi, I.Y. Design, development and implementation of a smartphone overdependence management system for the self-control of smart devices. Appl. Sci. 2016, 6, 440. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, O.T. Factors affecting the intention to use digital banking in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 303–310. [Google Scholar] [CrossRef]

- Malaquias, R.F.; Hwang, Y. An empirical study on trust in mobile banking: A developing country perspective. Comput. Hum. Behav. 2016, 54, 453–461. [Google Scholar] [CrossRef]

- Kaur, S.J.; Ali, L.; Hassan, M.K.; Al-Emran, M. Adoption of digital banking channels in an emerging economy: Exploring the role of in-branch efforts. J. Financ. Serv. Mark. 2021, 26, 107–121. [Google Scholar] [CrossRef]

- Alkhowaiter, W.A. Digital payment and banking adoption research in Gulf countries: A systematic literature review. Int. J. Inf. Manag. 2020, 53, 102102. [Google Scholar] [CrossRef]

- Kamdjoug, J.R.K.; Wamba-Taguimdje, S.-L.; Wamba, S.F.; Kake, I.B. Determining factors and impacts of the intention to adopt mobile banking app in Cameroon: Case of SARA by afriland First Bank. J. Retail. Consum. Serv. 2021, 61, 102509. [Google Scholar] [CrossRef]

- Momtaz, P.P. The pricing and performance of cryptocurrency. Eur. J. Financ. 2021, 27, 367–380. [Google Scholar] [CrossRef]

- Nourani, V.; Gökçekuş, H.; Umar, I.K. Artificial intelligence based ensemble model for prediction of vehicular traffic noise. Environ. Res. 2020, 180, 108852. [Google Scholar] [CrossRef] [PubMed]

- DeLone, W.H.; McLean, E.R. The DeLone and McLean model of information systems success: A ten-year update. J. Manag. Inf. Syst. 2003, 19, 9–30. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I.; Albarracin, D.; Hornik, R. A reasoned action approach: Some issues, questions, and clarifications. In Prediction and Change of Health Behavior; Lawrence Erlbaum Associates, Inc.: Mahwah, NJ, YSA, 2007; pp. 281–295. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 19, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Processes 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef] [Green Version]

- Smith, J.R.; McSweeney, A. Charitable giving: The effectiveness of a revised theory of planned behaviour model in predicting donating intentions and behaviour. J. Community Appl. Soc. Psychol. 2007, 17, 363–386. [Google Scholar] [CrossRef]

- Merhi, M.; Hone, K.; Tarhini, A. A cross-cultural study of the intention to use mobile banking between Lebanese and British consumers: Extending UTAUT2 with security, privacy and trust. Technol. Soc. 2019, 59, 101151. [Google Scholar] [CrossRef]

- Rajaee, T.; Ebrahimi, H.; Nourani, V. A review of the artificial intelligence methods in groundwater level modeling. J. Hydrol. 2019, 572, 336–351. [Google Scholar] [CrossRef]

- Ghiasi, R.; Ghasemi, M.R.; Noori, M. Comparative studies of metamodeling and AI-Based techniques in damage detection of structures. Adv. Eng. Softw. 2018, 125, 101–112. [Google Scholar] [CrossRef]

- Kumar, V.; Lai, K.-K.; Chang, Y.-H.; Bhatt, P.C.; Su, F.-P. A structural analysis approach to identify technology innovation and evolution path: A case of m-payment technology ecosystem. J. Knowl. Manag. 2020, 25, 477–499. [Google Scholar] [CrossRef]

- De Reuver, M.; Ondrus, J. When technological superiority is not enough: The struggle to impose the SIM card as the NFC Secure Element for mobile payment platforms. Telecommun. Policy 2017, 41, 253–262. [Google Scholar] [CrossRef]

- Téllez, J.; Zeadally, S. Architectures and Models for Mobile Payment Systems. In Mobile Payment Systems; Springer: Berlin/Heidelberg, Germany, 2017; pp. 35–91. [Google Scholar] [CrossRef]

- Teng, S.; Khong, K.W. Examining actual consumer usage of E-wallet: A case study of big data analytics. Comput. Hum. Behav. 2021, 121, 106778. [Google Scholar] [CrossRef]

- Pal, A.; Herath, T.; Rao, H.R. Why do people use mobile payment technologies and why would they continue? An examination and implications from India. Res. Policy 2021, 50, 104228. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Alalwan, A.A.; Rana, N.P.; Kizgin, H.; Patil, P. Consumer use of mobile banking (M-Banking) in Saudi Arabia: Towards an integrated model. Int. J. Inf. Manag. 2019, 44, 38–52. [Google Scholar] [CrossRef] [Green Version]

- Lewis, J.R. Sample sizes for usability tests: Mostly math, not magic. Interactions 2006, 13, 29–33. [Google Scholar] [CrossRef]

- Sharma, S.K. Integrating cognitive antecedents into TAM to explain mobile banking behavioral intention: A SEM-neural network modeling. Inf. Syst. Front. 2019, 21, 815–827. [Google Scholar] [CrossRef]

- Shen, W.; Zhou, M.; Yang, F.; Yu, D.; Dong, D.; Yang, C.; Zang, Y.; Tian, J. Multi-crop convolutional neural networks for lung nodule malignancy suspiciousness classification. Pattern Recognit. 2017, 61, 663–673. [Google Scholar] [CrossRef]

- Ungerman, O.; Dedkova, J.; Gurinova, K. The impact of marketing innovation on the competitiveness of enterprises in the context of industry 4.0. J. Compet. 2018, 10, 132. [Google Scholar] [CrossRef]

- Sharma, P.; Machiwal, D. Streamflow forecasting: Overview of advances in data-driven techniques. In Advances in Streamflow Forecasting; Elsevier: Amsterdam, The Netherlands, 2021; pp. 1–50. [Google Scholar] [CrossRef]

- El-Hasnony, I.M.; Barakat, S.I.; Mostafa, R.R. Optimized ANFIS model using hybrid metaheuristic algorithms for Parkinson’s disease prediction in IoT environment. IEEE Access 2020, 8, 119252–119270. [Google Scholar] [CrossRef]

- Nourani, V. An emotional ANN (EANN) approach to modeling rainfall-runoff process. J. Hydrol. 2017, 544, 267–277. [Google Scholar] [CrossRef]

- Hussain, S.A.; Cavus, N.; Sekeroglu, B. Hybrid Machine Learning Model for Body Fat Percentage Prediction Based on Support Vector Regression and Emotional Artificial Neural Networks. Appl. Sci. 2021, 11, 9797. [Google Scholar] [CrossRef]

- Cavus, N.; Mohammed, Y.B.; Yakubu, M.N. Determinants of learning management systems during COVID-19 pandemic for sustainable education. Sustainability 2021, 13, 5189. [Google Scholar] [CrossRef]

- Cai, H.; Jia, X.; Feng, J.; Li, W.; Hsu, Y.-M.; Lee, J. Gaussian Process Regression for numerical wind speed prediction enhancement. Renew. Energy 2020, 146, 2112–2123. [Google Scholar] [CrossRef]

- Rabehi, A.; Guermoui, M.; Lalmi, D. Hybrid models for global solar radiation prediction: A case study. Int. J. Ambient. Energy 2020, 41, 31–40. [Google Scholar] [CrossRef]

- Gaya, M.; Zango, M.; Yusuf, L.; Mustapha, M.; Muhammad, B.; Sani, A.; Tijjani, A.; Wahab, N.; Khairi, M. Estimation of turbidity in water treatment plant using Hammerstein-Wiener and neural network technique. Indones. J. Electr. Eng. Comput. Sci. 2017, 5, 666–672. [Google Scholar] [CrossRef]

- Taylor, K.E. Summarizing multiple aspects of model performance in a single diagram. J. Geophys. Res. Atmos. 2001, 106, 7183–7192. [Google Scholar] [CrossRef]

- Gholami, H.; Mohammadifar, A.; Golzari, S.; Kaskaoutis, D.G.; Collins, A.L. Using the Boruta algorithm and deep learning models for mapping land susceptibility to atmospheric dust emissions in Iran. Aeolian Res. 2021, 50, 100682. [Google Scholar] [CrossRef]

- Zhou, Q.; Lim, F.J.; Yu, H.; Xu, G.; Ren, X.; Liu, D.; Wang, X.; Mai, X.; Xu, H. A study on factors affecting service quality and loyalty intention in mobile banking. J. Retail. Consum. Serv. 2021, 60, 102424. [Google Scholar] [CrossRef]

- Choi, H.; Park, J.; Kim, J.; Jung, Y. Consumer preferences of attributes of mobile payment services in South Korea. Telemat. Inform. 2020, 51, 101397. [Google Scholar] [CrossRef]

- Rahman, T.; Noh, M.; Kim, Y.S.; Lee, C.K. Effect of word of mouth on m-payment service adoption: A developing country case study. Inf. Dev. 2021, 47, 771–780. [Google Scholar] [CrossRef]

- Lu, J.; Wei, J.; Yu, C.-S.; Liu, C. How do post-usage factors and espoused cultural values impact mobile payment continuation? Behav. Inf. Technol. 2017, 36, 140–164. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Lutfi, A.; Alsaad, A.; Taamneh, A.; Alsyouf, A. The determinants of digital payment systems’ acceptance under cultural orientation differences: The case of uncertainty avoidance. Technol. Soc. 2020, 63, 101367. [Google Scholar] [CrossRef]

- Chenarlogh, V.A.; Razzazi, F.; Mohammadyahya, N. A multi-view human action recognition system in limited data case using multi-stream CNN. In Proceedings of the 2019 5th Iranian Conference on Signal Processing and Intelligent Systems (ICSPIS), Shahrood, Iran, 18–19 December 2019; pp. 1–11. [Google Scholar] [CrossRef]

- Roshani, M.; Sattari, M.A.; Ali, P.J.M.; Roshani, G.H.; Nazemi, B.; Corniani, E.; Nazemi, E. Application of GMDH neural network technique to improve measuring precision of a simplified photon attenuation based two-phase flowmeter. Flow Meas. Instrum. 2020, 75, 101804. [Google Scholar] [CrossRef]

- Jafari Gukeh, M.; Moitra, S.; Ibrahim, A.N.; Derrible, S.; Megaridis, C.M. Machine Learning Prediction of TiO2-Coating Wettability Tuned via UV Exposure. ACS Appl. Mater. Interfaces 2021, 13, 46171–46179. [Google Scholar] [CrossRef]

- Azimirad, V.; Ramezanlou, M.T.; Sotubadi, S.V.; Janabi-Sharifi, F. A consecutive hybrid spiking-convolutional (CHSC) neural controller for sequential decision making in robots. Neurocomputing 2022, 40, 319–336. [Google Scholar] [CrossRef]

| Input Parameters | DC Values | Rank |

|---|---|---|

| Security | 0.9991 | 1 |

| Privacy | 0.9899 | 2 |

| Service excellence | 0.8693 | 3 |

| Interface quality | 0.8211 | 4 |

| Ease of use | 0.4762 | 5 |

| Culture | 0.4386 | 6 |

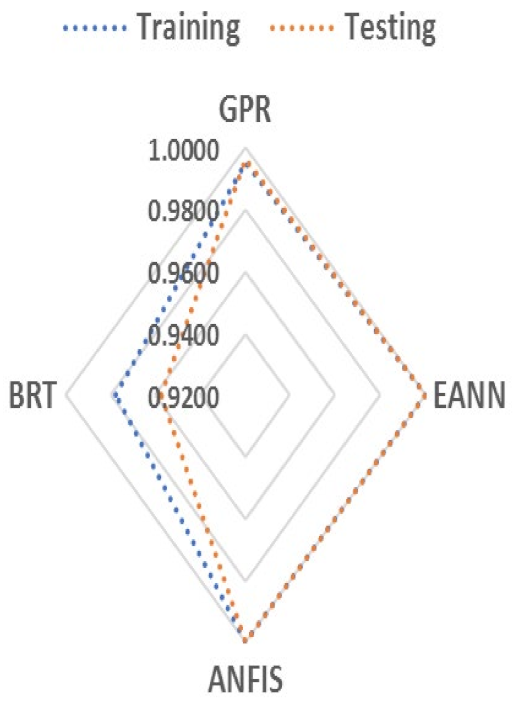

| Training | Testing | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MODELS | NSE | RMSE | MAE | MAPE | rRMSE | NSE | RMSE | MAE | MAPE | rRMSE |

| ANFIS | 0.9951 | 0.0931 | 0.0617 | 23.0142 | 8.5317 | 0.9962 | 0.0364 | 0.0168 | 8.4587 | 5.2631 |

| GPR | 0.9999 | 0.0001 | 0.0009 | 0.0428 | 0.0201 | 0.9999 | 0.0001 | 0.0002 | 0.0123 | 0.0147 |

| EANN | 0.9999 | 0.0012 | 0.0082 | 0.0720 | 0.0964 | 0.9998 | 0.0009 | 0.0037 | 0.0623 | 0.0792 |

| BRT | 0.9773 | 0.0612 | 0.0197 | 13.9462 | 6.6381 | 0.9573 | 0.0536 | 0.0636 | 11.3127 | 8.0736 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cavus, N.; Mohammed, Y.B.; Gital, A.Y.; Bulama, M.; Tukur, A.M.; Mohammed, D.; Isah, M.L.; Hassan, A. Emotional Artificial Neural Networks and Gaussian Process-Regression-Based Hybrid Machine-Learning Model for Prediction of Security and Privacy Effects on M-Banking Attractiveness. Sustainability 2022, 14, 5826. https://doi.org/10.3390/su14105826

Cavus N, Mohammed YB, Gital AY, Bulama M, Tukur AM, Mohammed D, Isah ML, Hassan A. Emotional Artificial Neural Networks and Gaussian Process-Regression-Based Hybrid Machine-Learning Model for Prediction of Security and Privacy Effects on M-Banking Attractiveness. Sustainability. 2022; 14(10):5826. https://doi.org/10.3390/su14105826

Chicago/Turabian StyleCavus, Nadire, Yakubu Bala Mohammed, Abdulsalam Ya’u Gital, Mohammed Bulama, Adamu Muhammad Tukur, Danlami Mohammed, Muhammad Lamir Isah, and Abba Hassan. 2022. "Emotional Artificial Neural Networks and Gaussian Process-Regression-Based Hybrid Machine-Learning Model for Prediction of Security and Privacy Effects on M-Banking Attractiveness" Sustainability 14, no. 10: 5826. https://doi.org/10.3390/su14105826