Management Control and Business Model Innovation in the Context of a Circular Economy in the Dutch Construction Industry

Abstract

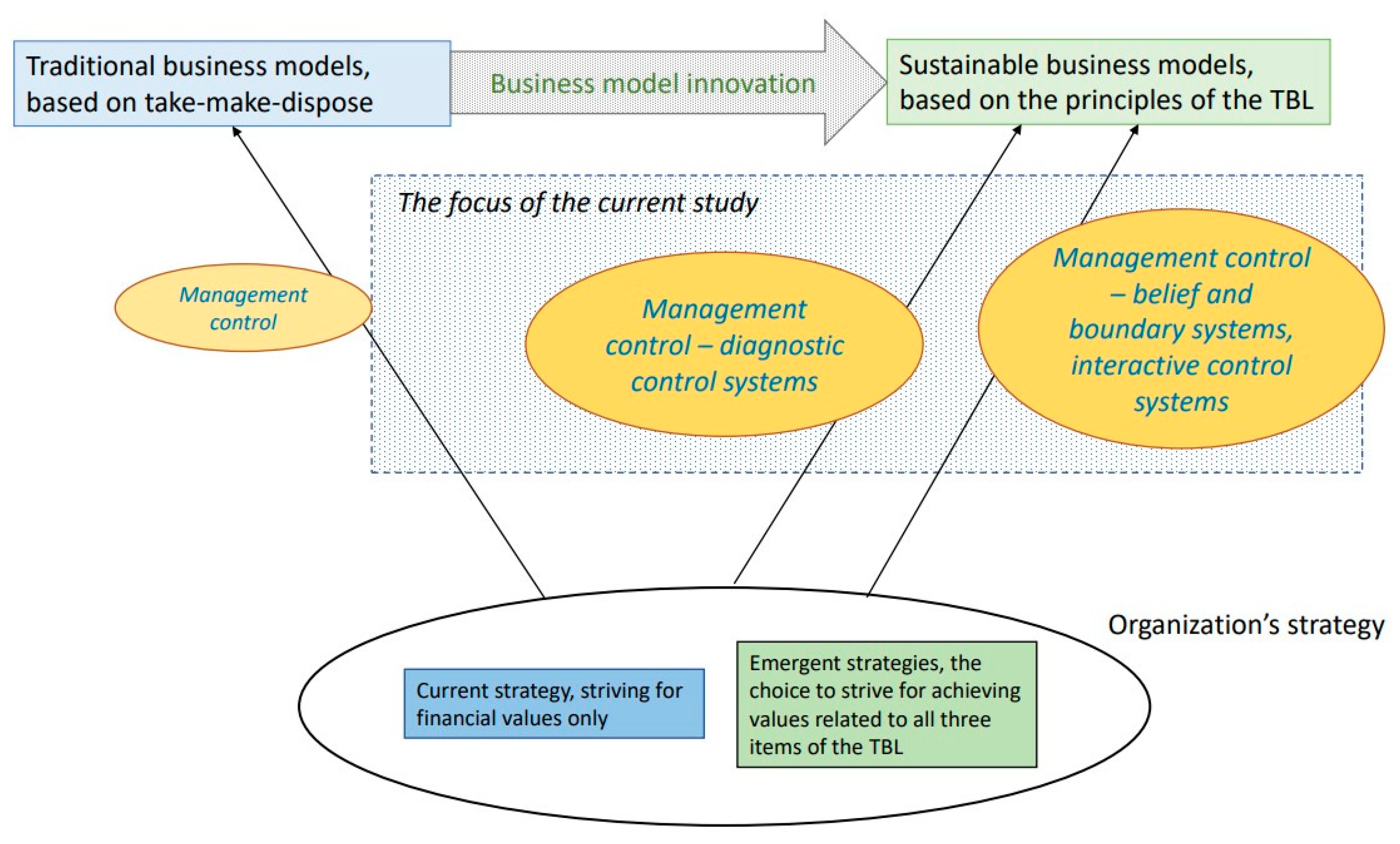

:1. Introduction

2. Theoretical Background

2.1. Levers of Control Framework

- Beliefs systems. According to Simons, a belief system is “the explicit set of organizational definitions that senior managers communicate formally and reinforce systematically to provide basic values, purpose, and direction for the organization” [10] (p. 34). Simons argues that many opportunities to create value are available within the organization external environment. Top management can use beliefs systems to direct the search for new ways of creating value by individual organizational members.

- Boundary systems. In relation to motivating organizational members to explore new opportunities, boundaries are required to direct and control employees in order to search for strategic opportunities in line with the organization’s vision. Boundary systems communicate the boundaries that organization members should respect at all times.

- Interactive control systems. Many valuable opportunities for circular business model innovation are currently available [17]. Consequently, selecting the best opportunities is key. According to Simons [10], an organization’s top management uses interactive control systems to explore innovative initiatives. These systems include the way top management challenges the company staff to come up with new ideas and to work these out successfully. These interactive control systems function primarily bottom-up and include room for the creativity needed to discover circular business models.

- Diagnostic control systems are designed to monitor if the current strategy is achieved in accordance with the plan. For instance, construction companies use financial performance indicators at the level of individual projects to monitor whether or not and to what extent the company achieves its objectives.

2.2. Individual Levers of Control

2.2.1. Beliefs Systems

2.2.2. Interactive Control Systems

2.2.3. Boundary Systems

2.2.4. Diagnostic Control Systems

2.3. Towards Analytical Focus Points

3. Research Approach

3.1. Context of the Empirical Data Collection

3.2. Data Collection and Analysis

4. Results

4.1. Industry Patterns

4.2. Belief Systems

4.2.1. Cornerstone

Because we aim to explore, to reach for new boundaries; that’s what we are focused on. It’s either: this way of thinking is truly part of your DNA or it is not. It is a matter of choice to explore. […] Moreover, it’s because our view is about the long run: if our choices do not pay off this year, this will be the case in the next.Interview 3D, RoadService managing director

4.2.2. Radical Innovations

A group of very outspoken citizens in a certain city area urged the municipality to replace the existing asphalt pavement in their living environment for noise-reducing asphalt pavement, however, the existing asphalt pavement would last for many years.Interview 2C, municipality’s representative

4.3. Interactive Control Systems

4.3.1. Dialogue

Each year, construction company A organizes a company-wide strategy meeting to reconsider the chosen strategy, assessing the recent risks and discussing relevant developments in the external environment. About twenty of the company’s employees join this strategy meeting, they represent various organizational levels varying from the carpenters to the managing director. The annual strategy meeting contributes to continually rethinking the strategic choices from the perspective of a new generation. Company A strives to change the company from the inside, bottom-up, instead of implementing strategy from the top-down. Giving an example of the results of the most recent strategy meeting, company A noted that the organization lacks the knowledge and experience to transfer existing buildings towards a new intended use.Interview 1A, representatives of construction company A

4.3.2. Coalition

You [the governmental organization] should stop asking for assurances in the way you used to do; it is more about facing the risks together and sharing the consequences alike. Now, in the current situation, the government tends to transfer every risk to the market; instead government should rather take on the role to control risks.Interview 2B, province representative

4.4. Boundary Systems

4.4.1. Code of Conduct

The company can be regarded as a frontrunner regarding the CE. Our ambition is to change the market as we have shown recently by offering the concept “Road construction as a service”. Currently, we develop critical performance indicators (KPIs) that support behavioral choices in line with the CE principles. This approach contrasts with that of public-owned companies which seem to introduce KPIs mainly for the sake of external reporting. They use the CE-related KPIs for shareholder reporting purposes.Interview 2D, sustainability officer, representing a large privately-owned construction company

4.4.2. Opportunity Space

And it is up to the group company how creative you are: how do you act in cooperation with other market parties? How creative can you be, which alternatives can you think off to get things going?Interview 1E, Finance director representing a large privately-owned construction company

4.5. Diagnostic Control System

4.5.1. Output

Joining a tender in the area of public procurement, RoadService is regularly required to provide lots of information detailing the calculations of the project’s circularity. We have to specify and make things measurable… all for the sake of comparing the proposals made by the various companies. But these requirements do not imply that you solve the problem in a sustainable way.Interview 3D, RoadService managing director

4.5.2. Evaluation

Scaling up business model innovation is crucial. It is essential to know who or what is needed to scale up an innovative initiative. Otherwise, no one embraces the innovation and you have to continually explain the same story.Interview 2A, government representative, national level

5. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Interviewees | Date | ||

|---|---|---|---|

| 1A | Building & development company | Managing director | 21 March 2016 |

| Controller | |||

| Senior employee, responsible for research & development | |||

| 1B | Road construction industry | Managing director | 4 April 2016 |

| Finance director | |||

| 1BB | Finance director | 28 August 2017 | |

| 1C | Construction company | Managing director | 6 April 2016 |

| 1CC | Managing director | 18 September 2017 | |

| Project manager | |||

| 1D | Building & development company | Controller | 19 April 2016 |

| 1E | Large construction company | Finance director | 12 June 2017 |

| Project manager | |||

| 1F | Building & development company | Managing director | 10 October 2017 |

| Finance director | |||

| 6 different construction companies | 12 managers and senior employees contributing to the themes future proof management control | 8 interviews |

| Representative | Interviewees | Date | |

|---|---|---|---|

| 2A | National department for road construction | national level | 22 March 2019 |

| 2B | Province | regional level | 27 March 2019 |

| 2C | Purchase department at a municipality | local level | 2 April 2019 |

| 2D | Large construction company | commercial perspective | 17 April 2019, by phone |

| Interviewees/Attendees | Date | ||

|---|---|---|---|

| 1A | Preliminary interview during internship | RoadService managing director | 2019 |

| 1B | Preliminary interview during internship | RoadService project manager | 2019 |

| 1BB | Presentation and discussion of the bachelor thesis | A group representing both RoadService staff and management | 12 July 2019 |

| 1C | Final interview | RoadService managing director and project manager | 13 December 2019 |

References

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Jonker, J. New Business Models. Working Together on Value Creation; Academic Service: The Hague, The Netherlands, 2014. [Google Scholar]

- García-Muiña, F.E.; Medina-Salgado, M.S.; Ferrari, A.M.; Cucchi, M. Sustainability transition in Industry 4.0 and Smart Manufacturing with the triple-layered business model canvas. Sustainability 2020, 12, 2364. [Google Scholar] [CrossRef] [Green Version]

- Urbinati, A.; Rosa, P.; Sassanelli, C.; Chiaroni, D.; Terzi, S. Circular business models in the European manufacturing industry: A multiple case study analysis. J. Clean. Prod. 2020, 274, 122964. [Google Scholar] [CrossRef]

- Carraresi, L.; Bröring, S. How does business model redesign foster resilience in emerging circular value chains? J. Clean. Prod. 2021, 289, 125823. [Google Scholar] [CrossRef]

- Rijksoverheid (Ministerie van Infrastructuur en Milieu & Ministerie van Economische Zaken). The Netherlands in 2050. Government-Wide Circular Economy Programme; The Hague, The Netherlands. 2016. Available online: https://www.rijksoverheid.nl/onderwerpen/circulaire-economie/documenten/rapporten/2016/09/14/bijlage-1-nederland-circulair-in-2050 (accessed on 28 November 2021).

- MacArthur, E.; Zumwinkel, K.; Stuchtey, M. Growth Within: A Circular Economy Vision for a Competitive Europe; Ellen MacArthur Foundation: Isle of Wight, UK, 2015. [Google Scholar]

- Lüdeke-Freund, F.; Gold, S.; Bocken, N.M.P. A Review and Typology of Circular Economy Business Model Patterns. J. Ind. Ecol. 2018, 23, 36–61. [Google Scholar] [CrossRef] [Green Version]

- Willekes, E.; Wagensveld, K. De levers of control en nieuwe businessmodellen: Een exploratieve case study. Maandbl. Voor Account. En Bedrijfsecon. 2016, 90, 486–496. [Google Scholar] [CrossRef]

- Simons, R. Levers of Control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business Press: Boston, MA, USA, 1995. [Google Scholar]

- Strauß, E.; Zecher, C. Management control systems: A review. J. Manag. Control 2013, 23, 233–268. [Google Scholar] [CrossRef]

- Merchant, K.A.; van der Stede, W.A. Management Control Systems: Performance Measurement, Evaluation and Incentives, 2nd ed.; Prentice Hall: Harlow, UK, 2007. [Google Scholar]

- Anthony, R.N.; Govindarajan, V. Management Control Systems, 12th ed.; McGraw-Hill: Boston, MA, USA, 2007. [Google Scholar]

- Widener, S.K. An empirical analysis of the levers of control framework. Account. Organ. Soc. 2007, 32, 757–788. [Google Scholar] [CrossRef]

- Arjaliès, D.-L.; Mundy, J. The use of management control systems to manage CSR strategy: A levers of control perspective. Manag. Account. Res. 2013, 24, 284–300. [Google Scholar] [CrossRef]

- Wagensveld, K. How Do Organizations Stay in Control in a Fast-Changing Environment: Inaugural Speech Professor Financial Control. 2016. Available online: https://hbo-kennisbank.nl/details/sharekit_han:Oai:Surfsharekit.nl:8f55e91f-5800-4ea2-9e20-1bd6a9a9815f (accessed on 24 October 2019).

- Pieroni, M.P.P.; McAloone, T.C.; Pigosso, D.C.A. Business model innovation for circular economy and sustainability: A review of approaches. J. Clean. Prod. 2019, 215, 198–216. [Google Scholar] [CrossRef]

- Veleva, V.; Bodkin, G. Corporate-entrepreneur collaborations to advance a circular economy. J. Clean. Prod. 2018, 188, 20–37. [Google Scholar] [CrossRef]

- Frishammar, J.; Parida, V. Circular Business Model Transformation: A Roadmap for Incumbent Firms. Calif. Manag. Rev. 2018, 61, 5–29. [Google Scholar] [CrossRef]

- Esposito, M.; Tse, T.; Soufani, K. Introducing a Circular Economy: New Thinking with New Managerial and Policy Implications. Calif. Manag. Rev. 2018, 60, 5–19. [Google Scholar] [CrossRef]

- Urbinati, A.; Chiaroni, D.; Chiesa, V. Towards a new taxonomy of circular economy business models. J. Clean. Prod. 2017, 168, 487–498. [Google Scholar] [CrossRef]

- Gusmerotti, N.M.; Testa, F.; Corsini, F.; Pretner, G.; Iraldo, F. Drivers and approaches to the circular economy in manufacturing firms. J. Clean. Prod. 2019, 230, 314–327. [Google Scholar] [CrossRef]

- De Haan-Hoek, J.; Lambrechts, W.; Semeijn, J.; Caniëls, M.C.J. Levers of Control for Supply Chain Sustainability: Control and Governance Mechanisms in a Cross-Boundary Setting. Sustainability 2020, 12, 3189. [Google Scholar] [CrossRef] [Green Version]

- Mendoza, J.M.F.; Sharmina, M.; Gallego-Schmid, A.; Heyes, G.; Azapagic, A. Integrating Backcasting and Eco-Design for the Circular Economy: The BECE Framework. J. Ind. Ecol. 2017, 21, 526–544. [Google Scholar] [CrossRef] [Green Version]

- Heyes, G.; Sharmina, M.; Mendoza, J.M.F.; Gallego-Schmid, A.; Azapagic, A. Developing and implementing circular economy business models in service-oriented technology companies. J. Clean. Prod. 2018, 177, 621–632. [Google Scholar] [CrossRef]

- Sarre, R.; Doig, M.; Fiedler, B. Reducing the Risk of Corporate Irresponsibility: The Trend to Corporate Social Responsibility. Account. Forum 2001, 25, 300–317. [Google Scholar] [CrossRef]

- Manninen, K.; Koskela, S.; Antikainen, R.; Bocken, N.; Dahlbo, H.; Aminoff, A. Do circular economy business models capture intended environmental value propositions? J. Clean. Prod. 2018, 171, 413–422. [Google Scholar] [CrossRef] [Green Version]

- CROW Handreiking voor Gemeenten: Duurzaamheid in Projecten en Organisaties [Guidelines for municipalities: Sustainability in Projects and Organizations]. 2018. Available online: https://www.crow.nl/over-crow/nieuws/2018/maart/handreiking-voor-gemeenten-duurzaamheid-in-project (accessed on 17 January 2020).

- Platform CB’23. Leidraad Meten van Circulariteit. Werkafspraken voor een Circulaire Bouw, Versie 2.0 [Working Instructions for Measuring Circularity, Agreed Working Rules for a Circular Construction Industry, Version 2.0]. 2020. Available online: https://platformcb23.nl/aan-de-slag/2020 (accessed on 15 December 2020).

| Simons [10], Considering Traditional Business Models | Analytical Focus Points in This Study Concerning Circular Business Models | |

|---|---|---|

| Belief systems | Formal and systematic in nature. | The beliefs systems

|

| Interactive control systems | Regulated. Mainly bottom-up. | The interactive control systems

|

| Boundary systems | The organization’s strategic boundaries are predefined. | The boundary systems

|

| Diagnostic control systems | Measuring output, comparing this with preset goals, and taking corrective actions if appropriate. | The diagnostic control systems

|

| Analytical Focus Points in This Study Concerning Circular Business Models | The Collected Empirical Examples of Circular Business Models | |

|---|---|---|

| Belief systems | The beliefs systems

|

|

| Interactive control systems | The interactive control systems

|

|

| Boundary systems | The boundary systems

|

|

| Diagnostic control systems | The diagnostic control systems

|

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ruiter, H.; De Feijter, F.; Wagensveld, K. Management Control and Business Model Innovation in the Context of a Circular Economy in the Dutch Construction Industry. Sustainability 2022, 14, 366. https://doi.org/10.3390/su14010366

Ruiter H, De Feijter F, Wagensveld K. Management Control and Business Model Innovation in the Context of a Circular Economy in the Dutch Construction Industry. Sustainability. 2022; 14(1):366. https://doi.org/10.3390/su14010366

Chicago/Turabian StyleRuiter, Henk, Frank De Feijter, and Koos Wagensveld. 2022. "Management Control and Business Model Innovation in the Context of a Circular Economy in the Dutch Construction Industry" Sustainability 14, no. 1: 366. https://doi.org/10.3390/su14010366