A Step-by-Step Process towards an Evolutionary Policy Encouraging the Adoption of Sustainable Business Models

Abstract

:1. Introduction

2. Firms Innovation: From Corporate Sustainability to Sustainable Business Models

3. The Role of Policies and Incentives in Fostering Corporate Sustainability

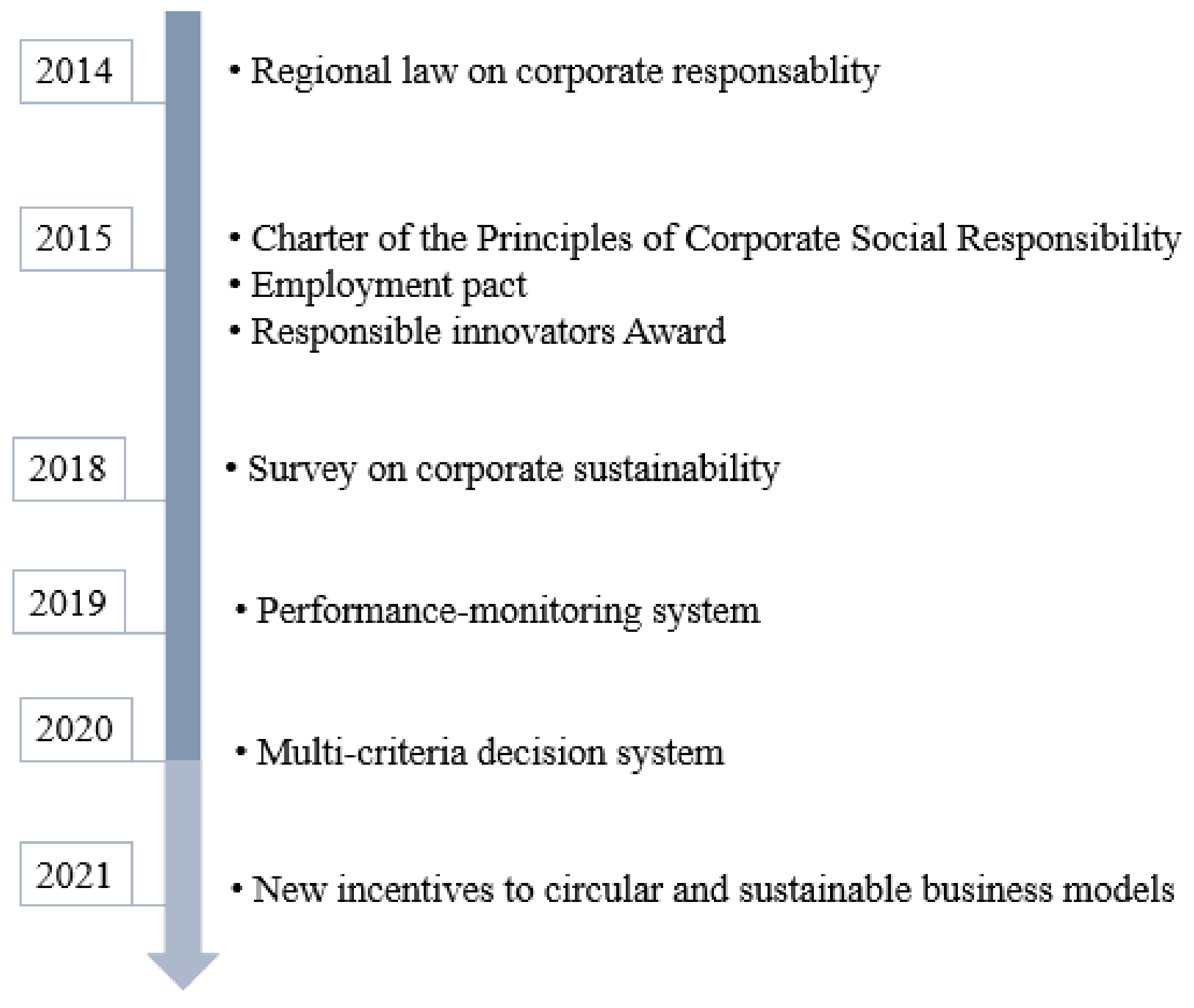

4. Emilia Romagna’s Process towards the Adoption of a Sustainable Business Model

- The critical issues relating to underperformance in the environmental management of regional economic activities.

- The internal levers pushing the company to innovate.

- The possible external inputs incentivizing the firm to rethink their business.

5. Materials and Methods

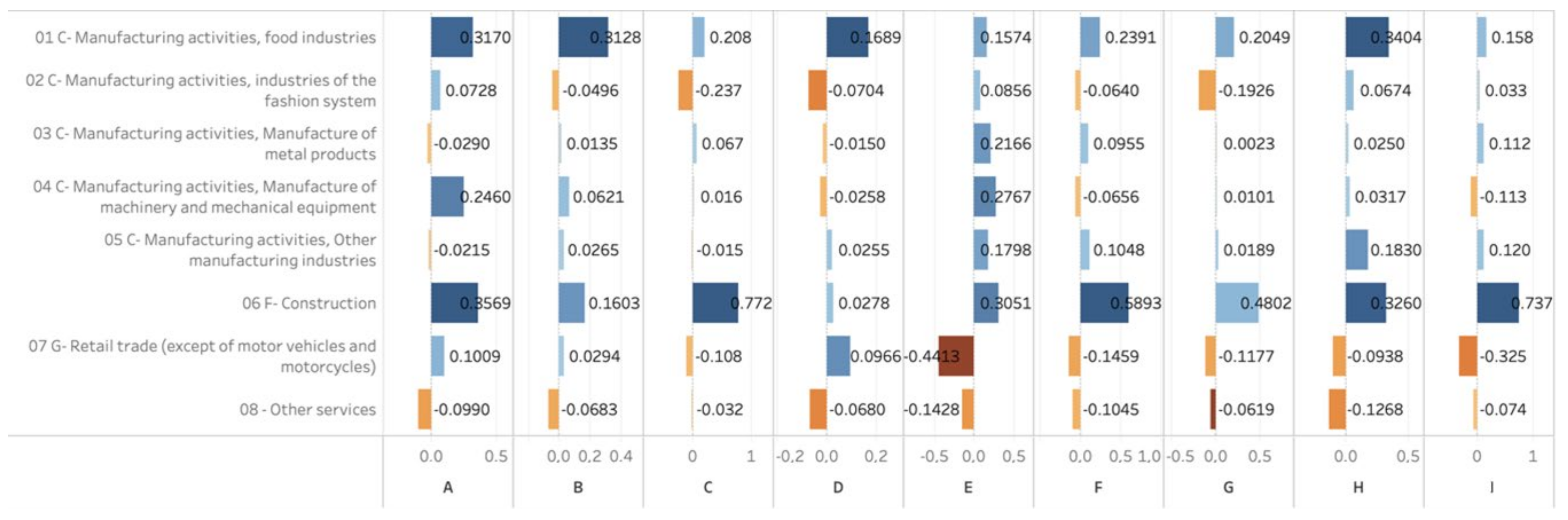

- Vendors’ choice—conventional criteria (Factor A) include five matters representing the typical criteria used in the supply chain definition; it investigates the companies’ approaches in adopting certain traditional characteristics such as economic convenience, product quality, trust and direct knowledge of suppliers.

- Vendors’ choice—sustainability criteria (Factor B) include five matters indicating the additional criteria summarizing the sustainability strategy adopted in the supply chain; it measures the propensity to choose suppliers with respect to ethical, environmental and social criteria, considering the effect on local employment, the environmental impact and other certifications.

- The monitoring of suppliers on sustainability (Factor C) includes seven elements that relate to safety and environmental protection, use of products and rules in compliance with the environmental impact and workers’ health and other ethical and social clauses.

- The section information and dialogue with customers/consumers (Factor D) is composed of seven elements that indicate the information that the company gives to its customers with respect to the environmental values and performances, results, social commitments, waste and sustainability actions that have been adopted.

- Worker benefits (Factor E) are calculated with eight elements on training, social security, hourly flexibility, services, teleworking, leave and conventions and generally represents the actions on welfare.

- The reporting tools (Factor F) are composed of six sub-topics referring to the external communication with attention to the social and sustainability report and the sustainability objectives of the United Nations.

- The relations with the local community and the territory (Factor G) consist of five items on collaborations with the university, support for projects on the promotion of the territory, well-being, health or dialogue and support for social and environmental issues.

- The strategic and financial motivations (Factor H) are composed of eight items with respect to the adoption of sustainable strategies and are measured with six elements on ethical sensitivity, the various competitive strategies, the supply chain, the reduction in waste and management savings.

- The compliance motivation (Factor I) is composed of six items on the benefits of companies from residual sales, government incentives and regulatory requests.

- The Ecological Footprint—Energy (Factor J) is measured with seven items ranging from the supply of energy from renewable sources and energy efficiency measures to the estimate of emissions into the atmosphere.

- The Ecological Footprint—Materials (Factor K) is measured with seven items and takes higher values in the case of companies that use environmentally sustainable stationery materials, biodegradable and compostable plastics, ecological cleaning products, which cause material consumption reductions during production and the elimination of single-use products.

- The Ecological Footprint—Water (Factor L), is measured with four items on the installation of flow limiters and electronic taps/with timers, use of tap water to replace mineral water bottles, installation of collection systems and use of rainwater and/or systems for the recovery and reuse of water and reduction in water consumption per unit of product, in the production process.

- The Ecological Footprint—Plastic (Factor M) is composed of four items and has been introduced to increase awareness on marine plastic pollution and is measured from four questions on the practices of reducing harmful substances and the use of packaging and plastic residues.

- The Ecological Footprint—Waste (Factor N) is measured by four items on the organization of separate collection, waste recovery and reduction.

6. Results and Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable Innovation, Business Models and Economic Performance: An Overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- The United Nations. United Nations Agenda 2030; United Nations: New York, CA, USA, 2015. [Google Scholar]

- Fischedick, M.; Roy, J.; Abdel, A.A.; Acquaye, A.; Ceron, J.P.; Geng, Y.; Kheshgi, H.; Lanza, A.; Per-czyk, D.; Price, L.; et al. Industry. In Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014. [Google Scholar]

- Miller, T.R.; Wiek, A.; Sarewitz, D.; Robinson, J.; Olsson, L.; Kriebel, D.; Loorbach, D. The Future of Sustainability Science: A Solutions-Oriented Research Agenda. Sustain. Sci. 2014, 9, 239–246. [Google Scholar] [CrossRef]

- Bos-Brouwers, H.E.J. Corporate Sustainability and Innovation in SMEs: Evidence of Themes and Activities in Practice. Bus. Strat. Environ. 2009, 19, 417–435. [Google Scholar] [CrossRef]

- Ramaswamy, V.; Ozcan, K. The Co-Creation Paradigm; Walter de Gruyter GmbH: Berlin, Germany, 2014. [Google Scholar]

- Bevir, M. The SAGE Handbook of Governance; Indian Institute of Management: Kozhikode, India, 2011. [Google Scholar]

- Heinrichs, H.; Laws, N. “Sustainability State” in the Making? Institutionalization of Sustainability in German Federal Policy Making. Sustainability 2014, 6, 2623–2641. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. In Managing Sustainable Business: An Executive Education Case and Textbook; Lenssen, G.G., Smith, N.C., Eds.; Springer: Dordrecht, The Netherlands, 2019; pp. 323–346. ISBN 978-94-024-1144-7. [Google Scholar]

- WBCSD. Business Case for Sustainable Development Making a Difference toward the Johannesburg Summit 2002 and Beyond; World Business Council for Sustainable Development: Johanesburg, South Africa, 2002. [Google Scholar]

- Montiel, I. Corporate Social Responsibility and Corporate Sustainability. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef] [Green Version]

- Keeble, B.R. The Brundtland Report: ‘Our Common Future’. Med. War 1988, 4, 17–25. [Google Scholar] [CrossRef]

- Morioka, S.N.; Bolis, I.; Evans, S.; Carvalho, M.M. Transforming Sustainability Challenges into Competitive Advantage: Multiple Case Studies Kaleidoscope Con-Verging into Sustainable Business Models. J. Clean. Prod. 2017, 167, 723–738. [Google Scholar] [CrossRef]

- Stubbs, W.; Cocklin, C. Conceptualizing a “Sustainability Business Model”. Organ. Environ. 2008, 21, 103–127. [Google Scholar] [CrossRef]

- Biloslavo, R.; Bagnoli, C.; Edgar, D. An Eco-Critical Perspective on Business Models: The Value Triangle as an Approach to Closing the Sustainability Gap. J. Clean. Prod. 2018, 174, 746–762. [Google Scholar] [CrossRef] [Green Version]

- Van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. J. Bus. Ethic. 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Bansal, P. Evolving Sustainably: A Longitudinal Study of Corporate Sustainable Development. Strat. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Gladwin, T.N.; Kennelly, J.J.; Krause, T.-S. Shifting Paradigms for Sustainable Development: Implications for Management Theory and Research. Acad. Manag. Rev. 1995, 20, 874. [Google Scholar] [CrossRef] [Green Version]

- Dyllick, T.; Hockerts, K. Beyond the Business Case for Corporate Sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Burritt, R.L.; Schaltegger, S. Sustainability Accounting and Reporting: Fad or Trend? Account. Audit. Account. J. 2010, 23, 829–846. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Dembek, K. Sustainable Business Model Research and Practice: Emerging Field or Passing Fancy? J. Clean. Prod. 2017, 168, 1668–1678. [Google Scholar] [CrossRef]

- Geissdoerfer, M.; Vladimirova, D.; Evans, S. Sustainable Business Model Innovation: A Review. J. Clean. Prod. 2018, 198, 401–416. [Google Scholar] [CrossRef]

- Ordonez-Ponce, E.; Clarke, A.C.; Colbert, B.A. Collaborative Sustainable Business Models: Understanding Organizations Partnering for Community Sustainability. Bus. Soc. 2020, 0007650320940241. [Google Scholar] [CrossRef]

- Fiore, M.; Galati, A.; Gołębiewski, J.; Drejerska, N. Stakeholders’ Involvement in Establishing Sustainable Business Models. Br. Food J. 2020, 122, 1671–1691. [Google Scholar] [CrossRef]

- Shields, J.; Shelleman, J.M. Integrating Sustainability into SME Strategy. JSBS 2015, 25, 59–78. [Google Scholar]

- Upward, A.; Jones, P. An Ontology for Strongly Sustainable Business Models. Organ. Environ. 2016, 29, 97–123. [Google Scholar] [CrossRef] [Green Version]

- Goni, F.A.; Chofreh, A.G.; Orakani, Z.E.; Klemeš, J.J.; Davoudi, M.; Mardani, A. Sustainable Business Model: A Review and Framework Development. Clean Technol. Environ. Policy 2020, 1–9. [Google Scholar] [CrossRef]

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A Literature and Practice Review to Develop Sustainable Business Model Archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef] [Green Version]

- Manninen, K.; Koskela, S.; Antikainen, R.; Bocken, N.; Bontempi, E.; Aminoff, A. Do Circular Economy Business Models Capture Intended Environmental Value Propositions? J. Clean. Prod. 2018, 171, 413–422. [Google Scholar] [CrossRef] [Green Version]

- Velter, M.; Bitzer, V.; Bocken, N.; Kemp, R. Sustainable Business Model Innovation: The Role of Boundary Work for Multi-Stakeholder Alignment. J. Clean. Prod. 2020, 247, 119497. [Google Scholar] [CrossRef]

- Seiffert, M.E.B.; Loch, C. Systemic Thinking in Environmental Management: Support for Sustainable Development. J. Clean. Prod. 2005, 13, 1197–1202. [Google Scholar] [CrossRef]

- Vieira, P.F. Environmental Problematic and Social Sciences in Brazil. Ecology and Development: Problematic and Politics; Escola Profissional para a Educaciao e Desenvolvimento (EPED): Rio de Janeiro, Brazil, 1992. [Google Scholar]

- Schaltegger, S.; Freund, F.L.; Hansen, E.G. Business Cases for Sustainability: The Role of Business Model Innovation for Corporate Sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the Integration of Corporate Sustainability into Strategic Management: A Literature Review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- Lewandowski, M. Designing the Business Models for Circular Economy—Towards the Conceptual Framework. Sustainability 2016, 8, 43. [Google Scholar] [CrossRef] [Green Version]

- Lozano, R.; Carpenter, A.; Huisingh, D. A Review of ‘Theories of the Firm’ and Their Contributions to Corporate Sustainability. J. Clean. Prod. 2015, 106, 430–442. [Google Scholar] [CrossRef]

- Nosratabadi, S.; Mosavi, A.; Shamshirband, S.; Zavadskas, E.K.; Rakotonirainy, A.; Ahmadi, M.H. Sustainable Business Models: A Review. Sustainability 2019, 11, 1663. [Google Scholar] [CrossRef] [Green Version]

- Barbieri, R.; Santos, D.F.L. Sustainable Business Models and ECo-innovation: A Life Cycle Assessment. J. Clean. Prod. 2020, 266, 121954. [Google Scholar] [CrossRef]

- Denning, S. Navigating the Phase Change to the Creative Economy. Strat. Leadersh. 2014, 42, 3–11. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hansen, E.G.; Lüdeke-Freund, F. Business Models for Sustainability: Origins, Present Research, and Future Avenues. Organ. Environ. 2015, 29, 3–16. [Google Scholar] [CrossRef]

- Colombo, L.A.; Pansera, M.; Owen, R. The Discourse of Eco-Innovation in the European Union: An Analysis of the ECo-innovation Action Plan and Horizon 2020. J. Clean. Prod. 2019, 214, 653–665. [Google Scholar] [CrossRef] [Green Version]

- Triguero, A.; Moreno-Mondéjar, L.; Davia, M.A. Drivers of Different Types of Eco-Innovation in European SMEs. Ecol. Econ. 2013, 92, 25–33. [Google Scholar] [CrossRef]

- Cerin, P.; Karlson, L. Business Incentives for Sustainability: A Property Rights Approach. Ecol. Econ. 2002, 40, 13–22. [Google Scholar] [CrossRef]

- Porter, M.E.; Van Der Linde, C. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Chen, C.; Liu, L.Q. Pricing and Quality Decisions and Financial Incentives for Sustainable Product Design with Recycled Material Content under Price Leadership. Int. J. Prod. Econ. 2014, 147, 666–677. [Google Scholar] [CrossRef]

- Schneider, A.; Ingram, H. Behavioral Assumptions of Policy Tools. J. Polit. 1990, 52, 510–529. [Google Scholar] [CrossRef] [Green Version]

- Coase, R.H. The Problem of Social Cost. J. Law Econ. 1960, 3, 1–44. [Google Scholar] [CrossRef]

- Coase, R.H. The Problem of Social Cost. In Economic Analysis of the Law; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 2007; pp. 1–13. ISBN 978-0-470-75213-5. [Google Scholar]

- Fullerton, D. Why Have Separate Environmental Taxes? NBER Tax Policy Econ. 1996, 10, 33–70. [Google Scholar] [CrossRef] [Green Version]

- Demsetz, H. The Theory of the Firm Revisited. J. Law Econ. Organ. 1988, 4, 141–161. [Google Scholar] [CrossRef]

- Nill, J.; Kemp, R. Evolutionary Approaches for Sustainable Innovation Policies: From Niche to Paradigm? Res. Policy 2009, 38, 668–680. [Google Scholar] [CrossRef]

- Zollo, M.; Cennamo, C.; Neumann, K. Beyond What and Why. Organ. Environ. 2013, 26, 241–259. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Sharma, S. A Contingent Resource-Based View of Proactive Corporate Environmental Strategy. Acad. Manag. Rev. 2003, 28, 71–88. [Google Scholar] [CrossRef] [Green Version]

- Goetz, K.S. Encouraging Sustainable Business Practices Using Incentives: A Practitioner’s View. Manag. Res. Rev. 2010, 33, 1042–1053. [Google Scholar] [CrossRef]

- Stirling, A. Pluralising Progress: From Integrative Transitions to Transformative Diversity. Environ. Innov. Soc. Transit. 2011, 1, 82–88. [Google Scholar] [CrossRef]

- European Environment Agency. European Commission Closing the Loop—An EU Action Plan for the Circular Economy COM/2015/0614 Final; European Environment Agency: Copenhagen, Denmark, 2015. [Google Scholar]

- European Environment Agency. European Commission A Sustainable Bioeconomy for Europe: Strengthening the Connection between Economy, Society and the Environment {SWD(2018) 431 Final}; European Environment Agency: Copenhagen, Denmark, 2018. [Google Scholar]

- European Environment Agency. European Commission Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. A New Industrial Strategy for Europe COM(2020) 102 Final; European Environment Agency: Copenhagen, Denmark, 2020. [Google Scholar]

- Hoffman, A.J. Competitive Environmental Strategy: A Guide to the Changing Business Landscape; Island Press: Washington, DC, USA, 2000. [Google Scholar]

- Long, N. From Paradigm Lost to Paradigm Regained? The Case for an Actor-Oriented Sociology of Development. Revista Europea de Estudios Latinoamericanos y del Caribe. Eur. Rev. Lat. Am. Caribb. Stud. 1990, 49, 23–24. [Google Scholar]

- Musiolik, J.; Markard, J.; Hekkert, M. Networks and Network Resources in Technological Innovation Systems: Towards a Conceptual Framework for System Building. Technol. Forecast. Soc. Chang. 2012, 79, 1032–1048. [Google Scholar] [CrossRef] [Green Version]

- Aristovnik, A.; Obadić, A. The Impact and Efficiency of Public Administration Excellence on Fostering SMEs in EU Countries. Amfiteatru Econ. 2015, 17, 15. [Google Scholar]

- Ou, C.; Haynes, G. Acquisition of Additional Equity Capital by Small Firms—Findings from the National Survey of Small Business Finances. Small Bus. Econ. 2006, 27, 157–168. [Google Scholar] [CrossRef]

- Moors, E.H.; Mulder, K.; Vergragt, P.J. Towards Cleaner Production: Barriers and Strategies in the Base Metals Producing Industry. J. Clean. Prod. 2005, 13, 657–668. [Google Scholar] [CrossRef] [Green Version]

- European Court of Auditors. Review No 03/2019: Allocation of Cohesion Policy Funding to Member States for 2021–2027 (Rapid Case Review). Eur. Court. Audit. 2019. Available online: https://www.eca.europa.eu/en/Pages/DocItem.aspx?did=49531 (accessed on 15 January 2021).

- Farla, J.; Markard, J.; Raven, R.R.; Coenen, L. Sustainability Transitions in the Making: A Closer Look at Actors, Strategies and Resources. Technol. Forecast. Soc. Chang. 2012, 79, 991–998. [Google Scholar] [CrossRef] [Green Version]

- ASviS. L’Italia e Gli Obiettivi Di Sviluppo Sostenibile; ASviS: Rome, Italy, 2019. [Google Scholar]

- Clayton, A.F.; Rogerson, J.M.; Rampedi, I. Integrated Reporting vs. Sustainability Reporting for Corporate Responsibility in South Africa. Bull. Geogr. Sociocon. Ser. 2015, 29, 7–17. [Google Scholar] [CrossRef] [Green Version]

- O’Dwyer, B.; Owen, D.L. Assurance Statement Practice in Environmental, Social and Sustainability Reporting: A Critical Evaluation. Br. Account. Rev. 2005, 37, 205–229. [Google Scholar] [CrossRef]

- Newig, J.; Schulz, D.; Fischer, D.; Hetze, K.; Laws, N.; Lüdecke, G.; Rieckmann, M. Communication Regarding Sustainability: Conceptual Perspectives and Exploration of Societal Subsystems. Sustainability 2013, 5, 2976–2990. [Google Scholar] [CrossRef] [Green Version]

- Borga, F.; Citterio, A.; Noci, G.; Pizzurno, E. Sustainability Report in Small Enterprises: Case Studies in Italian Furniture Companies. Bus. Strat. Environ. 2009, 18, 162–176. [Google Scholar] [CrossRef]

- Anastas, P.T.; Breen, J.J. Design for the Environment and Green Chemistry: The Heart and Soul of Industrial Ecology. J. Clean. Prod. 1997, 5, 97–102. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Spalanzani, A. Sustainability of Manufacturing and Services: Investigations for Research and Applications. Int. J. Prod. Econ. 2012, 140, 35–47. [Google Scholar] [CrossRef]

- Saarinen, J. Traditions of Sustainability in Tourism Studies. Ann. Tour. Res. 2006, 33, 1121–1140. [Google Scholar] [CrossRef]

- Jin, Z.; Navare, J.; Lynch, R. The Relationship between Innovation Culture and Innovation Outcomes: Exploring the Effects of Sustainability Orientation and Firm Size. R&D Manag. 2018, 49, 607–623. [Google Scholar] [CrossRef]

- Seuring, S.; Müller, P.D.M. From a Literature Review to a Conceptual Framework for Sustainable Supply Chain Management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Costantini, V.; Crespi, F. Public Policies for a Sustainable Energy Sector: Regulation, Diversity and Fostering of Innovation. J. Evol. Econ. 2010, 23, 401–429. [Google Scholar] [CrossRef] [Green Version]

- Emilia Romagna Region E-R. Bollettino Ufficiale Della Regione Emilia-Romagna (BURERT); Emilia Romagna Region E-R: Bologna, Italy, 2015. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Factor | Questionnaire Items | Cronbach’s Alpha | RMSEA | CFI | TLI | AVE | CR |

|---|---|---|---|---|---|---|---|

| A. Vendors’ Choice—Conventional Criteria | 5 | 0.70 | 0.059 | 0.98 | 0.95 | 0.51 | 0.71 |

| B. Vendors’ Choice—Sustainability Criteria | 5 | 0.79 | 0.067 | 0.97 | 0.96 | 0.49 | 0.70 |

| C. Monitoring of suppliers on sustainability | 7 | 0.89 | 0.014 | 0.98 | 0.99 | 0.51 | 0.87 |

| D. Information and dialogue with customers/consumers | 7 | 0.87 | 0.074 | 0.98 | 0.96 | 0.53 | 0.86 |

| E. Benefits for workers | 8 | 0.83 | 0.09 | 0.96 | 0.94 | 0.49 | 0.81 |

| F. Reporting tools | 6 | 0.79 | 0.062 | 0.99 | 0.98 | 0.57 | 0.89 |

| G. Relations with the local community and the territory | 5 | 0.84 | 0.07 | 0.98 | 0.96 | 0.49 | 0.82 |

| H. Strategic and financial reasons for sustainability | 8 | 0.87 | 0.07 | 0.98 | 0.95 | 0.48 | 0.87 |

| I. Compliance reasons for sustainability | 6 | 0.82 | 0.060 | 0.98 | 0.96 | 0.49 | 0.81 |

| J. Ecological Footprint: Energy | 7 | 0.84 | 0.08 | 0.94 | 0.92 | 0.46 | 0.82 |

| K. Ecological Footprint: Materials | 5 | 0.76 | 0.08 | 0.96 | 0.93 | 0.49 | 0.76 |

| L. Ecological Footprint: Water | 4 | 0.81 | 0.07 | 0.94 | 0.92 | 0.47 | 0.79 |

| M. Ecological Footprint: Plastic | 4 | 0.76 | 0.06 | 0.98 | 0.97 | 0.47 | 0.77 |

| N. Ecological Footprint: Waste | 4 | 0.71 | 0.07 | 0.98 | 0.96 | 0.49 | 0.71 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Paletta, A.; Foschi, E.; Alimehmeti, G.; Bonoli, A. A Step-by-Step Process towards an Evolutionary Policy Encouraging the Adoption of Sustainable Business Models. Sustainability 2021, 13, 1176. https://doi.org/10.3390/su13031176

Paletta A, Foschi E, Alimehmeti G, Bonoli A. A Step-by-Step Process towards an Evolutionary Policy Encouraging the Adoption of Sustainable Business Models. Sustainability. 2021; 13(3):1176. https://doi.org/10.3390/su13031176

Chicago/Turabian StylePaletta, Angelo, Eleonora Foschi, Genc Alimehmeti, and Alessandra Bonoli. 2021. "A Step-by-Step Process towards an Evolutionary Policy Encouraging the Adoption of Sustainable Business Models" Sustainability 13, no. 3: 1176. https://doi.org/10.3390/su13031176