The Impact of the COVID-19 Pandemic on the Global Value Chain of the Manufacturing Industry

Abstract

:1. Introduction

2. Materials and Methods

2.1. Data Sources and Processing

2.2. GYDN Model Improvements

2.2.1. GYDN Model

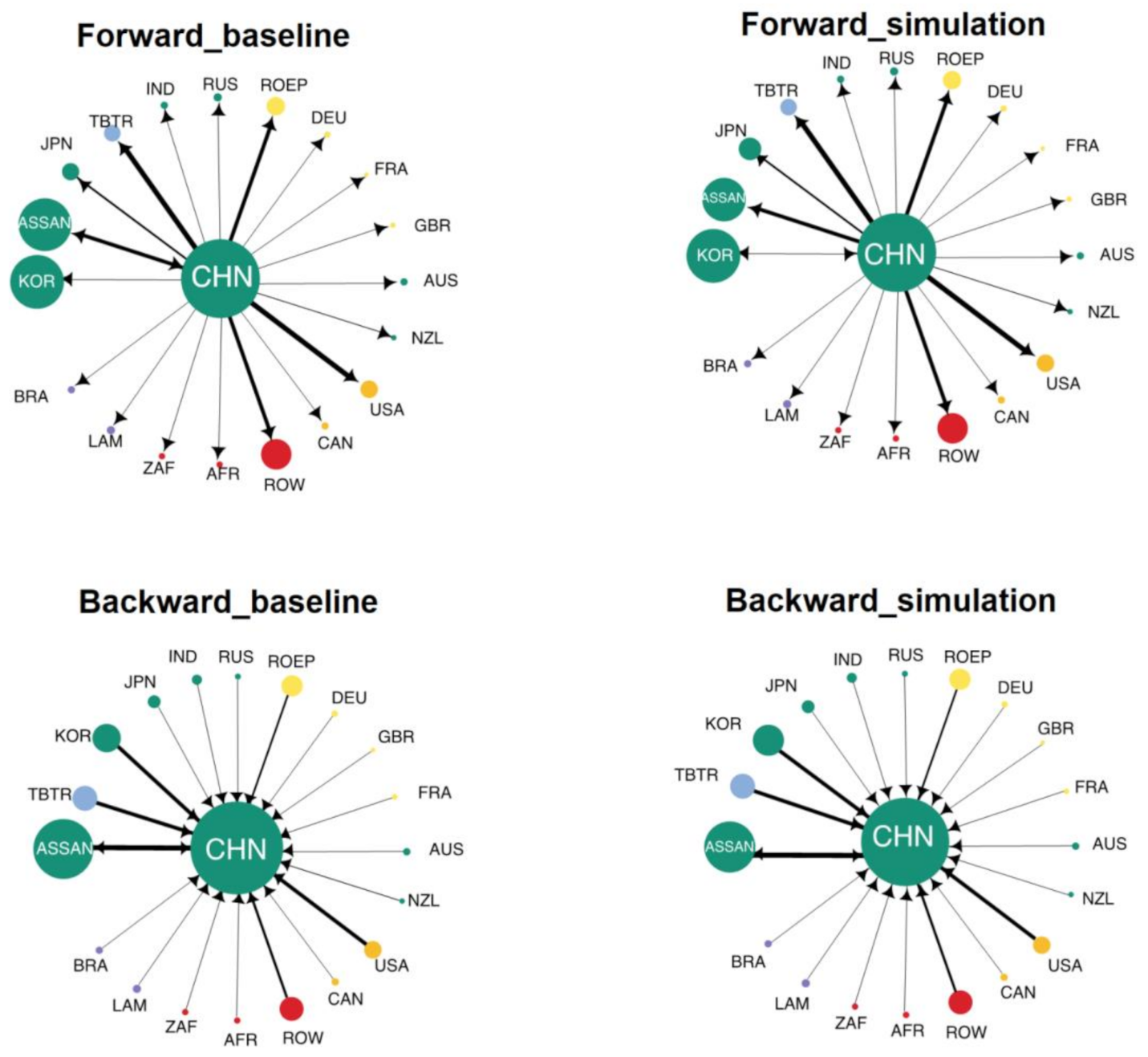

2.2.2. Method of Social Network Analysis

2.2.3. Scenario Setting

Employment Rate

Consumption

Trade Facilitation

Investment Level

2.3. Global Value Chain Participation Index

3. Results and Analysis

3.1. The Impact on the Output of Global Manufacturing

3.2. Impact on the GVC of the Global Manufacturing Industry

3.2.1. Impact of Novel Coronavirus Pneumonia on the Participation of Global Value Chains at the National Level

3.2.2. Structural Changes in the GVC of Traditional Manufacturing

3.2.3. Structural Changes in the Manufacturing GVC from the Angle of Simple GVC

3.2.4. Structural Changes in Complex GVC of Manufacturing Industries

4. Discussion

4.1. Modification of the GDYN Model and the Data Base

4.2. The Impact of Epidemics on Specific Manufacturing Industries

4.3. Limitations

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- OECD. OECD Employment Outlook 2020: Worker Security and the COVID-19 Crisis; OECD Publishing: Paris, France, 2020. [Google Scholar]

- OECD. OECD Policy Responses to Coronavirus (COVID-19): An Assessment of the Impact of COVID-19 on Job and Skills Demand Using Online Job Vacancy Data. 2021. Available online: https://www.oecd.org/coronavirus/policy-responses/an-assessment-of-the-impact-of-covid-19-on-job-and-skills-demand-using-online-job-vacancy-data-20fff09e/ (accessed on 1 February 2021).

- World Economic Look January 2021. Available online: https://www.imf.org/en/Publications/WEO?page=1 (accessed on 21 January 2021).

- German Federal Statistical Office (destatis.de): Gross Domestic Product (GDP). Available online: https://www.destatis.de/EN/Themes/Economy/National-Accounts-Domestic-Product/Tables/gdp-bubbles.html;jsessionid=1853BA9C044EE3164A33400145E67EFD.live722 (accessed on 11 September 2021).

- The Cabinet Office: National Economic Statistics. Available online: https://www.esri.cao.go.jp/jp/sna/menu.html (accessed on 11 September 2021).

- The Guardian: UK Economy Shrinks Record 9.9% in 2020 on Virus. Available online: https://guardian.ng/news/uk-economy-shrinks-record-9-9-in-2020-on-virus (accessed on 11 September 2021).

- IMF. Policy Responses to COVID-19. 2020. Available online: https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19 (accessed on 21 January 2021).

- Porter, M. Competitive Advantage: Creating and Sustaining Superior Performance; The Free Press: New York, NY, USA, 1985. [Google Scholar]

- Kogut, B. Designing Global Strategies: Comparative and Competitie Value-added Chains. Sloan Manag. Rev. 1985, 26, 15. [Google Scholar]

- Hummels, D.; Ishii, J.; Yi, K.-M. The nature and growth of vertical specialization in world trade. J. Int. Econ. 2001, 54, 75–96. [Google Scholar] [CrossRef]

- Daudin, G.; Rifflart, C.; Schweisguth, D. Who produces for whom in the world economy? Can. J. Econ. Rev. Can. Déconomique 2011, 44, 1403–1437. [Google Scholar] [CrossRef] [Green Version]

- Johnson, R.C.; Noguera, G. Accounting for intermediates: Production sharing and trade in value added. J. Int. Econ. 2012, 86, 224–236. [Google Scholar] [CrossRef] [Green Version]

- Koopman, R.; Wang, Z.; Wei, S.-J. Tracing Value-added and Double Counting in Gross Exports. Am. Econ. Rev. 2012, 104, 459–494. [Google Scholar] [CrossRef] [Green Version]

- Wang, Z.; Wei, S.-J.; Zhu, K. Quantifying International Production Sharing at the Bilateral and Sector Levels. NBER Working Paper. 2013. Available online: https://www.nber.org/papers/w19677 (accessed on 18 May 2021).

- Wang, Z.; Wei, S.J.; Zhu, K.F. Gross Trade Accounting Method: Offical Trade Statistics and Measurement of the Global Value Chain. Soc. Sci. China 2015, 9, 108–127. [Google Scholar]

- Wang, Z.; Wei, S.-J.; Yu, X.; Zhu, K. Measures of Participation in Global Value Chains and Global Business Cycles. NBER Working Paper. 2017. Available online: https://www.nber.org/papers/w23222 (accessed on 18 May 2021).

- Verikios, G. The dynamic effects of infectious disease outbreaks: The case of pandemic influenza and human coronavirus. Socio-Econ. Plan. Sci. 2020, 71, 100898. [Google Scholar] [CrossRef] [PubMed]

- Islam, M.R.; Muyeed, A. Impacts of COVID-19 pandemic on global economy: A meta-analysis approach. Int. J. Tech. Res. Sci. 2020, 5, 8–19. [Google Scholar] [CrossRef]

- Guan, D.; Wang, D.; Hallegatte, S.; Davis, S.J.; Huo, J.; Li, S.; Gong, P. Global supply-chain effects of COVID-19 control measures. Nat. Hum. Behav. 2020, 4, 577–587. [Google Scholar] [CrossRef] [PubMed]

- Li, H.l.; Chen, W.H. COVID-19 Epidemic Impact on the Global Manufacturing Supply Chain and my country’s strategy. Price Theory Pract. 2020, 5, 9–12. [Google Scholar]

- Rajak, S.; Mathiyazhagan, K.; Agarwal, V.; Sivakumar, K.; Kumar, V.; Appolloni, A. Issues and analysis of critical success factors for the sustainable initiatives in the supply chain during COVID- 19 pandemic outbreak in India: A case study. Res. Transp. Econ. 2021, 101114. [Google Scholar] [CrossRef]

- Walmsley, T.L.; Rose, A.; Wei, D. Impacts on the U.S. macroeconomy of mandatory business closures in response to the COVID-19 Pandemic. Appl. Econ. Lett. 2021, 28, 1293–1300. [Google Scholar] [CrossRef]

- Duan, H.; Bao, Q.; Tian, K.; Wang, S.; Yang, C.; Cai, Z. The hit of the novel coronavirus outbreak to China’s economy. China Econ. Rev. 2021, 67, 101606. [Google Scholar] [CrossRef]

- Zhao, Z.X.; Yang, J. The Impact of COVID—19 on Shandong’s Economyand Industry Chain and Its Countermeasures. Rev. Econ. Manag. 2020, 3, 5–10. [Google Scholar]

- Shen, G.B.; Xu, Y.H. The Impacts of Global Spread of COVID—19 Pandemic on China’s Export, Import and Global Industrial Chain and Related Countermeasures. J. Sichuan Univ. 2020, 4, 75–90. [Google Scholar]

- Zhu, K.F.; Gao, X.; Yang, C.H.; Wang, S.Y. The COVID-19 Shock on Global Production Chains and Risk of Accelerated China’s Industrial Chains Outflow. Bull. Chin. Acad. Sci. 2020, 35, 283–288. [Google Scholar]

- Minor, P.; Tsigas, M. Impacts of Better Trade Facilitation in Developing Countries: Analysis with a New GTAP Database for the Value of Time in Trade; Global Trade Analysis Project, Working Paper; Purdue University: West Lafayette, IN, USA, 2008. [Google Scholar]

- Dixon, P.; Rimmer, M.; Lee, B.; Rose, A.; Rose, A.; Verikios, G. Effects on the U.S. Of an H1N1 Epidemic: Analysis with a Quarterly CGE Model. J. Homel. Secur. Emerg. Manag. 2010, 7, 7. [Google Scholar] [CrossRef] [Green Version]

- Hertel, T.D.; Tsigas, M.E. Structure of GTAP. In Global Trade Analysis: Modeling and Applications; Hertel, T.W., Ed.; Cambridge: New York, NY, USA, 1997; pp. 13–73. [Google Scholar]

- Ianchovichina, E.; Walmsley, T.L. Dynamic Modeling and Applications for Global Economic Analysis; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- Chappuis, T.; Walmsley, T. Projections for World CGE Model Baselines; GTAP Research Memoranda 3728, Center for Global Trade Analysis; Working Paper; Department of Agricultural Economics, Purdue University: West Lafayette, IN, USA, 2011. [Google Scholar]

- Meng, B.; Xiao, H.; Ye, J.; Li, S. Are Global Value Chains Truly Global? A New Perspective Based on the Measure of Trade in Value-Added; Institute of Developing Economies, Japan External Trade Organization (JETRO): Tokyo, Japan, 2019. [Google Scholar]

- U.S. Bureau of Economic Analysis (BEA): Gross Domestic Product, (Third Estimate), GDP by Industry, and Corporate Profits, Fourth Quarter and Year 2020. Available online: https://www.bea.gov/index.php/news/2021/gross-domestic-product-third-estimate-gdp-industry-and-corporate-profits-4th-quarter-and (accessed on 18 May 2021).

- Dunn, A.C.; Hood, K.K.; Driessen, A. Measuring the Effects of the COVID-19 Pandemic on Consumer Spending Using Card Transaction Data. BEA Working Paper Series 2020-5. 2020. Available online: https://www.bea.gov/system/files/papers/BEA-WP2020-5_0.pdf (accessed on 11 March 2021).

- Yang, J.; Huang, J.; Hong, J.J.; Dong, W.L. Analysis of Impacts of Trade Facilitation on China’s Economy. J. Int. Trade 2015, 9, 156–166. [Google Scholar]

- Zhao, J.L.; Xiao, W. The Influence of COVID-19 Epidemic on the Global Value Chain of China. China Econ. Trade Guide. 2020, 6, 15–16. [Google Scholar]

- Fujimori, S.; Oshiro, K.; Shiraki, H.; Hasegawa, T. Energy transformation cost for the Japanese mid-century strategy. Nat. Commun. 2019, 10, 4737. [Google Scholar]

- Kapitza, S.; Van Ha, P.; Kompas, T.; Golding, N.; Cadenhead, N.C.R.; Bal, P.; Wintle, B.A. Assessing biophysical and socio-economic impacts of climate change on regional avian biodiversity. Sci. Rep. 2021, 11, 3304. [Google Scholar]

- Li, X.; Ghadami, A.; Drake, J.M.; Rohani, P.; Epureanu, B.I. Mathematical model of the feedback between global supply chain disruption and COVID-19 dynamics. Sci. Rep. 2021, 11, 15450. [Google Scholar]

- Zhou, L.L.; Zhang, K.Y. Study of Reconstruction of Chinese Global Value Chains Participation on COVID-19. Rev. Ind. Econ. 2020, 25, 5–15. [Google Scholar]

- McKibbin, W.; Fernando, R. The Global Macroeconomic Impacts of COVID-19: Seven Scenarios. Asian Econ. Pap. 2021, 20, 1–30. [Google Scholar] [CrossRef]

- Walmsley, T.; Minor, P. ImpactECON Global Supply Chain Model: Documentation of Model Changes; Working Paper No. 06; ImpactECON: Boulder, CO, USA, 2016. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country Division | GTAP Primitive Country Division |

|---|---|

| Country | Australia (AUS), China (CHN), Japan (JPN), South Korea (KOR), India (IND), United State of America (USA), Germany (DEU), Brazil (RUS), Russia (RUS), South Africa (ZAF), United Kingdom (UK) |

| Region | ASEAN, Latin America (except Brazil, LAM), European Union (except France and Germany, EU), Belt and Road Initiative (TBTR), other countries in the world (ROW) |

| Industry Division | |

|---|---|

| Low tech | Textile and clothing; Leather products industry; Wood processing; Papermaking and printing, other manufacturing industries |

| Medium tech | Petroleum and coal processing; Rubber and plastic manufacturing; Ferrous metal smelting and processing; Non-ferrous metal smelting and processing; Metal products industry; Other fuel processing industries; |

| High tech | Chemical fiber manufacturing industry; Medical manufacturing industry; Automobile manufacturing; Transportation equipment manufacturing; Computer, communications and other electronic equipment manufacturing (referred to as electronic equipment manufacturing); Electrical equipment; Instrument manufacturing; General and special equipment manufacturing (mechanical equipment manufacturing for short) |

| Forward | Backwards | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| VA_D (%) | VA_RT (%) | VA_GVC (%) | VA_GVC_S (%) | VA_GVC_C (%) | FGY_D (%) | FDY_RT (%) | FGY_GVC (%) | FGY_GVC_S (%) | FGY_GVC_C (%) | |

| AUS | −0.01 | −0.07 | −0.01 | 0.05 | −0.20 | −0.01 | −0.07 | −0.11 | −0.05 | −0.26 |

| NZL | 0.00 | −0.05 | −0.17 | −0.11 | −0.34 | 0.00 | −0.05 | −0.11 | −0.05 | −0.21 |

| CHN | −0.03 | −0.07 | −0.18 | −0.07 | −0.36 | −0.03 | −0.07 | −0.32 | −0.24 | −0.47 |

| CAN | 0.02 | −0.18 | −0.08 | 0.02 | −0.29 | 0.02 | −0.18 | −0.04 | 0.05 | −0.23 |

| JPN | −0.06 | −0.02 | −0.19 | −0.11 | −0.34 | −0.06 | −0.02 | −0.14 | −0.08 | −0.28 |

| KOR | −0.12 | 0.04 | −0.13 | −0.01 | −0.31 | −0.12 | 0.04 | −0.14 | −0.10 | −0.22 |

| IND | 0.08 | −0.35 | −0.30 | −0.24 | −0.44 | 0.08 | −0.35 | −0.10 | 0.02 | −0.45 |

| USA | 0.05 | −0.21 | −0.22 | −0.14 | −0.37 | 0.05 | −0.21 | −0.13 | −0.04 | −0.31 |

| DEU | −0.06 | −0.06 | −0.12 | −0.02 | −0.32 | −0.06 | −0.06 | −0.10 | −0.04 | −0.19 |

| GBR | −0.16 | −0.17 | −0.25 | −0.11 | −0.46 | −0.16 | −0.17 | −0.18 | −0.08 | −0.25 |

| FRA | −0.18 | −0.19 | −0.18 | −0.07 | −0.38 | −0.18 | −0.19 | −0.17 | −0.08 | −0.23 |

| BRA | 0.03 | −0.16 | −0.30 | −0.24 | −0.47 | 0.03 | −0.16 | −0.13 | −0.06 | −0.33 |

| RUS | 0.04 | −0.15 | −0.14 | −0.01 | −0.33 | 0.04 | −0.15 | −0.07 | 0.00 | −0.28 |

| ZAF | −0.09 | −0.04 | −0.47 | −0.36 | −0.67 | −0.09 | −0.04 | −0.20 | −0.14 | −0.34 |

| ROEP | 0.02 | −0.12 | −0.21 | −0.13 | −0.40 | 0.02 | −0.12 | −0.16 | −0.06 | −0.33 |

| TBTR | 0.03 | −0.09 | −0.20 | −0.11 | −0.38 | 0.03 | −0.09 | −0.19 | −0.10 | −0.37 |

| LAM | 0.10 | −0.26 | −0.30 | −0.23 | −0.46 | 0.10 | −0.26 | −0.15 | −0.06 | −0.37 |

| AssAN | 0.02 | −0.21 | −0.22 | −0.15 | −0.39 | 0.02 | −0.21 | −0.28 | −0.14 | −0.47 |

| AFR | 0.04 | −0.17 | 1.00 | −0.04 | −0.36 | 0.04 | −0.17 | 1.00 | −0.10 | −0.35 |

| ROW | −0.29 | 0.04 | 1.00 | 0.06 | −0.29 | −0.29 | 0.04 | 1.00 | −0.24 | −0.31 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, J.; Lee, H.; Yang, J. The Impact of the COVID-19 Pandemic on the Global Value Chain of the Manufacturing Industry. Sustainability 2021, 13, 12370. https://doi.org/10.3390/su132212370

Sun J, Lee H, Yang J. The Impact of the COVID-19 Pandemic on the Global Value Chain of the Manufacturing Industry. Sustainability. 2021; 13(22):12370. https://doi.org/10.3390/su132212370

Chicago/Turabian StyleSun, Jiaze, Huijuan Lee, and Jun Yang. 2021. "The Impact of the COVID-19 Pandemic on the Global Value Chain of the Manufacturing Industry" Sustainability 13, no. 22: 12370. https://doi.org/10.3390/su132212370