Hybrid Genetic Algorithm-Based Approach for Estimating Flood Losses on Structures of Buildings

Abstract

:1. Introduction

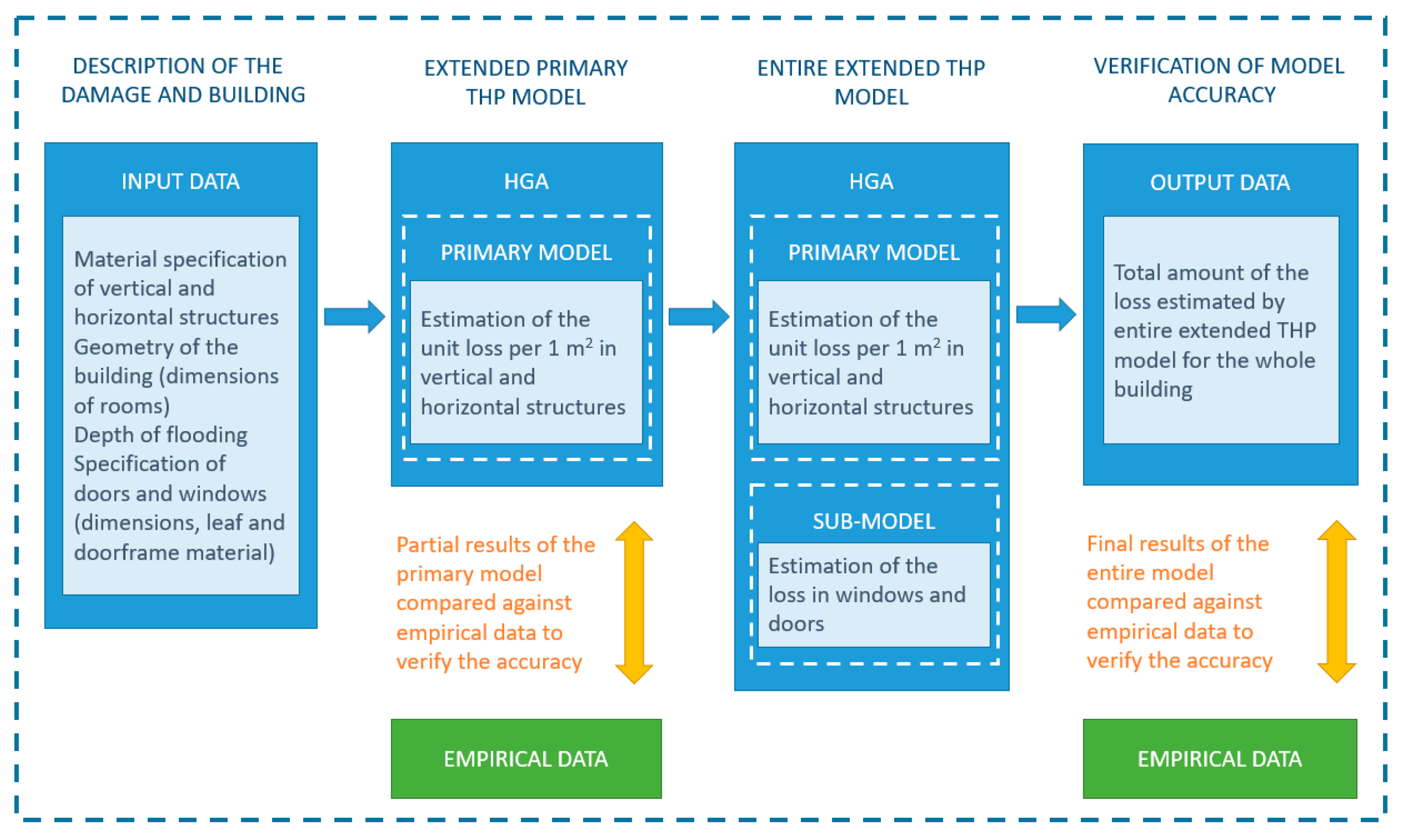

2. Data and Methods

2.1. Data

2.2. Methods

3. Results and Discussion

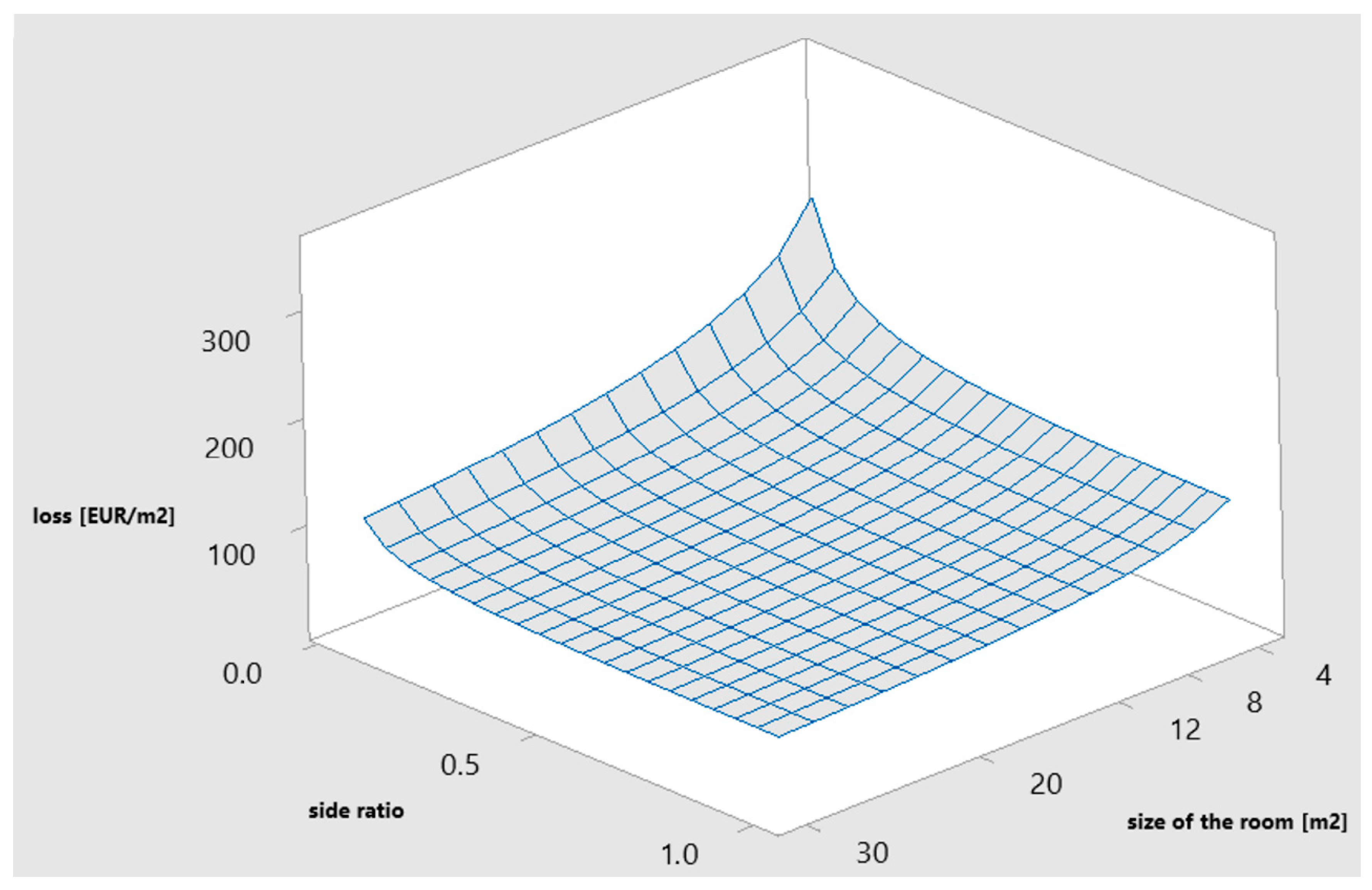

3.1. Verification of the Accuracy of the Primary Model Combining the Least Squares Method and the Genetic Algorithm

3.2. Verification of Accuracy of the Entire Hybrid Computational Model on a Case Study

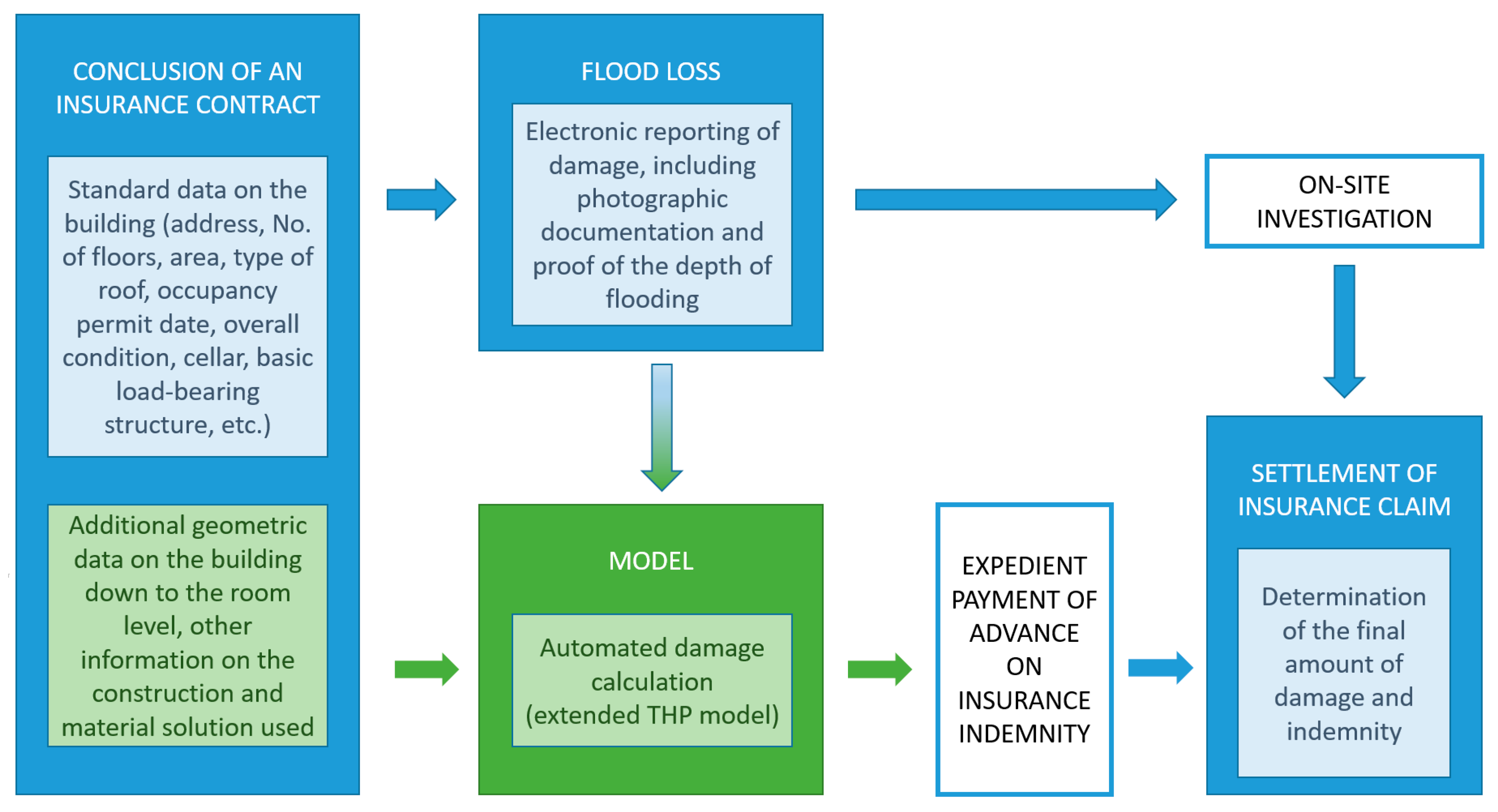

3.3. Potential Interconnection of the Model with Information Systems of Insurance Companies

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Kron, W.; Muller, O. Efficiency of flood protection measures: Selected examples. Water Policy 2019, 21, 449–467. [Google Scholar] [CrossRef]

- Zeleňáková, M.; Fijko, R.; Labant, S.; Weiss, E.; Markovič, G.; Weiss, R. Flood risk modelling of the Slatvinec stream in Kružlov village, Slovakia. J. Clean. Prod. 2019, 212, 109–118. [Google Scholar] [CrossRef]

- Paprotny, D.; Sebastian, A.; Morales-Nápoles, O.; Jonkman, S.N. Trends in flood losses in Europe over the past 150 years. Nat. Commun. 2018, 9. [Google Scholar] [CrossRef]

- Dutta, D.; Herath, S.; Musiake, K. A mathematical model for flood loss estimation. J. Hydrol. 2003, 277, 24–49. [Google Scholar] [CrossRef]

- Kousky, C. Financing flood losses: A discussion of the national flood insurance program. Risk Manag. Insur. Rev. 2018, 21, 11–32. [Google Scholar] [CrossRef]

- Jonkman, S.N. Global perspectives on loss of human life caused by floods. Nat. Hazards 2005, 34, 151–175. [Google Scholar] [CrossRef]

- Brázdil, R.; Rezníčková, L.; Valášek, H.; Havlíček, M.; Dobrovolný, P.; Soukalová, E.; Řehánek, T.; Skokanová, H. Fluctuations of floods of the river Morava (Czech Republic) in the 1691-2009 period: Interactions of natural and anthropogenic factors. Hydrolog. Sci. J. 2011, 56, 468–484. [Google Scholar] [CrossRef]

- Floods 1997. Official Website of Povodí Moravy. Available online: http://www.pmo.cz/cz/uzitecne/povoden-1997/ (accessed on 15 January 2020).

- Chlebek, A.; Jařabáč, M. Catastrophic flooding in the Czech Republic since 5 July 1997. IAHS-AISH Publ. 2002, 271, 19–24. [Google Scholar]

- Tapia-Silva, F.O.; Itzerott, S.; Foerster, S.; Kuhlmann, B.; Kreibich, H. Estimation of flood losses to agricultural crops using remote sensing. Phys. Chem. Earth 2011, 36, 253–265. [Google Scholar] [CrossRef]

- Špitalar, M.; Gourley, J.J.; Lutoff, C.; Kirstetter, P.; Brilly, M.; Carr, N. Analysis of flash flood parameters and human impacts in the US from 2006 to 2012. J. Hydrol. 2014, 519, 863–870. [Google Scholar] [CrossRef]

- Prettenthaler, F.; Amrusch, P.; Habsburg-Lothringen, C. Estimation of an absolute flood damage curve based on an Austrian case study under a dam breach scenario. Nat. Hazard Earth Syst. 2010, 10, 881–894. [Google Scholar] [CrossRef]

- Merz, B.; Kreibich, H.; Schwarze, R.; Thieken, A. Review article “Assessment of economic flood damage”. Nat. Hazard Earth Syst. 2010, 10, 1697–1724. [Google Scholar] [CrossRef]

- Mendoza, M.T.; Schwarze, R. Sequential Disaster Forensics: A case study on direct and socio-economic impacts. Sustainability 2019, 11, 5898. [Google Scholar] [CrossRef] [Green Version]

- Grahn, T.; Nzberg, R. Damage assessment of lake floods: Insured damage to private property during two lake floods in Sweden 2000/2001. Int. J. Disast. Risk Reduct. 2014, 10, 305–314. [Google Scholar] [CrossRef]

- Korytárová, J.; Hromádka, V. Assessment of the flood damages on the real estate property in the Czech Republic area. Agric. Econ. 2010, 56, 317–324. [Google Scholar] [CrossRef] [Green Version]

- Zeleňáková, M.; Gaňová, L. A multicriteria flood hazard assessment in the selected countries. In Proceedings of the International Scientific Conference People, Buildings and Environment 2012, Lednice, Czech Republic, 7–9 November 2012; Brno University of Technology, Faculty of Civil Engineering: Brno, Czech Republic, 2012; pp. 645–651. [Google Scholar]

- Deniz, D.; Arneson, E.E.; Liel, A.B.; Dashti, S.; Javernick-Will, A.N. Flood loss models for residential buildings, based on the 2013 Colorado floods. Nat. Hazards 2017, 85, 977–1003. [Google Scholar] [CrossRef]

- Velasco, M.; Cabello, A.; Russo, B. Flood damage assessment in urban areas. Application to the Raval district of Barcelona using synthetic depth damage curves. Urban Water J. 2016, 13, 426–440. [Google Scholar] [CrossRef]

- Notaro, V.; De Marchis, M.; Fontanazza, C.M.; La Loggia, G.; Puleo, V.; Freni, G. The effect of damage functions on urban flood damage appraisal. Procedia Eng. 2014, 70, 1251–1260. [Google Scholar] [CrossRef] [Green Version]

- Glavan, I.; Prelec, Z. The analysis of trigeneration energy systems and selection of the best option based on criteria of GHG emission, cost and efficiency. Eng. Rev. 2012, 32, 131–139. [Google Scholar]

- Thieken, A.H.; Ackermann, V.; Elmer, F.; Kreibich, H.; Kuhlmann, B.; Kunert, U.; Maiwald, H.; Merz, B.; Müller, M.; Piroth, K.; et al. Methods for the evaluation of direct and indirect flood losses. In Proceedings of the 4th International Symposium on Flood Defence: Managing Flood Risk, Reliability and Vulnerability, Toronto, ON, Canada, 6–8 May 2008; Institute for Catastrophic Loss Reduction: Toronto, ON, Canada, 2008. [Google Scholar]

- Su, M.D.; Kang, J.L.; Chang, L.F. Industrial and commercial depth-damage curve assessment. WSEAS Trans. Environ. Dev. 2009, 5, 199–208. [Google Scholar]

- Freni, G.; La Loggia, G.; Notaro, V. Uncertainty in urban flood damage assessment due to urban drainage modelling and depth-damage curve estimation. Water Sci. Technol 2010, 61, 2979–2993. [Google Scholar] [CrossRef] [PubMed]

- Jongman, B.; Kreibich, H.; Apel, H.; Barredo, J.I.; Bates, P.D.; Feyen, L.; Gericke, A.; Neal, J.; Aerts, J.C.J.H.; Ward, P.J. Comparative flood damage model assessment: Towards a European approach. Nat. Hazards Earth Syst. Sci. 2012, 12, 3733–3752. [Google Scholar] [CrossRef] [Green Version]

- Tezuka, S.; Takiguchi, H.; Kazama, S.; Sato, A.; Kawagoe, S.; Sarukkalige, R. Estimation of the effects of climate change on flood-triggered economic losses in Japan. Int. J. Disast. Risk Reduct. 2014, 9, 58–67. [Google Scholar] [CrossRef]

- Shan, X.; Wen, J.; Zhang, M.; Wang, L.; Ke, Q.; Li, W.; Du, S.; Shi, Y.; Chen, K.; Liao, B.; et al. Scenario-based extreme flood risk of residential buildings and household properties in Shanghai. Sustainability 2019, 11, 3202. [Google Scholar] [CrossRef] [Green Version]

- Wu, X.; Zhou, L.; Gao, G.; Guo, J.; Ji, Z. Urban flood depth-economic loss curves and their amendment based on resilience: Evidence from Lizhong town in Lixia river and Houbai town in Jurong river of China. Nat. Hazards 2016, 82, 1981–2000. [Google Scholar] [CrossRef]

- Garrote, J.; Alvarenga, F.M.; Díez-Herrero, A. Quantification of flash flood economic risk using ultra-detailed stage–damage functions and 2-D hydraulic models. J. Hydrol. 2016, 541, 611–625. [Google Scholar] [CrossRef]

- McGrath, H.; Abo El Ezz, A.; Nastev, M. Probabilistic depth–damage curves for assessment of flood-induced building losses. Nat. Hazards 2019, 97, 1–14. [Google Scholar] [CrossRef]

- Kheiri, F. A review on optimization methods applied in energy-efficient building geometry and envelope design. Renew. Sustain. Energy Rev. 2018, 92, 897–920. [Google Scholar] [CrossRef]

- Mora, T.D.; Righi, A.; Peron, F.; Romagnoni, P. Cost-optimal measures for renovation of existing school buildings towards nZEB. Energy Procedia 2017, 140, 288–302. [Google Scholar] [CrossRef]

- Belniak, S.; Leśniak, A.; Plebankiewicz, E.; Zima, K. The influence of the building shape on the costs of its construction. J. Financ. Manag. Prop. Constr. 2013, 18, 90–102. [Google Scholar] [CrossRef]

- Cunningham, T. Factors Affecting the Cost of Building Work—An Overview. 2013. Available online: http://arrow.dit.ie/cgi/viewcontent.cgi?article=1028&context=beschreoth (accessed on 5 December 2019).

- Tuscher, M.; Hanák, T. Evaluation of flood losses to buildings: Effect of room dimensions. Period. Polytech. Soc. Manag. Sci. 2016, 24, 60–64. [Google Scholar] [CrossRef] [Green Version]

- Tuscher, M.; Přibyl, O.; Hanák, T. Influence of material composition of structures on the accuracy of flood loss evaluation. IOP Conf. Ser. Earth Environ. Sci. 2019, 222, 012017. [Google Scholar] [CrossRef]

- Kalkulační a Rozpočtovací Program KROS, Cenová Úroveň 2019 (Calculation and Budgeting Software KROS, Price Database 2019) [computer software]. ÚRS Praha: Prague, Czech Republic. Available online: https://www.pro-rozpocty.cz/software-a-data/kros-4-ocenovani-a-rizeni-stavebni-vyroby/ (accessed on 5 February 2020).

- Ram Jethmalani, C.H.; Simon, S.P.; Sundareswaran, K.; Srinivasa Rao Nayak, P.; Padhy, N.P. Real coded genetic algorithm based transmission system loss estimation in dynamic economic dispatch problem. Alex. Eng. J. 2018, 57, 3535–3547. [Google Scholar] [CrossRef]

- Wang, Z.; Gu, C.; Zhang, Z. Evaluation method of loss-of-life caused by dam breach based on GIS and neural networks optimized by genetic algorithms. Wuhan Daxue Xuebao (Xinxi Kexue Ban)/Geomat. Inf. Sci. Wuhan Univ. 2010, 35, 64–68. [Google Scholar]

- Afshar, A.; Rasekh, A.; Afshar, M.H. Risk-based optimization of large flood-diversion systems using genetic algorithms. Eng. Optim. 2009, 41, 259–273. [Google Scholar] [CrossRef]

- Li, J.; Liao, B.; Huang, M. Structural damage identification via modal data based on genetic algorithm. Presented at the 2010 International Conference on Computational Intelligence and Software Engineering, Wuhan, China, 10–12 December 2010. [Google Scholar] [CrossRef]

- El-Mihoub, T.A.; Hopgood, A.A.; Nolle, L.; Battersby, A. Hybrid genetic algorithms: A review. Eng. Lett. 2006, 13, 2–11. [Google Scholar]

- Wan, W.; Birch, J.J. An Improved Hybrid Genetic Algorithm with a New Local Search Procedure. J. Appl. Math. 2013, 2013, 103591. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| RSG (Room Size Group) | Size of the Room [m2] | Initial Number of Model Rooms with Various SR | Adapted Number of Model Rooms with Various SR |

|---|---|---|---|

| RSG1 | 4 | 11 | 20 |

| RSG2 | 6 | 15 | 20 |

| RSG3 | 8 | 19 | 20 |

| RSG4 | 10 | 22 | 20 |

| RSG5 | 12 | 25 | 20 |

| RSG6 | 14 | 28 | 20 |

| RSG7 | 16 | 31 | 20 |

| RSG8 | 18 | 33 | 20 |

| RSG9 | 20 | 35 | 20 |

| RSG10 | 22 | 37 | 20 |

| RSG11 | 24 | 39 | 20 |

| RSG12 | 26 | 41 | 20 |

| RSG13 | 28 | 43 | 20 |

| RSG14 | 30 | 45 | 20 |

| TOTAL | - | 424 | 280 |

| PEPM [%] | Frequency of Occurrence for Individual Material Variants | |||||

|---|---|---|---|---|---|---|

| FV1-PV1 | FV1-PV2 | FV2-PV1 | FV2-PV2 | FV3-PV1 | FV3-PV2 | |

| 0.00–0.10 | 519 | 456 | 383 | 353 | 337 | 303 |

| 0.10–0.20 | 471 | 472 | 385 | 330 | 369 | 344 |

| 0.20–0.30 | 380 | 422 | 373 | 359 | 283 | 337 |

| 0.30–0.40 | 358 | 413 | 418 | 524 | 325 | 359 |

| 0.40–0.50 | 313 | 356 | 398 | 294 | 272 | 340 |

| 0.50–0.60 | 310 | 330 | 384 | 378 | 286 | 294 |

| 0.60–0.70 | 231 | 263 | 375 | 360 | 294 | 299 |

| 0.70–0.80 | 230 | 226 | 287 | 330 | 279 | 311 |

| 0.80–0.90 | 177 | 214 | 107 | 185 | 242 | 292 |

| 0.90–1.00 | 158 | 123 | 63 | 100 | 184 | 164 |

| 1.00–1.10 | 102 | 42 | 74 | 47 | 151 | 93 |

| 1.10–1.20 | 62 | 25 | 30 | 38 | 96 | 52 |

| 1.20–1.30 | 26 | 13 | 26 | 36 | 71 | 47 |

| 1.30–1.40 | 12 | 5 | 19 | 13 | 47 | 50 |

| 1.40–1.50 | 8 | 0 | 15 | 8 | 34 | 29 |

| 1.50–1.60 | 3 | 0 | 9 | 4 | 27 | 20 |

| 1.60–1.70 | 0 | 0 | 6 | 1 | 27 | 14 |

| 1.70–1.80 | 0 | 0 | 4 | 0 | 16 | 11 |

| 1.80–1.90 | 0 | 0 | 3 | 0 | 10 | 1 |

| 1.90–2.00 | 0 | 0 | 1 | 0 | 8 | 0 |

| 2.00–2.10 | 0 | 0 | 0 | 0 | 2 | 0 |

| Material Variant | PEPM Min [%] | PEPM Max [%] |

|---|---|---|

| FV1-PV1 | 0.0001 | 1.5393 |

| FV1-PV2 | 0.0000 | 1.3310 |

| FV2-PV1 | 0.0001 | 1.9500 |

| FV2-PV2 | 0.0003 | 1.6018 |

| FV3-PV1 | 0.0001 | 2.0316 |

| FV3-PV2 | 0.0003 | 1.8198 |

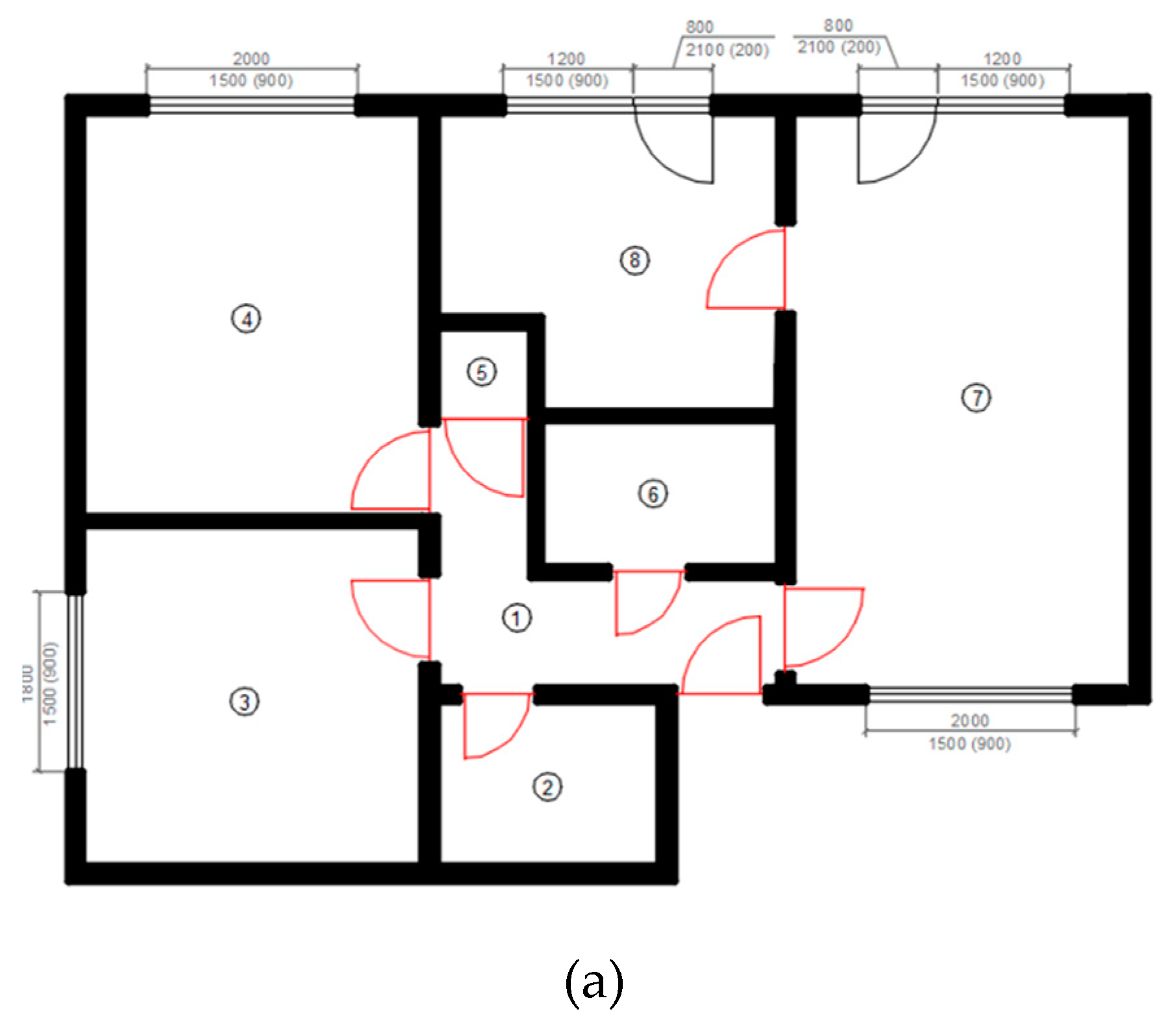

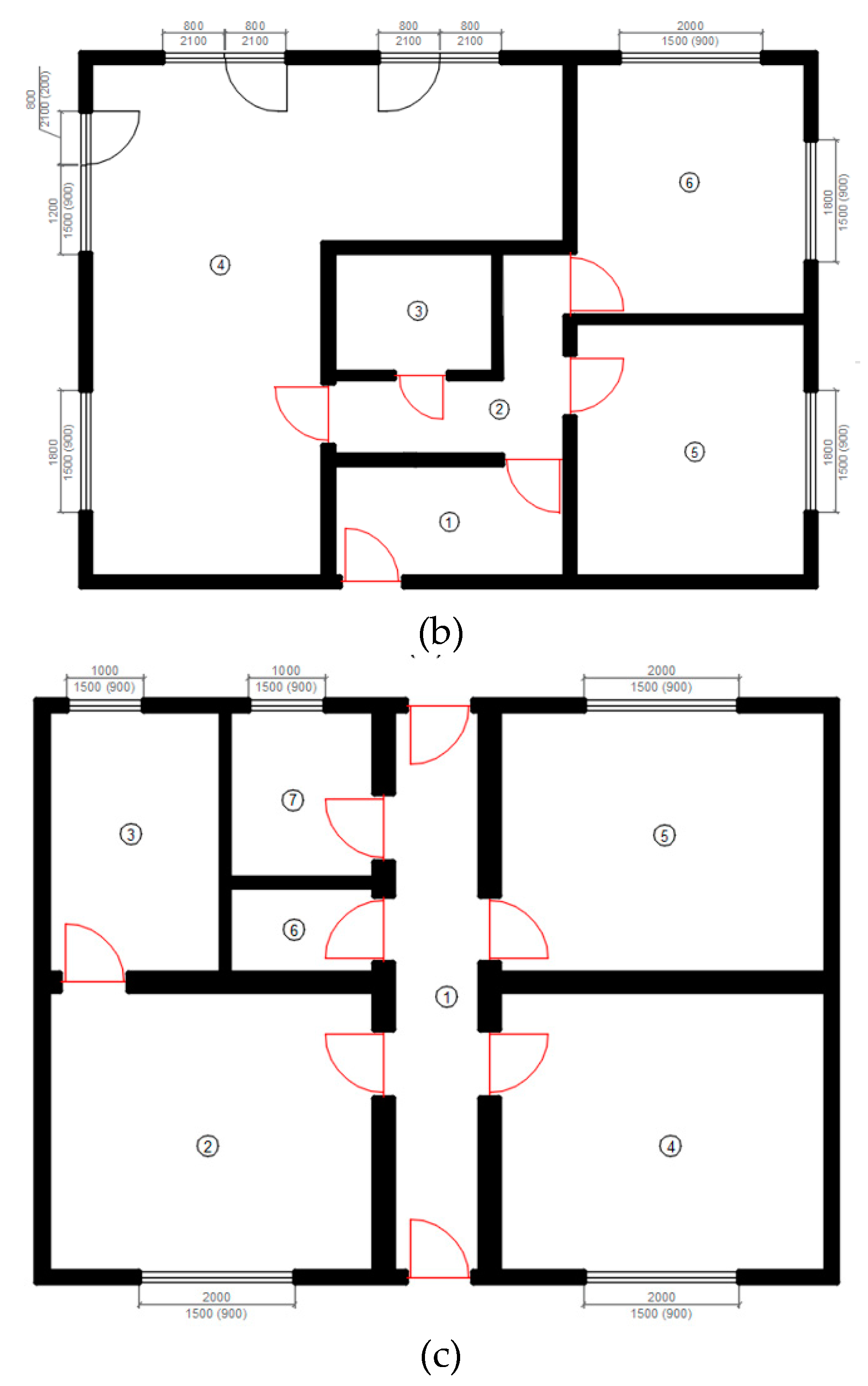

| Building Variant | Room No. | Length | Width | Horizontal Construction | Vertical Construction | Window | Door—Doorframe |

|---|---|---|---|---|---|---|---|

| A | 1 | 3.46 | 2.74 | FV2 | PV1 | - | adjustable |

| 2 | 2.25 | 1.67 | FV2 | PV1 | - | adjustable | |

| 3 | 3.48 | 3.45 | FV1 | PV1 | plastic | adjustable | |

| 4 | 4.12 | 3.45 | FV1 | PV1 | plastic | adjustable | |

| 5 | 0.95 | 0.94 | FV2 | PV1 | - | adjustable | |

| 6 | 2.40 | 1.49 | FV2 | PV1 | - | adjustable | |

| 7 | 5.87 | 3.47 | FV3 | PV1 | plastic | adjustable | |

| 8 | 3.46 | 3.04 | FV1 | PV1 | plastic | adjustable | |

| B | 1 | 3.45 | 1.67 | FV2 | PV2 | - | adjustable |

| 2 | 3.45 | 3.03 | FV1 | PV2 | - | adjustable | |

| 3 | 2.39 | 1.80 | FV2 | PV2 | - | adjustable | |

| 4 | 7.70 | 7.09 | FV1 | PV2 | wooden | adjustable | |

| 5 | 3.82 | 3.45 | FV3 | PV2 | wooden | adjustable | |

| 6 | 3.77 | 3.45 | FV3 | PV2 | wooden | adjustable | |

| C | 1 | 7.70 | 1.20 | FV1 | PV1 | - | steel |

| 2 | 4.49 | 3.85 | FV1 | PV1 | plastic | steel | |

| 3 | 3.60 | 2.39 | FV2 | PV1 | plastic | steel | |

| 4 | 4.49 | 3.85 | FV3 | PV1 | plastic | steel | |

| 5 | 4.49 | 3.60 | FV2 | PV1 | plastic | steel | |

| 6 | 2.00 | 1.20 | FV2 | PV1 | - | steel | |

| 7 | 2.30 | 2.00 | FV2 | PV1 | plastic | steel |

| Building A | Building B | Building C | |

|---|---|---|---|

| Extended THP model | 8341.43 | 8585.03 | 7486.34 |

| Bill of costs | 8249.71 | 8556.42 | 7408.99 |

| PEEM | 1.11% | 0.33% | 1.04% |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hanák, T.; Tuscher, M.; Přibyl, O. Hybrid Genetic Algorithm-Based Approach for Estimating Flood Losses on Structures of Buildings. Sustainability 2020, 12, 3047. https://doi.org/10.3390/su12073047

Hanák T, Tuscher M, Přibyl O. Hybrid Genetic Algorithm-Based Approach for Estimating Flood Losses on Structures of Buildings. Sustainability. 2020; 12(7):3047. https://doi.org/10.3390/su12073047

Chicago/Turabian StyleHanák, Tomáš, Martin Tuscher, and Oto Přibyl. 2020. "Hybrid Genetic Algorithm-Based Approach for Estimating Flood Losses on Structures of Buildings" Sustainability 12, no. 7: 3047. https://doi.org/10.3390/su12073047