2.1. Certified B Corps

B Corp certificates are issued by the independent non-profit organization B Lab, which was founded in the US in 2006. This organization’s goals are fourfold:

(a) building a community of Certified B Corporations; (b) promoting legislation creating a new corporate form that meets higher standards of purpose, accountability, and transparency; (c) accelerating the growth of “impact investing” through the use of B Lab’s impact investment rating system; and (d) galvanizing support for the movement by sharing the stories of Certified B Corporations.

B Corps are for-profit companies that integrate societal and environmental goals in their business model and strategies. In order to be eligible for B Corp certification, a firm must first conduct a B Impact Assessment (BIA), a self-test measuring the impact on workers, customers, society and the environment. More precisely, the BIA generates a B Impact Report covering the following aspects: Governance (Mission and Engagement; Ethics and Transparency), Workers (Financial Security, Health, Wellness and Safety, Career Development, Engagement and Satisfaction), Environment (Environmental Management, Air and Climate, Water, Land and Life) and finally Customers (Customer Stewardship) [

18].

If the minimum threshold BIA score of 80 on 200 is reached, B Lab conducts a rigorous audit procedure to verify this score. If this verification is successful, a company can achieve the B Corp certification by signing an agreement and paying a yearly fee to B Lab which is based on the annual sales level. Currently the fee ranges from

$1000 to

$50,000 [

19]. The agreement states that B Corps are legally required to consider their impact on all stakeholders. Such legal requirement can be met by amending the company’s governing documents or taking on the benefit corporation legal status [

20]. The certificate implies that companies adhere to rigorous transparency and accountability requirements and become part of a global network of corporations. Certification is valid for three years. At the end of this period a firm has to retake the BIA. In addition, B Lab conducts randomly chosen in-depth site reviews with 10% of its certified B Corps per year [

20].

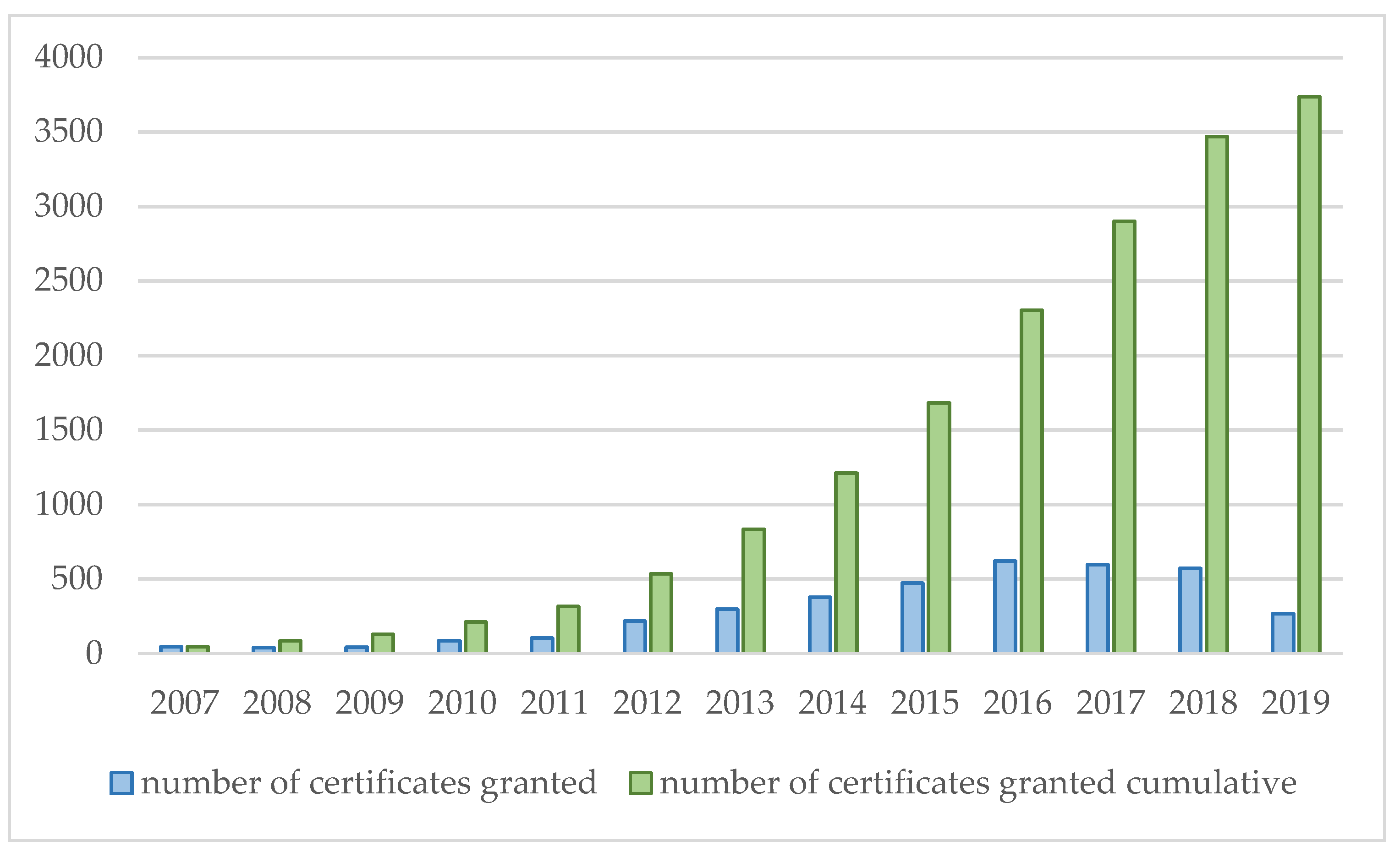

In the first year after the foundation of B Lab in the US in 2006, 82 certificates were granted. In the meantime, a geographical expansion occurred with regional B Labs currently operating in more than 50 countries and more than 3500 companies certified to date [

21].

Figure 1 provides an overview of the yearly number of certificates that were granted to new B Corps worldwide.

Table 1 and

Table 2 portray the geographical and sectoral distribution of the B Corps existing in 2019.

B Corps are distinct from Benefit Corporations, a company concept which refers to a specific legal structure that exists in several states in the US for companies with societal or environmental goals. A European counterpart of this legal structure is the Societa Benefit in Italy [

22]. Various B Corps have a legal structure which is adapted to their hybrid form and vice versa, however, these are not prerequisites for each other.

The BIA and B Corp certification are not the only impact measurement system and CSR related standard. Some well-known alternative impact measurement systems are the GRI and IRIS+. A common characteristic is the provision comparable information which supports benchmarking. There are however also some differences. While the GRI guidelines mainly focus on standardized reporting of non-financial information by companies [

23], the BIA focuses on the actual performance of companies and provides a B Impact Report with scores in several domains. Also, while the IRIS+ system is mainly aimed at investors [

24], the BIA targets all stakeholders. With regard to CSR related standards, alternatives to B Corp certification are for example ISO 14001:2015, ISO 26000:2020, SA 8000:2014. Like SA 8000, B Corp certification is a proprietary scheme developed by a group of independent experts in business and academia, i.e., the Standards Advisory Council (SAC) [

25,

26]. In contrast to ISO 26000 [

27], B Corp requirements are certifiable, meaning that the implementation of a standard’s requirements can be audited and certified by an independent external entity (i.e., the certification body) [

28]. Besides, the BIA covers the three sustainable development dimensions (economic, social and environmental), while ISO 14001 and SA 8000 mainly focus on environmental and social aspects, respectively [

26,

29].

2.2. Literature Review and Hypothesis Development

The pursuit of a mix of financial and social goals is not exclusively the domain of hybrid firm as also more traditional companies may envisage social outcomes. Numerous studies have explored the financial consequences of CSR activities of traditional companies [

30,

31,

32]. Margolis and Walsh [

30] reviewed 127 empirical studies, almost half of which documented a positive association between social and financial performance. Only seven studies found a negative relationship. A meta-analysis of Orlitzky et al. [

31], came to the same conclusion. While the two previous papers considered empirical studies on large listed companies, Fonseca and Ferro [

32], surveyed Portuguese SMEs and reached similar conclusions.

While the empirical evidence for traditional enterprises seems to suggest a positive relation between social and financial performance (it pays to be good), hybrid companies are often believed to suffer from tensions because of their duality of financial and social purposes [

7]. Hybrid companies are considered as “sites of contradiction, contestation and conflict” [

33] (p. 425). The literature typically assumes that social and economic objectives exist at either end of a continuum with hybrid companies operating somewhere in the middle. Hybrid enterprises risk drifting away from their social mission when financial objectives are in danger [

34]. A potential solution to this tension and danger of mission drift is the conception of the social mission as a strategic advantage. This would mean that the social mission is not considered in a trade-off with the financial performance but rather is used as an impetus to improve the competitive position, to hire, motivate and retain employees, to assure finance and develop strategic alliances with other organizations [

34,

35]. Chauhan and O’Neill [

3] argue that external verification of the social mission could be instrumental in turning the social mission into a strategic advantage. In their survey of B Corps, they find that the reported motives to obtain certification are manifold ranging from cognitive changes and increased awareness among the founders and managers, over increased promotional opportunities vis-à-vis clients and suppliers, clearer communication of corporate identity and strategy to stakeholders, improved perception and motivation of employees to more clear and credible profiling to investors and creditors.

Various academics have explored the characteristics of companies that pursue B Corp certification and their motivation to do so [

17,

36,

37,

38,

39,

40]. As concerns the motivation to pursue certification, Gehman, Grimes and Cao [

41] and Stubbs [

2] consider the B Corp model as a tool for change, which provides collective identity for internal and external validation by serving as a visual classification for the type of company that they are. This stamp lends credibility towards stakeholders and provides the opportunity to network with like-minded businesses [

2]. This form of certification would positively affect accountability and corporate governance [

42] and the BIA tool is used to integrate sustainability into the day-to-day decision-making [

43]. Harjoto et al. [

37] conclude that B Corp certification is a way of companies to respond to high competition. Alonso-Martínez, De Marchi and Di Maria [

44] investigate which formal and informal institutions affect the BIA scores of European B Corps. Their results show that market pressure from demanding and conscious consumers as well as high technological and innovation capacities, are positively associated with BIA scores, while regulatory pressure has an adverse effect. The latter indicates that institutional voids offer the opportunity to surpass local standards as a differentiation strategy. As concerns the characteristics of the companies that pursue B Corp certification, Harjoto et al. [

37] and Grimes et al. [

36] find that woman-owned businesses are not only more likely to qualify for certification given their high scores on the BIA, but are also more likely to actually pursue certification. Furthermore, a large share of both American and European certified B Corps is active in the services and manufacturing industry [

17,

39,

40]. While companies in the services industry generally excel in terms of progressive business models, those in the manufacturing industry appear to focus rather on process innovations. Regional differences also have been examined. López-Navarro et al. [

40] conclude that B Corps are geographically clustered within each country around the country partner, being the B Corp that bears the responsibility of promoting the B Corp movement. Hickman et al. [

38] and Harjoto et al. [

37] find that US states with highly educated people, which exhibit liberal or progressive attitudes, show a higher number of B Corps per capita.

Besides studies on the motivation for and characteristics of companies that pursue certification, some studies examine the effect of geographical and sectoral contexts on the promotion and communication strategies regarding B Corp membership [

8,

17]. Cao et al. [

12] stipulate different promotion strategies for B Corps, given the prevalence of B Corp peers within the same geographical area or industry. Such strategies might help companies to stand out or fit in, by showing the distinctiveness or legitimacy of their practices, respectively. Building on the idea that category promotion helps companies stand out while category membership helps companies to fit in, Gehman and Grimes [

8] empirically assess the effect of regional and industrial contextual distinctiveness on the promotion of B Corp membership on companies’ websites. Their findings suggest that in situations where B Corps can clearly distinguish themselves from competitors or geographically proximate companies by being part of a sustainable community, they tend to promote their B Corp membership more strongly. Besides, the number of peers (other B Corps) present in the same state or industry amplifies these effects.

For hybrid companies, financial health is no less important to guarantee firm survival and success than for other companies. Consequently, some studies have investigated the financial characteristics of B Corps, such as growth rates and access to finance. To date, the majority of these studies focus on North American companies [

10,

16] and the evidence is mixed.

By becoming a B Corp, a company can gain media exposure on its responsible business practices and become part of a global network [

5]. Given that the certification process is time and cost intensive, certification lends credence to a company’s commitment to sustainability practices [

45]. According to Stubbs [

46], B Corp certification can help to integrate social and economic opportunities in the marketing strategy. This type of certification could enhance consumers’ motivation to purchase from socially responsible companies [

4]. This way, B Corp certification could positively affect turnover. Chen and Kelly [

15] compared the financial performance of B Corps and their publicly listed and small private competitors. Their findings show that B Corps outperform their public competitors with regard to revenue growth rates. No significant differences with small private firms were found. Romi et al. [

16] conduct a similar analysis, however, using more extensive matching criteria and report that B Corps experience higher sales growth than their non-B peers. These findings imply that these hybrid organizations have a strategic advantage in generating sales. An analysis within the sample of B Corps indicated that excellent employee and consumer scores on the BIA are associated with higher employee productivity and sales growth, respectively. Hence, additional investments in these domains are financially rewarding. These empirical findings corroborate on what would be expected from the Stakeholder Theory [

47] and the Resource-Based Theory [

48]. The former theory states that business success depends on collaboration with multiple stakeholders, hence, hybrid companies that better manage a broad set of stakeholders could benefit superior firm performance [

49]. The latter theory states that firms’ competitive advantages depend on internal and external tangible, intangible and personnel-based resources. By engaging in proactive CSR, companies can generate new competitive resources [

50]. Parker et al. [

10] on the other hand document that B Corps experience a negative effect on the revenue growth rate in the year post certification. They argue that positive effects are potentially only noticeable in the longer term, given that the process of signaling B Corp membership to external stakeholders takes some time. Internal disruptions owing to the certification process, however, could have an immediate negative influence on turnover. More specifically, the rigorous third-party audit and certification might shift managerial attention away from the normal course of business, causing management to spend less time on generating sales.

Furthermore, for other growth measures than sales, potential effects of B Corp certification are conceivable. For instance, B Corp certification might change the position of a hybrid company on the job market, affecting employee growth rates. This change in employee growth can be supply or demand-driven. As concerns the supply side, B Lab certification demonstrates a company’s commitment to create a healthy and engaging working environment [

51]. Besides, certification shows a sense of purpose of companies which can be used in recruitment practices [

46], especially appealing in job markets where purposeful jobs are more aspired. According to the social identity theory, job seekers compare and classify potential employers, and attempt to imagine working at companies they identify with [

52]. By comparing B Corps with traditional firms, potential candidates might identify more strongly with the former. Furthermore, B Lab launched a job platform dedicated to vacancies of B Corps [

53]. Hence, it might be easier this way for B Corps to find talented employees [

5]. From the demand side, companies might experience a need for additional workforce to comply with B Corp standards and make improvements on the BIA [

46] without losing sight of the regular course of business [

10].

Finally, B Corp certification might help a company scale up, by facilitating access to finance [

54]. The majority of B Corps are small businesses, and the asset growth of these small firms is often constrained by internal financing mechanisms. Firms that make use of external finance have asset growth rates which are much higher than what could be supported by solely internal finance [

55,

56]. Choi and Gray [

57] argue that socially responsible companies are especially selective about their financing sources, since traditional investors could impede the ability to reach non-financial goals. Likewise, Siqueira, Guenster Vanacker, and Crucke [

58] conclude that Belgian so-called Social Purpose Companies, companies with a legal structure for for-profit social enterprises, display lower leverage ratios than commercial companies. B Corp certification could mitigate information asymmetry and agency costs, reducing capital constraints [

59] and attract socially responsible investors [

17], which could allow companies to scale up.

In sum, our analysis of the financial consequences of B Corp certification indicates that B Corp certification might have consequences for (short-term) firm growth of sales, employees and assets. However, whether the effect will be positive or negative remains an empirical question. We therefore posit the following hypothesis:

Hypothesis (H1). Ceteris paribus, B Corp Certification has an effect on the short-term growth rate of firms.

{kind=link}