1. Introduction

In the next two to four decades, CO

2 emissions from the use of fossil fuels needs to be eliminated and the large amount of CO

2 that is already in the atmosphere needs to be removed, to prevent the Earth’s temperature from rising above 2 °C. The industrial sector accounts for over a third of the global CO

2 emissions, and was responsible for nearly two-thirds of their increase in 2018 reaching an all-time peak [

1]. Energy-intensive industries (EIIs) are the most polluting sub-sectors, accounting for 64% of the total industry emissions [

2] and 30% of the global GHG emissions [

3]. Efforts aimed at curbing industrial CO

2 emissions can have broad positive and negative impacts. Among the most accepted policies to enhance the industrial transition and curb CO

2 emissions is carbon pricing, a policy instrument aimed at internalising the costs of emitting CO

2 under the polluter pays principle [

4,

5,

6,

7,

8]. The economic literature suggests that if the externalities of CO

2 emissions are included in the cost structure within firms, they will see them as a resource for production, creating an incentive to reduce their use. The theory of induced innovation builds on Hicks’ notions [

9]. He noted that when one production factor increases its costs, firms have an incentive to innovate by finding new ways of making a more efficient use of that resource or replacing it by a new production input.

In the context of industrial transition and carbon pricing, CO

2 emissions represent the resource that increases its price, creating an incentive for firms to make less intensive use of this resource or innovate new technology that will replace it [

10,

11]. However, the hypothesis of carbon leakage suggests that the opposite could happen, and firms facing a higher CO

2 price would relocate operations to less-regulated regions where production costs are lower and investments lower [

12,

13,

14,

15]. As most countries’ economies are highly sensitive to industrial activity, the threat of carbon leakage and its effects on the economy and the environment has kept many legislations hostage of the business as usual regular way of working, and there have not been significant increases in the price of CO

2 nor reductions in the emission levels [

15,

16].

This study assessed the applicability of both the carbon leakage hypothesis and the theory of induced innovation in the context of a carbon tax on industrial GHG emissions proposed in the Dutch National Climate Agreement. The case study used in this research was the industrial cluster based at the Port of Rotterdam (PoR), and the research aimed to assess the effects that such a tax has in its competitiveness, by analysing both the risks of carbon leakage and the opportunities for the implementation of low-carbon technology. Furthermore, this research unveils and explains the relationships between these concepts in the context of the case study. The industrial cluster of the PoR constitutes an interesting case to test the applicability of these theories and perform this study. Over 20% of the CO

2 emissions of The Netherlands are produced in Rotterdam, particularly from the port area. The port’s industrial cluster is comprised of, to a great extent, companies operating in the energy and CO

2-intensive sectors. With more than 45 petrochemical companies and five oil refineries, the PoR is one of the world’s largest oil and chemical centres [

17]. The PoR is a vital and strategic actor in the economy of the city and the country. Considering direct and indirect employment, it currently employs over 384,500 people and provides a total added value of 45.6 billion euros to the Dutch economy. These figures represent 4.2% of the total Dutch employment and 6.5% of the GDP of The Netherlands, respectively [

17]. Many aspects inherent to the PoR and the context in which it is comprised facilitate the implementation of low-carbon technology. The economies of the scale associated with an industrial cluster, and the infrastructure and logistics services that have developed around it, have facilitated operational aspects that make it possible to implement low-carbon technology. The existence of knowledge hubs specialising in low-carbon technology, and close connections with academia and think tanks, create favourable conditions for innovative developments, testing and managing of low-carbon technology.

3. Methodology

This study assessed the effects that a carbon tax would produce in the competitiveness of the industrial cluster of the Port of Rotterdam. According to the theory presented in the previous section, by increasing the cost of emissions, a carbon tax has the potential to induce both carbon leakage and technological innovation. An increase in the production costs would reduce the competitiveness of the businesses operating in the PoR and in turn may provide an incentive for carbon leakage. Pricing CO2 emissions may also induce technological innovations, both in developing new technologies or implementing existing ones, in doing so, businesses would gain competitiveness in an ever-closer low-carbon economy.

This study performed qualitative analysis on a large body of data, which was collected through 13 in depth semi-structured interviews with stakeholders from various organisations, which included academia, banking, industrial, consulting and the public sectors. Representatives from the following organisations were interviewed: ABN Amro bank, Royal Haskoning DHV, TNO, Deltalinqs, VPNI Oil, VNCI Chemical, BP Netherlands, Municipality of Rotterdam, Port of Rotterdam Authority and the Erasmus University Centre for Urban, Port and Transport Economics. The list of interviewees can be found in

Appendix A. The selection of semi-structured interviewees was devised from both previous knowledge of the sector by the researchers on the phenomenon being investigated, and the need to acquire new insights into the variables and sub-variables, in order to investigate potential unknown relationships between them. The interviews guidelines are presented in

Appendix B. Primary data was triangulated with secondary data to improve the reliability and validity of the study. Secondary data was collected from different sources covering the subject matter, including official policy documents from the government, studies commissioned by the government that were carried out by specialised consulting firms, facts and figures from the Port of Rotterdam Authority and academic research that partly overlapped with the scope of this study. Official policy documents were obtained from the website of the government departments, and information of the PoR from their publicly available documents.

Given the complexity of the phenomena being studied in this research, the selection of the interviewee sample aimed at including experts from a broad selection of different sectors. This allowed the researcher to gather many different perspectives about the impacts of a carbon tax using the variables and sub-variables that were developed to assess both the carbon leakage hypothesis and the theory of induced innovation. The analysis of the collected qualitative data was performed with the software Atlas TI, which allowed for the creation of codes and categories and it made connections between them. Co-occurrence tables and the query tool were used to show correlations between the various codes. The operationalisation table with concepts, variables, sub-variables and indicators used to analyse the data gathered is shown in

Appendix C.

4. Results

4.1. Carbon Leakage as Relocation of Operations and Investment Leakage

The industries operating in the industrial cluster of the PoR are characterised by the production of low-value commodities with no product differentiation, and their trading is based in large volumes with low margins. This means that the demand for these products is highly sensitive to changes in prices, which leaves little room for firms to pass-through increases in production costs. Therefore, a carbon tax represents an incentive for them to relocate to regions with lower production costs. However, the enormous sunk costs of the firms in the Port of Rotterdam, the long-term commitments with suppliers and customers and the agglomeration externalities mediate this effect, reducing the risk of carbon leakage as the relocation of operations, as seen in

Figure 1.

Furthermore, the infrastructure and logistic services that have developed around the port also act as strong barriers of exit, as they add value and efficiency to the industrial operations, which are unlikely to be found in a different location. The advantages of the Port of Rotterdam are the reasons why companies have clustered in this location, and they will not change with a higher price of carbon. There is a highly specialised labour force, it is situated in a strategic geographical location, and it has a proximity to an intricate and strong network of suppliers and customers, and efficient logistic services. The pipeline networks that have been built around the PoR are perhaps the most important feature preventing companies from relocating, as they are known to substantially increase operational efficiency. In the absence of pipelines, the alternatives that are available for companies to connect with suppliers and customers would be to ship enormous volumes of inputs and outputs, which would increase the costs significantly. These features make the real cost of doing business in Rotterdam difficult to assess as the various businesses benefit from a range of positive agglomeration externalities, and the cost disadvantage posed by a carbon tax would have to be extremely high in order to outweigh all the benefits of the location. This perspective was shared by all interviewees, as illustrated for example by the following quote: “If you would relocate, you would need 10–20 years to earn back your investment, at least. What you always have to imagine is, if we were to increase your carbon taxation here, does the extra penalty that you pay here, where you have all these skilled workers, supply chain, big volume, does it weigh up against the alternative, for which you basically need 20 years of advantage?”

There are also arguments from a regional economic perspective against the relocation hypothesis. The investments and efforts to start operating in a different location are monumental, and many businesses would probably decide not to take such a large risk, to relocate to other European countries. The trend in Europe is to make climate policy more stringent, increasing the price of CO2 emissions within a short time period, which would leave the relocating firm with an equally high CO2 price and without the benefits of being in the Port of Rotterdam. Thus, the decision to cease European production altogether makes more sense under this perspective than relocating within Europe. The demand for fossil-based products is decreasing in Europe, which would support the decision of exiting the European market, but there are at least two reasons against this argument.

First, even in the most optimistic decarbonisation scenarios, European economies will remain reliant on fossil fuels and fossil-based chemicals for at least another three decades, which ensures a market for that period.

Second, decarbonisation efforts are leading to the development of new sources of energy and feedstock, which will surpass fossil fuels and fossil-based products as soon as the technologies are able to be scaled up. The businesses in the industrial cluster in the PoR are in an extremely advantageous position to become frontrunners in the production of clean energy and products. With a long-term perspective, it would make more sense for the firms to invest in adapting their production processes to clean energy sources and implementing low-carbon technology, instead of investing in traditional oil refineries or petrochemical facilities elsewhere.

The introduction of a carbon tax in The Netherlands would distort the level playing field for the firms operating in the PoR, as their production costs will be higher only for the facilities in this location. This distortion would affect the sub-variable of regulatory and legal framework, reducing the attractiveness of the PoR as a location for investment, as seen in

Figure 2. The following quote by an interviewee from the Port of Rotterdam Authority explains the rationale behind businesses investment decisions: “What companies look at is the level playing field. Is my business case, is my production here better off than anywhere else? Do we have a disadvantage in the Netherlands compared to Belgium, or to Germany, or to wherever else in Europe?” The companies operating in the Port of Rotterdam are multinationals with facilities and operations in different regions of the world. Hence, there is a high risk of investment leakage, as firms will most likely divert investment to more profitable facilities where production costs are lower, allowing them to get a faster return on investment. Regardless of the extent to which firms are affected, many of them already have low operational returns and profits. Facing a cost increase, firms might use the facilities in the PoR as swing facilities in the short-mid-term, operating them at a lower capacity and reducing their production levels. In this scenario, companies will sweat their assets and keep operating the facilities as they are, trying to make the most profit of their remaining operating life, while increasing the investment and production capacity of facilities in other regions. Facilities in the PoR will continue ageing with no significant new investment, and keep losing their value until companies potentially decide to cease operations or recoup their remaining value by, for example, selling them to investment funds. It is important to emphasise that companies might be subject to clean up bills if they decide to exit, and these act as important barriers to the cease of operations. At the same time, the scenario in which the companies sell the assets to investment funds is hypothetical as there are more aspects that investment funds consider when planning their investment decisions. Faced with a higher price of carbon, multinationals are likely to decrease the level of investment in the facilities in the PoR and increase their investment in less regulated geographical areas where returns on investments are higher. According to an interviewee from the Port of Rotterdam Authority working with the chemical industry sector, this is already happening in Europe: “At the moment Europe is lagging on production capacity, you do not see much new investment. This also means that the facilities are becoming older, and then you get the challenge that although Europe is known for its energy efficiency in the industry, but with older facilities you do not get any more efficiency gains. If you make yourself so expensive then you cannot attract new energy efficient facilities anymore, which would help you in the transition”.

The analysis shows that the risk of relocation of operations is not as big as the investment leakage. A recent example of the sensitivity of investment decisions was the INEOS’ investment case. INEOS is a UK owned multinational chemical firm that decided to make an investment of approximately 3 billion Euros in the industrial cluster of the Port of Antwerp, instead of in the PoR. After a long bidding battle between both ports, the final decision started a discussion about whether it was influenced by the environmental stringency of The Netherlands, and the case was used as an example of investment leakage. However, the CEO of the company stated publicly that the composition of the cluster in the Port of Antwerp is more favourable for the needs of the company, which ultimately motivated the decision. Additionally, INEOS already had operations in Belgium and long-standing relations with the Port of Antwerp. The company employs 2500 people in their nine manufacturing sites in Belgium, of which six are located in Antwerp (Ineos, n.d.). This example illustrates that firms analyse a myriad of variables for their investment decisions, with environmental stringency being just one of them. However, if regulations create an environment that is perceived as unfavourable for a firm’s production and business, the likelihood that they decide to locate to a different region is high. The distortions in the level playing field were acknowledged by all the interviewees.

4.2. The Theory of Induced Innovation

In the face of a higher price of CO2 emissions, paying for CO2 abatement might become a more profitable option for companies than paying for the tax, depending on the availability and costs of CO2 abatement technology. The data gathered and analysed in this study showed that, in the case of industries operating in the PoR, there are no readily available technologies that could substantially abate CO2 emissions, besides carbon capture, usage and storage (CCUS), which is currently being developed by the Porthos project organisation. In the short term, this is the only relatively realistic option to abate emissions for the oil refining and petrochemical industries. Nevertheless, although CCUS technology has been proven and applied, it has never been implemented in an interconnected and large-scale industrial cluster like the one in the PoR, which makes it a pioneer and very challenging work. This is a reflection of one of the main barriers to the implementation of low-carbon technology in industrial processes and energy production.

Although many of the technologies have been around for years, they have not yet been tested in large-scale industrial complexes. Furthermore, there are many operational challenges associated with their implementation that have not been solved. Among the most promising low-carbon technologies to curb emissions in industrial processes and energy production are green hydrogen and electrification. Both are real options which will help to abate emissions, but they will only work if the electricity grid is fully switched to renewables, in order to ensure net-zero emissions in the whole production chain. Oil refineries need extremely high temperatures during their processes, which are not currently achievable by only using electricity. Green hydrogen may be a solution, but the conditions have not yet been created to implement green hydrogen on a large scale. The enormous amount of renewable electricity needed for its production through electrolysis remains a challenge as there is currently no such production capacity in The Netherlands. Offshore wind is among the most developed renewable sources of electricity in The Netherlands, but the various technical aspects regarding bringing the electricity to the industrial sites, and how to store it on a large scale are still issues that have not totally been solved. Additionally, there is the need for a legal framework and infrastructure, namely a hydrogen backbone, which needs to be set up in order to ensure the safe production and transportation of hydrogen.

The fact that the current costs of abatement options are too high, preventing the technologies to be scaled up and be made available for mass production, is largely due to a lack of market for new technologies like green hydrogen and cleaner products. Most of the barriers mentioned above can be overcome if there is a market for them, which would trigger investments in the development of solutions for the barriers mentioned. Regulation is perhaps the only mechanism that is able to create a market for low-carbon products and technologies, as firms will not make investments that are not profitable within their investment cycles and will not produce goods for which there is no demand. Analysis has shown that the lack of a market is keeping firms from making favourable business cases, in order to implement low-carbon technology, which in turn is the main force stopping technologies to be scaled up.

4.3. Tackling Investment Leakage and Enhancing Low-Carbon Innovation

Government support policies and regulations can buffer the effects of a carbon tax by mediating the distortion that it induces on the level playing field. For instance, the free allocation of emission permitted to companies with high risks of carbon leakage in the case of the EU ETS, or the introduction of a Carbon Tax Border Adjustment in the case of a carbon tax, would reduce the distortion in the level playing field and consequently prevent the loss of competitiveness and investment leakage to take place. The composition of the policy mix in which the carbon tax is included is of great importance as besides penalising emitters, it is able to provide incentives for the industry to invest in CO

2 abatement. Such incentives can be in the form of direct subsidies, tax rebates or exemptions for companies with undergoing investments in abatement technology. One of the mechanisms by which green investment is enhanced is shown in detail in

Figure 3.

According to the data gathered, a carbon tax will provide the certainty of the future carbon price required by businesses to plan their investment decisions. The extent to which this enhances the perception of The Netherlands, and consequently the PoR, as a place with stable and clear regulations is mediated by the regulations included in the policy mix. This was clearly pointed out by an interview from the Port of Rotterdam Authority working on strategic environmental management: “If the instrument is clear, there are pathways, subsidies, a mix of instruments, which is focusing on building up and implementing new technologies, then the companies feel secure and they will invest. That is what we need as PoR. We need an interesting investment climate in The Netherlands and in Rotterdam. The mix of instruments should work for building up new technologies and reducing CO

2 emissions”. Without regulations protecting the industry from international competition, other businesses will not perceive The Netherlands as stable country for investment. However, in the presence of clear penalisations and protection measures, the sub-variable stability of a regulatory environment will be enhanced. The extent to which it translates into an increase in its attractiveness as a location for investment is mediated by the support policies implemented with the carbon tax. If the support policies are aimed at scaling up the existing low-carbon technologies are also implemented, their combination with a stable regulatory environment will trigger green investment, which in turn will increase the competitiveness of the PoR by becoming a frontrunner in low-carbon production. This makes government support a vital element to create an attractive place for investment. Without it, a carbon tax could only be seen as a barrier for industrial activity and an incentive for investment leakage. According to the data gathered, although the most direct mechanism for government support is making public funding available through subsidies, it can also enable conditions for green investment by, for example, making sure that the infrastructure required as a pre-condition for the implementation of low-carbon technology is in place. For instance, building a hydrogen backbone, infrastructure for CCUS, or building a large-scale deployment of offshore wind would give clear signals and certainty to companies that the government is aligned and committed with the industrial transition.

Figure 4 shows the detailed mechanisms by which regulation can enhance the competitiveness of firms and prevent carbon leakage.

When there is a market, firms will create business cases to satisfy the demand by innovating with new products or implementing new technology in their production processes. Product differentiation and the implementation of low-carbon technology in production processes will increase the competitiveness of the industries in the future low-carbon economy. Given the relatively small scale of the Dutch industry, the regulations should be implemented at a European level. An example of these sort of regulations can be found in the EU regulations for biofuels, which created a demand for a new product that would have not been created by the market on its own. As a result, companies have adapted part of their production processes to comply with the regulations and in order to satisfy the demand. Similarly, regulations are required to create a market for both cleaner products and energy resources, such as green hydrogen. For example, there is 1.3 Mt per year of grey hydrogen being produced currently in The Netherlands. If a regulation forced at least 10% of the hydrogen produced to be green, businesses would follow suit and satisfy the demand. The production of new products, or innovations in production processes of existing products, would enhance the competitiveness of the firms in the ever-closer low-carbon economy. The extent to which businesses are able to implement new production methods is to a great extent mediated by whether the conditions for their implementation are in place. For example, production method alterations, such as green hydrogen or the electrification of the production processes, require either that the electricity grid is completely switched to renewables or dedicated offshore wind electricity production, which is able to ensure zero emissions in the whole chain. If these conditions are not in place, the implementation of the new technology as a consequence of newly created demands will not take place. Additionally, product differentiation allows for businesses to pass-through the increased production costs which would in turn act against carbon leakage.

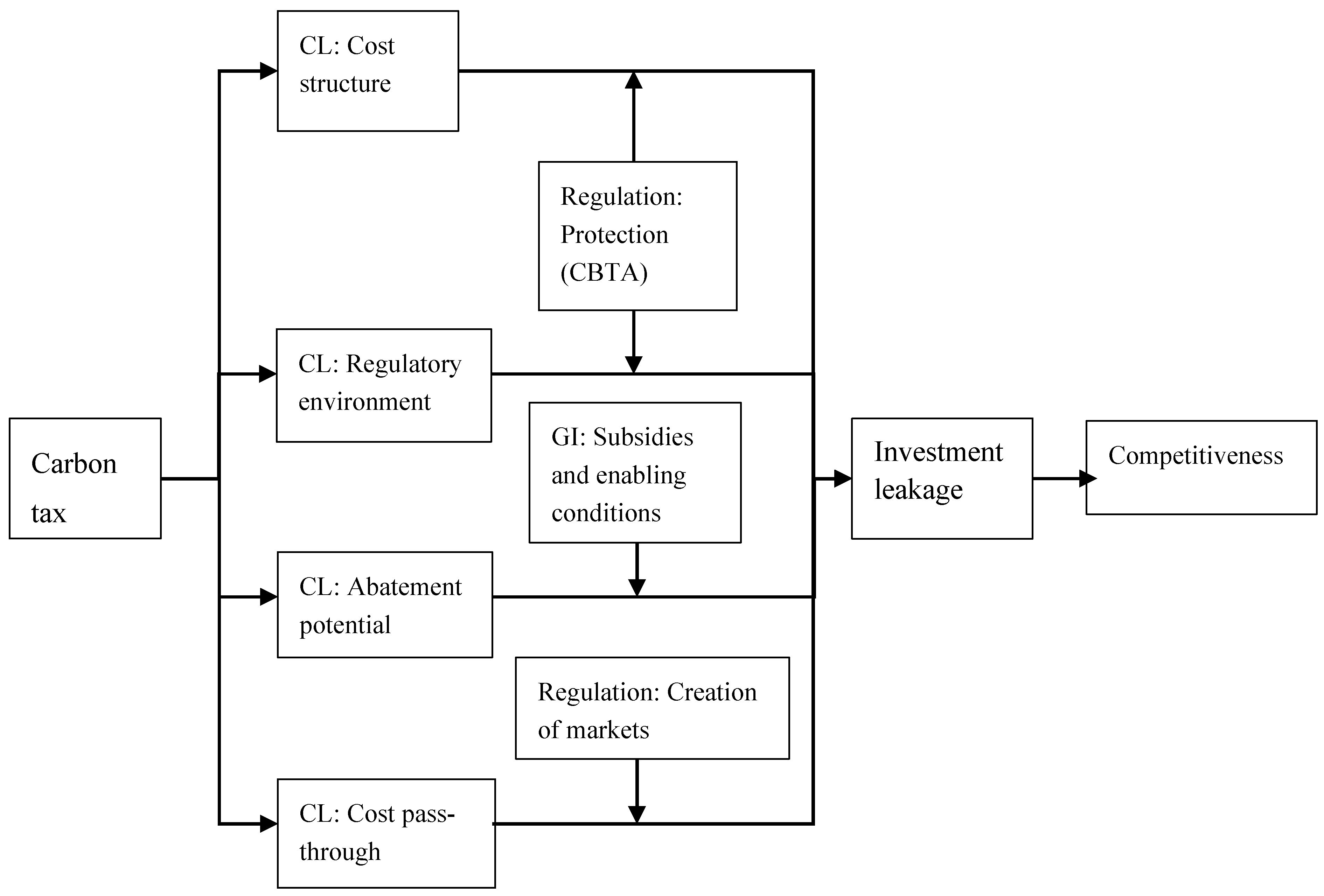

Figure 5 and

Figure 6 show a summary of the relationships found between the variables and sub-variables of carbon leakage and the theory of induced innovation with government intervention.

Figure 5 shows that government intervention in the form of regulations, funding and enabling conditions play a key role by mediating the effects of different variables of carbon leakage and investment leakage. As mentioned earlier in this text, the protection of industries with a carbon border tax adjustment (CBTA) can buffer the effects of an increase in production costs and prevent investment leakage taking place. This mechanism would also provide certainty for the future price of carbon that is needed by businesses to plan their investment decisions. Subsidies and enabling conditions mediate the effect between abatement potential and investment leakage, as they tackle two of the most important barriers for the implementation of abatement technology. Lastly, the creation of markets enables companies to innovate in new products or production processes, as product differentiation is one of the mechanisms that is used by firms to pass-through increases in production costs.

In

Figure 6, organisational innovation is modelled as a precursor for product and process innovation, as they come as a consequence of a shift in a business model, vision or goals. Organisational innovation take place after a company perceives that their investments are safe, for which a regulation like a CBTA is required. Once any business can make a favourable business cases for new products or the implementation of low-carbon technology, product or process innovation can take place. This will translate into a green investment, as companies would need to implement low-carbon technologies to comply with regulations and satisfy the newly created demand. In a context in which European environmental policy is becoming more stringent, companies that act as first movers will increase their competitiveness and create momentum for the decarbonisation of the European industry.

5. Discussion

This study was aimed at developing and applying a framework to assess the implications of the implementation of a carbon tax on the industrial cluster for the Port of Rotterdam by analysing two potential effects. This research tested the carbon leakage hypothesis by assessing the extent to which a higher price of carbon, represented by a carbon tax, would affect the competitiveness of the industries operating in the PoR and whether it would induce carbon and investment leakage. It also assessed the extent to which a carbon tax could enhance technological innovation aimed at the implementation of low-carbon technology and the decarbonisation of these industries. Additionally, this research aimed at understanding the role of the government in both preventing carbon and investment leakage and creating an attractive environment for green investment. As presented in the previous section, government support was found to have a mediating effect in buffering the distortions induced by a carbon tax in the level playing field, with regulations that protects the industries’ competitiveness. Government support is also required to create an attractive investment environment, preventing firms from diverting investments to other regions and incentivising them to invest in low-carbon technologies in their facilities in the PoR. There was consensus among the interviewees in that the current policies in Europe are focusing almost exclusively on penalising emitters, and do not provide sufficient support to the industrial sector to make the transition.

Another point of discussion lies in the uneven distribution of abatement costs among the various industries and facilities. There are only a few firms that currently have cheap abatement options in The Netherlands, these businesses are better equipped to bear the higher carbon costs and might also be in line for subsidies in order to implement these low-carbon technologies. For instance, in the case of oil refineries, the only facilities with relatively cheap abatement options are those who already have hydrogen production units, which give them a comparative advantage over the rest of the refineries. Consequently, if the government introduces a subsidy on the implementation of green hydrogen, these companies will have a greater chance of receiving the funds as they already have hydrogen production units and are closer to fully implementing the technology. If a subsidy scheme is not carefully designed, it could lead to the subsidies only benefitting a few companies that have cheap abatement options and leaving the rest to bear the costs of the carbon tax. Similarly, the decision on which technologies are to be subsidised is also controversial, as several abatement technologies for the industrial cluster were identified in the collected data. Subsidies can also distort the market and benefit some technologies over others with the same abatement potential. This links to the criticism of government intervention that was presented in the background section of this paper, which suggested that, by providing subsidies, the government would be picking winners and losers. This is not to deny the findings of this research, which consistently put government intervention as having a key mediating role to both prevent carbon and investment leakage and inducing the implementation of low-carbon technologies. The findings are also in line with and validate the SDE++ subsidy scheme that was implemented in The Netherlands, promoted by the ministry of economic affairs and climate with the aim of stimulating sustainable energy production and supply. The production of renewable electricity lies at the core of most of the low-carbon technologies, and there is a need to accelerate switching the electricity grid to renewables as much as possible. If electrification or green hydrogen are produced with electricity from fossil sources, the effects could lead to an increase in the total emissions. As stated by one of the interviewees, “electrification would require an enormous and not realistic deployment of low-carbon electricity. Currently we are decarbonising the power mix that we need simply for our current electricity demands. So, if you are going to add other electricity options, the power still needs to come from somewhere. The same goes for what we call green hydrogen, it is a perfect example”.

The fact that the abatement cost curve presents an exponential growth, with an increasing marginal abatement, has implications for the decarbonisation of industry in The Netherlands. Given that the industrial sector of the country is technologically advanced compared to the rest of Europe, the abatement cost curve for the Dutch industry probably makes it as or less attractive to invest in than in other countries. With this perspective, it makes more sense from the cost-effectiveness of CO2 abatement to invest primarily in other countries before starting to invest in the decarbonisation of The Netherlands. Then, for the industries in The Netherlands to be ahead of the curve and among the 10% best performing industries in Europe, it will require higher investments than in other European countries. This would involve strong support schemes and investing in it as a society. In terms of where it makes more sense to make the first investment in curbing CO2 emissions at the European level, The Netherlands is not necessarily the priority country. The lowest abatement costs are currently in banning coal in countries like Germany and Poland, and the more advanced industrial transitions lies further down the line.

There are also concerns about the development and use of CCUS, as it can slow down the development of other technologies. For instance, projects like Porthos need to develop a business case in order to be developed and implemented. This means that companies need to be fully behind the changes and sign contracts and be totally committed to delivering CO2 to Porthos and store it under the North Sea. The danger lies in the fact that the companies will be legally committed to keeping using fossil fuels and paying to store the emissions when they could be investing that money in scaling up clean technologies or the generation of renewable electricity. Although there is wide consensus in that CCUS is the only feasible option to abate emissions in the industrial cluster at the PoR in the short term, there is the need to find ways that ensure that it will not delay the scaling-up of low-carbon technologies that do not use fossil fuels. It should be noted that many of the aspects of scaling up low-carbon technologies are based on the assumption that businesses collaboratively finance projects aiming for a common goal. Nevertheless, the very nature of a business operating and trading in competitive scenarios is to develop technology and production techniques to be used for themselves, not to be shared with the competition. If there are efficiency gains or cost reductions from developing, scaling up and implementing technology, companies will want to have that as a competitive advantage against the competition. However, recent developments, such as the Porthos project, show that it is possible to develop joint projects involving competing firms. An assessment and analysis of the drivers of cooperation between firms would shed light on which factors are involved in this cooperation, which would, in turn, make it possible for policymakers to enhance them.

With regards to the literature upon which this study was built upon, there are also several points of discussion. The variables and indicators used in this research to assess the risk of carbon leakage were based mainly on the drivers identified by Droege [

19]. This research validates these as important and appropriate drivers to assess the risk of carbon leakage from an industrial cluster. Perhaps the most important finding related to carbon leakage and the theory presented in the background of this paper is that investment leakage is the main threat in the face of a higher price of carbon. A cease of production in Rotterdam and a subsequent relocation of operations are unlikely, given the benefits that firms gain from the agglomeration externalities and the enormous sunk costs that they have already invested into this location. Even though there was no scientific proof found of carbon leakage or losses of competitiveness in empirical ex-post studies [

4], the findings of this research suggest that investment leakage is a real possibility in the case of a carbon tax implemented with no protection to incumbent industries. In the case of the industrial cluster of the PoR, the growth of firms in terms of production capacity will occur in facilities located in less regulated regions, where investments are more profitable. However, the current instruments used to protect incumbents from carbon leakage have received many critics, mainly because currently in Europe businesses are still not paying for the emissions, making the policies ineffective. Furthermore, businesses receiving free allocation permits have passed-through their opportunity cost to the price of the products, which have resulted in windfall profits for the various businesses [

19]. This highlights the importance of the design of the regulations aimed at protecting the industry and the need to increase the price of fossil-based products for the whole European market, with a mechanism such as the CBTA.

An interesting finding involved the certainty of the future price of carbon that is required for firms to plan their investment decisions. Setting a floor to the price of carbon could provide a competitive advantage for firms in The Netherlands. The regulatory environment would be providing businesses with extra certainty, preventing them from investing at the wrong point in time and reducing the risk associated in their investment decision. By introducing price certainty, the investment decisions that businesses make will be at lower costs. This reduction in uncertainty will lead to a reduction in the risk associated with the investment, and it also means that investors would be able to finance businesses at a lower rate. For instance, banks price the risk when financing businesses determining who pays what premiums according to the level of risk. If the risk is too high, banks might not even provide financing at all. To further reduce the risk, a price ceiling would also be necessary. Just as when carbon prices fall below the price floor they do not provide businesses with an incentive, the opposite also holds true, prices skyrocketing can also have detrimental effects, it would cause firms to rush to make investment decisions that they might regret when the price returns to normal levels.

If a minimum and maximum carbon price was introduced, businesses would both be incentivised to invest in low-carbon technology, and they would be protected from incorrect price signals that may lead to incorrect investment decisions. As pointed out previously in this paper, EIIs make investments with a long-term perspective. As such, long-term carbon prices are more relevant than current carbon prices and that is what drives the majority of the investment decisions. With this in mind, as long as the price of carbon increases by a given factor over time, firms will consequently have a different approach to investments. This certainty and predictability of the future prices of carbon would encourage them to invest in green technology. Regarding the theory of induced innovation, the findings are consistent with related work on the topic, but this research has expanded the scope by including more insights. First, the literature reviewed tends to ignore or overlook the costs involved in technological development and innovation, which, in this case study, proved to be enormous. In this case study, instead of innovating or paying tax, companies or branches of multinationals can become bankrupt if their profits before tax are too slim. Indeed, many of the facilities in the PoR have abatement options that greatly exceed their profits when represented as EUR/ton CO2, leaving them without options to avoid paying for the higher price of carbon. Second, there is no consensus in the literature about whether a higher price of carbon could enhance or be detrimental for the industrial transition. The findings of this research suggest that a higher price of carbon is necessary, but it will not create a sufficient condition to initiate the decarbonisation of the industry. Furthermore, this study concludes that a carbon tax on its own will not enhance the industrial transition of the companies operating in the PoR towards low-carbon production and could instead induce investment leakage. However, the findings also suggest that in presence of support mechanisms, firms are willing to invest in low-carbon technology.

There is an important distinction that can be made between the various sorts of funding mechanisms. This research highlights the importance of scale-up funding rather, than R&D funding, to accelerate the industrial transition. However, data suggests that the efforts of private and public sectors have been mainly focused on R&D funding. As stated in previous sections of this paper, the technological developments of low-carbon technologies are currently in place like the CCUS, green hydrogen and offshore wind, and the technology is to a certain extent mature. What is needed for its implementation is to scale it up and test it in large scale industrial complexes, which requires different kinds of funding mechanisms. Lastly, the findings of this study confirm that markets on their own will not be able to provide the necessary incentives for industries to initiate the transition with any great speed. The forces keeping business as usual are strong, and the lack of demand for cleaner products and technologies is preventing the new technologies from being scaled up. This translates into extremely high costs of low-carbon technology, making it impossible for firms to make favourable business cases for their implementation. These results are in line with the neo-Schumpeterian approach to government intervention, which gives governments an active role letting them create and shape markets, rather than just fixing market failures [

30,

31]. Furthermore, the results of this research suggest that government intervention in the economy is acceptable, desirable and required to achieve a low-carbon development and the decarbonisation of industry.

It should, however, be pointed out that, within the European context, the Treaty on the Functioning of the European Union refers to government support as state aid, which can be in the form of grants, interest and tax reliefs, guarantees, government holdings of all or part of a company, or providing goods and services on preferential terms [

35]. The Treaty generally forbids state aid, unless it is justified by reasons of general economic development, and it leaves room for a number of policy objectives for which state aid can be considered acceptable [

35]. In a 2014 reform, the European Commission has introduced changes to the state aid rules aiming at boosting investment in innovation and R&D. The new rules were aimed at giving countries the flexibility to invest in, for example, innovation clusters or broadband infrastructure [

35,

36]. The most recent changes in the area of state aid are currently being introduced as part of the European Green Deal, a set of policies that aim at climate neutrality by 2050. The overall objective is decarbonising the energy sector and supporting the industrial sector to innovate and become a world leader in the green economy [

37].

6. Conclusions

The carbon leakage hypothesis has been assessed for industries operating in the industrial cluster of the PoR, and the analysis focused mainly on oil refining and petrochemical production. The main findings were that investment leakage is a far more serious threat than carbon leakage and relocation of operations. There enormous sunk costs, long term commitments with suppliers and customers, the high operational efficiency facilitated by the infrastructure and logistics and agglomeration externalities mediate the effect of a carbon tax in the cost structure of firms and would prevent them from relocating.

The theory of induced innovation has potential to materialise in this case, but subject to government support. Many of the facilities in the PoR have abatement options that greatly exceed their profits when represented as EUR/ton CO2, leaving them without options to avoid paying for a higher price of carbon. A carbon tax on its own will not enhance the industrial transition of the companies operating in the PoR towards low-carbon production, and could instead induce investment leakage. This research also showed the willingness of businesses to invest in low-carbon technology and are behind accelerating the industrial transition, but only if they can make favourable business cases. The instruments to incentivise the industry that were present in the data collected included direct subsidies, grants and enabling conditions for the implementation of new technology. The industrial cluster of the PoR has the appropriate scale to become a frontrunner in the testing and implementation of low-carbon technologies, such as green hydrogen. It currently has an offshore wind power grid, large and highly emitting industries, pipeline networks and CCUS facilities. These are important factors to implement this new technology and enable it to rapidly create a market for it. According to the data gathered, the scale is the most important feature when it comes to creating a favourable business case for green hydrogen and bringing the costs down. That scale can be found in a place along the coast, where there are transportation infrastructure, large industries, carbon emissions and the know-how to implement, maintain and manage the new technology.

Regarding future research opportunities opened up by this study, it would be interesting to widen the sample of stakeholders, which could give new perspectives on the implications of introducing a carbon tax. This would enable a more complete identification of factors that need to be taken into consideration in order to devise new regulations and advise the government as to how it can support and enhance the industrial transition while protecting the local economy. Further, a more in-depth analysis could be performed identifying the various facilities that are currently running and would be required to run in the industrial cluster of the PoR in order to identify the abatement potential of each one. This would allow to monetise the investment required to implement the appropriate low-carbon technology and comply with the national or European reduction targets, or to bring the facilities in the PoR to the 10% best performing industries in Europe, pushing the industrial transition forward. Additionally, it would provide a close estimation of the costs that the new technologies would require for companies to be able invest in and thus not only remain in business but on a stable footing. These estimates can then be used by decision-makers, as they provide information about the amount of subsidy that would be required to clean the entire production of the industrial cluster of the PoR.

As mentioned earlier in this study, as long as there is no market for cleaner products, companies will not make the necessary investments that are required to produce them. Further research aimed at disentangling the complexity behind the creation of new markets would help to shed a light on the disruptions that would be created within the existing markets. It would show how directly and indirectly they would impact stakeholders, such as suppliers, customers and related industries, and what the impact would be on the prices of goods for the end consumers, national and international trade lanes, and how it would affect the regional economy. Further research is also required to identify and develop pathways to overcome the most pressing barriers for the scaling up of low-carbon technologies, such as green hydrogen and electrification. On the one hand, this could be researched by exploring the possibilities of producing, transporting and obtaining the required capacity for renewable electricity to industrial sites. On the other hand, what the possibilities are for importing it from regions with better natural resources and conditions for its production, like the possibility of solar energy, should also be explored. There is a need to assess the absolute generation potential in The Netherlands and project the extra demand that would be induced by fully switching to a green electricity grid and decarbonising the industry. Comparing these results will give an estimation of the total amount of green electricity that needs to be generated or imported. According to the findings of this research, the full potential of renewable electricity generation in The Netherlands is not enough to support a full industrial transition, which is one of the most important barriers in the decarbonisation of the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}