Sustainable Development, Governance and Performance Measurement in Public Private Partnerships (PPPs): A Methodological Proposal

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Public Private Partnerships (PPPs)

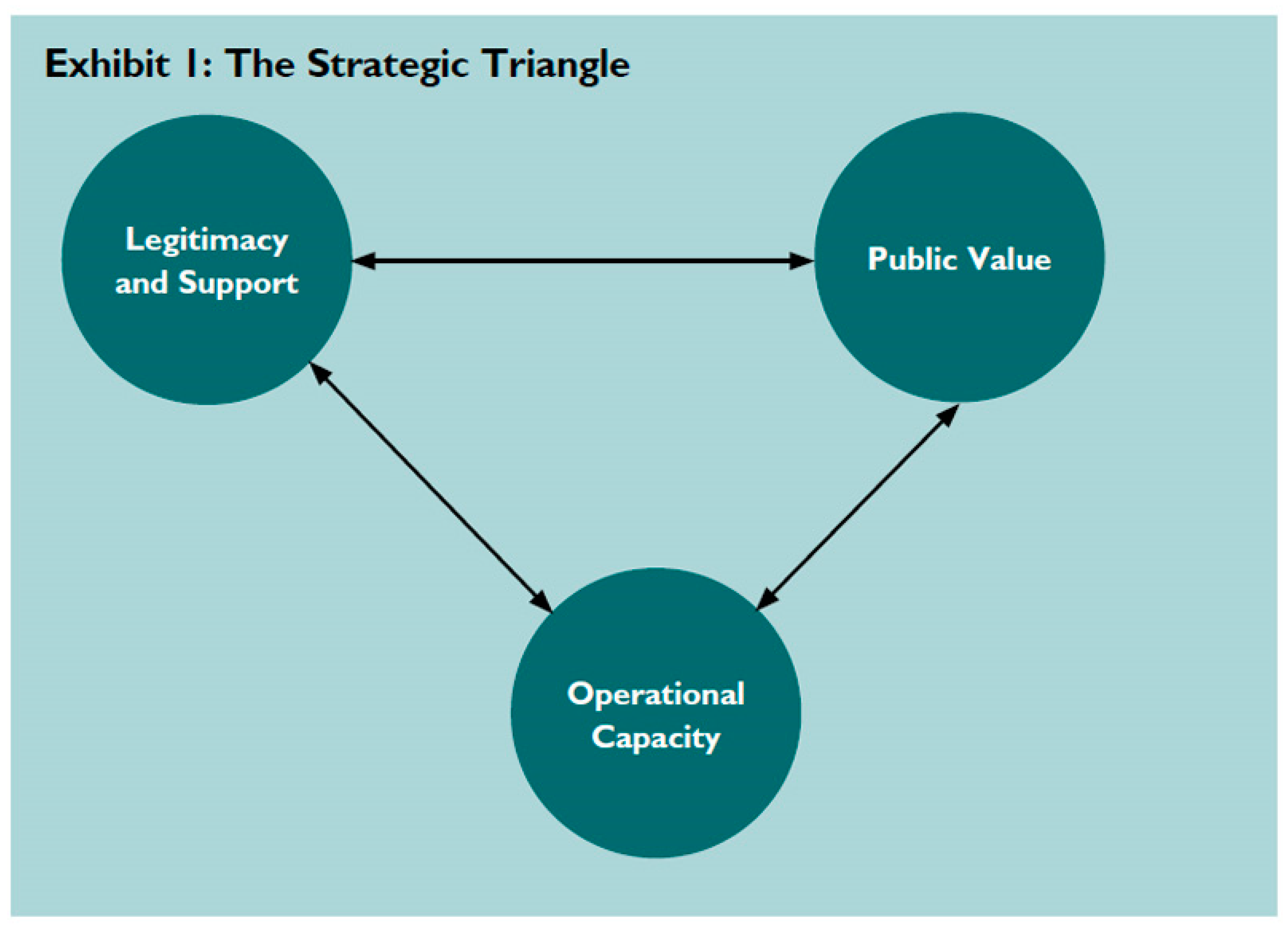

2.2. The Performance of Local PPPs

- -

- the mission and the ability to produce Public Value;

- -

- social and political legitimacy;

- -

- operational and financial sustainability.

3. Research Design and Method

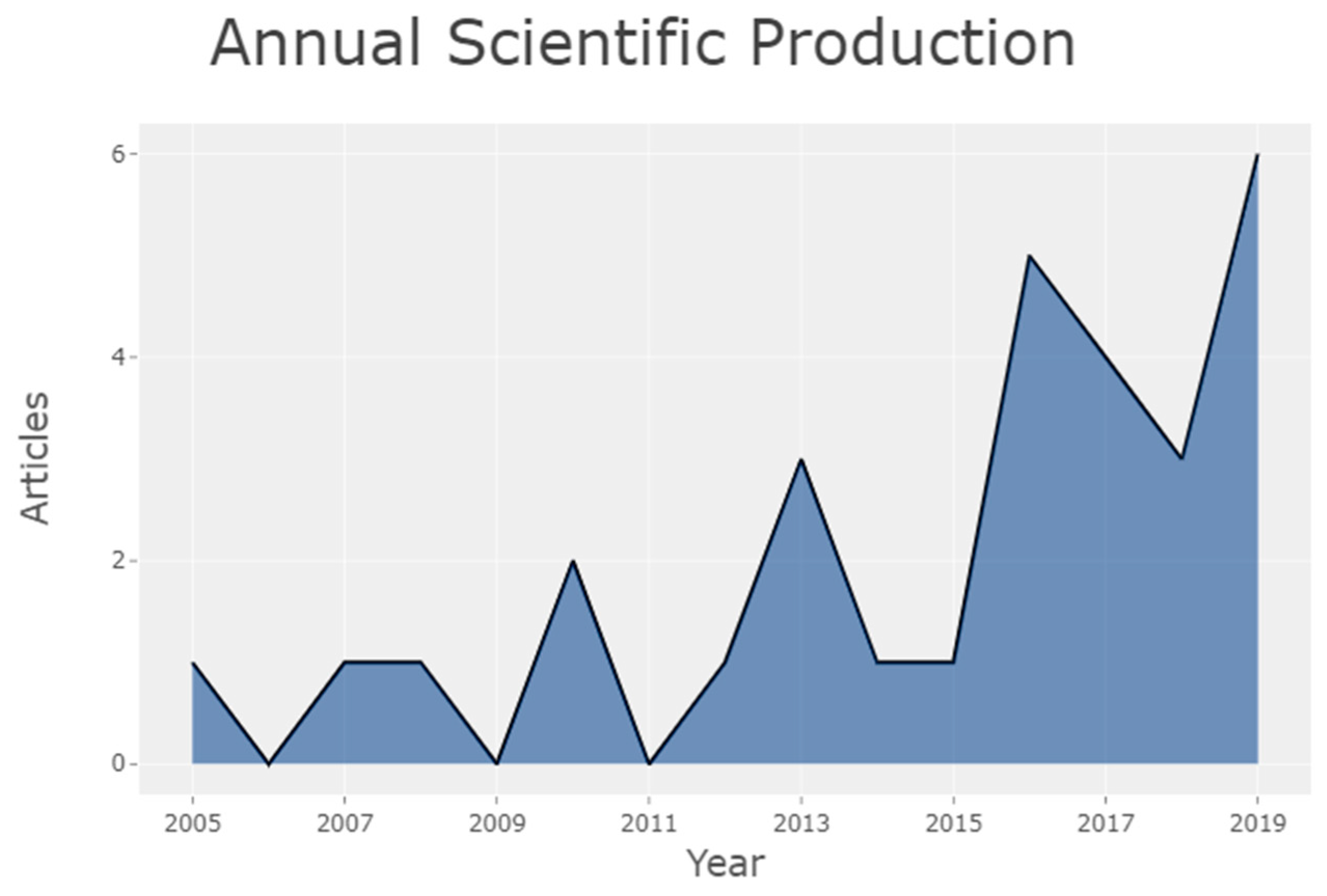

3.1. Analytical Strategy and Results

3.2. Most Cited Articles

4. Literature Review: How to Meet the Need for Multilayered Performance Measurement in PPPs?

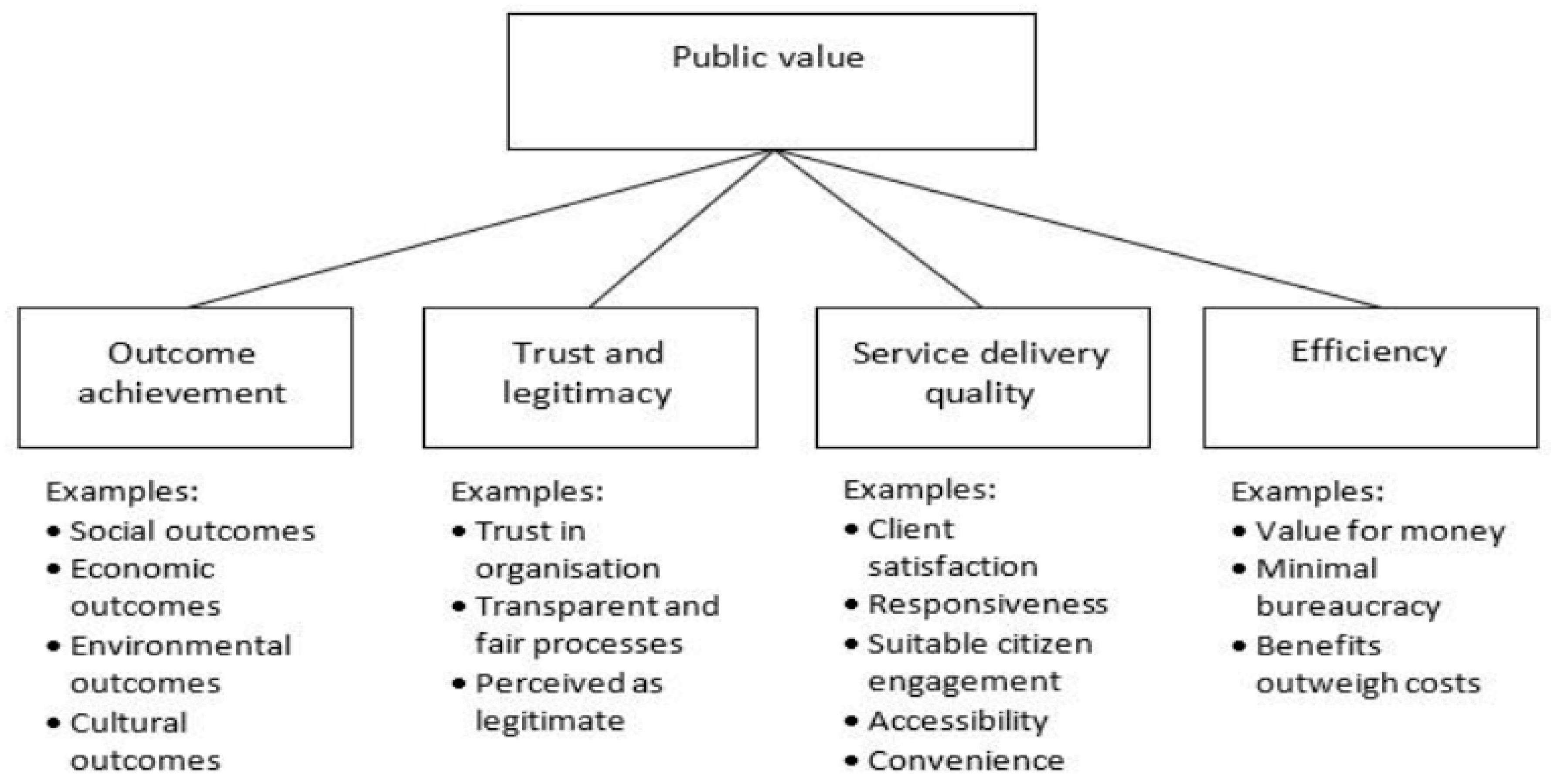

4.1. Public Value As a Tool for Conceptualizing Performance

4.2. Predictors of Performance

4.3. Public Value, Performance Measurement and Sustainable Development: Determinants and Mechanisms

5. Discussion

Findings and Implications

6. Primary Conclusions, Limitations and the Future Research Agenda

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Title | Year | Source Title | Volume |

|---|---|---|---|---|

| Gultom Y.M.L. | Transaction Costs and Efficiency in Design-Build Contracting: Empirical Evidence from the Transportation Infrastructure Sector in Oregon | 2019 | Public Performance and Management Review | 42 |

| Cabral S., Mahoney J.T., McGahan A.M., Potoski M. | Value creation and value appropriation in public and nonprofit organizations | 2019 | Strategic Management Journal | 40 |

| Hossain M., Guest R., Smith C. | Performance indicators of public private partnership in Bangladesh: An implication for developing countries | 2019 | International Journal of Productivity and Performance Management | 68 |

| Steinfeld J., Koala K., Carlee R. | Contracting for public stewardship in public-private partnerships | 2019 | International Journal of Procurement Management | 12 |

| Yuan J., Li W., Xia B., Chen Y., Skibniewski M.J. | Operation performance measurement of public rental housing delivery by ppps with fuzzy-ahp comprehensive evaluation | 2019 | International Journal of Strategic Property Management | 23 |

| Traxler A.A., Greiling D. | Sustainable public value reporting of electric utilities | 2019 | Baltic Journal of Management | 14 |

| Todoruţ A.V., Tselentis V. | Digital technologies and the modernization of public administration | 2018 | Quality-Access to success | 19 |

| Bao F., Martek I., Chen C., Chan A.P.C., Yu Y. | Lifecycle performance measurement of public-private partnerships: A case study in China’s water sector | 2018 | International Journal of Strategic Property Management | 22 |

| Liu H.J., Love P.E.D., Smith J., Irani Z., Hajli N., Sing M.C.P. | From design to operations: a process management life-cycle performance measurement system for Public-Private Partnerships | 2018 | Production Planning and Control | 29 |

| Cappellaro G., Ricci A. | PPPs in health and social services: a performance measurement perspective | 2017 | Public Money and Management | 37 |

| Sundararajan S.K., Tseng C.-L. | Managing Project Performance Risks under Uncertainty: Using a Dynamic Capital Structure Approach in Infrastructure Project Financing | 2017 | Journal of Construction Engineering and Management | 143 |

| Dyllick T., Rost Z. | Towards true product sustainability | 2017 | Journal of Cleaner Production | 162 |

| Hashim H., Che-Ani A.I., Ismail K. | Public Private Partnership (PPP) project performance in Malaysia: Identification of issues and challenges | 2017 | International Journal of Supply Chain Management | 6 |

| Klijn E.H., Koppenjan J. | The impact of contract characteristics on the performance of public–private partnerships (PPPs) | 2016 | Public Money and Management | 36 |

| Häyhtiö M. | Requirements as operational metrics?-Case: Finnish defense forces | 2016 | Management and Production Engineering Review | 7 |

| Liu J., Love P.E.D., Smith J., Matthews J., Sing C.-P. | Praxis of performance measurement in public-private partnerships: Moving beyond the iron triangle | 2016 | Journal of Management in Engineering | 32 |

| Motoyama Y., Knowlton K. | From resource munificence to ecosystem integration: the case of government sponsorship in St. Louis | 2016 | Entrepreneurship and Regional Development | 28 |

| Reynaers A.-M., Paanakker H. | To Privatize or Not? Addressing Public Values in a Semiprivatized Prison System | 2016 | International Journal of Public Administration | 39 |

| Greve C. | Ideas in Public Management Reform for the 2010s. Digitalization, Value Creation and Involvement | 2015 | Public Organization Review | 15 |

| Reynaers A.-M. | Public Values in Public-Private Partnerships | 2014 | Public Administration Review | 74 |

| Mahadi Z., Sino H. | Defining public needs in sustainable development: a case study of Sepang, Malaysia | 2013 | Pertanika Journal of Social Science and Humanities | 21 |

| Karunasena K., Deng H., Harasgama K.S. | An investigation of the critical factors for evaluating the public value of e-government: a thematic analysis | 2013 | Information System and Technology for Organization in a Networked Society | |

| Warner M.E. | Private finance for public goods: Social impact bonds | 2013 | Journal of Economic Policy Reform | 16 |

| Diggs S.N., Roman A.V. | Understanding and tracing accountability in the public procurement process: Interpretations, performance measurements, and the possibility of developing public-private partnerships | 2012 | Public Performance and Management Review | 36 |

| English L., Baxter J. | The changing nature of contracting and trust in public-private partnerships: The case of Victorian PPP prisons | 2010 | Abacus | 46 |

| Warner M.E. | The future of local government: Twenty-first-century challenges | 2010 | Public Administration Review | 70 |

| Weihe G. | Public-private partnerships and public-private value trade-offs | 2008 | Public Money and Management | 28 |

| Khadaroo I., Abdullah A. | Private finance initiative (or public private partnership) implementation processes and perception of value for money | 2007 | International Journal of Economics and Management | 1 |

| Maxwell K., Husain T. | Public private partnerships: Building capacity while effecting change | 2005 | Evaluation and Program Planning | 28 |

References

- Pollitt, C. Managerialism and the Public Services: Cuts or Cultural Change in the 1990s? Blackwell Business: Oxford, UK; Cambridge, MA, USA, 1993. [Google Scholar]

- Mussari, R. Public sector financial management reform in Italy. In International Public Financial Management Reform: Progress, Contradictions, and Challenges; Guthrie, J., Humphrey, C., Jones, L.R., Olson, O., Eds.; Information Age Publishing Inc.: Charlotte, NC, USA, 2005. [Google Scholar]

- Reginato, E.; Fadda, I.; Pavan, A. Italian municipalities’ NPFM reforms: An institutional theory perspective. Pecvnia 2010, 11, 153–175. [Google Scholar] [CrossRef] [Green Version]

- Pavan, A.; Reginato, E.; Fadda, I. The Implementation Gap of NPM Reforms in Italian Local Government. An Empirical Analysis; FrancoAngeli: Milano, Italy, 2014. [Google Scholar]

- Pavan, A.; Reginato, E.; Landis, C. Institutional Governance. In Global Encyclopedia of Public Administration, Public Policy, and Governance; Farazmand, A., Ed.; Springer International Publishing: Cham, Switzerland, 2018. [Google Scholar]

- Greve, C.; Flinders, M.; Thiel, S. Quangos—What’s in a name? Defining Quangos from a comparative perspective. Gov. Int. J. Policy Adm. 1999, 12, 124–146. [Google Scholar] [CrossRef] [Green Version]

- Vining, A.; Weimer, D. Economic perspective on public organizations. In Oxford Handbook of Public Management; Oxford University Press: Oxford, UK, 2006. [Google Scholar]

- Røiseland, A. Understanding local governance. Institutional forms of collaboration. Public Adm. 2011, 89, 879–893. [Google Scholar] [CrossRef]

- Christensen, T.; Lægreid, P. Complexity and Hybrid Public Administration—Theoretical and Empirical Challenges. Public Organ. Rev. 2011, 11, 407–423. [Google Scholar] [CrossRef] [Green Version]

- Commission of the European Communities. Green Paper on Public—Private Partnerships and Community Law on Public Contracts and Concessions; Office for Official Publications of the European Communities: Brussels, Belgium, 2004; 327p. [Google Scholar]

- Ferreira Da Cruz, N.; Marques, R.; Marra, A.; Pozzi, C. Local mixed companies: The theory and practice in an international perspective. Ann. Public Coop. Econ. 2014, 85, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Hwang, B.-G.; Zhao, X.; Gay, M.J.S. Public private partnership projects in Singapore: Factors, critical risks and preferred risk allocation from the perspective of contractors. Int. J. Proj. Manag. 2013, 31, 424–433. [Google Scholar] [CrossRef]

- Zhang, S.; Chan, A.P.C.; Feng, Y.; Duan, H.; Ke, Y. Critical review on PPP Research—A search from the Chinese and International Journals. Int. J. Proj. Manag. 2016, 34, 597–612. [Google Scholar] [CrossRef]

- World Bank. The World Bank Annual Report 2014; World Bank: Washington, DC, USA, 2014. [Google Scholar]

- OECD. Guidelines on Corporate Governance of State-Owned Enterprises; OECD Publishing: Paris, France, 2015. [Google Scholar]

- Ringkjøb, H.-E.; Aars, J.; Vabo, S.I. Lokalt Folkestyre AS: Eierskap og Styringsroller i Kommunale Selskap; Rapport 1; Rokkansenteret: Bergen, Norway, 2008. [Google Scholar]

- Grossi, G.; Papenfuss, U.; Tremblay, M.S. Corporate governance and accountability of state-owned enterprises. Int. J. Public Sect. Manag. 2015, 28, 274–285. [Google Scholar] [CrossRef]

- Liu, J.; Love, P.E.D.; Smith, J.; Regan, M.; Sutrisna, M. Public-private Partnerships: A Review of Theory and Practice of Performance Measurement. Int. J. Prod. Perform. Manag. 2014, 63, 499–512. [Google Scholar] [CrossRef]

- Ferreira Da Cruz, N.; Cunha Marques, R. Accountability and governance in local public services: The particular case of mixed companies. Innovar 2011, 21, 41–54. [Google Scholar]

- Boardman, A.E.; Vining, A.R. Ownership and Performance in Competitive Environments: A Comparison of the Performance of Private, Mixed, and State-Owned Enterprises. J. Law Econ. 1989, 32, 1–33. [Google Scholar] [CrossRef]

- Guatri, L. La Teoria di Creazione del Valore. Una via Europea; Egea: Milano, Italy, 1991. [Google Scholar]

- Donna, G. La Creazione di Valore Nella Gestione D’impresa; Carocci: Roma, Italy, 1999. [Google Scholar]

- Ziruolo, A. Il Controllo delle Leve di Creazione del Valore Aziendale; Giappichelli Editori: Torino, Italy, 2005. [Google Scholar]

- Brealey, R.A.; Meyers, S.C. Principles of Corporate Finance; McGraw-Hill: New York, NY, USA, 1991. [Google Scholar]

- Pratuckchai, Patanapongse. The Study of Management Control Systems in State Owned Enterprises: A Proposed Conceptual Framework. Int. J. Organ. Innov. 2012, 5, 83–115. [Google Scholar]

- Guatri, L.; Sicca, L. Strategie, Leve del Valore, Valutazione delle Aziende; Egea: Milano, Italy, 2000. [Google Scholar]

- Donna, G.; Borsic, D. La Sfida del Valore. Strumenti e Strategie per il Successo D’impresa; Guerini e Associati: Milano, Italy, 2000. [Google Scholar]

- Searcy, C. Measuring Enterprise Sustainability. Bus. Strategy Environ. 2016, 25, 120–133. [Google Scholar] [CrossRef]

- Martín-de Castro, G.; Amores-Salvadó, J.; Navas-López, J.E. Environmental Management Systems and Firm Performance: Improving Firm Environmental Policy through Stakeholder Engagement. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 243–256. [Google Scholar] [CrossRef]

- Brown, P.J.; Bajada, C. An economic model of circular supply network dynamics: Toward an understanding of performance measurement in the context of multiple stakeholders. Bus. Strategy Environ. 2018, 27, 643–655. [Google Scholar] [CrossRef]

- Olsen, G.W.; Mair, D.C.; Lange, C.; Harrington, L.M.; Church, T.R.; Goldberg, C.L.; Herron, R.M.; Hanna, H.; Nobiletti, J.B.; Rios, J.A.; et al. Per- and polyfluoroalkyl substances (PFAS) in American Red Cross adult blood donors, 2000–2015. Environ. Res. 2017, 157, 87–95. [Google Scholar] [CrossRef]

- Cepiku, D. Performance management in public administrations. In Handbook of Global Public Policy and Administration; Klassen, T.R., Cepiku, D., Lah, T.J., Eds.; Routledge: Abingdon, UK, 2015. [Google Scholar]

- Mbo, M.; Adjasi, C. Drivers of organizational performance in state owned enterprises. Int. J. Prod. Perform. Manag. 2017, 66, 405–423. [Google Scholar] [CrossRef]

- Sannino, G.; Aversano, N.; Tartaglia Polcini, P. Heritage assets e categorie contabili nel reporting della pubblica amministrazione: Un connubio realizzabile? Riv. Ital. Ragioneria Econ. Aziend. 2013, 10, 11–12. [Google Scholar]

- Reginato, E.; Landis, C.; Fadda, I.; Pavan, A. German and Italian Municipalities’ Internal Control Systems: Convergence to a Neo-Weberian Reform Pattern? Int. J. Public Adm. 2014, 37, 601–610. [Google Scholar] [CrossRef]

- Tien, N.H.; Anh, D.B.H.; Ngoc, N.M. Corporate financial performance due to sustainable development in Vietnam. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 694–705. [Google Scholar] [CrossRef]

- Esposito, P.; Ricci, P. Public (dis)Value: A case study. In Public Value Management, Measurement and Reporting; Guthrie, J., Marcon, G., Russo, S., Farneti, F., Eds.; Emerald: Bingley, UK, 2014; pp. 291–300. [Google Scholar]

- Esposito, P.; Ricci, P. How to turn public (dis)value into new public value? Evidence from Italy. Public Money Manag. 2015, 35, 227–231. [Google Scholar] [CrossRef]

- Haldar, S. Towards a conceptual understanding of sustainability-driven entrepreneurship. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1157–1170. [Google Scholar] [CrossRef]

- Kayani, G.M.; Ashfaq, S.; Siddique, A. Assessment of Financial Development on Environmental Effect: Implications for Sustainable Development. J. Clean. Prod. 2020, 261, 120984. [Google Scholar] [CrossRef]

- Le Blanc, D. Towards Integration at Last? The Sustainable Development Goals as a Network of Targets. Sustain. Dev. 2015, 23, 176–187. [Google Scholar] [CrossRef]

- Stacchezzini, R.; Melloni, G.; Lai, A. Sustainability management and reporting: The role of integrated reporting for communicating corporate sustainability management. J. Clean. Prod. 2016, 136, 102–110. [Google Scholar] [CrossRef]

- Whincop, M.J. Corporate Governance in Government Corporations, Law, Ethics and Governance; Ashgate Publishing: Williston, VT, USA, 2005. [Google Scholar]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef] [Green Version]

- Geissdoerfer, M.; Morioka, S.N.; De Carvalho, M.M.; Evans, S. Business models and supply chains for the circular economy. J. Clean. Prod. 2018, 190, 712–721. [Google Scholar] [CrossRef]

- Bebbington, J.; Unerman, J. Achieving the United Nations Sustainable Development Goals: An enabling role for accounting research. Account. Audit. Account. J. 2018, 31, 2–24. [Google Scholar] [CrossRef]

- Ramos, T.B. Sustainability Assessment: Exploring the Frontiers and Paradigms of Indicator Approaches. Sustainability 2019, 11, 824. [Google Scholar] [CrossRef] [Green Version]

- Izzo, M.F.; Ciaburri, M.; Tiscini, R. The Challenge of Sustainable Development Goal Reporting: The First Evidence from Italian Listed Companies. Sustainability 2020, 12, 3494. [Google Scholar] [CrossRef] [Green Version]

- Gultom, Y.M.L. Transaction Costs and Efficiency in Design-Build Contracting: Empirical Evidence from the Transportation Infrastructure Sector in Oregon. Public Perform. Manag. Rev. 2019, 42, 1230–1258. [Google Scholar] [CrossRef]

- Reynaers, A.; Paanakker, H.L. To privatize or not? Addressing public values in a semi privatized prison system. Int. J. Public Adm. 2016, 39, 6–14. [Google Scholar] [CrossRef]

- Diggs, S.N.; Roman, A.V. Understanding and Tracing Accountability in the Public Procurement Process. Public Perform. Manag. Rev. 2012, 36, 290–315. [Google Scholar] [CrossRef]

- Warner, M.E. The Future of Local Government: Twenty-First-Century Challenges. Public Adm. Rev. 2010, 70, s145–s147. [Google Scholar] [CrossRef]

- Rajan, R.G.; Zingales, L. Salvare il Capitalismo dai Capitalisti; Einaudi Editore: Torino, Italy, 2004. [Google Scholar]

- An, X.; Li, H.; Wang, L.; Wang, Z.F.; Ding, J.; Cao, Y. Compensation mechanism for urban water environment treatment PPP project in China. J. Clean. Prod. 2018, 201, 246–253. [Google Scholar] [CrossRef]

- Yang, T.; Long, R.; Li, W. Suggestion on tax policy for promoting the PPP projects of charging infrastructure in China. J. Clean. Prod. 2018, 174, 133–138. [Google Scholar] [CrossRef]

- Wu, Y.; Xu, C.; Li, L.; Wang, Y.; Chen, K.; Xu, R. A risk assessment framework of PPP waste-to-energy incineration projects in China under 2-dimension linguistic environment. J. Clean. Prod. 2018, 183, 602–617. [Google Scholar] [CrossRef]

- Liu, J.; Xue, X. Application of a performance-based public and private partnership model for river management in China: A case study of Nakao River. J. Clean. Prod. 2019, 236, 117684. [Google Scholar] [CrossRef]

- Franceschelli, M.V.; Santoro, G.; Giacosa, E.; Quaglia, R. Assessing the determinants of performance in the recycling business: Evidence from the Italian context. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1086–1099. [Google Scholar] [CrossRef]

- James, P. Business environmental performance measurement. Bus. Strategy Environ. 1994, 3, 59–67. [Google Scholar] [CrossRef]

- Megginson, W.L.; Netter, J.M. From State to Market: A Survey of Empirical Studies on Privatization. J. Econ. Lit. 2001, 39, 321–389. [Google Scholar] [CrossRef] [Green Version]

- Ardito, L.; Carrillo-Hermosilla, J.; Río, P.; Pontrandolfo, P. Sustainable innovation: Processes, strategies, and outcomes. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1009–1011. [Google Scholar] [CrossRef]

- Baldwin, R.; Cave, M. Understanding Regulation. Theory, Strategy and Practice; Oxford University: Oxford, UK, 1999; pp. 19–20. [Google Scholar]

- Toninelli, P.A. The Rise and Fall of State-Owned Enterprise in the Western World; Cambridge University: Cambridge, UK, 2000. [Google Scholar]

- Sheshinski, E.; Lopez-Calva, L. Privatization and Its Benefits: Theory and Evidence, CESifo Economic Studies is Currently; Illing, G., Ed.; Oxford University: Oxford, UK, 2003. [Google Scholar]

- Borlotti, B.; Faccio, M. Government Control of Privatized Firms. Rev. Financ. Stud. 2009, 22, 2907–2939. [Google Scholar] [CrossRef]

- Capobianco, A.; Christiansen, H. Competitive Neutrality and State-Owned Enterprises: Challenges and Policy Options; Corporate Governance Working Papers; OECD: Paris, France, 2011. [Google Scholar]

- OECD. Managing Conflict of Interest in the Public Sector: A Toolkit; OECD Publishing: Paris, France, 2005. [Google Scholar]

- Peters, G.P.; Minx, J.C.; Weber, C.; Edenhofer, O. Growth in emission transfers via international trade from 1990 to 2008. Proc. Natl. Acad. Sci. USA 2011, 108, 8903–8908. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Guerrero-Villegas, J.; Sierra-García, L.; Palacios-Florencio, B. The role of sustainable development and innovation on firm performance. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1350–1362. [Google Scholar] [CrossRef]

- Memon, A.; An, Z.Y.; Memon, M.Q. Does financial availability sustain financial, innovative, and environmental performance? Relation via opportunity recognition. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 562–575. [Google Scholar] [CrossRef]

- Verdier, A.; Martinez, S.; Hoorens, D. Local Public Companies in the 25 Countries of the European Union; Dexia Editions: Paris, France, 2004. [Google Scholar]

- Bruton, G.D.; Khavul, S.; Siegel, D.; Wright, M. New Financial Alternatives in Seeding Entrepreneurship: Microfinance, Crowdfunding, and Peer-to-Peer Innovations. Entrep. Theory Pract. 2014, 39, 9–26. [Google Scholar] [CrossRef]

- Farnia, L.; Cavalli, L.; Vergalli, S. Italian Cities SDGs Composite Index: A Methodological Approach to Measure the Agenda 2030 at Urban Level; Fondazione Eni Enrico Mattei: Milano, Italy, 2019. [Google Scholar]

- McCraw, T.K. TVA and the Power Fight, 1933–1939; Philadelphia, J.B., Ed.; Lippincott Company: New York, NY, USA, 1971. [Google Scholar]

- Caro, R. The Power Broker: Robert Moses and the Fall of New York; Alfred a Knopf Incorporated: New York, NY, USA, 1974. [Google Scholar]

- Eckel, C.C.; Vining, A.R. Elements of a theory of mixed enterprise. Scott. J. Political Econ. 1985, 32, 82–94. [Google Scholar] [CrossRef]

- Bovaird, T. Public–Private Partnerships: From Contested Concepts to Prevalent Practice. Int. Rev. Adm. Sci. 2004, 70, 199–215. [Google Scholar] [CrossRef]

- Aharoni, Y. The Evolution and Management of State Owned Enterprises; Ballinger Publishing Company: Pensacola, FL, USA, 1986. [Google Scholar]

- Vining, A.; Boardman, A. Ownership versus Competition: Efficiency in Public Enterprise. Public Choice 1992, 73, 205–239. [Google Scholar] [CrossRef]

- Domberger, S.; Piggott, S. Privatization Policies and Public Enterprise: A Survey; Oxford University: Oxford, UK, 1994. [Google Scholar]

- Gathon, H.J.; Pestieau, P. La performance des entreprises publiques. Une question de propriété ou de concurrence? Rev. Écon. 1996, 47, 1225–1238. [Google Scholar] [CrossRef] [Green Version]

- Walter, F.A.; Monsen, R.J. On the Measurement of Corporate Social Responsibility: Self-Reported Disclosures as a Method of Measuring Corporate Social Involvement. Acad. Manag. J. 1979, 22, 501–515. [Google Scholar]

- Villalonga, B. Privatization and efficiency: Differentiating ownership effects from political, organizational, and dynamic effects. J. Econ. Behav. Organ. 2000, 42, 43–74. [Google Scholar] [CrossRef]

- Furubotn, E.G.; Pejovich, S. Property Rights and Economic Theory: A Survey of Recent Literature. J. Econ. Lit. 1972, 10, 1137–1162. [Google Scholar]

- Li, S.; Ngniatedema, T.; Chen, F. Understanding the Impact of Green Initiatives and Green Performance on Financial Performance in the US. Bus. Strategy Environ. 2017, 26, 776–790. [Google Scholar] [CrossRef]

- Alchian, A.A. Some Economics of property rights. Il Politico 1965, 30, 816–829. [Google Scholar]

- Alchian, A.A.; Demsetz, H. Production, Information Costs, and Economic Organization. IEEE Eng. Manag. Rev. 1972, 62, 777–795. [Google Scholar]

- Demsetz, H. The Theory of the Firm Revisited. J. Law Econ. Organ. 1988, 4, 141. [Google Scholar]

- Grossman, S.J.; Hart, O.D. The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration. J. Political Econ. 1986, 94, 691–719. [Google Scholar] [CrossRef] [Green Version]

- Boycko, M.; Shleifer, A.; Vishny, R. A Theory of Privatisation. Econ. J. 1996, 106, 309–319. [Google Scholar] [CrossRef]

- Bhagat, S.; Black, B. The Uncertain Relationship between Board Composition and Firm Performance. Bus. Lawyer 1999, 54, 921–963. [Google Scholar] [CrossRef] [Green Version]

- Baysinger, B.D.; Butler, H.N. Corporate Governance and the Board of Directors: Performance Effects of Changes in Board Composition. J. Law Econ. Organ. 1985, 1, 101–124. [Google Scholar]

- Perry, T.; Shivdasani, A. Do Boards Affect Performance? Evidence from Corporate Restructuring. J. Bus. 2005, 78, 1403–1432. [Google Scholar] [CrossRef]

- Lægreid, P.; Roness, P.G.; Rubecksen, K. Controlling Regulatory Agencies. Scand. Political Stud. 2008, 31, 1–26. [Google Scholar] [CrossRef]

- Padovani, E.; Yetano, A.; Orelli, R.L. Municipal performance measurement and management in practice. Public Adm. Q. 2010, 34, 591–635. [Google Scholar]

- Chen, H.; Zhu, T. The public order and social responsibility in urban mass transit sustainable governance. J. Clean. Prod. 2020, 261, 121053. [Google Scholar] [CrossRef]

- De Bruijn, H. Managing Performance in the Public Sector; Routledge: London, UK, 2002. [Google Scholar]

- Van Dooren, W.; Bouckaert, G.; Halligan, J. Performance Management in the Public Sector; Routledge: London, UK, 2010. [Google Scholar]

- Merchant, K.A.; Van der Stede, W.A. Management Control Systems: Performance Measurement, Evaluation and Incentives, 3rd ed.; Pearson: Harlow, UK, 2012. [Google Scholar]

- Borisova, G.; Brockman, P.; Salas, J.M.; Zagorchev, A. Government ownership and corporate governance: Evidence from the EU. J. Bank. Financ. 2012, 36, 2917–2934. [Google Scholar] [CrossRef]

- Beuselinck, C.; Cao, L.; Deloof, M.; Xia, X. The value of government ownership during the global financial crisis. J. Corp. Financ. 2017, 42, 481–493. [Google Scholar] [CrossRef]

- Inoue, C.F.K.V.; Lazzarini, S.G.; Musacchio, A. Leviathan as a Minority Shareholder: Firm-Level Implications of State Equity Purchases. Acad. Manag. J. 2013, 56, 1775–1801. [Google Scholar] [CrossRef] [Green Version]

- Vaaler, P.M.; Schrage, B.N. Residual State Ownership, Policy Stability and Financial Performance Following Strategic Decisions by Privatizing Telecoms. J. Int. Bus. Stud. 2009, 40, 621–641. [Google Scholar] [CrossRef]

- Goldeng, E.; Grünfeld, L.A.; Benito, G.R.G. The Performance Differential between Private and State Owned Enterprises: The Roles of Ownership, Management and Market Structure. J. Manag. Stud. 2008, 45, 1244–1273. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-De-Silanes, F. The Benefits of Privatization: Evidence from Mexico. Q. J. Econ. 1999, 114, 1193–1242. [Google Scholar] [CrossRef]

- Dharwadkar, R.; George, G.; Brandes, P. Privatization in emerging economies: An agency theory perspective. Acad. Manag. Rev. 2000, 25, 650–669. [Google Scholar] [CrossRef]

- Monteduro, F. Apertura al Capitale Privato e Performance Economiche. Un’analisi Empirica Nelle Imprese di Servizio Pubblico Locale; Maggioli Editore: Santarcangelo, Italy, 2010. [Google Scholar]

- Lazzarini, S.G.; Musacchio, A. What Do State-Owned Development Banks Do? Evidence from BNDES, 2002–2009. World Dev. 2015, 66, 237–253. [Google Scholar] [CrossRef] [Green Version]

- Doherty, T.L.; Horne, T. Managing Public Services—Implementing Changes: A Thoughtful Approach to the Practice of Management; Routledge: London, UK; New York, NY, USA, 2002. [Google Scholar]

- Kearney, R.; Berman, E. Public Sector Performance, Management, Motivation, and Measurement; Routledge: Abingdon, UK, 1999. [Google Scholar]

- Matei, A.I.; Enescu, E.B. Good Local Public Administration and Performance: An Empirical Study. Procedia Soc. Behav. Sci. 2013, 81, 449–453. [Google Scholar] [CrossRef] [Green Version]

- Moore, M.H. Creating Public Value: Strategic Management in Government; Harvard University: Cambridge, MA, USA, 1995. [Google Scholar]

- Moore, M.H. Selected Writings; Routledge, Taylor & Francis Group: Abingdon, UK, 2013. [Google Scholar]

- Ziruolo, A. Valore Pubblico e Società Partecipate; FrancoAngeli: Milano, Italy, 2016. [Google Scholar]

- Marcon, G. L’evoluzione delle teorie sui processi decisionali delle amministrazioni pubbliche, premessa per l’interpretazione della riforma della contabilità. Azienda Pubblica 2011, 3, 207–221. [Google Scholar]

- Valotti, G. La Riforma Delle Autonomie Locali: Dal Sistema All’azienda; Egea: Milano, Italy, 2000. [Google Scholar]

- Guarini, E.; Magli, F.; Nobolo, A. Accounting for community building: The municipal amalgamation of Milan in 1873–1876. Account. Hist. Rev. 2018, 28, 5–30. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Guthrie, J. On the shoulders of giants: Undertaking a structured literature review in accounting. Account. Audit. Account. J. 2016, 29, 767–801. [Google Scholar] [CrossRef]

- Secundo, G.; Ndou, V.; Del Vecchio, P.; De Pascale, G. Sustainable development, intellectual capital and technology policies: A structured literature review and future research agenda. Technol. Forecast. Soc. Chang. 2020, 153, 119917. [Google Scholar] [CrossRef]

- Petticrew, M.; Roberts, H. Systematic Reviews in the Social Sciences: A Practical Guide; Blackwell Publishing: Oxford, UK, 2006. [Google Scholar]

- Kraus, S.; Breier, M.; Dasí-Rodríguez, S. The art of crafting a systematic literature review in entrepreneurship research. Int. Entrep. Manag. J. 2020, 1–20. [Google Scholar] [CrossRef] [Green Version]

- Bracci, E.; Papi, L.; Bigoni, M.; Deidda Gagliardo, E.; Bruns, H.-J. Public value and public sector accounting research: A structured literature review. J. Public Budg. Account. Financ. Manag. 2019, 31, 103–136. [Google Scholar] [CrossRef]

- Torchia, M.; Calabrò, A.; Morner, M. Public–private partnerships in the health care sector: A systematic review of the literature. Public Manag. Rev. 2015, 17, 236–261. [Google Scholar] [CrossRef]

- Weihe, G. Ordering Disorder—On the Perplexities of the Partnership Literature. Aust. J. Public Adm. 2008, 67, 430–442. [Google Scholar] [CrossRef]

- Steinfeld, J.; Koala, K.; Carlee, R. Contracting for public stewardship in public-private partnerships. Int. J. Procure. Manag. 2019, 12, 135–155. [Google Scholar] [CrossRef]

- Brundtland, G.H. (Ed.) Our Common Future: The World Commission on Environment and Development; Oxford University: Oxford, UK, 1987. [Google Scholar]

- Chaney, P. The Substantive Representation of Women-Does Issue-Salience Matter? Party Politicization and UK Westminster Elections 1945–2010. Br. J. Politics Int. Relat. 2014, 16, 96–116. [Google Scholar] [CrossRef]

- Bao, F.; Martek, I.; Chen, C.; Chan, A.P.C.; Yu, Y. Lifecycle performance measurement of public-private partnerships: A case study in China’s water sector. Int. J. Strateg. Prop. Manag. 2018, 22, 516–531. [Google Scholar] [CrossRef]

- Greve, C. Ideas in Public Management Reform for the 2010s. Digitalization, Value Creation and Involvement. Public Organ. Rev. 2015, 15, 49–65. [Google Scholar] [CrossRef]

- Pollitt, C.; Bouckaert, G. Public Management Reform: A Comparative Analysis; OUP: Oxford, UK, 2000. [Google Scholar]

- Voorn, B.; Van Genugten, M.; Van Thiel, S. Performance of municipally owned corporations: Determinants and mechanisms. Ann. Public Coop. Econ. 2020, 91, 191–212. [Google Scholar] [CrossRef] [Green Version]

- Bouckaert, G.; Peters, B.G. Performance Measurement and Management, The Achilles’ Heel in Administrative Modernization. Public Perform. Manag. Rev. 2002, 25, 359–362. [Google Scholar]

- Deidda Gagliardo, E. La Creazione del Valore Nell’ente Locale; Giuffrè: Milano, Italy, 2002; pp. 261–266. [Google Scholar]

- Tiscini, R. The expert report on the post-merger business plan sustainability: The case of the Italian company law. In Leveraged Buyouts. Valuation, Execution Strategies and Law; Baldi, F., Ed.; Giappichelli: Torino, Italy, 2015. [Google Scholar]

- Pollifroni, M. Environmental Sustainability and Social Responsibility: A theoretical proposal for an accounting evaluation. Econ. Aziend. 2011, 2, 345–354. [Google Scholar]

- Borgonovi, E. Principi e Sistemi Aziendali per le Amministrazioni Pubbliche; Egea: Milano, Italy, 2006. [Google Scholar]

- Carbonara, N.; Pellegrino, R. Public-private partnerships for energy efficiency projects: A win-win model to choose the energy performance contracting structure. J. Clean. Prod. 2011, 170, 1065–1075. [Google Scholar] [CrossRef]

- Pollifroni, M. E-Government towards Transparency: A comparative analysis applied to the Italian Public Sector. J. Account. Manag. Inf. Syst. 2015, 14, 217–233. [Google Scholar]

- Stoker, G. Public value management. Am. Rev. Public Adm. 2006, 36, 41–57. [Google Scholar] [CrossRef] [Green Version]

- Tiscini, R.; Fasan, M.; Fiori, G. What drives value relevance: The visibility effect in the adoption of a new accounting standard. Int. J. Account. Audit. Perform. Eval. 2014, 10, 430–446. [Google Scholar]

- Deidda Gagliardo, E. Il Sistema Multidimensionale di Programmazione a Supporto della Governance Locale; Giuffrè Editore: Milano, Italy, 2007. [Google Scholar]

- Ricci, P. Il Soggetto Economico Nell’azienda Pubblica. Un’introduzione su chi Comanda Davvero Nell’azienda Pubblica e Perché; RIREA: Roma, Italy, 2010. [Google Scholar]

- Ricci, P. Il potenziale impatto delle nuove disposizioni contabili sui comportamenti aziendali e sul sistema economico. Azienda Pubblica 2012, 25, 41–67. [Google Scholar]

- Anselmi, L. Percorsi Aziendali per le Pubbliche Amministrazioni; Giappichelli Editore: Torino, Italy, 2014. [Google Scholar]

- Meynhardt, T. Public Value Inside: What is Public Value Creation? Int. J. Public Adm. 2009, 32, 192–219. [Google Scholar] [CrossRef]

- Rhodes, R.A.W. Understanding Governance: Policy Networks, Governance, Reflexivity and Accountability; Open University: Milton Keynes, UK, 1997. [Google Scholar]

- Osborne, S.P. The new public governance? Public Manag. Rev. 2006, 8, 377–387. [Google Scholar] [CrossRef]

- Aveyard, H. Doing a Literature Review in Health and Social Care; McGraw-Hill Companies: New York, NY, USA, 2007. [Google Scholar]

- Borgonovi, E. Principi e Sistemi Aziendali per le Amministrazioni Pubbliche; Egea: Milano, Italy, 2005. [Google Scholar]

- Marcon, G. Public Value Theory in the Context of Public Sector Modernization. In Public Value Management, Measurement and Reporting; Guthrie, J., Marcon, G., Russo, S., Farneti, F., Eds.; Emerald Group Publishing: Bingley, UK, 2014; pp. 323–351. [Google Scholar]

- Kooiman, J. Modern Governance: New Government-Society Interactions; Sage: Thousand Oaks, CA, USA, 1993. [Google Scholar]

- Kloot, L.; Martin, J. Strategic performance management: A balanced approach to performance management issue in local government. Manag. Account. Res. 2000, 11, 231–251. [Google Scholar] [CrossRef]

- Kelly, G.; Mulgan, G.; Muers, S. Creating Public Value: An Analytical Framework for Public Service Reform; The Cabinet Office Strategy Unit: London, UK, 2002. [Google Scholar]

- Alford, J.; O’Flynn, J. Making Sense of Public Value: Concepts, Critiques and Emergent Meanings. Int. J. Public Adm. 2009, 32, 171–191. [Google Scholar] [CrossRef]

- Moore, M.H. Recognising Public Value: The Challenge of Measuring Performance in Government. In A Passion for Policy; Wanna, J., Ed.; The Australian National University (ANU E Press): Canberra, Australia, 2007; pp. 91–116. [Google Scholar]

- Cowling, K. Prosperity, Depression and Modern Capitalism. Int. Rev. Soc. Sci. 2006, 59, 369–381. [Google Scholar] [CrossRef]

- Spano, A. Public value creation and management control systems. Int. J. Public Adm. 2009, 32, 328–348. [Google Scholar] [CrossRef]

- Spano, A. How do we measure public value? From theory to practice. In Public Value Management, Measurement and Reporting; Guthrie, J., Marcon, G., Russo, S., Farneti, F., Eds.; Emerald Group Publishing: Bingley, UK, 2014; Volume 3, pp. 353–373. [Google Scholar]

- Deidda Gagliardo, E. Il Valore Pubblico. La Nuova Frontiera delle Performance; RIREA: Rome, Italy, 2015. [Google Scholar]

- Collins, R. The BBC and “Public Value”. Med. Kommun. Swiss. 2007, 55, 164–184. [Google Scholar] [CrossRef]

- Al-Raisi Ahmad, N.; Al-Khouri Ali, M. Public Value and ROI in the Government Sector. Adv. Manag. 2010, 3, 33–38. [Google Scholar]

- Cole, M.; Parston, G. Unlocking Public Value; John Wiley & Sons: Hoboken, NJ, USA, 2006. [Google Scholar]

- Papi, L.; Bigoni, M.; Bracci, E.; Deidda Gagliardo, E. Measuring public value: A conceptual and applied contribution to the debate. Public Money Manag. 2018, 38, 503–510. [Google Scholar] [CrossRef]

- Faulkner, N.; Kaufman, S. Theoretical Stagnation: A Systematic Review and Framework for Measuring Public Value. Aust. J. Public Adm. 2018, 77, 69–86. [Google Scholar] [CrossRef]

- Bozeman, B.; Rimes, H.; Youtie, J. The Evolving State-of-the-Art in Technology TransferResearch: Revisiting the Contingent Effectiveness Model. Res. Policy 2015, 44, 34–49. [Google Scholar] [CrossRef]

- Benington, J. Creating the Public in Order to Create Public Value? Int. J. Public Adm. 2009, 32, 232–249. [Google Scholar] [CrossRef]

- Benington, J. From Private Choice to Public Value? In Public Value: Theory and Practice; Benington, J., Moore, M.H., Eds.; Palgrave Macmillan: Basingstoke, UK, 2011; pp. 31–51. [Google Scholar]

- Talbot, C.; Wiggan, J. The Public Value of the National Audit Office. Int. J. Public Sect. Manag. 2010, 23, 54–70. [Google Scholar] [CrossRef]

- Meynhardt, T.; Bartholomes, S. (De)Composing Public Value: In Search of Basic Dimensions and Common Ground. Int. Public Manag. J. 2011, 14, 284–308. [Google Scholar] [CrossRef]

- Connolly, W.E. The ‘New Materialism’ and the Fragility of Things. Millennium 2013, 41, 399–412. [Google Scholar] [CrossRef]

- Bracci, E.; Gagliardo, E.D.; Bigoni, M. Performance Management Systems and Public Value: A Case Study. In Public Value Management, Measurement and Reporting; Guthrie, J., Marcon, G., Russo, S., Farneti, F., Eds.; Emerald: Bingley, UK, 2014; pp. 129–157. [Google Scholar]

- Heeks, R. ICT4D 2.0: The Next Phase of Applying ICT for International Development; The University of Manchester: Manchester, UK, 2008. [Google Scholar]

- Karunasena, K.; Deng, H. Critical Factors for Evaluating the Public Value of e-Government in Sri Lanka. Gov. Inf. Q. 2012, 29, 76–84. [Google Scholar] [CrossRef]

- Karkin, N.; Janssen, M. Evaluating Websites from a Public Value Perspective: A Review of Turkish Local GovernmentWebsites. Int. J. Inf. Manag. 2014, 34, 351–363. [Google Scholar] [CrossRef]

- Brookes, S.; Wiggan, J. Reflecting the Public Value of Sport: A Game of Two Halves. Public Manag. Rev. 2009, 11, 401–420. [Google Scholar] [CrossRef]

- Al-Hujran, O.; Al-Debei, M.M.; Chatfield, A.; Migdadi, M. The Imperative of Influencing Citizen Attitude toward E-government Adoption and Use; Elsevier: Amsterdam, The Netherlands, 2015. [Google Scholar]

- Horner, L.; Fauth, R.; Mahdon, M. Creating Public Value: Case Studies; The Work Foundation: London, UK, 2006. [Google Scholar]

- Bozeman, B. Public values theory: Three big questions. Int. J. Public Policy 2009, 4, 369–375. [Google Scholar] [CrossRef]

- Williams, I.; Shearer, H. Appraising public value: Past, present and futures. Public Adm. 2011, 89, 1367–1384. [Google Scholar] [CrossRef]

- Rutgers, M.R. As good as it gets? On the meaning of public value in the study of policy and management. Am. Rev. Public Adm. 2015, 45, 29–45. [Google Scholar] [CrossRef] [Green Version]

- Peda, P.; Argento, D.; Grossi, G. Governance and Performance of a Mixed Public-Private Enterprise: An Assessment of a Company in the Estonian Water Sector. Public Organ. Rev. 2013, 13, 185–196. [Google Scholar] [CrossRef]

- Ricci, P.; Civitillo, R. Italian Public Administration Reform: What are the limits of financial performance measures? In Outcome-Based Performance Management in the Public Sector; Borgonovi, E., Anessi Pessina, E., Bianchi, C., Eds.; Springer International Publishing: Berlin/Heidelberg, Germany, 2017; pp. 121–140. [Google Scholar]

- Bryson, J.; Crosby, B. Public value governance. Public Adm Rev. 2014, 74, 445–456. [Google Scholar] [CrossRef]

- Swilling, M. Reconceptualising urbanism, ecology and networked infrastructures. Soc. Dyn. 2011, 37, 78–95. [Google Scholar] [CrossRef]

- Traxler, A.; Greiling, D. Sustainable public value reporting of electric utilities. Balt. J. Manag. 2018, 14, 103–121. [Google Scholar] [CrossRef]

- Gray, R. Social, Environmental and Sustainability Reporting and Organizational Value Creation: Whose Value? Whose creation? Account. Audit. Account. J. 2006, 19, 793–819. [Google Scholar] [CrossRef]

- Dyllick, T.; Rost, Z. Towards true product sustainability. J. Clean. Prod. 2017, 162, 346–360. [Google Scholar] [CrossRef]

- Farneti, F.; Dumay, J. Sustainable public value inscriptions: A critical approach. In Public Value Management, Measurements and Reporting; Guthrie, J., Marcon, G., Russo, S., Eds.; Emerald Group Publishing: Bingley, UK, 2014; pp. 375–389. [Google Scholar]

- Mahadi, Z.; Sino, H. Defining public needs in sustainable development: A case study of Sepang, Malaysia. Pertanika. J. Soc. Sci. Hum. 2013, 21, 1341–1360. [Google Scholar]

- Todorut, A.V.; Tselentis, V. Digital technologies and the modernization of public administration. Qual. Access Success 2018, 19, 73–78. [Google Scholar]

- Karunasena, K.; Deng, H.; Harasgama, K.S. An investigation of the critical factors for evaluating the public value of e-government: A thematic analysis. In Information Systems and Technology for Organizations in a Networked Society; IGI Global: Hershey, PA, USA, 2013; pp. 1130–1150. [Google Scholar]

- OECD. Report on the Implementation of the OECD Strategy on Development; OECD Publishing: Paris, France, 2014. [Google Scholar]

- Hayashi, M.; Yamamoto, W. Information sharing, neighbourhood demarcation, and yardstick competition: An empirical analysis of intergovernmental expenditure interaction in Japan. Int. Tax Public Financ. 2017, 24, 134–163. [Google Scholar] [CrossRef] [Green Version]

- Cabral, S.; Mahoney, J.; Mcgahan, A.; Potoski, M. Value Creation and Value Appropriation in Public and Non-Profit Organizations. Strateg. Manag. J. 2019, 40, 465–475. [Google Scholar] [CrossRef]

- Häyhtiö, M. Requirements as Operational Metrics?—Case: Finnish Defense Forces. Manag. Prod. Eng. Rev. 2016, 7, 49–61. [Google Scholar] [CrossRef] [Green Version]

- Purvis, B.; Mao, Y.; Robinson, D. Three pillars of sustainability: In search of conceptual origins. Sustain. Sci. 2018, 14, 681–695. [Google Scholar] [CrossRef] [Green Version]

- Allini, A.; Manes Rossi, F.; Hussainey, K. The board’s role in risk disclosure. An exploratory study of Italian listed State-Owned Enterprises. Public Money Manag. 2016, 36, 113–120. [Google Scholar] [CrossRef] [Green Version]

- Dixon, T.H.; Farina, F.; DeMets, C.; Jansma, P.; Mann, P.; Calais, E. Relative motion between the Caribbean and North American plates and related boundary zone deformation from a decade of GPS observations. J. Geophys. Res. Space Phys. 1998, 103, 15157–15182. [Google Scholar] [CrossRef] [Green Version]

- Hossain, M.; Guest, R.; Smith, C. Performance indicators of public private partnership in Bangladesh: An implication for developing countries. Int. J. Prod. Perform. Manag. 2019, 68, 46–68. [Google Scholar] [CrossRef]

- Maxwell, K.; Husain, T. Public Private Partnerships: Building Capacity while Effecting Change. Eval. Progr. Plan. 2005, 28, 349–353. [Google Scholar] [CrossRef]

- Khadaroo, I.; Abdullah, A. Private finance initiative (or public private partnership) implementation processes and perception of value for money. Int. J. Econ. Manag. 2007, 1, 407–435. [Google Scholar]

- Yuan, J.; Li, W.; Xia, B.; Chen, Y.; Skibniewski, M.J. Operation performance measurement of public rental housing delivery by PPPS with fuzzy-AHP comprehensive evaluation. Int. J. Strateg. Prop. Manag. 2019, 23, 328–353. [Google Scholar] [CrossRef]

- Liu, H.J.; Love, P.E.D.; Smith, J.; Matthews, J.; Sing, C.P. Praxis of performance measurement in public-private partnerships: Moving beyond the iron triangle. J. Manag. Eng. 2016, 32, 04016004. [Google Scholar] [CrossRef]

- Liu, H.J.; Love, P.E.D.; Smith, J.; Irani, Z.; Hajli, N.; Sing, M.C.P. From design to operations: A process management life-cycle performance measurement system for Public-Private Partnerships. Prod. Plan. Control 2018, 29, 68–83. [Google Scholar] [CrossRef]

- Cappellaro, G.; Ricci, A. PPPs in health and social services: A performance measurement perspective. Public Money Manag. 2017, 37, 417–424. [Google Scholar] [CrossRef]

- Hashim, H.; Che-Ani, A.I.; Ismail, K. Public Private Partnership (PPP) Project Performance in Malaysia: Identification of Issues and Challenges. Int. J. Supply Chain Manag. 2017, 6, 265–275. [Google Scholar]

- Sundararajan, S.; Tseng, C.-L. Managing Project Performance Risks under Uncertainty: Using a Dynamic Capital Structure Approach in Infrastructure Project Financing. J. Constr. Eng. Manag. 2017, 143, 04017046. [Google Scholar] [CrossRef]

- Klijn, E.-H.; Koppenjan, J. The impact of contract characteristics on the performance of public–private partnerships (PPPs). Public Money Manag. 2016, 36, 455–462. [Google Scholar] [CrossRef] [Green Version]

- English, L.; Baxter, J. The Changing Nature of Contracting and Trust in Public-Private Partnerships: The Case of Victorian PPP Prisons. Abacus 2010, 46, 289–319. [Google Scholar] [CrossRef]

- Motoyama, Y.; Knowlton, K. From resource munificence to ecosystem integration: The case of government sponsorship in St. Louis. Entrep. Reg. Dev. 2016, 28, 448–470. [Google Scholar] [CrossRef]

- Moore, M.H. The Mediation Process: Practical Strategies for Resolving Conflict; Jossey-Bass, A Wiley Brand: San Francisco, CA, USA, 2014. [Google Scholar]

- Guthrie, J.; Marcon, G.; Russo, S.; Farneti, F. Public Value Management, Measurement and Reporting; Emerald Group Publishing: Bingley, UK, 2014. [Google Scholar]

- Northcott, D.; Taulapapa, T. Using the balanced scorecard to manage performance in public sector organizations: Issues and challenges. Int. J. Public Sect. Manag. 2012, 25, 166–191. [Google Scholar] [CrossRef]

- Fadda, I.; Paglietti, P.; Reginato, E.; Pavan, A. Transparency and corruption. Evidences from the case of the Italian regions. In Proceedings of the Cambridge Business & Economics Conference, Cambridge, UK, 1–2 July 2016. [Google Scholar]

- Fadda, I.; Paglietti, P.; Reginato, E.; Pavan, A. Analysing Corruption: Effects on the Transparency of Public Administrations. In Outcome-Based Performance Management in the Public Sector; Borgonovi, E., Anessi-Pessina, E., Bianchi, C., Eds.; Springer International Publishing: Berlin/Heidelberg, Germany, 2018; pp. 251–267. [Google Scholar]

- Mahadi, Z.; Mohamad, R.J.; Sino, H. Public Development Sustainability Values: A Case Study in Sepang Malaysia. Akademika 2017, 87, 31–44. [Google Scholar] [CrossRef] [Green Version]

- Casey, C. Public Values in Governance Networks: Management Approaches and Social Policy Tools in Local Community and Economic Development. Am. Rev. Public Adm. 2015, 45, 106–127. [Google Scholar] [CrossRef]

- Bertot, J.; Estevez, E.; Janowski, T. Universal and contextualized public services: Digital public service innovation framework. Gov. Inf. Q. 2016, 33, 211–222. [Google Scholar] [CrossRef]

- O’Flynn, J. From new public management to public value: Paradigmatic change and managerial implications. Aust. J. Public Adm. 2007, 66, 353–366. [Google Scholar] [CrossRef]

- Guarini, E. Measuring public value in bureaucratic settings: Opportunities and constraints. In Public Value Management, Measurement and Reporting; Guthrie, J., Marcon, G., Russo, S., Farneti, F., Eds.; Emerald Group Publishing: Bingley, UK, 2014; Volume 3, pp. 301–319. [Google Scholar]

- Katamba, D.; Nkiko, C.M.; Kazooba, C.T.; Kemeza, I.; Mpisi, S.B. Community involvement and development: An inter-marriage of ISO 26000 and millennium development goals. Int. J. Soc. Econ. 2014, 41, 837–861. [Google Scholar] [CrossRef]

- Mccann, G.; Mccloskey, S. From the Local to the Global: Key Issues in Development Studies, 3rd ed.; Pluto Press: London, UK, 2015. [Google Scholar]

- Holm, R.; Wandschneider, P.; Felsot, A.; Msilimba, G. Achieving the sustainable development goals: A case study of the complexity of water quality health risks in Malawi. J. Health Popul. Nutr. 2016, 35, 20. [Google Scholar] [CrossRef] [Green Version]

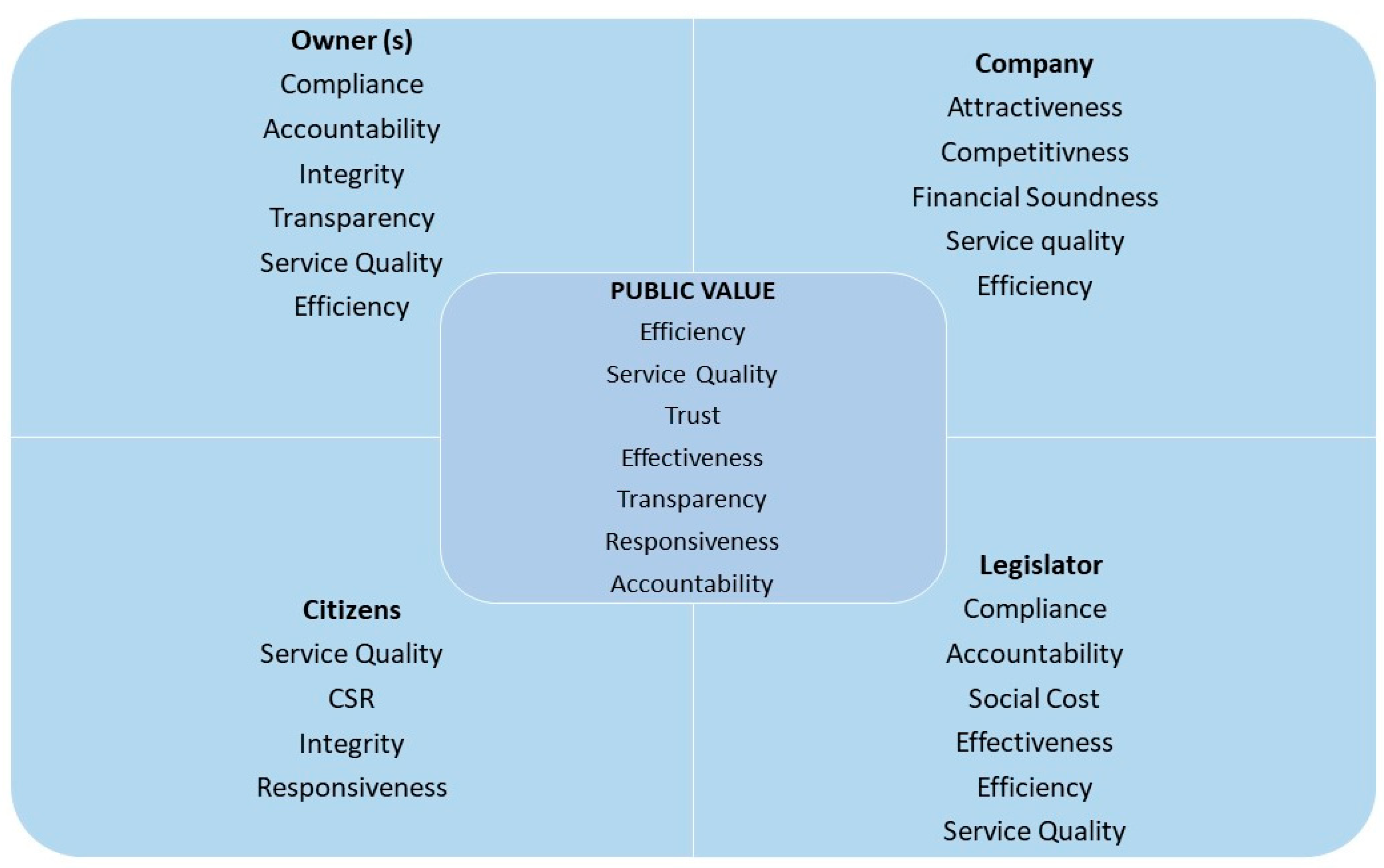

| Stakeholders | Institutional Logics | Performance Expectations | Performance Criteria |

|---|---|---|---|

| Owner(s)/Control role | Politics and bureaucracy | Service quality Efficiency Transparency Probity Accountability Compliance | Provision and price dividend Information No misconduct Control mechanism Respecting rules |

| Municipal company/Strategy role | Corporate governance and market | Service quality Efficiency Competitive Attractive Financially robust | Competent and reliable Profitable Wins contracts Recruits good people Able to invest |

| External stakeholders/Service role | Community | Service quality Responsiveness Probity and decency CSR | Competent and reliable Welcome criticism Behaves properly Supports civic activity |

| Criteria | Description |

|---|---|

| Field: | Business, Management and Accounting |

| Literature Typology: | Pure SLR (excluding grey analysis) |

| Period: | 1995–2019 |

| Groups of keywords: |

|

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Esposito, P.; Dicorato, S.L. Sustainable Development, Governance and Performance Measurement in Public Private Partnerships (PPPs): A Methodological Proposal. Sustainability 2020, 12, 5696. https://doi.org/10.3390/su12145696

Esposito P, Dicorato SL. Sustainable Development, Governance and Performance Measurement in Public Private Partnerships (PPPs): A Methodological Proposal. Sustainability. 2020; 12(14):5696. https://doi.org/10.3390/su12145696

Chicago/Turabian StyleEsposito, Paolo, and Spiridione Lucio Dicorato. 2020. "Sustainable Development, Governance and Performance Measurement in Public Private Partnerships (PPPs): A Methodological Proposal" Sustainability 12, no. 14: 5696. https://doi.org/10.3390/su12145696