The Sustainability of Energy Substitution in the Chinese Electric Power Sector

Abstract

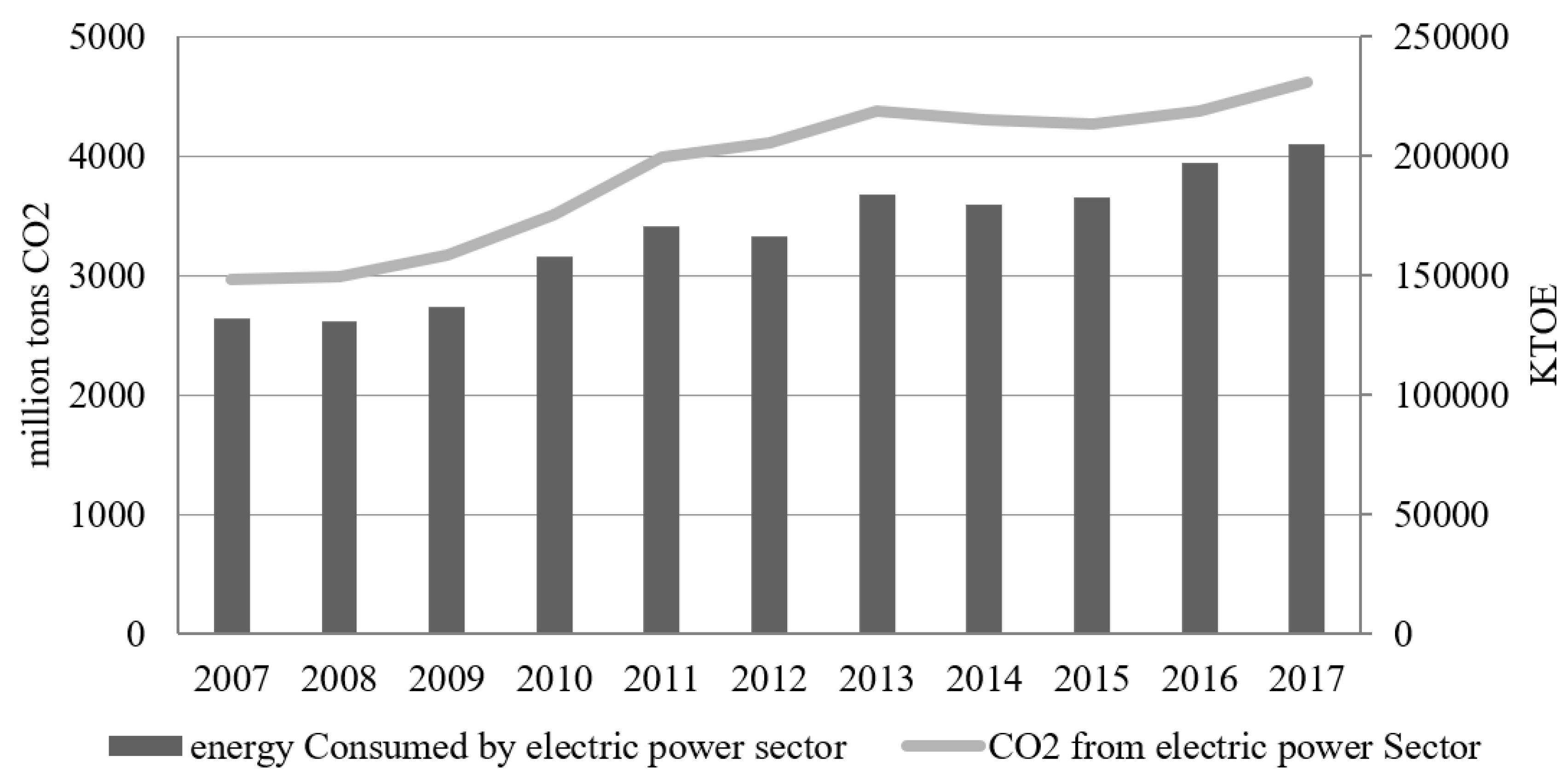

:1. Introduction

2. Literature Review

3. Data and Methodology

4. Methodologies

5. Results and Discussion

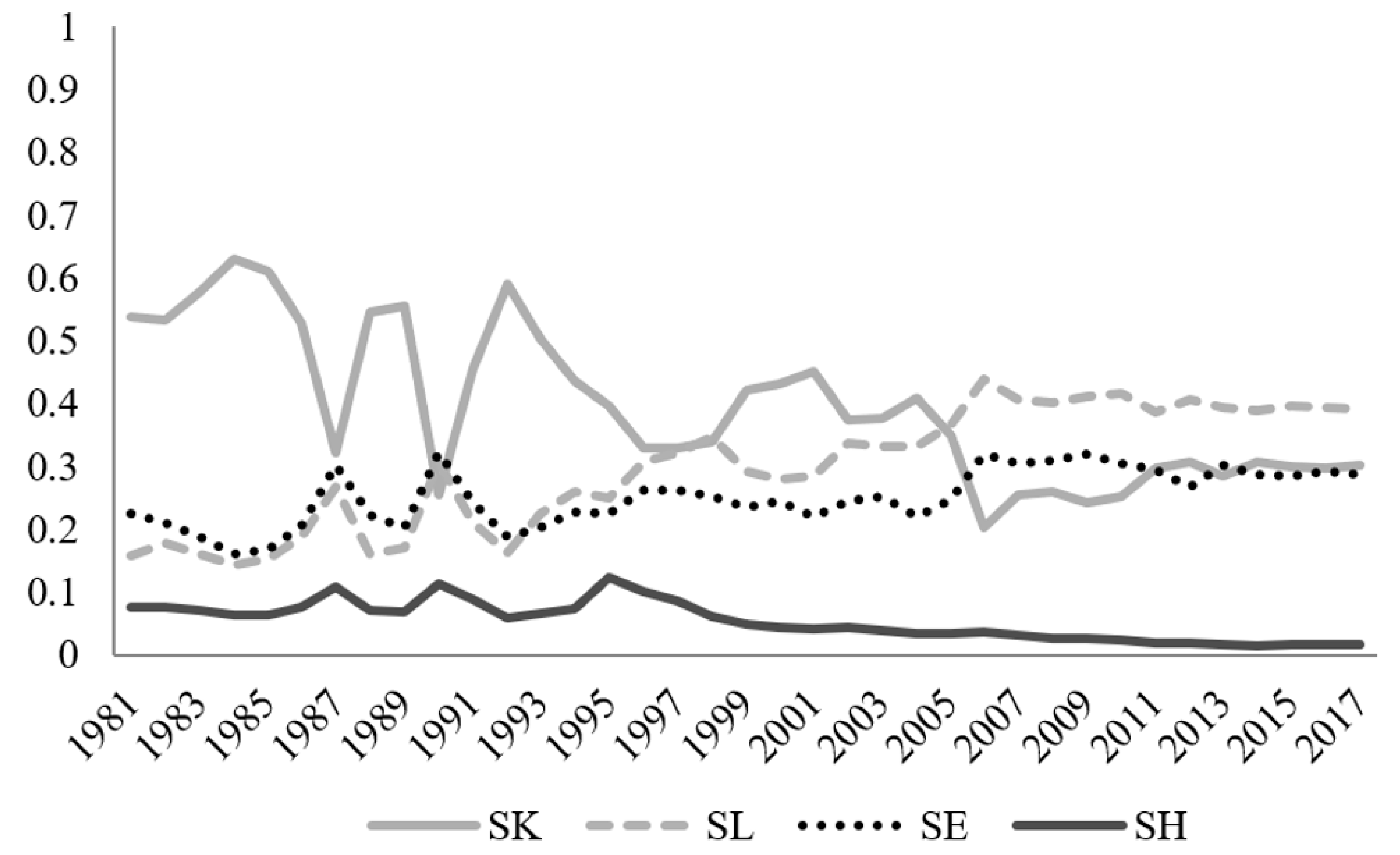

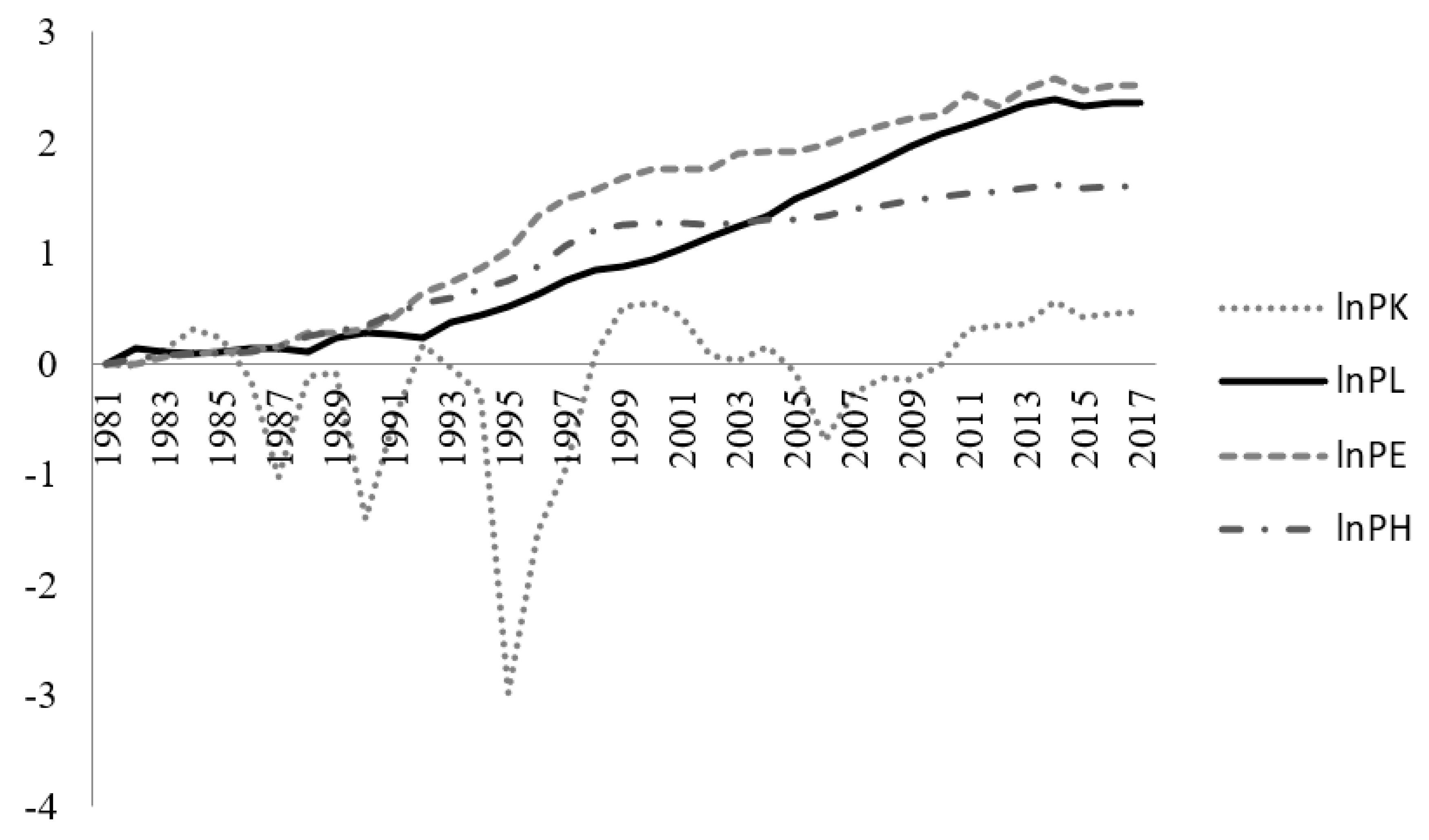

5.1. Estimation Results

5.2. Derived Demand Elasticities

- (i)

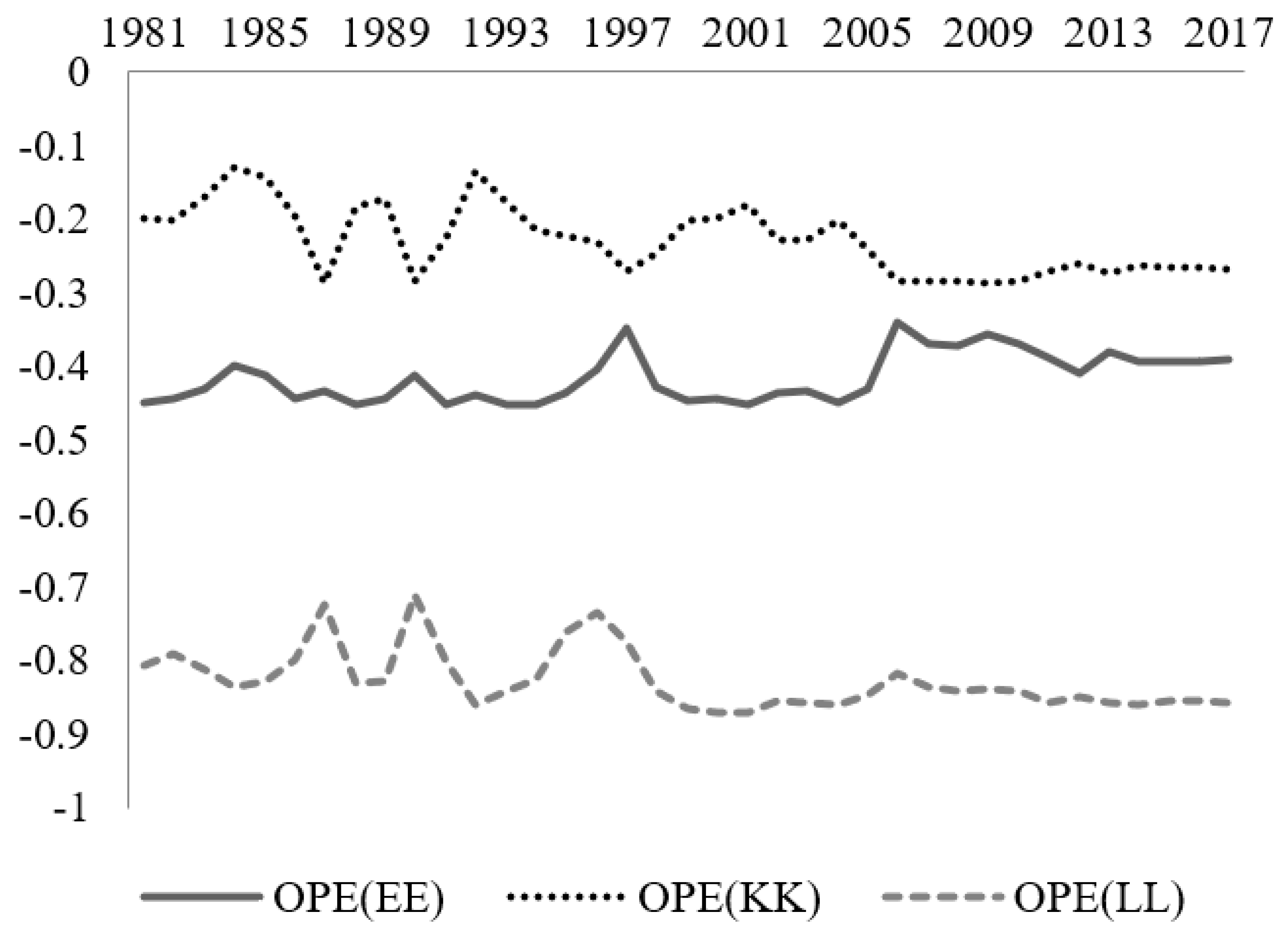

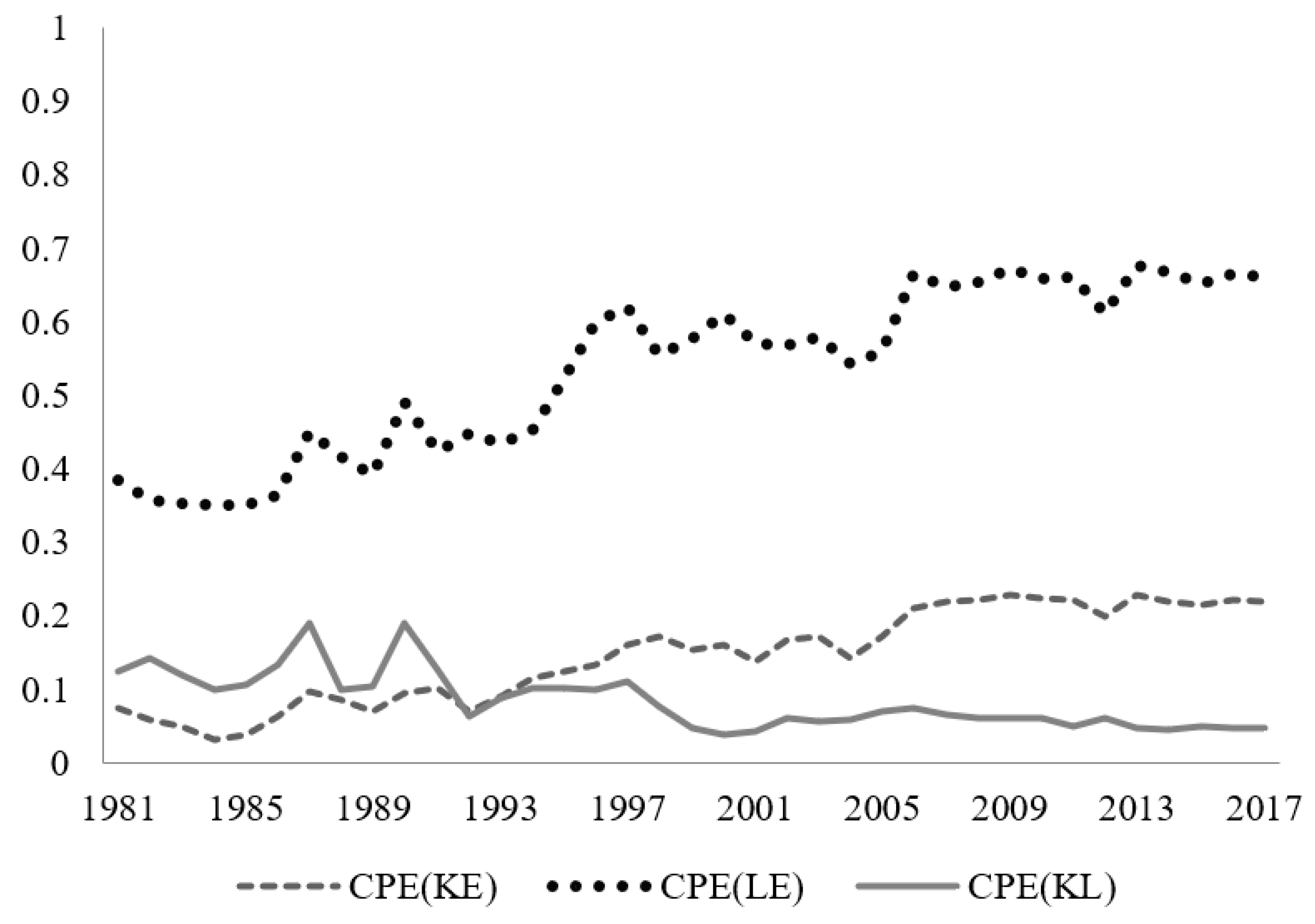

- Consistent with all the existing economic theories, all own-price elasticities have negative signs. Each factor is responsive to the change in its price. The median own-price elasticities for energy, capital and labor are 0.4089, 0.221 and 0.8216, respectively. The demands in both labor and energy are more sensitive to the change in their price than that of capital. The magnitude and direction of the elasticity of own-price have been used in some empirical studies, including Costantini et al. [33] and Sharimakin [3].

- (ii)

- When considering the cross-price elasticities of capital demand, we find positive elasticities with respect to the price of energy. The estimated results of the cross-price elasticities imply that both capital and energy have substantial substitution sustainability, demonstrating a slightly upward trend. This indicates more potential for alleviating energy supply shortages with higher capital investment in China’s electric industry, thus discovering an effective way of saving energy.

- (iii)

- Likewise, we find positive elasticities with respect to the price of energy regarding the cross-price elasticities of labor demand, inferring that both energy and labor appear to be significantly substitutable. Additionally, both labor and capital are substitutes with values for the cross-price elasticities of substitution at 0.0873. Substitution between energy and labor necessarily arises from technical innovation, in the context that technological development brings the mechanization and automation of the electric industry and enables many things that were originally done manually to be accomplished with more energy consumption, setting some surplus labor free.

- (iv)

- As can be noted, labor demand is more sensitive to the energy price change than capital, for a median CPE(KE) of 0.1337 and a median CPE(LE) of 0.5336. Compared with overseas countries such as the US, there is less potential for energy substitution when the price of energy rises [34].

- (i)

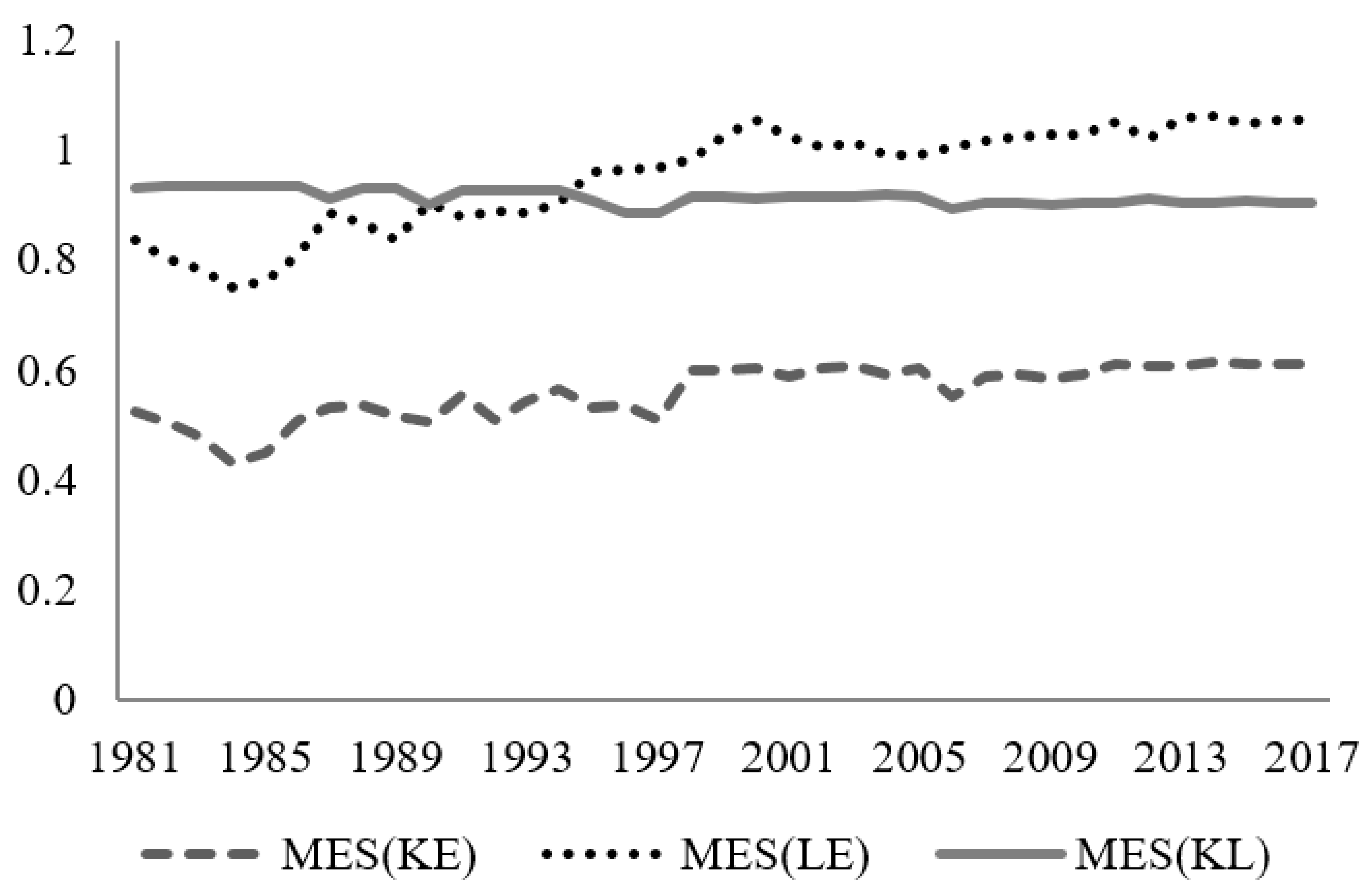

- The estimated results imply that both capital and energy are substitutable, and similarly, labor is also a substitute for energy, indicating that both capital and labor demand are elastic to changes in energy price.

- (ii)

- The Morishima elasticities outnumber the corresponding cross-price elasticities in general, especially for capital and labor. The result is consistent with the findings of Koetse et al. [9], who found a distinction between Morishima elasticities and cross-price elasticities.

- (iii)

- Labor demand is more sensitive to energy-price change than capital, because MES(KE) = 0.5408 and MES(LE) = 0.9426, inferring that holding other variables constant, energy prices increase 1%, and the demand ratio for both capital–energy and labor–energy will rise 0.5408% and 0.9426%, respectively.

- (iv)

5.3. Scenario Analysis

5.4. The Role of Human Capital in Inter-Factor Substitution

- (i)

- Both capital and energy are substitutable, and similarly, labor is substantially substitutable with energy.

- (ii)

- In general, the Morishima elasticities of labor outnumber the corresponding Morishima elasticities of capital.

- (iii)

- Compared with the Morishima elasticities between the two cost-share equations, both labor and capital demand are more sensitive to energy-price change in the four-factor model, because both MES(KE) * and MES(LE) * increase by 23.96 and 12.31 points, respectively. This shows that human capital does contribute to both China’s energy conservation and emissions reduction, and that it is useful to raise the factor elasticity of substitution, and optimize resource allocation and utilization.

- (iv)

- Human capital is a significant substitute to energy itself, with a median Morishima elasticity of 1.0522. This shows that human capital is more substitutable to energy than capital.

6. Conclusions and Implications

Author Contributions

Funding

Conflicts of Interest

References

- Abid, F.; Leung, P.L.; Mroua, M.; Wong, W.K. International diversification versus domestic diversification: Mean-variance portfolio optimization and stochastic dominance approaches. J. Risk Financ. Manag. 2014, 7, 45–66. [Google Scholar] [CrossRef]

- Apostolakis, B.E. Energy–Capital substitutability/complementarity: The dichotomy. Energy Econ. 1990, 12, 48–58. [Google Scholar] [CrossRef]

- Safarzadeh, S.; Rasti-Barzoki, M.; Hejazi, S.R. A review of optimal energy policy instruments on industrial energy efficiency programs, rebound effects, and government policies. Energy Policy 2020, 139, 111342. [Google Scholar] [CrossRef]

- Berndt, E.R.; Wood, D.O. Technology, prices, and the derived demand for energy. Rev. Econ. Stat. 1975, 57, 259–268. [Google Scholar] [CrossRef]

- Munkh-Ulzii, B.J.; McAleer, M.; Moslehpour, M.; Wong, W.K. Confucius and Herding Behaviour in the Stock Markets in China and Taiwan. Sustainability 2018, 10, 4413. [Google Scholar] [CrossRef] [Green Version]

- Christopoulos, D.K.; Tsionas, E.G. Allocative inefficiency and the capital-energy controversy. Energy Econ. 2002, 24, 305–318. [Google Scholar] [CrossRef]

- Arnberg, S.; Bjorner, T.B. Substitution between energy, capital and labor within industrial companies: A micro panel data analysis. Resour. Energy Econ. 2007, 29, 122–136. [Google Scholar] [CrossRef]

- Welsch, H.; Ochsen, C. The determinants of aggregate energy use in west Germany: Factor substitution, technological change, and trade. Energy Econ. 2005, 27, 93–111. [Google Scholar] [CrossRef]

- Koetse, M.J.; De Groot, H.L.; Florax, R.J. Capital-energy substitution and shifts in factor demand: A meta-analysis. Energy Econ. 2008, 30, 2236–2251. [Google Scholar] [CrossRef] [Green Version]

- Lin, B.Q.; Xie, C.P. Energy substitution effect on transport industry of China-based on trans-log production function. Energy 2014, 67, 213–222. [Google Scholar] [CrossRef]

- Halvorsen, R.; Ford, J. Substitution among energy, capital and labour inputs in U.S. manufacturing. In Capital and Labour Inputs in U.S. Manufacturing. Advances in the Economics of Energy and Resources 1; Pindyck, R.S., Ed.; Jai Press: Greenwich, CT, USA, 1978. [Google Scholar]

- Field, B.C.; Grebenstein, C. Capital-Energy substitution in U.S. manufacturing. Rev. Econ. Stat. 1980, 62, 207–212. [Google Scholar] [CrossRef]

- Frondel, M.; Schmidt, C.M. The Real Elasticity of Substitution: An Obituary; Discussion paper No. 341; Department of Economics, University of Heidelberg: Heidelberg, Germany, 2000; Available online: www.uni-heidelberg.de/institute/fak18/publications/papers/dp341.pdf (accessed on 15 April 2020).

- Kander, A.; Schön, L. The energy-capital relation of Sweden 1870–2000. Struct. Chang. Econ. Dyn. 2007, 18, 291–305. [Google Scholar] [CrossRef] [Green Version]

- Presley, K.W.; Lin, B.; Appiah, M.O. Delving into Liberia’s energy economy: Technical change, inter-factor and inter-fuel substitution. Renew. Sustain. Energy Rev. 2013, 24, 122–130. [Google Scholar]

- Guo, J.; Guo, C.H.; Ling, Y. Energy rebound effect of the industrial sector in China. Quant. Tech. Econ. Res. 2010, 11, 114–126. [Google Scholar]

- Ma, H.; Oxley, L.; Gibson, J. China’s energy economy: A survey of the literature. Econ. Syst. 2010, 34, 105–132. [Google Scholar] [CrossRef]

- Lu, C.J.; Zhou, D.M. The positive demonstration of energy substitution on China: Based on the revision of the model of Allen Substitution. Quant. Tech. Econ. Res. 2008, 5, 30–42. [Google Scholar]

- Su, X.M.; Zhou, W.S.; Nakagami, K.I.; Ren, H.B.; Mu, H.L. Capital stock-labor-energy substitution and production efficiency study for China. Energy Econ. 2012, 34, 1208–1213. [Google Scholar] [CrossRef]

- He, Y.; Lin, B. Heterogeneity and asymmetric effects in energy resources allocation of the manufacturing sectors in China. Energy 2019, 170, 1019–1035. [Google Scholar] [CrossRef]

- Wei, Z.; Han, B.; Han, L.; Shi, Y. Factor substitution, diversified sources on biased technological progress and decomposition of energy intensity in China’s high-tech industry. J. Clean. Prod. 2019, 231, 87–97. [Google Scholar] [CrossRef]

- Jiao, B.; Jiao, Z. Estimation of China’s human capital stock: 1978–2007. Economist 2010, 9, 27–33. [Google Scholar]

- Chiang, T.C.; Lean, H.H.; Wong, W.K. Do REITs Outperform Stocks and Fixed-Income Assets? New Evidence from Mean-Variance and Stochastic Dominance Approaches. J. Risk Financ. Manag. 2008, 1, 1–37. [Google Scholar] [CrossRef] [Green Version]

- Lean, H.H.; McAleer, M.; Wong, W.K. Market efficiency of oil spot and futures: A mean-variance and stochastic dominance approach. Energy Econ. 2010, 32, 979–986. [Google Scholar] [CrossRef] [Green Version]

- Hicks, J.R. The Theory of Wages; Macmillan: London, UK, 1932. [Google Scholar]

- Allen, R.G.D.; Hicks, J.R. A reconsideration of the theory of value. Economica 1934, 1, 52–76. [Google Scholar]

- Blackorby, C.; Russell, R.R. The Partial Elasticity of Substitution; Discussion paper No. 75–1, economics; University of California: San Diego, CA, USA, 1975. [Google Scholar]

- Thompson, P.; Taylor, T.G. The capital-energy substitutability debate: A new look. Rev. Econ. Stat. 1995, 77, 565–569. [Google Scholar] [CrossRef]

- Li, Z.X.; Li, X.G.; Hui, Y.C.; Wong, W.K. Maslow Portfolio Selection for Individuals with Low Financial Sustainability. Sustainability 2018, 10, 1128. [Google Scholar] [CrossRef] [Green Version]

- Lean, H.H.; McAleer, M.; Wong, W.K. Preferences of risk-averse and risk-seeking investors for oil spot and futures before, during and after the Global Financial Crisis. Int. Rev. Econ. Financ. 2015, 40, 204–216. [Google Scholar] [CrossRef]

- Nguyen, S.V.; Reznek, A.P. Factor substitution in small and large U.S. manufacturing establisnments. Small Bus. Econ. 1993, 5, 37–54. [Google Scholar] [CrossRef]

- Cheng, A.W.W.; Chow, N.S.C.; Chui, D.K.H.; Wong, W.K. The Three Musketeers relationships between Hong Kong, Shanghai and Shenzhen before and after Shanghai-Hong Kong Stock Connect. Sustainability 2019, 11, 3845. [Google Scholar] [CrossRef] [Green Version]

- Costantini, V.; Crespi, F.; Paglialunga, E. Capital–energy substitutability in manufacturing sectors: Methodological and policy implications. Eurasian Bus. Rev. 2019, 9, 157–182. [Google Scholar] [CrossRef]

- Shaik, S.; Yeboah, O.A. Does climate influence energy demand? A regional analysis. Appl. Energy 2018, 212, 691–703. [Google Scholar] [CrossRef]

- Lv, Z.H.; Chu, A.M.Y.; McAleer, M.; Wong, W.K. Modelling Economic Growth, Carbon Emissions, and Fossil Fuel Consumption in China: Cointegration and Multivariate Causality. Int. J. Environ. Res. Public Health 2019, 16, 4176. [Google Scholar] [CrossRef] [Green Version]

- Lean, H.H.; Phoon, K.F.; Wong, W.K. Stochastic dominance analysis of CTA funds. Rev. Quant. Financ. Account. 2013, 40, 155–170. [Google Scholar] [CrossRef] [Green Version]

- Woo, C.K.; Wong, W.K.; Horowitz, I.; Chan, H.L. Managing a scarce resource in a growing Asian economy: Water usage in Hong Kong. J. Asian Econ. 2012, 23, 374–382. [Google Scholar] [CrossRef]

- Guo, X.; Wong, W.K.; Xu, Q.F.; Zhu, L.X. Production and Hedging Decisions under Regret Aversion. Econ. Model. 2015, 51, 153–158. [Google Scholar] [CrossRef]

- Guo, X.; Li, G.-R.; McAleer, M.; Wong, W.K. Specification Testing of Production in a Stochastic Frontier Model. Sustainability 2018, 10, 3082. [Google Scholar] [CrossRef] [Green Version]

- Guo, X.; Wong, W.K. Comparison of the production behaviour of regret-averse and purely risk-averse firms. Estud. Econ. 2019, 46, 157–171. [Google Scholar]

- Guo, X.; Egozcue, M.; Wong, W.K. Production theory under price uncertainty for firms with disappointment aversion. Int. J. Prod. Res. 2020. forthcoming. [Google Scholar] [CrossRef]

- Moslehpour, M.; Pham, V.K.; Wong, W.-K.; Bilgiçli, İ. E-Purchase Intention of Taiwanese Consumers: Sustainable Mediation of Perceived Usefulness and Perceived Ease of Use. Sustainability 2018, 10, 234. [Google Scholar] [CrossRef] [Green Version]

- Moslehpour, M.; Altantsetseg, P.; Mou, W.M.; Wong, W.K. Organizational Climate and Work Style: The Missing Links for Sustainability of Leadership and Satisfied Employees. Sustainability 2019, 11, 125. [Google Scholar] [CrossRef] [Green Version]

- Mou, W.M.; Wong, W.K.; McAleer, M. Financial Credit Risk Evaluation Based on Core Enterprise Supply Chains. Sustainability 2018, 10, 3699. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, H.M.; Vuong, T.H.G.; Nguyen, T.H.; Wu, Y.C.; Wong, W.K. Sustainability of Both Pecking Order and Trade-off Theories in Chinese Manufacturing Firms. Sustainability 2020, 12, 3883. [Google Scholar] [CrossRef]

- Demirer, R.; Gupta, R.; Lv, Z.H.; Wong, W.K. Equity Return Dispersion and Stock Market Volatility: Evidence from Multivariate Linear and Nonlinear Causality Tests. Sustainability 2019, 11, 351. [Google Scholar] [CrossRef] [Green Version]

- Gupta, R.; Lv, Z.H.; Wong, W.K. Macroeconomic Shocks and Changing Dynamics of the U.S. REITs Sector. Sustainability 2019, 11, 2776. [Google Scholar] [CrossRef] [Green Version]

- Levy, H. The Investment Home Bias with Peer Effect. J. Risk Financ. Manag. 2020, 13, 94. [Google Scholar] [CrossRef]

- Yuan, X.; Tang, J.; Wong, W.-K.; Sriboonchitta, S. Modeling Co-Movement among Different Agricultural Commodity Markets: A Copula-GARCH Approach. Sustainability 2020, 12, 393. [Google Scholar] [CrossRef] [Green Version]

- Wong, W.K.; Lean, H.H.; McAleer, M.; Tsai, F.T. Why are Warrant Markets stained in Taiwan but not in China? Sustainability 2018, 10, 3748. [Google Scholar] [CrossRef] [Green Version]

- Clark, E.A.; Qiao, Z.; Wong, W.K. Theories of risk: Testing investor behaviour on the Taiwan stock and stock index futures markets. Econ. Inq. 2016, 54, 907–924. [Google Scholar] [CrossRef] [Green Version]

- Qiao, Z.; Clark, E.; Wong, W.K. Investors’ preference towards risk: Evidence from the Taiwan stock and stock index futures markets. Account. Financ. 2014, 54, 251–274. [Google Scholar] [CrossRef]

- Qiao, Z.; Wong, W.K.; Fung, J.K.W. Stochastic dominance relationships between stock and stock index futures markets: International evidence. Econ. Model. 2013, 33, 552–559. [Google Scholar] [CrossRef]

- Woo, K.Y.; Mai, C.; McAleer, M.; Wong, W.K. Review on Efficiency and Anomalies in Stock Markets. Economies 2020, 8, 20. [Google Scholar] [CrossRef] [Green Version]

- Chang, C.-L.; McAleer, M.; Wong, W.K. Big Data, Computational Science, Economics, Finance, Marketing, Management, and Psychology: Connections. J. Risk Financ. Manag. 2018, 11, 15. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Coefficient | Regression Estimate | Standard Error |

|---|---|---|

| 0.6687 ** | 0.0140 | |

| 0.1122 a | - | |

| 0.2191 ** | 0.0160 | |

| 0.1268 ** | 0.0270 | |

| 0.0036 a | - | |

| 0.0746 ** | 0.0170 | |

| −0.0279 a | - | |

| −0.0989 ** | 0.0177 | |

| 0.0243 a | - |

| Year | Scenario 1: Capital Increased by 5% | Scenario 2: Capital Increased by 10% | ||

|---|---|---|---|---|

| Energy Savings (Mtoe) | CO2 Emission Reduction (Million Metric Tons) | Energy Savings (Mtoe) | CO2 Emission Reduction (Million Metric Tons) | |

| 2014 | 8.98 | 22.27 | 17.96 | 44.54 |

| Year | MES(KE) * | Rate of Change (%) | MES(LE) * | Rate of Change (%) | MES(HE) * |

|---|---|---|---|---|---|

| 1981 | 0.7235 | 37.9935 | 1.1828 | 41.7715 | 1.067 |

| 1982 | 0.7114 | 41.0668 | 1.1352 | 41.4403 | 1.053 |

| 1983 | 0.6984 | 45.5910 | 1.1459 | 46.1794 | 1.0303 |

| 1984 | 0.6725 | 56.2863 | 1.1531 | 53.9931 | 1 |

| 1985 | 0.6807 | 51.6711 | 1.1381 | 49.3962 | 1.0087 |

| 1986 | 0.7057 | 39.1364 | 1.1109 | 37.2837 | 1.048 |

| 1987 | 0.6955 | 31.0286 | 1.084 | 22.7216 | 1.1354 |

| 1988 | 0.723 | 34.7623 | 1.1789 | 35.8649 | 1.0641 |

| 1989 | 0.7095 | 37.9009 | 1.1409 | 36.2920 | 1.0445 |

| 1990 | 0.6573 | 29.7730 | 1.0635 | 17.7480 | 1.1529 |

| 1991 | 0.7172 | 29.3417 | 1.1086 | 26.6248 | 1.0838 |

| 1992 | 0.6988 | 37.2888 | 1.1419 | 28.7228 | 1.0242 |

| 1993 | 0.699 | 29.0382 | 1.0614 | 19.8374 | 1.0439 |

| 1994 | 0.7022 | 23.9541 | 1.049 | 16.0398 | 1.0713 |

| 1995 | 0.5617 | 127.2249 | 1.0245 | 6.8300 | 1.2144 |

| 1996 | 0.4211 | 25.4768 | 1.0321 | 6.9312 | 1.1995 |

| 1997 | 0.558 | 9.6698 | 1.0105 | 4.3043 | 1.1545 |

| 1998 | 0.6798 | 13.3189 | 1.0102 | 2.7984 | 1.0897 |

| 1999 | 0.7021 | 17.2120 | 1.0295 | 0.6649 | 1.0606 |

| 2000 | 0.7112 | 17.7094 | 1.0445 | 0.8919 | 1.0583 |

| 2001 | 0.7004 | 18.9740 | 1.0233 | 0.0685 | 1.0273 |

| 2002 | 0.6917 | 14.6337 | 1.0115 | 0.8073 | 1.059 |

| 2003 | 0.6967 | 15.0050 | 1.0176 | 0.4144 | 1.0533 |

| 2004 | 0.688 | 16.2948 | 0.9957 | 0.4844 | 1.0068 |

| 2005 | 0.6824 | 13.4120 | 0.9988 | 0.8889 | 1.0332 |

| 2006 | 0.5997 | 8.8385 | 1.0089 | 0.2584 | 1.1162 |

| 2007 | 0.6513 | 10.5210 | 1.013 | 0.5107 | 1.0756 |

| 2008 | 0.6576 | 10.9312 | 1.0161 | 0.9359 | 1.0597 |

| 2009 | 0.6445 | 10.5299 | 1.0169 | 1.1471 | 1.0564 |

| 2010 | 0.6495 | 9.7314 | 1.0089 | 1.7241 | 1.0188 |

| 2011 | 0.6785 | 11.2660 | 1.0155 | 3.3041 | 0.9534 |

| 2012 | 0.6707 | 10.4215 | 0.9947 | 2.3943 | 0.9235 |

| 2013 | 0.6742 | 10.9064 | 1.0164 | 3.7409 | 0.9173 |

| 2014 | 0.6809 | 10.9138 | 1.0113 | 4.6573 | 0.8704 |

| 2015 | 0.6753 | 10.7472 | 1.0075 | 3.5975 | 0.9037 |

| 2016 | 0.6768 | 10.8558 | 1.0117 | 3.9986 | 0.8971 |

| 2017 | 0.6777 | 10.8389 | 1.0102 | 4.0845 | 0.8904 |

| Mean | 0.6709 | 25.4126 | 1.0547 | 14.3068 | 1.0396 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, Y.; Xia, Y.; Wu, Y.-C.; Wong, W.-K. The Sustainability of Energy Substitution in the Chinese Electric Power Sector. Sustainability 2020, 12, 5463. https://doi.org/10.3390/su12135463

Li Y, Xia Y, Wu Y-C, Wong W-K. The Sustainability of Energy Substitution in the Chinese Electric Power Sector. Sustainability. 2020; 12(13):5463. https://doi.org/10.3390/su12135463

Chicago/Turabian StyleLi, Ying, Yue Xia, Yang-Che Wu, and Wing-Keung Wong. 2020. "The Sustainability of Energy Substitution in the Chinese Electric Power Sector" Sustainability 12, no. 13: 5463. https://doi.org/10.3390/su12135463