1. Introduction

Permanent grassland systems contain the most biodiverse habitats of Central Europe [

1]. They are also a central field of action for climate protection [

2,

3]. In Germany, grassland area covered 4.7 Mio ha or 28% of agricultural land in 2015 [

4]. Milk production from cattle is by far the most important exploiter of grassland biomass growth and is the most important branch of German agriculture. The value of Germany’s agricultural production was 52.75 billion euro in 2018 of which dairying accounted for 10.4 billion euro [

5,

6]. The market for milk thus has a high significance for resource conservation on grassland. Alongside retailers, consumers and agricultural policy, dairies are important market influencers.

Germany is the largest milk producer in the EU-28, producing about one fifth of the total milk output (156 million tonnes) [

7]. In 2018, German dairies processed 34 million tonnes of milk (of which 2.3 million tonnes were imported). Around 16.6 million tonnes of processed milk products were destined for export, 17.4 million tonnes for domestic consumption and a further 12.2 million tonnes of milk products were imported for the German market [

8].

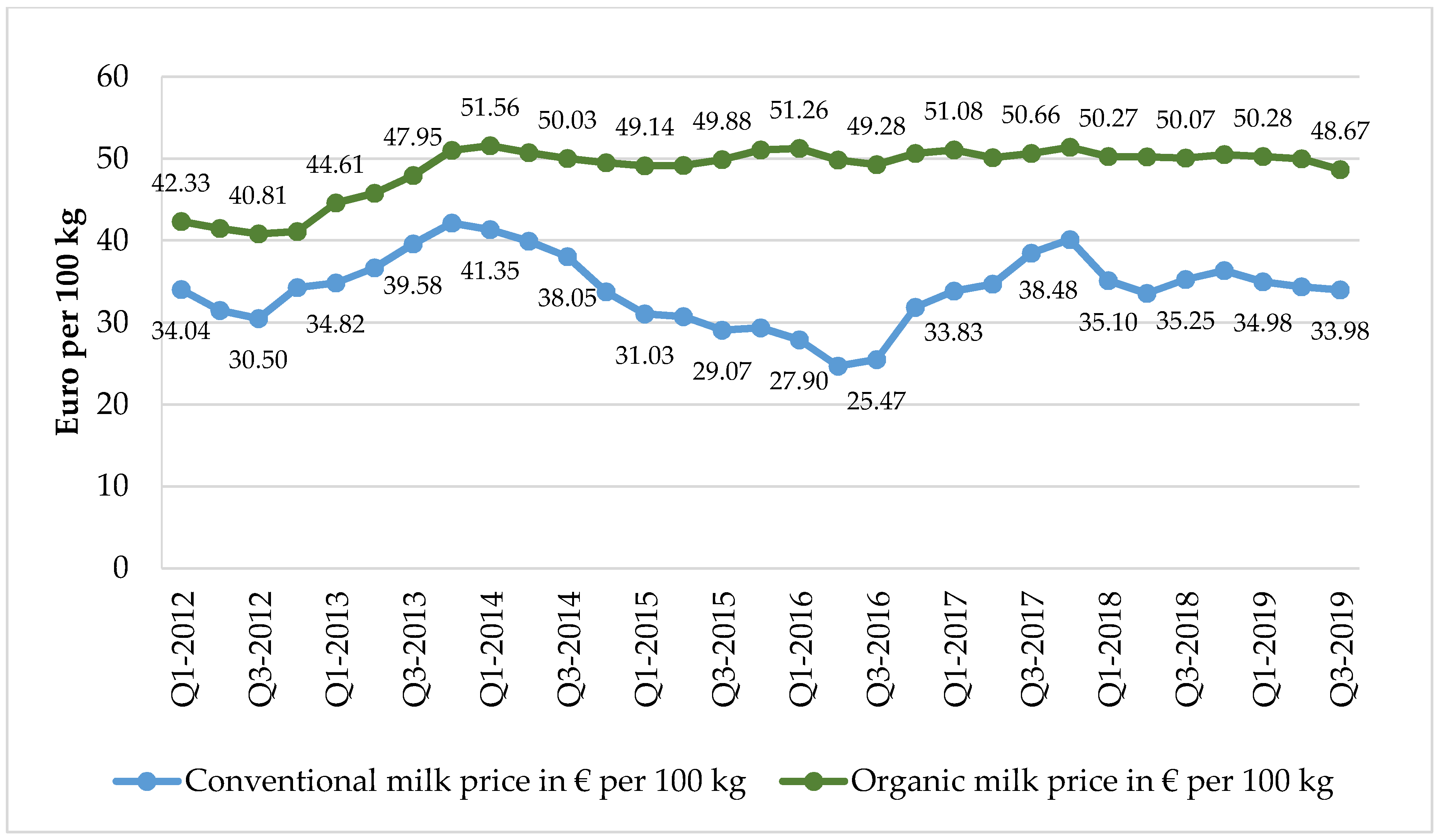

Developments in the globalised dairy market have been problematic for dairy farmers in recent years. For average German production, milk producer incomes (adjusted for subsidies) have not covered costs in any of the last ten years (

Figure 1). Added to this is the volatility of prices in the conventional production sector. So far, organic prices have been more stable in comparison (

Figure 2). However, fiercer price competition is to be expected in the future. Due to a wave of organic conversion resulting from the price crisis, 20% more organic milk has been produced in Germany over the last three years compared to previous levels. German organic milk producers are not able to cover their costs only by selling milk. Incomes primarily depend on subsidies from the first pillar of the Common Agriculture Policy of the EU (CAP)—direct payments account for 42% of farmer’s annual income between 2011–2015 [

9].

In the year 2000, there were still about 138,500 active milk producers in Germany; by 2018, there were only 62,813 [

13]. The unfavourable market situation led a growth in the number of expanded, over-indebted business, co-existing with small and part-time businesses in more deprived regions (

Figure 3) [

14]. At the same time, the total number of dairy cows decreased from around 4.57 million in 2000 to around 4.1 million [

15] and remains nearly unchanged since 2008 [

16]. The dairy cows are, therefore, concentrated on ever-fewer and ever-larger farms resulting in an increased stocking density on those farms, with implications for resource conservation (e.g., widespread eutrophication) [

17].

In the context of the nature conservation of grasslands, it is significant that these developments were accompanied by an increase in milk production per dairy cow, which in turn is attributable to a change in feed and grassland management (more concentrates, silage, intensive ryegrass meadows) and increases in performance due to breeding (

Figure 4). High-yielding breeds such as the German Holstein, which account for about 46% of all pure-bred dairy cows [

16], rely on high-energy feed. The intensification was accompanied by an increasing, but not more quantifiable, period of housing for the animals. According to Reijs et al., this trend is set to continue [

18]. In Germany, according to a survey carried out ten years ago, around 42% of dairy cattle grazed for an average of five months in the field [

19]. This value is certainly lower today.

Feed costs are and will remain a central economic factor. The energetic resource base for milk—despite high proportions of concentrated feed—continues to be grassland, which has important effects on both quantitative and qualitative aspects of nature conservation on grasslands. In the current milk production system described above, however, dairy cows are less and less available as grassland utilisers—especially as grazing animals—from a national perspective.

Only on the small number of dairy farms that today, contrary to the general trend, rely economically on low-input systems with lower milk yield levels, grassland use and grazing remain very much the focus [

21]. Pure natural grassland with (very) poor forage values (e.g., Nardus grassland, dwarf-shrub heathland) is, however, irrelevant for these farms as well; in exceptional cases, young stock may still be driven to areas with such poor forage values (see [

22]).

Structural change has also affected the wider dairy industry. In 1950, there were still 3401 milk processing companies in Germany with at least 20 employees. In 2018, statistics show that just 210 diaries remain [

23].

Market forces drive the behaviour of the dairy industry. On the other hand, dairies are a market force themselves. Dairies are embedded in the value chain between the production and sale of dairy products as (further) processing companies. Only in theory can a dairy farm decide freely to which dairy it sells its raw milk; in practice, catchment areas and the location of the farm largely determine the choice of dairy. Very long contractual commitments and the obligation to sell to the dairy in the region exacerbate this problem. As a result, producers are also not so indirectly tied to the dairy’s production requirements.

In other words, the dairies’ assessment of their markets and their resulting competitiveness strategies have a significant impact on farm operations and thus on the management of grassland. Current examples are the pasture and hay milk programmes designed and promoted by some dairies (see below).

A better understanding of the behaviour of market participants can contribute to more effective policy advice and design (see [

24]). The goal of our work was:

- (1)

Generation of insights on the state, of current developments in and the future of the production system as a direct influencing factor of German grassland management from the perspective of dairying. The following topics are of interest for this: characteristics of German dairies, interaction with suppliers, grazing management programmes/offers regarding grazing management, market developments with regard to nature and conservation-related production conditions, assessment of key market players.

- (2)

The aim was also to test the following hypotheses:

- (i)

The size of the dairy, measured in kg of milk processed per day, has an influence on the assessment of market-regulating parameters (production, processing, sales, policies) and the development of consumer needs.

- (ii)

The size of the dairy correlates with positive market behaviour in terms of grassland nature conservation.

2. Methods

An anonymous, standardised online survey of German dairies with a daily throughput of at least 5000 kg (farm dairies excluded) was carried out between July 2016 and November 2017. The complete questionnaire can be found in the Annex. The questions were developed in conjunction with experts with a practical and scientific background. The invitation to participate was sent by e-mail to the management of each dairy.

In Germany, a complete list of dairies does not exist; this had to be created first. Diaries have an interest in merchandising; it is therefore a reasonable assumption that they use an online presence as a tool to market themselves, and that they provide contact information on their website. This was the basis of our database. Dairies’ websites were identified via Google searches using the terms “dairy”, “cheese dairy”, “milk processing” (original German: “Molkerei”, “Meierei”, “Käserei”, “Milchverarbeitung”). We did not try to cover dairies which purchase milk from German farms but have no processing operations in Germany. In order to avoid duplicate surveys of companies with several plants, we only contacted the main place of business, which can be determined by checking the imprint on identified websites. This explains the differences between the number of identified dairies written to (159) and the total number of milk processing plants (210 in 2018, see above). The majority of experts recommended not putting the promised anonymity in question by asking overly detailed questions about the company structure, so the question of the legal structure of the dairies was not raised.

The questionnaire comprised 30 questions with five predominantly ordinally and some nominally-scaled possible answers. Questions were grouped according to the research objectives.

The answer to hypothesis (2) (i) results from the accumulation of the answers to eight individual questions about current and future consumer needs with regard to grazing livestock farming, regionality and the role of the retail trade and other market participants (consumers, policymakers, producer associations, producers, dairies).

To answer research question (2) (ii), the variable “positive market behaviour” must be defined. This can be derived approximately from the answers to the six questions concerning the entrepreneurial promotion of extensive pastures, the management of certifications and the promotion of corresponding product lines (current and future). Also relevant in regard to the hypothesis test were answers to the question of differentiating the prices paid to dairy farms: for example, a dairy that supports both a high proportion of hay and certification with a higher payment in this way acts positively with regard to grassland nature conservation.

The sample was not normally distributed with regard to dairy sizes; therefore, the hypotheses of (2) were tested with the Spearman rank correlation coefficient. We used Unipark software from Questback (Cologne, Germany) to develop and execute the survey and SPSS 24 for statistics.

3. Results of the Dairy Survey

3.1. Description of the Participating Dairies

Of 159 companies contacted, between 35 (= 22% of dairies contacted) and 47 (= 29.6%) responded, depending on the question, hereinafter “Navailable”). Many dairies declined the invitation to participate in the survey on the basis that participation would take too long.

The field of survey participants is normally distributed according to the “number of employees” characteristic; big players in the industry also took part in the survey (

Table 1). The dairy size of the survey participants is defined by the quantity of milk processed daily (N

available = 35). The top producer in the survey processed 4.5 million kg of milk per day, the smallest dairy 5000 kg/day. The median of the participant field was 425,000 kg/day. The 1st quartile (

p = 0.25) is 30,000 kg/day, the 3rd (

p = 0.75) at 120,000 kg/day. Twelve dairies did not provide any information on the daily processing volume.

Fourteen dairies stated that they purchased milk from only one federal state, eleven from two, two from three and eight from more than three federal states (Navailable = 35). Four dairies also purchased milk from other EU countries. As a delivery region, all territorial states were represented: Bavaria was most frequently named (N = 19), followed by Baden-Württemberg (13), Lower Saxony (eight) and Hesse, North Rhine-Westphalia and Thuringia (six each). Next were Saxony, Saxony-Anhalt (five each), Brandenburg, Rhineland-Palatinate (three each), Mecklenburg-Western Pomerania, Schleswig-Holstein (two each) and Saarland (one). One participant stated that their dairy purchased milk “from more or less all over Germany”.

The question of certification of the products sold was also of interest for later analyses. Dairies, unlike dairy farmers, can use multiple certifications when selling different product lines, or of course can refrain from certification. Only the large certification systems were asked about by name, which led to a correspondingly high number of mentions of “other certifications” (N = 24). Bioland organic certification was the one cited most frequently by dairies (13); more mentions than EU organic certification (ten). Four dairies each had their products certified by Demeter and Naturland, six refrained from certifying their products, while five dairies did not feel unable to provide an answer (Navailable = 35).

3.2. Interactions with Supplier Farms

Of 47 dairies, 46 stated that they were in contact with the dairy farms supplying them regarding their cows’ rations; in the case of the remaining one dairy, this was only “to some extent” the case. Six dairies considered their influence on their suppliers to be “strong”, 13 to be “quite strong”, 16 to be “quite low”, six to be “low” and two each had no influence or gave no answer (Navailable = 45).

However, despite all the dairies being in contact with their dairy farms, 17 respondents were unable to provide information on the change in the use of green fodder by their suppliers over the last ten years. Eight dairies in each case had witnessed a decrease or an increase in the percentage of green fodder in diets, while 14 considered it to have remained unchanged (Navailable = 47). A prediction of the trend in green fodder percentage for the next 20 years was also requested. Here, too, the dairies tend to assume that the ratio will remain constant. Two dairies chose to “fully agree” with the statement “the proportion of grassland growth will increase nationally in the next 20 years”, five chose “rather agree”, 18 “somewhat agree”, eight “somewhat disagree” and three “completely disagree (Navailable = 36).

The next questions related to the differentiation of prices to suppliers. Here, too, the focus was on the green fodder percentage for feed: the certification associations generally do not specify mandatory green fodder percentages, but do provide for some marketing initiatives, such as “Sternenfair” (min. 60% green fodder percentage) [

25]. Multiple answers to this question were possible: of the 39 dairies that replied, eleven did not differentiate prices any further. Deviating amounts were linked in 18 dairies to the (respective) certification of the suppliers. Twelve dairies differentiate prices on quantity/stop costs, which could be problematic from the perspective of small farmers. Only one dairy rewards a relatively higher percentage of green fodder, but five mentioned a price adjustment for a higher proportion of hay and six mentioned higher prices for farms with a particularly high level of grazing. Three dairies gave a GMO-free diet and three “mountain farming areas” as price-differentiating parameters. Six dairies did not answer this question.

The dairies were then asked whether they were currently discussing strategies to pay higher prices to dairy farms with a stronger focus on grassland. This was currently an issue in five of 39 dairies. These five dairies were asked to describe the considerations in more detail (multiple answers were possible): four were currently discussing higher prices for longer grazing periods, two for higher hay percentages and two for higher green fodder percentages.

The performance of a dairy farm in terms of biodiversity conservation can only be estimated to a limited extent by reference to existing certification. If these tend to be low in the case of EU organic certification, the guidelines to be observed by organic associations (above all Bioland, Demeter, Naturland) are more likely to form the basis for livestock farming that preserves and promotes biodiversity (e.g., because the use of potentially biodiversity-damaging antiparasitic agents is more strongly regulated). Depending on demand for certified products lines, dairies have the potential to encourage or discourage participation in certification schemes by their supplier farms. We therefore asked the dairies whether they could accept more certified suppliers. Only two of 41 dairies reported a shortage of suitable suppliers. Eleven dairies received enquiries from certified suppliers, but saw the market as being saturated. For 16 dairies, this is currently not an issue and twelve want to expand their certified supplies.

3.3. Influence on and Attitude towards Grazing

Dairies are also an as yet unquantified influencing factor in determining whether, how often and for how long dairy cows are given access to grazing. In 2010, 42% of all dairy farms nationwide practised grazing, which was not specified by type and duration [

26]. Reijs et al. expect, however, that, by 2025, 95% of all cattle in Northwest Germany will be kept exclusively indoors [

18]. Although grazing is prima facie to be advocated from the point of view of animal welfare (not so with corresponding parasite pressure), from a nature conservation point of view, a pasture only becomes valuable with appropriate management (e.g., stocking rate, stocking density, fertiliser, pasture care, size of a pasture area) [

27]. The temporal-spatial quantity of grazing on dairy farms allows the drawing of only limited conclusions about aspects of biodiversity conservation. As mentioned, it also has a bearing on questions of animal welfare and landscape aesthetics [

28]. With this background, the next question was devoted to the grazing of dairy cattle. Seventeen dairies agreed with our assumption that the number of dairy cows grazing will decrease over the next 20 years, while twelve disagreed and seven were undecided (N

available = 35).

Of the 45 dairies in our survey, ten used the German word “Weide” (“pasture” or “grazing”) in product marketing. Two dairies used the term under the provisions of the certification guidelines for grazing labels and eight used the term to mean compliance with their own minimum provisions regarding grazing management. Of the eight dairies using their own regulations, two said that dairy cows must have year-round access to grazing; in three, access to grazing must last for at least five months; in two, at least four, and in one, at least three.

The dairies were then asked whether they would like to promote pasture farming, aside from separate remuneration (see above), via appropriate product lines. Of 38 responding dairies, three affirmed this; ten diaries are already using such labels, 19 did not intend to and six did not respond.

The next two questions focused more closely on the future of grazing. It can be assumed that the survey participants have a great deal of expertise with regard to demand, including consumer preferences. Out of 36 responding dairies, 17 (two “completely”, 15 “rather”) agreed that the importance of grazing in consumer preferences would increase over the next ten years, 13 were undecided and six disagreed (four chose “rather disagree”, two “completely disagree”). According to the dairies, grazing will play a more important role in communicating dairy products as “particularly healthy foods". Twenty-one dairies saw this as likely to have an increasing importance (five “strongly increasing”, 16 “somewhat increasing”), ten a constant importance and three a decreasing importance (two “rather decreasing”, one “strongly decreasing”); six dairies expressed no opinion (Navailable = 40).

3.4. Market Assessment of Desired Production Conditions from a Nature Conservation Perspective

Production processes that are more complex in operational terms but desirable from the point of view of grassland conservation must pay off for the farms and dairies. To understand their market integration, it is, therefore, also crucial to grasp how dairies assess consumer willingness to pay more for any value-added milk production (with more grazing, hay feeding). The dairies were asked what proportion of consumers would be prepared to pay a surcharge of >20 euro cents/kg for more demanding production conditions. Of 35 responding dairies, 16 currently estimate this consumer share at 0–10% (of all consumers), 14 at 11–25%, four at 26–50%, one at 51–75% and no dairies at 76–100%.

We also asked whether the proportion of consumers who would be willing to pay such premium prices could be increased over the next ten years (e.g., through consumer education or better marketing). One dairy believes that this consumer share could be increased to 76–100% (of all consumers). Three see it at 51–75%, twelve at 26–50%, nine at 11–25% and eight see it remaining at 0–10%.

Since the nature conservation value of a pasture is not given per se, the next question was: “Are there any concrete measures at your dairy beyond any existing bonus payments or certification to explicitly promote extensive grassland farming—a stocking density <1.4 livestock unit/ha or a maximum of two cuts a year, as a minimum?” Of 38 dairies, 24 answered “no”, and ten participants gave no answer; four dairies answered in the affirmative.

The answers to the question of whether the “regionality” of dairy products will gain in importance among consumers in future tended to be affirmative. Thirteen dairies chose “completely agree’, 15 “rather agree”, five “50/50”, one “rather disagree” and two “completely disagree”. Finally, the dairies were asked whether a national regulation for the label “Weidemilch” (“meadow-grazed milk”) would promote the sale of products of appropriate farming systems. This was mostly affirmed (Navailable = 41): 16 thought this was “certainly” useful, 14 admitted this was “perhaps useful”, three were undecided, 5 thought this was only “conditionally useful” and two said this was “not useful”. One dairy gave no response.

We also wanted to know the extent to which ecosystem services (e.g., landscape aesthetics, species-rich grassland) potentially supplied by dairy farming are currently important for the sale of dairy products. First, we requested an assessment of the actual situation. For eleven dairies, the communication of ecosystem services (ES) had a high level of importance in the marketing process (four “very high”, seven “rather high”). For twelve dairies, ES had a “medium” level of importance in marketing. Two attested “rather low”, eight “very low” and two survey participants chose that they are not able to assess the current situation (Navailable = 35). In the opinion of the dairies, there will be an increase in the importance of ES communication in marketing over the next ten years: three see it as “strongly increasing”, 21 see it to be “increasing somewhat”, six see it as “constant”, two as “somewhat decreasing” in importance. No dairy considers ES to have a “strongly decreasing” importance in marketing. Three dairies reported that they are not able to rate this question (Navailable = 35).

3.5. Assessment of the Influence of Other Market Forces

The market behaviour of market players correlates, among other things, with the self-evaluation of their role in market developments [

29,

30]. On this understanding, the dairies’ self-image is a factor in determining patterns of milk production and grassland use relative to the influence of other market players. When given the choice “dairy, retailers or consumers”, the dairies (N

available = 35) mainly see the retailers as the market player which exerts the strongest influence on management systems in the grassland farming sector ([

31] dairies assigned a “strong influence” for retailers).

The next question asked which group of actors could contribute most to overcoming the “milk price crisis” in the long term (Navailable = 35). Here, it was not the retailers that were mentioned most frequently (two), but the EU Common Agricultural Policy (CAP) and milk producers (nine mentions each). Six dairies saw market self-regulation as a decisive factor. Four dairies saw dairies as the decisive player in permanently overcoming the crisis, three others considered consumers to be the decisive player and one dairy saw the milk producer associations in particular as the major factor. One survey participant did not believe that a “lasting solution” was even possible. No dairy considered national policy to be in a position to make a decisive contribution towards overcoming the crisis.

3.6. Relationship between Dairy Size, Market Assessment and Market Behaviour

The second research objective of this survey was to evaluate the hypotheses (2) (i), namely that: The size of the dairy, measured in processed milk (kg) per day, has an influence on the assessment of market-regulating parameters (production, processing, sales, policies) and the development of consumer needs.

Table 2 lists the relevant (sub)questions. The test for a possible relationship between the dairy size and the respective variables (questions) is also shown. With regard to the assessment of consumer needs (questions no. 1 to no. 4), Spearman’s rank correlation coefficient shows a significant correlation between the variables for:

Question no. 1: There is an average correlation between dairy size and the degree of agreement (see answer options) with the statement: “Consumer preferences will (continue to) develop in the direction of grazing-based dairy products in the next 10 years”. The correlation has a significance level of 0.05: as the dairy size increases, respondents tend to disagree with the statement.

Question no. 2: There is a high correlation, with a significance level of 0.01, between dairy size and the degree of agreement with the statement: “Consumer preferences will (continue to) develop in the direction of ’regionality’ of the value chain over the next 10 years”. With increasing dairy size, participants tend to disagree with the statement.

Question no. 4: There is an average, negative correlation, with a significance level of 0.05, between the size of the dairy and the assessment of the extent to which the proportion of consumers willing to pay a significant surcharge for more expensive milk production can be increased. Simplified: smaller dairies tend to believe that their share can be increased more.

The test in Question no. 3 does not show a sufficient significance level.

The other questions on the assessment of market regulation variables (no. 5 to no. 8) show no correlations or significance for the tested variables (

Table 2). The presumed relationship between dairy size and the assessment of market trends in regard to grazing and market-regulating factors cannot be confirmed Here, it seems that other variables than dairy size determine diaries’ assessments.

Hypothesis 2 (ii) was also tested:

Depending on the size of the dairy, measured in kg of milk processed per day, there is a correlation/association with elements of positive market behaviour in terms of grassland conservation (and animal welfare).

Table 3 lists the (sub)questions asked and shows the test for a relationship between the dairy size and the respective variables. Only for the test on the variable of Question no. 12 (emphasis on regionality), measured by Spearman’s rank correlation coefficient, is a high correlation at a significance level of 0.01 given. In simple terms, the larger the dairy, the less emphasis is placed on the regionality of the products sold. This question is only indirectly (e.g., awareness training for consumers) important for grassland conservation. Since no other questions/variables were related to dairy size, the hypothesis should be rejected for the given sample: There is no correlation between the size of dairies and a more sustainable market behaviour.

3.7. Evaluation and Discussion of the Results

3.7.1. Discussion of the Methodology

The way we created the contact list excludes such diaries, which does not have a web presence. It is very unlikely that such diaries still exist in Germany [

32]. Like all surveys of this kind, bias can be introduced through external and/or self-deception of the survey participants or by perceptions of social desirability [

33]. Furthermore, it cannot be completely ruled out that the survey participants did not correspond to the intended role within the company, i.e., that they may have less relevant expertise than was assumed.

The average time spent by participants confirms the approach of a standardised test design with closed questions. The low use of the comment functions by the participants also indicates that qualitative and therefore much more “time-consuming” interview techniques would have met with stronger rejection in the dairies. The post-test experts also took this view. The standardised online survey provided access to the industry leaders.

This seems to have been possible only because (1) absolute anonymity was assured and (2) this was not diluted by questions that allowed conclusions to be drawn about the company name (e.g., question about location, etc.). The latter requirement was additionally circumvented by asking categorising questions (e.g., about the number of employees or the amount of milk processed per day) at the end of the survey. The “disadvantage” of this procedure is that the test for correlations of variables (e.g., testing correlations with milk volumes) is taken to a higher N because not all survey participants complete a survey. For the specific description and the primary objective of the survey, this is of lesser importance anyway; for the hypothesis tests, it can be assumed that categorising questions at the beginning of the survey would have led to a higher dropout rate because, for some respondents, the perceived anonymity would presumably have been lost.

The chosen methodology provides insights into the industry and a better understanding, in particular of the dairies’ own view, and points to possible approaches to pursue in subsequent research. The number in the sample was low due to the number of dairies still in operation nationally. Given the “milk crisis” occurring at the same time, it was gratifying, even surprising, to have relatively high participation rate, including from the very large dairies.

3.7.2. Discussion of the Results

Discussions on the future orientation of agriculture give only marginal attention to the dairy industry. The focus of the discourse is on the CAP instruments, i.e., the subsidy payments. The example of dairies shows that processing industry is, amongst others, able to influence agricultural practices. The dairies in the survey see the retail sector as the most important factor in grassland conservation issues.

For the most part, dairies assign the responsibility to overcome milk price crises permanently to other actors. At first glance, it is surprising that, with the exception of the CAP, dairies think that individual milk producers have the greatest influence on the course of milk crises, while national policy is thought to play practically no role. To a certain extent, this follows in the tradition of the modern-day view and implementation of market design, where politics in many areas do not see itself as an intervening force and, as far as possible, leaves the organising principles to the market itself [

34]. In the existing market system, the permanently (and excessively) low milk price is ultimately a result of the free, globalised market, but with the following important qualification: in practice in Europe, the relationships between dairies and milk producers are still largely fixed within a rigid framework of tendering and delivery obligations and to long-dated contracts. The new rules provided for by Article 148 of Regulation (EU) No. 1308/2013 have created some wiggle room for changing supply relationships. As of yet, they are largely unexploited. In many cases, the milk producer is still prevented from reacting more flexibly to market changes. Good examples are existing obligations to tender delivery. The milk producer does not receive a price for the milk sold; rather, the price paid for the milk is retrospectively determined for him once the milk has been processed and marketed by the dairies. In a way that is seemingly contrary to economic assumptions, the supply at the producer stage (quantity of milk) therefore initially increases when milk prices fall because the companies want to compensate for the drop in prices with higher production. In a milk market that was more subject to free-market mechanisms (without tendering and delivery obligations), falling prices would move all market participants to reduce the supply quantities. The milk market in many European countries (including Germany) is still lacking an important control function in this regard, even if the new regulation under Article 148 of Regulation (EU) No. 1308/2013 has opened up options for the Member States when it comes to designing price and quantity systems. The latest producer price crises are therefore not sales crises for German exporters. Rather, the unchecked quantities available for German dairies have created a cheap, demand-driven market for export partners in the global markets [

10,

35]. In the existing system, global competition will always lead to unpredictable distortions in the milk price. This will lead to corresponding impacts on dairy farms, which are on a drip feed of CAP-subsidies—even in periods of good market situations. International competition within a structurally uneven system of production will always create losers—in addition to a few winners. In order to prevent this, a more active intervention by the state to steer and regulate the market may be imperative [

21]. The dairies are therefore consistent in pointing out the importance of a political solution, especially against the background of potential side effects of the producer stage on biotic and abiotic resource conservation that have not been factored in.

Our survey was not able to confirm that small dairies maintain closer contact with producers. The hypothesis after that smaller dairies are more willing to act in the interests of protecting grassland also cannot be confirmed by the responses of the survey participants. However, smaller dairies tend to the prediction of changing consumer preferences towards a more regional production and pasture grazing.

Altogether, the dataset is an indication that statements such as “small is beautiful” could be seductive, but could also simplify things to an inadmissible degree when it comes to forming any kind of conclusions: in the first instance, the customer clearly prefers regional production [

36]. The logical conclusion, given our results, was that an increase in the number of small dairies alone would not have a positive effect on biotic resource conservation. An improved market position for smaller dairies could only be explained by the customer’s preferred distribution channels, which tend to favour regional channels. In turn, this does not correlate with qualified production, even though the regionalisation of processing and distribution channels is an important prerequisite for sparing fossil-fuel resources [

37].

The assessment of the majority of dairies is relatively unambiguous: the generation of ecosystem services, like the conservation of biodiversity, is becoming more important for consumers. Similarly, the nature of the responses to the questions regarding future consumer behavior—if these ever materialise and are taken up accordingly by the dairies—gives reason to hope that dairy farms’ management of grasslands will be qualified. However, when asked about the development and promotion of pasture feeding or high-nature-value grassland, it also becomes clear that such topics start from a relatively low level among the survey participants: Only four of 38 responding dairies contemporary support pastures or meadows that can be categorized as extensive grassland cultivation. Furthermore, it is surprising to us that only ten out of 45 dairies use the wording “pasture” when marketing their products. There is no clear meaning for “pasture-fed cows” (“Weidemilch”) in Germany. Dairies and retailers use it in different contexts. The majority of dairies (30 of 41) believe that a national uniform regulation for this label would help for higher sales.

The survey confirms that dairies play a central role when it comes to the operational orientation of milk producers, and that this group of actors has so far received too little attention when it comes to the quantitative and qualitative protection of grassland. However, the communication between dairies and their suppliers is not optimal. Seventeen of 47 dairies that responded could not provide any information on the development of the proportion of green fodder. According to their own information, 19 of the 45 dairies who responded are able to exert a strong or rather strong influence on the feed composition of the dairy cattle; a further 22 consider themselves to have at least a small influence. The basic prerequisite for improvements would be to know the basis for the production chain (feeding) for certain. With this information, it surely would be easier to inform the consumer about grassland management. This could be used to trigger a changing consumer preference towards a more resource-saving production on the basis of higher quality milk (no silage, less or no concentrated feed).

In order to get the dairies to act in a producer-friendly manner and thus effectively counter the resource-intensive structural change in the milk sector (longer transport routes, more spatially concentrated accumulation of farm manure, etc.), the first step could be to loosen the contractual relationship between the producer and the dairy. Producers should be able to change their buyers more easily, so that the dairies are more motivated to offer conditions that motivate producers to stay.

For the milk producer, the price formation processes on the milk market must be designed not only to support free choice of dairies—so that the obvious cost recovery problems and strong milk price fluctuations at the milk production level are reduced [

38] but also greater protection of resources. Under constant cost pressure, it is difficult for milk producers to be any more resource-efficient. The only slightly higher prices that pasture-fed milk commands compared to conventional milk already clearly show that it will not be possible to secure adequate prices for milk producers for additional environmental benefits within the market structures that have existed up until now. The majority of dairies is convinced that further information of consumers will raise the willingness to pay.

Another political measure to strengthen producers and qualify the processing stage could be that dairy farms that participate in dairy programmes that can guarantee particularly resource-saving grassland management techniques are relieved of bureaucracy, for example, by not additionally having to comply with official documentation requirements, thus avoiding unnecessarily labour-intensive work. On the other site, dairies could use farmer’s participation on agri-environmental measures to easily confirm a more sustainable grassland-management for high-quality products.

4. Conclusions

The paper describes the German dairy sector from the perspective of sustainable resources management. The underlying analysis was conducted on the basis of a sample of standardised interviews with dairies (N = 47). Until now, the German dairy sector has not been considered to have much relevance in the debate around the sustainability of grassland management, and the question of how dairies can wield influence on dairy farms in this regard has not been studied. This despite milk production being by far the biggest user of grassland in Germany.

Most dairies said that there is a willingness on the part of the consumer to pay for good quality products including a more sustainable milk-production. This attitude could be strengthened by improved communication with consumers. There seems to have been no thought given as yet to marketing products as deriving specifically from high nature value farming systems.

The survey data neither confirm nor refute the hypothesis that small dairies may have a better understanding of ecological aspects and may thus be more favourable to achieving sustainable agriculture objectives.

Dairies see the potential to strengthen resource conservation by appealing to farmer’s practices, but one key problem is that dairy farmers and dairies in the conventional sector are prone to extremely volatile market fluctuations. As its share of the market grows, this volatility may also start to impact the organic milk production sector. On the one hand, the dairies are already seeing a growing demand for regional products. However, at the same time, market pressures are leading to a growing concentration on an ever-smaller number of actors in the dairy sector. The dairies, participating in our survey, are mainly passing responsibility to other market actors such as retailers.

Our analysis suggests that while in theory dairies have an important role in influencing and improve environmental and ecological performance, at the same time, dairies currently exercise little power in the change process affecting their sector.

{kind=link}

{kind=link}

{kind=link}

{kind=link}