Sustainable Supply Chain of Enterprises: Value Analysis

Abstract

:1. Introduction

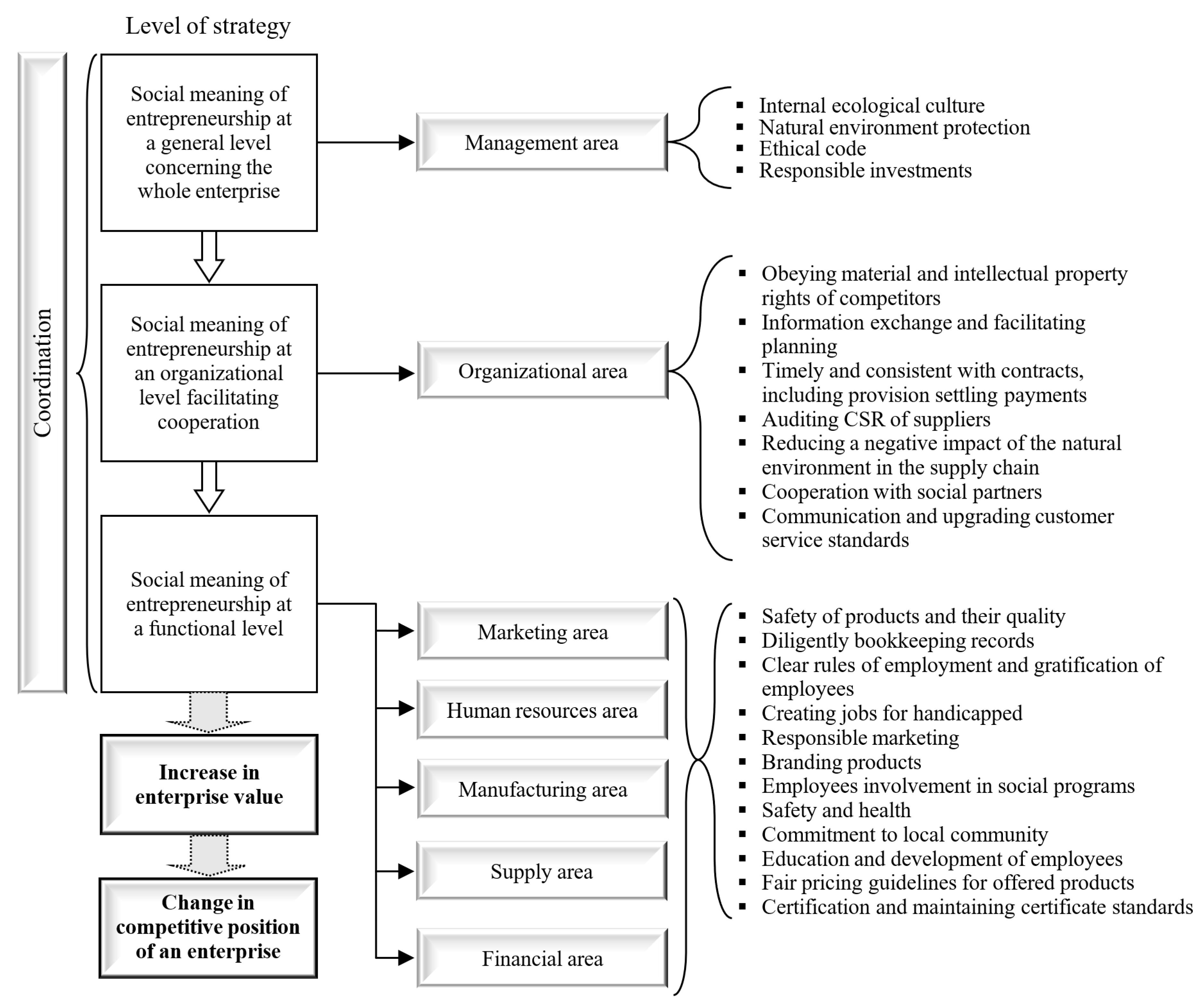

2. SD of Enterprises and CSR in Business

- ▪

- Accounting employees to undertake obligations and managerial involvement of staff in SD-related matters,

- ▪

- creating and cultivating a culture of social responsibility,

- ▪

- creating a motivation system (i.e., based on financial and non-financial incentives) that promotes socially responsible attitudes,

- ▪

- efficient utilization of financial, natural, and human resources,

- ▪

- propagating equal opportunities for groups insufficiently represented at higher posts,

- ▪

- achieving a compromise between the organization and interest groups,

- ▪

- establishing bilateral communicative processes with interest groups,

- ▪

- propagating participation of all levels of operations, directed within the sphere of social responsibility,

- ▪

- balancing levels of authorities, responsibilities, and a number of people making decisions on behalf of the enterprise,

- ▪

- monitoring implementation and decisions in a socially adequate manner, and

- ▪

- periodic verification and assessment of organization order, its modifications, and manifesting changes.

3. Case study

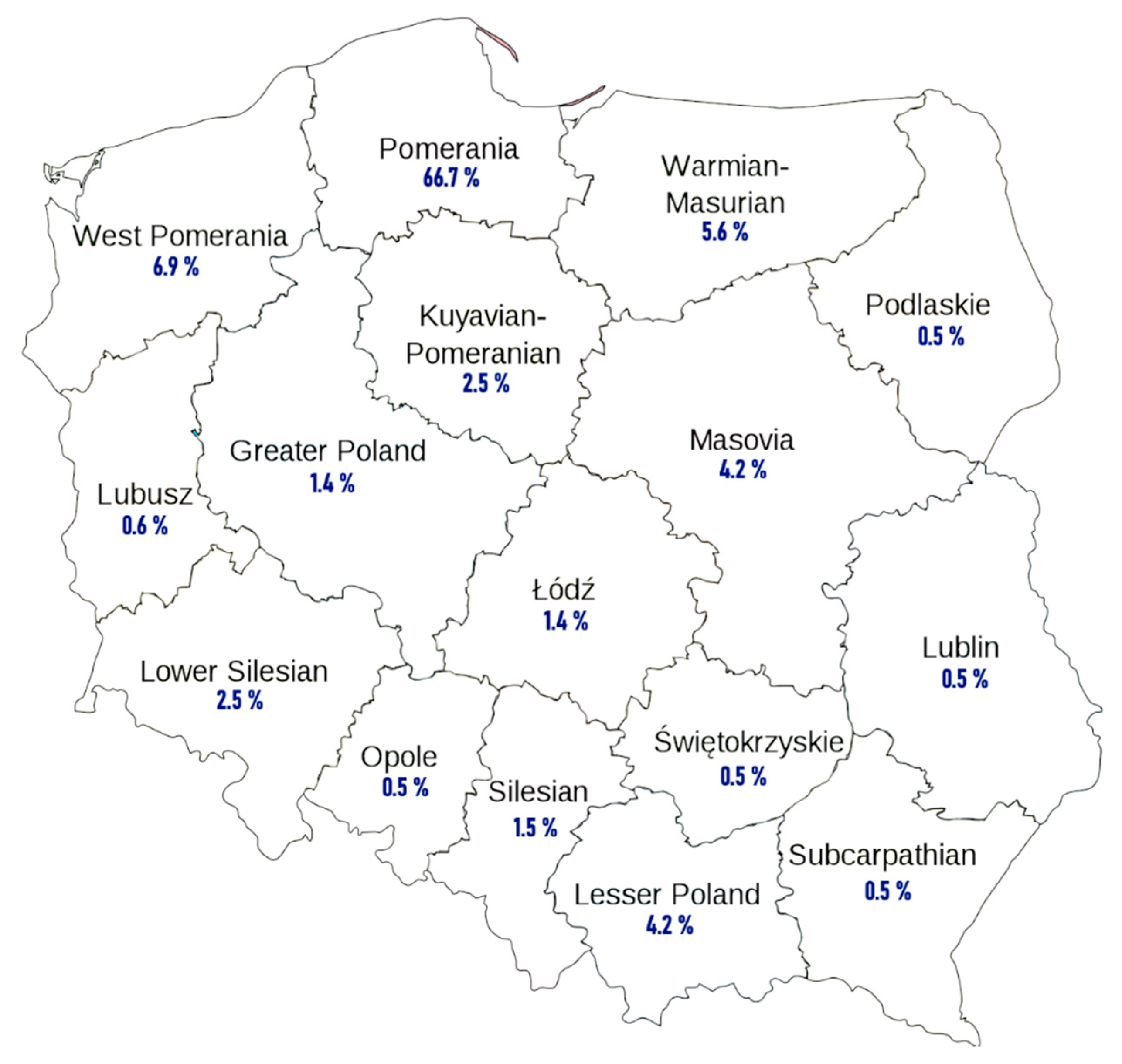

3.1. Methodology

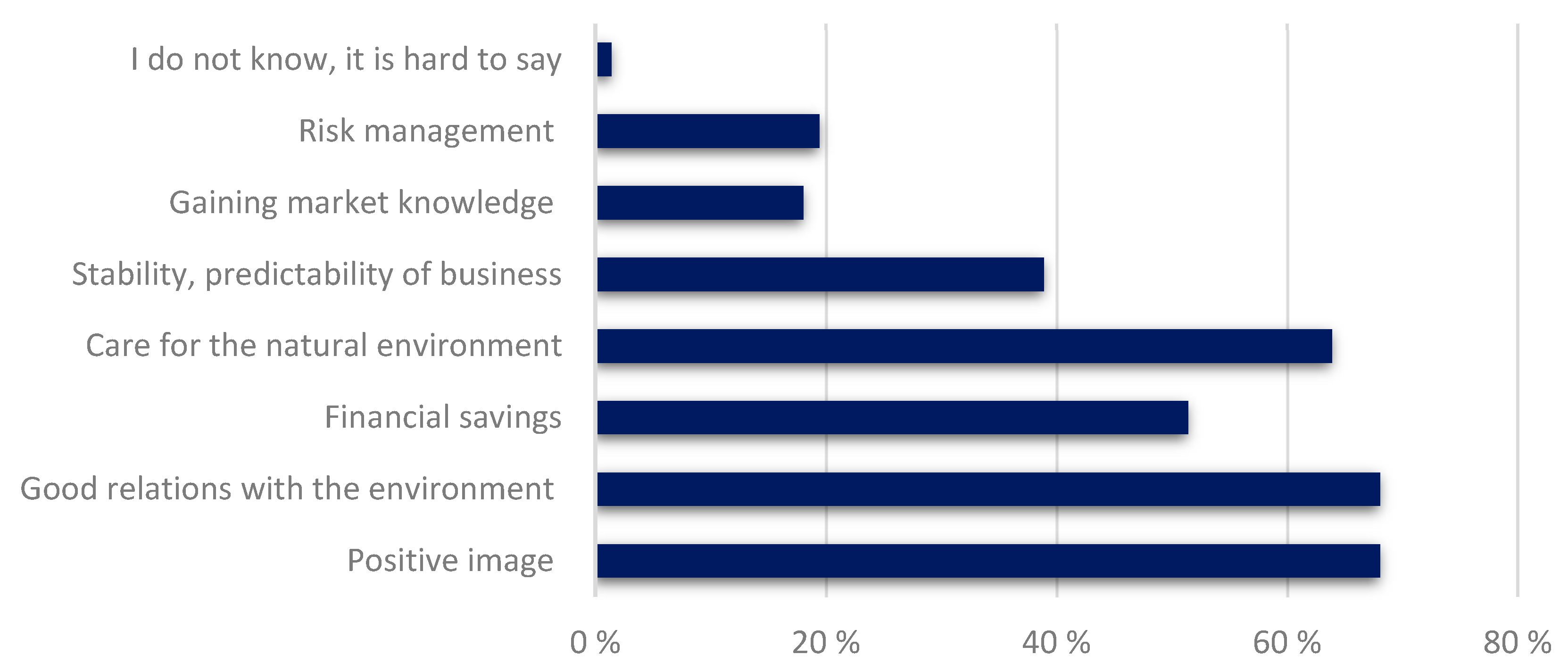

3.2. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- World Bank Rankings and Ease of Doing Business Score: Economy Rankings. Available online: https://www.doingbusiness.org/en/rankings (accessed on 30 May 2019).

- Matopoulos, A.; Barros, A.C.; van der Vorst, J.G.A.J. Resource-efficient supply chains: A research framework, literature review and research agenda. Supply Chain Manag. Int. J. 2015, 20, 218–236. [Google Scholar] [CrossRef] [Green Version]

- Reiner, G.; Hofmann, P. Efficiency analysis of supply chain processes. Int. J. Prod. Res. 2006, 44, 5065–5087. [Google Scholar] [CrossRef]

- Niranjan, T.T.; Weaver, M. A unifying view of goods and services supply chain management. Serv. Ind. J. 2011, 31, 2391–2410. [Google Scholar] [CrossRef]

- Nemtajela, N.; Mbohwa, C. Relationship between Inventory Management and Uncertain Demand for Fast Moving Consumer Goods Organisations. Procedia Manuf. 2017, 8, 699–706. [Google Scholar] [CrossRef]

- Jones, D.A.; Willness, C.R.; Glavas, A. When Corporate Social Responsibility (CSR) Meets Organizational Psychology: New Frontiers in Micro-CSR Research, and Fulfilling a Quid Pro Quo through Multilevel Insights. Front. Psychol. 2017, 8, 520. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Boulouta, I.; Pitelis, C.N. Who Needs CSR? The Impact of Corporate Social Responsibility on National Competitiveness. J. Bus. Ethics 2014, 119, 349–364. [Google Scholar] [CrossRef]

- Goel, M.; Ramanathan, M.P.E. Business Ethics and Corporate Social Responsibility—Is there a Dividing Line? Procedia Econ. Financ. 2014, 11, 49–59. [Google Scholar] [CrossRef] [Green Version]

- Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals With Forks: The Triple Bottom Line of 21st Century Business; New Society Publishers: Stony Creek, CT, USA, 1998; ISBN 1841120847. [Google Scholar]

- Elkington, J. 25 Years Ago I Coined the Phrase “Triple Bottom Line.” Here’s Why It’s Time to Rethink It. Harv. Bus. Rev. 2018. Available online: https://hbr.org/2018/06/25-years-ago-i-coined-the-phrase-triple-bottom-line-heres-why-im-giving-up-on-it (accessed on 10 July 2019).

- Kruk, H. Konkurencyjność przedsiębiorstw w świetle zasad rozwoju zrównoważonego. In Przedsiębiorstwo w Otoczeniu Globalnym; Dębicka, O., Oniszczuk-Jastrząbek, A., Gutowski, T., Winiarski, J., Eds.; UG: Gdansk, Poland, 2015; p. 116. [Google Scholar]

- Albińska, E. Człowiek w Środowisku Przyrodniczym i Społecznym; Wydawnictwo Katolickiego Uniwersytetu Lubelskiego: Lublin, Poland, 2005. [Google Scholar]

- Borys, T.; Śleszyński, J. Ekorozwój jako zbiór zasad. In Wskaźniki Ekorozwoju. Wydawnictwo Ekonomia i Środowisko; Borys, T., Ed.; Foundation of Environmental and Resource Economists: Białystok, Poland, 1999; pp. 85–92. [Google Scholar]

- Pigłowski, M. Współczesne uwarunkowanie rozwoju zrównoważonego. In Uwarunkowania Rozwoju Przedsiębiorczości. Determinanty i Narzędzia Zdobywania Przewagi Konkurencyjnej; Adamkiewicz-Drwilło, H.G., Ed.; PWN: Warsaw, Poland, 2007; p. 80. [Google Scholar]

- Wąchol, J. Wartość przedsiębiorstwa w aspekcie rozwoju zrównoważonego i trwałego oraz procesów globalizacji. In Zarządzanie Wartością Przedsiębiorstwa a Alokacja Kapitału; Bielinskiego, J., Ed.; CeDeWu: Warsaw, Poland, 2004; p. 45. [Google Scholar]

- Kulig-Moskwa, K. Odpowiedzialność społeczna jako czynnik konkurencyjności przedsiębiorstw w gospodarce opartej na wiedzy. In Europejskie Wymiary Przedsiębiorczości; Kruk, H., Skrzeszewska, K., Eds.; AM: Gdynia, Poland, 2008; p. 137. [Google Scholar]

- Chudy, K. Istota konkurencyjności przedsiębiorstw w świetle koncepcji społecznej odpowiedzialności przedsiębiorstw. In Europa Wobec Wyzwań Gospodarki Globalnej; Balcerzak, A.P., Rogalska, E., Eds.; Wyd. Adam Marszałek: Torun, Poland, 2008. [Google Scholar]

- Aguilera, R.V.; Rupp, D.; Williams, C.A.; Ganapathi, J. Putting the S Back in Corporate Social Responsibility: A Multi-level Theory of Social Change in Organizations. Acad. Manag. Rev. 2004, 32, 836–863. [Google Scholar] [CrossRef] [Green Version]

- Gasiński, T.; Pijanowski, S. Zarządzanie ryzykiem w procesie zrównoważonego rozwoju biznesu. In Podręcznik dla Dużych i Średnich Przedsiębiorstw; Ministerstwo Gospodarki: Warsaw, Poland, 2011. [Google Scholar]

- Nakonieczna, J. Społeczna odpowiedzialność—nowy akcent globalnej strategii przedsiębiorstw międzynarodowych. In Globalizacja a Stosunki Międzynarodowe; Haliżak, E., Kuźniar, R., Simonides, J., Eds.; Wyd. Oficyna Wydawnicza Bratna: Bydgoszcz-Warszawa, Poland, 2004; p. 192. [Google Scholar]

- Al-Odeh, M.; Smallwood, J. Sustainable Supply Chain Management: Literature Review, Trends, and Framework. Int. J. Comput. Eng. Manag. 2012, 15, 85–90. [Google Scholar]

- Castillo, V.E.; Mollenkopf, D.A.; Bell, J.E.; Bozdogan, H. Supply Chain Integrity: A Key to Sustainable Supply Chain Management. J. Bus. Logist. 2018, 39, 38–56. [Google Scholar] [CrossRef]

- Chin, T.A.; Tat, H.H.; Sulaiman, Z. Green Supply Chain Management, Environmental Collaboration and Sustainability Performance. Procedia Cirp 2015, 26, 695–699. [Google Scholar] [CrossRef] [Green Version]

- Da Silva, M.E.; Neutzling, D.M.; Alves, A.P.F.; Dias, P.; Dos Santos, C.A.F.; Nascimento, L.F. Sustainable Supply Chain Management: A Literature review on Brazilian publications. J. Oper. Supply Chain Manag. 2015, 8, 29. [Google Scholar] [CrossRef] [Green Version]

- Alexander, A.; Walker, H.; Naim, M. Decision theory in sustainable supply chain management: A literature review. Supply Chain Manag. Int. J. 2014, 19, 504–522. [Google Scholar] [CrossRef] [Green Version]

- Touboulic, A.; Walker, H. Theories in sustainable supply chain management: A structured literature review. Int. J. Phys. Distrib. Logist. Manag. 2015, 45, 16–42. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and Society: The Link between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.L.; de Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010; ISBN 0521137934. [Google Scholar]

- Ministerstwo Gospodarki. CSR: Społeczna odpowiedzialność biznesu w Polsce. In Krajowy Program Reform Europa 2020; Ministerstwo Gospodarki: Warsaw, Poland, 2011. [Google Scholar]

- Good Brand CSR w Polsce. Menedżerowie, Menedżerki 500, Lider/Liderka CSR. In Proceedings of the Forum Odpowiedzialnego Biznesu; Good Brand & Company Polska: Warsaw, Poland, 2010; p. 10. [Google Scholar]

- Kärnä, J.; Hansen, E.; Juslin, H. Social responsibility in environmental marketing planning. Eur. J. Mark. 2003, 37, 848–871. [Google Scholar] [CrossRef]

- Portal Biznesowy—TP-IR CSR. Available online: http://tp-ir.pl/ (accessed on 31 August 2019).

- Lu, R.X.A.; Lee, P.K.C.; Cheng, T.C.E. Socially responsible supplier development: Construct development and measurement validation. Int. J. Prod. Econ. 2012, 140, 160–167. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Hafez, H. Corporate social responsibility and firm value: An empirical study of an emerging economy. J. Gov. Regul. 2016, 5, 40–53. [Google Scholar]

- Lima Crisóstomo, V.; de Souza Freire, F.; Cortes de Vasconcellos, F. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef]

- Chen, R.C.Y.; Lee, C.-H. The influence of CSR on firm value: An application of panel smooth transition regression on Taiwan. Appl. Econ. 2017, 49, 3422–3434. [Google Scholar] [CrossRef]

- Gompers, P.; Ishii, J.; Metrick, A. Corporate Governance and Equity Prices. Q. J. Econ. 2003, 118, 107–156. [Google Scholar] [CrossRef] [Green Version]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Richardson, A.J.; Welker, M.; Hutchinson, I.R. Managing Capital Market Reactions to Corporate Social Resposibility. Int. J. Manag. Rev. 1999, 1, 17–43. [Google Scholar] [CrossRef]

- Cornell, B.; Shapiro, A.C. Corporate Stakeholders and Corporate Finance. Financ. Manag. 1987, 16, 5. [Google Scholar] [CrossRef]

- Jamali, D.; Mirshak, R. Corporate Social Responsibility (CSR): Theory and Practice in a Developing Country Context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Mikołajek-Gocejna, M. Wyzwania na szczeblu przedsiębiorstwa—Imperatyw kształtowania wartości. In Przedsiębiorstwo, Wartość, Zarządzanie; Suszyński, C., Ed.; PWE: Warsaw, Poland, 2007; p. 99. [Google Scholar]

- Jo, H.; Harjoto, M.A. Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Knack, S.; Keefer, P. Does Social Capital Have an Economic Payoff? A Cross-Country Investigation. Q. J. Econ. 1997, 112, 1251–1288. [Google Scholar] [CrossRef]

- Goyal, A. Corporate Social Responsibility as a Signalling Device for Foreign Direct Investment. Int. J. Econ. Bus. 2006, 13, 145–163. [Google Scholar] [CrossRef]

- Campbell, J.Y. Understanding Risk and Return. J. Polit. Econ. 1996, 104, 298–345. [Google Scholar] [CrossRef] [Green Version]

- Brown, W.O.; Helland, E.; Smith, J.K. Corporate philanthropic practices. J. Corp. Financ. 2006, 12, 855–877. [Google Scholar] [CrossRef] [Green Version]

- Barnea, A.; Rubin, A. Corporate Social Responsibility as a Conflict Between Shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Windsor, D. The future of corporate social responsibility. Int. J. Organ. Anal. 2001, 9, 225–256. [Google Scholar] [CrossRef]

- Gasiński, T.; Piekalski, G. Zrównoważony Biznes: Podręcznik dla Małych i Średnich Przedsiębiorstw; Ministerstwo Gospodarki: Warsaw, Poland, 2006.

- Kim, W.S.; Oh, S. Corporate social responsibility, business groups and financial performance: A study of listed Indian firms. Econ. Res. Istraž. 2019, 32, 1777–1793. [Google Scholar] [CrossRef] [Green Version]

- Zuraida, Z.; Houqe, N.; van Zijl, T. Value Relevance of Environmental, Social and Governance Disclosure. In Handbook of Finance and Sustainability; SSRN: Rochester, NY, USA, 2016. [Google Scholar]

- Rappaport, A. Ten Ways to Create Shareholder Value. Harv. Bus. Rev. 2006, 84, 66–77. [Google Scholar]

- Filek, J. Społeczna odpowiedzialność biznesu. In Tylko Moda Czy Nowy Model Prowadzenia Działalności Gospodarczej? Urząd Ochrony Konsumentów i Konkurentów: Cracow, Poland, 2006. [Google Scholar]

- Sjøberg, S.; Schreiner, C. How Do Learners in Different Cultures Related to Science and Technology? Results and Perspectives from the Project Rose. In Asia-Pacific Forum on Science Learning and Teaching; The Education University of Hong Kong: Hong Kong, China, 2005; Volume 6, pp. 1–17. [Google Scholar]

- Sullivan, G.M.; Artino, A.R., Jr. Analyzing and interpreting data from likert-type scales. J. Grad. Med. Educ. 2013, 5, 541–542. [Google Scholar] [CrossRef] [Green Version]

- Aguinis, H.; Glavas, A. What We Know and Don’t Know About Corporate Social Responsibility. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef] [Green Version]

- Ararat, M.; Colpan, A.M.; Matten, D. Business Groups and Corporate Responsibility for the Public Good. J. Bus. Ethics 2018, 153, 911–929. [Google Scholar] [CrossRef] [Green Version]

- Smith, N.C. Corporate Social Responsibility: Whether or How? Calif. Manag. Rev. 2003, 45, 52–76. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate Social Responsibility: Strategic Implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Hockerts, K. Entrepreneurial Opportunity in Social Purpose Business Ventures. In Social Entrepreneurship; Mair, J., Robertson, J., Hockerts, K., Eds.; Palgrave Macmillan UK: London, UK, 2006; pp. 142–154. [Google Scholar]

- Mair, J.; Martí, I. Social entrepreneurship research: A source of explanation, prediction, and delight. J. World Bus. 2006, 41, 36–44. [Google Scholar] [CrossRef]

- Glavas, A. Corporate Social Responsibility and Organizational Psychology: An Integrative Review. Front. Psychol. 2016, 7, 144. [Google Scholar] [CrossRef] [Green Version]

- Brieger, S.A.; Anderer, S.; Fröhlich, A.; Bäro, A.; Meynhardt, T. Too Much of a Good Thing? On the Relationship Between CSR and Employee Work Addiction. J. Bus. Ethics 2019, 1–19. [Google Scholar] [CrossRef] [Green Version]

- De Ruiter, M.; Schaveling, J.; Ciulla, J.B.; Nijhof, A. Leadership and the Creation of Corporate Social Responsibility: An Introduction to the Special Issue. J. Bus. Ethics 2018, 151, 871–874. [Google Scholar] [CrossRef]

- Sisco, C.; Chorn, B.; Pruzan-Jorgensen, P.M. Supply Chain Sustainability: A Practical Guide for Continuous Improvement, 2nd ed.; UN Global Compact Office and Business for Social Responsibility: New York, NY, USA, 2010. [Google Scholar]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Millington, A. Managing Sustainable Global Supply Chain: Framework and Best Practices; Network for Business Sustainability: London, ON, Canada, 2011. [Google Scholar]

- Brønn, P.S.; Vrioni, A.B. Corporate social responsibility and cause-related marketing: An overview. Int. J. Advert. 2001, 20, 207–222. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Short, J.C.; Moss, T.W.; Lumpkin, G.T. Research in social entrepreneurship: Past contributions and future opportunities. Strateg. Entrep. J. 2009, 3, 161–194. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Risk | Threat |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

| Subtopic | Percentage † |

|---|---|

| The mission, objectives, and policies consider SD issues | 45.8 |

| A defined strategy for SD is implemented | 36.1 |

| Business plans addressing SD are prepared | 29.2 |

| Forms of cooperation with other entities, in order to pursue SD, are implemented | 41.7 |

| Forms of cooperation with other entities, in order to pursue SD, are prepared | 26.4 |

| Cooperation is preferred with other entities that also apply the principles of SD | 20.8 |

| Logistics chains are arranged according to the principles of SSC | 27.8 |

| SD (including SSC) is not included in the strategic elements of the enterprise | 16.7 |

| Other | 2.9 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oniszczuk-Jastrząbek, A.; Czermański, E.; Cirella, G.T. Sustainable Supply Chain of Enterprises: Value Analysis. Sustainability 2020, 12, 419. https://doi.org/10.3390/su12010419

Oniszczuk-Jastrząbek A, Czermański E, Cirella GT. Sustainable Supply Chain of Enterprises: Value Analysis. Sustainability. 2020; 12(1):419. https://doi.org/10.3390/su12010419

Chicago/Turabian StyleOniszczuk-Jastrząbek, Aneta, Ernest Czermański, and Giuseppe T. Cirella. 2020. "Sustainable Supply Chain of Enterprises: Value Analysis" Sustainability 12, no. 1: 419. https://doi.org/10.3390/su12010419