The Influence of Managerial Mindfulness on Innovation: Evidence from China

Abstract

:1. Introduction

2. Literature Review and Research Hypothesis

2.1. Defining Managerial Mindfulness

2.2. Influence of Managerial Mindfulness on R&D Intensity

2.3. Moderating Role of Firm Characteristics

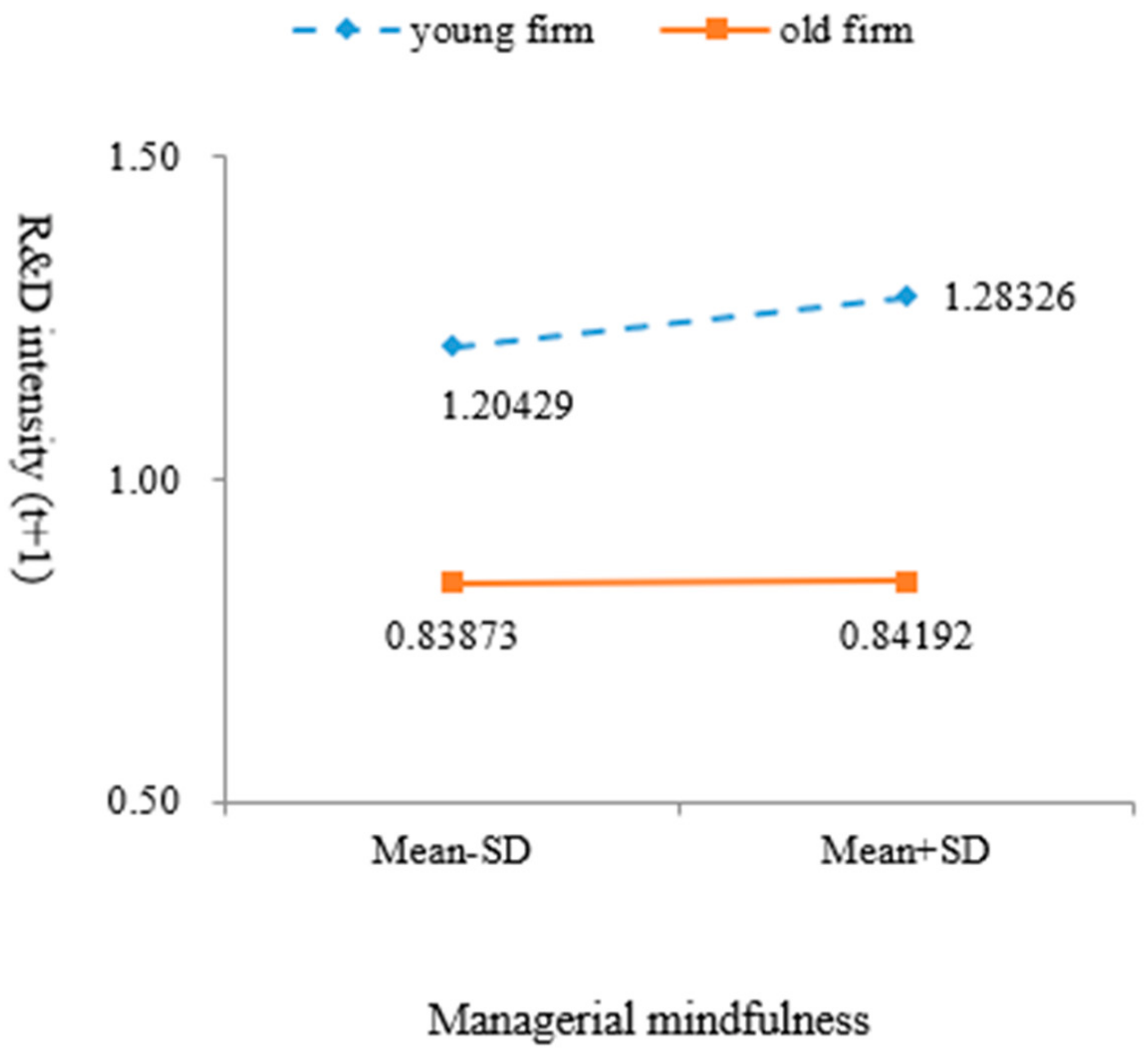

2.2.1. Firm Age

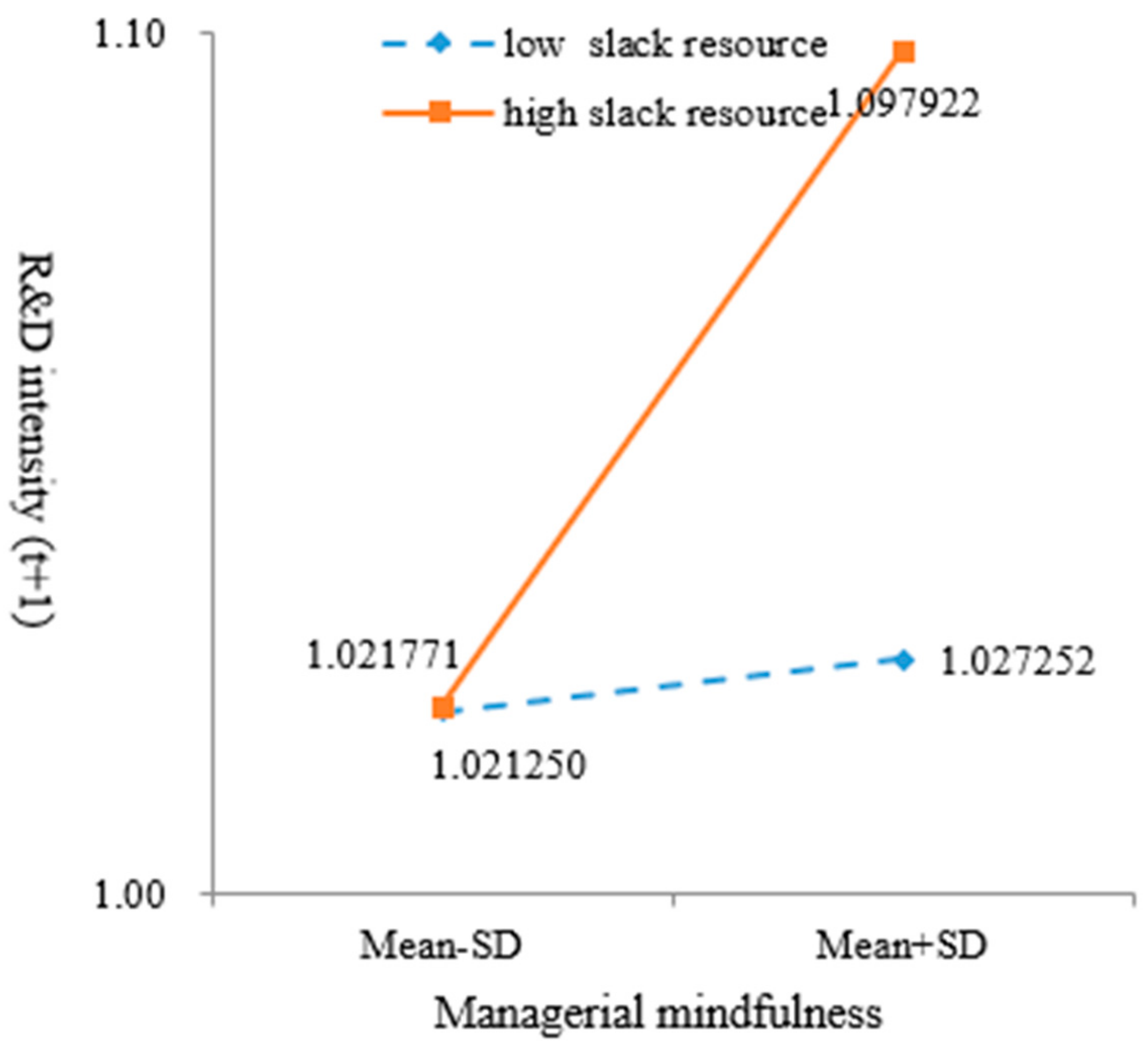

2.2.2. Slack Resources

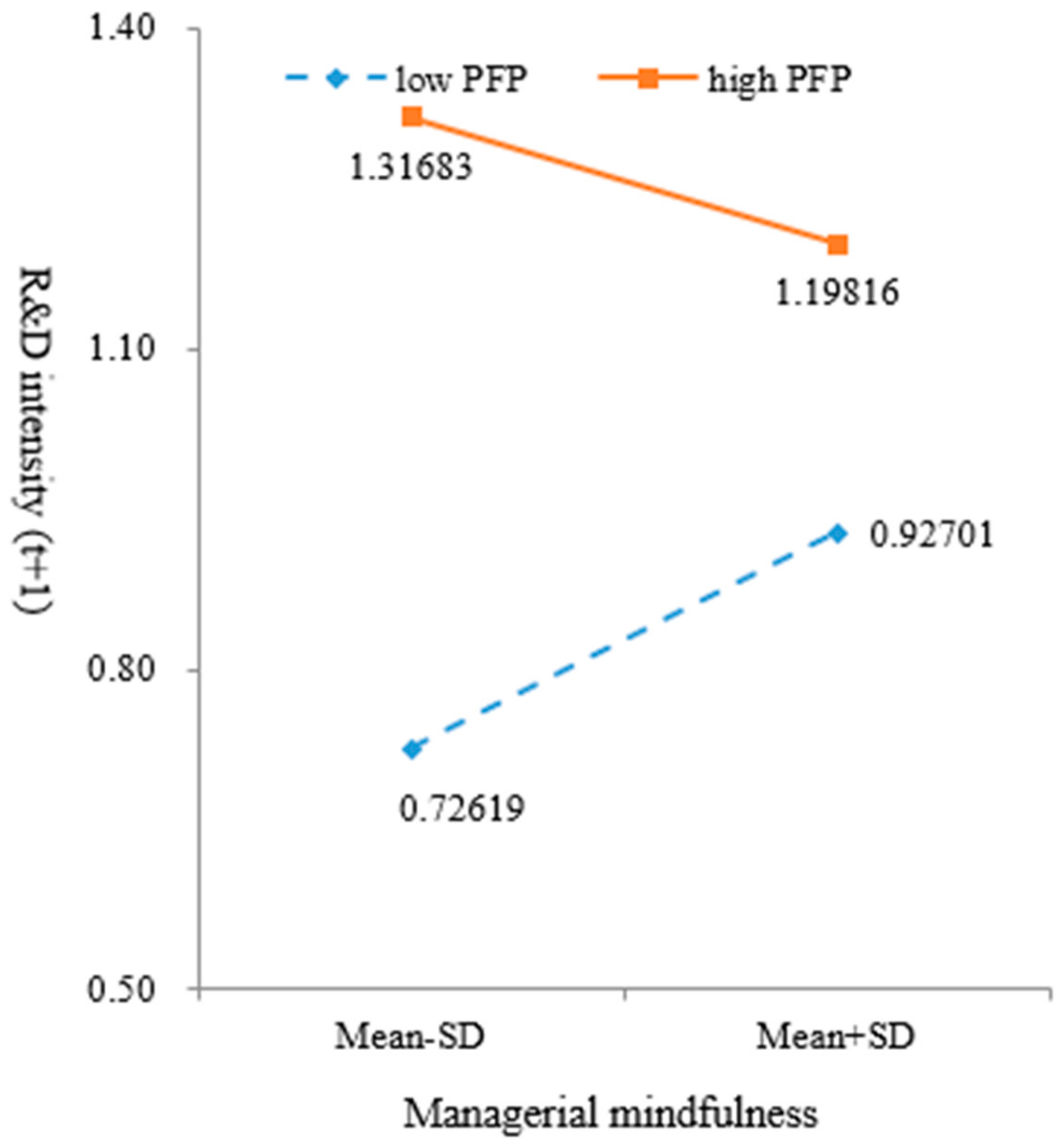

2.2.3. Past Financial Performance

3. Research Methodology

3.1. Sample Description and Data Resource

3.2. Measures

3.3. Estimation Methods

4. Results and Discussion

4.1. Descriptive Statistics and Correlation Analysis

4.2. Empirical Results

4.3. Robust Test

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Zang, Z.; Zhu, Q.; Mogorrón-Guerrero, H. How Does R&D Investment Affect the Financial Performance of Cultural and Creative Enterprises? The Moderating Effect of Actual Controller. Sustainability 2019, 11, 297. [Google Scholar] [Green Version]

- Chen, L.; Chen, Z.; Li, J. Can Trade Credit Maintain Sustainable R&D Investment of SMEs?—Evidence from China. Sustainability 2019, 11, 843. [Google Scholar]

- Loredo, E.; Lopez-Mielgo, N.; Pineiro-Villaverde, G.; García-Álvarez, M.T. Utilities: Innovation and Sustainability. Sustainability 2019, 11, 1085. [Google Scholar] [CrossRef]

- Omobhude, C.; Chen, S.H. The Roles and Measurements of Proximity in Sustained Technology Development: A Literature Review. Sustainability 2019, 11, 224. [Google Scholar] [CrossRef]

- Lee, C.Y. Industry R&D intensity distributions: Regularities and underlying determinants. J. Evol. Econ. 2002, 12, 307–341. [Google Scholar]

- Cohen, W.M. Fifty years of empirical studies of innovative activity and performance. In Handbook of the Economics of Innovation; Elsevier: North-Holland, The Netherlands, 2010; Volume 1, pp. 129–213. [Google Scholar]

- Kor, Y.Y. Direct and interaction effects of top management team and board compositions on R&D investment strategy. Strateg. Manag. J. 2006, 27, 1081–1099. [Google Scholar]

- Christensen, D.M.; Dhaliwal, D.S.; Boivie, S.; Graffin, S.D. Top management conservatism and corporate risk strategies: Evidence from managers’ personal political orientation and corporate tax avoidance. Strateg. Manag. J. 2015, 36, 1918–1938. [Google Scholar] [CrossRef]

- Bromiley, P.; Rau, D.; Zhang, Y. Is R & D risky? Strateg. Manag. J. 2017, 38, 876–891. [Google Scholar]

- Zheng, X.; Xie, Q. The world’s top 500 are meditating. What about you? Tsinghua Bus. Rev. 2015, 14–19. [Google Scholar]

- Good, D.J.; Lyddy, C.J.; Glomb, T.M.; Bono, J.E.; Brown, K.W.; Duffy, M.K.; Baer, R.A.; Brewer, J.A.; Lazar, S.W. Contemplating mindfulness at work: An integrative review. J. Manag. 2016, 42, 877–880. [Google Scholar] [CrossRef]

- Brown, K.W.; Ryan, R.M. The benefits of being present: Mindfulness and its role in psychological well-being. J. Personal. Soc. Psychol. 2003, 84, 822–848. [Google Scholar] [CrossRef]

- Baas, M.; Nevicka, B.; Ten Velden, F.S. Specific mindfulness skills differentially predict creative performance. Personal. Soc. Psychol. Bull. 2014, 40, 1092–1106. [Google Scholar] [CrossRef] [PubMed]

- Bishop, S.R.; Lau, M.; Shapiro, S.; Carlson, L.; Anderson, N.D.; Carmody, J.; Devins, G. Mindfulness: A proposed operational definition. Clin. Psychol. Sci. Pract. 2004, 11, 230–241. [Google Scholar] [CrossRef]

- Park, T.; Reilly-Spong, M.; Gross, C.R. Mindfulness: A systematic review of instruments to measure an emergent patient-reported outcome (PRO). Qual. Life Res. 2013, 22, 2639–2659. [Google Scholar] [CrossRef] [PubMed]

- Quaglia, J.T.; Brown, K.W.; Lindsay, E.K.; Creswell, J.D.; Goodman, R.J. From conception to operationalization of mindfulness. In Handbook of Mindfulness: Theory, Research, and Practice; Brown, K.W., Creswell, J.D., Ryan, R.M., Eds.; The Guilford Press: New York, NY, USA, 2015; pp. 151–170. [Google Scholar]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Finkelstein, S.; Hambrick, D.C. Top-management-team tenure and organizational outcomes: The moderating role of managerial discretion. Adm. Sci. Q. 1990, 35, 484–503. [Google Scholar] [CrossRef]

- Wiersema, M.F.; Bantel, K.A. Top management team demography and corporate strategic change. Acad. Manag. J. 1992, 35, 91–121. [Google Scholar]

- Hambrick, D.C.; Cho, T.S.; Chen, M.J. The influence of top management team heterogeneity on firms’ competitive moves. Adm. Sci. Q. 1996, 41, 659–684. [Google Scholar] [CrossRef]

- Knight, D.; Pearce, C.L.; Smith, K.G.; Olian, J.D.; Sims, H.P.; Smith, K.A.; Flood, P. Top management team diversity group process, and strategic consensus. Strateg. Manag. J. 1999, 20, 445–465. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Wang, J. Managerial Humanistic Attention and CSR: Do Firm Characteristics Matter? Sustainability 2018, 10, 4029. [Google Scholar] [CrossRef]

- Wiseman, R.M.; Gomez-Mejia, L.R. A behavioral agency model of managerial risk taking. Acad. Manag. Rev. 1998, 23, 133–153. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 39–67. [Google Scholar] [CrossRef]

- Greve, H.R.; Taylor, A. Innovations as catalysts for organizational change: Shifts in organizational cognition and search. Adm. Sci. Q. 2000, 45, 54–80. [Google Scholar] [CrossRef]

- Shapiro, S.L.; Carlson, L.E.; Astin, J.A.; Freedman, B. Mechanisms of mindfulness. J. Clin. Psychol. 2006, 62, 373–386. [Google Scholar] [CrossRef]

- Glomb, T.M.; Duffy, M.K.; Bono, J.E.; Yang, T. Mindfulness at Work. In Research in Personnel and Human Resources Management; Emerald Group Publishing Limited: Bingley, UK, 2011; Volume 30, pp. 115–157. [Google Scholar]

- Davis, J.H.; Schoorman, F.D.; Donaldson, L. Toward a stewardship theory of management. Acad. Manag. Rev. 1997, 22, 20–47. [Google Scholar] [CrossRef]

- Levesque, C.; Brown, K.W. Mindfulness as a moderator of the effect of implicit motivational self-concept on day-to-day behavioral motivation. Motiv. Emot. 2007, 31, 284–299. [Google Scholar] [CrossRef]

- Ryan, R.M.; Deci, E.L. Self-determination theory and the facilitation of intrinsic motivation social development, and well-being. Am. Psychol. 2000, 55, 68–78. [Google Scholar] [CrossRef]

- Weick, K.E.; Sutcliffe, K.M.; Obstfeld, D. Organizing for High Reliability: Processes of Collective Mindfulness. In Research in Organizational Behavior; Staw, B.M., Cummings, L.L., Eds.; JAI Press: Greenwich, CT, USA, 1999; pp. 81–123. [Google Scholar]

- Brown, K.W.; Ryan, R.M.; Creswell, J.D. Mindfulness: Theoretical foundations and evidence for its salutary effects. Psychol. Inq. 2007, 18, 211–237. [Google Scholar] [CrossRef]

- Jha, A.P.; Morrison, A.B.; Dainer-Best, J.; Parker, S.; Rostrup, N.; Stanley, E.A. Minds “at attention”: Mindfulness training curbs attentional lapses in military cohorts. PLoS ONE 2015, 10, e0116889. [Google Scholar] [CrossRef]

- Tan, C.M. Search Inside Yourself: The Unexpected Path to Achieving Success, Happiness (and World Peace); Harper One: New York, NY, USA, 2012. [Google Scholar]

- West, C.P.; Dyrbye, L.N.; Rabatin, J.T.; Call, T.G.; Davidson, J.H.; Multari, A.; Shanafelt, T.D. Intervention to promote physician well-being job satisfaction, and professionalism: A randomized clinical trial. JAMA Intern. Med. 2014, 174, 527–533. [Google Scholar] [CrossRef]

- Wolever, R.Q.; Bobinet, K.J.; McCabe, K.; Mackenzie, E.R.; Fekete, E.; Kusnick, C.A.; Baime, M. Effective and viable mind-body stress reduction in the workplace: A randomized controlled trial. J. Occup. Health Psychol. 2012, 17, 246. [Google Scholar] [CrossRef]

- Black, D.S. Mindfulness research guide: A new paradigm for managing empirical health information. Mindfulness 2010, 1, 174–176. [Google Scholar] [CrossRef]

- Weick, K.E.; Roberts, K.H. Collective mind in organizations: Heedful interrelating on flight decks. Adm. Sci. Q. 1993, 38, 357–381. [Google Scholar] [CrossRef]

- Zhang, J.; Wu, C. The influence of dispositional mindfulness on safety behaviors: A dual process perspective. Accid. Anal. Prev. 2014, 70, 24–32. [Google Scholar] [CrossRef]

- Ocasio, W. Attention to attention. Organ. Sci. 2011, 22, 1286–1296. [Google Scholar] [CrossRef]

- Dreyfus, G. Is mindfulness present-centered and non-judgmental? A discussion of the cognitive dimensions of mindfulness. Contemp. Buddhism 2011, 12, 41–54. [Google Scholar] [CrossRef]

- Ray, J.L.; Baker, L.T.; Plowman, D.A. Organizational mindfulness in business schools. Acad. Manag. Learn. Educ. 2011, 10, 188–203. [Google Scholar]

- Katila, R.; Ahuja, G. Something old something new: A longitudinal study of search behavior and new product introduction. Acad. Manag. J. 2002, 45, 1183–1194. [Google Scholar]

- Rosenkopf, L.; Nerkar, A. Beyond local search: Boundary-spanning 2001, exploration, and impact in the optical disk industry. Strateg. Manag. J. 2001, 22, 287–306. [Google Scholar] [CrossRef]

- Castellion, G.; Markham, S.K. Perspective: New product failure rates: Influence of argumentum ad populum and self-interest. J. Prod. Innov. Manag. 2013, 30, 976–979. [Google Scholar] [CrossRef]

- Crawford, C.M. Marketing research and the new product failure rate. J. Mark. 1977, 41, 51–61. [Google Scholar] [CrossRef]

- Gourville, J.T. Eager sellers and stony buyers: Understanding the psychology of new-product adoption. Harv. Bus. Rev. 2006, 84, 98–106, 145. [Google Scholar]

- Masicampo, E.J.; Baumeister, R.F. Relating mindfulness and self-regulatory processes. Psychol. Inq. 2007, 18, 255–258. [Google Scholar] [CrossRef]

- Papies, E.K.; Barsalou, L.W.; Custers, R. Mindful attention prevents mindless impulses. Soc. Psychol. Personal. Sci. 2012, 3, 291–299. [Google Scholar] [CrossRef]

- Kirk, U.; Brown, K.W.; Downar, J. Adaptive neural reward processing during anticipation and receipt of monetary rewards in mindfulness meditators. Soc. Cogn. Affect. Neurosci. 2015, 10, 752–759. [Google Scholar] [CrossRef]

- BarNir, A.; Gallaugher, J.M.; Auger, P. Business process digitization strategy, and the impact of firm age and size: The case of the magazine publishing industry. J. Bus. Ventur. 2003, 18, 789–814. [Google Scholar] [CrossRef]

- Hannan, M.T.; Freeman, J. Structural inertia and organizational change. Am. Sociol. Rev. 1984, 49, 149–164. [Google Scholar] [CrossRef]

- Smallwood, J.; Schooler, J.W. The science of mind wandering: Empirically navigating the stream of consciousness. Psychology 2015, 66, 487–518. [Google Scholar] [CrossRef]

- Nohria, N.; Gulati, R. Is slack good or bad for innovation? Acad. Manag. J. 1996, 39, 1245–1264. [Google Scholar] [CrossRef]

- Greve, H.R. Organizational Learning from Performance Feedback—A Behavioral Perspective on Innovation and Change; Cambridge University Press: New York, NY, USA, 2003. [Google Scholar]

- Banalieva, E.R.; Eddleston, K.A.; Zellweger, T.M. When do family firms have an advantage in transitioning economies? Toward a dynamic institution-based view. Strateg. Manag. J. 2015, 36, 1358–1377. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. Organizational Structure as a Decentralization Device: Evidence from Corporate Pyramids. 2007. Available online: https://dx.doi.org/10.2139/ssrn.963430 (accessed on 21 May 2019).

- Qian, C.; Wang, H.; Geng, X.; Yu, Y. Rent appropriation of knowledge-based assets and firm performance when institutions are weak: A study of Chinese publicly listed firms. Strateg. Manag. J. Forthcom. 2017, 38, 892–911. [Google Scholar] [CrossRef]

- Xia, J.; Ma, X.; Lu, J.W.; Yiu, D.W. Outward foreign direct investment by emerging market firms: A resource dependence logic. Strateg. Manag. J. 2014, 35, 1343–1363. [Google Scholar] [CrossRef]

- Zhu, H.; Toru, Y. Contingent value of director identification: The role of government directors in monitoring and resource provision in an emerging economy. Strateg. Manag. J. 2016, 37, 1787–1807. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Innovation and learning: The two faces of R & D. Econ. J. 1989, 99, 569–596. [Google Scholar]

- Dosi, G. Sources, procedures, and microeconomic effects of innovation. J. Econ. Lit. 1988, 26, 1120–1171. [Google Scholar]

- Hülsheger, U.R.; Alberts, H.J.E.M.; Feinholdt, A.; Lang, J.W.B. Benefits of mindfulness at work: The role of mindfulness in emotion regulation, emotional exhaustion, and job satisfaction. J. Appl. Psychol. 2013, 98, 310–325. [Google Scholar] [CrossRef]

- Kabat-Zinn, J. Mindfulness-based interventions in context: Past, present, and future. Clin. Psychol. Sci. Pract. 2003, 10, 144–156. [Google Scholar] [CrossRef]

- Reb, J.; Narayanan, J.; Chaturvedi, S. Leading mindfully: Two studies on the influence of supervisor trait mindfulness on employee well-being and performance. Mindfulness 2014, 5, 36–45. [Google Scholar] [CrossRef]

- Pennebaker, J.W.; Graybeal, A. Patterns of natural language use: Disclosure personality, and social integration. Curr. Dir. Psychol. Sci. 2001, 10, 90–93. [Google Scholar] [CrossRef]

- Huang, C.L.; Chung, C.K.; Hui, N.; Lin, Y.C.; Seih, Y.T.; Chen, W.C.; Pennebaker, J.W. The development of the Chinese linguistic inquiry and word count dictionary. Chin. J. Psychol. 2012, 54, 185–201. [Google Scholar]

- Voss, G.B.; Sirdeshmukh, D.; Voss, Z.G. The effects of slack resources and environmental threat on product exploration and exploitation. Acad. Manag. J. 2008, 51, 147–164. [Google Scholar] [CrossRef]

- Chang, Y.C. Benefits of co-operation on innovative performance: Evidence from integrated circuits and biotechnology firms in the UK and Taiwan. RD Manag. 2003, 33, 425–437. [Google Scholar] [CrossRef]

- Leiponen, A. Organization of knowledge and innovation: The case of Finnish business services. Ind. Innov. 2005, 12, 185–203. [Google Scholar] [CrossRef]

- Boyd, B.K. CEO duality and firm performance: A contingency model. Strateg. Manag. J. 1995, 16, 301–312. [Google Scholar] [CrossRef]

- Aiken, L.S.; West, S.G. Multiple Regression: Testing and Interpreting Interactions; Sage: Thousand Oaks, CA, USA, 1991. [Google Scholar]

- Di Fabio, A. The psychology of sustainability and sustainable development for well-being in organizations. Front. Psychol. 2017, 8, 1534. [Google Scholar] [CrossRef]

- Zhao, X.; Chen, S.; Xiong, C. Organizational attention to corporate social responsibility and corporate social performance: The moderating effects of corporate governance. Bus. Ethics A Eur. Rev. 2016, 25, 386–399. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Mean | SD | Median | Min | Max | First Quartile | Third Quartile | |

|---|---|---|---|---|---|---|---|

| 1. Profitability | 0.0122 | 1.0182 | 0.0274 | −48.3159 | 4.8366 | 0.0067 | 0.0585 |

| 2. Sales growth | 0.5876 | 14.2534 | 0.0913 | −28.4967 | 665.5401 | -0.0519 | 0.2352 |

| 3. Financial resources | 0.0318 | 0.1336 | 0.0338 | −4.2696 | 0.5227 | -0.0047 | 0.0783 |

| 4. Financial leverage | 0.5657 | 1.3738 | 0.5150 | 0.0000 | 63.9712 | 0.3744 | 0.6631 |

| 5. Firm size | 9.3943 | 0.7004 | 9.3755 | 4.8001 | 11.7993 | 9.0350 | 9.8069 |

| 6. State-ownership | 0.5547 | 0.4971 | 1 | 0 | 1 | 0 | 1 |

| 7. CEO duality | 0.1417 | 0.3488 | 0 | 0 | 1 | 0 | 0 |

| 8. Board independence | 0.3643 | 0.0515 | 0.3333 | 0.1818 | 0.6667 | 0.3333 | 0.3750 |

| 9. Market munificence | −0.0184 | 0.1633 | −0.0002 | −4.6277 | 0.9123 | -0.0008 | -0.0001 |

| 10. Market dynamism | 0.0128 | 0.1316 | 0.0000 | 0.0000 | 2.7845 | 0.0000 | 0.0003 |

| 11. Attention to past | 0.2099 | 0.0891 | 0.2117 | 0.0000 | 0.4124 | 0.1417 | 0.2810 |

| 12. Attention to future | 0.5771 | 0.1786 | 0.5732 | 0.0000 | 0.9785 | 0.4368 | 0.7122 |

| 13. Firm age | 15.3618 | 4.2027 | 15 | 1 | 30 | 13 | 18 |

| 14. Slack resource | 0.0078 | 0.1000 | 0.0028 | −1.2685 | 0.7202 | -0.0282 | 0.0376 |

| 15. Past financial performance | 0.0286 | 0.3715 | 0.0287 | −16.2940 | 4.4884 | 0.0055 | 0.0594 |

| 16. Endogeneity control | 0.06 | 0.03 | 0.07 | −0.28 | 0.23 | 0.05 | 0.08 |

| 17. Managerial mindfulness | 0.35 | 0.18 | 0.33 | 0.00 | 1.00 | 0.22 | 0.48 |

| 18. R&D Decision | 0.8622 | 0.3448 | 1 | 0 | 1 | 1 | 1 |

| 19. R&D Intensity (%) | 1.36 | 1.34 | 1.06 | 0.00 | 6.86 | 0.18 | 2.16 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Profitability | 1 | ||||||||||||||||||

| 2.Sales growth | 0.002 | 1 | |||||||||||||||||

| 3. Financial resources | −0.030 | −0.007 | 1 | ||||||||||||||||

| 4.Financial leverage | −0.952 ** | 0.003 | −0.036 | 1 | |||||||||||||||

| 5.Firm size | 0.059 ** | 0.017 | 0.218 ** | −0.074 ** | 1 | ||||||||||||||

| 6. State-ownership | 0.017 | 0.006 | −0.014 | −0.016 | 0.230 ** | 1 | |||||||||||||

| 7.CEO duality | 0.008 | −0.004 | 0.013 | −0.013 | 0.008 | −0.009 | 1 | ||||||||||||

| 8. Board independence | −0.013 | 0.006 | −0.041 * | 0.009 | −0.030 | 0.019 | 0.023 | 1 | |||||||||||

| 9.Market munificence | −0.004 | 0.003 | −0.014 | 0.011 | 0.061 ** | 0.069 ** | −0.013 | 0.011 | 1 | ||||||||||

| 10.Market dynamism | 0.001 | −0.004 | −0.053 * | −0.009 | −0.093 ** | −0.053 * | 0.020 | −0.013 | −0.373 ** | 1 | |||||||||

| 11.Attention to past | 0.050 * | 0.005 | 0.107 ** | −0.057 ** | 0.414 ** | 0.264 ** | −0.012 | −0.113 ** | 0.016 | −0.017 | 1 | ||||||||

| 12.Attention to future | −0.050 * | −0.008 | −0.104 ** | 0.057 ** | −0.414 ** | −0.262 ** | 0.010 | 0.141 ** | −0.011 | 0.015 | −0.966 ** | 1 | |||||||

| 13.Firm age | −0.006 | 0.052 * | −0.033 | 0.022 | −0.111 ** | −0.003 | 0.073 ** | −0.058 ** | 0.009 | −0.004 | −0.254 ** | 0.245 ** | 1 | ||||||

| 14.Slack resource | 0.047 * | 0.025 | 0.142 ** | −0.020 | 0.063 ** | −0.023 | 0.014 | 0.010 | −0.001 | 0.009 | 0.034 | −0.032 | −0.044 * | 1 | |||||

| 15. Past financial performance | 0.929 ** | −0.002 | −0.047 * | −0.881 ** | 0.028 | −0.007 | 0.010 | 0.000 | −0.007 | −0.001 | 0.045* | −0.045 * | −0.007 | −0.024 | 1 | ||||

| 16.Endogeneity control | −0.007 | 0.041 | −0.064 ** | 0.032 | 0.067 ** | 0.355 ** | 0.098 ** | 0.001 | 0.041 | −0.042 * | −0.021 | 0.018 | 0.589 ** | −0.056 ** | −0.002 | 1 | |||

| 17.Managerial mindfulness | −0.018 | 0.029 | −0.030 | 0.016 | 0.010 | 0.068 ** | 0.022 | 0.016 | 0.042 * | −0.012 | −0.018 | 0.034 | 0.013 | −0.063 ** | 0.011 | 0.121 ** | 1 | ||

| 18.R&D Decision | −0.008 | −0.005 | 0.117 ** | −0.039 | 0.340 ** | 0.097 ** | 0.005 | −0.027 | 0.021 | −0.067 ** | 0.152 ** | −0.150 ** | −0.093 ** | 0.001 | −0.018 | 0.079 ** | 0.077 ** | 1 | |

| 19.R&D Intensity (%) | 0.030 | −0.025 | 0.117 ** | −0.060 ** | 0.191 ** | 0.019 | 0.013 | −0.015 | 0.019 | −0.048 * | 0.075 ** | −0.080 ** | −0.077 ** | 0.033 | 0.041 * | 0.039 | 0.045 ** | 0.404 ** | 1 |

| RD | RD | RD | RD | |

|---|---|---|---|---|

| Constant | −8.871 *** | −8.986 *** | −8.702 ** | −8.792 ** |

| (−3.38) | (−3.52) | (−3.15) | (−3.26) | |

| Profitability | −2.148 ** | −2.095 ** | −2.138 ** | −2.085 ** |

| (−3.18) | (−3.17) | (−3.17) | (−3.16) | |

| Sales growth | −0.00584 | −0.00585 | −0.00585 | −0.00587 |

| (−0.82) | (−0.79) | (−0.83) | (−0.80) | |

| Financial resources | 2.011 | 2.004 * | 2.014 | 2.007 * |

| (1.95) | (1.96) | (1.95) | (1.97) | |

| Financial leverage | −2.007 *** | −1.982 *** | −2.003 *** | −1.978 *** |

| (−3.89) | (−3.93) | (−3.88) | (−3.92) | |

| Firm size | 1.487 *** | 1.475 *** | 1.463 *** | 1.444 *** |

| (5.62) | (5.74) | (5.53) | (5.62) | |

| State-ownership | −0.264 | −0.260 | −0.284 | −0.285 |

| (−0.78) | (−0.79) | (−0.84) | (−0.87) | |

| CEO duality | −0.0330 | −0.0523 | −0.0351 | −0.0548 |

| (−0.14) | (−0.23) | (−0.15) | (−0.24) | |

| Board independent | −0.213 | −0.353 | −0.0597 | −0.156 |

| (−0.09) | (−0.16) | (−0.03) | (−0.07) | |

| Market munificence | 0.251 | 0.211 | 0.252 | 0.212 |

| (0.47) | (0.42) | (0.47) | (0.42) | |

| Market dynamism | −1.121 | −1.100 | −1.119 | −1.098 |

| (−1.66) | (−1.72) | (−1.65) | (−1.72) | |

| Attention to past | −0.314 | −0.446 | ||

| (−0.18) | (−0.26) | |||

| Attention to future | −0.157 | −0.178 | ||

| (−0.18) | (−0.20) | |||

| Firm age | −0.0977 * | −0.105 * | −0.0951 * | −0.101 * |

| (−2.31) | (−2.51) | (−2.26) | (−2.44) | |

| Slack resources | −1.555 * | −1.514 | −1.572 * | −1.534 * |

| (−1.98) | (−1.95) | (−2.00) | (−1.98) | |

| Past financial performance | −1.631 | −1.692 | −1.645 | −1.709 |

| (−1.19) | (−1.28) | (−1.21) | (−1.29) | |

| Endogeneity control | 32.53 *** | 30.64 *** | 32.52 *** | 30.63 *** |

| (8.40) | (8.11) | (8.40) | (8.11) | |

| Managerial mindfulness | 0.919 + | 0.914 + | ||

| (1.92) | (1.91) | |||

| lnsig2u | ||||

| Constant | 2.465 *** | 2.353 *** | 2.466 *** | 2.354 *** |

| (15.60) | (14.68) | (15.60) | (14.67) | |

| Wald Chi | 129.95 *** | 130.9 *** | 129.67 *** | 130.46 *** |

| RDI (%) | RDI (%) | RDI (%) | RDI (%) | RDI (%) | RDI (%) | |

|---|---|---|---|---|---|---|

| Constant | −0.949 ** | −1.045 *** | −0.906 ** | −1.166 *** | −1.240 *** | −1.200 *** |

| (−3.27) | (−3.58) | (−3.21) | (−3.70) | (−3.92) | (−3.95) | |

| Profitability | −0.0801 | −0.0871 | −0.169 ** | −0.0781 | −0.0841 | −0.158 * |

| (−1.33) | (−1.40) | (−2.73) | (−1.28) | (−1.35) | (−2.53) | |

| Sales growth | −0.000807 | −0.000867 | −0.000906 | −0.000850 | −0.000890 | −0.000918 |

| (−1.46) | (−1.55) | (−1.64) | (−1.50) | (−1.56) | (−1.64) | |

| Financial resources | 0.00768 | 0.00506 | 0.0909 | 0.00511 | 0.00236 | 0.0833 |

| (0.09) | (0.06) | (1.07) | (0.06) | (0.03) | (0.95) | |

| Financial leverage | −0.0723 | −0.0755 | −0.0526 | −0.0644 | −0.0691 | −0.0385 |

| (−1.92) | (−1.94) | (−1.40) | (−1.68) | (−1.76) | (−1.02) | |

| Firm size | 0.291 *** | 0.306 *** | 0.290 *** | 0.293 *** | 0.302 *** | 0.298 *** |

| (9.89) | (10.44) | (10.42) | (9.56) | (9.95) | (10.09) | |

| State-ownership | −0.196 *** | −0.197 *** | −0.209 *** | −0.179 *** | −0.190 *** | −0.190 *** |

| (−4.13) | (−4.23) | (−4.73) | (−3.70) | (−4.01) | (−4.13) | |

| CEO duality | 0.0323 | 0.0295 | 0.0427 * | 0.0223 | 0.0223 | 0.0270 |

| (1.66) | (1.44) | (2.29) | (1.06) | (1.03) | (1.27) | |

| Board independent | −0.576 * | −0.611 * | −0.609 * | −0.465 | −0.501 | −0.528 * |

| (−2.32) | (−2.44) | (−2.42) | (−1.82) | (−1.95) | (−2.05) | |

| Market munificence | −0.0778 | −0.0793 | −0.0649 | −0.0816 | −0.0840 | −0.0756 |

| (−0.88) | (−0.88) | (−0.71) | (−0.92) | (−0.93) | (−0.83) | |

| Market dynamism | −0.000999 | −0.0122 | −0.0214 | −0.00850 | −0.0183 | −0.0182 |

| (−0.01) | (−0.12) | (−0.21) | (−0.08) | (−0.18) | (−0.18) | |

| Attention to past | −0.405 | −0.507 * | −0.366 | |||

| (−1.87) | (−2.30) | (−1.81) | ||||

| Attention to future | 0.0588 | 0.0861 | 0.0953 | |||

| (0.49) | (0.71) | (0.82) | ||||

| Firm age | −0.0440 *** | −0.0462 *** | −0.0480 *** | −0.0420 *** | −0.0442 *** | −0.0454 *** |

| (−7.85) | (−8.37) | (−8.87) | (−7.42) | (−7.94) | (−8.25) | |

| Slack resources | 0.128 | 0.132 | 0.178 * | 0.128 | 0.131 | 0.180 * |

| (1.52) | (1.50) | (2.11) | (1.44) | (1.44) | (1.99) | |

| Past financial performance | 0.0636 | 0.0692 | 0.580 *** | 0.0866 | 0.0841 | 0.605 *** |

| (0.53) | (0.57) | (3.78) | (0.73) | (0.70) | (3.89) | |

| Endogeneity control | 6.264 *** | 6.236 *** | 6.271 *** | 6.157 *** | 6.154 *** | 6.174 *** |

| (14.74) | (14.46) | (14.15) | (14.24) | (14.10) | (13.84) | |

| Managerial mindfulness | 0.100 + | 0.113 * | 0.0971 + | 0.108 * | ||

| (1.87) | (2.07) | (1.80) | (1.98) | |||

| Managerial mindfulness X firm age | −0.0248 * | −0.0239 * | ||||

| (−1.92) | (−1.85) | |||||

| Managerial mindfulness X slack resources | 0.965 * | 0.947 * | ||||

| (1.84) | (1.78) | |||||

| Managerial mindfulness X past financial performance | −1.183 *** | −1.213 *** | ||||

| (−4.09) | (−4.16) | |||||

| Wald Chi | 375.52 *** | 388.07 *** | 403.88 *** | 366.37 *** | 379.11 *** | 392.53 *** |

| Constant | −7.46 *** | −7.52 *** |

| (−8.63) | (−8.72) | |

| Profitability | −0.513 ** | −0.487 ** |

| (−2.92) | (−2.79) | |

| Sales growth | −0.00114 | −0.00124 |

| (−0.94) | (−1.02) | |

| Financial resources | 0.988 *** | 0.965 *** |

| (−3.61) | (−3.53) | |

| Financial leverage | −0.255 * | −0.243 * |

| (−2.24) | (−2.14) | |

| Firm size | 0.621 *** | 0.619 *** |

| (−7.69) | (−7.7) | |

| State-ownership | −0.0192 | −0.0265 |

| (−0.14) | (−0.19) | |

| CEO duality | −0.0161 | −0.0183 |

| (−0.32) | (−0.36) | |

| Board independence | −0.641 | −0.626 |

| (−1.15) | (−1.12) | |

| Market munificence | −0.111 | −0.119 |

| (−0.81) | (−0.86) | |

| Market dynamism | 0.141 | 0.123 |

| (−0.75) | (−0.66) | |

| Attention to past | 3.31 *** | 3.42 *** |

| (−4.85) | (−5.03) | |

| Attention to future | 2.26 *** | 2.31 *** |

| (−9.64) | (−9.85) | |

| Firm age | 0.0793 *** | 0.0731 *** |

| (−7.55) | (−6.84) | |

| Slack resource | −0.164 | −0.131 |

| (−0.86) | (−0.69) | |

| Managerial mindfulness | 0.563 * | 0.531 + |

| (−2.05) | (−1.95) | |

| sigma_u | 1.42 *** | 1.41 *** |

| (25.67) | (25.71) | |

| sigma_e | 0.718 *** | 0.719 *** |

| (55.20) | (55.22) | |

| Wald Chi | 256.78 *** | 262.63 *** |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hu, Y.; Zhao, X.; Chen, Y. The Influence of Managerial Mindfulness on Innovation: Evidence from China. Sustainability 2019, 11, 2914. https://doi.org/10.3390/su11102914

Hu Y, Zhao X, Chen Y. The Influence of Managerial Mindfulness on Innovation: Evidence from China. Sustainability. 2019; 11(10):2914. https://doi.org/10.3390/su11102914

Chicago/Turabian StyleHu, Yuanyuan, Xiaoping Zhao, and Yang Chen. 2019. "The Influence of Managerial Mindfulness on Innovation: Evidence from China" Sustainability 11, no. 10: 2914. https://doi.org/10.3390/su11102914