Stakeholder Role for Developing a Conceptual Framework of Sustainability in Organization

Abstract

:1. Introduction

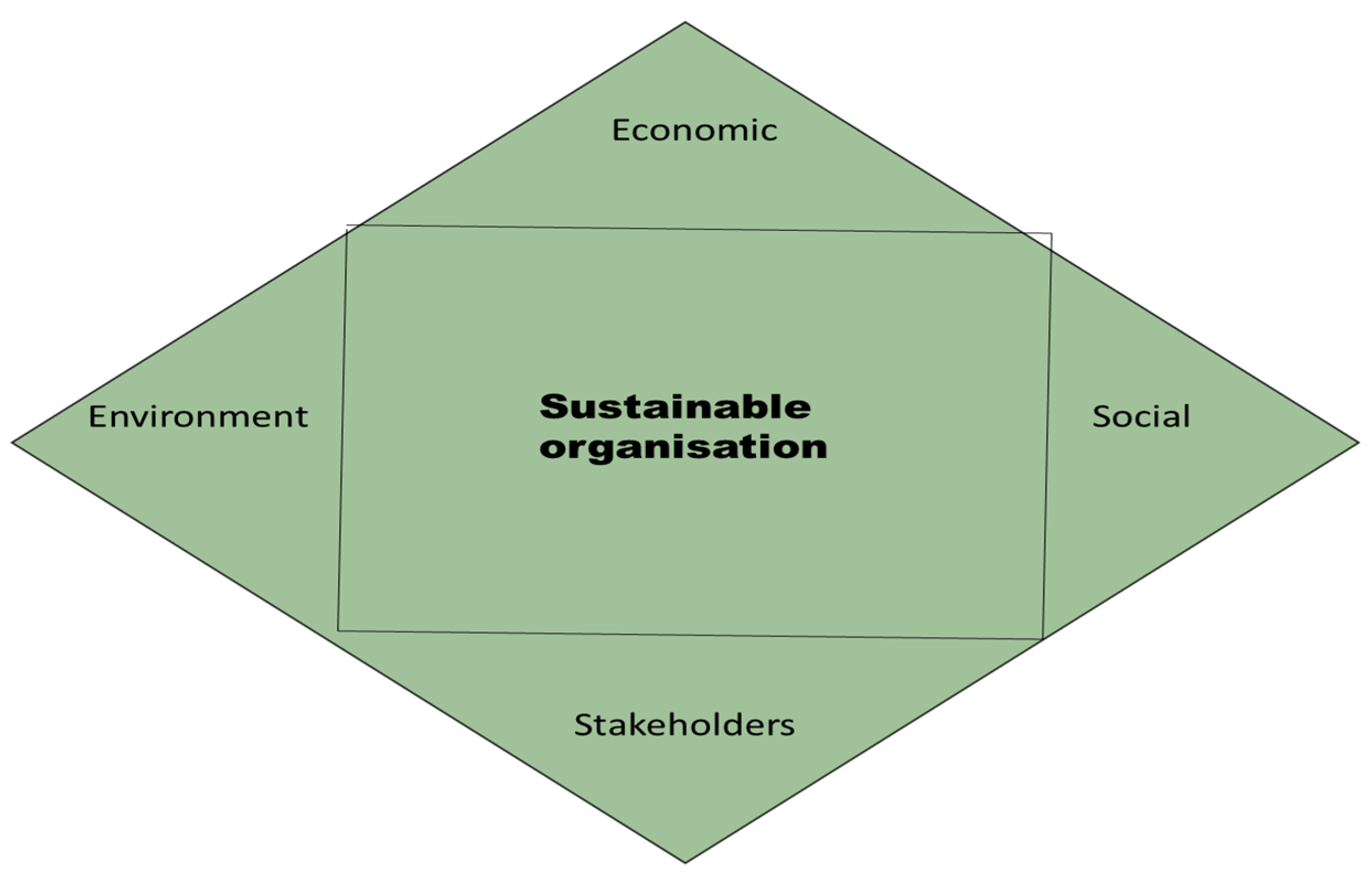

2. Sustainability in the Organization

3. Research Methodology

3.1. Content Analysis for Factor Identification

3.2. TISM Development for the Conceptualization of Sustainability in the Organization

3.3. t-Test for Data Verification

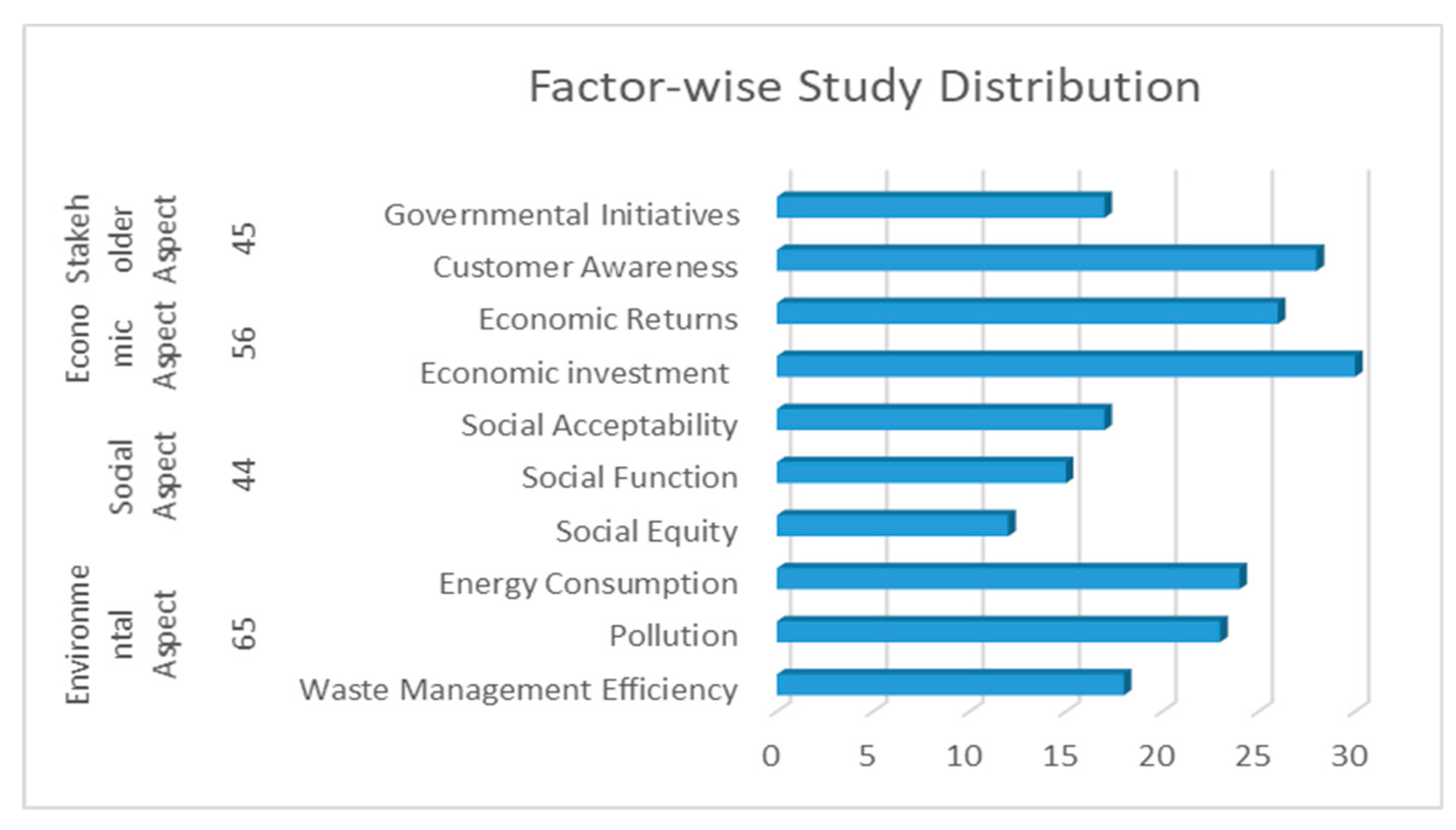

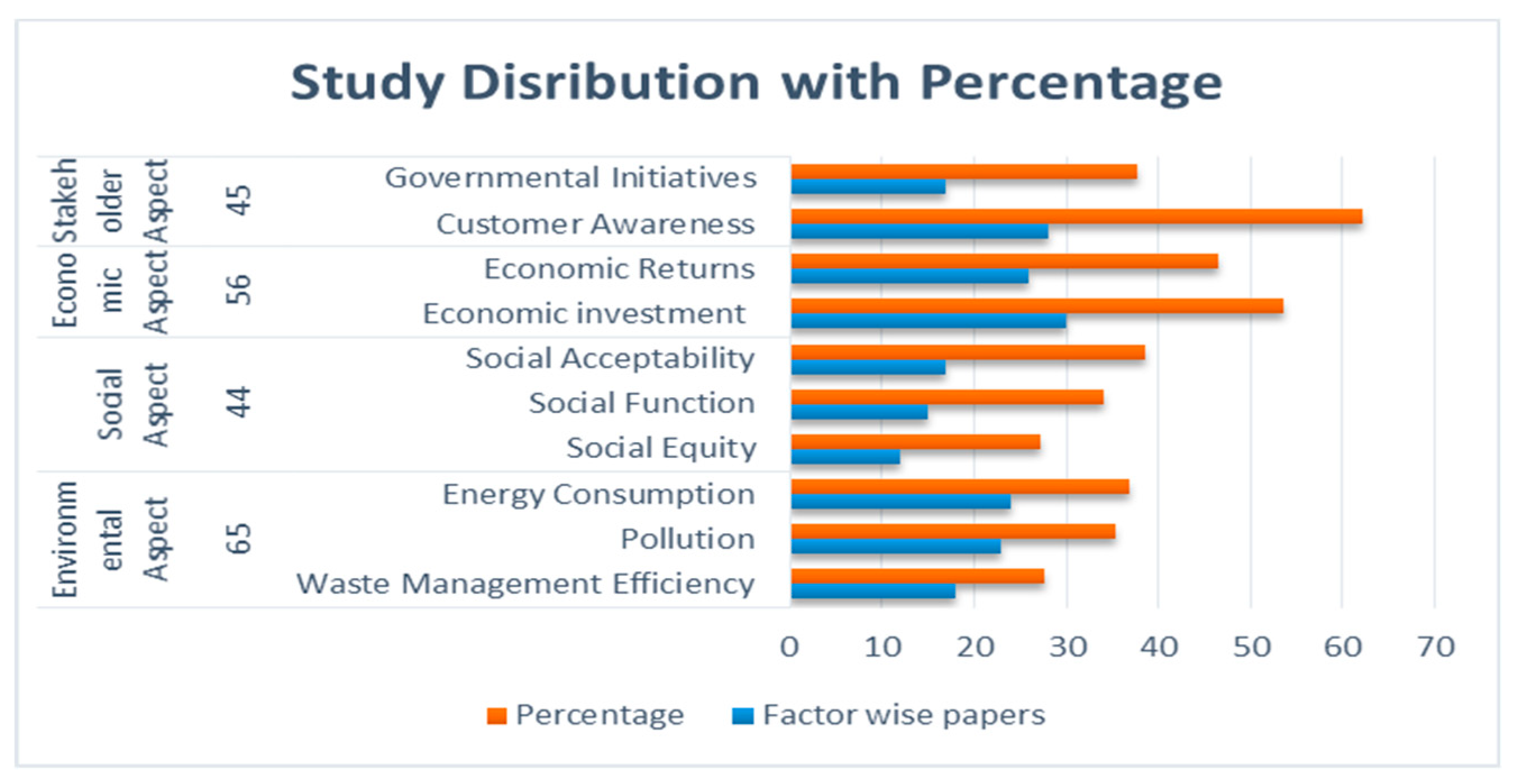

4. Step I: Identify and Verification of Factors in the Organizational Context through Content Analysis

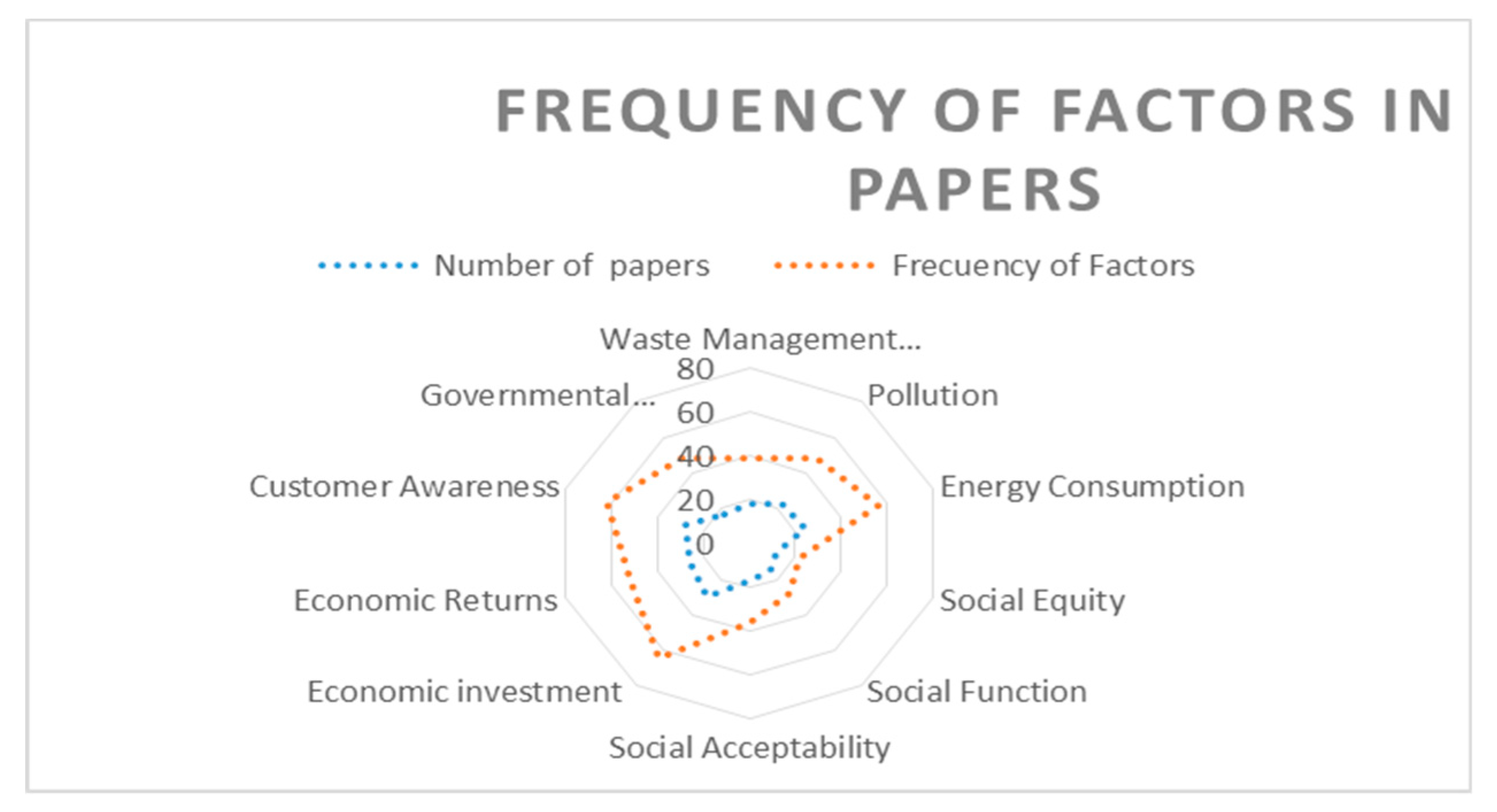

4.1. Descriptive Analysis

4.2. Verification of Identified Sustainability Factors in the Organization

4.3. Reliability Analysis

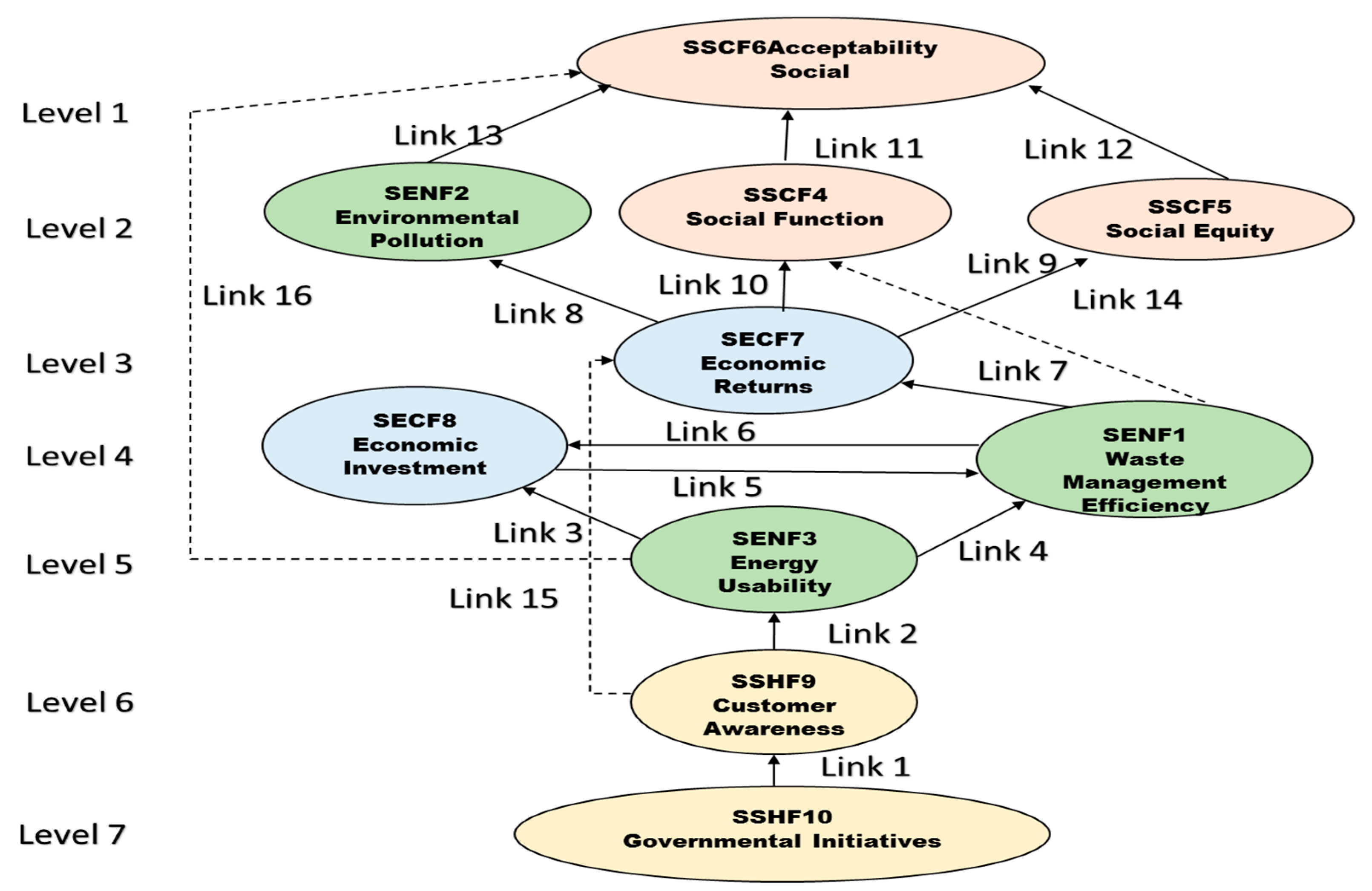

5. Step II: Develop the Hierarchical Relationship between the Sustainability Factors in the Organization Using TISM

Total Interpretive Structural Modeling (TISM)

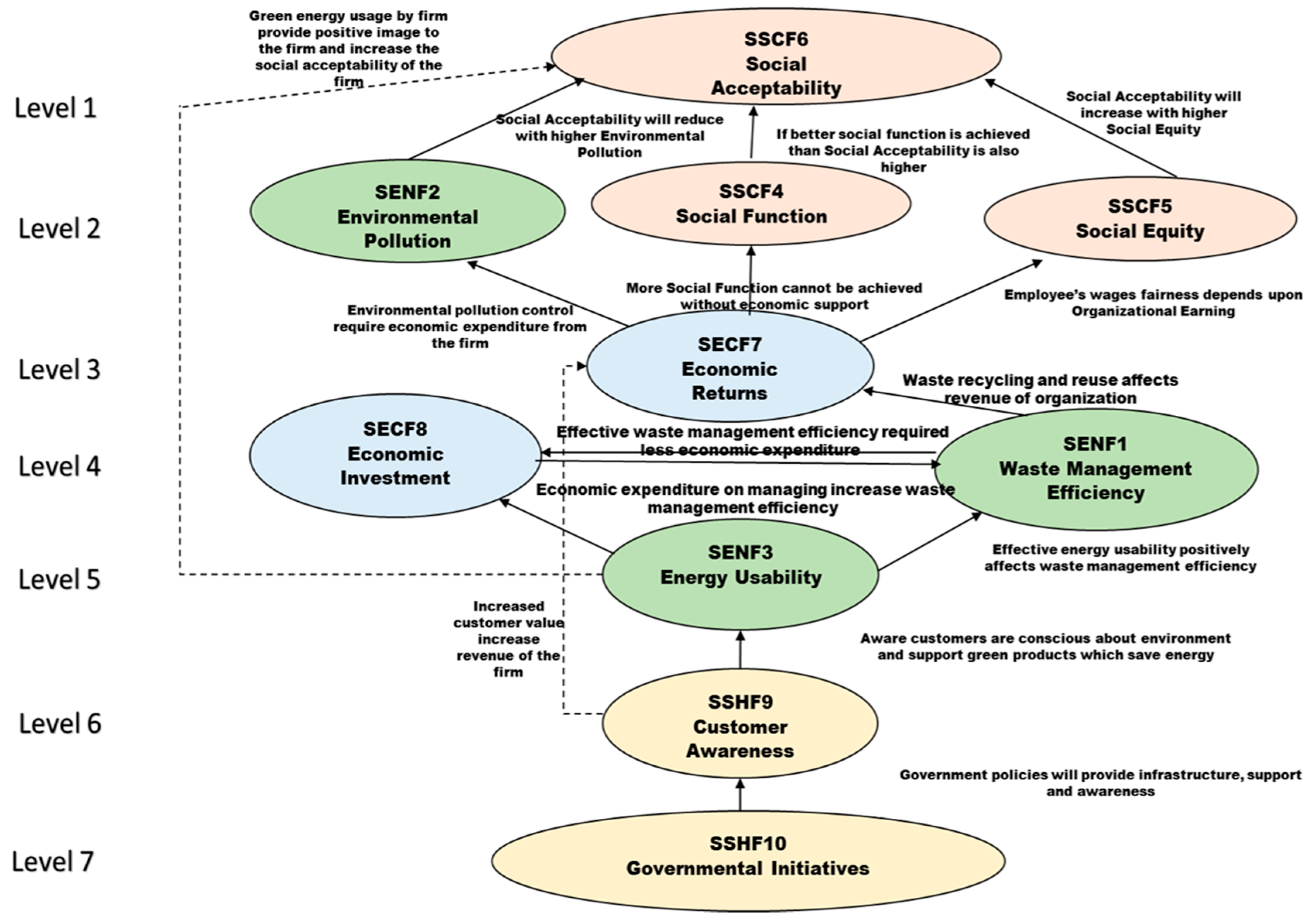

6. Step III: Validating the Hierarchical Model of Sustainability in the Organizational Context through Experts Opinion

Validation of TISM

7. Results and Discussion

7.1. Implications

7.2. Limitations

8. Conclusions and Future Research Directions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sustainability Factors | SENF1 | SENF2 | SENF3 | SSCF4 | SSCF5 | SSCF6 | SECF7 | SECF8 | SSHF9 | SSHF10 |

|---|---|---|---|---|---|---|---|---|---|---|

| SENF1 | 1 | 1 | 0 | 1 * | 1 * | 1 | 1 | 1 | 0 | 0 |

| SENF2 | 0 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| SENF3 | 1 | 1 | 1 | 1* | 1* | 1* | 1 | 1 | 0 | 0 |

| SSCF4 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 0 | 0 | 0 |

| SSCF5 | 0 | 0 | 0 | 0 | 1 | 1 | 0 | 0 | 0 | 0 |

| SSCF6 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 |

| SECF7 | 0 | 1 | 0 | 1 | 1 | 1 | 1 | 0 | 0 | 0 |

| SECF8 | 1 | 1 | 0 | 1 | 1 | 1 | 1 * | 1 | 0 | 0 |

| SSHF9 | 1 | 1 | 1 | 1 ** | 1 ** | 1 | 1 * | 1* | 1 | 0 |

| SSHF10 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Sustainability Factors | Reachability Set | Antecedent Set | Intersection Set | Level |

| SENF1 | 1,2,4,5,6,7,8 | 1,3,8,9,10 | 1,8 | |

| SENF2 | 2,6 | 1,2,3,7,8,9,10 | 2 | |

| SENF3 | 1,2,3,4,5,6,7,8 | 3,9,10 | 3 | |

| SSCF4 | 4,6 | 1,3,4,7,8,9,10 | 4 | |

| SSCF5 | 5,6 | 1,3,5,7,8,9,10 | 5 | |

| SSCF6 | 6 | 1,2,3,4,5,6,7,8,9,10 | 6 | 1 |

| SECF7 | 2,4,5,6,7 | 1,3,7,8,9,10 | 7 | |

| SECF8 | 1,2,4,5,6,7,8 | 1,3,8,9,10 | 1,8 | |

| SSHF9 | 1,2,3,4,5,6,7,8,9 | 9,10 | 9 | |

| SSHF10 | 1,2,3,4,5,6,7,8,9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SENF1 | 1,2,4,5,6,7,8 | 1,3,8,9,10 | 1,8 | |

| SENF2 | 2 | 1,2,3,7,8,9,10 | 2 | 2 |

| SENF3 | 1,2,3,4,5,6,7,8 | 3,9,10 | 3 | |

| SSCF4 | 4 | 1,3,4,7,8,9,10 | 4 | 2 |

| SSCF5 | 5 | 1,3,5,7,8,9,10 | 5 | 2 |

| SECF7 | 2,4,5,6,7 | 1,3,7,8,9,10 | 7 | |

| SECF8 | 1,2,4,5,6,7,8 | 1,3,8,9,10 | 1,8 | |

| SSHF9 | 1,2,3,4,5,6,7,8,9 | 9,10 | 9 | |

| SSHF10 | 1,2,3,4,5,6,7,8,9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SENF1 | 1,7,8 | 1,3,8,9,10 | 1,8 | |

| SENF3 | 1,3, 7,8 | 3,9,10 | 3 | |

| SECF7 | 7 | 1,3,7,8,9,10 | 7 | 3 |

| SECF8 | 1,7,8 | 1,3,8,9,10 | 1,8 | |

| SSHF9 | 1,3,7,8,9 | 9,10 | 9 | |

| SSHF10 | 1,3,7,8,9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SENF1 | 1,8 | 1,3,8,9,10 | 1,8 | 4 |

| SENF3 | 1,3,8 | 3,9,10 | 3 | |

| SECF8 | 1,8 | 1,3,8,9,10 | 1,8 | 4 |

| SSHF9 | 1,3,8,9 | 9,10 | 9 | |

| SSHF10 | 1,3,8,9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SENF1 | 3 | 3,9,10 | 3 | 5 |

| SSHF9 | 3,4,5,9 | 9,10 | 9 | |

| SSHF10 | 3,9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SSHF9 | 9 | 9,10 | 9 | 6 |

| SSHF10 | 9,10 | 10 | 10 | |

| Sustainability Factors | Reachability set | Antecedent set | Intersection set | Level |

| SSHF10 | 10 | 10 | 10 | 7 |

References

- Scheffer, M.; Carpenter, S.; Foley, J.A.; Folke, C.; Walker, B. Catastrophic shifts in ecosystems. Nature 2001, 413, 591–596. [Google Scholar] [CrossRef] [PubMed]

- Grewatsch, S.; Kleindienst, I. When does it pay to be good? Moderators and mediators in the corporate sustainability–corporate financial performance relationship: A critical review. J. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Lee, S.; Geum, Y.; Lee, H.; Park, Y. Dynamic and multidimensional measurement of product-service system (PSS) sustainability: A triple bottom line (TBL)-based system dynamics approach. J. Clean. Prod. 2012, 32, 173–182. [Google Scholar] [CrossRef]

- Hall, T.J. The triple bottom line: What is it and how does it work? Indiana Bus. Rev. 2011, 86, 4. [Google Scholar]

- Gray, R.; Milne, M. Sustainability reporting: who’s kidding whom? Chart. Account. J. N. Z. 2002, 81, 66–70. [Google Scholar]

- Gray, R. Does sustainability reporting improve corporate behaviour?: Wrong question? Right time? Account. Bus. Res. 2006, 36, 65–88. [Google Scholar] [CrossRef]

- Walton, S.; Tregidga, H.; Milne, M.J. The Triple-Bottom-Line: Benchmarking New Zealand’s Early Reporters; University of Otago: Dunedin, New Zealand, 2003. [Google Scholar]

- Bebbington, J. Sustainable development: A review of the international development, business and accounting literature. In Accounting Forum; Blackwell Publishers Ltd.: Hoboken, NJ, USA, 2001; Volume 25, pp. 128–157. [Google Scholar]

- Erusalimsky, A.; Gray, R.; Spence, C. Towards a more systematic study of standalone corporate social and environmental: An exploratory pilot study of UK reporting. Soc. Environ. Account. J. 2006, 26, 12–19. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.J. Sustainability in action: Identifying and measuring the key performance drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Kopelman, S.; Weber, J.M.; Messick, D.M. Commons dilemma management: Recent experimental results. In Proceedings of the 8th Biennial Conference of the International Society for the Study of Common Property, Bloomington, IN, USA, 31 May–4 June 2000. [Google Scholar]

- Holling, C.S. The Resilience of Terrestrial Ecosystems; Local Surprise and Global Change. In Sustainable Development of the Biosphere; Clark, W.C., Munn, R.E., Eds.; Cambridge University Press: Cambridge, UK, 1986; pp. 292–317. [Google Scholar]

- Chatterjee, K.; Pamucar, D.; Zavadskas, E.K. Evaluating the performance of suppliers based on using the R’AMATEL-MAIRCA method for green supply chain implementation in electronics industry. J. Clean. Prod. 2018, 184, 101–129. [Google Scholar] [CrossRef]

- Lozano, R. Envisioning sustainability three-dimensionally. J. Clean. Prod. 2008, 16, 1838–1846. [Google Scholar] [CrossRef]

- Lele, S.M. Sustainable development: A critical review. World Dev. 1991, 19, 607–621. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Singla, A.; Ahuja, I.P.S.; Sethi, A.P.S. The effects of demand pull strategies on sustainable development in manufacturing industries. Int. J. Innov. Eng. Technol. 2017, 8, 27–34. [Google Scholar]

- Ulhoi, J.P.; Madsen, H.; Kjaer, M. Training in Environmental Management: Industry and Sustainability; Office for Official Publications of the European Communities: Luxembourg, 1999; p. 43. [Google Scholar]

- Stenzel, P.L. Sustainability, the triple bottom line, and the global reporting initiative. Glob. Edge Bus. Rev. 2010, 4, 1–2. [Google Scholar]

- Sushil. Interpreting the Interpretive Structural Model. Glob. J. Flex. Syst. Manag. 2012, 13, 87–106. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Bansal, P. The corporate challenges of sustainable development. Acad. Manag. Exec. 2002, 16, 122–131. [Google Scholar] [CrossRef]

- Hart, S.L.; Milstein, M.B. Creating sustainable value. Acad. Manag. Exec. 2003, 17, 56–67. [Google Scholar] [CrossRef]

- Roberts, B.; Cohen, M. Enhancing sustainable development by triple value adding to the core business of government. Econ. Dev. Q. 2002, 16, 127–137. [Google Scholar] [CrossRef]

- Jovane, F.; Yoshikawa, H.; Alting, L.; Boer, C.R.; Westkamper, E.; Williams, D.; Paci, A.M. The incoming global technological and industrial revolution towards competitive sustainable manufacturing. CIRP Ann.-Manuf. Technol. 2008, 57, 641–659. [Google Scholar] [CrossRef]

- Nguyen, D.K.; Slater, S.F. Hitting the sustainability sweet spot: Having it all. J. Bus. Strategy 2010, 31, 5–11. [Google Scholar] [CrossRef]

- Garvare, R.; Johansson, P. Management for sustainability–a stakeholder theory. Total Qual. Manag. 2010, 21, 737–744. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Garvare, R.; Ahmad, N. Including sustainability in business excellence models. Total Qual. Manag. Bus. Excell. 2011, 22, 773–786. [Google Scholar] [CrossRef]

- Zollo, M.; Cennamo, C.; Neumann, K. Beyond what and why: Understanding organizational evolution towards sustainable enterprise models. Organ. Environ. 2013, 26, 241–259. [Google Scholar] [CrossRef]

- Dorsey, S.G.; Schiffman, R.; Redeker, N.S.; Heitkemper, M.; McCloskey, D.J.; Weglicki, L.S.; Grady, P.A. NINR Centers of Excellence: A logic model for sustainability, leveraging resources and collaboration to accelerate cross-disciplinary science. Nurs. Outlook 2014, 62, 384. [Google Scholar] [CrossRef] [PubMed]

- Paracchini, M.L.; Bulgheroni, C.; Borreani, G.; Tabacco, E.; Banterle, A.; Bertoni, D.; De Paola, C. A diagnostic system to assess sustainability at a farm level: The SOSTARE model. Agric. Syst. 2015, 133, 35–53. [Google Scholar] [CrossRef]

- Byerlee, D. Technical change, productivity, and sustainability in irrigated cropping systems of South Asia: Emerging issues in the post-green revolution Era. J. Int. Dev. 1992, 4, 477–496. [Google Scholar] [CrossRef]

- Shrivastava, P. Environmental technologies and competitive advantage. Strateg. Manag. J. 1995, 16, 183–200. [Google Scholar] [CrossRef]

- Phillips, R.A.; Reichart, J. The environment as a stakeholder? A fairness-based approach. J. Bus. Ethics 2000, 23, 185–197. [Google Scholar] [CrossRef]

- Kefalas, A.G. The environmentally sustainable organization (ESO): A systems approach. Ethics Environ. 2001, 6, 90–105. [Google Scholar]

- Swart, R.J.; Raskin, P.; Robinson, J. The problem of the future: Sustainability science and scenario analysis. Glob. Environ. Chang. 2004, 14, 137–146. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T. Sustainable value added—Measuring corporate contributions to sustainability beyond eco-efficiency. Ecol. Econ. 2004, 48, 173–187. [Google Scholar] [CrossRef]

- Du Pisani, J.A. Sustainable development–historical roots of the concept. Environ. Sci. 2006, 3, 83–96. [Google Scholar] [CrossRef]

- Darby, L.; Jenkins, H. Applying sustainability indicators to the social enterprise business model: The development and application of an indicator set for Newport Wastesavers, Wales. Int. J. Soc. Econ. 2006, 33, 411–431. [Google Scholar] [CrossRef]

- Sen, S.K.; Swierczek, F.W. Societal, environmental and stakeholder value drivers: A case analysis of us and Asian international firms. J. Hum. Values 2007, 13, 119–134. [Google Scholar] [CrossRef]

- Parrish, B.D. Designing the sustainable enterprise. Futures 2007, 39, 846–860. [Google Scholar] [CrossRef]

- Badi, I.; Abdulshahed, A. Prediction of the surface roughness for the end milling process using Adaptive Neuro-Fuzzy Inference System ANFIS. Oper. Res. Eng. Sci. Theory Appl. 2018, 1, 1–12. [Google Scholar] [CrossRef]

- Kocmanova, A.; Docekalova, M.; Nemecek, P.; Simberova, I. Sustainability: Environmental, Social and Corporate Governance Performance in Czech SMEs. In Proceedings of the 15th World Multi-Conference on Systemics, Cybernetics and Informatics, Orlando, FL, USA, 19–22 July 2011; pp. 94–99. [Google Scholar]

- Kiron, D.; Kruschwitz, N.; Haanaes, K.; Velken, I.V.S. Sustainability nears a tipping point. MIT Sloan Manag. Rev. 2012, 53, 69. [Google Scholar] [CrossRef]

- Barth, M.; Michelsen, G. Learning for change: An educational contribution to sustainability science. Sustain. Sci. 2013, 8, 103–119. [Google Scholar] [CrossRef]

- Munoz, E.; Capon-Garcia, E.; Lainez, J.M.; Espuna, A.; Puigjaner, L. Considering environmental assessment in an ontological framework for enterprise sustainability. J. Clean. Prod. 2013, 47, 149–164. [Google Scholar] [CrossRef]

- Jain, A. The Concept of Triple Bottom Line Reporting and India’s Perspective. Corp. Gov. 2014, 4, 5. [Google Scholar]

- Rambaud, A.; Richard, J. The “Triple Depreciation Line” instead of the “Triple Bottom Line”: Towards a genuine integrated reporting. Crit. Perspect. Account. 2015, 33, 92–116. [Google Scholar] [CrossRef]

- Roy, J.; Adhikary, K.; Kar, S.; Pamucar, D. A rough strength relational DEMATEL model for analysing the key success factors of hospital service quality. Decis. Mak. Appl. Manag. Eng. 2018, 1, 121–142. [Google Scholar] [CrossRef]

- Stojčić, M. Application of ANFIS model in road traffic and transportation: A literature review from 1993 to 2018. Oper. Res. Eng. Sci. Theory Appl. 2018, 1, 40–61. [Google Scholar] [CrossRef]

- Mukhametzyanov, I.; Pamucar, D. A sensitivity analysis in MCDM problems: A statistical approach. Decis. Mak. Appl. Manag. Eng. 2018, 1, 51–80. [Google Scholar] [CrossRef]

- Liu, F.; Aiwu, G.; Lukovac, V.; Vukic, M. A multicriteria model for the selection of the transport service provider: A single valued neutrosophic DEMATEL multicriteria model. Decis. Mak. Appl. Manag. Eng. 2018, 1, 121–130. [Google Scholar] [CrossRef]

- Popovic, M.; Kuzmanovic, M.; Savic, G. A comparative empirical study of Analytic Hierarchy Process and Conjoint analysis: Literature review. Decis. Mak. Appl. Manag. Eng. 2018, 1, 153–163. [Google Scholar] [CrossRef]

- Holsti, O.R. Content Analysis for the Social Sciences and Humanities; Addison-Wesley Pub. Co.: Reading, MA, USA, 1969. [Google Scholar]

- Kassarjian, H.H. Content Analysis in Consumer Research. J. Consum. Res. 1977, 4, 8–18. [Google Scholar] [CrossRef]

- Krippendorff, K. Content Analysis: An Introduction to its Methodology; Sage: Thousand Oaks, CA, USA, 2004. [Google Scholar]

- Sushil. Flexibility, Viability and Sustainability. Glob. J. Flex. Syst. Manag. 2012, 12, 1–2. [Google Scholar] [CrossRef]

- Sushil. How to Check Correctness of Total Interpretive Structural Models? Ann. Oper. Res. 2016. [Google Scholar] [CrossRef]

- Weber, R.P. Basic Content Analysis, 2nd ed.; SAGE Publications Inc.: Newbury Park, CA, USA, 1990. [Google Scholar]

- Verma, J.P. Data Analysis in Management with SPSS Software; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2012. [Google Scholar]

- Scott, F.E. Promotion and protection of human health in the context of sustainable development: Canada and USA; WEHAB Working Group UN: New York, NY, USA, 2009. [Google Scholar]

- Bamgbade, J.A.; Kamaruddeen, A.M.; Nawi, M.N.M. Malaysian construction firms’ social sustainability via organizational innovativeness and government support: The mediating role of market culture. J. Clean. Prod. 2017, 154, 114–124. [Google Scholar] [CrossRef]

- Kanda, W.; Mejía-Dugand, S.; Hjelm, O. Governmental export promotion initiatives: Awareness, participation, and perceived effectiveness among Swedish environmental technology firms. J. Clean. Prod. 2015, 98, 222–228. [Google Scholar] [CrossRef]

- Bell, D.V. The Role of Government in Advancing Corporate Sustainability; Background Paper; Final Draft; Sustainable Enterprise Academy, York University: Toronto, ON, Canada, 2002. [Google Scholar]

- Hamann, R. Mining companies’ role in sustainable development: the ‘why’ and ‘how’ of corporate social responsibility from a business perspective. Dev. South. Afr. 2003, 20, 237–254. [Google Scholar] [CrossRef]

- Luck, D.J. Broadening the concept of marketing—Too far? J. Market. 1969, 33, 53–63. [Google Scholar] [CrossRef]

- Holm, M.; Kumar, V.; Plenborg, T. An investigation of customer accounting systems as a source of sustainable competitive advantage. Adv. Account. 2016, 32, 18–30. [Google Scholar] [CrossRef]

- Biju, P.L.; Shalij, P.R.; Prabhushankar, G.V. Evaluation of customer requirements and sustainability requirements through the application of fuzzy analytic hierarchy process. J. Clean. Prod. 2015, 108, 808–817. [Google Scholar] [CrossRef]

- Pamučar, D.; Lukovac, V.; Božanić, D.; Komazec, N. Multi-criteria FUCOM-MAIRCA model for the evaluation of level crossings: case study in the Republic of Serbia. Oper. Res. Eng. Sci. Theory Appl. 2018, 1, 108–129. [Google Scholar]

- Christmann, P. Effects of “best practices” of environmental management on cost advantage: The role of complementary assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar]

- Cohen, B.; Winn, M.I. Market imperfections, opportunity and sustainable entrepreneurship. J. Bus. Ventur. 2007, 22, 29–49. [Google Scholar] [CrossRef]

- Singh, A. Developing a conceptual framework of waste management in the organizational context. Manag. Environ. Qual. Int. J. 2017, 28, 786–806. [Google Scholar] [CrossRef]

- Singh, A. Flexible Waste Management Practices in Service Sector: A Case Study. In Global Value Chains, Flexibility and Sustainability; Springer: Singapore, 2018; pp. 301–318. [Google Scholar]

- Singh, A.; Raj, P. Sustainable Recycling Model for Municipal Solid Waste in Patna. Energy Environ. 2018. [Google Scholar] [CrossRef]

| S. No. | Model | The Conclusion of Sustainability Models | References |

|---|---|---|---|

| 1 | Theory of the Firm Model | This model explains the conjunction of two industries for maintaining social attribute of product and CSR activity of organizations. | [22] |

| 2 | Society versus Firm Model | Sustainability implies sustainable competitive advantage not sustainable development firms. | [23] |

| 3 | Shareholder value creation model | How the business organizations maintain the dynamic, sustainable development without compromising shareholder value. | [24] |

| 4 | Triple Value Triangle Model | Sustainable development through the axes of the triangle where each axis represents the social, environmental and economic values. | [25] |

| 5 | Sustainable value creating a model | Essential actions were taken by different level of stakeholders for maintaining sustainability in organization. | [26] |

| 6 | Sustainability Sweet Spot Model | This model represents sustainability as a sweet spot. | [27] |

| 7 | Organizational Sustainability Model | This model presents the definition of a stakeholder which satisfies the demands of each level of stakeholders in the organization. | [28] |

| 8 | Integrated Management of Quality and Sustainability Model | Corporate sustainability has been discussed in this model. It has been abstracted as economic, social and environmental bottom lines. | [29] |

| 9 | Star Model | Government and customer (as a driver) are also an essential part of sustainability, along with the environment, society and economy. | [21] |

| 10 | Sustainable enterprise model innovation | A conceptual framework which helps to learn development processes, densities faced during trade-off for sustainable enterprises. | [30] |

| 11 | NINR Logic Model for Center Sustainability | Center Sustainability includes strategies to control resources for providing the long-term sustainability while planning a center. | [31] |

| 12 | The SOSTARE model | Stepwise assimilated farm sustainability valuations about technical efficiency, and its impact on environmental and economic sustainability. | [32] |

| S. No. | Authors | Sustainability Intent of the Organization |

|---|---|---|

| 1 | Byerlee [33] | The organization promotes sustainable practices at the time of crisis. |

| 2 | Shrivastava [34] | Linking the effect of populations on ecosystems. |

| 3 | Ulhoi et al. [19] | Solutions for fulfilling simple needs with minimum environmental impact and the maximum economic and social return. |

| 4 | Philips and Reichart [35] | Stakeholder status in the non-human environment. |

| 5 | Kefalas [36] | Environmentally Sustainable Organization (ESO) as a system approach. |

| 6 | Hart and Milstein [24] | Sustainable-value framework for designing shareholder value of the organization. |

| 7 | Swart et al. [37] | Sustainability science and scenario analysis are the problems of the future. |

| 8 | Figge and Hahn [38] | This research article discusses corporate contributions to sustainability. |

| 9 | Du Pisani [39] | Demand for natural resources and their effect on the environment was an endless concern all through human history. |

| 10 | Darby and Jenkins [40] | Measure social accounting procedures and tools to quantify social enterprise (SE) contribution to retaining sustainability. |

| 11 | Sen and Swierczek [41] | Societal, environmental and stakeholder dimensions for active organizational functions through case analysis of US and Asian international firms. |

| 12 | Parrish [42] | What creates a sustainable enterprise through exploration of its principle and purpose. |

| 13 | Nguyen and Slater [43] | Discussed hitting the sustainability sweet spot in the sweet spot model. |

| 14 | Kocmanova et al. [44] | Business sustainability has been studied in term of environmental, social and corporate governance performance small and medium enterprises in the Czech Republic. |

| 15 | Kiron et al. [45] | Sustainability terminology, to cover environmental, economic and societal topics. Long-term perspective has been studied in term of sustainability factors. |

| 16 | Barth and Michelsen [46] | Education is contributing to sustainability. |

| 17 | Munoz et al. [47] | The ontological framework has been developed to eases the environmental performance of an organization. |

| 18 | Jain [48] | The Concept of Triple Bottom Line Reporting in India’s Perspective. |

| 19 | Rambaud and Richard [49] | Sustainability as “Triple Depreciation Line” instead of “Triple Bottom Line”. |

| Factor | Coding |

|---|---|

| Environmental Aspect | |

| Waste Management efficiency (SENF1) | Waste Management efficiency, waste management, waste management used for creating sustainability in the organization, eco-efficiency of the organization, eco-efficiency was used to co-relate the environment with economic growth, organization waste minimization, organizational waste, recycling, organizational waste reduction. |

| Pollution (SENF2) | Environmental Kuznets curve, environmental pollution, sustainable organizations are majorly concerned about pollution, environmental degradation. |

| Energy consumption (SENF3) | Energy consumption affects energy requirements, green energy, substitution of traditional energy sources, payback from green energy, solar energy, environmental load, greenhouse gas emission. |

| The social aspect of sustainability | |

| Social Function (SSCF4) | The functional aspect of the organization toward society, social approaches, the economic benefit to the society, employment creation, providing training and vocational education. |

| Social Equity (SSCF5) | Employment equity among the organization. Stakeholder participation rate, employees wage fairness, positioning and promotion of organization staffs. |

| Social acceptability (SSCF6) | Perception and participation of employees in the organization, societal perception, opinion of society, societies’ view about the organization, understanding the needs of people and stakeholders, organizational development. |

| Economic Aspect | |

| Economic Returns (SECF7) | Profit maximization. Organizational earning, organization profit, financial returns environmental and social welfare maximization, economic capital, natural resource capital, long-term returns by making more profit as well as fulfilling responsibilities towards nature. |

| Economic Investment (SECF8) | Organizations utilize their core capabilities for absorbing sustainable changes without affecting growth, dynamic capability of gaining, the competitive advantages, investment over sustainability, investment over green energy, investment over social acceptability, social function, and investment over innovation. |

| Stakeholders Aspect | |

| Customer Awareness (SSHF9) | Customers demand green products, customer preference, critical selection of products, customer awareness of choosing sustainable products and organization, mindful consumption pull the organization towards responsible, social and societal marketing which promotes sustainability. |

| Governmental Initiatives (SSHF10) | Government policies, direct regulations, direct and indirect governmental initiatives, government forms a political ecology for nurturing sustainability, governmental incentives, rules for avoiding exploitation of human rights and empowers the society. |

| S. No. | Factors | Test Value = 3.5 | ||||

|---|---|---|---|---|---|---|

| Mean | Std. Deviation | Sig.(2tailed) Mean Difference | t Value | Result | ||

| 1 | Waste Management Efficiency | 4.26 | 0.846 | 0.000 | 6.120 | Significant |

| 2 | Pollution | 3.94 | 0.791 | 0.000 | 3.779 | Significant |

| 3 | Energy Consumption | 3.94 | 0.870 | 0.001 | 3.437 | Significant |

| 4 | Social Equity | 4.11 | 0.729 | 0.000 | 5.700 | Significant |

| 5 | Social Function | 4.09 | 0.830 | 0.000 | 4.835 | Significant |

| 6 | Social Acceptability | 4.15 | 0.932 | 0.000 | 4.773 | Significant |

| 7 | Economic investment | 4.34 | 0.788 | 0.000 | 7.313 | Significant |

| 8 | Economic Returns | 4.11 | 0.429 | 0.00 | 9.68 | Significant |

| 9 | Customer Awareness | 3.96 | .806 | 0.000 | 3.889 | Significant |

| 10 | Governmental Initiatives | 4.26 | 0.736 | 0.000 | 7.033 | Significant |

| Reliability Statistics | |

|---|---|

| Cronbach’s Alpha | Number of Items |

| 0.786 | 10 |

| S. No. | Factors Link | Mean | Std. Deviation | Sig.(2tailed) Mean Difference | t-Value | Accept/Reject * |

|---|---|---|---|---|---|---|

| 1 | Link1 | 4.24 | 0.831 | 0.000 | 4.454 | Accept |

| 2 | Link2 | 4.32 | 0.802 | 0.000 | 5.112 | Accept |

| 3 | Link4 | 4.40 | 0.577 | 0.000 | 7.794 | Accept |

| 4 | Link3 | 4.40 | 0.707 | 0.000 | 6.364 | Accept |

| 5 | Link6 | 4.28 | 0.891 | 0.000 | 4.379 | Accept |

| 6 | Link5 | 4.20 | 0.764 | 0.000 | 4.583 | Accept |

| 7 | Link7 | 4.04 | 0.978 | 0.011 | 2.760 | Accept |

| 8 | Link8 | 4.04 | 0.978 | 0.011 | 2.760 | Accept |

| 9 | Link9 | 4.20 | 0.957 | 0.001 | 3.656 | Accept |

| 10 | Link10 | 4.08 | 0.862 | 0.003 | 3.364 | Accept |

| 11 | Link11 | 4.36 | 0.757 | 0.000 | 5.679 | Accept |

| 12 | Link12 | 4.20 | 0.913 | 0.001 | 3.834 | Accept |

| 13 | Link13 | 4.08 | 0.759 | 0.001 | 3.819 | Accept |

| 14 | Link 14 | 3.92 | 1.213 | 0.106 | 1.683 | Reject |

| 15 | Link15 | 4.20 | 0.866 | 0.000 | 4.041 | Accept |

| 16 | Link16 | 3.96 | 0.676 | 0.002 | 3.404 | Accept |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Singh, A.; Sushil; Kar, S.; Pamucar, D. Stakeholder Role for Developing a Conceptual Framework of Sustainability in Organization. Sustainability 2019, 11, 208. https://doi.org/10.3390/su11010208

Singh A, Sushil, Kar S, Pamucar D. Stakeholder Role for Developing a Conceptual Framework of Sustainability in Organization. Sustainability. 2019; 11(1):208. https://doi.org/10.3390/su11010208

Chicago/Turabian StyleSingh, Aarti, Sushil, Samarjit Kar, and Dragan Pamucar. 2019. "Stakeholder Role for Developing a Conceptual Framework of Sustainability in Organization" Sustainability 11, no. 1: 208. https://doi.org/10.3390/su11010208