Why Are Warrant Markets Sustained in Taiwan but Not in China?

Abstract

:1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Data

3.2. Methodology

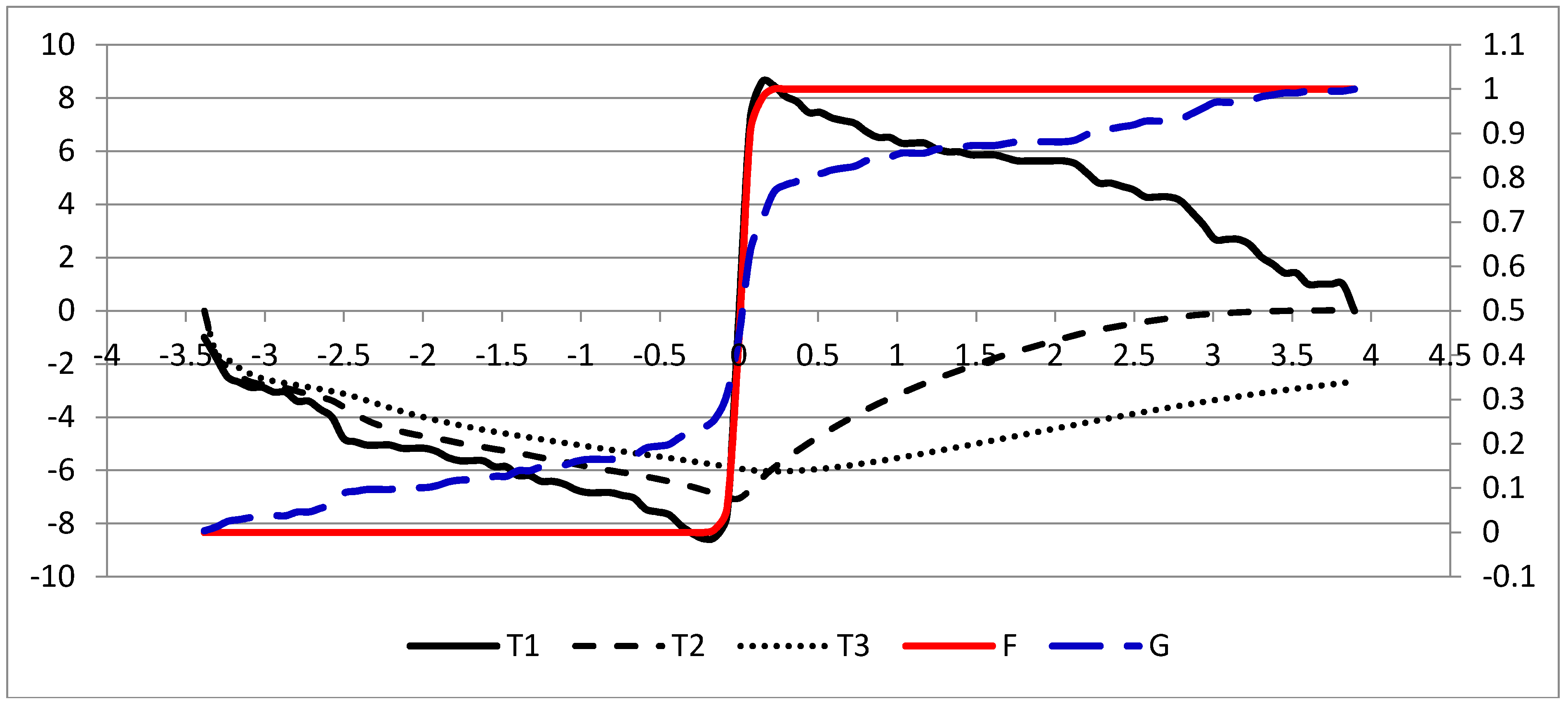

3.2.1. Mean-Variance (MV) Criteria

3.2.2. Stochastic Dominance (SD) Approach

4. Empirical Results

4.1. Moments Analysis

4.2. CAPM Analysis

4.3. SD Analysis

4.4. Volume Analysis

5. Concluding Remarks

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Xiong, W.; Yu, J. The Chinese warrants Bubble. Am. Econ. Rev. 2011, 101, 2723–2753. [Google Scholar] [CrossRef]

- Draper, P.; Mak, B.S.C.; Tang, G.Y.N. The Derivative Warrant Market in Hong Kong: Relationships with Underlying Assets. J. Deriv. 2001, 8, 72–83. [Google Scholar] [CrossRef]

- Aitken, M.; Segara, R. Impact of warrant introductions on the behaviour of underlying stocks: Australian evidence. Account. Financ. 2005, 45, 127–144. [Google Scholar] [CrossRef]

- Liao, X.-H.; Chen, K.C. Expiration Effects of Covered Warrants in China. Chin. Econ. 2010, 43, 54–75. [Google Scholar] [CrossRef]

- Chung, S.-L.; Liu, W.-R.; Tsai, W.-C. The impact of derivatives hedging on the stock market: Evidence from Taiwan’s covered warrants market. J. Bank. Financ. 2014, 42, 123–133. [Google Scholar] [CrossRef]

- Li, G.; Zhang, C. Why Are Derivative Warrants More Expensive Than Options? An Empirical Study. J. Financ. Quant. Anal. 2011, 46, 275–297. [Google Scholar] [CrossRef]

- Chan, H.W.-H.; Pinder, S.M. The value of liquidity: Evidence from the derivatives market. Pacific-Basin Financ. J. 2000, 8, 483–503. [Google Scholar] [CrossRef]

- Horst, J.T.; Veld, C. An Empirical Analysis of the Pricing of Bank Issued Options versus Options Exchange Options. Eur. Financ. Manag. 2008, 14, 288–314. [Google Scholar] [CrossRef] [Green Version]

- Bartram, S.M.; Fehle, F. Competition without fungibility: Evidence from alternative market structures for derivatives. J. Bank. Financ. 2007, 31, 659–677. [Google Scholar] [CrossRef]

- Petrella, G. Option bid-ask spread and scalping risk: Evidence from a covered warrants market. J. Futures Mark. 2006, 26, 843–867. [Google Scholar] [CrossRef]

- Liu, Y.-J.; Zhang, Z.; Zhao, L. Speculation Spillovers. Manag. Sci. 2014, 61, 649–664. [Google Scholar] [CrossRef]

- Tang, K.; Wang, C. Are China warrants derivatives? Evidence from connections to their underlying stocks. Quant. Financ. 2013, 13, 1225–1240. [Google Scholar] [CrossRef]

- Scheinkman, J.A.; Xiong, W. Overconfidence and Speculative Bubbles. J. Political Econ. 2003, 111, 1183–1219. [Google Scholar] [CrossRef]

- Liao, L.; Li, Z.; Zhang, W.; Zhu, N. Exercise to Lose Money? Irrational Exercise Behavior from the China warrants Market. J. Futures Mark. 2014, 34, 399–419. [Google Scholar] [CrossRef]

- Chang, E.C.; Luo, X.; Shi, L.; Zhang, J.E. Is warrant really a derivative? Evidence from the China warrant market. J. Financ. Mark. 2013, 16, 165–193. [Google Scholar] [CrossRef] [Green Version]

- Powers, E.; Xiao, G. Mispricing of China warrants. Pac.-Basin Financ. J. 2014, 30, 62–86. [Google Scholar] [CrossRef]

- Liao, L.; Li, Z.; Zhang, W.; Zhu, N. Security Supply and Bubbles: A Natural Experiment from the China Warrants Market; Working Paper; Hsinghua University: Beijing, China, 2010. [Google Scholar]

- Fung, H.-G.; Zhang, G.; Zhao, L. China’s Equity Warrants Market: An Overview and Analysis. Chin. Econ. 2009, 42, 86–97. [Google Scholar] [CrossRef]

- Chan, C.Y.; de Peretti, C.; Qiao, Z.; Wong, W.K. Empirical test of the efficiency of UK covered warrants market: Stochastic dominance and likelihood ratio test approach. J. Empir. Financ. 2012, 19, 162–174. [Google Scholar] [CrossRef]

- Abid, F.; Mroua, M.; Wong, W.K. The Impact of Option Strategies in Financial Portfolios Performance: Mean-Variance and Stochastic Dominance Approaches. Financ. India 2009, 23, 503–526. [Google Scholar] [CrossRef]

- Qiao, Z.; Clark, E.; Wong, W.K. Investors’ Preference towards Risk: Evidence from the Taiwan Stock and Stock Index Futures Markets. Account. Financ. 2012, 54, 251–274. [Google Scholar] [CrossRef]

- Qiao, Z.; Wong, W.K.; Fung, J.K.W. Stochastic Dominance Relationships between Stock and Stock Index Futures Markets: International Evidence. Econ. Model. 2013, 33, 552–559. [Google Scholar] [CrossRef]

- Lean, H.H.; McAleer, M.; Wong, W.K. Market Efficiency of Oil Spot and Futures: A Mean-Variance and Stochastic Dominance Approach. Energy Econ. 2010, 32, 979–986. [Google Scholar] [CrossRef]

- Lean, H.H.; McAleer, M.; Wong, W.K. Preferences of risk-averse and risk-seeking investors for oil spot and futures before, during and after the Global Financial Crisis. Int. Rev. Econ. Financ. 2015, 40, 204–216. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Wong, W.K.; Zhu, Z.Z. Is Wine a Good Choice for Investment? Pac.-Basin Financ. J. 2018, 51, 171–183. [Google Scholar] [CrossRef]

- Qiao, Z.; Wong, W.K. Which is a better investment choice in the Hong Kong residential property market: A big or small property? Appl. Econ. 2015, 47, 1670–1685. [Google Scholar] [CrossRef]

- Tsang, C.K.; Wong, W.K.; Horowitz, I. Arbitrage Opportunities, Efficiency, and the Role of Risk Preferences in the Hong Kong Property Market. Stud. Econ. Financ. 2016, 33, 735–754. [Google Scholar] [CrossRef]

- Hoang, T.H.V.; Lean, H.H.; Wong, W.K. Is gold good for portfolio diversification? A stochastic dominance analysis of the Paris stock exchange. Int. Rev. Financ. Anal. 2015, 42, 98–108. [Google Scholar] [CrossRef]

- Hoang, T.H.V.; Wong, W.K.; Xiao, B.; Zhu, Z.Z. The seasonality of gold prices in China: Does the risk-aversion level matter? Account. Financ. 2018, 58. [Google Scholar] [CrossRef]

- Hoang, T.H.V.; Wong, W.K.; Zhu, Z.Z. Is gold different for risk-averse and risk-seeking investors? An empirical analysis of the Shanghai Gold Exchange. Econ. Model. 2015, 50, 200–211. [Google Scholar] [CrossRef]

- Khamlichi, A.E.; Hoang, T.H.V.; Wong, W.K.; Zhu, Z.Z. Does the Shari’ah Screening Impact the Gold-Stock Nexus? A Sectorial Analysis. Resour. Policy 2018. Available online: https://www.researchgate.net/publication/328073570_Does_the_Shari%27ah_Screening_Impact_the_Gold-Stock_Nexus_A_Sectorial_Analysis (accessed on 11 October 2018).

- Vieito, J.P.; Wong, W.K.; Zhu, Z.Z. Could The Global Financial Crisis Improve the Performance of the G7 Stocks Markets? Appl. Econ. 2015, 48, 1066–1080. [Google Scholar] [CrossRef]

- Zhu, Z.Z.; Bai, Z.D.; Vieito, J.P.; Wong, W.K. The Impact of the Global Financial Crisis on the Efficiency of Latin American Stock Markets. Estudios de Economía 2018. Available online: https://www.researchgate.net/publication/326758644_The_Impact_of_the_Global_Financial_Crisis_on_the_Efficiency_and_Performance_of_Latin_American_Stock_Markets (accessed on 11 October 2018). [CrossRef]

- Broll, U.; Guo, X.; Welzel, P.; Wong, W.K. The banking firm and risk taking in a two-moment decision model. Econ. Model. 2015, 50, 275–280. [Google Scholar] [CrossRef]

- Broll, U.; Jack, E.; Wahl, J.E.; Wong, W.K. Elasticity of Risk Aversion and International Trade. Econ. Lett. 2006, 92, 126–130. [Google Scholar] [CrossRef]

- Egozcue, M.; Fuentes García, L.; Wong, W.K.; Zitikis, R. Do Investors Like to Diversify? A Study of Markowitz Preferences. Eur. J. Oper. Res. 2011, 215, 188–193. [Google Scholar] [CrossRef]

- Egozcue, M.; Wong, W.K. Gains from Diversification on Convex Combinations: A Majorization and Stochastic Dominance Approach. Eur. J. Oper. Res. 2010, 200, 893–900. [Google Scholar] [CrossRef]

- Abid, F.; Leung, P.L.; Mroua, M.; Wong, W.K. International Diversification versus Domestic diversification: Mean-Variance Portfolio Optimization and stochastic dominance approaches. J. Risk Financ. Manag. 2014, 7, 45–66. [Google Scholar] [CrossRef]

- Lozza, S.O.; Wong, W.K.; Fabozzi, F.J.; Egozcue, M. Diversification versus Optimal: Is There Really a Diversification Puzzle? Appl. Econ. 2018, 50, 4671–4693. [Google Scholar] [CrossRef]

- Fong, W.M.; Lean, H.H.; Wong, W.K. Stochastic Dominance and Behavior towards Risk: The Market for Internet Stocks. J. Econ. Behav. Organ. 2008, 68, 194–208. [Google Scholar] [CrossRef]

- Fong, W.M.; Wong, W.K.; Lean, H.H. International momentum strategies: A stochastic dominance. J. Financ. Mark. 2005, 8, 89–109. [Google Scholar] [CrossRef]

- Lean, H.H.; Smyth, R.; Wong, W.K. Revisiting Calendar Anomalies in Asian Stock Markets Using a Stochastic Dominance Approach. J. Multinatl. Financ. Manag. 2007, 17, 125–141. [Google Scholar] [CrossRef]

- Ma, C.; Wong, W.K. Stochastic dominance and risk measure: A decision-theoretic foundation for VaR and C-VaR. Eur. J. Oper. Res. 2010, 207, 927–935. [Google Scholar] [CrossRef]

- Alghalith, M.; Guo, X.; Wong, W.K.; Zhu, L.X. A General Optimal Investment Model in the Presence of Background Risk. Ann. Financ. Econ. 2016, 11, 1650001. [Google Scholar] [CrossRef]

- Guo, X.; Jiang, X.J.; Wong, W.K. Stochastic Dominance and Omega Ratio: Measures to Examine Market Efficiency. Arbitr. Oppor. Anomaly Econ. 2017, 5, 38. [Google Scholar]

- Niu, C.Z.; Wong, W.K.; Xu, Q.F. Kappa Ratios and (Higher-Order) Stochastic Dominance. Risk Manag. 2017, 19, 245–253. [Google Scholar] [CrossRef]

- Chiang, T.C.; Lean, H.H.; Wong, W.K. Do REITs Outperform Stocks and Fixed-Income Assets? New Evidence from Mean-Variance and Stochastic Dominance Approaches. J. Risk Financ. Manag. 2008, 1, 1–37. [Google Scholar] [CrossRef]

- Lean, H.H.; Phoon, K.F.; Wong, W.K. Stochastic Dominance Analysis of CTA Funds. Rev. Quant. Financ. Account. 2013, 40, 155–170. [Google Scholar] [CrossRef]

- Wong, W.K.; Phoon, K.F.; Lean, H.H. Stochastic dominance analysis of Asian hedge funds. Pacific-Basin Financ. J. 2008, 16, 204–223. [Google Scholar] [CrossRef]

- Markowitz, H.M. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar]

- Bai, Z.D.; Liu, H.X.; Wong, W.K. Enhancement of the applicability of Markowitz’s portfolio optimization by utilizing random matrix theory. Math. Financ. 2009, 19, 639–667. [Google Scholar] [CrossRef]

- Leung, P.L.; Ng, H.Y.; Wong, W.K. An Improved Estimation to Make Markowitz’s Portfolio Optimization Theory Users Friendly and Estimation Accurate with Application on the US Stock Market Investment. Eur. J. Oper. Res. 2012, 222, 85–95. [Google Scholar] [CrossRef]

- Wong, W.K. Stochastic Dominance and Mean-Variance Measures of Profit and Loss for Business Planning and Investment. Eur. J. Oper. Res. 2017, 182, 829–843. [Google Scholar] [CrossRef]

- Guo, X.; Wong, W.K. Multivariate Stochastic Dominance for Risk Averters and Risk Seekers. RAIRO Oper. Res. 2016, 50, 575–586. [Google Scholar] [CrossRef]

- Wong, W.K.; Ma, C. Preferences over Meyer’s location-scale family. Econ. Theory 2008, 37, 119–146. [Google Scholar] [CrossRef]

- Sriboonchitta, S.; Wong, W.K.; Dhompongsa, S.; Nguyen, H.T. Stochastic Dominance and Applications to Finance, Risk and Economics; Chapman and Hall/CRC, Taylor and Francis Group: Boca Raton, FL, USA, 2009. [Google Scholar]

- Levy, H. Stochastic Dominance: Investment Decision Making under Uncertainty; Springer: New York, NY, USA, 2015. [Google Scholar]

- Davidson, R.; Duclos, J.Y. Statistical inference for stochastic dominance and for the measurement of poverty and inequality. Econometrica 2000, 68, 1435–1464. [Google Scholar] [CrossRef]

- Bai, Z.D.; Li, H.; McAleer, M.; Wong, W.K. Stochastic dominance statistics for risk averters and risk seekers: An analysis of stock preferences for USA and China. Quant. Financ. 2015, 15, 889–900. [Google Scholar] [CrossRef]

- Bai, Z.D.; Li, H.; Liu, H.X.; Wong, W.K. Test Statistics for Prospect and Markowitz Stochastic Dominances with Applications. Econ. J. 2012, 14, 278–303. [Google Scholar]

- Ng, P.; Wong, W.K.; Xiao, Z.J. Stochastic dominance via quantile regression with applications to investigate arbitrage opportunity and market efficiency. Eur. J. Oper. Res. 2017, 261, 666–678. [Google Scholar] [CrossRef]

- Lean, H.H.; Wong, W.K.; Zhang, X.B. The size and power of some stochastic dominance tests: A Monte Carlo study for correlated heteroskedastic distributions. Math. Comput. Simul. 2008, 79, 30–48. [Google Scholar] [CrossRef]

- Chan, R.H.; Clark, E.; Wong, W.K. On the Third Order Stochastic Dominance for Risk-Averse and Risk-Seeking Investors with Analysis of their Traditional and Internet Stocks; MPRA Paper No. 75002; University Library of Munich: Munich, Germany, 2016. [Google Scholar]

- Leshno, M.; Levy, H. Preferred by “all” and preferred by “most” decision makers: Almost stochastic dominance. Manag. Sci. 2002, 48, 1074–1085. [Google Scholar] [CrossRef]

- Guo, X.; Post, T.; Wong, W.K.; Zhu, L.X. Moment Conditions for Almost Stochastic Dominance. Econ. Lett. 2014, 124, 163–167. [Google Scholar] [CrossRef]

- Guo, X.; Wong, W.K.; Zhu, L.X. Almost Stochastic Dominance for Risk Averters and Risk Seeker. Financ. Res. Lett. 2016, 19, 15–21. [Google Scholar] [CrossRef]

- Guo, X.; Zhu, X.H.; Wong, W.K.; Zhu, L.X. A Note on Almost Stochastic Dominance. Econom. Lett. 2013, 121, 252–256. [Google Scholar] [CrossRef] [Green Version]

- Gasbarro, D.; Wong, W.K.; Zumwalt, J.K. Stochastic Dominance Analysis of iShares. Eur. J. Financ. 2007, 13, 89–101. [Google Scholar] [CrossRef] [Green Version]

- Clark, E.; Qiao, Z.; Wong, W.K. Theories of Risk: Testing Investor Behaviour on the Taiwan Stock and Stock Index Futures Markets. Econ. Inquiry 2016, 54, 907–924. [Google Scholar] [CrossRef]

- Chan, R.H.; Chow, S.C.; Guo, X.; Wong, W.K. Central Moments, Stochastic Dominance, and The Moment Rules; Social Science Research Network Working Paper Series 3034903; SSRN: Rochester, NY, USA, 2017. [Google Scholar]

- Guo, X.; Wagener, A.; Wong, W.K.; Zhu, L.X. The Two-Moment Decision Model with Additive Risks. Risk Manag. 2017, 20, 77–94. [Google Scholar] [CrossRef]

- Chang, C.L.; McAleer, M.; Wong, W.K. Behavioural, Financial, and Health & Medical Economics: A Connection. J. Health Med. Econ. 2016, 2, 1–4. [Google Scholar]

- Chang, C.L.; McAleer, M.; Wong, W.K. Informatics, Data Mining, Econometrics and Financial Economics: A Connection. J. Inform. Data Min. 2016, 1, 1–5. [Google Scholar]

- Chang, C.L.; McAleer, M.; Wong, W.K. Management Science, Economics and Finance: A Connection. Int. J. Econ. Manag. Sci. 2016, 5, 1–19. [Google Scholar]

- Chang, C.L.; McAleer, M.; Wong, W.K. Management Information, Decision Sciences, and Financial Economics: A Connection. J. Manag. Inf. Decis. Sci. 2017, 20. Available online: https://ideas.repec.org/p/tin/wpaper/20180004.html (accessed on 11 October 2018). [CrossRef]

- Chang, C.L.; McAleer, M.; Wong, W.K. Big Data, Computational Science, Economics, Finance, Marketing, Management, and Psychology: Connections. J. Risk Financ. Manag. 2018, 11, 15. [Google Scholar] [CrossRef]

- Moslehpour, M.; Pham, V.K.; Wong, W.K.; Bilgiçli, İ. e-Purchase Intention of Taiwanese Consumers: Sustainable Mediation of Perceived Usefulness and Perceived Ease of Use. Sustainability 2018, 10, 234. [Google Scholar] [CrossRef]

- Li, Z.; Li, X.; Hui, Y.C.; Wong, W.K. Maslow Portfolio Selection for Individuals with Low Financial Sustainability. Sustainability 2018, 10, 1128. [Google Scholar] [CrossRef]

- Li, C.S.; Wong, W.K.; Peng, S.C.; Tsendsuren, S. The effects of health status on life insurance holding in 16 European countries. Sustainability 2018, 10, 3454. [Google Scholar]

- Wong, W.K.; Chan, R. Prospect and Markowitz Stochastic Dominance. Ann. Financ. 2008, 4, 105–129. [Google Scholar] [CrossRef]

{kind=link}

| Warrant Code | Mean | Std. Dev. | Skewness | Kurtosis | JB | Sharpe | Beta | Treynor | Jensen |

|---|---|---|---|---|---|---|---|---|---|

| C06 | −0.0201 | 0.0781 | −3.7196 | 33.9411 | 10084.75 | −0.2579 | 0.0150 | −1.3384 | −0.0186 |

| C12 | −0.0186 | 0.1440 | −13.0898 | 242.2479 | 1160912.00 | −0.1294 | −0.0009 | 20.5741 | −0.0183 |

| C14 | −0.0638 | 0.2956 | −8.3235 | 80.9023 | 30407.42 | −0.2157 | −0.0059 | 10.8959 | −0.0624 |

| C23 | 0.0011 | 0.0555 | 0.4351 | 5.1238 | 52.02 | 0.0204 | 0.0175 | 0.0647 | −0.0056 |

| C44 | −0.0057 | 0.0300 | 2.7879 | 24.6026 | 6885.69 | −0.1527 | 0.0115 | −0.4943 | −0.0058 |

| C47 | −0.0365 | 0.3155 | −13.5417 | 197.7772 | 377048.90 | −0.1158 | −0.0174 | 2.0965 | −0.0298 |

| C52 | −0.0270 | 0.2297 | −13.2963 | 195.6075 | 373322.80 | −0.1175 | 0.0397 | −0.6796 | −0.0405 |

| C55 | −0.0189 | 0.1171 | −2.2507 | 29.5247 | 7117.58 | −0.1615 | 0.0003 | −60.9548 | −0.0190 |

| T1 | −0.0511 | 0.2409 | −0.4242 | 12.6574 | 454.26 | −0.2121 | 0.0814 | −0.6280 | −0.0565 |

| T12 | −0.0341 | 0.4486 | −0.0494 | 20.9576 | 1679.60 | −0.0760 | 0.0289 | −1.1812 | −0.0307 |

| T13 | −0.0573 | 0.2730 | 1.3731 | 15.5192 | 800.82 | −0.2100 | 0.0232 | −2.4702 | −0.0560 |

| T15 | −0.0374 | 0.1388 | −2.2828 | 22.0487 | 2925.68 | −0.2693 | 0.0225 | −1.6632 | −0.0343 |

| T17 | 0.0053 | 0.0588 | 1.9440 | 11.7270 | 475.41 | 0.0892 | 0.0056 | 0.9310 | 0.0037 |

| T25 | −0.0434 | 0.1742 | 0.2863 | 11.0227 | 336.94 | −0.2491 | 0.0103 | −4.2091 | −0.0441 |

| T26 | −0.0032 | 0.2247 | 0.9245 | 5.1186 | 41.19 | −0.0144 | 0.1324 | −0.0245 | −0.0109 |

| T33 | 0.0128 | 0.1545 | −1.0409 | 10.6930 | 320.22 | 0.0829 | 0.0523 | 0.2451 | 0.0094 |

| Pairwise Comparison | t Test | F Test | MV Dominance |

|---|---|---|---|

| C14-T13 | µC < µT −0.1474 | σC > σT 1.1529 | No |

| C23-T33 | µC < µT −1.041 | σC < σT 7.7611 *** | C23 T33 |

| C44-T17 | µC < µT −2.6106 *** | σC < σT 3.8564 *** | No |

| C47-T12 | µC < µT −0.0597 | σC < σT 2.0222 *** | C47 T12 |

| C06-T15 | µC > µT 1.6191 | σC < σT 3.1598 *** | C06 T15 |

| C23-T17 | µC < µT −0.6578 | σC < σT 1.1249 | No |

| C47-T17 | µC < µT −1.4663 | σC > σT 28.7523 *** | C47 T17 |

| C52-T26 | µC < µT −0.9425 | σC > σT 1.0449 | No |

| C55-T25 | µC < µT 1.5869 | σC < σT 2.2131 *** | C55 T25 |

| C12-T17 | µC < µT −1.8125 * | σC > σT 5.9872 *** | T17 C12 |

| C23-T01 | µC > µT 3.1743 *** | σC < σT 18.8615 *** | C23 T01 |

| C14-T33 | µC < µT −2.4578 ** | σC > σT 3.5309 *** | T33 C14 |

| Pairwise Comparison | Ascending SD |

|---|---|

| C14-T13 | No SD |

| C23-T33 | |

| C44-T17 | |

| C47-T12 | |

| C06-T15 | |

| C23-T17 | |

| C47-T17 | No SD |

| C52-T26 | |

| C55-T25 | |

| C12-T17 | |

| C23-T01 | |

| C14-T33 | No SD |

| Warrant Code | Mean | Std. Dev. | Skewness | Kurtosis | JB |

|---|---|---|---|---|---|

| C06 | 96,150.9500 | 73,283.1200 | 2.1843 | 10.0706 | 690.7704 |

| C12 | 173,603.0000 | 324,388.6000 | 3.4949 | 17.0166 | 4926.9010 |

| C14 | 46,306.6400 | 44,987.5000 | 1.8837 | 7.1179 | 150.5576 |

| C23 | 55,458.4900 | 46,573.7300 | 1.9508 | 8.4068 | 440.8489 |

| C44 | 214,101.4000 | 178,940.0000 | 1.9563 | 7.5217 | 718.0678 |

| C47 | 40,012.9900 | 40,078.6000 | 2.3406 | 10.4683 | 760.7066 |

| C52 | 59,475.6700 | 51,874.5500 | 2.4878 | 10.7968 | 848.3305 |

| C55 | 48,996.5800 | 60,061.5300 | 3.2302 | 16.5166 | 2216.2940 |

| T1 | 15.3537 | 103.6143 | 10.5616 | 113.3553 | 61,544.3700 |

| T12 | 18.4588 | 72.0669 | 9.8558 | 105.4079 | 57,098.5700 |

| T13 | 25.7770 | 127.7570 | 10.4158 | 111.5797 | 60,098.8800 |

| T15 | 11.4235 | 75.4091 | 13.2409 | 178.1744 | 240,636.5000 |

| T17 | 0.1405 | 0.4666 | 4.8718 | 29.5315 | 4194.0060 |

| T25 | 37.7894 | 74.4648 | 2.3908 | 8.2631 | 265.4654 |

| T26 | 79.8744 | 149.2158 | 7.2949 | 69.3507 | 24,230.2100 |

| T33 | 107.3186 | 117.9072 | 2.8163 | 14.5546 | 839.9515 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wong, W.-K.; Lean, H.H.; McAleer, M.; Tsai, F.-T. Why Are Warrant Markets Sustained in Taiwan but Not in China? Sustainability 2018, 10, 3748. https://doi.org/10.3390/su10103748

Wong W-K, Lean HH, McAleer M, Tsai F-T. Why Are Warrant Markets Sustained in Taiwan but Not in China? Sustainability. 2018; 10(10):3748. https://doi.org/10.3390/su10103748

Chicago/Turabian StyleWong, Wing-Keung, Hooi Hooi Lean, Michael McAleer, and Feng-Tse Tsai. 2018. "Why Are Warrant Markets Sustained in Taiwan but Not in China?" Sustainability 10, no. 10: 3748. https://doi.org/10.3390/su10103748