3.1. Reasons for the Semiconductor Crisis

Various factors have led to the current supply bottlenecks, with both acute incidents and longer-term conditions having an impact on production volumes and the availability of electronic components for the automotive industry. The incidents that had an acute impact at the beginning of the crisis include:

In October 2020, a fire at a semiconductor plant of the Japanese chip manufacturer AKM, a subsidiary of Asahi Kasei K.K., led to the complete closure of production lines at the plant in Nobeoka City for about 12 months [

12]. The electronic components produced there are used, among others, in audio and navigation systems for the automotive industry.

In February 2021, an arctic winter storm led to the collapse of the power supply and the closure of semiconductor factories in the US state of Texas. Among others, plants of NXP Semiconductors N.V., one of the largest suppliers to the automotive industry, Samsung Group and Infineon Technologies AG were affected [

13,

14,

15]. Production was restricted for approximately 1 to 1.5 months.

In March 2021, a fire at a semiconductor plant of the Japanese chip manufacturer Renesas Electronics K.K. in Naka led to a halt in the production of wafer components in particular [

16].

The longer-term factors are rooted in the structure of the semiconductor market and the semiconductor industry itself, as well as in complex, elaborate production processes for manufacturing the chips. These more structural conditions mean that the problem is difficult for the automotive industry to solve in the near future. They will be described in detail in the following.

3.1.1. Structure of the Semiconductor Market and Automotive Share

The current structure of the semiconductor market works against the possibilities of a short-term increase in production capacities for customers in the automotive industry, as it represents only a small share of sales compared with other segments (such as communications). In 2020, for example, they accounted for only around 11% of global sales, while the communications and data technology segments accounted for almost 65% of total sales, amounting to EUR 352 billion [

3].

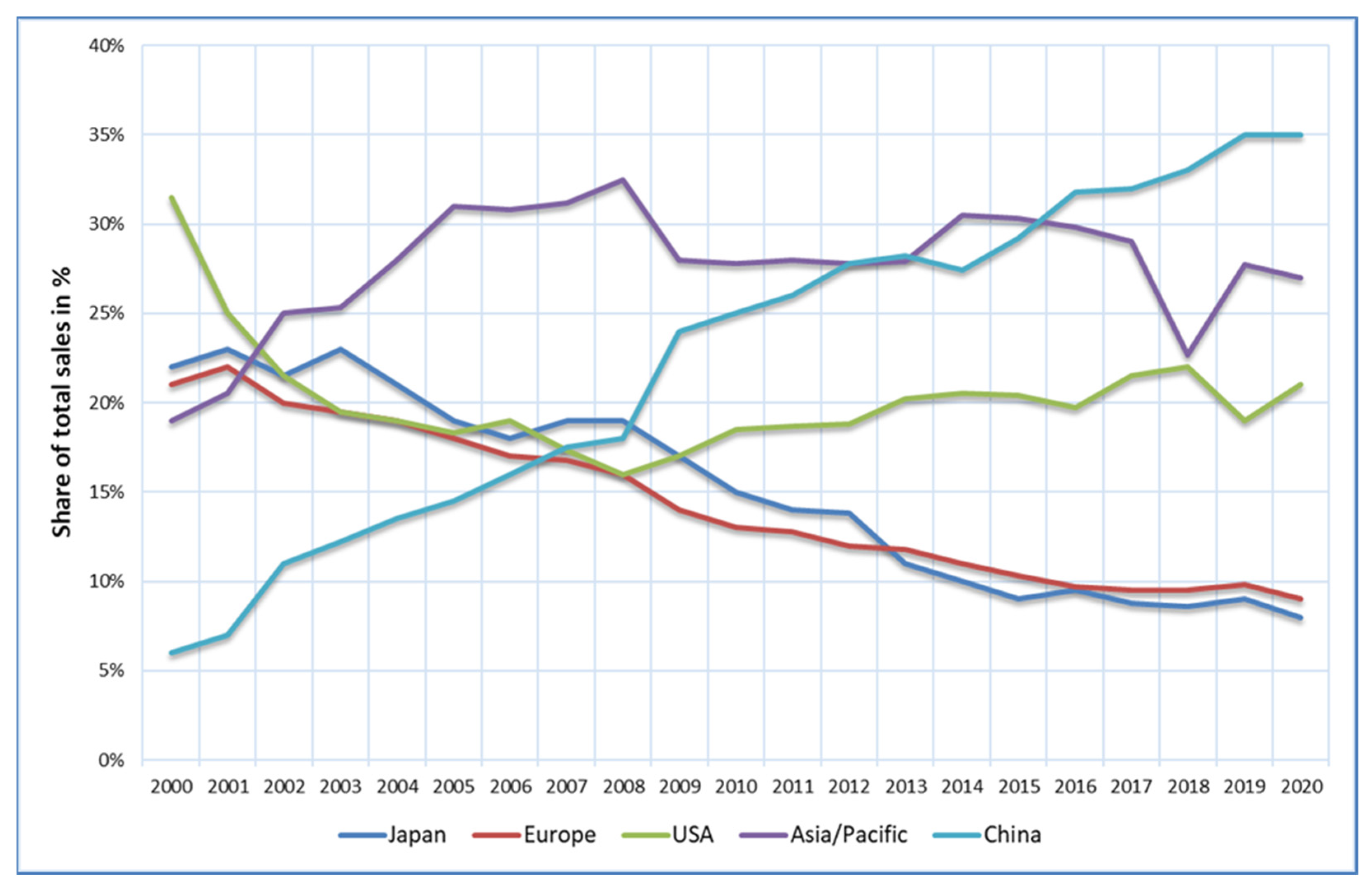

China is now the world’s largest sales market for semiconductor applications, with a market share of 35% in 2020. The development of market shares for the world regions of China, the Americas, Europe and Asia/Pacific from the year 2000 is shown in the following

Figure 1:

Europe and Japan have an overall market share for semiconductors of less than 10% worldwide, and furthermore, the demand is mainly automotive-driven: the automotive industry accounted for 37% of semiconductor sales in Europe and 28% in Japan in 2019. By comparison, other segments dominate demand in the USA (with 10% automotive share) and China (7%). In the USA, for example, the “Computers” segment is in the lead with a share of 38%, in China the “Communications” segment is in the lead with 42% [

4].

The shares of the individual segments in the total sales of the semiconductor market in comparison of the regions “World” and “Europe” are shown again graphically in the following

Figure 2—the strong automotive focus for Europe (shown in purple) is clearly visible:

As an example, for eight of the largest semiconductor manufacturers, the respective relevance of the automotive business in terms of sales is shown below, whereby only NXP (44%), Infineon (42%) and Renesas (48%) have significant sales shares in the automotive sector. The other manufacturers, Texas Instruments (20%), Qualcomm (4%), AMD/ATI (1%) and NVIDIA (6%) primarily serve customers in the communications and consumer segments, which therefore buy much higher volumes overall and also provide chip manufacturers with greater profit margins. Even the world’s largest chip manufacturer, TSMC (Taiwan), has an automotive share of sales of only 3% (annual reports of NXP, Infineon, Renesas, Texas Instruments, Qualcomm, AMD, NVIDIA, TSMC, 2020). The market and negotiating position of the automotive industry for semiconductor products is correspondingly lower compared to other industries.

In the area of semiconductor components for automated and autonomous driving, the German manufacturers Audi, BMW, Mercedes and VW rely mainly on cooperation with the U.S. companies Qualcomm and Texas Instruments, and also in part on NVIDIA. In the case of electronic components for processing signal and information data, the German OEMs are supplied by Texas Instruments, BMW and Volkswagen, also by NXP (Netherlands), and Audi, also by Renesas (Japan). For the supply of power semiconductors for vehicle control, all German OEMs rely primarily on cooperation with Infineon (Germany) (Annual reports Audi, BMW, Infineon, Mercedes, NXP, Qualcomm, Renesas, Texas Instruments, VW, 2019).

3.1.2. Structure of the Semiconductor Industry and Production Capacities

The structure of the semiconductor industry itself, as well as the complex production process, also counteract any short-term easing of the supply situation in the automotive industry. Companies in the semiconductor industry can generally be divided into contract manufacturers with production capacities (so-called foundries) and companies without their own manufacturing and production facilities (so-called fabless) [

5].

The latter focus their activities, in particular, on the areas of development of superior functions and designs (e.g., circuits), but not on the development and construction of investment-intensive production facilities. The so-called fabless companies include NVIDIA (USA), AMD/ATI (USA) and Qualcomm (USA), all of which—as described above—do not have a sales focus on the automotive business. Nevertheless, they also develop products that are a prerequisite for the realization of automated and autonomous driving functions. The main customer of these companies is TSMC in Taiwan, the world’s leading company in terms of production capacity only in the 200 mm wafer sector [

5]. However, TSMC also has a very small automotive share of sales in comparison.

The so-called foundries have their own production capacities for the manufacture of semiconductor products, which are characterized by high investment sums in the construction of highly automated production lines and can only operate economically competitively with large production volumes and quantities—often in three-shift operation and 24/7. The cost of setting up suitable production facilities amounts to several billion dollars [

17]. The foundries include manufacturers such as TSMC (Taiwan), Texas Instruments (USA), Infineon (Germany), NXP (Netherlands) and Renesas (Japan). These producers focus mainly on the manufacture of chips for processing signal and information data (e.g., network controllers and navigation) or for vehicle control. Most of the other producing companies are located in Asia, e.g., Samsung (Korea), UMC (Taiwan), SMIC (China), TowerJazz Panasonic Semiconductor (Japan), VIS (Taiwan), PSMC (Taiwan), Hua Hong (China) and DB HiTek (Korea).

Production facilities at Chinese locations are also leading in the production of so-called wafers (the basic material of electronic components, primarily made of silicon) required for semiconductor components in a comparison of monthly production capacities of 200 mm variants: with approx. 5.6 million units and a share of 20%, ahead of Taiwan with approx. 5.3 million units (19%), South Korea and Japan with approx. 4.8 million units each (17%), the USA with 3.1 million units (11%) and Europe with 2.2 million units (8%). Fabs in these six world regions represent a total of 92% of global wafer production (approx. 28 million units per month). Experts expect this share to shift even further towards Chinese production facilities by 2024, with simultaneous growth in global output volume per year of approx. 5% to then approx. 36 million units per month [

3].

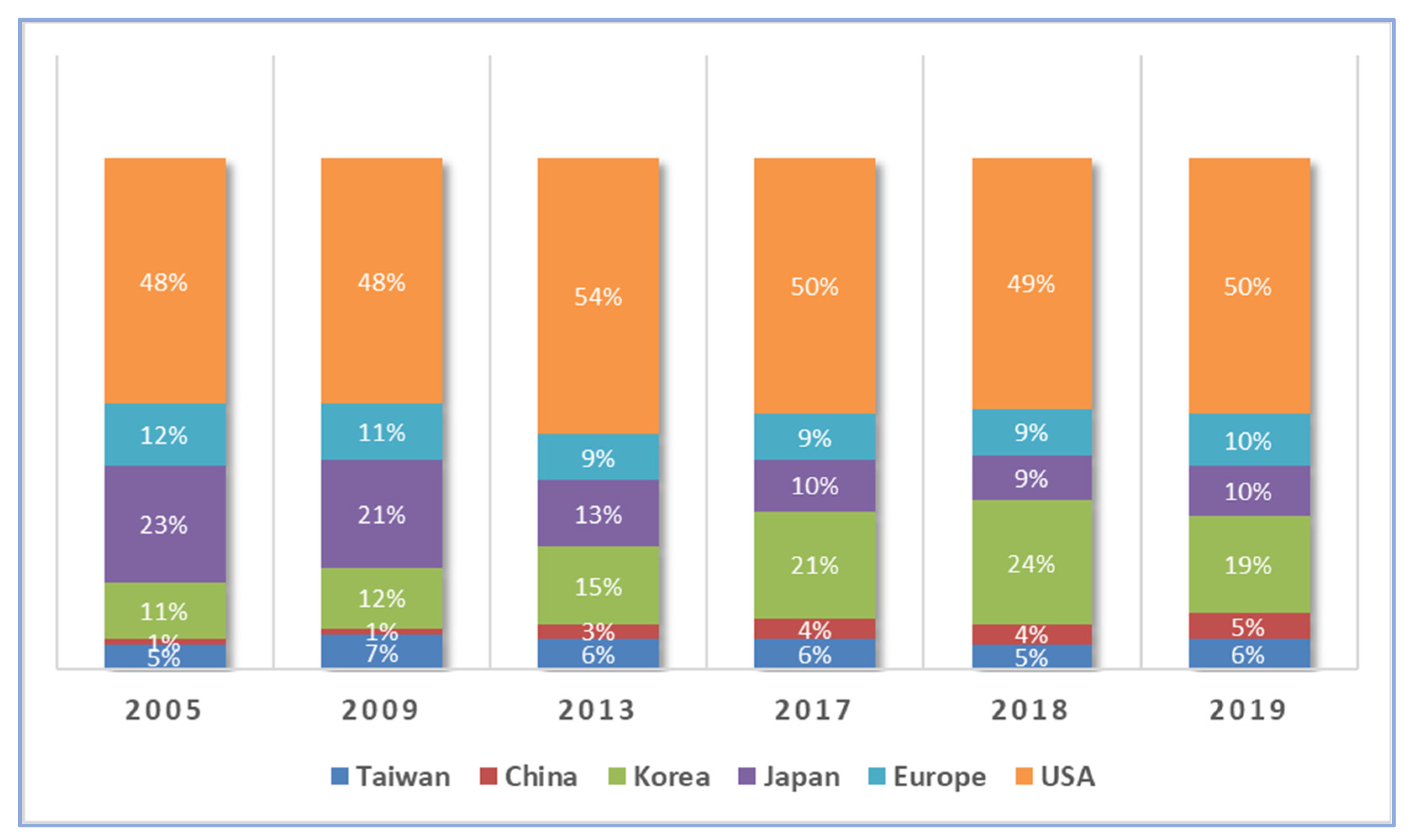

In an analysis by headquarters of the leading semiconductor companies, however, U.S. manufacturers dominated the global market in 2019, with a 51% share of sales, followed by South Korea (19%), Europe and Japan (10% each), Taiwan (6%) and China (5%), as shown in

Figure 3. Over a period of around 10 years, US companies have consistently accounted for a high share of sales (between 48% and 54%), similarly Europe and Taiwan with, however, much lower shares of sales (between 12% and 9% and 4% and 7%, respectively). Japan has seen a sharp decline over the same period since 2001, from 28% to just 10% in 2019, while at the same time South Korean companies increased their sales share from 6% to 24% in 2018. In 2019, however, this fell back to 19%. Chinese companies also increased their share of sales from 0% in 2001 to 5% in 2019 [

3].

3.1.3. Complex Production Processes and Supply Chains

The manufacture of semiconductor components is subject to a complex and elaborate production process, which also counteracts any rapid easing of the supply situation in the automotive industry. A total of around 5 to 8 months elapse between the order and the delivery of the component. The production of the wafer takes the most time, at around 3 months.

The raw material silicon required for this is separated from the quartz rock at high temperatures via a chemical reaction (so-called raw silicon) and freed from foreign substances (such as iron, aluminum, phosphorus). Subsequently, the arrangement of the atomic lattice structure is homogenized, and a so-called single crystal is produced from the silicon substrate or “pulled” from the silicon melt (so-called ingot).

These single-crystalline rods are processed into wafers in various steps, which are then coated and polished to form extremely flat surfaces, into which the circuit structures are burned on different levels in the nanometer range, for example using high-energy lasers (lithography). Finally, the individual chips are separated from the wafer, e.g., by sawing.

Wafers are produced in different sizes from 100 mm to 300 mm, whereby an increase in the diameter allows a higher production throughput and thus, lower production costs. By increasing the diameter from 200 mm to 300 mm, for example, the number of chips per wafer can be doubled. If the diameter is increased further (to 450 mm, for example), problems arise due to more complex processing steps and possible deformation.

The following

Figure 4 schematically illustrates the production process and supply chain from ordering to delivery:

3.1.4. Increasing Importance of Microelectronics in the Automotive Industry

The demand and market for semiconductor elements will continue to grow in the automotive sector in the future. This is due to the higher requirements for digital and networked functions in the vehicle compared to today’s conventionally powered vehicles, increasing levels of automation, the use of driver assistance systems and the electrification of the powertrain [

6].

The value shares for semiconductor components thus increase from approx. EUR 330 to EUR 690 material value for plug-in hybrids or purely battery-electric vehicles against the background of electrified drive components alone. Automated and/or autonomous driving functions will require additional semiconductor elements with a pure material value of up to approx. EUR 1,030 [

19]. According to Roland Berger, the cost of the semiconductor end products in a premium vehicle with a combustion engine is already around EUR 2,500 today and will rise to EUR 5,900 by 2025 in a passenger car with semi-autonomous driving functions [

6]. The growing market for electrified and automated vehicles will further increase sales opportunities for semiconductors in the future. Semiconductor manufacturers are also responding to this by investing in the expansion of additional production capacities. As a rule, the construction phase for a semiconductor fab is expected to take around 3 years and cost up to EUR 20 billion (for state-of-the-art production in the 5 nm range).

3.3. Strategies and Options to Cope with Shortages

In this section, company strategies to deal with the disruptions in supply chains will be analyzed and described in detail. With its high dependence on exports, and the structures of a diversified, internationalized division of labor in global value networks that have been created over decades, the German automotive industry appears to be particularly vulnerable to external disruptions in the supply chain. In the course of the study, this thesis was discussed in expert discussions and in-depth interviews. The aim was to identify the effects of the supply chain disruption on the affected companies in the automotive industry and to identify measures for overcoming them. The latter include both operational, rather short-term measures, arising directly from the COVID-19 crisis, as well as strategic options and consequences with a rather longer-term perspective. The latter are aimed at generally increasing resilience in relation to external disruptions to production and supply chains.

3.3.1. Operational Measures (Short-Term)

Short-term and operational measures to deal with the disruptions caused by the COVID-19 pandemic and the shortage in semiconductor components could be clustered into the following five topics: “Use of short-time work and closure of production plants”, “Adjustment of production processes”, “Adjustment of inventories”, “Establishment of central emergency teams and task forces” and “Search for alternative suppliers”. The mentions relating to “Short-time work” and “Adjustment of production processes” were the most frequent. In the case of multiple mentions, the area “Establishment of central emergency teams and task forces”, in particular, was highlighted as a very relevant measure, both in relation to the company itself and in relation to the higher-level customer. The “Search for alternative suppliers” was mentioned only once.

Use of short-time work and closure of production plants: 66% of the interviewees were affected by the lockdown and the associated halt of production activities. They mainly used labor market policy instruments as a result of the lockdown, with part-time work in particular.

Adaptation of production processes: 53% adapted their production processes as a result of the pandemic, in particular to be able to implement safety measures to protect against infection. Where the minimum distance of 1.5 m could not be maintained (e.g., on production lines), plexiglass walls were built up, masks were made compulsory and disinfection facilities were installed. Overall, the implementation of these measures resulted in an increase in infection protection, but at the same time led to productivity losses for the companies. Unexpectedly, hygiene articles such as masks have turned out to be “critical goods” and have presented companies with procurement problems

Adjustment of inventories: 60% mentioned adjusting inventories as a tactical measure to deal with the pandemic and customers’ often unclear demands and call-offs. In this context, inventory levels were both increased and decreased. On the one hand, in the early phase and before the (partial) lockdown, production was continued to a large extent despite unclear customer demand, or deliveries were accepted and inventories increased in order to be able to continue to deliver with high volumes and at short notice in the event of an improvement in the coronavirus situation. Secondly, in the later course of the crisis, existing inventories were reduced again in order to be able to manufacture and deliver the company’s own products. This meant that the company was less dependent on upstream products that were no longer supplied or only supplied in small quantities. Adjustments to inventories were mainly made for products identified as “critical”, such as electronic parts or cable harnesses.

Establishment of centralized emergency response teams and task forces: The establishment of task forces was named by 64% of the interviewees as a short-term operational measure for dealing with the crisis. In this context, the interviewees were referring, in particular, to difficulties in general communication with customers in terms of the reliability and predictability of requirements and orders. They emphasized that customers, in particular, were able to quickly set up task forces and establish them at the interfaces of the supply chain, which have their own central logistics in a strong position and a distinct, established supplier management. Reference was also made here to those companies that were affected by Fukushima in 2011, where they were able to gain experience in setting up emergency task forces.

In addition to the organizational establishment of centralized emergency response teams and task forces, digital technologies for the exchange of information and, in particular, the tracking of the flow of goods along the value chain were also mentioned by 23% of the interviewees. This includes blockchain technology, which is intended to ensure a secure flow of information and is being tested by the automotive industry in initial pilot projects. Here, however, it is questionable whether cross-company data exchange along the entire supply chain is actually feasible. On the one hand, the emerging data volume is currently unmanageable, and on the other hand, the companies must agree to the data transfer. It is hard to imagine the semiconductor industry granting what it considers an insignificant market share appropriate access here.

Search for alternative suppliers: Only one interviewee mentioned the search for alternative suppliers as an operational measure to deal with the crisis. The majority of the companies were able to maintain their own production capacities on the basis of existing supplier relationships and/or by reducing inventories until production was able to restart again.

3.3.2. Strategic Options (Long-Term)

In the first weeks of the lockdown, broken supply chains were discussed as the cause of the production halt in the automotive industry. To avoid and/or better manage this problem in the future, a greater return to local production was called for as a way to contain the pandemic and stabilize the economy, according to broader public discussion. However, in the expert interviews, the opposite position was stated for the automotive industry: there will be no fundamental change in international division of labor or associated global supply chains. Instead, a modification of purchasing strategies is more likely. Overall, four fields of action could be identified in the question of long-term strategic fields of action for stabilizing supply chains in crisis situations: “Increase stockholding for critical components”, “Strengthen dual sourcing and flexible shares”, “Support local supply chains” and “Monitoring of the reliability of political action”. The responses were equally distributed across all interviews. In the case of multiple mentions, the area “Reliability of political action” was identified as most relevant option.

Increase inventory levels for critical components: 40% of the interviewees named an increase in inventories for critical components as a reasonable strategic option. Vulnerability to disruptions was already evident in 2011 during the Fukushima crisis but affected not as many products there. The COVID-19 pandemic with its global impact endangered production in the entire supply industry. Therefore, in addition to the identification of critical components and suppliers, higher stock levels for single parts were set up. Since warehousing requires corresponding areas, systems and staff, activities always have to be weighed against disadvantages in cost and efficiency in the automotive industry. For this reason, larger warehousing—if at all—would only be practicable for individual components that are considered to be particularly critical.

Strengthen dual sourcing and flexible shares: Another 40% stated that strengthening dual sourcing and flexible shares with suppliers is being discussed as a strategic option for the future. Dependence on one supplier, especially a foreign supplier, has already revealed weaknesses in supply chains during Fukushima and even more so in the pandemic. In the interests of resilient supply chains, consideration is therefore being given to purchasing from two suppliers instead of one for selected components and to a limited extent. As a result of the global disruption, splitting with a low-cost supplier, e.g., in Asia, and a European or German supplier is being considered here. However, this will only lead to a small return of production, if at all. This is because, when split between the suppliers, the significantly larger volume would still be sourced from the lower-cost foreign countries; the experts cited proportions of 70 to 80% here.

Supporting local supply chains: 33% mentioned a stronger focus on local supply chains as a possible strategic option, and as critical for the resilience of future value networks. In many cases, it is not only supplier relationships in Germany that are rated as “geographically local”, but also European ones on a larger scale. As a result of the pandemic, the need to adapt purchasing strategies in the interests of greater stability is seen. Here, the company experts see an advantage in greater geographical proximity, and thus, a focus of the supply chains in the European countries or in the future also in the (North) African countries. At the same time, the experts have pointed out that sourcing components and parts from European locations is associated with higher costs compared with sourcing from Asian production. Therefore, the advantages of regionalized supply chains must be weighed against higher costs. This raises the question of how far the current impressions from the pandemic will extend into the future, or whether purchasing decisions will soon again be made primarily on the basis of cost efficiency.

Monitoring the reliability of political action: When asked about possible political action, the experts focused mainly on reliability, and thus, on maintaining social and economic stability. This topic was mentioned most frequently among the long-term measures (47%). Three levels of action should be distinguished here: the municipal level or that of the federal state, the national level and the pan-European level. With its decisions on how to deal with the pandemic, the political arena provides the essential framework conditions under which economic activity, such as the company’s production, the purchase of inputs and the sale of its own products, is possible in the first place. Only the most effective possible limitation of the pandemic protects against restrictions on the company’s own production. The interviewees certainly acknowledged the great difficulties that politicians faced with the first lockdown decision in German history. Nevertheless, it is helpful for companies at the local level to have reliable and comparable regulations across different counties and cities. This was not always the case in the first lockdown in March/April 2020. For companies in the automotive industry, which are heavily dependent on foreign trade, this demand for politically regulated stable framework conditions also applies to other states with which they maintain economic relations. After all, limiting the pandemic can protect against a lockdown there as well. However, this change in supply chains is associated with disadvantages in terms of cost efficiency and, depending on the corporate strategy, is not feasible for everyone. In return, companies expect stability within the European economic area and agreements on border crossings for business purposes. Here, however, the expectations of companies in the automotive industry and the machine tool industry differ: while the automotive industry was primarily concerned with the supply of components and parts from foreign production sites, for the machine tool industry, the greatest difficulty was primarily in the supply of machines and in the commissioning and repair of machines abroad.

{kind=link}

{kind=link}

{kind=link}

{kind=link}