Factors Affecting Trust and Acceptance for Blockchain Adoption in Digital Payment Systems: A Systematic Review

Abstract

:1. Introduction

- RQ1

- What are the factors that influence users’ trust in the adoption of blockchain in digital payment systems?

- RQ2

- What are the factors that influence users’ acceptance of the adoption of blockchain in digital payment systems?

- RQ3

- How can the trust model be integrated into the acceptance model for blockchain adoption in digital payment systems?

2. Background

2.1. Overview of Blockchain

2.2. Role of Trust

2.3. Technology Acceptance

3. Related Works

4. Methodology

- Identify the need for the review, prepare a proposal, and develop the review protocol according to PRISMA.

- Identify the research, select the studies, assess the quality, take notes, extract data, and synthesise the data.

- Report the results of the review.

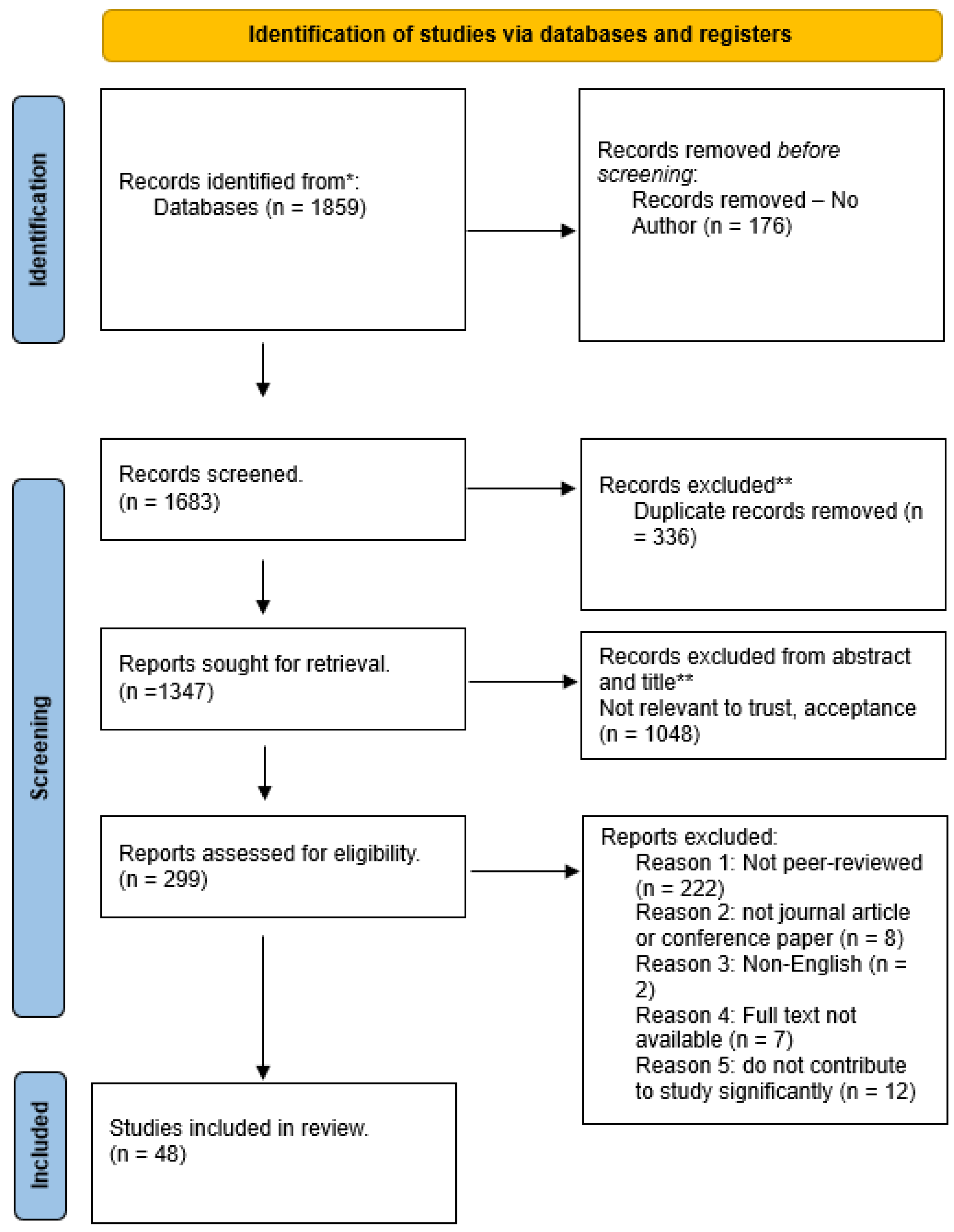

4.1. Conducting the Search

4.2. Study Selection and Evaluation

4.3. Analysis Process

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Selection Criteria | Scientific Database | |

|---|---|---|

| Inclusion | All articles which are peer-reviewed | |

| No time limitation | ||

| Exclusion | Prior to importation to bibliographic tool | Articles without author |

| During title screening | Duplicate articles related to the blockchain technology adoption | |

| During abstract screening | Articles related to the blockchain technology adoption, trust, and acceptance | |

| During full-text screening | Articles addressing trust and acceptance for the adoption of blockchain technology for payment | |

| Peer-reviewed | ||

| Other than journal articles | ||

| Non-English articles |

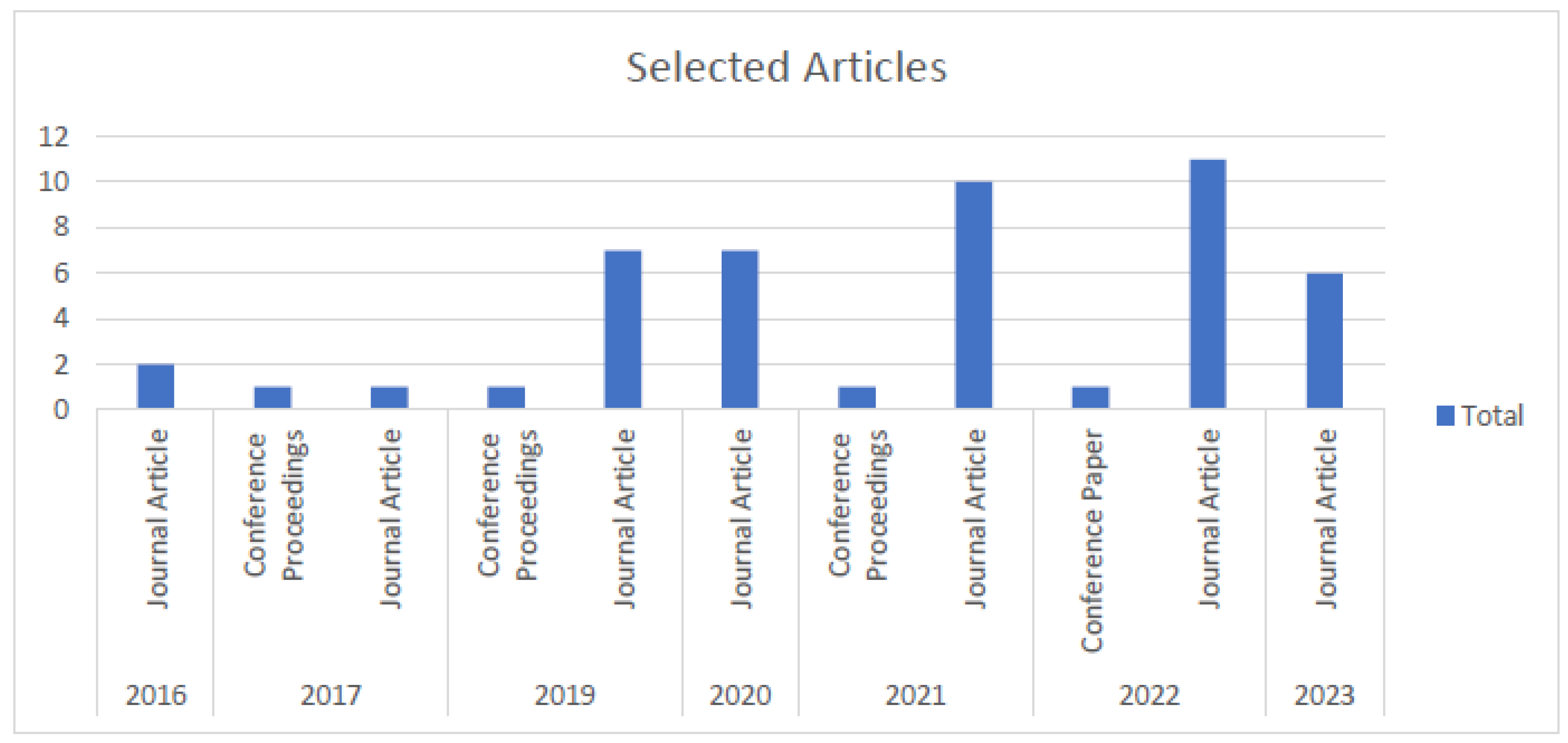

5. Descriptive Analysis

6. Results

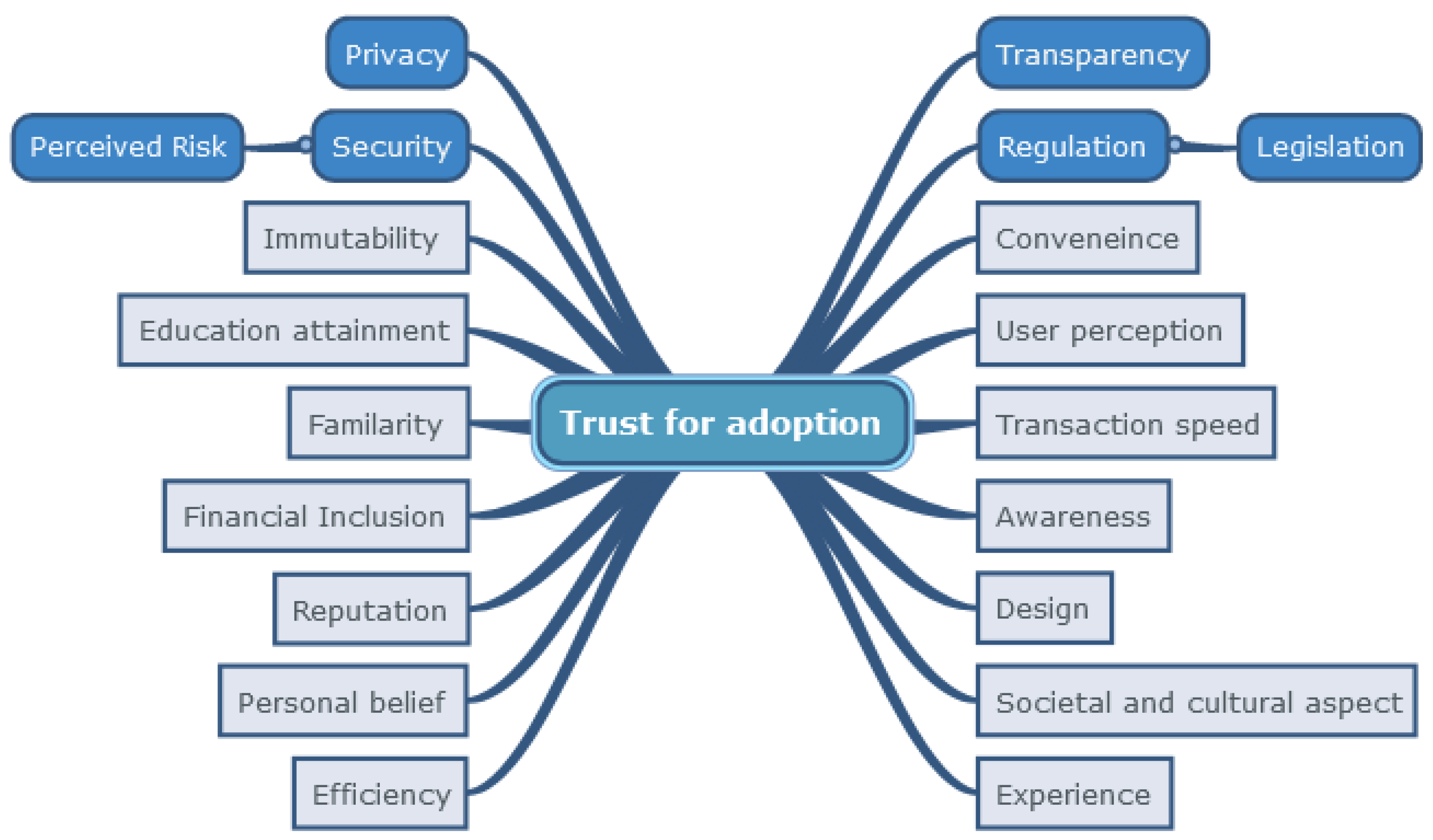

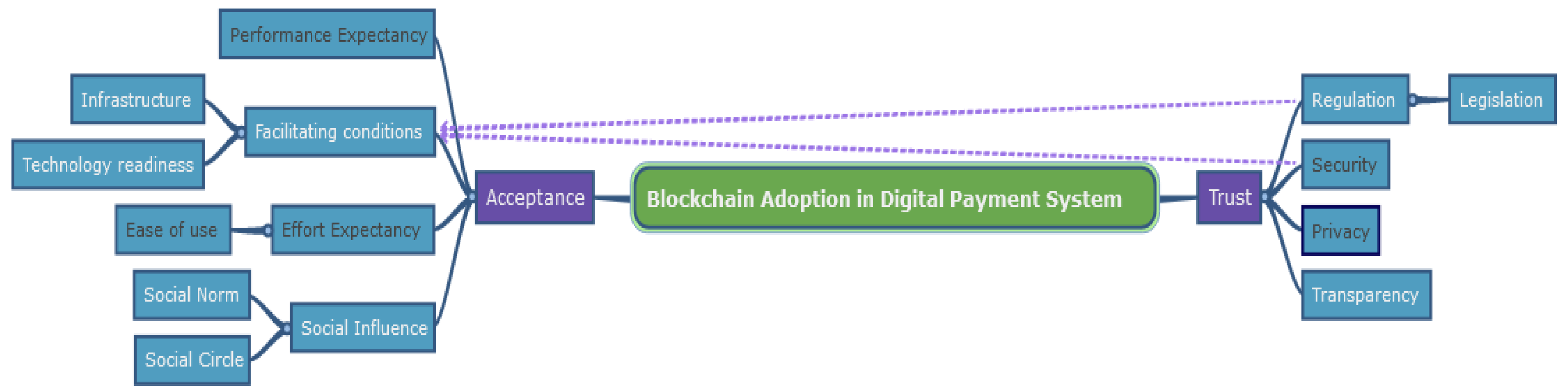

6.1. Factors That Influence Trust for Blockchain Adoption in Digital Payment Systems

6.1.1. Security

6.1.2. Privacy

6.1.3. Transparency

6.1.4. Regulation

6.1.5. Other Factors Influencing Trust

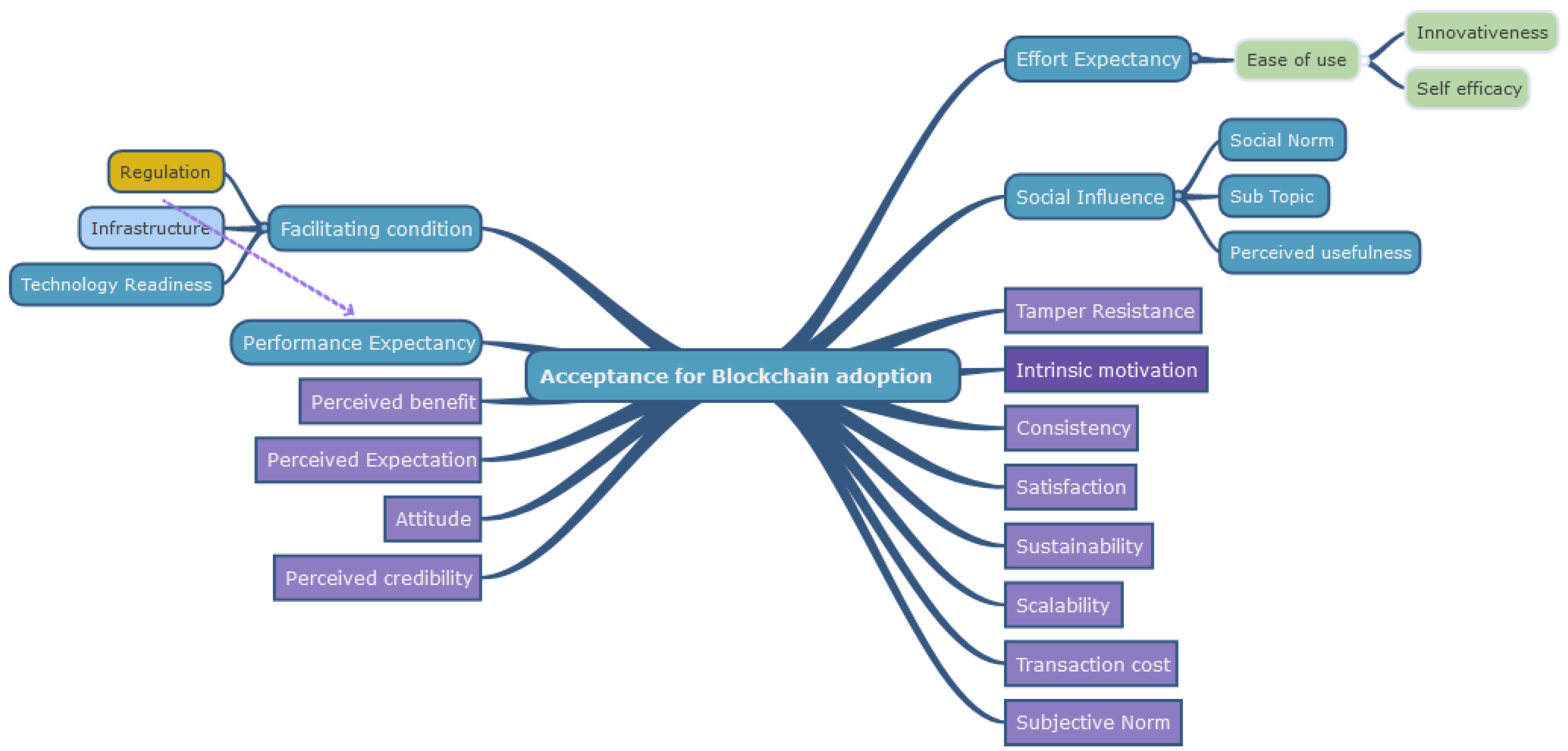

6.2. Factors That Influence Acceptance for Blockchain Adoption in Digital Payment Systems

6.2.1. Performance Expectancy

6.2.2. Effort Expectancy

6.2.3. Social Influence

6.2.4. Facilitating Conditions

6.2.5. Other Factors Influencing Acceptance

7. Discussion

7.1. Trust Enhancement

7.2. Strengthening Acceptance

7.3. Integrating Trust and Acceptance Factors to Reinforce Blockchain Adoption

8. Future Research Directions

9. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| UTAUT | Unified Theory of Acceptance and Use of Technology |

| PE | Performance Expectancy |

| EE | Effort Expectancy |

| SI | Social Influence |

| FC | Facilitating Condition |

Appendix A

| Sl. No | Author and Year | Security | Privacy | Reg | Tra | PE | EE | SI | FC |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Agbezoutsi et al., 2021 [51] | Y | Y | ||||||

| 2 | Ahmed et al. [30] | Y | Y | Y | |||||

| 3 | Ahn et al., 2019 [52] | Y | |||||||

| 4 | Al Karim et al., 2023 [9] | Y | Y | Y | |||||

| 5 | Auer and Tercero-Lucas, 2022 [53] | Y | Y | ||||||

| 6 | Biryukov and Tikhomirov, 2019 [54] | Y | Y | Y | Y | ||||

| 7 | Br et al., 2023 [50] | Y | Y | ||||||

| 8 | Butijn et al., 2020 [34] | Y | Y | Y | Y | ||||

| 9 | Campbell-Verduyn and Goguen, 2019 [22] | Y | |||||||

| 10 | Chiu, 2017 [55] | Y | Y | Y | |||||

| 11 | Clavin et al., 2020 [37] | Y | Y | Y | Y | ||||

| 12 | De Filippi and Loveluck, 2016 [56] | Y | Y | Y | |||||

| 13 | Fan et al., 2020 [57] | Y | Y | ||||||

| 14 | Guo, 2022 [19] | Y | Y | ||||||

| 15 | Han et al., 2022 [58] | Y | Y | Y | Y | ||||

| 16 | Haugum et al., 2022 [59] | Y | Y | Y | |||||

| 17 | Hwang et al., 2021 [78] | Y | Y | ||||||

| 18 | Knittel et al., 2019 [60] | Y | Y | ||||||

| 19 | Kolb et al., 2020 [61] | Y | |||||||

| 20 | Kowalski et al., 2023 [62] | Y | Y | Y | Y | ||||

| 21 | Li et al., 2021 [63] | Y | |||||||

| 22 | Liao et al., 2021 [64] | Y | Y | ||||||

| 23 | Lou et al., 2017 [32] | Y | |||||||

| 24 | Malherbe et al., 2019 [65] | Y | Y | Y | |||||

| 25 | Mansoor et al., 2023 [2] | Y | Y | Y | Y | Y | Y | Y | Y |

| 26 | Mensah and Mwakapesa, 2022 [25] | Y | Y | Y | Y | Y | Y | Y | Y |

| 27 | Mercan et al., 2021 [66] | Y | |||||||

| 28 | Mohanty et al., 2022 [35] | Y | Y | ||||||

| 29 | Narendra and Aghila, 2021 [67] | Y | |||||||

| 30 | Nerurkar et al., 2021 [68] | Y | |||||||

| 31 | Nuryyev et al., 2020 [69] | Y | Y | Y | Y | ||||

| 32 | Pal et al., 2021 [29] | Y | Y | Y | |||||

| 33 | Palos-Sanchez et al., 2021 [29] | Y | Y | Y | |||||

| 34 | Purohit et al., 2022 [33] | Y | Y | Y | Y | ||||

| 35 | Saxena et al., 2016 [70] | Y | |||||||

| 36 | Song et al., 2022 [31] | Y | Y | Y | Y | ||||

| 37 | Stach et al., 2022 [39] | Y | Y | Y | |||||

| 38 | Tian et al., 2022 [71] | Y | Y | Y | Y | ||||

| 39 | Trebat, 2023 [72] | Y | Y | Y | Y | Y | Y | ||

| 40 | Treiblmaier et al., 2021 [36] | Y | Y | Y | |||||

| 41 | Visconti-Caparros and Campos-Blazquez, 2022 [73] | Y | Y | ||||||

| 42 | Waheed et al., 2020 [74] | Y | Y | Y | |||||

| 43 | Wang et al., 2019 [40] | Y | Y | Y | |||||

| 44 | Wong et al., 2020 [21] | Y | Y | Y | Y | Y | Y | Y | Y |

| 45 | Zhang et al., 2019 [38] | Y | Y | ||||||

| 46 | Zhang, 2022 [75] | Y | Y | Y | |||||

| 47 | Zhu and Wang, 2019 [76] | Y | Y | Y | |||||

| 48 | Zutshi et al., 2021 [77] | Y | Y | Y | Y |

References

- Sumanjeet. Emergence of payment systems in the age of electronic commerce: The state of art. In Proceedings of the 2009 First Asian Himalayas International Conference on Internet, Kathmandu, Nepal, 3–5 November 2009; IEEE: Piscataway, NJ, USA, 2009; pp. 1–18. [Google Scholar]

- Mansoor, M.; Abbasi, A.Z.; Abbasi, G.A.; Ahmad, S.; Hwang, Y. Exploring the determinants affecting the usage of blockchain-based remittance services: An empirical study on the banking sector. Behav. Inf. Technol. 2023, 1–19. [Google Scholar] [CrossRef]

- Palos-Sanchez, P.; Saura, J.R.; Ayestaran, R. An exploratory approach to the adoption process of bitcoin by business executives. Mathematics 2021, 9, 355. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 2008. Available online: https://www.ussc.gov/sites/default/files/pdf/training/annual-national-training-seminar/2018/Emerging_Tech_Bitcoin_Crypto.pdf (accessed on 1 March 2024).

- Hashemi Joo, M.; Nishikawa, Y.; Dandapani, K. Cryptocurrency, a successful application of blockchain technology. Manag. Financ. 2020, 46, 715–733. [Google Scholar] [CrossRef]

- Nguyen, Q.K. Blockchain-a financial technology for future sustainable development. In Proceedings of the 2016 3rd International Conference on Green Technology and Sustainable Development (GTSD), Kaohsiung, Taiwan, 24–25 November 2016; IEEE: Piscataway, NJ, USA, 2016; pp. 51–54. [Google Scholar]

- Han, X.; Yuan, Y.; Wang, F.Y. A blockchain-based framework for central bank digital currency. In Proceedings of the 2019 IEEE International Conference on Service Operations and Logistics, and Informatics (SOLI), Zhengzhou, China, 6–8 November 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 263–268. [Google Scholar]

- Papadaki, M.; Karamitsos, I. Blockchain technology in the Middle East and North Africa region. Inf. Technol. Dev. 2021, 27, 617–634. [Google Scholar] [CrossRef]

- Al Karim, R.; Rabiul, M.K.; Ishrat, M.; Promsivapallop, P.; Kawser, S. Can blockchain payment services influence customers’ loyalty intention in the hospitality industry? A mediation assessment. Adm. Sci. 2023, 13, 85. [Google Scholar] [CrossRef]

- Albayati, H.; Kim, S.K.; Rho, J.J. Accepting financial transactions using blockchain technology and cryptocurrency: A customer perspective approach. Technol. Soc. 2020, 62, 101320. [Google Scholar] [CrossRef]

- Liu, N.; Ye, Z. Empirical research on the blockchain adoption–based on TAM. Appl. Econ. 2021, 53, 4263–4275. [Google Scholar] [CrossRef]

- Mendoza-Tello, J.C.; Mora, H.; Pujol-López, F.A.; Lytras, M.D. Disruptive innovation of cryptocurrencies in consumer acceptance and trust. Inf. Syst.-Bus. Manag. 2019, 17, 195–222. [Google Scholar] [CrossRef]

- Alazab, M.; Alhyari, S.; Awajan, A.; Abdallah, A.B. Blockchain technology in supply chain management: An empirical study of the factors affecting user adoption/acceptance. Clust. Comput. 2021, 24, 83–101. [Google Scholar] [CrossRef]

- Bahmanziari, T.; Pearson, J.M.; Crosby, L. Is trust important in technology adoption? A policy capturing approach. J. Comput. Inf. Syst. 2003, 43, 46–54. [Google Scholar]

- Shin, D.; Bianco, W.T. In blockchain we trust: Does blockchain itself generate trust? Soc. Sci. Q. 2020, 101, 2522–2538. [Google Scholar] [CrossRef]

- Srivastava, S.C.; Chandra, S.; Theng, Y.L. Evaluating the role of trust in consumer adoption of mobile payment systems: An empirical analysis. Commun. Assoc. Inf. Syst. 2010, 27, 561–588. [Google Scholar]

- Li, X.; Hess, T.J.; Valacich, J.S. Why do we trust new technology? A study of initial trust formation with organizational information systems. J. Strateg. Inf. Syst. 2008, 17, 39–71. [Google Scholar] [CrossRef]

- Fleischmann, M.; Ivens, B. Exploring the Role of Trust in Blockchain Adoption: An Inductive Approach; 2019. Available online: http://hdl.handle.net/10125/60120 (accessed on 1 March 2024).

- Guo, Y. Digital Trust and the Reconstruction of Trust in the Digital Society: An Integrated Model based on Trust Theory and Expectation Confirmation Theory. Digit. Gov. Res. Pract. 2022, 3, 1–19. [Google Scholar] [CrossRef]

- Hegner, S.M.; Beldad, A.D.; Brunswick, G.J. In automatic we trust: Investigating the impact of trust, control, personality characteristics, and extrinsic and intrinsic motivations on the acceptance of autonomous vehicles. Int. J.-Hum.-Comput. Interact. 2019, 35, 1769–1780. [Google Scholar] [CrossRef]

- Wong, L.W.; Tan, G.W.H.; Lee, V.H.; Ooi, K.B.; Sohal, A. Unearthing the determinants of Blockchain adoption in supply chain management. Int. J. Prod. Res. 2020, 58, 2100–2123. [Google Scholar] [CrossRef]

- CAMPBELL-VERDUYN, M.; Goguen, M. Blockchains, trust and action nets: Extending the pathologies of financial globalization. Glob. Netw. 2019, 19, 308–328. [Google Scholar] [CrossRef]

- AlHogail, A. Improving IoT technology adoption through improving consumer trust. Technologies 2018, 6, 64. [Google Scholar] [CrossRef]

- Gkinko, L.; Elbanna, A. Designing trust: The formation of employees’ trust in conversational AI in the digital workplace. J. Bus. Res. 2023, 158, 113707. [Google Scholar] [CrossRef]

- Mensah, I.K.; Mwakapesa, D.S. The drivers of the behavioral adoption intention of BITCOIN payment from the perspective of Chinese citizens. Secur. Commun. Netw. 2022, 2022, 7373658. [Google Scholar] [CrossRef]

- Taherdoost, H. A review of technology acceptance and adoption models and theories. Procedia Manuf. 2018, 22, 960–967. [Google Scholar] [CrossRef]

- Dillon, A.; Morris, M.G. User Acceptance of New Information Technology: Theories and Models; 1996. Available online: https://www.learntechlib.org/p/82513/ (accessed on 1 March 2024).

- Bradley, J. The technology acceptance model and other user acceptance theories. In Handbook of Research on Contemporary Theoretical Models in Information Systems; IGI Global: Pennsylvania, PA, USA, 2009; pp. 277–294. [Google Scholar]

- Pal, S.; Hill, A.; Rabehaja, T.; Hitchens, M. A blockchain-based trust management framework with verifiable interactions. Comput. Netw. 2021, 200, 108506. [Google Scholar] [CrossRef]

- Ahmed, K.A.; Saraya, S.F.; Wanis, J.F.; Ali-Eldin, A.M. A Blockchain Self-Sovereign Identity for Open Banking Secured by the Customer’s Banking Cards. Future Internet 2023, 15, 208. [Google Scholar] [CrossRef]

- Song, Y.; Sun, C.; Peng, Y.; Zeng, Y.; Sun, B. Research on multidimensional trust evaluation mechanism of fintech based on blockchain. IEEE Access 2022, 10, 57025–57036. [Google Scholar] [CrossRef]

- Lou, A.T.; Li, E.Y. Integrating Innovation Diffusion Theory and the Technology Acceptance Model: The Adoption of Blockchain Technology from Business Managers’ Perspective; 2017. Available online: https://www.semanticscholar.org/paper/Integrating-Innovation-Diffusion-Theory-and-the-The-Lou-Li/30714b0fcb924363d32f106b1b6af7b43d167bb9 (accessed on 1 March 2024).

- Purohit, S.; Arora, R.; Paul, J. The bright side of online consumer behavior: Continuance intention for mobile payments. J. Consum. Behav. 2022, 21, 523–542. [Google Scholar] [CrossRef]

- Butijn, B.J.; Tamburri, D.A.; Heuvel, W.J.v.d. Blockchains: A systematic multivocal literature review. ACM Comput. Surv. (CSUR) 2020, 53, 1–37. [Google Scholar] [CrossRef]

- Mohanty, D.; Anand, D.; Aljahdali, H.M.; Villar, S.G. Blockchain interoperability: Towards a sustainable payment system. Sustainability 2022, 14, 913. [Google Scholar] [CrossRef]

- Treiblmaier, H.; Swan, M.; De Filippi, P.; Lacity, M.; Hardjono, T.; Kim, H. What’s Next in Blockchain Research? -An Identification of Key Topics Using a Multidisciplinary Perspective. In ACM SIGMIS Database: The Database for Advances in Information Systems; 2021; Volume 52, pp. 27–52. Available online: https://dl.acm.org/doi/10.1145/3447934.3447938 (accessed on 1 March 2024).

- Clavin, J.; Duan, S.; Zhang, H.; Janeja, V.P.; Joshi, K.P.; Yesha, Y.; Erickson, L.C.; Li, J.D. Blockchains for government: Use cases and challenges. Digit. Gov. Res. Pract. 2020, 1, 1–21. [Google Scholar] [CrossRef]

- Zhang, R.; Xue, R.; Liu, L. Security and privacy on blockchain. ACM Comput. Surv. (CSUR) 2019, 52, 1–34. [Google Scholar] [CrossRef]

- Stach, C.; Gritti, C.; Przytarski, D.; Mitschang, B. Assessment and treatment of privacy issues in blockchain systems. ACM SIGAPP Appl. Comput. Rev. 2022, 22, 5–24. [Google Scholar] [CrossRef]

- Wang, S.; Tang, X.; Zhang, Y.; Chen, J. Auditable protocols for fair payment and physical asset delivery based on smart contracts. IEEE Access 2019, 7, 109439–109453. [Google Scholar] [CrossRef]

- Chaudhry, U.B.; Hydros, A.K. Zero-trust-based security model against data breaches in the banking sector: A blockchain consensus algorithm. IET Blockchain 2023, 3, 98–115. [Google Scholar] [CrossRef]

- Yao, Q.; Wang, Q.; Zhang, X.; Fei, J. Dynamic access control and authorization system based on zero-trust architecture. In Proceedings of the 2020 1st International Conference on Control, Robotics and Intelligent System, Xiamen, China, 27–29 October 2020; pp. 123–127. [Google Scholar]

- Li, Q.; Wen, Z.; Wu, Z.; Hu, S.; Wang, N.; Li, Y.; Liu, X.; He, B. A Survey on Federated Learning Systems: Vision, Hype and Reality for Data Privacy and Protection. IEEE Trans. Knowl. Data Eng. 2023, 35, 3347–3366. [Google Scholar] [CrossRef]

- Yin, X.; Zhu, Y.; Hu, J. A comprehensive survey of privacy-preserving federated learning: A taxonomy, review, and future directions. ACM Comput. Surv. (CSUR) 2021, 54, 1–36. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Rother, E.T. Systematic literature review X narrative review. Acta Paul. Enferm. 2007, 20, v–vi. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; Prisma Group. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. Ann. Intern. Med. 2009, 151, 264–269. [Google Scholar] [CrossRef] [PubMed]

- Khabsa, M.; Elmagarmid, A.; Ilyas, I.; Hammady, H.; Ouzzani, M. Learning to identify relevant studies for systematic reviews using random forest and external information. Mach. Learn. 2015, 102, 465–482. [Google Scholar] [CrossRef]

- Software, V. MAXQDA 2022. Version 2022.8. Available online: https://www.maxqda.com (accessed on 12 September 2023).

- Brandl, B.; Dieterich, L. The exclusive nature of global payments infrastructures: The significance of major banks and the role of tech-driven companies. Rev. Int. Political Econ. 2023, 30, 535–557. [Google Scholar] [CrossRef]

- Agbezoutsi, K.E.; Urien, P.; Dandjinou, T.M. Mobile money traceability and federation using blockchain services. Ann. Telecommun. 2021, 76, 223–233. [Google Scholar] [CrossRef]

- Ahn, J.; Park, M.; Shin, H.; Paek, J. A model for deriving trust and reputation on blockchain-based e-payment system. Appl. Sci. 2019, 9, 5362. [Google Scholar] [CrossRef]

- Auer, R.; Tercero-Lucas, D. Distrust or speculation? The socioeconomic drivers of US cryptocurrency investments. J. Financ. Stab. 2022, 62, 101066. [Google Scholar] [CrossRef]

- Biryukov, A.; Tikhomirov, S. Security and privacy of mobile wallet users in Bitcoin, Dash, Monero, and Zcash. Pervasive Mob. Comput. 2019, 59, 101030. [Google Scholar] [CrossRef]

- Chiu, I.H. A new era in fintech payment innovations? A perspective from the institutions and regulation of payment systems. Law Innov. Technol. 2017, 9, 190–234. [Google Scholar] [CrossRef]

- De Filippi, P.; Loveluck, B. The invisible politics of bitcoin: Governance crisis of a decentralized infrastructure. Internet Policy Rev. 2016, 5. [Google Scholar] [CrossRef]

- Fan, X.; Liu, L.; Zhang, R.; Jing, Q.; Bi, J. Decentralized trust management: Risk analysis and trust aggregation. ACM Comput. Surv. (CSUR) 2020, 53, 1–33. [Google Scholar] [CrossRef]

- Han, R.; Yan, Z.; Liang, X.; Yang, L.T. How can incentive mechanisms and blockchain benefit with each other? a survey. ACM Comput. Surv. 2022, 55, 1–38. [Google Scholar] [CrossRef]

- Haugum, T.; Hoff, B.; Alsadi, M.; Li, J. Security and Privacy Challenges in Blockchain Interoperability-A Multivocal Literature Review. In Proceedings of the 26th International Conference on Evaluation and Assessment in Software Engineering, Gothenburg, Sweden, 13–15 June 2022; pp. 347–356. [Google Scholar]

- Knittel, M.; Pitts, S.; Wash, R. “The Most Trustworthy Coin” How Ideological Tensions Drive Trust in Bitcoin. Proc. ACM Hum.-Comput. Interact. 2019, 3, 1–23. [Google Scholar] [CrossRef]

- Kolb, J.; AbdelBaky, M.; Katz, R.H.; Culler, D.E. Core concepts, challenges, and future directions in blockchain: A centralized tutorial. ACM Comput. Surv. (CSUR) 2020, 53, 1–39. [Google Scholar] [CrossRef]

- Kowalski, L.; Green, W.; Lilley, S.; Panourgias, N. Lackluster Adoption of Cryptocurrencies as a Consumer Payment Method in the United States—Hypothesis: Is This Independent Technology in Need of a Brand, and What Kind? J. Risk Financ. Manag. 2022, 16, 23. [Google Scholar] [CrossRef]

- Li, Y.; Jiang, S.; Shi, J.; Wei, Y. Pricing strategies for blockchain payment service under customer heterogeneity. Int. J. Prod. Econ. 2021, 242, 108282. [Google Scholar] [CrossRef]

- Liao, Q.; Shao, M. Discussion on payment application in cross-border e-commerce platform from the perspective of blockchain. In Proceedings of the E3S Web of Conferences, Strasbourg, France, 5–7 May 2021; EDP Sciences: Les Ulis, France, 2021; Volume 235. [Google Scholar]

- Malherbe, L.; Montalban, M.; Bédu, N.; Granier, C. Cryptocurrencies and blockchain: Opportunities and limits of a new monetary regime. Int. J. Political Econ. 2019, 48, 127–152. [Google Scholar] [CrossRef]

- Mercan, S.; Erdin, E.; Akkaya, K. Improving transaction success rate in cryptocurrency payment channel networks. Comput. Commun. 2021, 166, 196–207. [Google Scholar] [CrossRef]

- Narendra, K.; Aghila, G. Fortis-ámyna-smart contract model for cross border financial transactions. ICT Express 2021, 7, 269–273. [Google Scholar] [CrossRef]

- Nerurkar, P.; Patel, D.; Busnel, Y.; Ludinard, R.; Kumari, S.; Khan, M.K. Dissecting bitcoin blockchain: Empirical analysis of bitcoin network (2009–2020). J. Netw. Comput. Appl. 2021, 177, 102940. [Google Scholar] [CrossRef]

- Nuryyev, G.; Wang, Y.P.; Achyldurdyyeva, J.; Jaw, B.S.; Yeh, Y.S.; Lin, H.T.; Wu, L.F. Blockchain technology adoption behavior and sustainability of the business in tourism and hospitality SMEs: An empirical study. Sustainability 2020, 12, 1256. [Google Scholar] [CrossRef]

- Saxena, N.; Sloan, J.J.; Godbole, M.; Cai, J.Y.J.; Georgescu, M.; Harper, O.N.; Schwebel, D.C. Consumer Perceptions of Mobile and Traditional Point-of-Sale Credit/Debit Card Systems in the United States: A Survey. Int. J. Cyber Criminol. 2015, 9, 162. [Google Scholar]

- Tian, X.; Zhu, J.; Zhao, X.; Wu, J. Improving operational efficiency through blockchain: Evidence from a field experiment in cross-border trade. Prod. Plan. Control 2022, 1–16. [Google Scholar] [CrossRef]

- Trebat, N.M. Stateless Money? Cryptocurrency and Digital Banking in Brazil. J. Econ. Issues 2023, 57, 450–457. [Google Scholar] [CrossRef]

- Visconti-Caparrós, J.M.; Campos-Blázquez, J.R. The development of alternate payment methods and their impact on customer behavior: The Bizum case in Spain. Technol. Forecast. Soc. Chang. 2022, 175, 121330. [Google Scholar] [CrossRef]

- Waheed, N.; He, X.; Ikram, M.; Usman, M.; Hashmi, S.S.; Usman, M. Security and privacy in IoT using machine learning and blockchain: Threats and countermeasures. ACM Comput. Surv. (CSUR) 2020, 53, 1–37. [Google Scholar] [CrossRef]

- Zhang, Y. Research on multiparty payment technology based on blockchain and smart contract mechanism. J. Math. 2022, 2022. [Google Scholar] [CrossRef]

- Zhu, X.; Wang, D. Research on blockchain application for E-commerce, finance and energy. In IOP Conference Series: Earth and Environmental Science; IOP Publishing: Bristol, UK, 2019; Volume 252, p. 042126. [Google Scholar]

- Zutshi, A.; Grilo, A.; Nodehi, T. The value proposition of blockchain technologies and its impact on Digital Platforms. Comput. Ind. Eng. 2021, 155, 107187. [Google Scholar] [CrossRef]

- Hwang, Y.; Park, S.; Shin, N. Sustainable development of a mobile payment security environment using fintech solutions. Sustainability 2021, 13, 8375. [Google Scholar] [CrossRef]

- Irani, Z.; Dwivedi, Y.K.; Williams, M.D. Understanding consumer adoption of broadband: An extension of the technology acceptance model. J. Oper. Res. Soc. 2009, 60, 1322–1334. [Google Scholar] [CrossRef]

| Factors | Articles | Insights |

|---|---|---|

| Security | [2,3,9,19,21,22,25,29,30,31,32,33,34,35,36,37,38,39,40,50,51,52,53,54,55,56,57,58,59,60,61,62,63,64,65,66,67,68,69,70,71,72,73,74,75,76,77] | Trust can be fostered by highlighting the need for further development to create security. |

| Privacy | [2,3,9,19,21,25,29,30,31,34,35,37,38,39,54,55,56,57,58,59,60,61,62,65,69,72,74,75,76,77,78] | Consumers look for control and authorisation for sharing transactions to prevent privacy leaks. |

| Transparency | [2,3,9,21,22,25,29,31,34,36,37,40,51,58,59,63,65,72,74,75,76,77] | Banks implement blockchain-based payment services for safe, transparent, efficient, and cost-effective financial transactions. |

| Regulation | [2,21,25,30,31,34,36,37,39,40,50,53,55,56,58,60,62,64,65,69,73,77] | With effective government regulations, using blockchains can offer security for adoption. |

| Factors | Articles | Insights |

|---|---|---|

| Performance Expectancy | [2,21,25,33,72] | The degree to which individuals believe that technology can assist them in accomplishing their professional goals. |

| Effort Expectancy | [2,21,25,32,33,71,72] | An individual’s personal assessment of the technology’s usability, which includes their perception of the technology’s simplicity and the lack of mental or physical effort needed to operate it. |

| Social Influence | [2,21,25,33,62,69,71,72] | Individuals’ perceptions of the degree to which others assist them in adopting a particular technology |

| Facilitating conditions | [2,21,25,33,71,72] | Pertains to the evaluation made by users regarding the infrastructure support provided for utilising a particular technology or system. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Norbu, T.; Park, J.Y.; Wong, K.W.; Cui, H. Factors Affecting Trust and Acceptance for Blockchain Adoption in Digital Payment Systems: A Systematic Review. Future Internet 2024, 16, 106. https://doi.org/10.3390/fi16030106

Norbu T, Park JY, Wong KW, Cui H. Factors Affecting Trust and Acceptance for Blockchain Adoption in Digital Payment Systems: A Systematic Review. Future Internet. 2024; 16(3):106. https://doi.org/10.3390/fi16030106

Chicago/Turabian StyleNorbu, Tenzin, Joo Yeon Park, Kok Wai Wong, and Hui Cui. 2024. "Factors Affecting Trust and Acceptance for Blockchain Adoption in Digital Payment Systems: A Systematic Review" Future Internet 16, no. 3: 106. https://doi.org/10.3390/fi16030106