Analysis of the European Strategy for Hydrogen: A Comprehensive Review

Abstract

:1. Introduction

2. European Organisations, Initiatives, and Plans regarding Renewable Energy and Hydrogen

- Paris Agreement [9]: This agreement was already mentioned in the Introduction section, which is not rare given that it is one of the most popular environmental initiatives worldwide. As said before, through this initiative, different nations aim to maintain the rise in global temperature in this century below 2 °C above pre-industrial levels or even limit it to 1.5 °C.

- UN Sustainable Development Goals [18]: The United Nations developed the 17 sustainable development goals as part of its 2030 Agenda for Sustainable Development; all the UN member states committed to these goals in 2015, and every year, the UN reports the progress achieved. While all of these goals are equally important and crucial to sustainable growth, the ones concerning the topics of this review are: “Goal 7: Affordable and clean energy”, “Goal 9: Industry, innovation and infrastructure”, and “Goal 13: Climate action”.

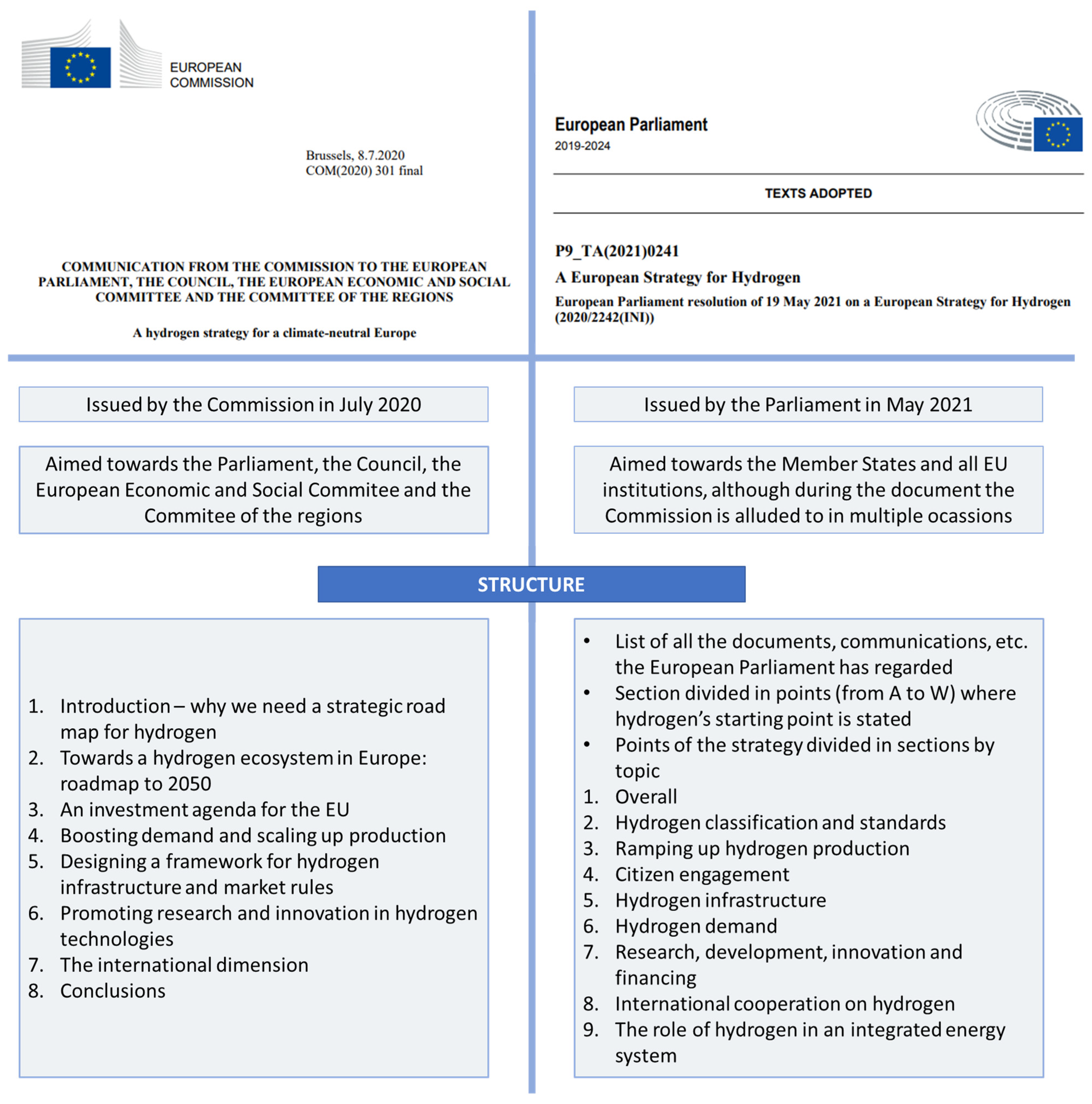

3. The European Strategy for Hydrogen

- Documents, reports, communications, directives, and just about everything falling under the spectrum of information the European Parliament has regarded in order to create this text.

- Goals and starting point for the hydrogen strategy.

- The statements made by the European Parliament.

- Moreover, the statements are also subdivided, facilitating the review and analysis. These subdivisions, which are subsequently developed, are the following:

- Overall.

- Hydrogen classification and standards.

- Ramping up hydrogen production.

- Citizen engagement.

- Hydrogen infrastructure.

- Hydrogen demand.

- Research, development, innovation, and financing.

- International cooperation on hydrogen.

- The role of hydrogen in an integrated energy system.

3.1. Statements

3.1.1. Overall

The EU hydrogen strategy [needs to] cover the whole value chain [and also has to] be compatible with [the agreements, plans, and goals already existing, particularly:] the Paris Agreement, the EU’s climate and energy targets for 2030 and 2050, the circular economy, the action plan for critical raw materials and the UN Sustainable Development Goals.

Welcomes the hydrogen strategy for a climate-neutral Europe proposed by the Commission including the future revision of the Renewable Energy Directive, as well as […] the Member State strategies and investment plans for hydrogen. [It] also urges the Commission to align its approach on hydrogen with the new EU industrial strategy and make it a part of a coherent industrial policy.

- Reinforce the resilience of the single market.

- Support EU’s open strategic autonomy by addressing strategic dependencies.

- Accelerate the twin transitions.

The importance of the principle of technology neutrality, [specifically:] the EU Parliament underlines the importance of a resilient and climate-neutral energy system based on the principles of energy efficiency, cost efficiency, affordability, and security of supply. [It also] notes that direct electrification from renewable sources is more cost-, resource-, and energy-efficient than hydrogen […] but factors such as security of supply, technical feasibility and energy system considerations should be taken into account when determining how a sector should decarbonise.

The need to maintain and further develop EU technological leadership in clean hydrogen through a competitive and sustainable hydrogen economy with an integrated hydrogen market.

Recognises the efforts undertaken by hydrogen valleys […] throughout the EU […], underlines their important role initiating the production and application of renewable hydrogen and urges the Commission to build on these initiatives, support their development and help those involved to pool their know-how and investments.

- They are large in scale.

- They have a clearly defined geographic scope.

- They cover the value chain broadly.

- They supply to various end sectors.

Hydrogen produced from renewable sources is key to the EU’s energy transition as only renewable hydrogen can sustainably contribute to achieving climate neutrality in the long term, [but also] notes with concern that renewable hydrogen is not yet competitive.

Highlights that hydrogen-derived products such as synthetic fuels produced with renewable energy constitute a carbon-neutral alternative to fossil fuels and can […] contribute […] to the decarbonisation of a wide variety of sectors.

3.1.2. Hydrogen Classification and Standards

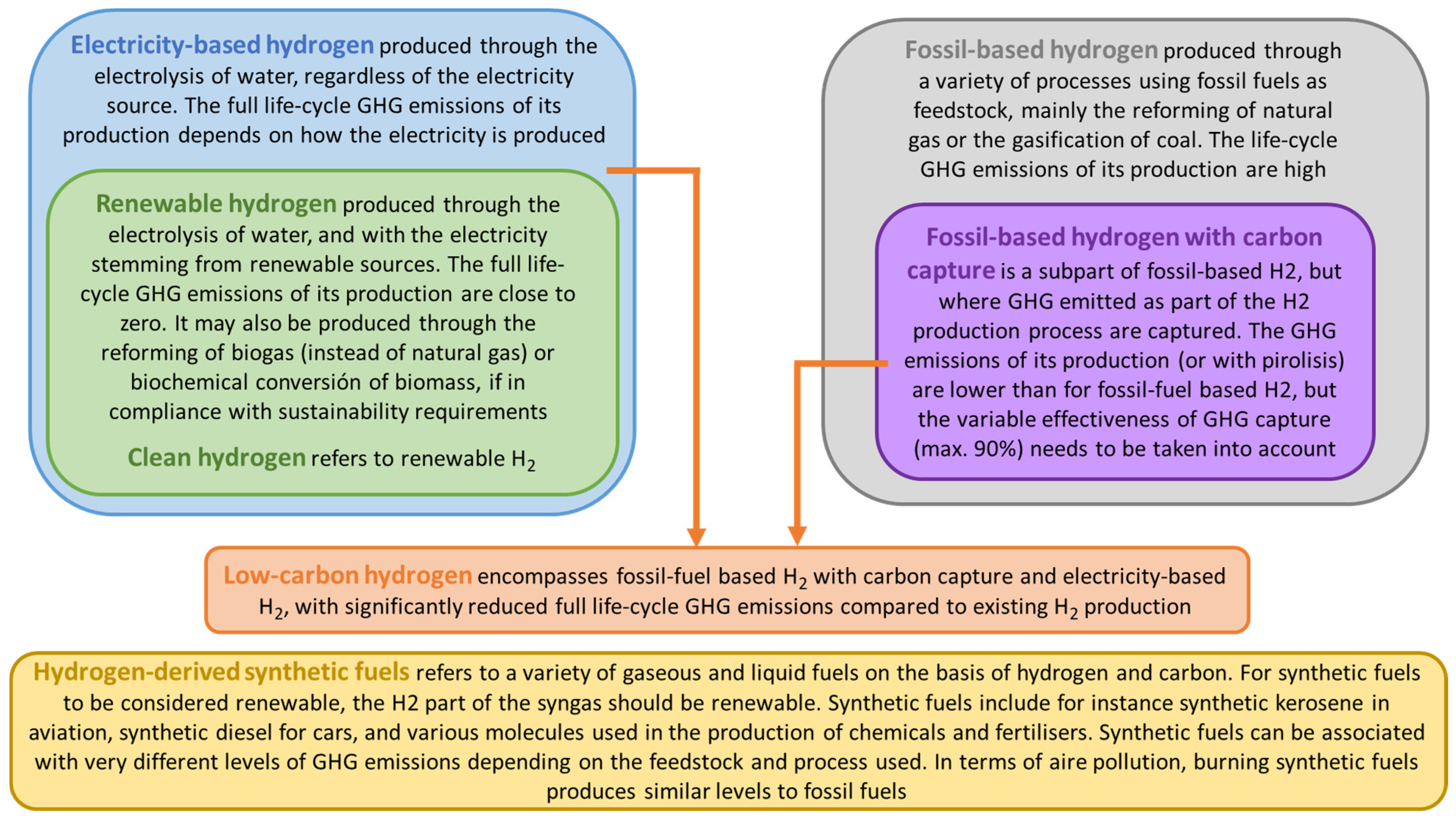

A common legal classification of the different types of hydrogen is of utmost importance, [and] the classification proposed by the Commission [is welcomed] as a first step. [This classification will require] comprehensive, precise, science-based and uniform EU-wide terminology [that will enable the adoption of] national legal definitions; [therefore, the Commission is urged to] conclude its work on establishing such terminology.

[Furthermore, the classification] should be determined according to an independent, science-based assessment, stepping away from the commonly used colour-based approach; [moreover, some desired characteristics for the classification are:]

- It should be based on the life cycle GHG emissions throughout hydrogen’s entire production and transport process

- It should take into account transparent and robust sustainability criteria in line with the principles of the circular economy

- It should be based on averages and standard values per category, such as the objectives of sustainable use and the protection of resources, the handling of waste and the increased use of raw and secondary materials, pollution prevention and control, and finally, the protection and restoration of biodiversity and ecosystems.

Notes […] that avoiding using two names for the same category of hydrogen, namely ‘renewable’ and ‘clean’, as proposed by the Commission, would provide further clarification, and […] that the term ‘renewable hydrogen’ is the most objective and science-based option.

- Green Hydrogen: produced through the electrolysis of water; the electricity that powers the electrolyser comes from renewable sources (wind, solar…); therefore, green hydrogen has no associated GHG emissions. It can also include hydrogen produced from waste biomass.

- Blue Hydrogen: it is produced by steam reforming together with carbon capture and storage (CCS).

- Grey Hydrogen: it is produced from fossil fuels, mostly by steam methane reforming but without carbon capture and storage. Some sources include black and brown hydrogen in this category.

- Brown and black Hydrogen: these types of hydrogen are produced through the gasification of brown coal (brown hydrogen) and black coal (black hydrogen), although some sources consider that hydrogen produced through the gasification of any fossil fuel is black or brown hydrogen. Since there is no carbon capture associated, this is the most environmentally damaging type of hydrogen.

- Turquoise hydrogen: this is the hydrogen produced through methane pyrolysis, resulting in hydrogen and solid carbon. There are no GHG emissions associated with the production itself. However, depending on the source making the classification, there are emissions associated with the mining and transport of the natural gas, emissions associated with how the thermal process is powered, and emissions associated with the use of the solid carbon generated as a by-product (whether it is used or stored).

- Pink/purple hydrogen: hydrogen produced through electrolysis powered by nuclear energy. Sometimes this type is also called red or even yellow, depending on the source making the classification.

- Yellow hydrogen: this colour for hydrogen demonstrates the lack of homogeneity previously acknowledged, since it is used to describe hydrogen produced by electrolysis using electricity from the grid, hydrogen produced by electrolysis using solar power, hydrogen produced through direct water splitting, or as mentioned before, it can sometimes be alluding to what is known as purple hydrogen.

- White hydrogen: this type of hydrogen is found in underground deposits, generated by natural geochemical processes inside the Earth’s crust. While this is the main definition, some sources also describe white hydrogen as the result of the direct splitting of water molecules thanks to concentrated solar energy.

- Renewable hydrogen (as defined in the proposal directive to amend RED II): renewable fuels of non-biological origin and biomass fuels that meet a 70% GHG emission reduction compared to fossil fuels setting specific sub-targets for the consumption of renewable hydrogen (50% of total H2 consumption for energy and feedstock purposes in industry by 2030 and 2.6% of the energy supplied to the transport sector).

- Low-carbon hydrogen: hydrogen, the energy content of which is derived from non-renewable sources, that meets a GHG emission reduction threshold of 70%.

The classification of different types of hydrogen would inter alia serve the purpose of providing consumers with information and it is not meant to stall the expansion of hydrogen in general.

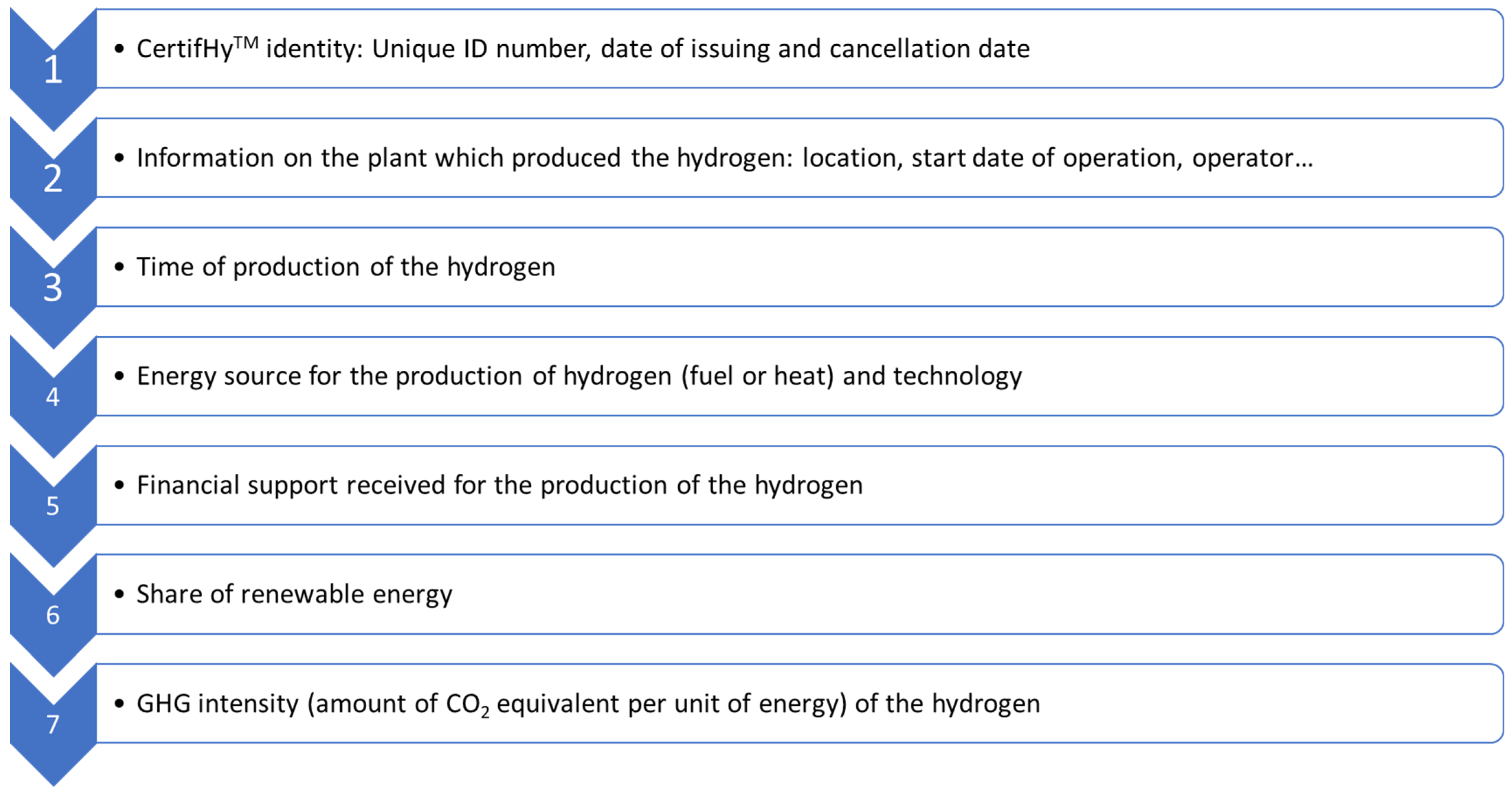

[Another matter at hand in this section is] the urgent need for EU and international standards and certification. [The EU Parliament] stresses that the standardisation system needs to be based on a holistic approach and must be applicable to imported hydrogen; calls on the Commission to introduce a regulatory framework with robust and transparent sustainability criteria for the certification and tracking of hydrogen in the EU, taking into account its greenhouse gas footprint throughout the value chain, including transport, in order to also trigger investment in sufficient supplementary renewable electricity generation; also calls on the Commission to provide […] a regulatory framework for hydrogen that ensures standardisation, certification, guarantees of origin, labelling and tradability across Member States.

- It incentivises the creation of a new business model through product differentiation.

- There is an increase in liquidity and transparency thanks to a globalised European market.

- It is a standardised solution recognised between the market players and makes it easy to trade.

- It provides trust to end consumers.

- It allows consumers to transfer value towards the production method they want to support.

- The use of renewable or low carbon H2 can be independent from the location.

- It increases the role of hydrogen in the energy transition.

- It measures the impact of CO2 emissions.

- Enables consumers disclosure.

Highlights that safety protocols in demand sectors need to be updated continuously with regard to hydrogen use […] [and] asks […] that best-practice examples and a hydrogen safety culture be promoted throughout the EU.

3.1.3. Ramping up Hydrogen Production

Highlights that in order to ensure the internal hydrogen market functions well […] a […] regulatory framework for a hydrogen market should be […] proposed by the Commission and calls on the Commission and the Member States to reduce regulatory and economic hurdles in order to foster a quick market uptake of hydrogen.

[This framework] should be aligned with other relevant legislation […]. The Commission [must] look […] into the review of the Renewable Energy Directive, the Energy Taxation Directive and the ETS Directive in order to ensure a level playing field and a future-proof regulatory framework.

[Moreover, the EU Parliament] believes that the EU gas market design and the Clean Energy Package could serve as a basis and example for the regulation of the hydrogen market.

An adequate regulatory framework [is a requisite, together with] the necessary investments [and competitive renewable energy, to make] renewable hydrogen competitive before 2030.

- Taxes and levies on renewable energy; the member states should reduce them in order to eliminate double charging of taxes and fees on electricity generated from hydrogen facilities.

- Missing regulation, poor regulatory environment, legal uncertainty, and inconsistency across countries.

- Issues regarding permits (for construction, deployment, operating…) due to the lack of H2 experience of the permitting authorities and the missing procedures for this sector; also, unclear requirements.

- High investments needed and high costs.

Coherent, integrated and comprehensive, respecting the principles of proportionality, subsidiarity and better regulation, [and allowing for the scaling up of the H2 market].

Encourages the Commission and the Member States to devise specific solutions in order to ramp up hydrogen production in less connected or isolated regions such as islands, while ensuring the development of related infrastructure, including by repurposing it.

[Moreover, it] stresses the potential to convert some existing industrial sites into renewable hydrogen production facilities, planning such conversions of industrial sites with the workers and their trade unions.

Welcomes the ambitious goals of increasing the capacity of electrolysers and renewable hydrogen production [and] calls on [this organisation] to develop a roadmap for the deployment and upscaling of electrolysers and to forge partnerships at the EU level to ensure their cost-effectiveness.

[Particularly], recognises that there will be different forms of hydrogen on the market, such as renewable and low-carbon hydrogen, and underlines the need for investment to scale up renewable production […] while recognising low-carbon hydrogen as a bridging technology in the short and medium term.

[The Parliament also] calls on the Commission to assess approximately how much low-carbon hydrogen will be needed for decarbonisation purposes until renewable hydrogen can play this role alone.

[That being said, the Parliament] stresses the importance of phasing out fossil-based hydrogen as soon as possible [and] urges the Commission and the Member States to […] start planning that transition […] so that the production of fossil-based hydrogen starts decreasing swiftly, predictably and irreversibly.

[It also] highlights that effective support measures should be directed at the decarbonisation of existing fossil-based hydrogen production [and] urges that measures aimed at the development of the European hydrogen economy should not lead to the closure of the fossil-based hydrogen production sites, but to their modernisation and further development.

Underlines the role that environmentally safe carbon capture storage and utilisation (CCS/U) can play in reaching the European Green Deal objectives and supports an integrated policy context to stimulate the uptake of environmentally safe CCS/U applications […] in order to make heavy industry climate-neutral where no direct emission reduction options are available, noting the need for research and development in CCS/U technologies.

Underlines that a hydrogen economy requires significant additional amounts of affordable renewable energy and the corresponding infrastructure for […] [its] production […] and its transport to hydrogen production sites and […] to the end users; [also] calls on the Commission and the Member States to start the roll-out of sufficient supplementary renewable energy capacity to supply the electrification process and the production of renewable hydrogen.

[It also] considers that the deployment of appropriate renewable energy capacity in proportion to the need for renewable hydrogen can help to avoid conflict between the capacity required for electrification, electrolysers and other purposes and the need to meet the EU’s climate goals; welcomes, in that regard, the Commission’s plans to increase EU renewable energy target for 2030 and its proposed strategy on offshore renewable energy.

[Moreover, it stresses that] renewable hydrogen can be produced from several renewable energy sources such as wind, solar and hydropower, [and that…brownfields have potential…] to provide space for renewable energy production; [also, it] invites the Commission […] to assess how offshore renewable energy sources could pave the way for the wide development and uptake of renewable hydrogen.

- Offshore wind technology, with bottom-fixed wind turbines;

- Floating offshore wind technology;

- Tidal energy technology;

- Wave energy technology;

- Algal biofuels technology;

- Ocean thermal energy conversion technology;

- Floating photovoltaic technology.

Calls for the revision of the Energy Taxation Directive; calls on Member States to consider reducing taxes and levies on renewable energy across the EU […] to eliminate double-charging of taxes and fees on electricity generated from hydrogen facilities […] and to strengthen financial incentives to produce renewable energy, while simultaneously further working towards the phase-out of fossil fuel subsidies, tax and levy exemptions.

- A new tax rate structure is established using the energy content and environmental performance of the electricity fuels as the criteria, not the volume. The most environmentally damaging fuels sustain the highest minimum rates.

- The minimum rates are to be adapted annually to reflect the most recent prices.

- The taxable base is being extended; more products are included, and some of the exemptions and rate reductions are removed.

- Kerosene and heavy oil used for air and maritime transport within the EU are no longer exempt from energy taxation.

The transition to a climate-neutral energy system should be planned carefully, taking into account […] starting points and infrastructure, which may differ across the Member States […]. The Member States should be flexible when designing […] State aid measures, for the development of their national hydrogen economies; also asks the Commission […] to provide more information on planned differentiation and the flexibility of support measures.

Underlines the significant amount of natural resources, such as water, needed for hydrogen production and the problems this may cause for water-scarce regions in the EU; stresses the importance of increasing resource efficiency, minimising the impact on regional water supplies, ensuring the careful management of resources and land use for the production of hydrogen and avoiding any contamination of water, air or soil, deforestation or loss of biodiversity, as a result of the hydrogen-related production chain.

3.1.4. Citizen Engagement

[It] will play an important role in the implementation of […] [the] energy transition [and that it is important to ensure] that all stakeholders share the costs and benefits in an integrated system.

[It also states] that renewable energy communities can be involved in the production of hydrogen and recalls the obligation to provide them with an enabling framework in accordance with Directive (EU) 2019/944 and requests that they benefit from the same advantages as other stakeholders.

[Afterwards, the Parliament] stresses that in order to have a properly functioning EU hydrogen market, people with specialised skills are needed, especially with regard to safety and underlines the necessity of a […] training system; calls on the Commission to adopt an action plan aimed at guiding Member States to develop […] training programmes for workers, engineers, technicians and the general public, and to create multi-disciplinary teaching programmes for economists, scientists and students […] [also] calls for the launch of an EU initiative focused on employment, training and development for women.

[It also] stresses the importance of preserving and tapping into the potential of workers with technical skills employed in existing industries, and recalls the right of workers to be trained and upskilled during working hours with their wages guaranteed.

Calls on the Commission to produce data on the possible impacts, opportunities and challenges […] in relation to the scaling-up of hydrogen […] [and] suggests the launch of an EU skills partnership on hydrogen under the Pact for Skills.

3.1.5. Hydrogen Infrastructure

Emphasises the urgent need to develop infrastructure for hydrogen production, storage and transport, to incentivise adequate capacity-building, and to develop demand and supply in parallel […] [also] notes the […] benefits of combining hydrogen production and infrastructure with other aspects of flexible, multi-energy systems such as waste heat recovery from electrolysis for district heating.

Welcomes the Commission’s proposal to amend the TEN-E Regulation and appreciates the inclusion of hydrogen as a dedicated energy infrastructure category.

Notes that […] the planning, regulation and development of infrastructure for the transmission of hydrogen over longer distances and storage, as well as adequate financial support for that infrastructure, should already be being undertaken […] welcomes […] the future inclusion of hydrogen infrastructure in EU plans, such as the Ten-Year Network Development Plans.

[The Parliament also] notes that […] hydrogen assets may be newly constructed or converted from natural gas, or a combination of the two. [It] encourages the Commission and Member States to make a science-based assessment of the possibility of repurposing existing gas pipelines for the transport of pure hydrogen and the underground storage of hydrogen and it notes that repurposing…gas infrastructure…could maximise cost efficiency, minimise land and resource use and investment costs and minimise the social impact, [and could also] be relevant for the use of hydrogen in the priority sectors of emission-intensive industries […] calls on the Commission to assess where hydrogen blending is currently used […] with a view to identifying infrastructure needs.

Stresses the importance of […] integrated network planning with the guidance of public bodies like the European Union Agency for the Cooperation of Energy Regulators (ACER) and the participation of stakeholders and scientific bodies; suggests, in that regard, that cost-benefit calculations for the location of renewable hydrogen production, transport and storage infrastructure be made and that the need to build new ones be examined […] highlights the financial benefits of placing hydrogen production facilities close to renewable energy production sites or the same site as demand facilities.

Underlines the necessity of regulating hydrogen infrastructure and the need to uphold unbundling as a guiding principle for the design of hydrogen markets […] [since it] plays a key role in ensuring that innovative new products are put on the energy market in the most cost-efficient manner.

Stresses the strategically essential role of multimodal maritime and inland ports as innovation pools and hubs for the import, production, storage, supply and utilisation of hydrogen; underlines the need for space for and investment in port infrastructure.

3.1.6. Hydrogen Demand

Acknowledges that the focus on hydrogen demand should be on sectors for which the use of hydrogen is close to being competitive or that currently cannot be decarbonised using other technological solutions […] the main markets […] are industry, air, maritime and heavy-duty transport; believes that, for these sectors, roadmaps for demand development, investment and research needs should be established.

[Also] agrees with the Commission that demand-focused policies and clear incentives for the […] use of hydrogen […] in order to trigger the demand for hydrogen—such as quotas for the use of renewable hydrogen in a limited number of specific sectors, European Investment Bank guarantees to reduce the initial risk of co-investments until they are cost-competitive, and financial tools, including Carbon Contracts for Difference (CCfD) for projects using renewable or low-carbon hydrogen—could be considered.

[There is a] need to ensure that the compensation remains proportionate and to avoid the duplication of subsidies for both production and use, the creation of artificial needs and undue market distortions.

Urges the Commission to promote lead markets for renewable hydrogen technologies and their use for climate-neutral production—especially in the steel, cement and chemical industries—as part of the update and implementation of the New Industrial Strategy for Europe; calls on the Commission to assess the option of recognising steel produced with renewable hydrogen as a positive contribution to meeting fleet-wide CO2 emission reduction targets; further urges the Commission to soon come forward with an EU strategy for clean steel.

Recalls that the transport sector is responsible for a quarter of CO2 emissions in the EU […] and underlines the potential of hydrogen to be one of the instruments used to reduce CO2 emissions in transport modes, in particular where full electrification is more difficult or not yet possible.

[Also] underlines […] the importance of revising the TEN-T (trans-European transport network) Regulation and the Alternative Fuels Infrastructure Directive to ensure the availability of publicly accessible hydrogen refuelling stations […] [and] welcomes the Commission’s intention to develop hydrogen refuelling infrastructure under the Sustainable and Smart Mobility Strategy.

[Moreover, the Parliament] underlines that hydrogen’s characteristics make it a good candidate to replace fossil fuels […] [and] stresses that the use of hydrogen in its pure form or as a synthetic fuel or biokerosene is a key factor in the substitution of fossil kerosene for aviation […] stresses that stronger legislation is needed to incentivise the use of zero-emission fuels.

[Finally], calls on the Commission to increase research and investment within the framework of the Sustainable and Smart Mobility Strategy.

3.1.7. Research, Development, Innovation, and Financing

Stresses the importance of research, development and innovation along the whole value chain and of carrying out demonstration projects […] including pilot projects […] in making renewable hydrogen competitive and affordable.

Calls on the Commission to stimulate research and innovation efforts relating to the implementation of large-scale high-impact projects.

Underlines that significant amounts of money need to be invested to develop and increase the production capacity of renewable hydrogen […] which would also require de-risking renewable hydrogen investments, for example through Contracts for Difference.

Calls on the Commission to develop a […] renewable energy and hydrogen investment strategy aligned with national research and innovation strategies.

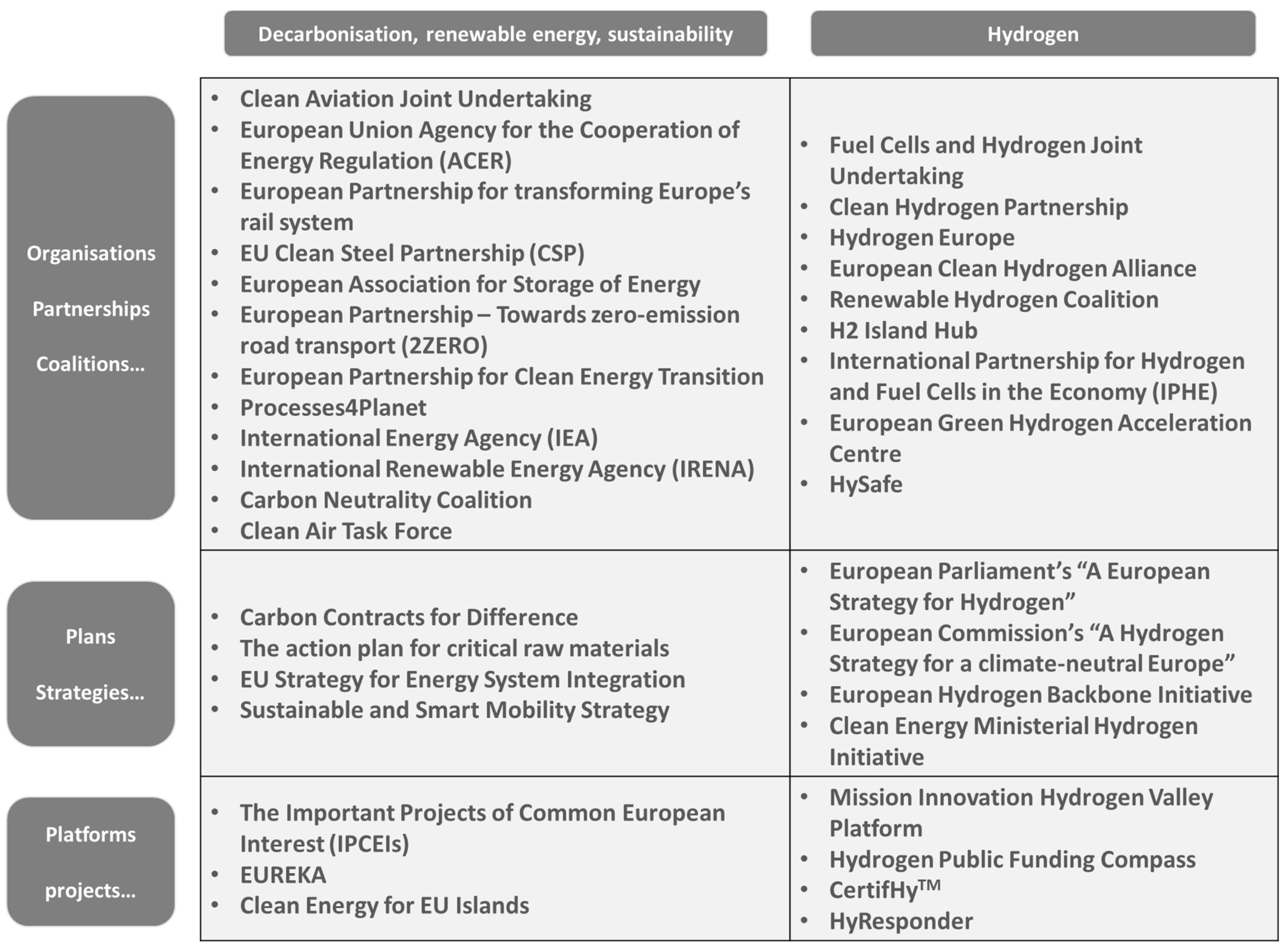

Welcomes the European Clean Hydrogen Alliance [and] the important projects of common European interest (IPCEI) amongst other renewable hydrogen initiatives. [Also] encourages the Alliance to come up, in cooperation with […] FCH JU, with an investment agenda and a project pipeline.

Welcomes the renewal of the FCH JU under Horizon Europe; stresses the importance of its work and asks the Commission to use it as a competence centre for hydrogen and provide it with sufficient financial resources […] [also] calls on the Commission to make use of the experience gained through the FCH JU and to incentivise further research into fuel cell and hydrogen energy technologies.

Believes that EU research and development efforts should focus on a wide range of potential new renewable hydrogen sources and technologies, such as hydrogen from photosynthesis, algae or electrolysers with sea water.

- Encompass large-scale demonstration projects.

- Cover new renewable hydrogen production technologies.

- Support every renewable energy technology and source since the production of renewable hydrogen requires renewable energy in large quantities and low prices.

- Encourage investments to develop projects with large-scale integrated hydrogen value chains.

- Stimulate the development of safe hydrogen infrastructure.

- Devise solutions for hard to abate transport sectors (aviation, train, heavy-duty vehicles, maritime).

- Encourage circularity of hydrogen equipment.

- Address the impact of hydrogen technology (environmentally, socially, economically).

- Reduce the consumption of critical raw materials.

- Enhance safety and public acceptance of the hydrogen technologies.

[Enumerates some EU] financing instruments [and] programmes [that] have a key role [in the] development of a hydrogen economy across the EU, [such as:] the Recovery and Resilience Facility, Horizon Europe, the Connecting Europe Facility, InvestEU […], the European Regional Development Fund, the Cohesion Fund, the Just Transition Fund and the ETS Innovation Fund.

[Also] stresses the need to make sure there are synergies between […] investment funds, programmes and financial instruments.

- 2ZERO;

- European Partnership on zero-emission waterborne transport;

- European Partnership for transforming Europe’s rail system;

- European Partnership for Clean Aviation;

- Processes4Planet;

- European Partnership for Clean Steel;

- European Partnership for Clean Energy Transition.

The inclusion of hydrogen deployment in the general objectives of the Partnership for Research and Innovation in the Mediterranean Area (PRIMA) […] in order to strengthen research and innovation capacities and to develop […] innovative solutions across the Mediterranean region.

3.1.8. International Cooperation on Hydrogen

It is emphasised that the EU’s leading role in the production of hydrogen technologies presents an opportunity to promote EU industrial leadership and innovation on a global level while reinforcing the EU’s role as a global climate leader; underlines […] the goal of increasing domestic hydrogen production, while acknowledging that Member States may also […] explore the possibility of importing energy or hydrogen.

Moreover, the Parliament calls […] on the Commission and the Member States to engage in an open and constructive dialogue in order to establish […] cooperation and partnerships with neighbouring regions, such as North Africa, the Middle East and the Eastern Partnership countries […] underlines that this cooperation would be beneficial for creating clean and new technology markets […], enhancing the transition to renewable energy and achieving the UN Sustainable Development Goals

[Furthermore, the Parliament] emphasises international cooperation on hydrogen with non-EU countries, in particular with the UK, the European Economic Area, the Energy Community and the US […] in order to strengthen the internal market and energy security; stresses that cooperation should be avoided with non-EU countries that are subject to EU restrictive measures […] and with those that do not guarantee compliance with safety, environmental standards and transparency requirements.

[Finally,] considers that hydrogen should become an element of the EU’s international cooperation, inter alia within the framework of the International Renewable Energy Agency’s (IRENA’s) work […] and the European Neighbourhood Policy.

The EU should promote its hydrogen standards and sustainability criteria internationally; [the Parliament also] calls […] for the development of international standards and the setting up of common definitions and methodologies for defining overall emissions from each unit of hydrogen produced, as well as international sustainability criteria as a prerequisite for […] imports.

[Moreover,] encourages the Commission to promote the role of the euro as the reference currency in the international trade of hydrogen.

3.1.9. The Role of Hydrogen in an Integrated Energy System

Underlines the need for an integrated energy system in order to achieve climate neutrality by 2050 […] and reach the goals of the Paris Agreement; welcomes in that regard the inclusion of hydrogen in the Commission’s Strategy for Energy System Integration […] considers that more emphasis needs to be placed on innovative projects combining the production and recovery of electricity, hydrogen and heat.

Notes that the development of the hydrogen economy can contribute to reducing imbalances in the energy system […] [since] hydrogen can play a key role in terms of storing energy to compensate for fluctuations in renewable energy supply and demand.

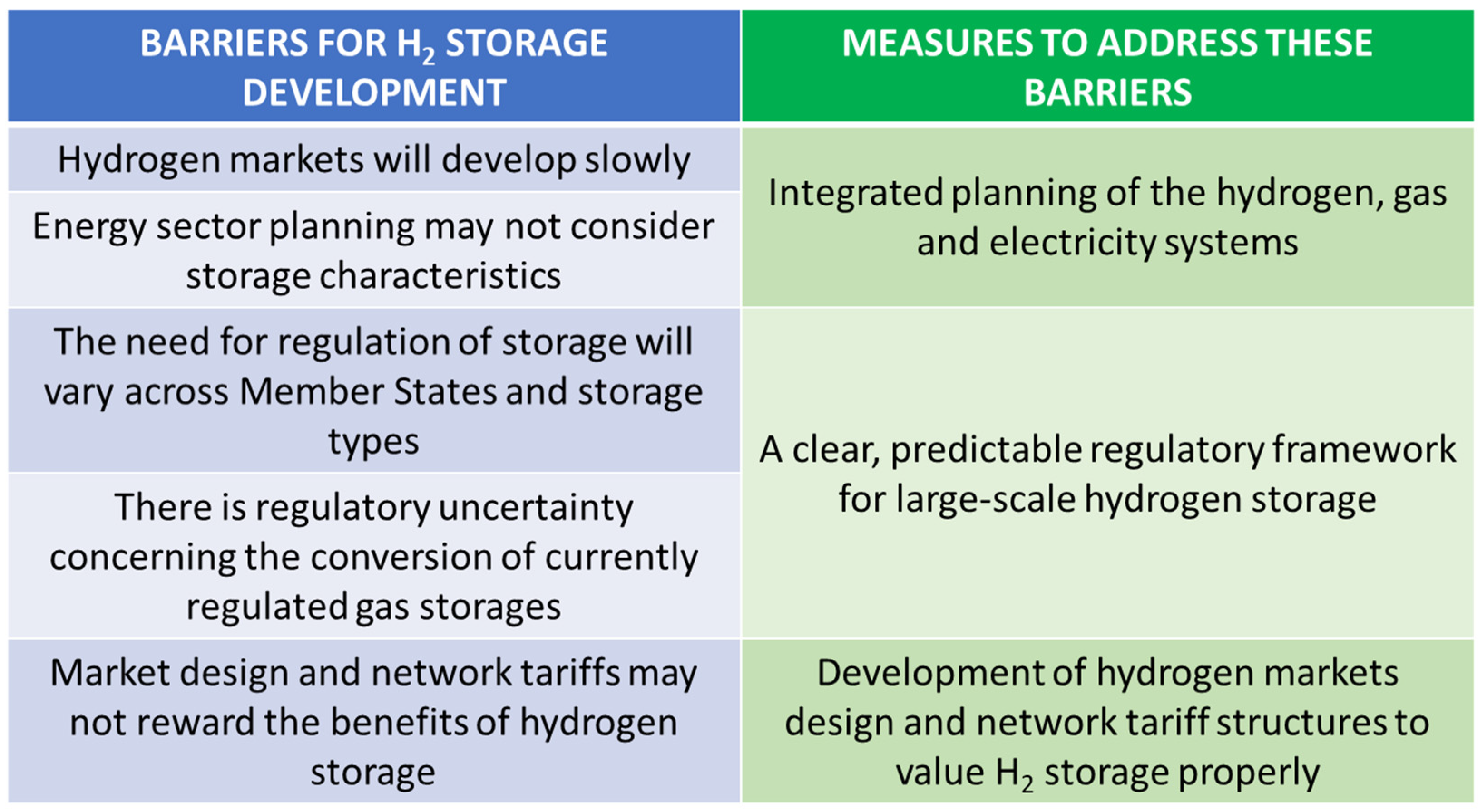

Highlights that an ambitious and timely strategy for energy storage through the use of hydrogen is required; notes, however, that the use of hydrogen for energy storage is not competitive yet.

Underlines […] the need to bring down costs for renewable hydrogen production […] therefore encourages the Commission to analyse options and capacities for hydrogen storage.

- Security of supply, since having hydrogen stored allows for its use whenever needed.

- Enabling system flexibility; the H2 storage can help maintain the stability of the network, can serve as a buffer in response to supply and demand variations, and can help to meet extreme or peak demands.

- Optimal development of infrastructure.

- For electrolyser operators, storage enables the decoupling of production and consumption times.

- For H2 consumers, the stability provided by storage can prevent price fluctuations, and can also contribute to the deployment of end uses affected by variations of demand.

3.2. Precedents

- The European Parliament’s resolution on a comprehensive European approach to energy storage (10 July 2020).

- The European Parliament’s resolution on the revision of the guidelines for trans-European energy infrastructure (10 July 2020).

- The European Commission’s communication “Stepping up Europe’s 2030 climate ambition—Investing in a climate-neutral future for the benefit of our people” (17 September 2020).

- The European Commission’s report “2020 report on the State of the Energy Union pursuant to Regulation (EU) 2018/1999 on Governance of the Energy Union and Climate Action” (14 October 2020).

- The European Commission’s communication on an EU strategy to reduce methane emissions (14 October 2020).

- The European Commission’s Pact for Skills (10 November 2020).

- The European Commission’s communication on an EU strategy to harness the potential of offshore renewable energy (19 November 2020).

- The UN Environment Programme’s Emissions Gap Report 2020 (9 December 2020).

- The European Commission’s communication “Sustainable and Smart Mobility Strategy—putting European transport on track for the future” (9 December 2020).

- IRENA’s report “Green hydrogen cost reduction—scaling up electrolysers to meet the 1.5 °C climate goal” (December 2020).

- The European Commission’s adoption of the proposal to revise the regulation on trans-European networks in energy (TEN-E) (15 December 2020).

- The European Commission’s communication “Updating the 2020 New Industrial Strategy: Building a stronger Single Market for Europe’s recovery” (5 May 2021).

4. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| CCS/U | Carbon capture storage and utilisation |

| CHP | Combined heat and power |

| CO2 | Carbon dioxide |

| CRM | Critical raw material |

| DOE | Department Of Energy (US Department of Energy) |

| EEA | European economic area |

| EU | European Union |

| EUR | Euro |

| FC | Fuel cell |

| FCEV | Fuel cell electric vehicle |

| GHG | Greenhouse gas |

| GNI | Gross national income |

| GO | Guarantee of origin |

| HRS | Hydrogen refuelling station |

| H2 | Hydrogen |

| IEA | International Energy Agency |

| LWH | Lower heating value |

| LNG | Liquid/liquefied natural gas |

| LPG | Liquefied petroleum fas |

| MJ | Megajoule |

| NH3 | Ammonia |

| PEM | Polymer electrolyte membrane |

| PGM | Platinum group metal |

| PV | Photovoltaic |

| RES | Renewable energy source |

| SME | Small- and medium-sized enterprise |

| SOFC | Solid oxide fuel cell |

| TJ | Terajoule |

| UK | United Kingdom |

| UN | United Nations |

| US | United States |

| USD | United States dollar |

References

- Hassan, Q.; Abdulateef, A.M.; Hafedh, S.A.; Al-samari, A.; Abdulateef, J.; Sameen, A.Z.; Jaszczur, M. Renewable energy-to-green hydrogen: A review of main resources routes, processes and evaluation. Int. J. Hydrogen Energy 2023, in press. [Google Scholar]

- Falcone, P.M.; Hiete, M.; Sapio, A. Hydrogen economy and sustainable development goals: Review and policy insights. Curr. Opin. Green Sustain. Chem. 2021, 31, 100506. [Google Scholar] [CrossRef]

- Nazir, H.; Louis, C.; Jose, S.; Prakash, J.; Muthuswamy, N.; Buan, M.E.; Flox, C.; Chavan, S.; Shi, X.; Kauranen, P.; et al. Is the H2 economy realizable in the foreseeable future? Part I: H2 production methods. Int. J. Hydrogen Energy 2020, 45, 13777–13788. [Google Scholar] [CrossRef]

- Younas, M.; Shafique, S.; Hafeez, A.; Javed, F.; Rehman, F. An Overview of Hydrogen Production: Current Status, Potential, and Challenges. Fuel 2022, 316, 123317, ISSN 0016-2361. [Google Scholar] [CrossRef]

- Nazir, H.; Muthuswamy, N.; Louis, C.; Jose, S.; Prakash, J.; Buan, M.E.; Flox, C.; Chavan, S.; Shi, X.; Kauranen, P.; et al. Is the H2 economy realizable in the foreseeable future? Part II: H2 storage, transportation, and distribution. Int. J. Hydrogen Energy 2020, 45, 20693–20708. [Google Scholar] [CrossRef]

- Langmi, H.W.; Engelbrecht, N.; Modisha, P.M.; Bessarabov, D. Chapter 13—Hydrogen Storage. In Electrochemical Power Sources: Fundamentals, Systems, and Applications; Smolinka, T., Garche, J., Eds.; Elsevier: Amsterdam, The Netherlands, 2022; pp. 455–486. ISBN 9780128194249. [Google Scholar]

- Nazir, H.; Muthuswamy, N.; Louis, C.; Jose, S.; Prakash, J.; Buan, M.E.; Flox, C.; Chavan, S.; Shi, X.; Kauranen, P.; et al. Is the H2 economy realizable in the foreseeable future? Part III: H2 usage technologies, applications, and challenges and opportunities. Int. J. Hydrogen Energy 2020, 45, 28217–28239. [Google Scholar] [CrossRef] [PubMed]

- European Parliament. TA-9-2021-0241_EN: European Parliament Resolution of 19 May 2021 on a European Strategy for Hydrogen. Available online: https://www.europarl.europa.eu/doceo/document/TA-9-2021-0241_EN.html (accessed on 15 February 2022).

- United Nations Framework Convention on Climate Change. Key Aspects of the Paris Agreement. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement/key-aspects-of-the-paris-agreement#:~:text=The%20Paris%20Agreement%27s%20central%20aim,further%20to%201.5%20degrees%20Celsius (accessed on 19 May 2022).

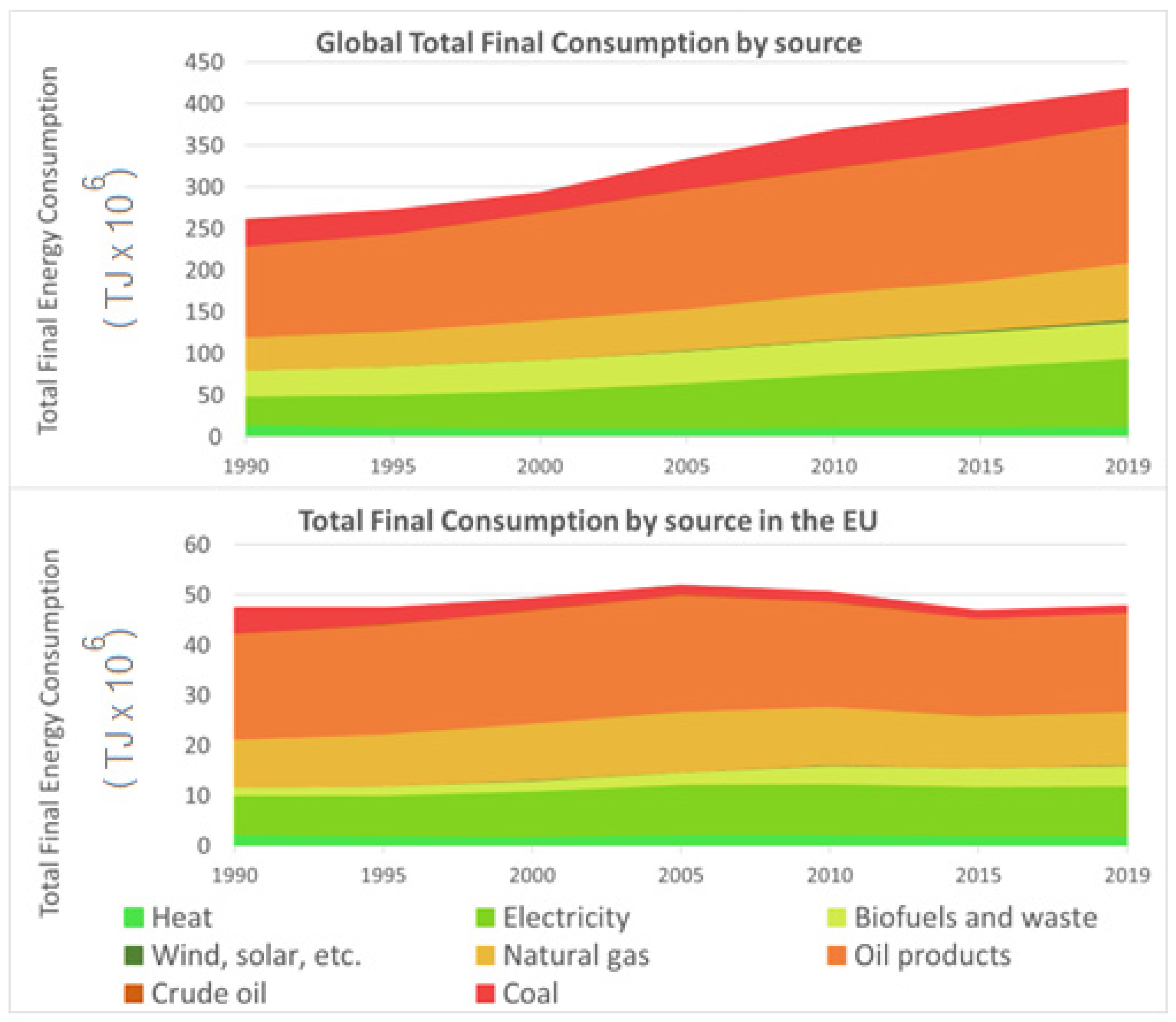

- International Energy Agency. Data and Statistics. Available online: https://www.iea.org/data-and-statistics/data-browser/?country=WORLD&fuel=Energy%20consumption&indicator=TFCbySource (accessed on 19 May 2022).

- International Energy Agency. Data and Statistics. Available online: https://www.iea.org/data-and-statistics/data-browser/?country=WEOEUR&fuel=Energy%20consumption&indicator=TFCbySource (accessed on 19 May 2022).

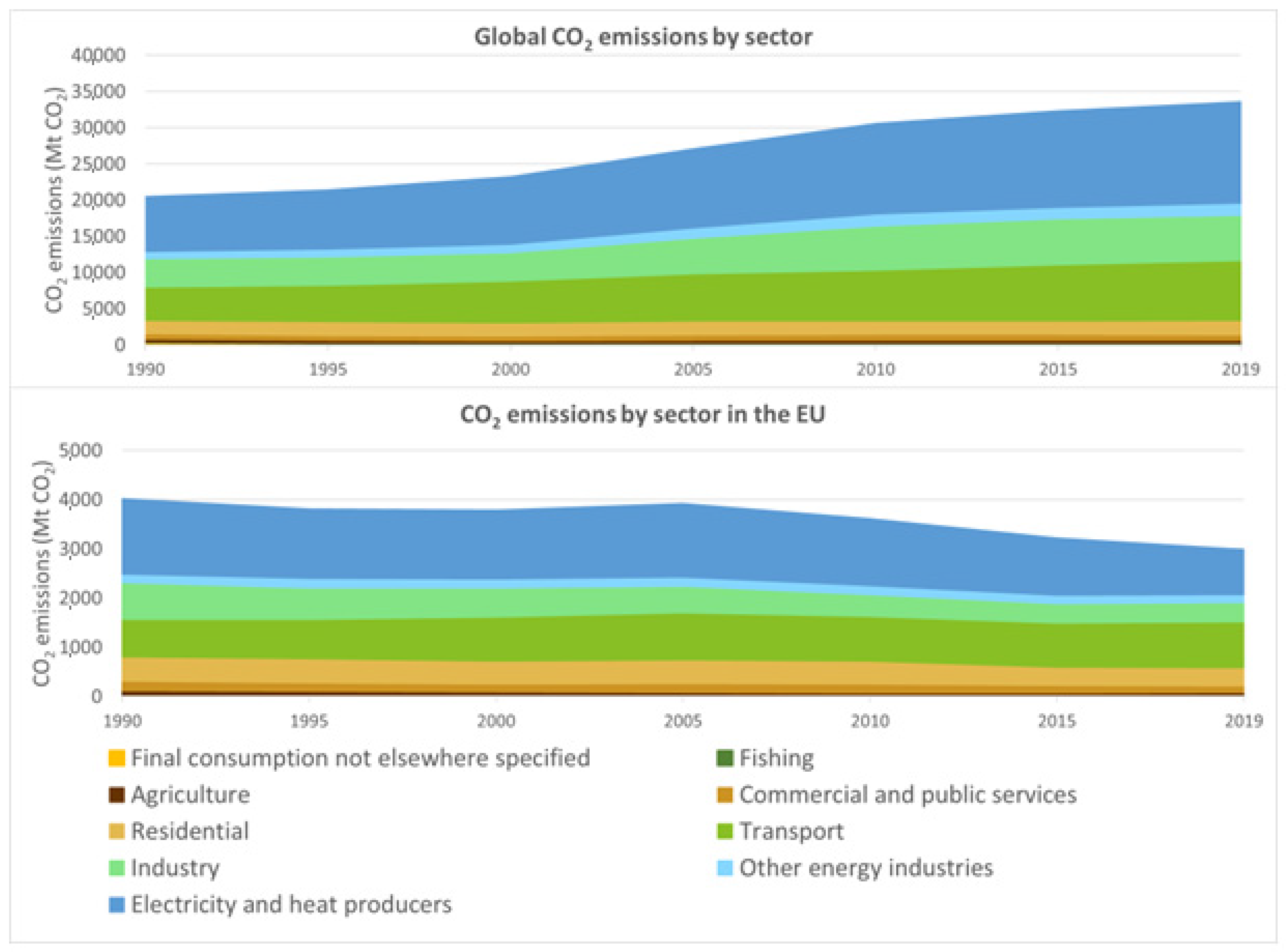

- International Energy Agency. Data and Statistics. Available online: https://www.iea.org/data-and-statistics/data-browser/?country=WORLD&fuel=CO2%20emissions&indicator=CO2BySector (accessed on 19 May 2022).

- International Energy Agency. Data and Statistics. Available online: https://www.iea.org/data-and-statistics/data-browser/?country=WEOEUR&fuel=CO2%20emissions&indicator=CO2BySector (accessed on 19 May 2022).

- European Commission. Home:Strategy:Priorities 2019–2024: A European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en (accessed on 7 June 2022).

- European Commission. Home: Strategy:Priorities 2019–2024: A European Green Deal: Delivering the European Green Deal. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/delivering-european-green-deal_en (accessed on 7 June 2022).

- European Commission. Home:Strategy:Priorities 2019–2024: A European Green Deal: REPowerEU: Affordable, Secure and Sustainable Energy for Europe. Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/repowereu-affordable-secure-and-sustainable-energy-europe_en (accessed on 18 June 2022).

- European Commission. REPowerEU: Joint European Action for More Affordable, Secure and Sustainable Energy. Available online: https://ec.europa.eu/commission/presscorner/detail/en/IP_22_1511 (accessed on 19 May 2022).

- United Nations. Department of Economic and Social Affairs, Sustainable Development, Sustainable Development Goals. Available online: https://sdgs.un.org/goals (accessed on 18 June 2022).

- European Commission. European Industrial Strategy. Available online: https://ec.europa.eu/growth/industry/strategy_en (accessed on 7 June 2022).

- Buttler, A.; Spliethoff, H. Current status of water electrolysis for energy storage, grid balancing and sector coupling via power-to-gas and power-to-liquids: A review. Renew. Sustain. Energy Rev. 2018, 82, 2440–2454. [Google Scholar] [CrossRef]

- International Renewable Energy Agency. Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- European Clean Hydrogen Alliance. European Electrolyser Summit: Joint Declaration. Available online: https://hydrogeneurope.eu/wp-content/uploads/2022/05/2022.05.05-EU-ELY-Summit_joint-declaration_signed-c70ff98b5001f55b76b50cf0221c895f.pdf (accessed on 7 June 2022).

- Fuel Cells and Hydrogen Joint Undertaking. Mission Innovation Hydrogen Valley Platform. Available online: https://www.h2v.eu/ (accessed on 7 June 2022).

- Fuel Cells and Hydrogen Joint Undertaking. Hydrogen Valleys: Insights into the Emerging Hydrogen Economies Around the World. Available online: https://www.fch.europa.eu/sites/default/files/documents/20210527_Hydrogen_Valleys_final_ONLINE.pdf (accessed on 18 June 2022).

- Fuel Cells and Hydrogen Joint Undertaking. Mission Innovation Hydrogen Valley Platform: HyWays for Future. Available online: https://www.h2v.eu/analysis/best-practices/hyways-future (accessed on 18 June 2022).

- HyNet North West. About: What Is HYNET? Available online: https://hynet.co.uk/about/ (accessed on 18 June 2022).

- Hydrogenious. Applications for a “Hydrogenated” World. Available online: https://www.hydrogenious.net/index.php/en/references/blue_danube/ (accessed on 7 June 2022).

- European Commission. A Hydrogen Strategy for a Climate-Neutral Europe. Available online: https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf (accessed on 7 June 2022).

- CertifHy. About Us: Our Mission and Vision. Available online: https://www.certifhy.eu/ (accessed on 18 June 2022).

- Babaei, R.; Ting, D.S.; Carriveau, R. Optimization of hydrogen-producing sustainable island microgrids. Int. J. Hydrogen Energy 2022, 47, 14375–14392. [Google Scholar] [CrossRef]

- European Environment Agency. Water Resources Across Europe—Confronting Water Stress: An Updated Assessment; Report; European Environment Agency: Copenhagen, Denmark, 2021.

- Böhm, H.; Moser, S.; Puschnigg, S.; Zauner, A. Power-to-hydrogen & district heating: Technology-based and infrastructure-oriented analysis of (future) sector coupling potentials. Int. J. Hydrogen Energy 2021, 46, 31938–31951. [Google Scholar]

- Schlund, D.; Schönfisch, M. Analysing the impact of a renewable hydrogen quota on the European electricity and natural gas markets. Appl. Energy 2021, 304, 117666, ISSN 0306-2619. [Google Scholar] [CrossRef]

- Toktarova, A.; Göransson, L.; Johnsson, F. Design of Clean Steel Production with Hydrogen: Impact of Electricity System Composition. Energies 2021, 14, 8349. [Google Scholar] [CrossRef]

- European Commission. Mobility and Transport: Trans-European Transport Network (TEN-T). Available online: https://transport.ec.europa.eu/transport-themes/infrastructure-and-investment/trans-european-transport-network-ten-t_en (accessed on 7 June 2022).

- European Commission. Questions and Answers: The Revision of the TEN-T Regulation. Available online: https://ec.europa.eu/commission/presscorner/detail/en/qanda_21_6725 (accessed on 7 June 2022).

- European Parliament. Briefing: Revision of the Trans-European Transport Network Guidelines. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2022/729314/EPRS_BRI(2022)729314_EN.pdf (accessed on 18 June 2022).

- European Commission. Commission Staff Working Document: Building a European Research Area for Clean Hydrogen—The Role of EU Research and Innovation Investments to Deliver on the EU’s Hydrogen Strategy. Available online: https://ec.europa.eu/info/sites/default/files/research_and_innovation/research_by_area/documents/ec_rtd_swd-era-clean-hydrogen.pdf (accessed on 18 June 2022).

- European Commission. EU Strategy on Energy System Integration. Available online: https://energy.ec.europa.eu/topics/energy-system-integration/eu-strategy-energy-system-integration_en (accessed on 18 June 2022).

- Energy Transition Expertise Centre. Report: The Role of Renewable H₂ Import & Storage to Scale Up the EU Deployment of Renewable H2. Available online: https://op.europa.eu/en/publication-detail/-/publication/7ab70e32-a5a0-11ec-83e1-01aa75ed71a1/language-en (accessed on 18 June 2022).

- European Commission. Study on the EU’s List of Critical Raw Materials; Final Report; Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs, Joint Research Centre Directorate GROW.C, JRC.D: Brussels, Belgium, 2020; ISBN 978-92-76-21049-8.

- International Energy Agency. World Energy Outlook 2022; IEA Publications: Paris, France, 2022. [Google Scholar]

- Lotrič, A.; Sekavčnik, M.; Kuštrin, I.; Mori, M. Life-cycle assessment of hydrogen technologies ith the focus on EU critical raw materials and end-of-life strategies. Int. J. Hydrogen Energy 2021, 46, 10143–10160. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vivanco-Martín, B.; Iranzo, A. Analysis of the European Strategy for Hydrogen: A Comprehensive Review. Energies 2023, 16, 3866. https://doi.org/10.3390/en16093866

Vivanco-Martín B, Iranzo A. Analysis of the European Strategy for Hydrogen: A Comprehensive Review. Energies. 2023; 16(9):3866. https://doi.org/10.3390/en16093866

Chicago/Turabian StyleVivanco-Martín, Begoña, and Alfredo Iranzo. 2023. "Analysis of the European Strategy for Hydrogen: A Comprehensive Review" Energies 16, no. 9: 3866. https://doi.org/10.3390/en16093866