A Sustainable Method for Evaluating the Activity of Logistics Service Providers (LSPs) in a Turbulent Environment—Case Study Analysis (2020–2021)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

Description of the Proposed Research Method

- It is based on known, and commonly used in other countries, measures of the economic evaluation of individual companies, as well as the measure of fleet assessment. These are the following measures:

- Profitability indicators (ROE, ROA, ROS, gross profit margin indicator, revenue dynamics indicator);

- Performance indicators (current assets turnover indicator, liabilities turnover indicator);

- Debt indicators (debt to equity ratio, total debt ratio);

- Liquidity indicators (quick ratio QR);

- Fleet emission index (the number of vehicles meeting the Euro 6 standard and higher in relation to the number of vehicles in the company’s fleet) [12].

- Economic measures are obtained in the same way in all countries, i.e., from published financial statements of companies or based on individual surveys.

- The evaluation measures have the same component parameters.

- The fractional measure (one of eleven) concerning the emissivity of the fleet is also a universal tool, because all LSP companies, regardless of the country of residence, must meet the requirements of the EU regulations on the emissivity of the fleet. Therefore, the evaluation of their resource potential based on the assessment of the emissivity of the fleet makes it possible to compare entities from different countries in a universal way.

- It includes a wide set of 10 economic evaluation indicators commonly used in the financial analysis of individual companies.

- Additionally, which is a novelty, it includes one fleet assessment measure, which is important in evaluating the resource potential of companies in the context of changes in the EU regulations in the field of emissions.

- It provides a better and more reliable evaluation than company rankings based, so far, on sets of 2–3 measures, eliminating the risk of randomness and selective assessments.

- It guarantees a balanced selection of assessment measures by prior checking the degree of correlation between them.

- Ensuring a variety of correlation coefficients in the set of 11 aggregate assessment measures ensures sufficient data comparability. The use of only highly correlated indicators leads to the duplication of information and excessive increase in its importance in the whole analysis, which is not taken into account by most of the authors of the rankings. Such errors occur in rankings, where the selection of the indicators is performed randomly, without examining the correlation between them.

- The compatibility of the segregating of companies was examined in the case of selecting indicators that were differently correlated (−0.2–1) and based on only highly correlated indicators (0.8–1). The results obtained allow us to conclude that limiting the number of indicators used to build a synthetic measure only to highly correlated indicators leads to the creation of a ranking of companies that shows a high randomness of their compilation in two consecutive years.

- The ranking based on a more diverse set of indicators in terms of the correlation showed a greater convergence in both years than the ranking based solely on indicators with a high correlation close to 1. This was particularly evident in the case of the top ten companies in the rankings and the use of indicators from the same group, i.e., profitability (ROE, ROA, ROS).

2. Emissivity of LSPs and the Method for Its Measurement

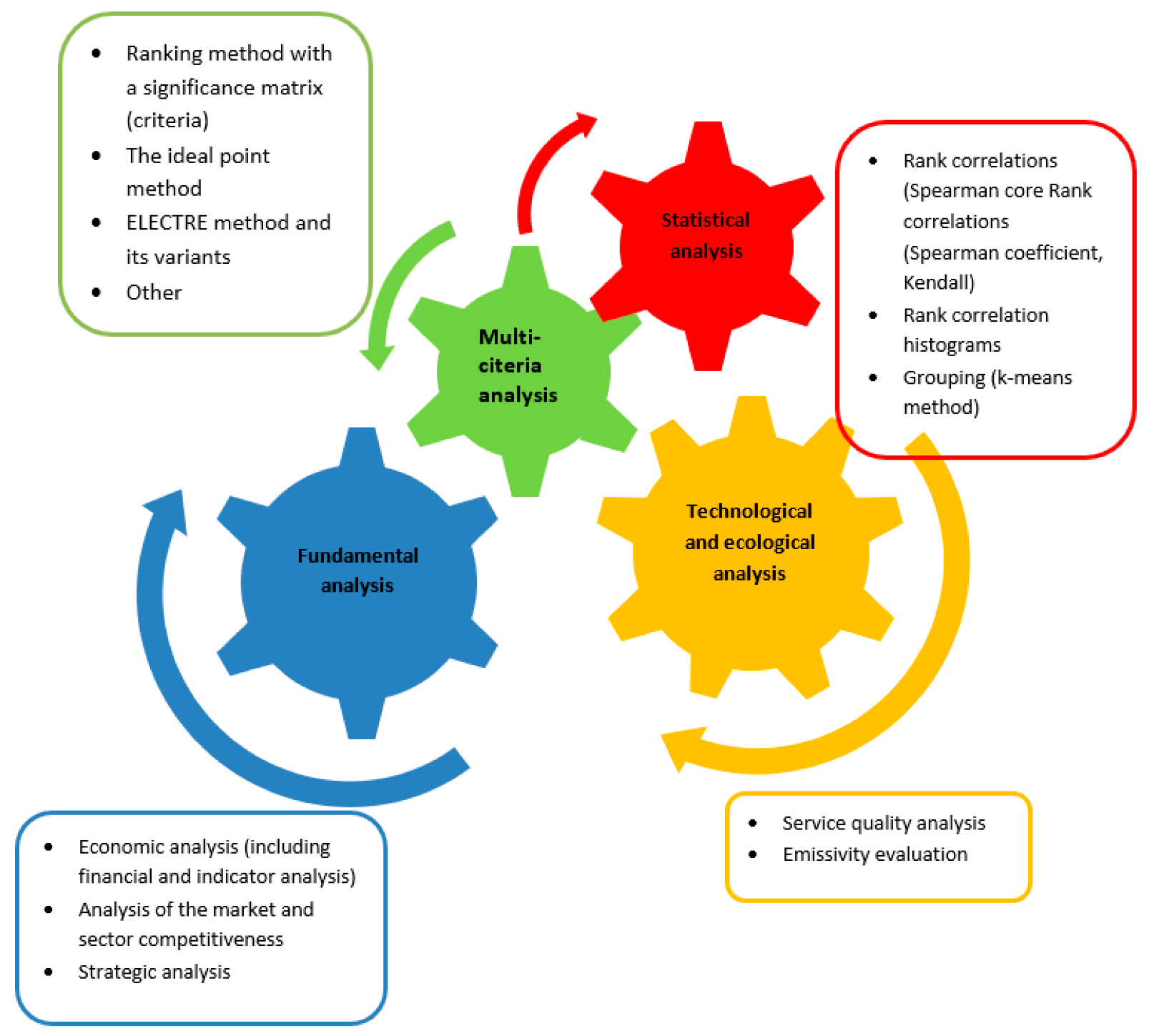

3. Methods Used in the Evaluation of LSPs

3.1. Multi-Criteria Analysis

3.2. Fundamental Analysis

3.3. Statistical Analysis of LSPs (Including Economic and Ecological Parameters)

4. An Example of Applying a Sustainable Method for Assessing LSPs

- A set of indicators for the comparative economic evaluation of LSP companies;

- Examining the degree of correlation of the economic indicators in order to ensure a reliable evaluation;

- Determining the fleet emission index and checking its correlation with the economic indicators;

- Changes in the rankings for 2020–2021 using different sets of indicators;

- Determining the method for the positioning of companies in the ranking;

- Determining the indicators for the aggregate evaluation of LSP sector companies based on the convergence of the rankings.

- The use of a set of partial indicators with diversified correlation results in a greater similarity of the rankings in successive years;

- The use of a set of indicators only from the same group (e.g., profitability) and with a high correlation (above 0.8) causes more randomness of the rankings in subsequent years;

- When selecting a set of partial indicators for the LSP ranking evaluation, care should be taken to select measures from various groups (profitability, operational efficiency, liquidity and debt) and to examine the correlation between them as well as selecting a set of indicators with a greater dispersion of the correlation coefficient value.

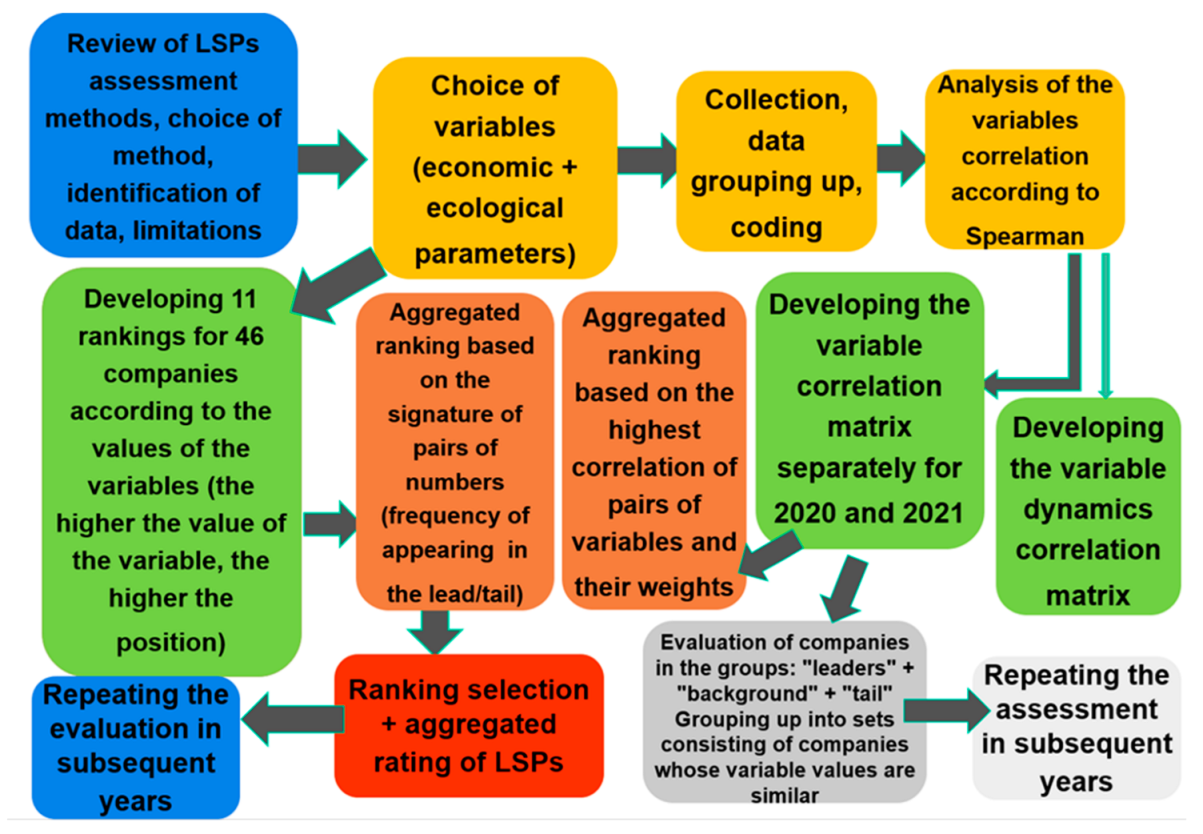

4.1. The Scheme and Stages of the Study

- Review of LSP assessment methods;

- Choice of partial characteristics (indicators);

- Data collection and grouping up of companies, coding;

- Analysis of the variable correlation;

- Developing the variable correlation matrix;

- Evaluation of companies in the subgroups (leaders, tail, background);

- Development of 11 partial rankings and aggregated one based on the characteristics of the two-number signatures of LSPs.

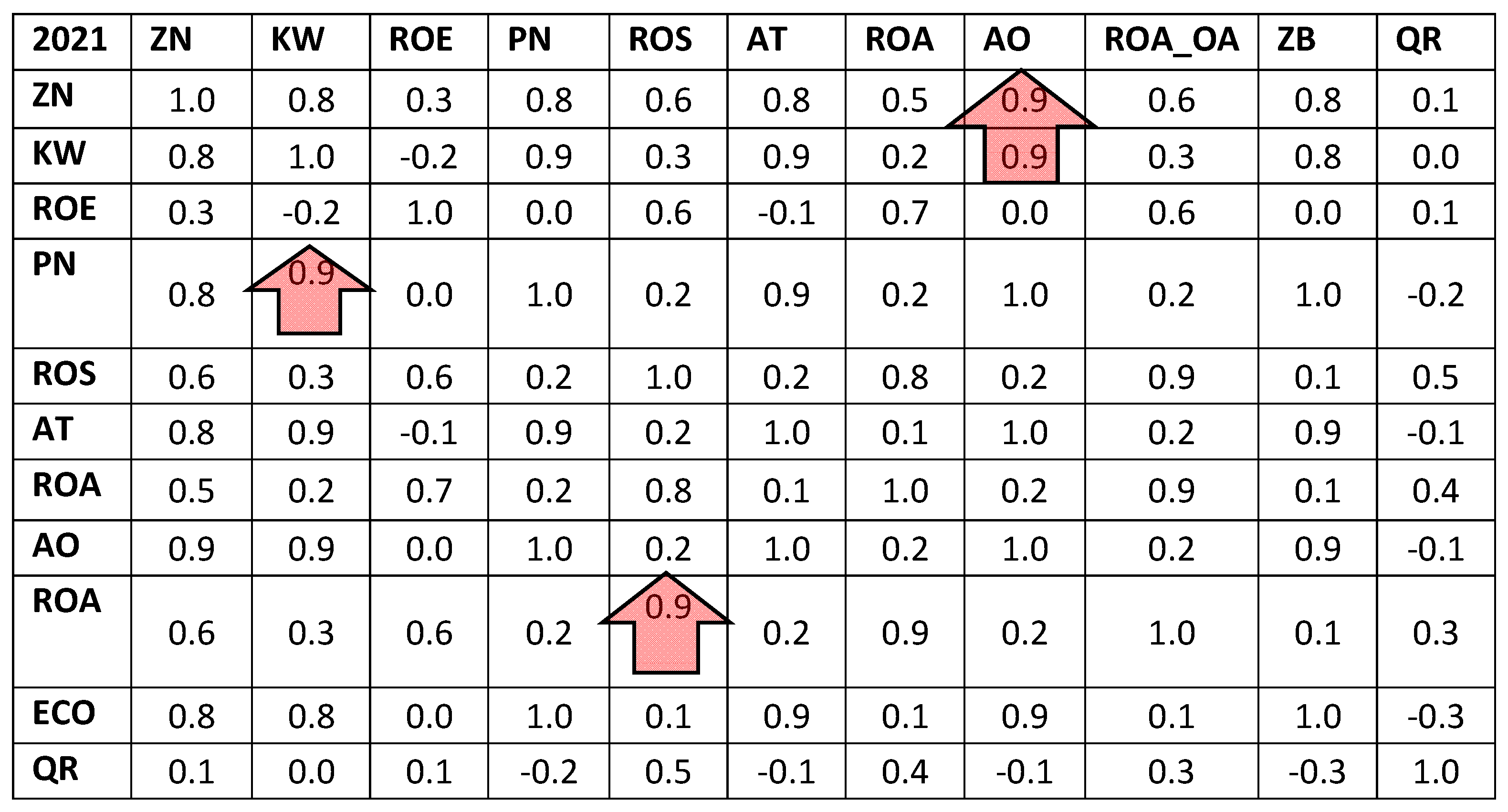

4.2. Characteristics Correlation

- Net profit and equity (0.9);

- Net profit and net revenues (0.8);

- Net profit and fixed assets (0.7–0.8).

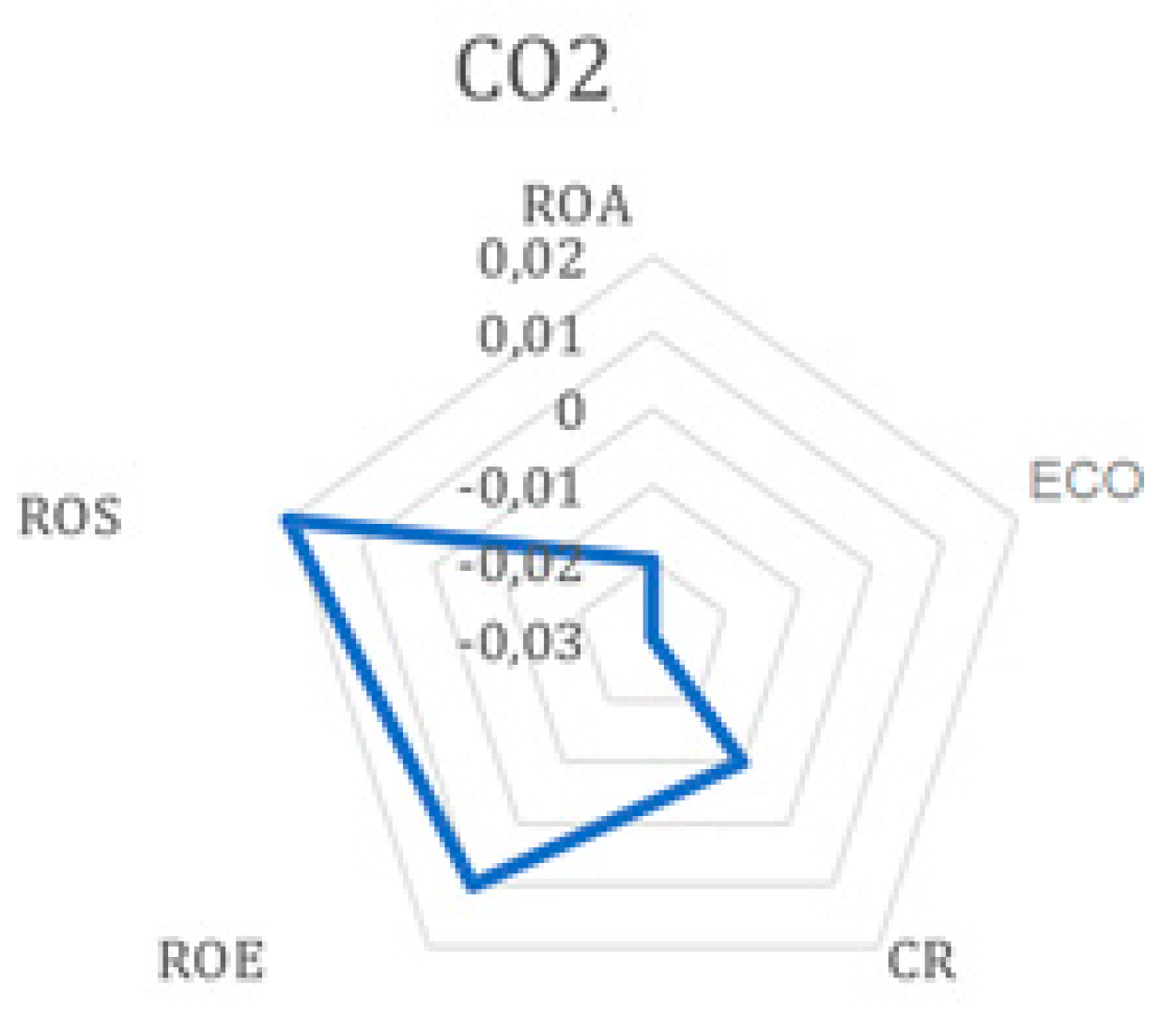

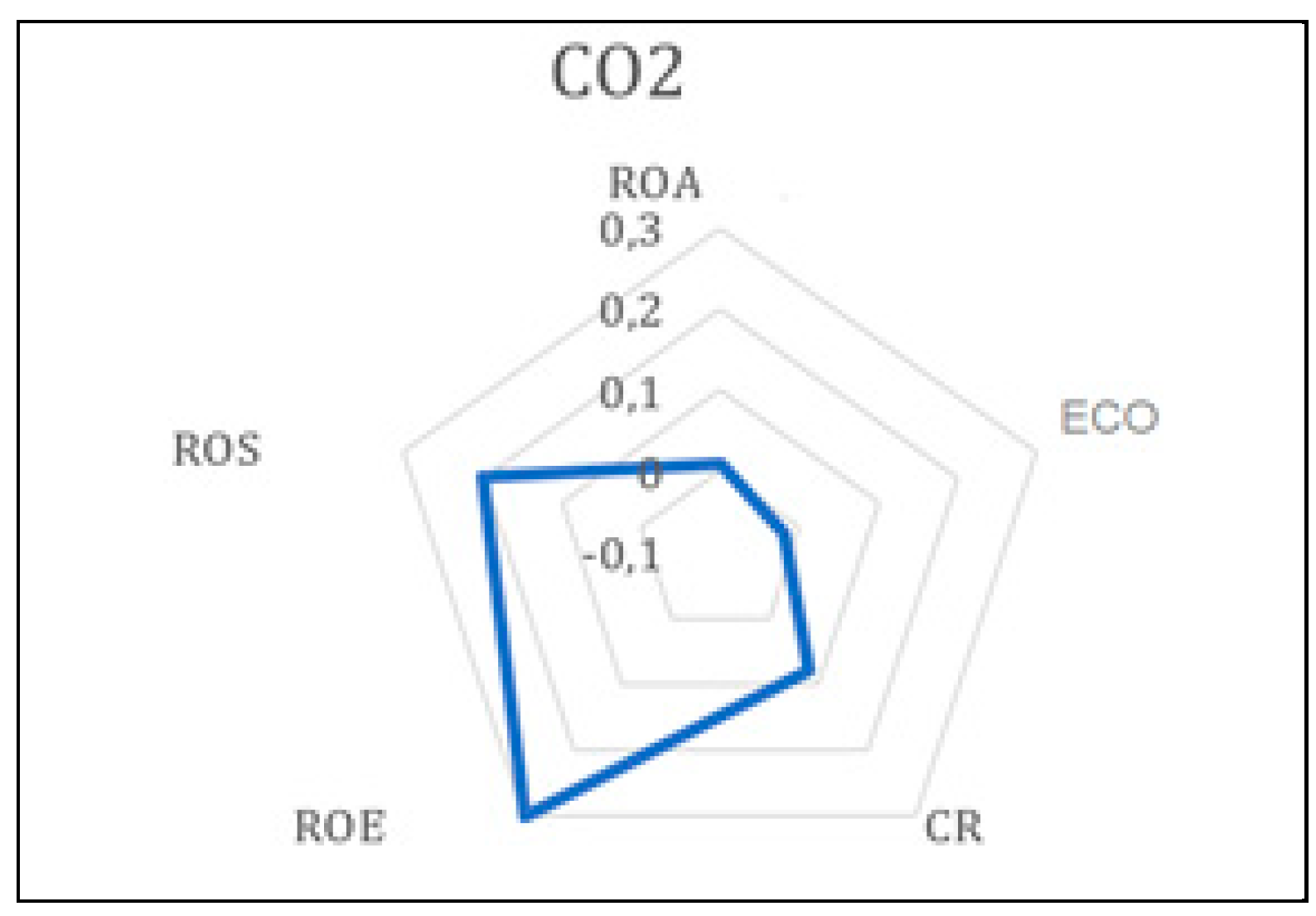

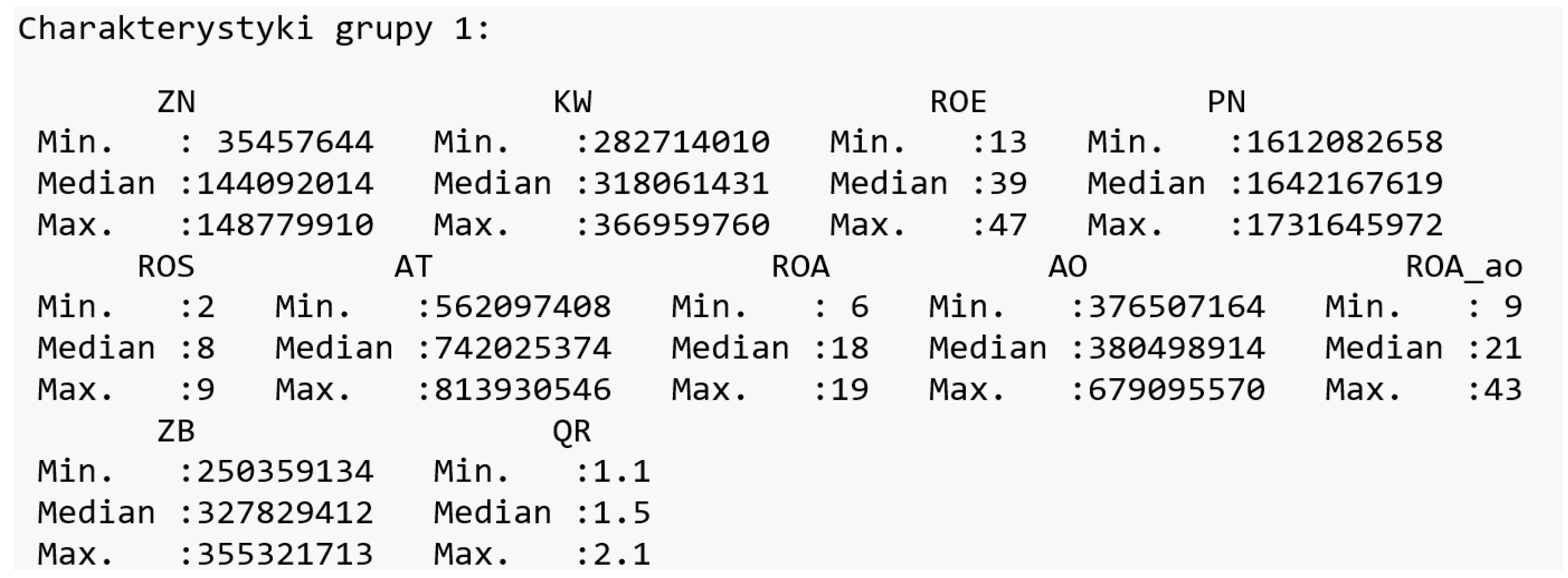

4.3. Grouping Up of the LSPs into Homogeneous Subsets

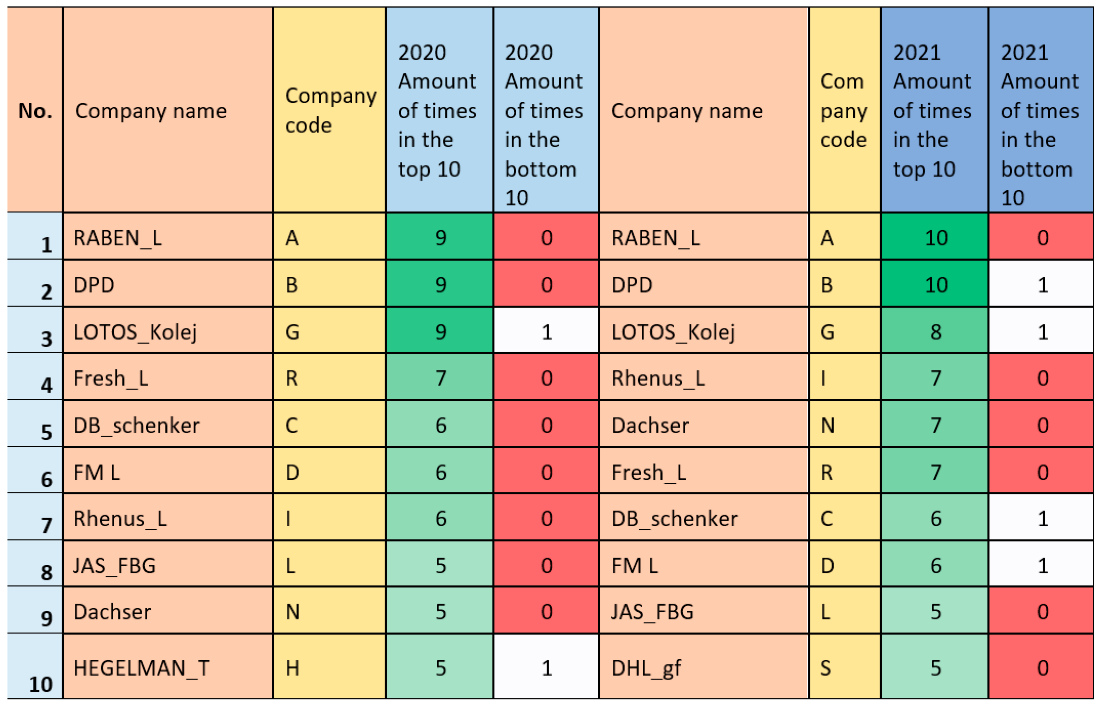

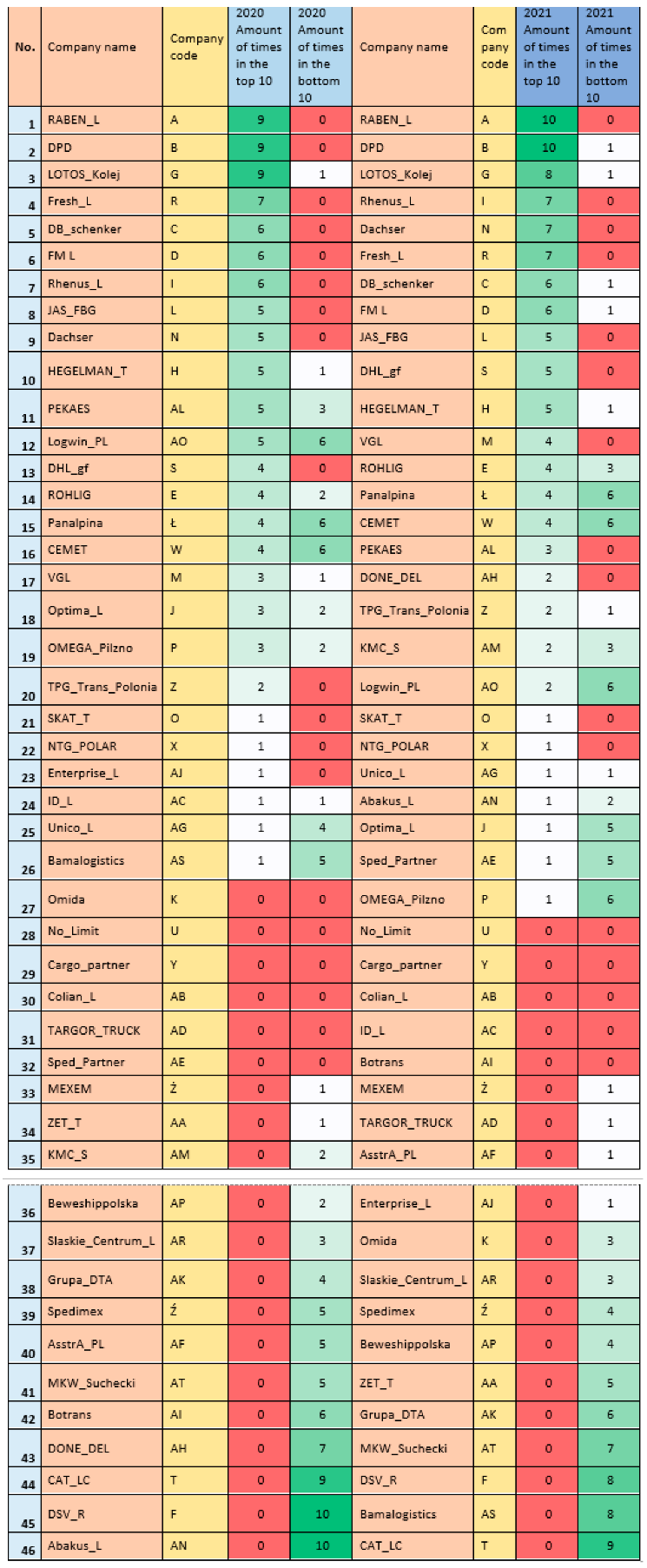

4.4. Signaturization of Companies and Development of a Collective LSP Ranking Up of the LSPs into Homogeneous Subsets

4.5. Conclusions Based on the Statistics

- Within each of the subgroups (profitability, efficiency, solvency, liquidity), the analyzed economic indicators were correlated with each other [41].

- Cases of correlating indicators belonging to different subgroups were less frequent.

- The thesis on the correlation between the financial condition indicators and the degree of application of pro-ecological solutions, in particular in the field of a low-emission fleet, has not been confirmed. Investments in this area are still characterized by a negligible nature, high randomness and the susceptibility of companies to short-term trends.

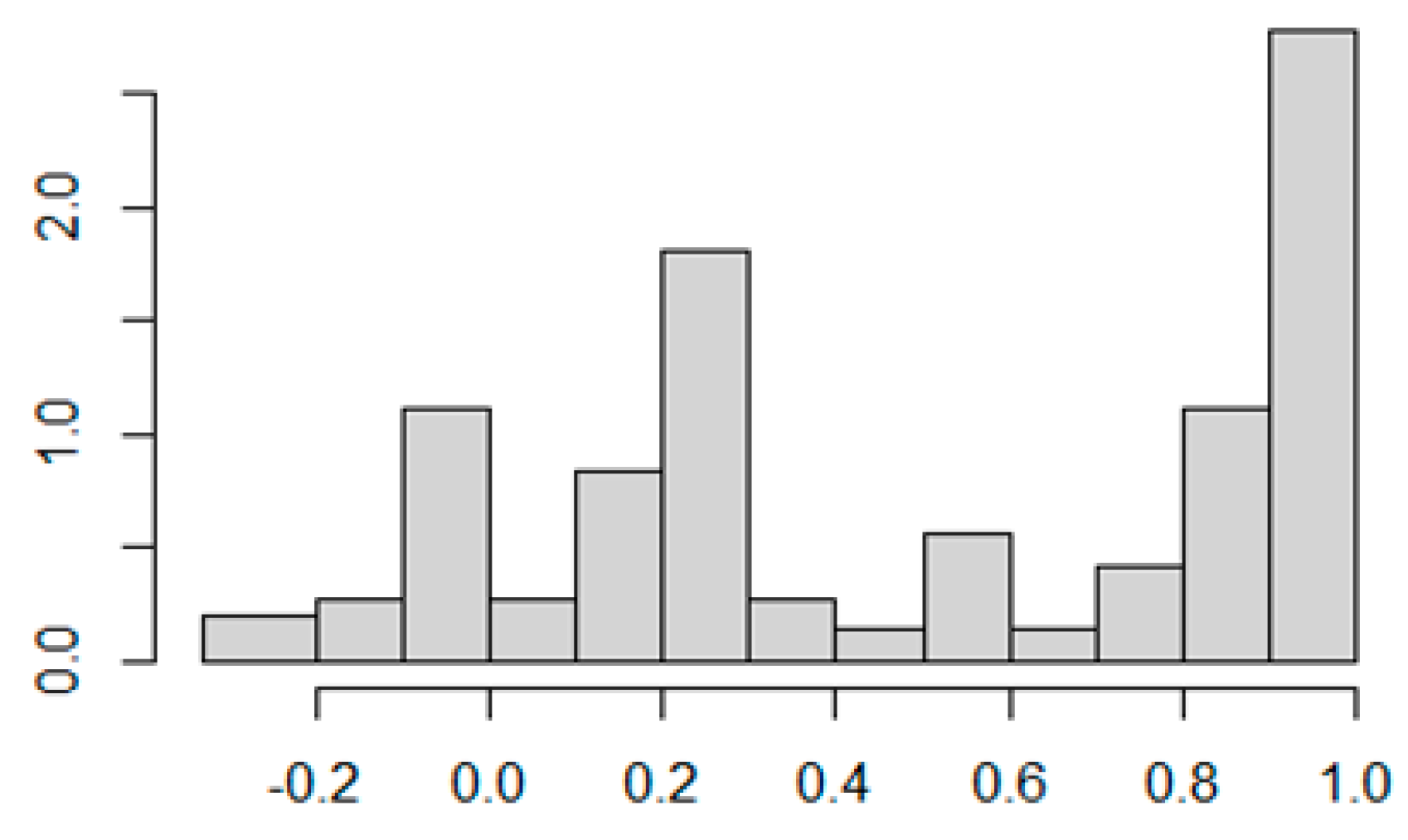

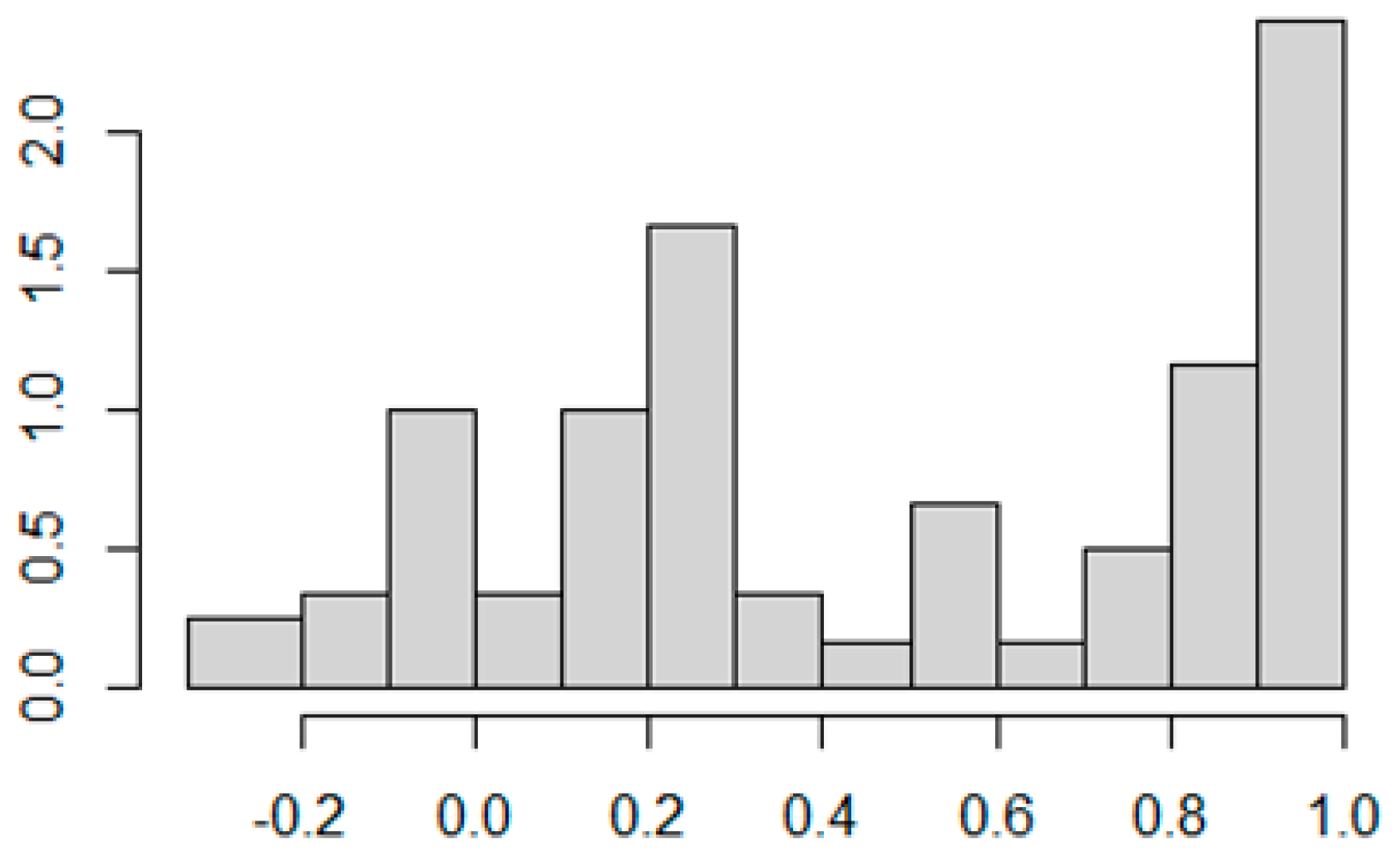

- Most of the variables were correlated at the level ≥ 0.6, slightly fewer at the level of 0.4, relatively few were correlated between 0.4–0.6. In both years, the relative positions (ranks) of the surveyed companies in the rankings, determined by the values of the adopted variables, did not change significantly. This allows to create only a simplified collective ranking based on two-number signatures obtained in a linear way, by counting the highest/lowest variables in the partial rankings

- The similarity of aggregated rankings for subsequent years was also confirmed by the Spearman’s rank correlation coefficient (r), assuming values in the range [−1.0–1.0]. The analysis prompted the conclusion that, in the analyzed years, the rankings of companies did not change significantly. However, if there was a need to develop an aggregated indicator based on partial indicators, then in the case of indicators characterized by a mutually high (above 0.85) correlation coefficient from the same group (e.g., regarding profitability, efficiency), it would be necessary to limit their number with the same simplified weighting factor. Another method that would not narrow down the set of partial indicators would be to assign weights lower than 1 (e.g., 0.5–0.8) for the indicators with mutually high correlation coefficients [17,39,41].

4.6. Economic Evaluation of the Studied Group of LSPs, Taking into Account the Leaders

5. Conclusions from the Research

6. Summary

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Available online: https://oees.pl/wp-content/uploads/2020/04/EKSPERTYZA-7-1.pdf (accessed on 10 July 2022).

- Brdulak, H.; Brdulak, A. Challenges and Threats Faced in 2020 by International Logistics Companies Operating on the Polish Market. Sustainability 2021, 13, 359. [Google Scholar] [CrossRef]

- Zysińska, M. Poradnik TSL. Gazeta Finansowa. 28 May—3 June 2021. Available online: https://gf24.pl/wp-content/uploads/2021/06/poradnik_TSL.pdf (accessed on 20 November 2022).

- Zysińska, M. Wyzwania firm TSL w dobie pandemii. Gazeta Finansowa, Biznes Raport, Poradnik TSL 2021. 17–23 June 2021. pp. 20–23. Available online: https://g.infor.pl/p/_files/37497000/1-tsl-ranking-27-06-2022-dobry-37496603.pdf (accessed on 20 November 2022).

- Available online: https://www.scopus.com/term/analyzer (accessed on 12 July 2022).

- Nascimentoa, C.; Belcavello, I.; Leise, R.; Oliveira, K. Characterization and analysis of the economic viability of cycle logistics transport in Brazil. Transp. Res. Procedia 2020, 46, 189–196. [Google Scholar] [CrossRef]

- Akhavana, M.; Ghiarab, H.; Mariottia, I.; Silligb, C. Logistics global network connectivity and its determinants. A European City network analysis. J. Transp. Geogr. 2020, 82, 102–624. [Google Scholar] [CrossRef]

- Barker, T.J.; Zabinsky, Z.B. A Multicriteria Decision Making Model for Reverse Logistics Using Analytical Hierarchy Process. Omega 2011, 39, 558–573. [Google Scholar] [CrossRef]

- Badassa, B.B.; Sun, B.; Qiao, L. Sustainable Transport Infrastructure and Economic Returns: A Bibliometric and Visualization Analysis. Sustainability 2020, 12, 2033. [Google Scholar] [CrossRef] [Green Version]

- Jacyna-Gołda, I.; Żak, J.; Gołębiowski, P. Models of traffic flow distribution for various scenarios of the development of proecological transport system. Arch. Transp. 2014, 32, 17–28. [Google Scholar] [CrossRef]

- Jacyna, M.; Merkisz, J. Proecological approach to modelling traffic organization in national transport system. Arch. Transp. 2014, 30, 31–41. [Google Scholar] [CrossRef] [Green Version]

- Tsakalidis, A.; Mitchell van Balen, G.K.; Pekar, F. Catalyzing Sustainable Transport Innovation through Policy Support and Monitoring: The Case of TRIMIS and the European Green Deal. Sustainability 2020, 12, 3171. [Google Scholar] [CrossRef] [Green Version]

- Evangelista, P.; Colicchia, A.; Crezaza, C. Is environmental sustainability a strategic priority for logistics service providers? J. Environ. Manag. 2017, 198, 353–362. [Google Scholar] [CrossRef]

- PZPM Automotive Industry Report 2020/2021 KPMG 2021. Available online: https://www.pzpm.org.pl/Publikacje/Raporty (accessed on 29 August 2022).

- Pamucar, D.; Chatterjee, K.; Zavadskas, E. Assessment of third-parfty logistics provider using multi-criteria decision-making approach based on interval rough numbers. Comput. Ind. Eng. 2019, 127, 383–407. [Google Scholar] [CrossRef]

- Senthil, S.; Srirangacharyulu, B.; Ramesh, A. A robust hybrid multi-criteria decision making methodology for contractor evaluation and selection in third-party reverse logistics. Expert Syst. Appl. 2014, 41, 50–58. [Google Scholar] [CrossRef]

- Aw, E.N.W.; Dornick, C.R.; Jiann, J.Q. Combining Quantitative and Fundamental Analysis: A Quant-amental Approach. J. Investig. Summer 2014, 2, 28–43. [Google Scholar]

- Gotzamani, K.; Longinidis, P.; Vouzas, F. The logistics services outsourcing dilemma: Quality management and financial performance perspectives. Supply Chain. Manag. 2010, 15, 438–453. [Google Scholar] [CrossRef]

- Olah, J.; Kovacs, Z.; Virglerova, Z.; Lakner, M.; Kovacova, A.; Poop, J. Analysis and Comparison of Economic and Financial Risk Sources in SMEs of the Visegrad Group and Serbia. Sustainability 2019, 11, 1853. [Google Scholar] [CrossRef] [Green Version]

- Barnard, G.A. The use of the likelihood function in statistical practice. In Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, Berkeley, CA, USA, 21 June–18 July 1967; pp. 27–40. [Google Scholar]

- Brozyna, J.; Mentel, G.; Pisula, T. Statistical methods of the bankruptcy prediction in the logistics sector in Poland and Slovakia. Transform. Bus. Econ. 2016, 15, 80–96. [Google Scholar]

- Zysińska, M. Ocena przedsiębiorstw TSL działających w Polsce—dylematy metodyczne badań. In Studia i Prace Kolegium Zarządzania i Finansów; SGH: Warsaw, Poland, 2019; Volume 173, pp. 141–162. Available online: https://ssl-kolegia.sgh.waw.pl/pl/KZiF/czasopisma/zeszyty_naukowe_studia_i_prace_kzif/D (accessed on 18 August 2022).

- Heiko, A.; Darkow, I.L. Scenarios for the logistics services industry. A Delphi-based analysis for 2025. Int. J. Prod. Econ. 2010, 127, 46–59. [Google Scholar]

- Forgy, E.W. Cluster analysis of multivariate data: Efficiency vs interpretability of classifications. Biometrics 1965, 21, 768–769. [Google Scholar]

- Wiegmans, B.; Donders, A. Benchmarking European Rail Freight Transport Companies. Transp. J. 2021, 46, 19–34. Available online: http://www.jstor.org/stable/20713669 (accessed on 10 November 2022). [CrossRef]

- Gupta, A. A stakeholder analysis approach for interorganizational systems. Ind. Manag. Data Syst. 1995, 95, 3–7. [Google Scholar] [CrossRef]

- Kaczorek, M.; Jacyna, M. Fuzzy logic as a decision-making support tool in planning transport development. Arch. Transp. 2022, 61, 52–68. [Google Scholar] [CrossRef]

- Soliman, M.T. The Use of DuPont Analysis by Market Participants, The Accounting Review. Acc. Rev. 2008, 83, 823–853. [Google Scholar] [CrossRef]

- Al-Mashari, M.; Zairi, M. BPR implementation process: An analysis of key success and failure factors. Bus. Process Manag. J. 1999, 5, 87–112. [Google Scholar] [CrossRef] [Green Version]

- Valentin, E. Swot Analysis from a Resource-Based View. J. Mark. Theory Pract. 2001, 9, 54–69. [Google Scholar] [CrossRef]

- Dobbs, E. Guidelines for applying Porter’s five forces framework: A set of industry analysis templates. Compet. Rev. 2014, 24, 32–45. [Google Scholar] [CrossRef]

- Available online: https://www.r-project.org/ (accessed on 12 July 2022).

- Kendall, M.G. A new measure of rank correlation. Biometrika 1938, 30, 81–93. [Google Scholar] [CrossRef]

- Kendall, M.G. The treatment of ties in rank problems. Biometrika 1945, 33, 67–72. [Google Scholar] [CrossRef]

- Boudt, K.; Cornelissen, J.; Croux, C. The Gaussian rank correlation estimator: Robustness properties. Stat. Comput. 2012, 22, 471–483. [Google Scholar] [CrossRef]

- Fieller, E.C.; Hartley, H.O. Tests for rank correlation coefficients. Biometrika 1957, 44, 470–481. [Google Scholar] [CrossRef]

- Yu, G.; Wenjuan, G. Decision Tree Method in Financial Analysis of Listed Logistics Companies. In Proceedings of the 2010 International Conference on Intelligent Computation Technology and Automation, Washington, DC, USA, 11–12 May 2010; pp. 340–353. [Google Scholar]

- Pernestål, A.; Engholm, A.; Bemler, M.; Gidofalvi, G. How Will Digitalization Change Road Freight Transport? Scenarios Tested in Sweden. Sustainability 2021, 13, 304. [Google Scholar] [CrossRef]

- Chen, L.G.; Huo, B. Logistics resources, capabilities and operational performance: A contingency and configuration approach. Ind. Manag. Data Syst. 2019, 119, 230–250. [Google Scholar]

- Watson, S.; Apostolou, B.H.J.M.; Webber, S. Accounting education literature review (2000–2005). J. Account. Educ. 2007, 25, 1–588. [Google Scholar] [CrossRef]

- Karia, N. Antecedents and Consequences of Environmental Capability towards Sustainability and Competitiveness. Sustainability 2022, 14, 12146. [Google Scholar] [CrossRef]

- Noor, A. Adoption of Blockchain Technology Facilitates a Competitive Edge for Logistic Service Providers. Sustainability 2022, 14, 15543. [Google Scholar] [CrossRef]

- Available online: https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal/transport-and-green-deal_pl (accessed on 19 July 2022).

- Bhushan, N.; Mohnert, F.; Sloot, D.; Jans, L.; Albers, C.; Steg, L. Using a Gaussian graphical model to explore relationships between items and variables in environmental psychology research. Front. Psychol. 2019, 10, 1050. [Google Scholar] [CrossRef] [Green Version]

- Langfelder, P.; Horvath, S. Fast R functions for robust correlations and hierarchical clustering. J. Stat. Softw. 2012, 46, 392. [Google Scholar] [CrossRef] [Green Version]

- Tang, C.; Veelenturf, L. The strategic role of logistics in the industry 4.0 era. Transp. Res. Part E Logist. Transp. Rev. 2019, 129, 1–11. [Google Scholar] [CrossRef]

- Bishara, H.J.B. Confidence intervals for correlations when data are not normal. Behav. Res. Methods 2017, 49, 294–309. [Google Scholar] [CrossRef] [Green Version]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zysińska, M.; Żak, J. A Sustainable Method for Evaluating the Activity of Logistics Service Providers (LSPs) in a Turbulent Environment—Case Study Analysis (2020–2021). Energies 2023, 16, 1984. https://doi.org/10.3390/en16041984

Zysińska M, Żak J. A Sustainable Method for Evaluating the Activity of Logistics Service Providers (LSPs) in a Turbulent Environment—Case Study Analysis (2020–2021). Energies. 2023; 16(4):1984. https://doi.org/10.3390/en16041984

Chicago/Turabian StyleZysińska, Małgorzata, and Jolanta Żak. 2023. "A Sustainable Method for Evaluating the Activity of Logistics Service Providers (LSPs) in a Turbulent Environment—Case Study Analysis (2020–2021)" Energies 16, no. 4: 1984. https://doi.org/10.3390/en16041984