5.1. Evaluation of the Cost of Electricity Produced by RE Power Plants in Ukraine’s Households and Investment Projects’ Payback Periods Based on the Current FIT Rates

This study will calculate the LCOE for household solar power plants with installed capacities of 5, 10, 20, 30, 40, and 50 kW and wind power plants with installed capacities of 5, 10, 20, and 30 kW. The specified capacity range corresponds to the households’ most common power plants and is also determined by the current (0–30 kW) and former (0–50 kW) legal limits. The difference in the selected capacities of the RE facilities is due to the productivity factor of wind power plants, which is 2–3 times higher than that of productivity factor of solar power plants [

51]. It is worth noting that the main focus of state support should be providing households with their own electricity and not obtaining profits from the sale of their surpluses at the FIT. Given this, extending state support mechanisms in the household sector to wind power plants with a capacity >30 kW is impractical. In the meantime, as mentioned above, starting from 2019, the FIT was applied to solar PV systems with a capacity of up to 50 kW, providing that they are located on building roofs or facades, without using agricultural land. However, at the end of 2019, the FIT for solar power plants whose installed capacity is between 30 and 50 kW was canceled. In this study, we will estimate the cost effectiveness of such RE projects in order to conclude the feasibility of repealing this legislative norm.

It is noteworthy that the datasets of the solar and wind power plant projects differ somewhat, as they depend on various factors (the solar insolation and wind speed in the region of the RE power plant installation, the technical characteristics of the solar panels and wind generators, etc.); therefore, for calculations in this research, their averaged data were taken, shown in

Table 2 [

52,

53,

54,

55,

56,

57,

58,

59].

It is worth mentioning that the data in

Table 2 concerning the electricity production amount will be adjusted for the production reduction factor, which for solar power plants is 0.8% annually [

60] for wind power plants is 0.2% annually [

61]. The operating and decommissioning expenditures in this study were determined as 1% and 5% of the investment expenditures, respectively [

62], and the lifecycle of both types of power plants was determined to be 25 years [

63].

Under this study, the cost of electricity production by the RE power plants will be calculated considering various options for the structure of the investment expenditures, as follows: (1) on the condition that the investment projects are implemented entirely with the investor’s funds; and (2) on the condition of attracting own and credit resources for five years within the framework of the Ukrgasbank “Eco Energy” program in the following ratios of 75:25, 50:50, and 25:75, respectively, which will affect the size of the discount rate.

To calculate the discount rate, the equity cost will be determined as the alternative investments in deposits for individuals in the national currency. For this aim, we analyzed the deposit rates in UAH in the most reliable banks in Ukraine based on their stability rating [

64]. As of the beginning of June 2023, the following banks offered such annual rates for deposits in UAH for individuals: Credit Agricole—12%, Raiffeisen—12.5%, and Kredobank—14% [

65]. Thus, Kredobank offered the highest rate, and it will be used to determine the equity cost.

The cost of the debt capital will be calculated according to the “Eco Energy” credit line. Therefore, subject to attracting credit resources for 5 years with the first instalment payments of 25%, 50%, and 75%, the annual interest rates on the loan are 20.99%, 19.59%, and 18.69%, respectively [

42].

Thus, the discount rate calculated according to Formula (2), provided that the investment projects are implemented entirely with the investor’s funds, is 14%, provided that own and credit funds are attracted in the following ratios: 25:75—19.2%, 50:50—16.8%, and 75:25—15.2%.

The LCOE values for the electricity produced by the RE power plants in households, considering different discount rates, are shown in

Table 3.

Next, we will compare the obtained LCOE values and the current FIT rates at which the households sell the excess electricity. We will calculate the FIT rates using Formula (3). As mentioned above, the minimum FIT rate is based on the FIT coefficients for the RE power plants, which are shown in

Table 4.

As seen in

Table 4, the FIT coefficients depend on the generating facility’s commissioning date. They tend to decrease due to the reduction in the cost of equipment, materials, and components for such power plants, which directly affects the electricity production cost.

In this study, the calculation will be carried out for the RE power plants commissioned in 2023; accordingly, the coefficient for the power plants commissioned from 1 January 2020 to 31 December 2024 will be used. As evidenced by the data in

Table 4, from 2020 the FIT does not apply to solar power plants with installed capacity between 30 and 50 kW. It is worth noting that, in 2019, the FIT coefficients were the same for the solar PV systems with with an installed capacity of ≤30 kW and those whose capacity is between 30 and 50 kW. Given this, to conclude regarding the feasibility of cancelling the FIT for this category of generating facilities, a coefficient of 3.02 will be used for the 40- and 50-kW solar PV systems. To carry out the FITs recalculation relative to the EUR exchange according to algorithm given in [

48], the exchange rate of UAH 3983 for EUR 100 will be used [

66].

Table 5 includes the obtained results.

Next, we will calculate investment projects’ payback periods according to Formula (4), based on the following factual data and assumptions:

- ▪

A household consumes 168 kWh of electricity per month (corresponding to the average monthly electricity consumption by Ukrainian households) [

14]) and sells the excess electricity at the FIT. Since the support scheme for RE promotion based on the FIT is valid until 31 December 2029, after its expiration, the electricity will be realized at the market price. When calculating cash flows, savings from the electricity expenditures received by the household as a result of their own production and consumption for their own needs will be considered. If the production is not enough to cover the household’s own needs, then the revenue from the power plant is calculated as the amount of electricity cost savings based on the produced amount;

- ▪

The electricity tariff for households as of 1 June 2023 was UAH 2.64/kWh [

67];

- ▪

As mentioned above, the revenue from selling electricity at the FIT is taxable at a cumulative rate of 19.5% [

39].

The results of the calculations of the payback periods of RE investment projects are given in

Table 6.

The results of the calculation of the RE investment projects’ payback periods in Ukraine’s households proved the existence of an economic effect depending on the project’s size. A reduction in investment and operating expenditures as the capacity of an RE power plants increases determines a more attractive payback period for projects with the maximum allowed capacity. Although it is an incentive for households that have the opportunity to implement large-scale projects, a certain category of households, in particular, those that do not have enough financial resources or the ability to install such generating facilities following the requirements of the law, cannot use this incentive. At the same time, for households with an electricity consumption of 2016 kWh/year, 5 kW solar power plants and wind power plants with a capacity of up to 10 kW are not paid off during their lifecycle. The payback period is unattractive for 10 kW solar and 20 kW wind power plants. When attracting a debt capital at 50% or more, the projects are not paid off. Given the above, it is reasonable to gradate the FIT rates in accordance with the RE power plants’ installed capacity. This will allow households with different revenue levels to have equal opportunities to invest in RE power plants.

The primary purpose of deciding to invest in micro RE projects is to ensure household energy autonomy, since the excess electricity for 5–10 kW RE power plants, i.e., that not consumed for the households’ needs, is insignificant. Therefore, supporting such projects should become a priority task of household energy policy. In the meantime, the payback periods of 20-, 30-, 40-, and 50-kW solar power plants and wind power plants with a capacity of 30 kW remain pretty attractive. Implementing solar power plant projects with 40–50 kW capacity is the most profitable. In our opinion, the decision to cancel the FIT for such generating facilities was not logical, because they can significantly contribute to achieving the indicative goals for increasing the green electricity share in the country’s energy consumption. However, the FIT rates for such generating capacities must be significantly adjusted in order to avoid excess profits by their owners and an increase in the financial burden on the final consumers, at the expense of which payments are made under the FIT. At the same time, for identical reasons, the FIT rates for 20- and 30-kW solar power plants also need some adjustment.

In addition, the obtained results have demonstrated the existing imbalance in the payback periods of solar and wind power plants. The difference between their payback periods is quite significant, which will likely continue to contribute to the predominance of solar power plants in households. Therefore, the adjustment of state support should be based on the priority of particular RE technology development, considering the evaluation of the economic, ecological, and social gains from its implementation. The development of hybrid solar–wind power plants is optimal, which will allow the attraction of both energy resources to electricity production. Therefore, the economic justification of the FIT for such plants is highly relevant.

As for acceptable payback periods for RE investment projects in the residential sector, world experience shows that they are usually, at most, 10 years. For example, for solar power plants in the US, the indicators fluctuate within 10–12 years [

68] and 16–22 years in the United Kingdom [

69]. In the meantime, the average payback period of small wind power plants in the US is 15 years [

70], and, in Poland, when they are located in areas with the best wind speed, it is 13 years [

71]. In our opinion, Ukraine should be guided by world experience, ensuring, by economic incentives, a payback period of RE plants of different installed capacities of 10–13 years. This approach to investment policy is logical in terms of the gradual reorientation of state policy towards the energy autonomy of households and the reduction in financial pressure on the final electricity consumers amid the dynamically increasing green electricity share in the country’s energy mix.

Thus, it can be concluded that effective RE development in households requires improving the methodology for the FIT calculation. We believe that the optimal FIT rates should ensure a payback period of investment projects of 10–13 years. With a lifecycle of RE power plants of 25 years, such a payback period will allow households to receive profits from the sale of the excess electricity for a reasonably long period after reaching the break-even point. On the one hand, it will allow to maintaine the investment attractiveness of the sector, and on the other hand, it will reduce the financial pressure on the final electricity consumers.

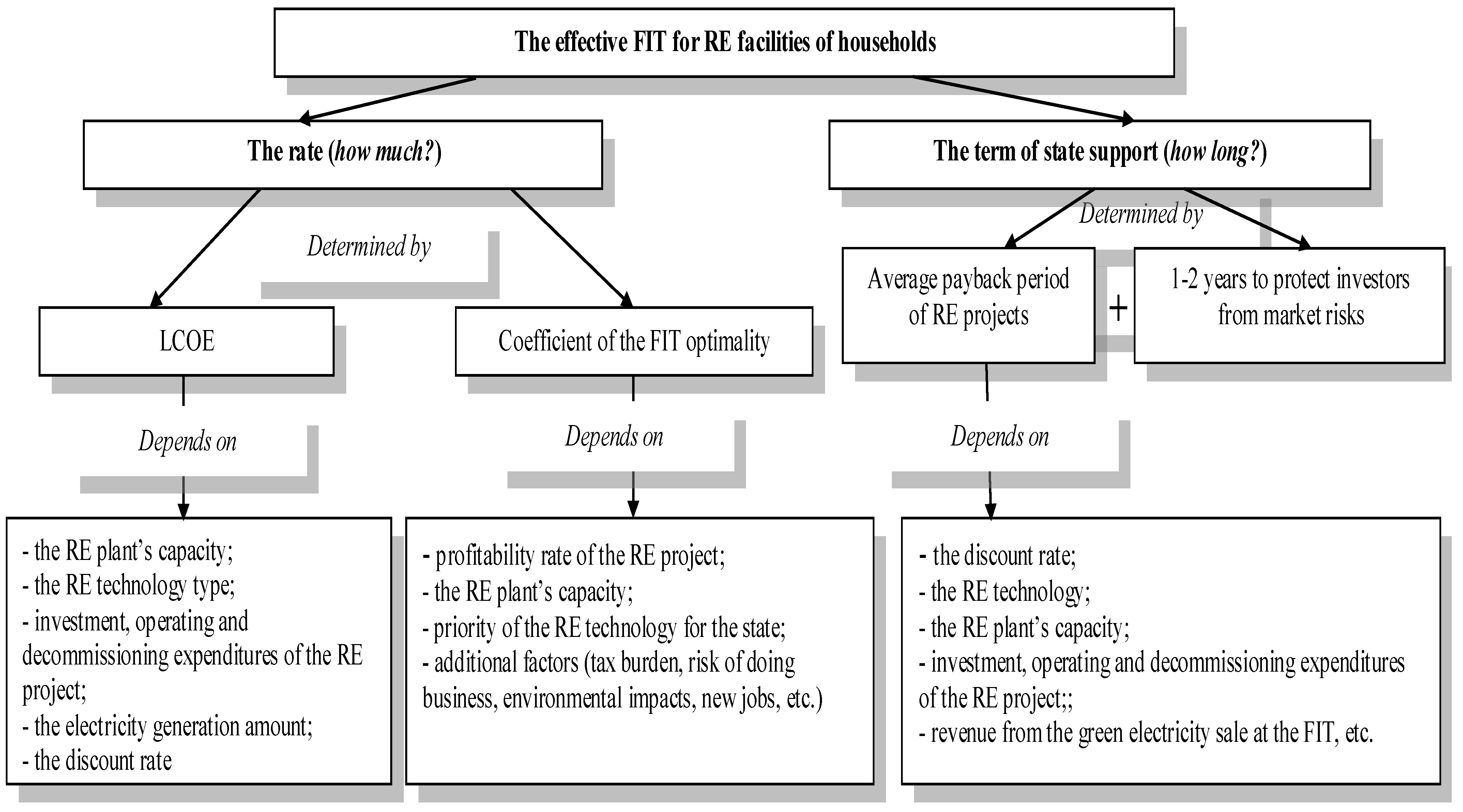

5.2. Methodical Approaches to Determine the Optimal FIT Rates and Policy Recommendations for Effective RE Development in Ukraine’s Households

To improve the methodology of the FIT calculation, we suggest using modernized methodical approaches to determine the optimal FIT rates outlined in [

72] and adjusted to the specifics of the residential sector. Thus, it is advisable to calculate the optimal rate of the FIT for the

i-th RE technology in the

t-th year (

FITopt_it) for the household sector by the following formula:

where

is the fixed electricity production cost throughout the power plant lifecycle, which uses the

i-th RE technology commissioned in the

t-th year, UAH/kWh (calculated according to Formula (1)), and

is the coefficient of optimality of the FIT for the household sector for the

i-th RE technology in the

t-th year, which is determined according to the following formula:

where

is a coefficient that considers the impact of the

j-th factor, which determines the economic, social, and environmental effects of the

i-th RE technology development in the

t-th year for the households, and

n is the number of factors considered.

It is reasonable to include the profitability of the RE power plant, its capacity, and the priority of the

i-th RE technology development for the state as part of the main influencing factors. The range of recommended values for

, from the main influencing factors, is presented in

Table 7. The higher the

, the greater the influence of the particular factor on the FIT rate.

In addition to the abovementioned main factors, other factors may be considered, due to which the state can adjust the final FIT rates for various RE technologies, encouraging or restraining the development of some of them. Such factors may include economic and financial (tax burden and the risk of doing business for the i-th RE technology), environmental (environmental effect of the i-th RE technology), social (creation of new jobs), etc.

The advantage of the proposed approach is flexibility in adjusting the FITs for different RE technologies depending on the needs and goals of the state policy. The FITs, calculated according to the proposed methodological approach, must be reviewed periodically, at least once every three years, due to the trends in reducing the cost of RE technologies. Additionally, as in the case of the current methodology, the FITs must be converted into EUR to insure the RE plants’ owners against possible inflation.

Along with determining the reasonable FIT rates in the household sector, the issue of the validity period of such a state support scheme is significant. It should be sufficient to ensure the return on the investment, but minimal to avoid overspending the state budget or/and that of the final electricity consumers. We believe such a validity period should be established according to the formula “average payback period of projects + 1–2 years” according to the particular RE technology and the group of installed capacity. Adherence to the average payback periods will allow us to return the main part of the funds to the RE power plants’ owners, and an additional 1–2 years will protect the investors from market risks and guarantee confidence in the profitability of the started projects. It is worth noting that the updated methodology for the FIT calculation should only be used for new RE energy power projects in order to maintain the confidence of the existing RE power plants owners.

It is worth noting that, for a more effective implementation of the FIT policy for RE development in the residential sector, improving other policy measures, particularly financial and credit mechanisms, is advisable. As evidenced by the calculation results given in

Section 5.1, the credit resources cost, which is reflected in the discount rate, significantly impacts the projects’ payback periods. Despite the availability of credit programs for financing RE projects in Ukraine’s households, the interest rates on loans are not affordable, especially in the absence of the ability of the households’ owners to pay a significant part of the down payment. Given this, the government should pay attention to improving the existing and developing new affordable loan programs, in particular, the formation of syndicated lending lines that will allow the accumulation of finance of banks of Ukraine and the European Bank for Reconstruction and Development, whose credit lines are already are open in Ukraine for RE projects in the industrial sector, but currently do not extend to the residential sector [

73].

Another approach that can ensure the accumulation of the necessary funds to implement RE projects is the formation of energy cooperatives. It should be noted that Ukraine has already created legislation for energy cooperative formation, and, since 2019, the FIT has been introduced for the RE power plants implemented under such energy associations [

74]. However, implementing RE projects within the framework of such cooperation has not gained significant popularity. The main barrier is the population’s lack of awareness of this issue. Therefore, the government should focus on the popularization of the advantages of creating energy cooperatives and informing about the economic, ecological, and social gains from implementing RE projects.

The cost of technologies directly affects the payback period of RE investment projects and, therefore, the FITs rate. One of the approaches to make them cheaper is state support for Ukrainian enterprises, which can produce equipment for the RE industry. It should be noted that two powerful factories in Ukraine have provided a full cycle of solar PV systems production—from growing the silicon to assembling the solar panels. However, the introduction in 2019 of benefits for the import of foreign-made solar panels negatively impacted their competitiveness. As a result of the introduction of such benefits, the prices of the imported panels became 20% lower than the domestic ones. As a result, enterprises were forced to reorient their activities mainly to the assembly of panels in Ukraine from imported equipment [

75]. A stimulus for the development of the industry could be the spread of the legislative norm regarding the allowance to the FIT for the use of Ukrainian-made equipment for RE project implementation, which currently applies to industrial RE power plants but does not apply to RE facilities in the residential sector [

12].

It should be noted that promoting RE development based on the FIT calculated according to the proposed methodology should be used in the transition period—from the current FIT model to a new support scheme for households to ensure further RE development without state support. Such mechanisms can be net metering or net billing, which are focused on covering exclusively a household’s own electricity consumption and do not require additional financial expenses from the state or from other consumers.

Net metering is a mechanism that allows the owners of RE power plants to store the excess electricity in the country’s energy grid and use it when the need arises. Net billing is a variation of net metering that works on a similar principle. The difference is that the excess electricity supplied to the grid, instead of kWh, is counted in monetary equivalents, according to the electricity price at the time of the supply. Thus, under net billing, the consumers receive a cash deposit for the excess electricity supplied into the grid, which can then be used to pay for the electricity consumed by them in subsequent periods, provided that the need for electricity exceeds the amount of its production.

A significant barrier to the effective implementation of the mentioned mechanisms can be the continuation of subsidizing electricity prices for Ukrainian households. This is because low electricity tariffs do not encourage household owners to invest in RE projects and negatively affect the profitability of their implementation under net metering/net billing support schemes. It is worth noting that, although, since June 2022, the electricity tariff for households in Ukraine has been increased to UAH 2.64/kWh (EUR 0.065/kWh), it remains extremely low compared to the tariffs in other European countries (for example, as of the beginning of 2023, in Greece it was EUR 0.18/kWh, in Italy—EUR 0.17/kWh, and in Switzerland—EUR 0.15/kWh [

76]). Adopting decisions regarding the metering/net billing introduction should be preceded by creating favorable organizational and economic conditions under which these mechanisms will allow households to transit to prosumerism without state incentives.

,

,

{kind=link}

{kind=link}