Employee Financial Wellness Programs (EFWPs) as an Innovation in Incentive Systems of Energy Sector Enterprises in Poland during the COVID-19 Pandemic—Current Status and Development Prospects

Abstract

:1. Introduction

2. Materials and Methods

- Do EFWPs operate in Poland and in what form?

- Which sectors of the Polish economy are predisposed to implement EFWP in all areas (payroll loans, financial education, financial coaching) in the context of their specific national conditions?

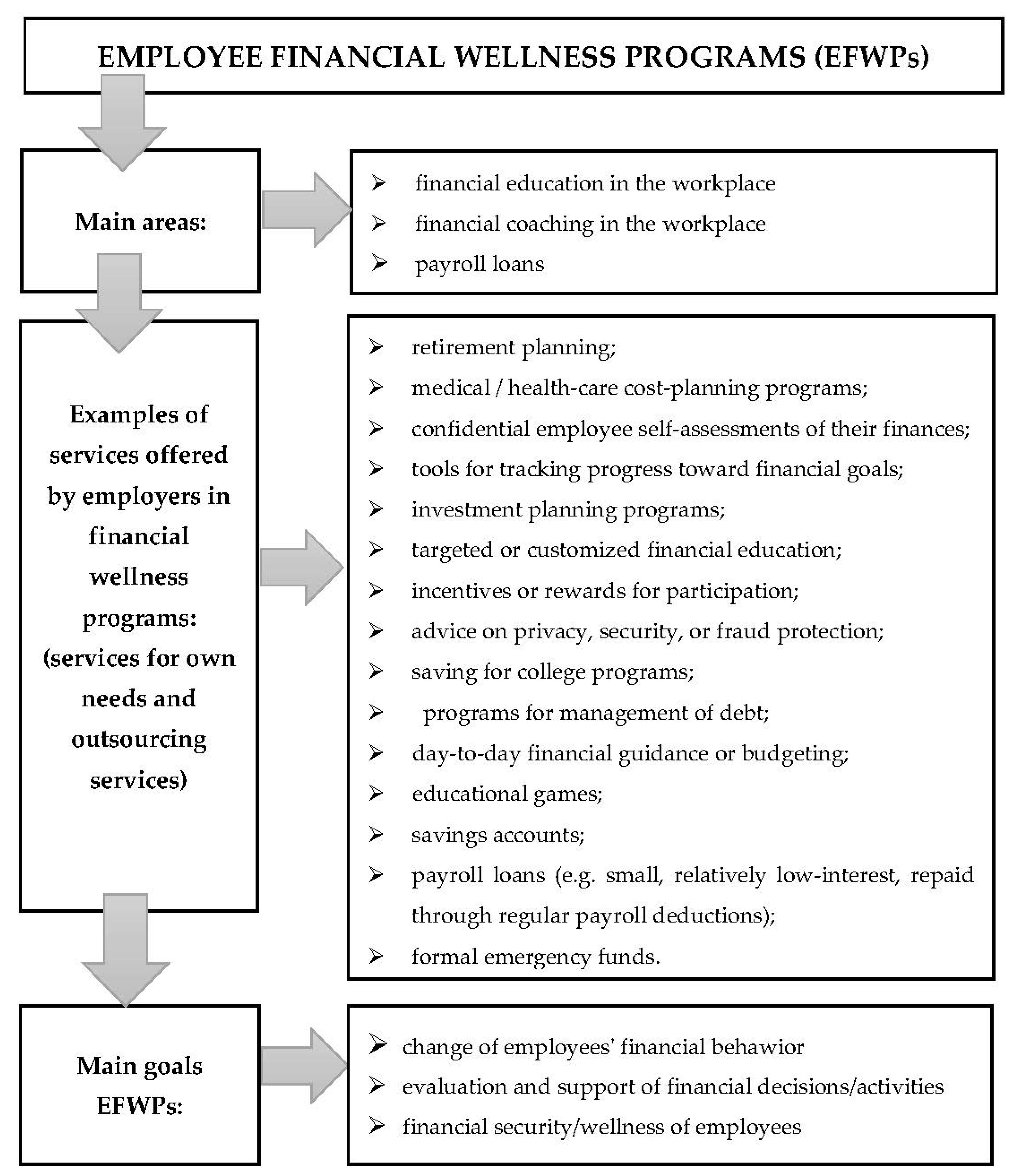

3. Literature Review

- Having control over day-to-day, month-to-month finances;

- Having the capability to absorb a financial shock;

- Being on track to meet financial goals;

- Having the financial freedom to make choices that allow one to enjoy life.

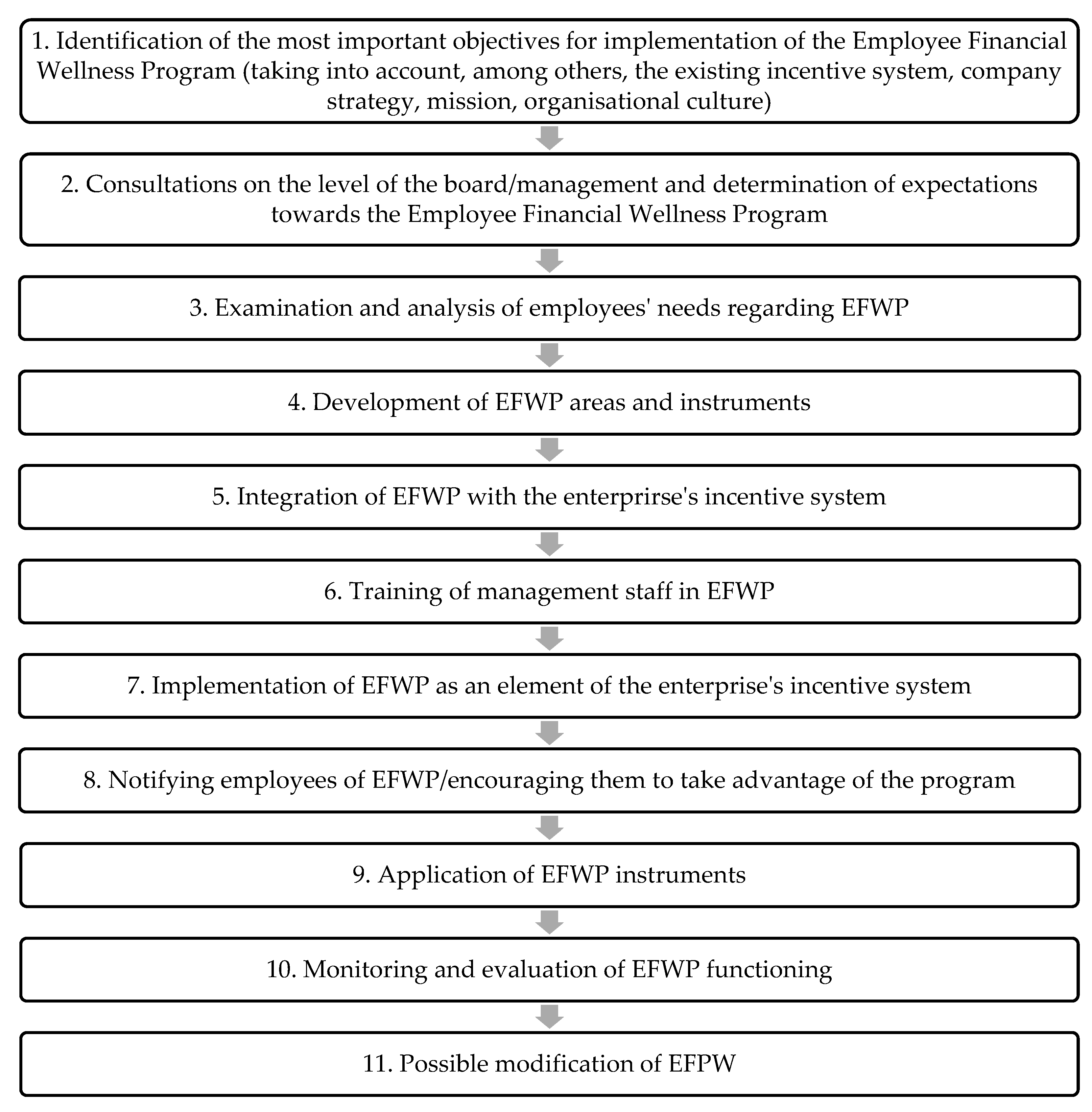

4. Changes in the Field of Motivating during COVID-19

- Offering an EFWP as an additional benefit within the incentive system to improve the quality of employees’ financial lives;

- Designing incentive system services based on identified financial challenges of employees and their families, so that tailored services can be implemented within the EFWPs;

- Assisting employees to manage so-called financial contingencies that arise in their daily financial lives;

- Help with financial planning for the future. Support should be tailored to the employee’s age, financial situation and capabilities, as well as composition and expectations of their family.

5. Results

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anderson, S.G.; Zhan, M.; Scott, J. Developing Financial Management Training in Low-Income Communities. J. Community Pract. 2005, 13, 31–49. [Google Scholar] [CrossRef]

- Kalleberg, A.L. 7 Good Jobs, Bad Jobs. In The SAGE Handbook of the Sociology of Work and Employment; SAGE Publications Ltd: London, UK, 2016; pp. 111–128. [Google Scholar] [CrossRef]

- Szydło, R.; Wiśniewska, S.; Tyrańska, M.; Dolot, A.; Bukowska, U.; Koczyński, M. Employer Expectations Regarding the Competencies of Employees on the Energy Market in Poland. Energies 2021, 14, 7233. [Google Scholar] [CrossRef]

- Joo, S. Personal Financial Wellness. In Handbook of Consumer Finance Research; Springer: New York, NY, USA, 2008. [Google Scholar] [CrossRef]

- Miller, R.B.; Strumpel, B. Economic Means for Human Needs: Social Indicators of Well-Being and Discontent. Contemp. Sociol. A J. Rev. 1978, 7, 800. [Google Scholar] [CrossRef]

- Hayhoe, C.R.; Wilhelm, M.S. Modeling Perceived Economic Well-Being in A Family Setting: A Gender Perspective. J. Financ. Couns. Plan. 1998, 9, 21–34. [Google Scholar]

- Wilhelm, M.S.; Varcoe, K. Assessment of financial well-being: Impact of objective economic indicators and money attitudes on financial satisfaction and financial progress. Annu. Proc. Assoc. Financ. Counsel. Plan. Educ. 1991, 4, 184–202. [Google Scholar]

- George, L.K. Economic status and subjective well-being: A review of the literature and an agenda for future research. In Aging, Money, and Life Satisfaction: Aspects of Financial Gerontology; Cutler, N.E., Gregg, D.W., Lawton, M.P., Eds.; Springer Publishing Company: New York, NY, USA, 1992; pp. 69–99. [Google Scholar]

- Porter, N.M.; Garman, E.T. Testing a Conceptual Model of Financial Well-Being. Financ. Couns. Plan. 1993, 4, 135–164. Available online: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.379.6832&rep=rep1&type=pdf (accessed on 19 February 2022).

- Baek, E.; DeVaney, S.A. Assessing the Baby Boomers’ Financial Wellness Using Financial Ratios and a Subjective Measure. Fam. Consum. Sci. Res. J. 2004, 32, 321–348. [Google Scholar] [CrossRef]

- Hayhoe, C.R. Theoretical model of perceived economic well-being. Annu. Proc. Assoc. Financ. Counsel. Plan. Educ. 1990, 116–141. [Google Scholar]

- Joo, S.; Garman, E.T. Personal Financial Wellness May be the Missing Factor in Understanding and Reducing Worker Absenteeism. Pers. Financ. Work. Product. 1998, 2, 172–182. [Google Scholar]

- Fergusson, D.M.; Horwood, L.J.; Beautrais, A.L. The Measurement of Family Material Well-Being. J. Marriage Fam. 1981, 43, 715. [Google Scholar] [CrossRef]

- Hayhoe, M. Spatial interactions and models of adaptation. Vis. Res. 1990, 30, 957–965. [Google Scholar] [CrossRef]

- Hansen, J.C.; Rossberg, R.H.; Cramer, S.H. Counseling: Theory and Practice; Allyn and Bacon: Boston, MA, USA, 1994. [Google Scholar]

- Zimmerman, S.L. Understanding Family Policy: Theories & Applications; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2012. [Google Scholar] [CrossRef]

- Breen, R.F. The financially mature: What they want and how to help them get it. Insur. Sales 1991, 134, 8–10. [Google Scholar]

- Williams, F.L. Financial counseling: Low-income or limited-income families. In Economic Changes: Challenges for Financial Counseling and Planning Professionals; Fitzsimmons, V.S., Ed.; Association for Financial Counseling and Planning Education: San Antonio, TX, USA, 1993; pp. 121–145. [Google Scholar]

- Narges, D.; Laily, H.P. Determinants of financial wellness among Malaysia workers. Afr. J. Bus. Manag. 2011, 5, 10092–10100. [Google Scholar] [CrossRef]

- Brown, R.C. The need for employee financial counseling: An industry perspective. In Financial Counseling: Assessing the State of Art; Myhre, D.C., Ed.; Financial counseling Project, Extension Division, Virginia Polytechnic Institute and State University: Blacksburg, VA, USA, 1979; pp. 29–38. [Google Scholar]

- Garman, E.T.; Leech, I.E.; Grable, J.E. The Negative Impact of Employee Poor Personal Financial Behaviors on Employers. J. Financ. Couns. Plan. 1996, 7, 157–168. Available online: https://www.researchgate.net/publication/253429682_The_Negative_Impact_Of_Employee_Poor_Personal_Financial_Behaviors_On_Employers (accessed on 19 February 2022).

- Williams, F.L.; Haldeman, V.; Cramer, C. Financial Concerns and Productivity. J. Financ. Couns. Plan. 1996, 7, 147–156. Available online: https://www.researchgate.net/publication/241526128 (accessed on 19 February 2022).

- Williams, F.; Lown, J.; Haldeman, V.; Garman, T.; Fletcher, C.N.; Cramer, S. Financial concerns of employees and their productivity. In Proceedings of 1990 Annual Meetings of Association for Financial Counseling and Planning Education; Weagley, R.O., Ed.; AFCPE: Columbia, MD, USA, 1990; pp. 45–68. [Google Scholar]

- Center for Credit Union Innovation. Financial Stress and Workplace Performance: Developing Employer-Credit Union Partnerships. Report no 82. Retrieved from Filene Research Institute Website. 2002. Available online: https://p.widencdn.net/gkjrh3/1752-82CCUIFinancial_Stress (accessed on 19 February 2022).

- Stanford Center on Longevity. The Future of Financial Wellness. Conference Proceedings, 3. 2014. Available online: http://longevity3.stanford.edu/wp-content/uploads/2015/11/Proceedings-final-draft-12.31.pdf (accessed on 19 February 2022).

- Brown, S.; Gray, D.; McHardy, J.; Taylor, K. Employee trust and workplace performance. J. Econ. Behav. Organ. 2015, 116, 361–378. [Google Scholar] [CrossRef] [Green Version]

- Rickard, C.; Spiegelhalter, K.; Cox, A. Employee Financial Well-Being: Practical Guidance; Research Report; Chartered Institute of Personnel and Development: London, UK, 2017; Available online: https://www.cipd.co.uk/Images/financial-well-being-practical-guidance-report-1_tcm18-17440.pdf (accessed on 19 February 2022).

- Garman, E.T. Financial education: Issues and answers. Pers. Financ. Work. Prod. 1998, 2, 79–81. [Google Scholar]

- Garman, E.T.; Bagwell, D.C. Comprehensive workplace financial education: The recommended PFEE Matrix. Pers. Financ. Work. Prod. 1999, 3, 48–50. [Google Scholar]

- Oyer, P.; Schaefer, S.; Barkume, A.; Hall, B.; Lazear, E.; Levin, J.; Murphy, K.J.; Zabojnik, J.; Zweibel, J. Why Do Some Firms Give Stock Options to All Employees?: An Empirical Examination of Alternative Theories; National Bureau of Economic Research: Cambridge, MA, USA, 2004. [Google Scholar] [CrossRef]

- Oyer, P.; Schaefer, S. Why Do Some Firms Give Stock Options to All Employees?: An Empirical Examination of Alternative Theories. NBER Working Paper, 10222. Available online: http://www.nber.org/papers/w10222 (accessed on 19 February 2022).

- Richardson, T.; Elliott, P.; Roberts, R. The relationship between personal unsecured debt and mental and physical health: A systematic review and meta-analysis. Clin. Psychol. Rev. 2013, 33, 1148–1162. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Consumer Financial Protection Bureau. Financial Wellness at Work. A Review of Promising Practices and Policies. Report. 2014. Available online: http://files.consumerfinance.gov/f/201407_cfpb_report_financial-literacy-annual-report.pdf (accessed on 19 February 2022).

- Prosperity NOW, Center for Social Development. Workplace Financial Wellness Services: A Primer for Employers. 2017. Available online: https://prosperitynow.org/files/PDFs/workplace_financial_wellness_services.pdf (accessed on 19 February 2022).

- Mrkvicka, J.S.N.; Held, J.C. Financial Education for Today’s Workforce: 2016 Survey Results. 2016. Available online: https://www.ifebp.org/bookstore/financial-education-2016-survey-results/Pages/financial-education-for-todays-workplace-2016-survey-results.aspx (accessed on 21 January 2022).

- Frank-Miller, E.G.; Despard, M.; Grinstein-Weiss, M.; Covington, M. Financial wellness programs in the workplace: Employer motivations and experiences. J. Work. Behav. Health 2019, 34, 241–264. [Google Scholar] [CrossRef]

- Hampton, J.; Wolter, S.; Fox-Dichter, S.; Frank-Miller, E. Employee Financial Wellness Programs: Tips for Providers. Social Policy Institute Research Brief, 20–02. 2020. Available online: https://doi.org/https://doi.org/10.7936/q71f-qp19 (accessed on 10 January 2022). [CrossRef]

- Tulloch, J. Building a Successful Workplace Financial Wellness Program, Employers as Caretakers. International Society of Certified Employee Benefit Specialists. Benefits Quarterly Third Quarter, 12–14. 2018. Available online: https://www.ifebp.org/inforequest/IFEBP/0201066.pdf (accessed on 19 February 2022).

- Pyron, D.; Pettus, L. The Case for Financial Wellness Programs to Unlock Heightened Employee Engagement, The Next Generation of Benefits. International Society of Certified Employee Benefit Specialists. Benefits Quarterly Fourth Quarter, 34–38. 2019. Available online: https://www.ifebp.org/inforequest/ifebp/0201608.pdf (accessed on 23 February 2022).

- Fox-Dichter, S.; Zeng, Y.; Despard, M.; Frank-Miller, E.; Germain, G. Employee Financial Wellness Programs: Differences in Reach by Financial Circumstances. Social Policy Institute Research Brief, 18–02. 2018. Available online: https://doi.org/10.7936/5g1g-dq59 (accessed on 7 January 2022). [CrossRef]

- Grinstein-Weiss, M.; Russell, B.; Tucker, B.; Comer, K. Lack of Emergency Savings Puts American Households at Risk: Evidence from the Refund to Savings Initiative. Center for Social Development Brief, 14–13. 2014. Available online: https://openscholarship.wustl.edu/cgi/viewcontent.cgi?article=1598&context=csd_research (accessed on 19 February 2022).

- Pew Charitable Trusts. The Role of Emergency Savings in Family Financial Security. How Do Families Cope with Financial Shocks? Brief from the Pew Charitable Trust. 2015. Available online: https://www.pewtrusts.org/~/media/assets/2015/10/emergency-savings-report-1_artfinal.pdf (accessed on 10 January 2022).

- Beverly, S.G. Measures of Material Hardship. J. Poverty 2001, 5, 23–41. [Google Scholar] [CrossRef]

- Boston College Center for Work and Family. The Metlife Study of Financial Wellness Across the Globe: A Look at How Multinational Companies are Helping Employees Better Manage Their Personal Finances; Metropolitan Life Insurance Company: New York, NY, USA, 2011; p. 7. [Google Scholar]

- Hannon, G.; Covington, M.; Despard, M.; Frank-Miller, E.; Grinstein-Weiss, M. Employee Financial Wellness Programs: A Review of the Literature and Directions for Future Research. Center for Social Development Brief, 17–23. 2017. Available online: https://openscholarship.wustl.edu/cgi/viewcontent.cgi?article=1595&context=csd_research (accessed on 19 January 2022).

- KeyBank. What is Financial Wellness? It Starts with Knowing Where you Stand. 2022. Available online: https://www.key.com/personal/financial-wellness/index.jsp (accessed on 15 February 2022).

- Morningstar. An Employer’s Guide to Financial Wellness. A Work Placeguide. 2015. Available online: https://www.financialimpact.com/wp-content/uploads/2018/08/employers-guide-to-financial-wellness.pdf (accessed on 19 February 2022).

- Boxall, P. HR strategy and competitive advantage in the service sector. Hum. Resour. Manag. J. 2003, 13, 5–20. [Google Scholar] [CrossRef]

- Lambert, S.J. Added Benefits: The Link Between Work-Life Benefits and Organizational Citizenship Behavior. Acad. Manag. J. 2000, 43, 801–815. [Google Scholar] [CrossRef]

- Batt, R.; Colvin, A.J.S. An Employment Systems Approach to Turnover: Human Resources Practices, Quits, Dismissals, and Performance. Acad. Manag. J. 2011, 54, 695–717. [Google Scholar] [CrossRef]

- Bagwell, D.C.; Kim, J. Financial stress, health status, and absenteeism in credit counseling clients. J. Consum. Educ. 2003, 21, 50–58. [Google Scholar]

- Society for Human Resource Management. SHRM Research Spotlight: Employee Financial Stress. 2014. Available online: https://www.shrm.org/hr-today/trends-and-forecasting/research-and-surveys/Documents/Employee-Financial-Stress-Flyer.pdf (accessed on 19 February 2022).

- Employee Financial Wellness Programs Project: Comprehensive Report of Findings. Available online: https://doi.org/10.7936/k7s46rfz (accessed on 19 February 2022). [CrossRef]

- Zellner, S. (n.d.) Financial Wellness in the Workplace: The Business Imperative. In U.S. Chamber of Commerce Foundation Corporate Citizenship Center’s Shape Leaders in Financial Wellness. Retrieved 16 February 2022. Available online: https://www.uschamberfoundation.org/sites/default/files/media-uploads/FinancialWellnessPaperLayoutFinalForWebsite.pdf (accessed on 10 January 2022).

- Oerlemans, W.G.M.; Bakker, A.B. Motivating job characteristics and happiness at work: A multilevel perspective. J. Appl. Psychol. 2018, 103, 1230–1241. [Google Scholar] [CrossRef] [PubMed]

- Coccia, M. Motivation and Theory of Self-Determination: Some Management Implications in Organizations. J. Econ. Bibliogr. 2019, 5, 223–230. [Google Scholar] [CrossRef]

- Calk, R.; Patrick, A. Millennials Through the Looking Glass: Workplace Motivating Factors. J. Bus. Inq. Res. Educ. Appl. 2017, 16, 131–139. [Google Scholar]

- Bawa, M.A. Employee motivation and productivity: A review of literature and implications for management practice. Int. J. Econ. Commer. Manag. 2017, V, 662–673. Available online: http://ijecm.co.uk/ (accessed on 20 January 2022).

- Abyad, A. Project Management: Motivation Theories and Process Management. Middle East J. Bus. 2018, 13, 18–22. [Google Scholar] [CrossRef]

- Badubi, R.M. Theories of Motivation and Their Application in Organizations: A Risk Analysis. Int. J. Innov. Econ. Dev. 2017, 3, 44–51. [Google Scholar] [CrossRef] [Green Version]

- Bordel, B.; Alcarria, R. Assessment of human motivation through analysis of physiological and emotional signals in Industry 4.0 scenarios. J. Ambient Intell. Humaniz. Comput. 2017, 1–21. [Google Scholar] [CrossRef]

- Mangi, A.A.; Kanasro, H.A.; Burdi, M.B. Motivation Tools and Organizational Success: A Criticle Analysis of Motivational Theories. Gov. Res. J. Polit. Sci. 2015, 4, 51–62. Available online: https://www.google.com.pk/search?q=Herzberg-Two-Factor+Theory (accessed on 19 February 2022).

- Berson, C. Local labor markets and taste-based discrimination. IZA J. Labor Econ. 2016, 5, 1–21. Available online: https://izajole.springeropen.com/articles/10.1186/s40172-016-0045-9 (accessed on 20 January 2022). [CrossRef] [Green Version]

- Usmanova, N.; Yang, J.; Sumarliah, E.; Khan, S.U.; Khan, S.Z. Impact of knowledge sharing on job satisfaction and innovative work behavior: The moderating role of motivating language. VINE J. Inf. Knowl. Manag. Syst. 2020, 51, 515–532. [Google Scholar] [CrossRef]

- Park, S. Motivating raters through work design: Applying the job characteristics model to the performance appraisal context. Cogent Psychol. 2017, 4, 1287320. [Google Scholar] [CrossRef]

- Troshina, E.P.; Mantulenko, V.V. Influence of Digitalization on Motivation Techniques in Organizations. Digital Age Chances Chall. Future ISCDTE 2019 Lect. Notes Netw. Syst. 2019, 84, 317–323. [Google Scholar] [CrossRef]

- Gagné, M.; Tian, A.W.; Soo, C.; Zhang, B.; Ho, K.S.B.; Hosszu, K. Different motivations for knowledge sharing and hiding: The role of motivating work design. J. Organ. Behav. 2019, 40, 783–799. [Google Scholar] [CrossRef]

- Zhao, X.R.; Ghiselli, R.; Law, R.; Ma, J. Motivating frontline employees: Role of job characteristics in work and life satisfaction. J. Hosp. Tour. Manag. 2016, 27, 27–38. [Google Scholar] [CrossRef]

- Rabiul, K.; Yean, T.F. Leadership styles, motivating language, and work engagement: An empirical investigation of the hotel industry. Int. J. Hosp. Manag. 2020, 92, 102712. [Google Scholar] [CrossRef]

- Burmeister, A.; Hirschi, A.; Zacher, H. Explaining Age Differences in the Motivating Potential of Intergenerational Contact at Work. Work. Aging Retire. 2021, 7, 197–213. [Google Scholar] [CrossRef]

- PricewaterhouseCoopers. Employee Financial Wellness Survey 2018 Results. Available online: https://www.harmonyhealth.com/wp-content/uploads/2021/04/pwc-2018-employee-wellness-survey.pdf (accessed on 20 January 2022).

- Reinfuss, R. Motywuj do pracy, a nie do premii: Dlaczego systemy premiowania nie poprawiają wyników i nie są motywujące? Personel i Zarządzanie 2018, 2, 76–81. [Google Scholar]

- White, N.D.; Packard, K.; Kalkowski, J. Financial Education and Coaching: A Lifestyle Medicine Approach to Addressing Financial Stress. Am. J. Lifestyle Med. 2019, 13, 540–543. [Google Scholar] [CrossRef] [PubMed]

- American Psychological Association. Stress in America: Paying with Our Health. 2015. Available online: https://www.apa.org/news/press/releases/stress/2014/stress-report.pdf (accessed on 11 January 2022).

- Lin, J.T.; Bumcrot, C.; Ulicny, T.; Lusardi, A.; Mottola, G.; Kieffer, C.; Walsh, G. Financial capability in the United States. 2016. Available online: https://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf (accessed on 19 February 2022).

- Birkenmaier, J.; Curley, J.; Kelly, P. Matched Savings Account Program Participation and Goal Completion for Low-Income Participants: Does Financial Credit Matter? J. Soc. Serv. Res. 2014, 40, 215–231. [Google Scholar] [CrossRef]

- Instytut GFK. Kurs na financial wellness. Jak firmy mogą wspierać komfort finansowy pracowników? Raport na zlecenie portalu Cash, Warszawa. 2021. Available online: https://stronakadry.pl/financial-wellness?k=mb&r=2021 (accessed on 19 February 2022).

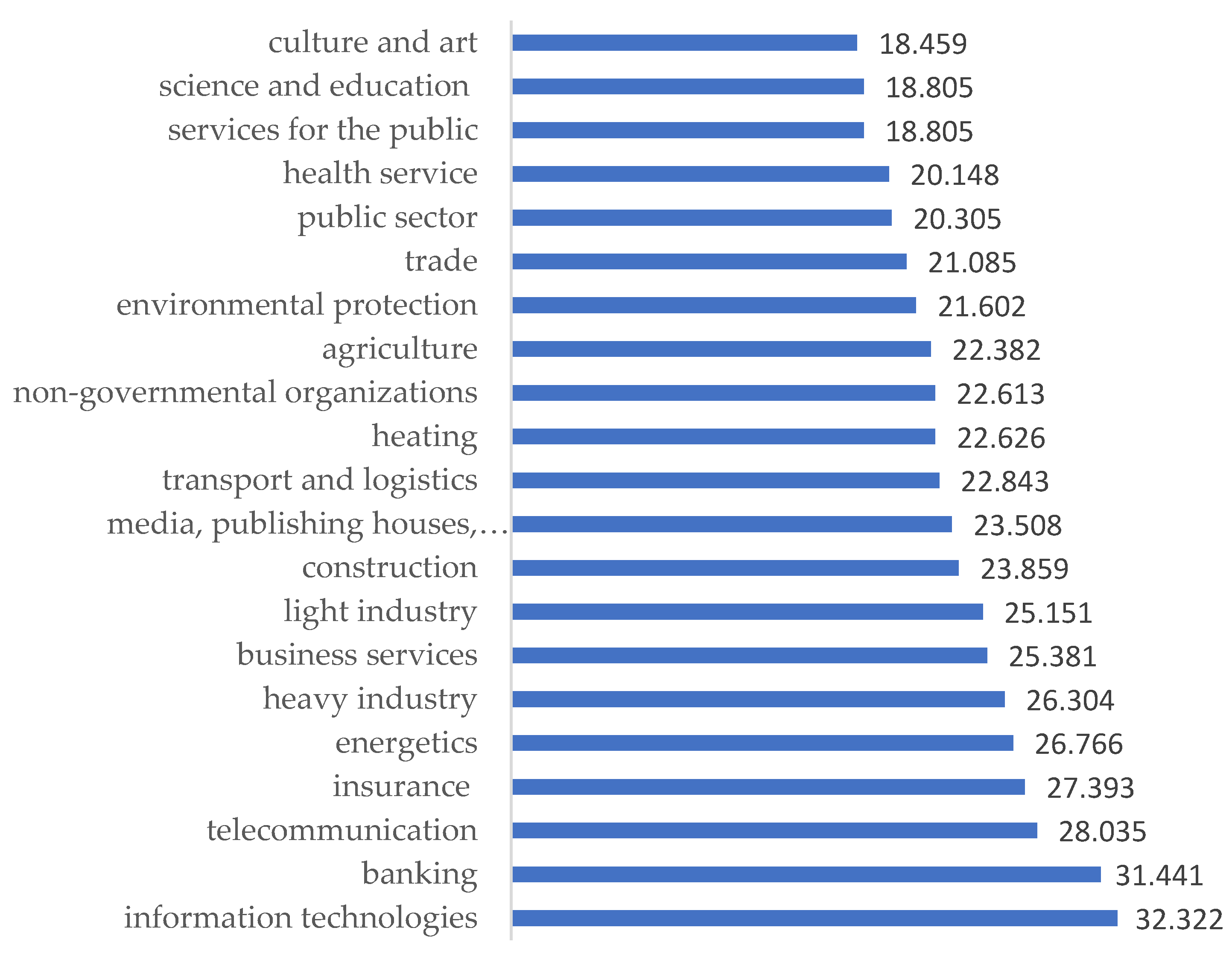

- Czepiel, M. Najwyżej i Najniżej Opłacane Branże w 2020 Roku—Wynagrodzenia.pl. Sedlak&Sedlak. 2021. Available online: https://wynagrodzenia.pl/artykul/najwyzej-i-najnizej-oplacane-branze-w-2020-roku (accessed on 20 January 2022).

- Ustawa z dnia 4 Marca 1994 r. o Zakładowym Funduszu Swiadczeń Socjalnych (Dz. U. 1994 Nr 43 poz. 163), Pub. L. No. Dz. U. z 2021 r. poz. 746, 2445. 2021. Available online: http://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU19940430163 (accessed on 19 February 2022).

- Ustawa z dnia 23 Maja 1991 Roku o Związkach Zawodowych (Dz.U. 1991 nr 55 poz. 234), Pub. L. No. Dz. U. z 2019 r. poz. 263, z 2021 r. poz. 1666. 1991. Available online: http://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU19910550234/U/D19910234Lj.pdf (accessed on 20 January 2022).

- USTAWA z dnia 11 sierpnia 2021 r. o kasach zapomogowo-pożyczkowych (Dz.U. z 2021 r. poz. 1666). 2021. Available online: http://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU20210001666/O/D20211666.pdf (accessed on 20 January 2022).

{kind=link}

{kind=link}

{kind=link}

| Database | “Emplyee Financial Wellness Progam” or “Finnacial Wellness Program” | “Emplyee Financial Wellness Progam” or “Finacial Wellness Program” and “Energy Sector” |

|---|---|---|

| Scopus | 8 | 0 |

| Web of Science | 3 | 0 |

| Elsevier | 5 | 0 |

| Emerald | 3 | 0 |

| EBSCO | 3 | 0 |

| For Employers | For Employees |

|---|---|

| investment in employees; | sense of financial security; |

| element of an innovative incentive system; | self-development in terms of finance; |

| improved effectiveness of the incentive system; | easy access to comprehensive financial services in the workplace; |

| lower employee turnover; | opportunities to improve personal/household financial management; |

| enhancing a positive image of the organisation; | making sound credit decisions; |

| increase in productivity/effectiveness/engagement/of employees; | sense of stability at work; |

| improvement of economic and financial results of the enterprise; | job satisfaction; |

| strengthening the competitive edge of the company; | reduction of financial debt; |

| possibility to use EFWP as a tool for recruitment, talent management and brand building; | reduced financial stress; |

| element of corporate social responsibility. | improved financial behaviour; |

| increased awareness of saving; | |

| acquisition of ability to set financial goals and develop action plans to achieve them; | |

| acquiring the skills to deal with difficult/crisis situations in the financial area; | |

| awareness of the possibility to obtain support from specialists in the workplace; | |

| increased motivation to work; awareness of being supported by the employer. |

| Criterion | Employee Financial Wellness Programs (EFWP) | Social Company Funds | |

|---|---|---|---|

| Company Social Benefits Fund (ZFŚS) | Employee Saving and Loan Association (KZP) | ||

| Legal basis | None | Yes | Yes |

| Nature of the instrument for the enterprise | Voluntary | Mandatory or voluntary, depending on criteria established by law | Mandatory if at least 10 employees so wish (employee benefit) |

| Main objective | Sense of financial security and motivation of employees to work more productively | Satisfies material and subsistence needs of members | Material assistance |

| Beneficiaries | Employees | Employees and their families, pensioners and retired individuals—former employees and their families and other persons to whom the employer has granted the entitlement under the rules | Employees and their families, pensioners and retired individuals |

| Availability | Condition for joining the program | No conditions | Condition of membership in KZP |

| Products | Depending on the needs of employees in the following areas: financial education in the workplace financial coaching in the workplace, payroll loans | - Support (including financial) for leisure activities, cultural and educational activities, sports and recreational activities, care of children at nurseries, children’s clubs, day care centres or nannies, in kindergartens and other forms of pre-school education, - Granting material assistance—in kind or financially (loan, assistance), as well as repayable or non-repayable aid for housing purposes under the conditions specified in the agreement | Loan Non-repayable assistance |

| Sources of financing | External—under a contract with a bank or other financial institution Internal—with the use of the company’s financial resources | Annual basic contribution from the employer’s funds, calculated in relation to the average number of employees (the amount of contribution is regulated by law) | Members’ monthly contributions—usually deducted from salaries |

| Purpose of the loan | Any | Strictly defined | Strictly defined |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Malkowska, A.; Tokarz-Kocik, A.; Drela, K.; Bera, A. Employee Financial Wellness Programs (EFWPs) as an Innovation in Incentive Systems of Energy Sector Enterprises in Poland during the COVID-19 Pandemic—Current Status and Development Prospects. Energies 2022, 15, 2102. https://doi.org/10.3390/en15062102

Malkowska A, Tokarz-Kocik A, Drela K, Bera A. Employee Financial Wellness Programs (EFWPs) as an Innovation in Incentive Systems of Energy Sector Enterprises in Poland during the COVID-19 Pandemic—Current Status and Development Prospects. Energies. 2022; 15(6):2102. https://doi.org/10.3390/en15062102

Chicago/Turabian StyleMalkowska, Agnieszka, Anna Tokarz-Kocik, Karolina Drela, and Anna Bera. 2022. "Employee Financial Wellness Programs (EFWPs) as an Innovation in Incentive Systems of Energy Sector Enterprises in Poland during the COVID-19 Pandemic—Current Status and Development Prospects" Energies 15, no. 6: 2102. https://doi.org/10.3390/en15062102