Decarbonizing Russia: Leapfrogging from Fossil Fuel to Hydrogen

Abstract

:1. Introduction

2. Materials and Methods

2.1. Description of Modeling Framework

2.2. Future Electricity Demand

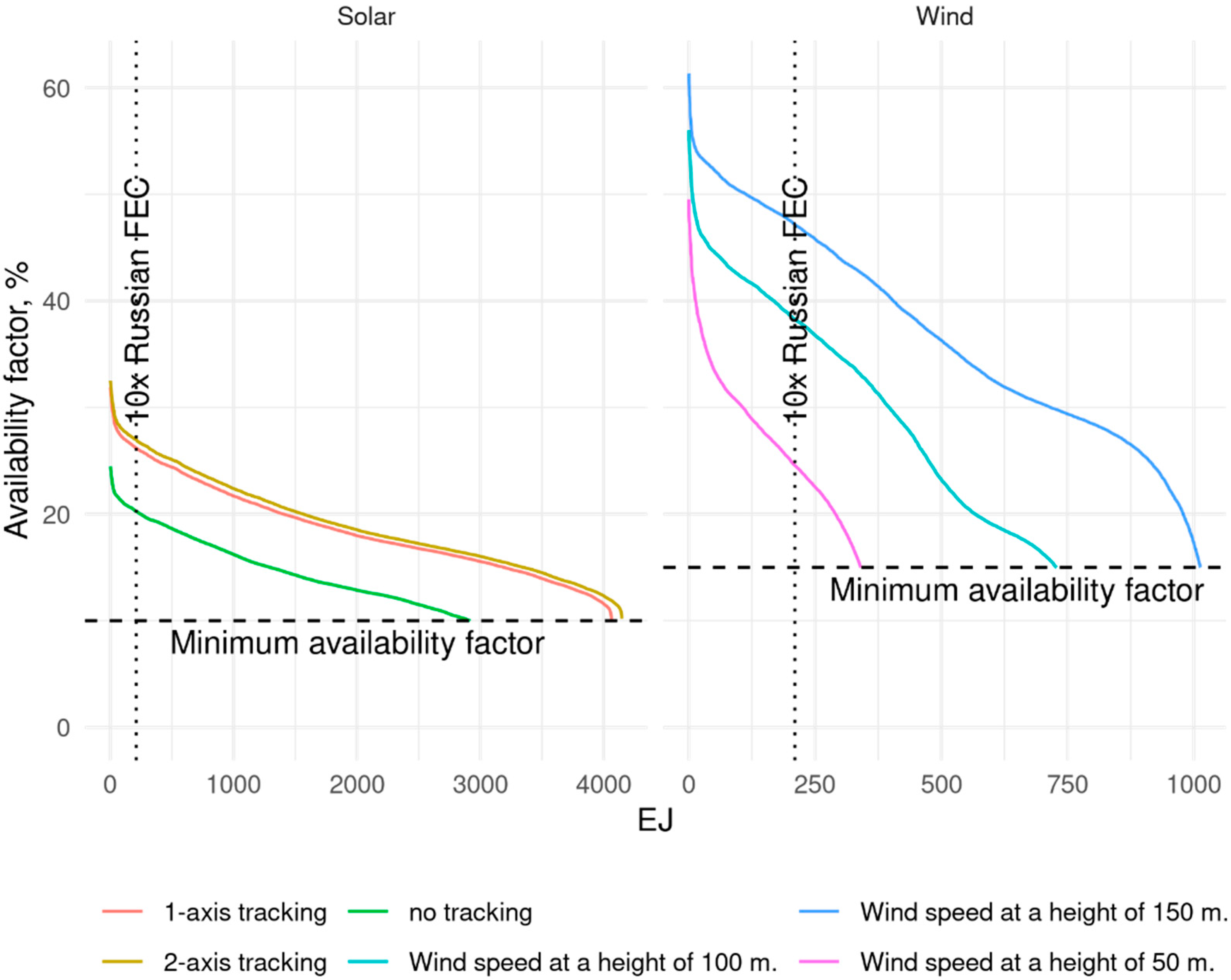

2.3. Solar and Wind Availability

2.4. Energy Storage

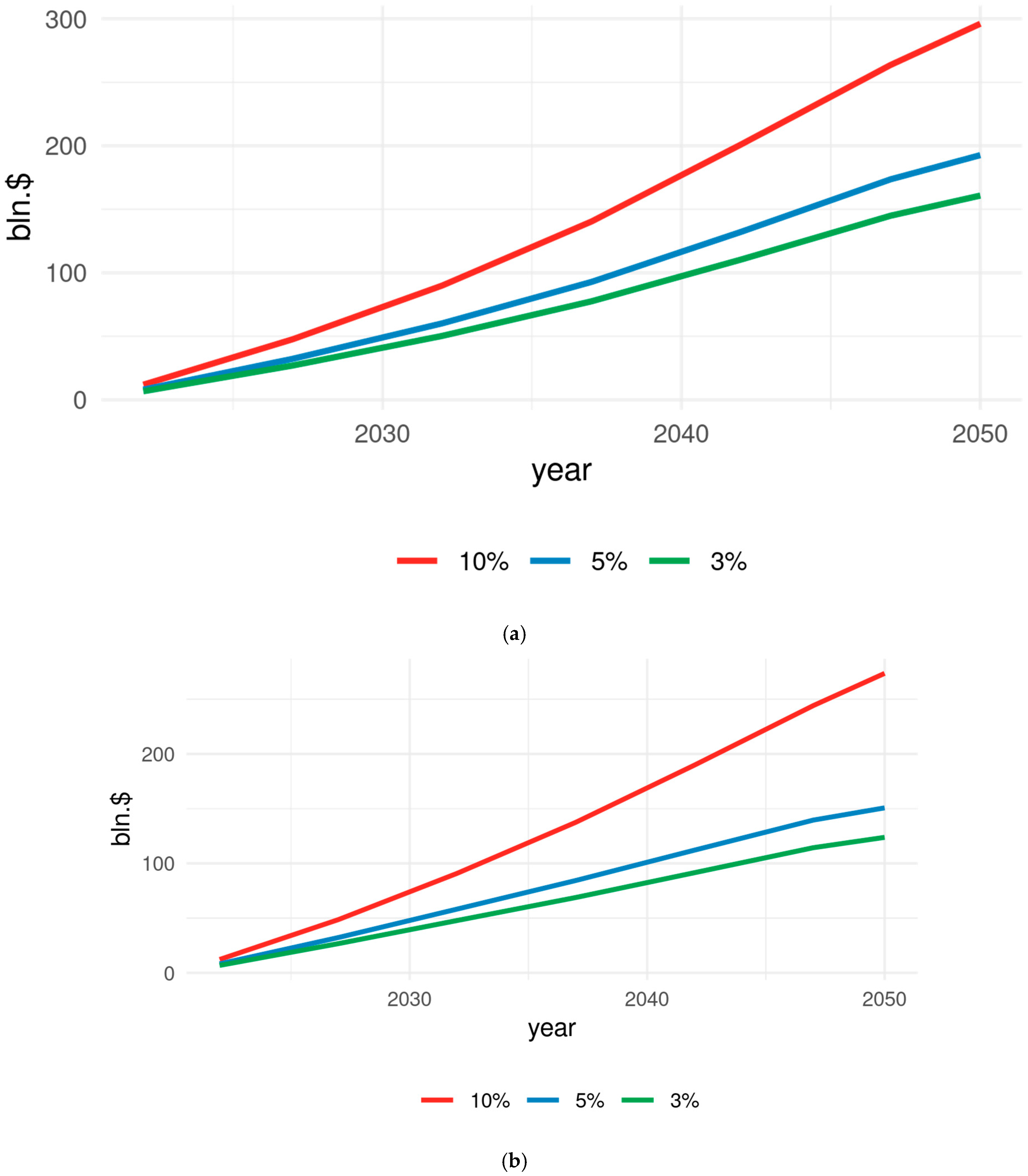

3. Results

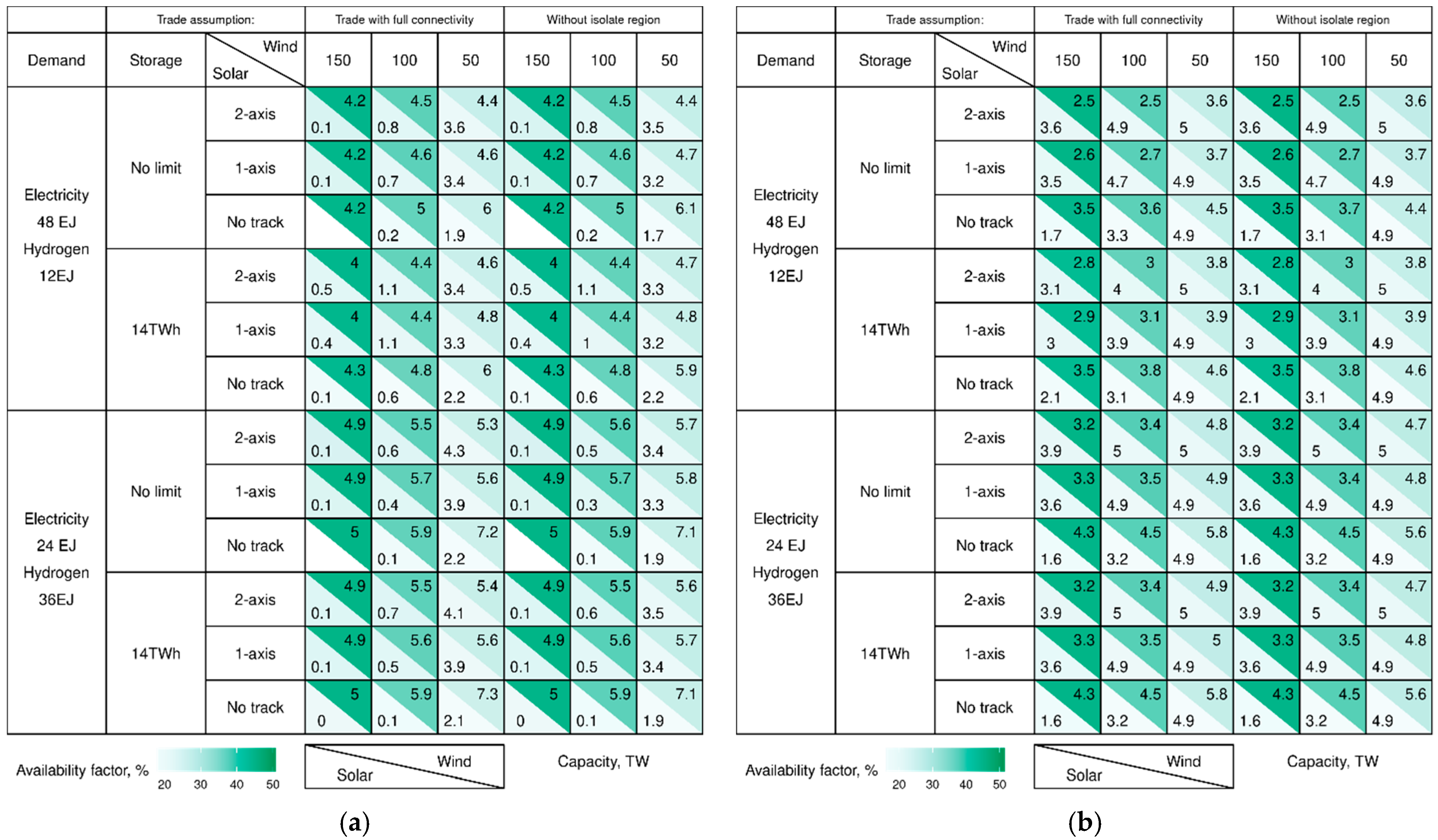

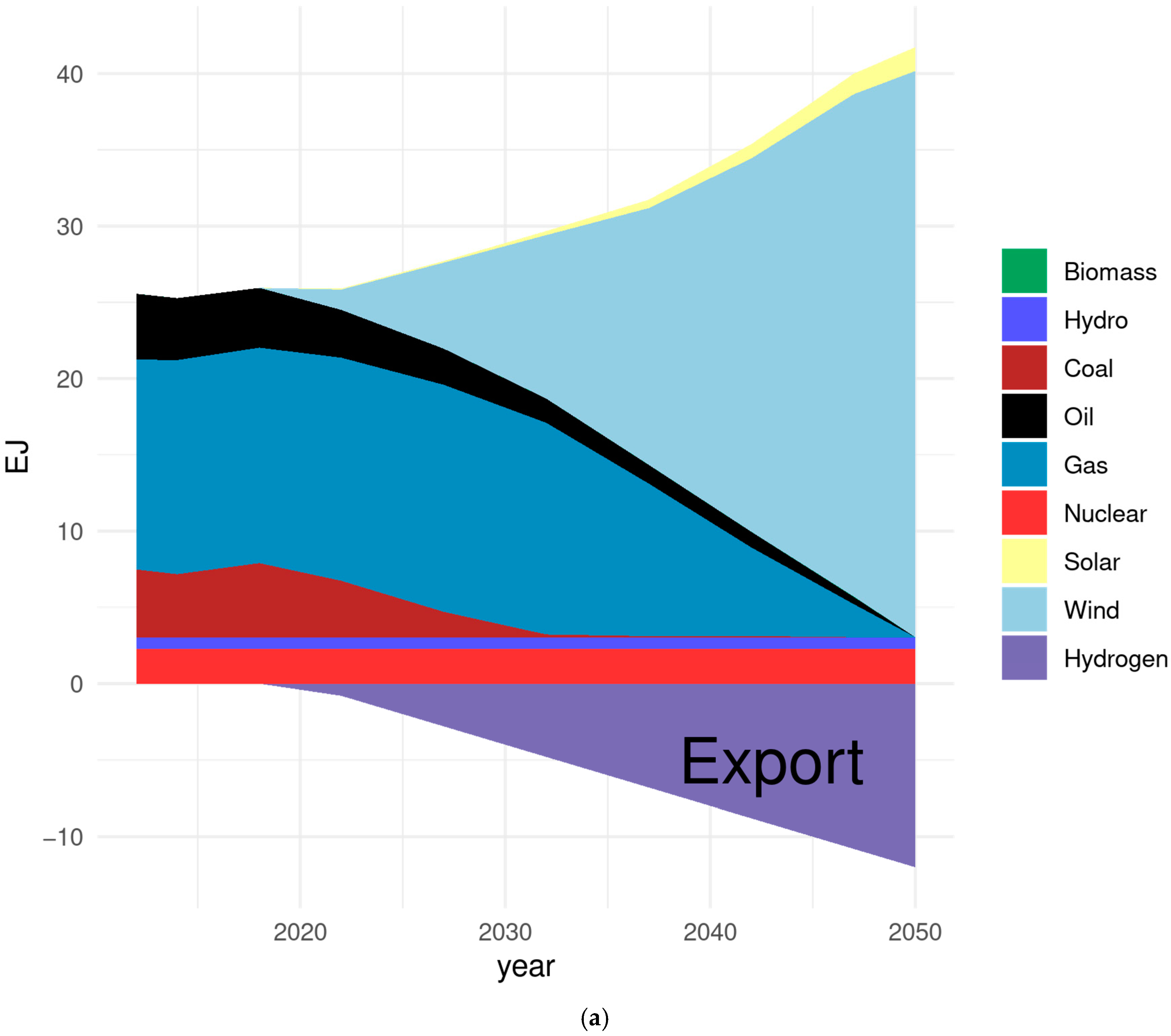

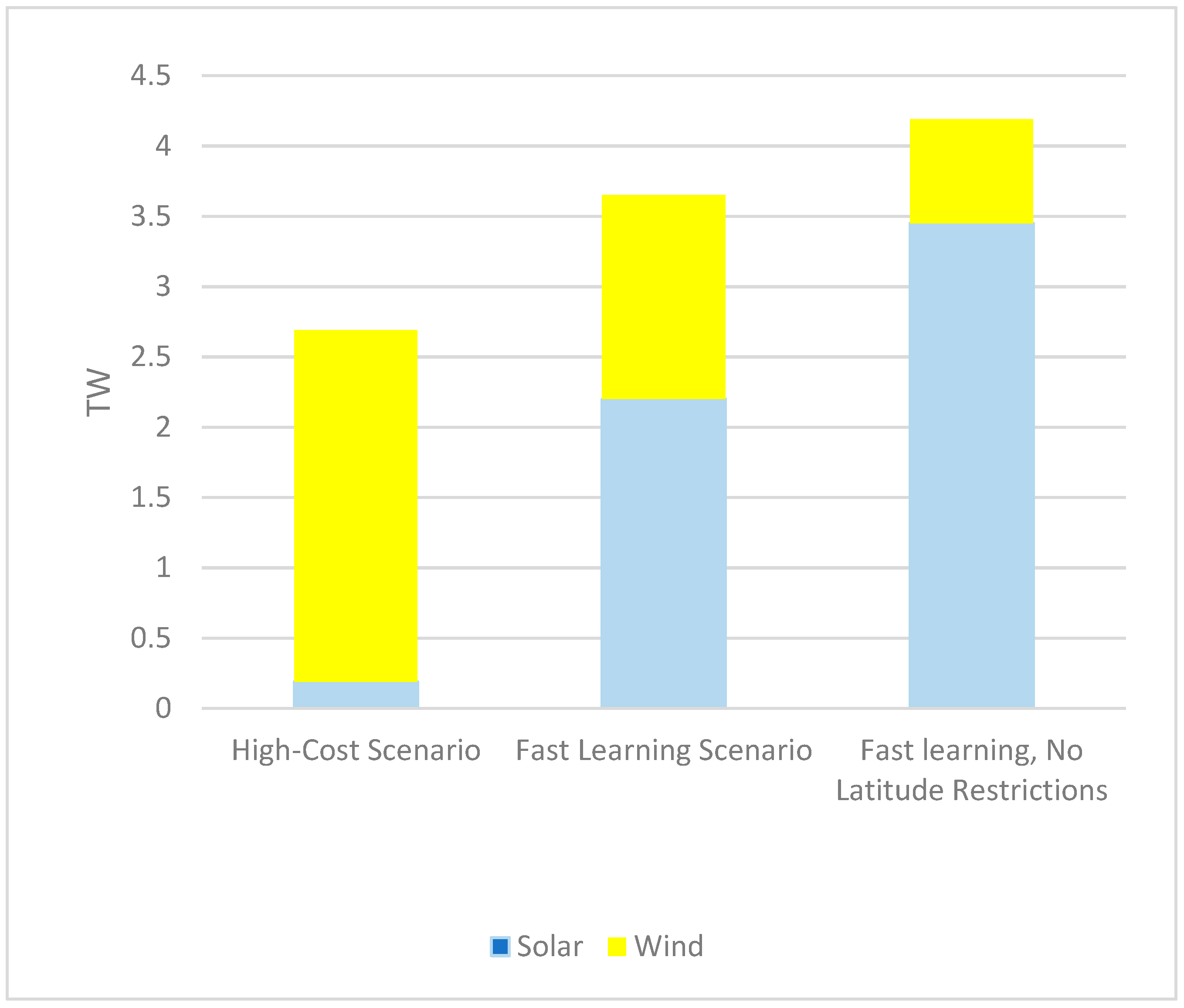

3.1. Feasibility Analysis

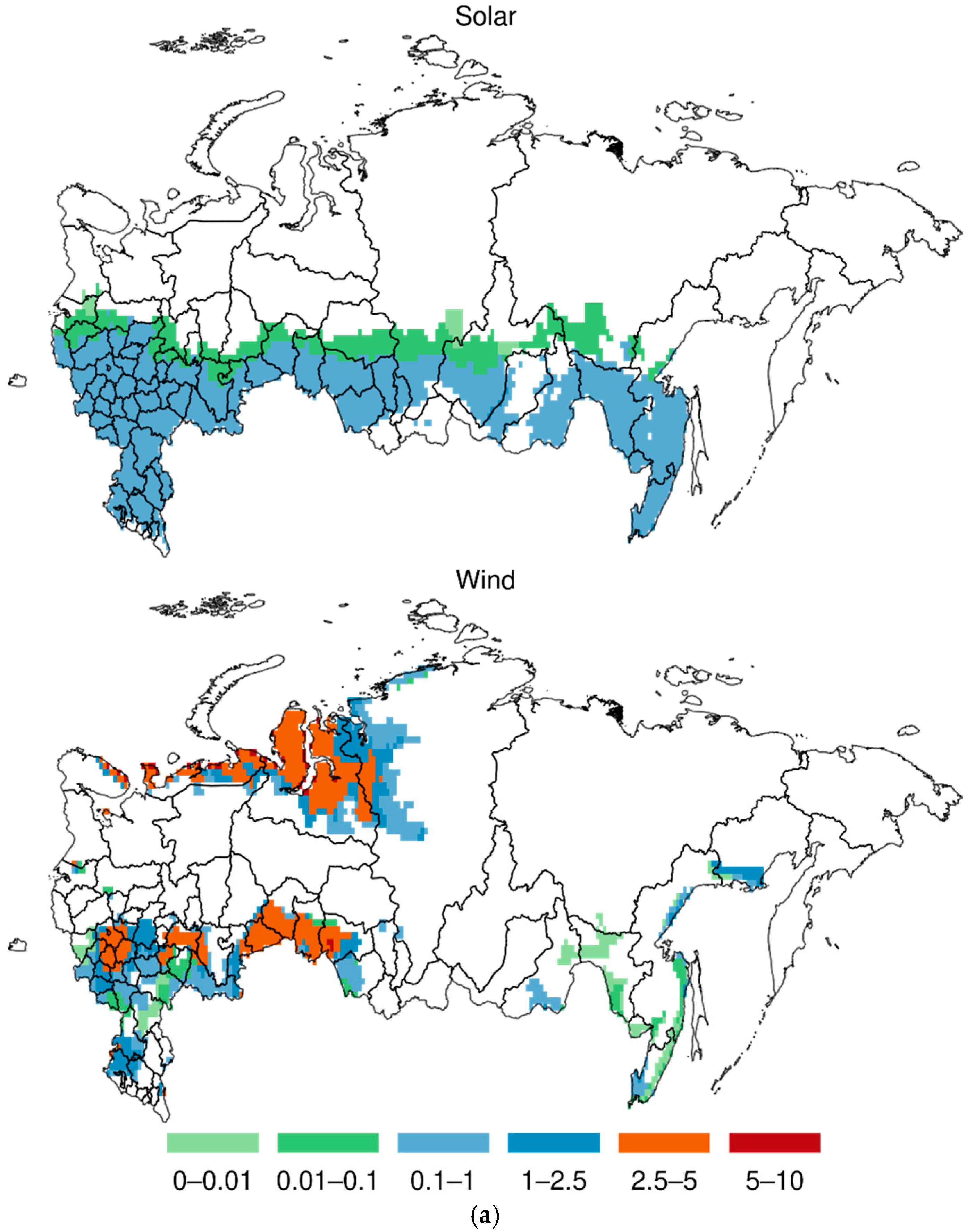

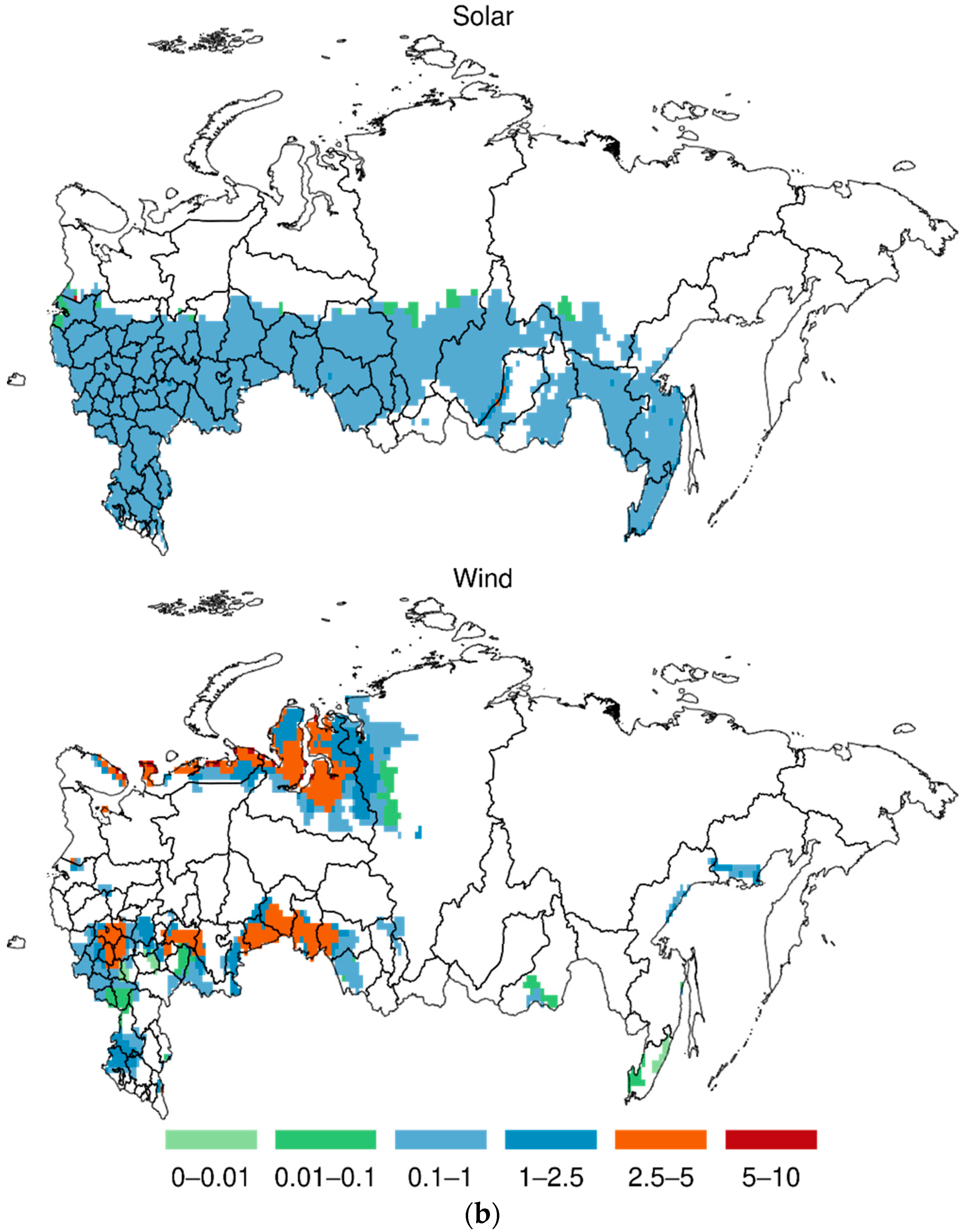

3.2. Geographic Distribution of Power Generation, Distribution System and Storage

3.3. Transitional Dynamics to a 100% Decarbonized Energy System

4. Discussion

Uses of Hydrogen and Excess Electricity

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

References

- IPCC. 2021: Summary for Policymakers. In Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Masson-Delmotte, V., Zhai, P., Pirani, A., Connors, S.L., Péan, C., Berger, S., Caud, N., Chen, Y., Goldfarb, L., Gomis, M.I., et al., Eds.; Cambridge University Press: Cambridge, UK, 2021. [Google Scholar]

- Brown, T.W.; Bischof-Niemz, T.; Blok, K.; Breyer, C.; Lund, H.; Mathiesen, B.V. Response to “Burden of proof: A comprehensive review of the feasibility of 100% renewable-electricity systems”. Renew. Sustain. Energy Rev. 2018, 92, 834–847. [Google Scholar] [CrossRef]

- Bogdanov, D.; Koskinen, O.; Aghahosseini, A.; Breyer, C. Integrated renewable energy based power system for Europe, Eurasia and MENA regions. In Proceedings of the 2016 International Energy and Sustainability Conference (IESC), Cologne, Germany, 30 June–1 July 2016; pp. 1–9. [Google Scholar]

- Bogdanov, D.; Farfan, J.; Sadovskaia, K.; Aghahosseini, A.; Child, M.; Gulagi, A.; Oyewo, A.S.; Barbosa, L.D.S.N.S.; Breyer, C. Radical transformation pathway towards sustainable electricity via evolutionary steps. Nat. Commun. 2019, 10, 1077. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bogdanov, D.; Ram, M.; Aghahosseini, A.; Gulagi, A.; Oyewo, A.S.; Child, M.; Caldera, U.; Sadovskaia, K.; Farfan, J.; Barbosa, L.D.S.N.S.; et al. Low-cost renewable electricity as the key driver of the global energy transition towards sustainability. Energy 2021, 227, 120467. [Google Scholar] [CrossRef]

- Hansen, K.; Breyer, C.; Lund, H. Status and perspectives on 100% renewable energy systems. Energy 2019, 175, 471–480. [Google Scholar] [CrossRef]

- Lugovoy, O.; Gao, S.; Gao, J.; Jiang, K. Feasibility study of China’s electric power sector transition to zero emissions by 2050. Energy Econ. 2021, 96, 105176. [Google Scholar] [CrossRef]

- Lugovoy, O.; Jyothiprakash, V.; Chatterjee, S.; Sharma, S.; Mukherjee, A.; Das, A.; Some, S.; Dinesha, D.L.; Das, N.; Bosu, P.; et al. Towards a Zero-Carbon Electricity System for India in 2050: IDEEA Model-Based Scenarios Integrating Wind and Solar Complementarity and Geospatial Endowments. Energies 2021, 14, 7063. [Google Scholar] [CrossRef]

- Sokolnikova, P.; Lombardi, P.; Arendarski, B.; Suslov, K.; Pantaleo, A.; Kranhold, M.; Komarnicki, P. Net-zero multi-energy systems for Siberian rural communities: A methodology to size thermal and electric storage units. Renew. Energy 2020, 155, 979–989. [Google Scholar] [CrossRef]

- Kozlova, M.; Collan, M. Modeling the effects of the new Russian capacity mechanism on renewable energy investments. Energy Policy 2016, 95, 350–360. [Google Scholar] [CrossRef]

- Hawken, P. (Ed.) Drawdown: The Most Comprehensive Plan Ever Proposed to Reverse Global Warming; Penguin Books: London, UK, 2017. [Google Scholar]

- Jacobson, M.Z.; Delucchi, M.A.; Bauer, Z.A.F. 100% Clean and Renewable Wind, Water, and Sunlight All-Sector Energy Roadmaps for 139 Countries of the World. Joule 2017, 1, 108–121. [Google Scholar] [CrossRef] [Green Version]

- Larson, E.; Greig, C.; Jenkins, J.; Mayfield, A.; Pascale, C.; Zhang, J.; Drossman, R.; Williams, S.; Pacala, R.; Socolow, E.J.; et al. Net-Zero America: Potential Pathways, Infrastructure, and Impacts; Interim Report; Princeton University: Princeton, NJ, USA, 2020. [Google Scholar]

- Vartiainen, E.; Breyer, C.; Moser, D.; Medina, E.R.; Busto, C.; Masson, G.; Bosch, E.; Jäger-Waldau, A. True Cost of Solar Hydrogen. Sol. RRL 2021, 5, 2100487. [Google Scholar] [CrossRef]

- Golub, A.; Lugovoy, O.; Potashnikov, V. Quantifying barriers to decarbonization of the Russian economy: Real options analysis of investment risks in low-carbon technologies. Clim. Policy 2019, 19, 716–724. [Google Scholar] [CrossRef]

- Laitner, J.; Lugovoy, O.; Potashnikov, V. Cost and Benefits of Deep Decarbonization in Russia. Econ. Policy 2020, 15, 86–105. [Google Scholar] [CrossRef]

- Safonov, G.; Potashnikov, V.; Lugovoy, O.; Safonov, M.; Dorina, A.; Bolotov, A. The low carbon development options for Russia. Clim. Chang. 2020, 162, 1929–1945. [Google Scholar] [CrossRef]

- Lugovoy, O.; Gao, S. MERRA-2 Subset for Evaluation of Renewables with Merra2ools R-Package: 1980–2020 Hourly, 0.5° lat × 0.625° lon Global Grid. 2021. Available online: https://datadryad.org/stash/our_platform (accessed on 8 January 2022).

- Vartiainen, E.; Masson, G.; Breyer, C.; Moser, D.; Medina, E.R. Medina: Impact of weighted average cost of capital, capital expenditure, and other parameters on future utility-scale PV levelised cost of electricity; Special Issue: EU PVSEC. Prog. Photovolt. Res. Appl. 2020, 28, 439–453. [Google Scholar] [CrossRef] [Green Version]

- IRENA. Renewable Power Generation Costs in 2020; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021; ISBN 978-92-9260-348-9. [Google Scholar]

- Kurtz, J.M.; Cader, T.; Ma, Z.; Saur, G.; Clark, P.L.; Mount, R.L.; Hammond, S.W. Sustainability, Feasibility, and Economics of a Fuel Cell-Powered Data Center. In Proceedings of the 2019 TechConnect World Innovation Conference, Boston, MA, USA, 17–19 June 2019; Available online: https://www.nrel.gov/docs/fy20osti/73604.pdf (accessed on 8 January 2022).

- Bistline, J.E. The importance of temporal resolution in modeling deep decarbonization of the electric power sector. Environ. Res. Lett. 2021, 16, 084005. [Google Scholar] [CrossRef]

- Lugovoy, O.; Potashnikov, V. EnergyRt: Energy Systems Modeling Toolbox in R. 2021. Available online: https://energyrt.org/. (accessed on 15 December 2021).

- Henry, C.L.; Eshraghi, H.; Lugovoy, O.; Waite, M.B.; DeCarolis, J.F.; Farnham, D.J.; Ruggles, T.H.; Peer, R.A.M.; Wu, Y.; de Queiroz, A.; et al. Promoting reproducibility and increased collaboration in electric sector capacity expansion models with community benchmarking and intercomparison efforts. Appl. Energy 2021, 304, 117745. [Google Scholar] [CrossRef]

- IRENA. Hydrogen from Renewable Power Technology Outlook for the Energy Transition. 2018. Available online: https://www.irena.org/-/media/files/irena/agency/publication/2018/sep/irena_hydrogen_from_renewable_power_2018.pdf (accessed on 9 October 2021).

- IMF. World Economic Outlook. Available online: https://www.imf.org/en/Publications/WEO/Issues/2021/07/27/world-economic-outlook-update-july-2021 (accessed on 10 October 2021).

- NREL. Land Use by System Technology. Available online: https://www.nrel.gov/analysis/tech-size.html (accessed on 10 January 2022).

- Peszko, G.; Van Der Mensbrugghe, D.; Golub, A.; Ward, J.; Marijs, C.; Schopp, A.; Rogers, J.; Midgley, A. Diversification and Cooperation in a Decarbonizing World: Climate Strategies for Fossil Fuel–Dependent Countries; World Bank Publications: Washington, DC, USA, 2020. [Google Scholar]

- Canadian Energy Research Institute. A Comprehensive Guide to Electricity Generation Options in Canada; Canadian Energy Research Institute: Calgary, AB, Canada, 2018; ISBN 1-927037-53-9. [Google Scholar]

- Carbon Disclosure Project. Available online: https://www.cdp.net/en/climate (accessed on 22 July 2021).

- IEA. Net Zero by 2050; IEA: Paris, France, 2020; Available online: https://www.iea.org/reports/net-zero-by-2050 (accessed on 6 July 2021).

- Rifkin, J. America 3.0. The Resilient Society: A Smart Third Industrial Revolution Infrastructure and The Recovery of The American Economy; TIR Consulting Group: Bethesda, MD, USA, 2021; Available online: https://www.rewiringamerica.org/policy/jobs-report (accessed on 3 October 2021).

- Lebot, B.; Weiland, M. Policies and Programs Critical for Greater Energy Efficiency. Econ. Policy 2020, 15, 148–167. [Google Scholar] [CrossRef]

- IEA. Hydrogen; IEA: Paris, France, 2020; Available online: https://www.iea.org/reports/hydrogen (accessed on 2 October 2021).

- IEA. The Future of Hydrogen: Report prepared by the IEA for the G20, Japan. In Seizing Today’s Opportunities; IEA: Paris, France, 2019. [Google Scholar]

- IRENA. Coalition for Action, Decarbonising End-Use Sectors: Practical Insights on Green Hydrogen; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021; ISBN 978-92-9260-346-5. [Google Scholar]

- IRENA. World energy transitions outlook: 1.5 °C pathway; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021. [Google Scholar]

- IRENA. Green Hydrogen Cost Reduction: Scaling Up Electrolysers to Meet the 1.5 °C Climate Goal; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Available online: https://cleantechnica.com/2021/12/11/solar-ammonia-in-a-climate-crisis-electrolysis-is-no-barrier-to-low-cost-renewable-ammonia/ (accessed on 9 December 2021).

- Hydrogen Use in EU Decarbonization Scenarios. Available online: https://ec.europa.eu/jrc/en/science-update/hydrogen-use-eu-decarbonisation-scenarios (accessed on 31 December 2021).

- Mitrova, T.; Melnikov, Y.; Chugunov, D. The Hydrogen Economy—A Path towards Low Carbon Development; SKOLKOVO Energy Centre, Moscow School of Management SKOLKOVO: Moscow, Russia, 2021. [Google Scholar]

- Reuters. Available online: https://www.reuters.com/business/energy/enel-eyes-potential-green-hydrogen-project-russia-2021-06-07/ (accessed on 10 June 2021).

- Available online: https://www.germanwatch.org/en/17961 (accessed on 9 December 2021).

- World Bank. The Changing Wealth of Nations 2021: Managing Assets for the Future; World Bank: Washington, DC, USA, 2021. [Google Scholar]

- Edwards, R. The Net Zero Transition and Offsetting of Carbon Intensity in Retail Investment Portfolios. In Forest Trends: Public-Private Finance Initiative; Forest Trends: Washington, DC, USA, 2021. [Google Scholar]

- European Commission. Proposal for a Regulation of the European Parliament and of the Council Establishing a Carbon Border Adjustment Mechanism; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- Makarov, I.; Besley, D.; Hasan, D.; Boratynski, J.; Chepeliev, M.; Golub, E.; Nemova, V.; Stepanov, I. Russia and Global Green Transition: Risks and Opportunities; World Bank: Washington, DC, USA, 2021. [Google Scholar]

- Brody, M.; Golub, A.; Potashnikov, V. The Effects of Increasing Population Granularity in PM2.5 Population-weighted Exposure and Mortality Risk Assessment. Environ. Health Perspect. 2021, 129, 127703. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technology | Cost | Technical Parameter |

|---|---|---|

| Solar PV | Investment cost—$825/kW, Fixed Operating and Maintenance (O&M)—$9.5/kW/year | Solar availability factor varies between 9–28% depending on location, and is estimated using Sandia’s plane-of-array model and algorithms for solar-array trackers 1 for a fixed tilted, 1-axis tracking system and 2-axis tracking system, with an operational life of 20 years, and is shown in the merra2ools package 2 |

| Wind Onshore | Investment cost $1050/kW, Fixed O&M—$27/kW/year | Wind availability factor can vary between 13% and 57% depending on station location, with precision data calculated using the merra2ools package, with an operational life of 30 years. Wind speeds for 100 m and 150 m were approximated from values at 10 m and 50 m. |

| Storage | $250/MWh investment cost | 10% loss during charging, operational life of 15 years |

| 500-kV HVDC transmission line | $367M per HVDC converter station in one direction, $0.87M per 1 km, for 2.4 GW | Losses vary between 2.5% and 7.2% depending upon distance between regions (Losses = 0.6% + 2.9% for every 1000 km). |

| Hydrogen electrolysis 3 | Fixed O&M, $18/kW/year, Investment cost of $900/kW/year | Efficiency of 51 kWh/kgH2, availability factor greater than 15%, with an operational life of 20 years |

| Indicator | 2018 | 2050 |

|---|---|---|

| GDP (bln constant 2018 US$) | 1744 | 4900 |

| Population (mln) | 146 | 146 |

| Living space, m2/person | 26 | 45 |

| Fossil fuel exports, EJ | 25 | 0 |

| Hydrogen exports EJ | 0 | 12 |

| Emission, MtCO2 | 1463 | 0 |

| Freight and Passenger transport demand, index % | 100 | 200 |

| Steel production, Mt | 71 | 128 |

| Non-energy fossil fuel demand, EJ | 4.6 | 4.6 |

| Parameter | Alternatives | Description |

|---|---|---|

| Demand | 1 | Total electricity demand is 48 EJ, 70% is critical demand, flexible portion is 30%. Hydrogen demand is 12 EJ |

| 2 | Total electricity demand is 24 EJ, 70% is critical demand, flexible portion is 30%. Hydrogen demand is 36 EJ | |

| Wind | 1 | Wind speed at 150 m height |

| 2 | Wind speed at 100 m height | |

| 3 | Wind speed at 50 m height | |

| Solar | 1 | 2-axis solar tracking |

| 2 | 1-axis solar tracking | |

| 3 | No solar tracking | |

| Storage | 1 | Unlimited |

| 2 | No more than 14 TWh (23–29% of average daily consumption) | |

| Trade | 1 | Trade with full connectivity across all regions of RES |

| 2 | Without isolated regions |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Potashnikov, V.; Golub, A.; Brody, M.; Lugovoy, O. Decarbonizing Russia: Leapfrogging from Fossil Fuel to Hydrogen. Energies 2022, 15, 683. https://doi.org/10.3390/en15030683

Potashnikov V, Golub A, Brody M, Lugovoy O. Decarbonizing Russia: Leapfrogging from Fossil Fuel to Hydrogen. Energies. 2022; 15(3):683. https://doi.org/10.3390/en15030683

Chicago/Turabian StylePotashnikov, Vladimir, Alexander Golub, Michael Brody, and Oleg Lugovoy. 2022. "Decarbonizing Russia: Leapfrogging from Fossil Fuel to Hydrogen" Energies 15, no. 3: 683. https://doi.org/10.3390/en15030683