Long-Term Planning of Electrical Distribution Grids: How Load Uncertainty and Flexibility Affect the Investment Timing

Abstract

:1. Introduction

2. Methodology and Related Literature

3. The Model

3.1. Problem Statement

3.2. Main Assumptions

3.3. What Value for the Option to Reinforce the Network?

- If , the DSO decides to continue with the actual configuration of the grid

- If , the DSO takes the decision to reinforce by adding an additional feeder

- i.

- The maximum power for which the reinforcement of the electric distribution grid is optimal is the positive root of the following second-order equation:with

- ii.

- The value of the option to reinforce the network with a new feeder is determined as follows:

4. Results and Discussion

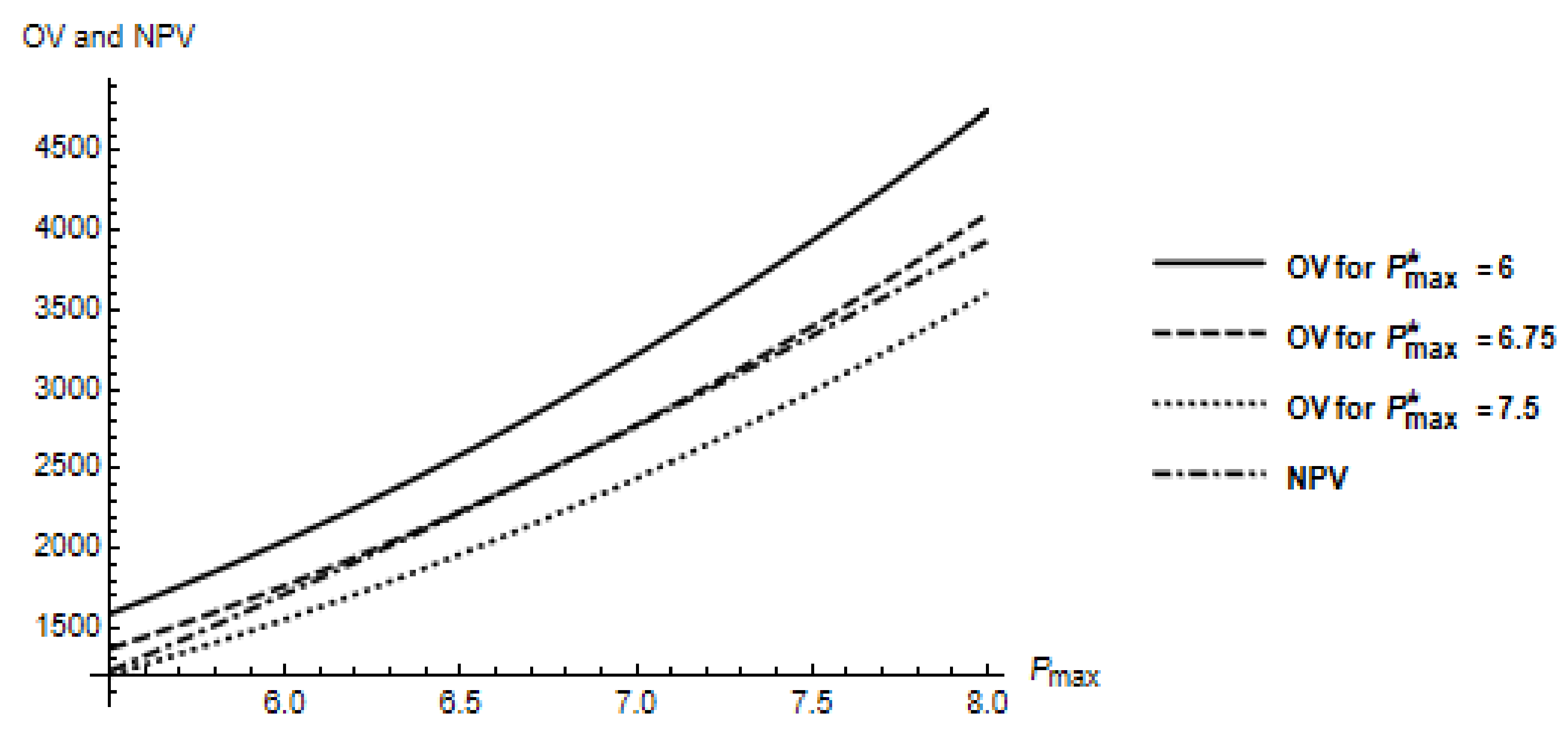

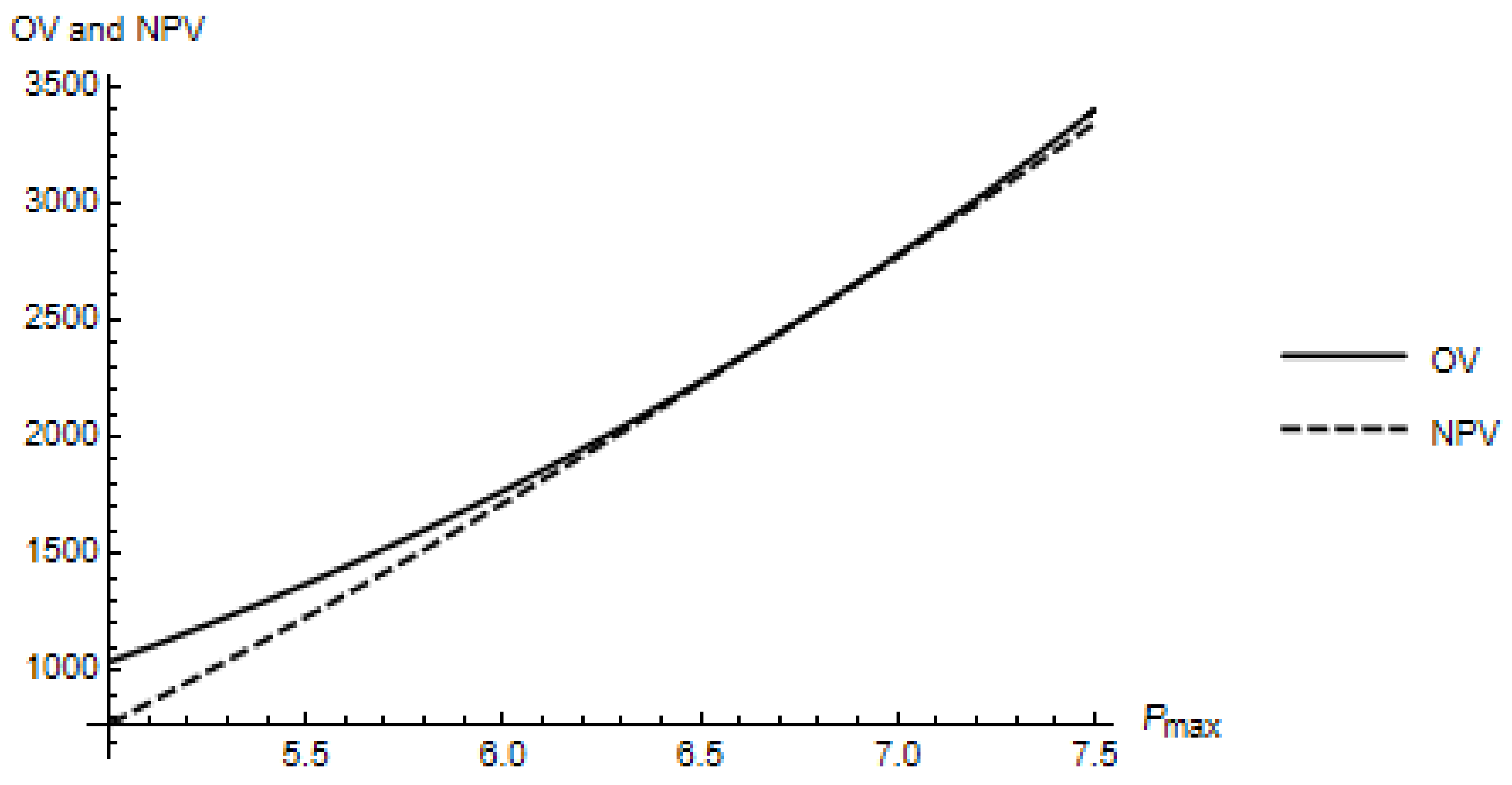

4.1. The Role of Load Uncertainty and Time Flexibility

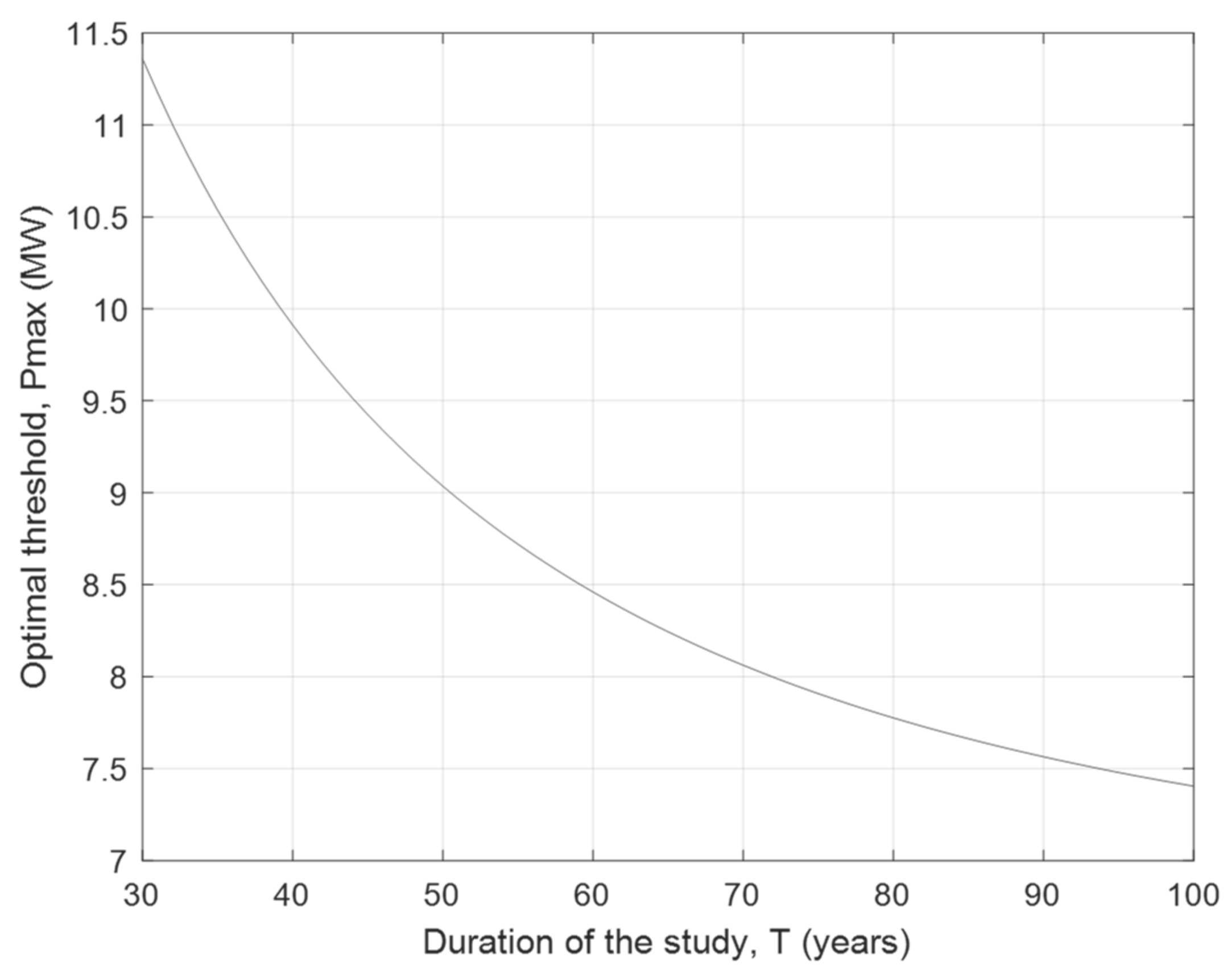

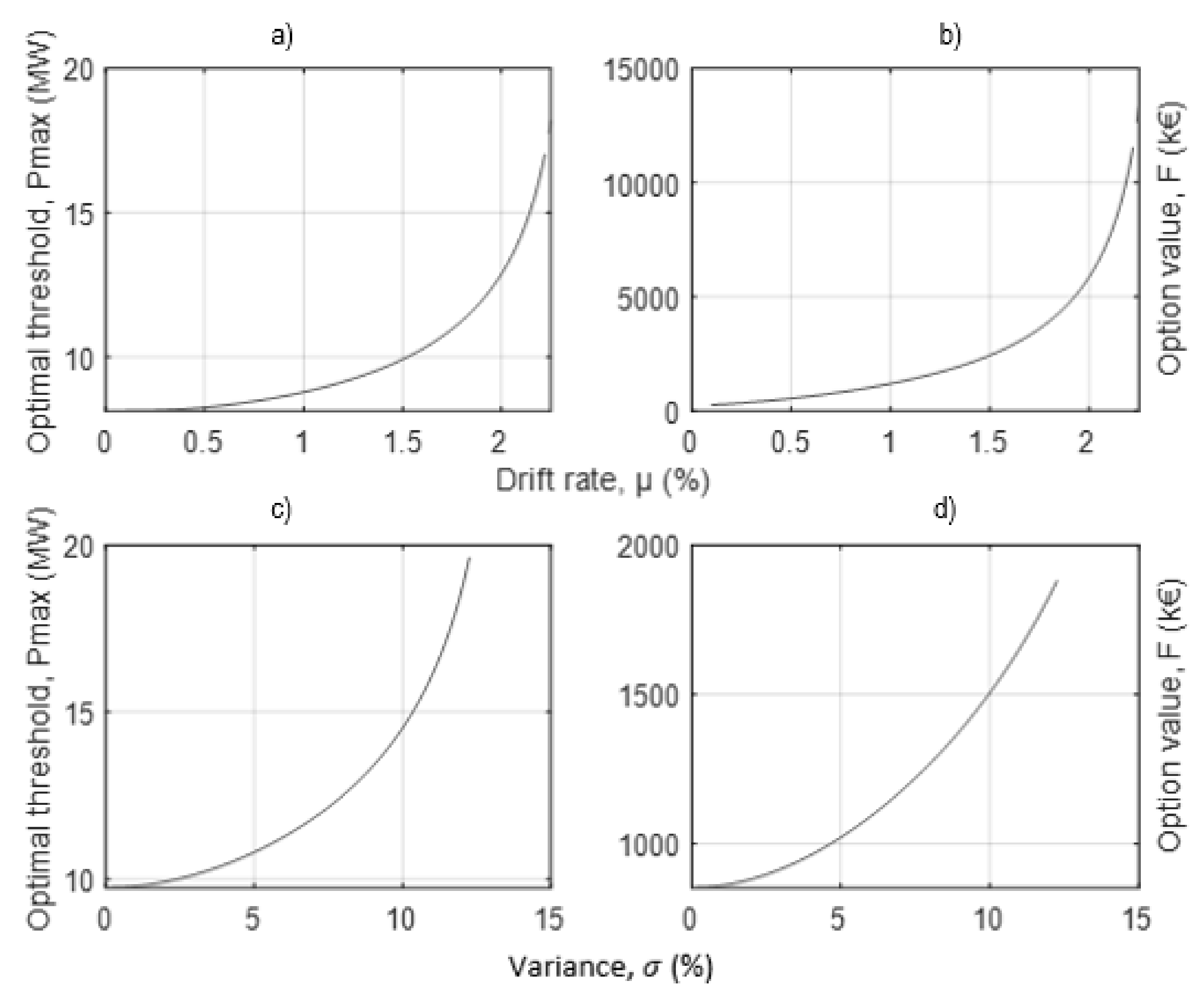

4.2. Impact of Load Uncertainty and Growth Rate on the Long-Term Distribution Network Planning

4.3. Impact of Electric Vehicles Integration on Load Growth and Investment Decision

4.4. Impact of Economic Parameters (Discount Rate, Costs) on the Long-Term Distribution Network Planning

4.5. Impact of Technical Conditions on the Long-Term Distribution Network Planning

4.6. Impact of Characteristics and Technologies of Cables on Power Losses and Environmental Issues

5. Conclusions

5.1. Study Contribution and Implications

5.2. Study Limitations

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

Appendix C

Appendix D

Appendix E

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technical Parameters | Unit | |

|---|---|---|

| T | ∞ (*) | Year |

| 6 | W | |

| 0.206 | Ω/km | |

| U | 20 | V |

| μ | 1.5 | % |

| 2 | % | |

| - | ||

| Failure/year/100 km | ||

| km | ||

| 4000 | hour | |

| hour | ||

| - | ||

| 0.92 | - | |

| Economic Parameters | Unit | |

| 120 | €/km | |

| Cost of overhead line | €/km | |

| 204 | €/W | |

| 10 | €/Wh | |

| 1 | €/W | |

| 4.5 | % | |

Appendix F

References

- ENEDIS. Description Physique du Réseau Public. NOI-RES_07E.2017. Available online: https://www.enedis.fr/sites/default/files/Enedis-NOI-RES_07E.pdf (accessed on 17 July 2022).

- CIRED. Reduction of Technical and Non-Technical Losses in Distribution Networks. ISSN 2684-1088. 2019. Available online: http://www.cired.net/cired-working-groups/technical-and-non-technical-losses (accessed on 17 July 2022).

- Kozlova, M. Real option valuation in renewable energy literature: Research focus, trends and design. Renew. Sustain. Energy Rev. 2017, 80, 180–196. [Google Scholar] [CrossRef]

- Dixit, A.K.; Pindyck, R.S. Investment under Uncertainty; Princeton University Press: Princeton, NJ, USA, 1994. [Google Scholar]

- Samper, M.E.; Vargas, A. Investment decisions in distribution networks under uncertainty with distributed generation—Part i: Model formulation. IEEE Trans. Power Syst. 2013, 28, 2331–2340. [Google Scholar] [CrossRef]

- Schachter, J.A.; Mancarella, P. A critical review of Real Options thinking for valuing investment flexibility in Smart Grids and low carbon energy systems. Renew. Sustain. Energy Rev. 2016, 56, 261–271. [Google Scholar] [CrossRef]

- Gouin, V.; Alvarez-Herault, M.C.; Raison, B. Stochastic integration of demand response and reconfiguration in distribution network expansion planning. IET Gener. Transm. Distrib. 2018, 12, 4536–4545. [Google Scholar] [CrossRef]

- Mehrjerdi, H.; Hemmati, R. Wind-hydrogen storage in distribution network expansion planning considering investment deferral and uncertainty. Sustain. Energy Technol. Assess. 2020, 39, 100687. [Google Scholar] [CrossRef]

- Guerra, M.; Nunes, C.; Oliveira, C. Exit option for a class of profit functions. Int. J. Comput. Math. 2017, 94, 2178–2193. [Google Scholar] [CrossRef]

- Lassila, J.; Verho, P.; Kaipia, T.; Kivikko, K.; Lohjala, J. A Comparison of the Electricity Distribution Investment Strategies. In Proceedings of the 19th International Conference on Electricity Distribution, Vienna, Austria, 21–24 May 2007. [Google Scholar]

- Silvestro, F.; Pilo, F.; Heymann, F.; Alvarez-Herault, M.C.; Braun, M.; Araneda, J.C.; Taylor, J. Review of Transmission and Distribution Investment Decision Making Processes under Increasing Energy Scenario Uncertainty. In Proceedings of the 25th International Conference on Electricity Distribution, Madrid, Spain, 3–6 June 2019. [Google Scholar]

- Liao, H. Review on distribution network optimization under uncertainty. Energies 2019, 12, 3369. [Google Scholar] [CrossRef] [Green Version]

- Liu, Y.; Zhou, H. Distribution Network Planning Considering DG Under Uncertainty. In Proceedings of the 3rd International Conference on Electrical and Information Technologies for Rail Transportation, Changsha, China, 20–22 October 2017; Springer: Singapore, 2018; pp. 79–87. [Google Scholar]

- Liu, Y.; Wang, M.; Liu, X.; Xiang, Y. Evaluating investment strategies for distribution networks based on yardstick competition and DEA. Electr. Power Syst. Res. 2019, 174, 105868. [Google Scholar] [CrossRef]

- Myers, S. Critical Insight into the First Introduction of the Concept of the Real Options. J. Financ. Econ. 1977, 5. [Google Scholar]

- Trigeorgis, L. Real Options and Interactions with Financial Flexibility. Financ. Manag. 1993, 22, 202–224. [Google Scholar] [CrossRef]

- Abadie, L.M.; Chamorro, J.M. Valuing expansions of the electricity transmission network under uncertainty: The binodal case. Energies 2011, 4, 1696–1727. [Google Scholar] [CrossRef]

- Kucsera, D.; Rammerstorfer, M. Regulation and grid expansion investment with increased penetration of renewable generation. Resour. Energy Econ. 2014, 37, 184–200. [Google Scholar] [CrossRef]

- Pringles, R.; Olsina, F.; Garcés, F. Real option valuation of power transmission investments by stochastic simulation. Energy Econ. 2015, 47, 215–226. [Google Scholar] [CrossRef]

- Henao, A.; Sauma, E.; Reyes, T.; Gonzalez, A. What is the value of the option to defer an investment in Transmission Expansion Planning? An estimation using Real Options. Energy Econ. 2017, 65, 194–207. [Google Scholar] [CrossRef]

- Loureiro, M.V.; Schell, K.R.; Claro, J.; Fischbeck, P. Renewable integration through transmission network expansion planning under uncertainty. Electr. Power Syst. Res. 2018, 165, 45–52. [Google Scholar] [CrossRef]

- Buzarquis, E.; Blanco, G.A.; Olsina, F.; Garcés, F.F. Valuing Investments in Distribution Networks with DG under Uncertainty. In Proceedings of the 2010 IEEE/PES Transmission and Distribution Conference and Exposition: Latin America (T&D-LA), Sao Paulo, Brazil, 8–10 November 2011. [Google Scholar]

- Von Haebler, J.; Osthues, M.; Rehtanz, C.; Blanco, G. Investment strategies as a portfolio of real options for distribution system planning under uncertainty. In Proceedings of the IEEE Grenoble Conference, Grenoble, France, 16–20 June 2013; pp. 1–6. [Google Scholar]

- Schachter, J.A.; Mancarella, P.; Moriarty, J.; Shaw, R. Flexible investment under uncertainty in smart distribution networks with demand side response: Assessment framework and practical implementation. Energy Policy 2016, 97, 439–449. [Google Scholar] [CrossRef]

- Ma, Y.; Verbič, G.; Chapman, A.C. Valuation of compound real options for co-investment in residential battery systems. Appl. Energy 2022, 318, 119111. [Google Scholar] [CrossRef]

- Prettico, G.; Flammini, M.G.; Andreadou, N.; Vitiello, S.; Fulli, G.; Masera, M. Distribution System Operator Observatory 2020; An in-depth look on distribution grids in Europe, JRC Science for Policy Report; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Alvarez-Hérault, M.C.; Gouin, V.; Chardin-Segui, T.; Malot, A.; Coignard, J.; Raison, B.; Coulet, J. Planification des Réseaux Electriques de Distribution: Évolution des Méthodes et Outils Numériques pour la Transition Energétique; Collection Energie; ISTE Group: London, UK, 2022; 476p. [Google Scholar]

- ENEDIS; ADEeF. Valorisation Économique des Smart Grids Contribution des Gestionnaires de Réseau Public de Distribution. 2017. Available online: www.enedis.fr (accessed on 17 July 2022).

- Chauhan, A.; Rajvanshi, S. Non-Technical Losses in power system: A review. In Proceedings of the International Conference on Power, Energy and Control, ICPEC, Dindigul, India, 6–8 February 2013; pp. 558–561. [Google Scholar] [CrossRef]

- Dixon, J.; Bell, K. Electric vehicles: Battery capacity, charger power, access to charging and the impacts on distribution networks. eTransportation 2020, 4, 100059. [Google Scholar] [CrossRef]

- Open Data Réseaux Énergies (ODRÉ). (2001–2019). Gross Annual Electricity Consumption Peaks 2020 [Data Set]. Available online: https://opendata.reseaux-energies.fr/ (accessed on 17 July 2022).

- CRE. Les Cadres Réglementaire, Normatif et Contractuel. 2016. Available online: https://www.cre.fr (accessed on 17 July 2022).

- Merton, R. Option Pricing When Underlying Stock Returns Are Discontinuous. J. Financ. Econ. 1976, 3, 125–144. [Google Scholar] [CrossRef] [Green Version]

- IEA. Global EV Outlook. 2019. Available online: https://www.iea.org/reports/global-ev-outlook-2019 (accessed on 17 July 2022).

- Gough, M.; Santos, S.F.; Javadi, M.; Castro, R.; Catalão, J.P.S. Prosumer flexibility: A comprehensive state-of-the-art review and scientometric analysis. Energies 2020, 13, 2710. [Google Scholar] [CrossRef]

- Bojnec, Š.; Križaj, A. Electricity Markets during the Liberalization: The Case of a European Union Country. Energies 2021, 14, 4317. [Google Scholar] [CrossRef]

- Bočkarjova, M.; Andersson, G. Transmission line conductor temperature impact on state estimation accuracy. In Proceedings of the IEEE Lausanne POWERTECH, Lausanne, Switzerland, 1–5 July 2007; pp. 701–706. [Google Scholar]

- Jones, C.; McManus, M.C. Life-cycle assessment of 11 kV electrical overhead lines and underground cables. J. Clean. Prod. 2010, 18, 1464–1477. [Google Scholar]

- RTE. eCO2mix Indicators 2020 [Data Set]. Available online: https://www.rte-france.com/en/eco2mix/key-figures (accessed on 17 July 2022).

- RTE. Emission de CO2 par kWh d’Electricité Produite en France. 2020. Available online: https://www.rte-france.com/eco2mix/les-emissions-de-co2-par-kwh-produit-en-france (accessed on 17 July 2022).

| Technical Parameters | Unit | |

|---|---|---|

| t | Time index | year |

| Subtime index of t | hour | |

| T | Time horizon | Year |

| k | k = {wr, r} wr: without reinforcement, r: with reinforcement | - |

| Maximum active power of the HV/MV substation at time t | W | |

| i | Feeder index | |

| Module of the maximum current at time t through the feeder i for strategy k | A | |

| Linear resistance of feeder i for strategy k | Ω/km | |

| Length of feeder i for strategy k | km | |

| Power losses in feeder i for strategy k at time t | W | |

| U | Nominal phase-to-phase voltage of the MV network | V |

| Maximum apparent power of the customer connected to feeder i for strategy k at time t | VA | |

| Maximum active power of the customer connected to feeder i for strategy k at time t | W | |

| ) | Apparent power of the HV/MV substation at time | VA |

| ) | Active power of the HV/MV substation at time | W |

| Average power of the HV/MV substation at time t | W | |

| μ | Growth rate of maximum power | % |

| Volatility | % | |

| Constant depending on the conductor type, length, and voltage for feeder i, strategy k | Ω/V2 | |

| Power ratio of feeder i for strategy k | - | |

| Respectively underground and overhead feeder failure rate | Failure/year/100 km | |

| Respectively underground and overhead length of feeder i for strategy k | km | |

| Equivalent maximum power runtime | hour | |

| Average power outage duration for feeder i for strategy k | hour | |

| Number of MV feeders of the HV/MV transformer for strategy k | - | |

| Net present value of the total discount cost for strategy k | € | |

| Power factor of the customer (assumed constant) | - | |

| Economic Parameters | Unit | |

| Cost of underground line (including the trench) | €/km | |

| Cost of overhead line | €/km | |

| Cost of peak power losses | €/W | |

| Cost of energy not supplied | €/Wh | |

| Cost of power outage | €/W | |

| Discount rate | % | |

| Annual cost of power losses for strategy k | € | |

| Annual cost of power cut due to outages | € | |

| Annual cost of the energy not delivered to the customers due to outages | € | |

| Operational expenditure of strategy k | € | |

| Test Name | Test Statistic | p-Value |

|---|---|---|

| Anderson–Darling Test | 0.2153 | 0.8477 |

| Cramer–Von Mises Test | 0.0291 | 0.8591 |

| Shapiro–Wilk Test | 0.9675 | 0.7013 |

| Shapiro–Francia Test | 0.9743 | 0.7589 |

| Jarque–Bera Test | 0.7724 | 0.6796 |

| DAgostino and Pearson Test | 0.7692 | 0.6807 |

| Project Valuation in Continuous Time Framework | Symbol | Unit | Value |

|---|---|---|---|

| Deterministic Case (breakeven) | |||

| Investment trigger | MW | 6 | |

| NPV | NPVd | k€ | 1661.80 |

| Expected time to invest | Td | years | 0 |

| Deterministic Case (optimal) | |||

| Investment trigger | MW | 6.67 | |

| NPV | NPV** | k€ | 1705.71 |

| Expected time to invest | T** | years | 5.8 |

| GBM Case | |||

| Investment trigger | MW | 6.75 | |

| NPV | NPV* | k€ | 2347.58 |

| Expected time to invest | T* | years | 7.99 |

| Option value to wait constant (A) | A | k€ | 9.36 |

| Current max power for reference | (0) | MW | 6 |

| Conductor Section (mm2) | Cable Resistance (Ω/km) |

|---|---|

| 95 Alu | 0.32 |

| 150 Alu | 0.206 |

| 240 Alu | 0.125 |

| 240 Cu | 0.075 |

| Variable | Average Change | Standard Deviation | Relative Change (%) |

|---|---|---|---|

| Discount Rate (R) | 0.38% | 0.31% | 8.4% |

| Drift Rate (µ) | 0.44% | 0.30% | 29.3% |

| Investment (I) | 364 k€ | 48.6 k€ | 15.9% |

| Cable resistance () | 0.09 Ω/km | 0.04 Ω/km | 43.7% |

| Power Factor (cos φ) | 0.13 | 0.028 | 14.1% |

| Equivalent maximum power runtime () | 882 h | 350 h | 22.1% |

| Cost of power losses () | 24.1 €/kW | 13.5 €/kW | 12% |

| Cost of non-distributed energy () | 2.12 €/kWh | 0.74 €/kWh | 27% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Alvarez-Herault, M.-C.; Dib, J.-P.; Ionescu, O.; Raison, B. Long-Term Planning of Electrical Distribution Grids: How Load Uncertainty and Flexibility Affect the Investment Timing. Energies 2022, 15, 6084. https://doi.org/10.3390/en15166084

Alvarez-Herault M-C, Dib J-P, Ionescu O, Raison B. Long-Term Planning of Electrical Distribution Grids: How Load Uncertainty and Flexibility Affect the Investment Timing. Energies. 2022; 15(16):6084. https://doi.org/10.3390/en15166084

Chicago/Turabian StyleAlvarez-Herault, Marie-Cécile, Jean-Pierre Dib, Oana Ionescu, and Bertrand Raison. 2022. "Long-Term Planning of Electrical Distribution Grids: How Load Uncertainty and Flexibility Affect the Investment Timing" Energies 15, no. 16: 6084. https://doi.org/10.3390/en15166084