Green Credit of China’s Coal Power Enterprises during Green Transformation: A Tripartite Evolutionary Game Analysis

Abstract

:1. Introduction

2. Literature Review

3. The Evolutionary Game Model

3.1. Assumptions

3.2. Model Analysis

3.2.1. Expected Return Function

3.2.2. Equilibrium Point Solution

3.3. Asymptotic Stability Analysis

3.3.1. Asymptotic Stability Analysis of Government

3.3.2. Asymptotic Stability Analysis of Coal Power Enterprises

3.3.3. Asymptotic Stability Analysis of Banks

4. Equilibrium Analysis

4.1. Game Equilibrium Point Analysis

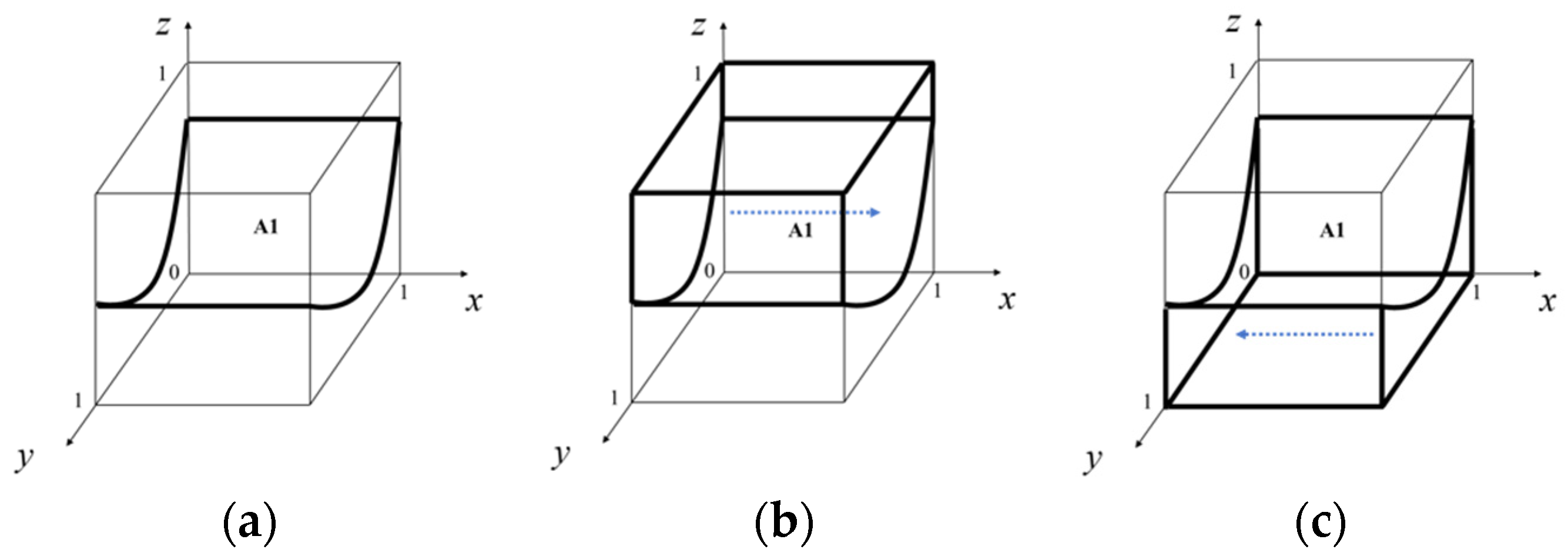

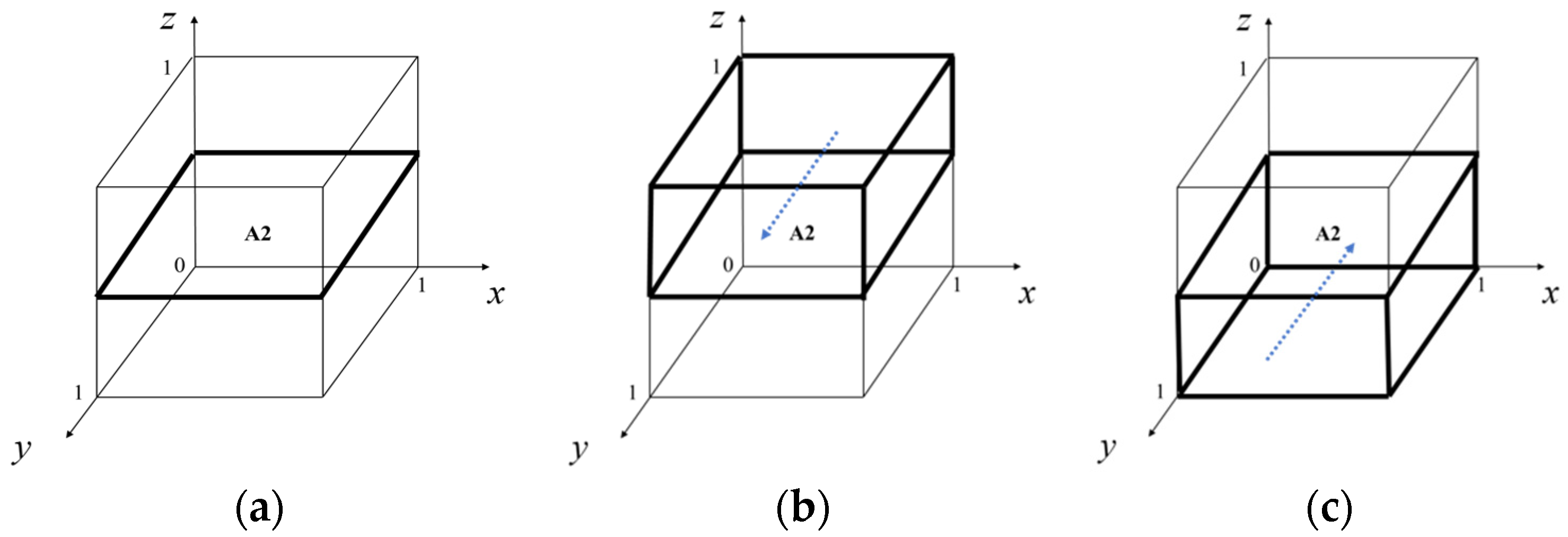

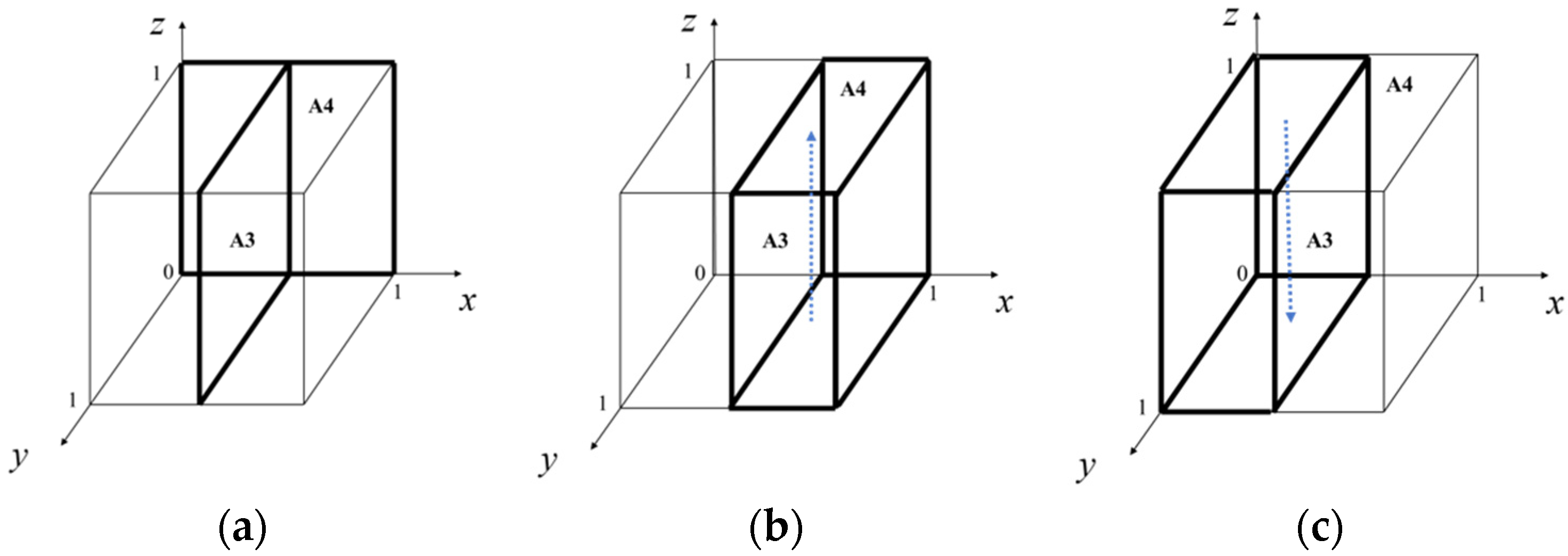

4.2. Evolutionary Path Analysis

5. Numerical Simulations

5.1. Basic Scenario

5.2. Sensitivity Analysis

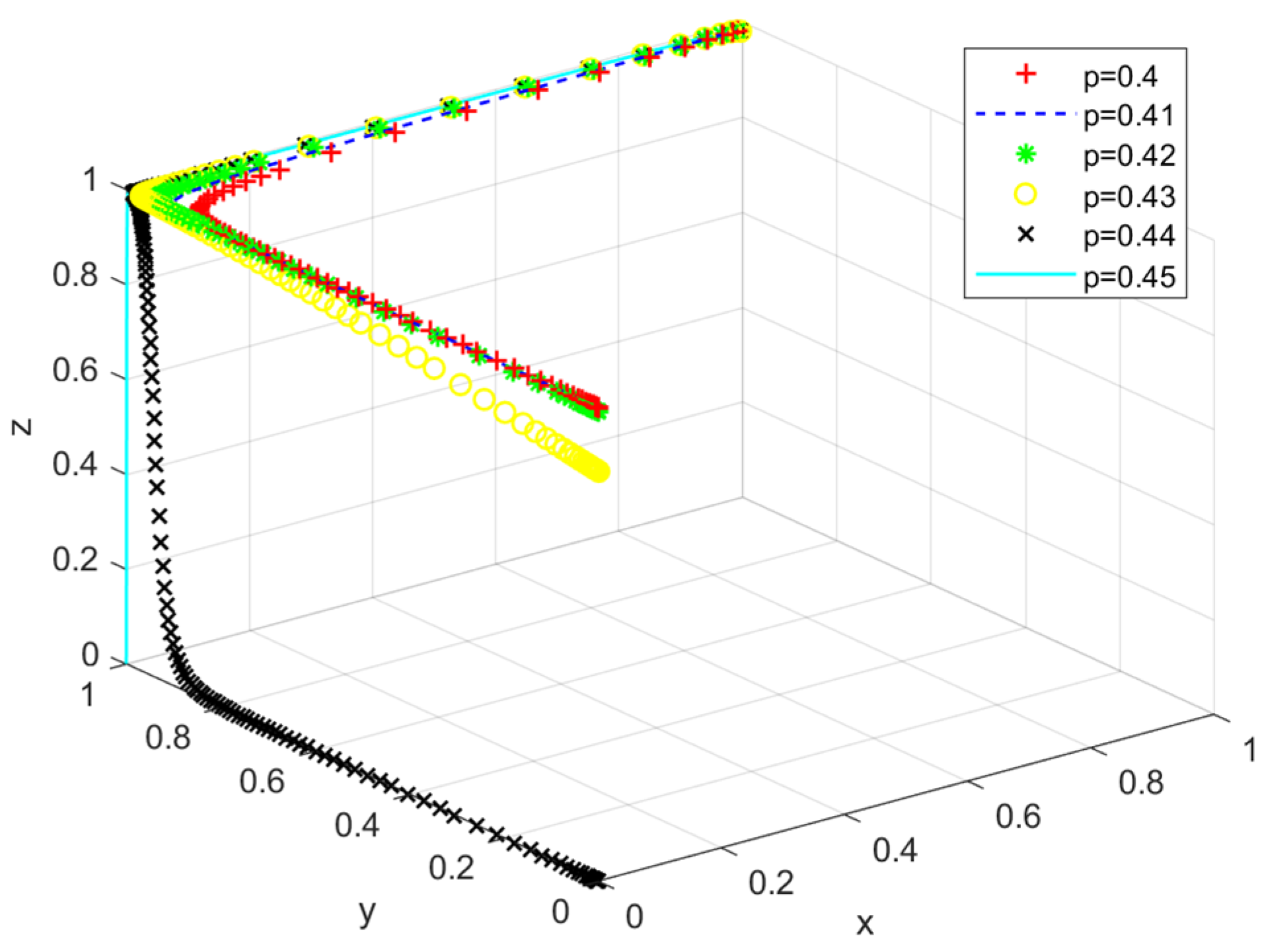

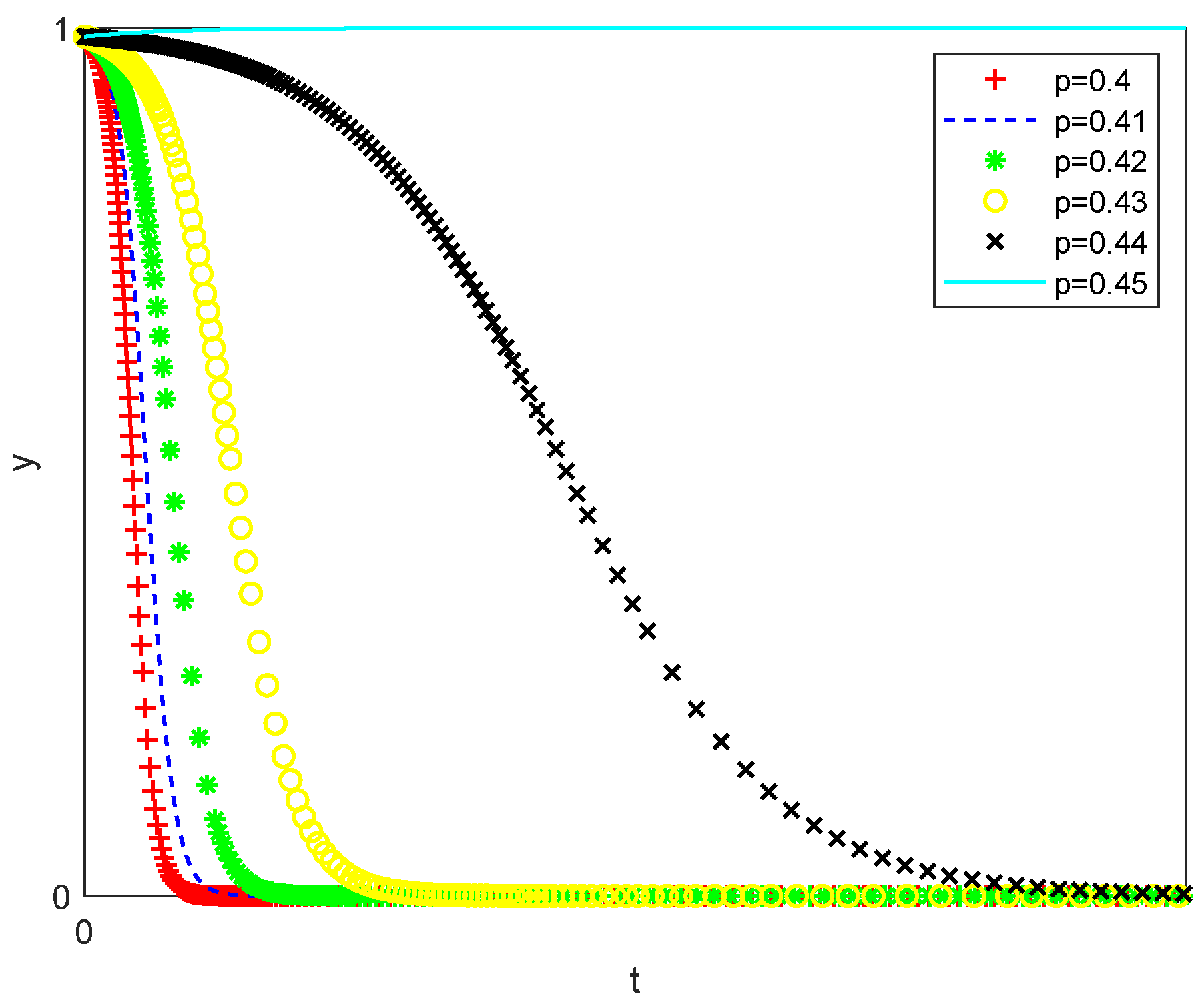

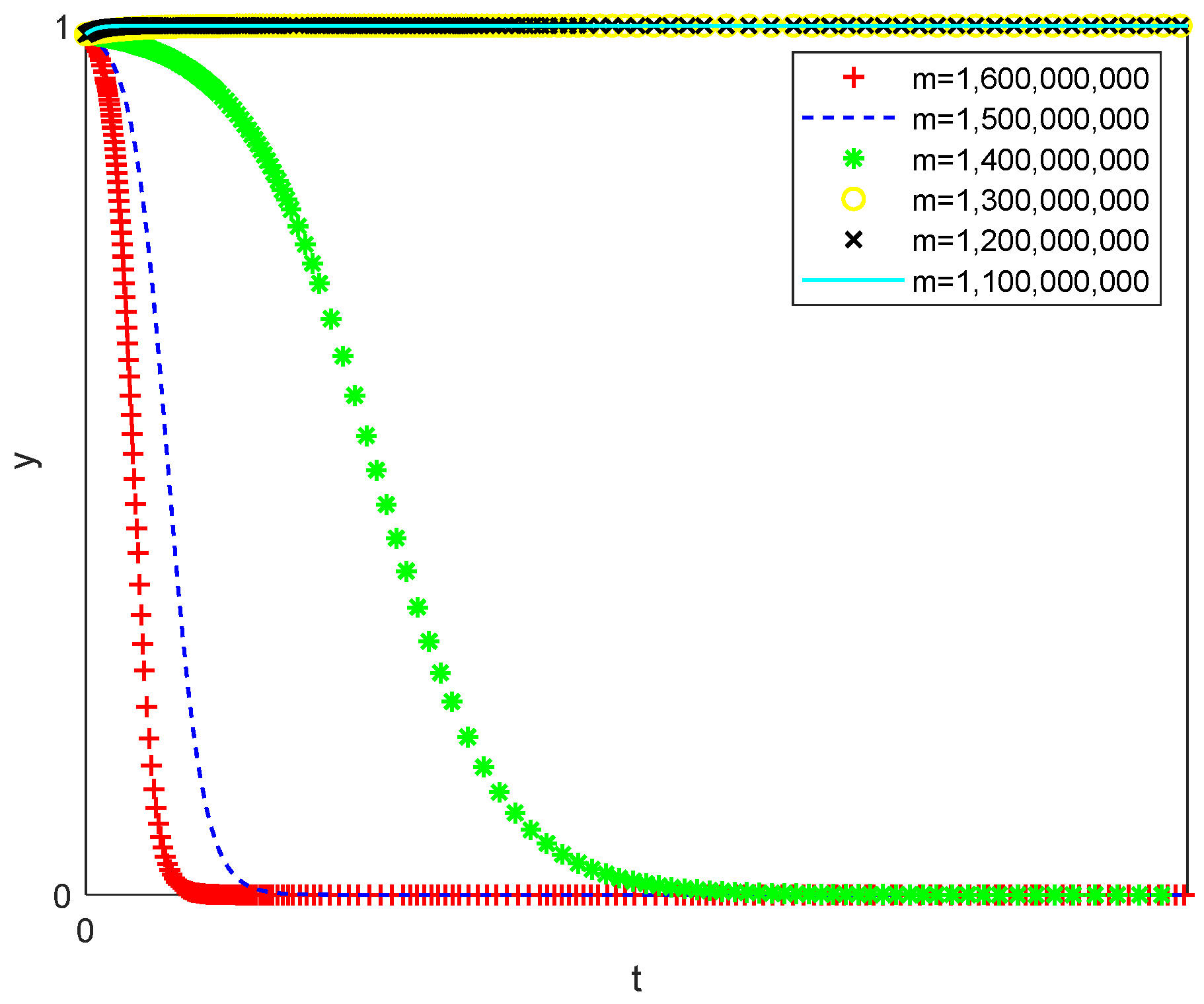

5.2.1. Electricity Price

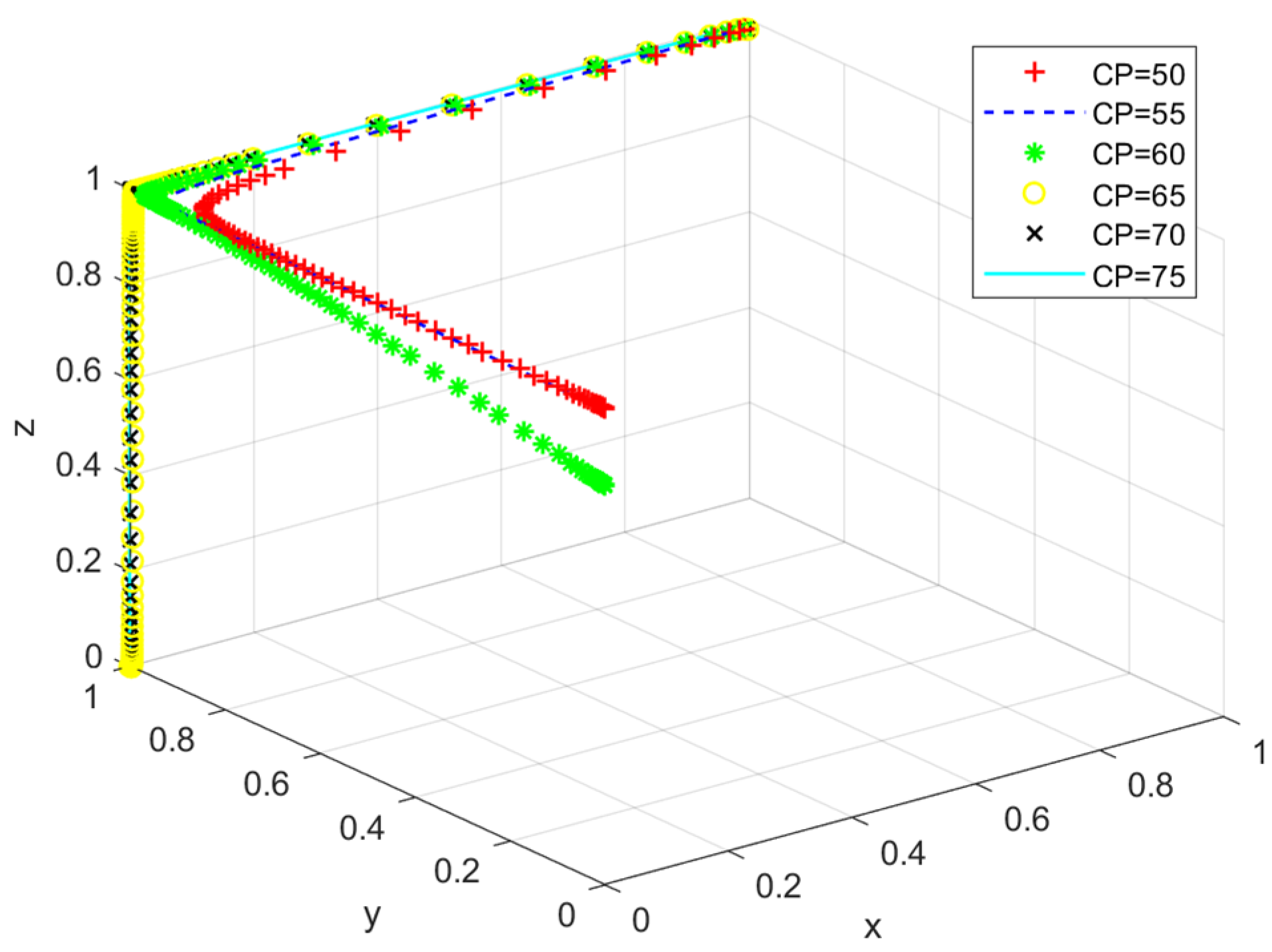

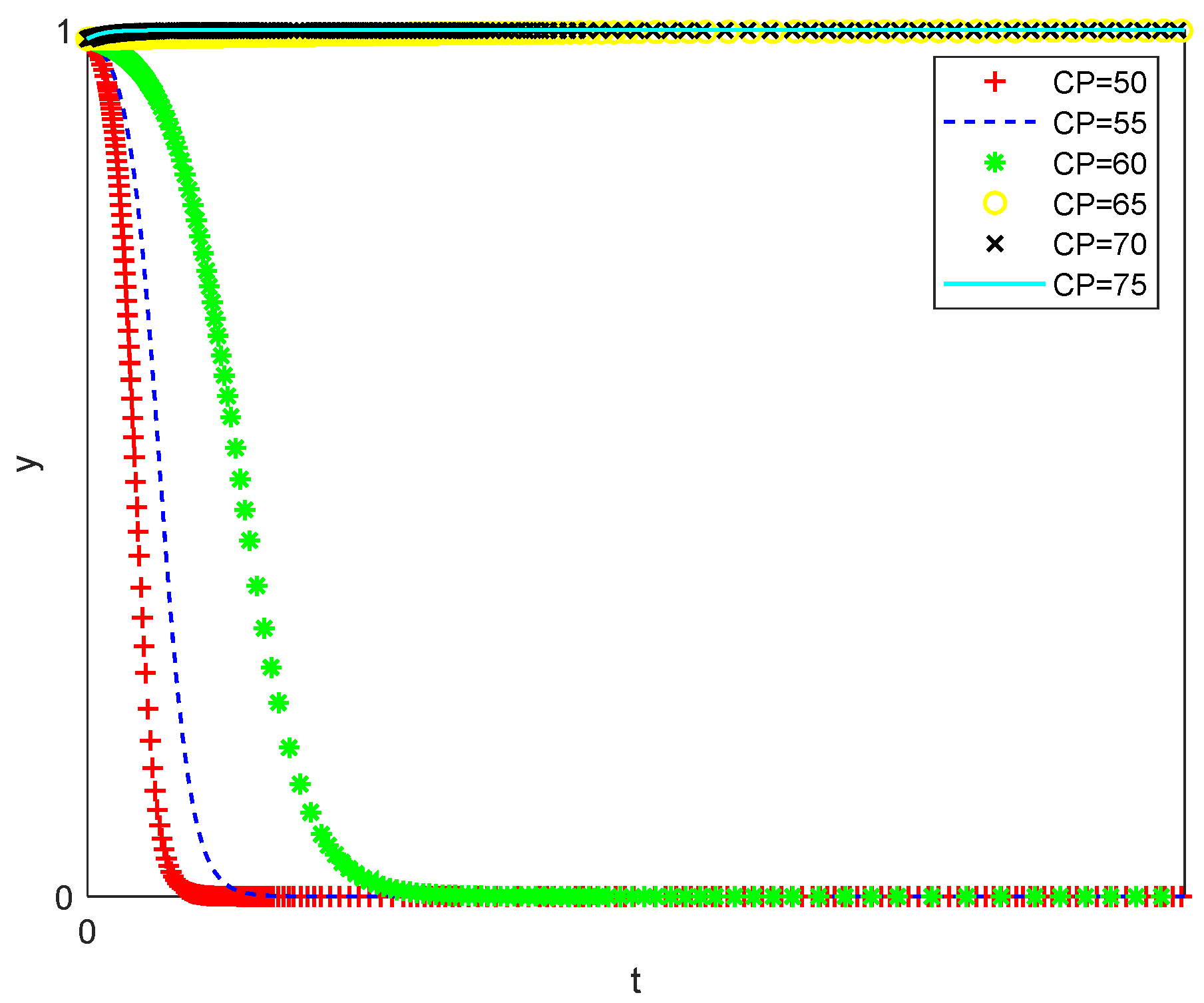

5.2.2. Carbon Emission Trading Price

5.2.3. Project Cost

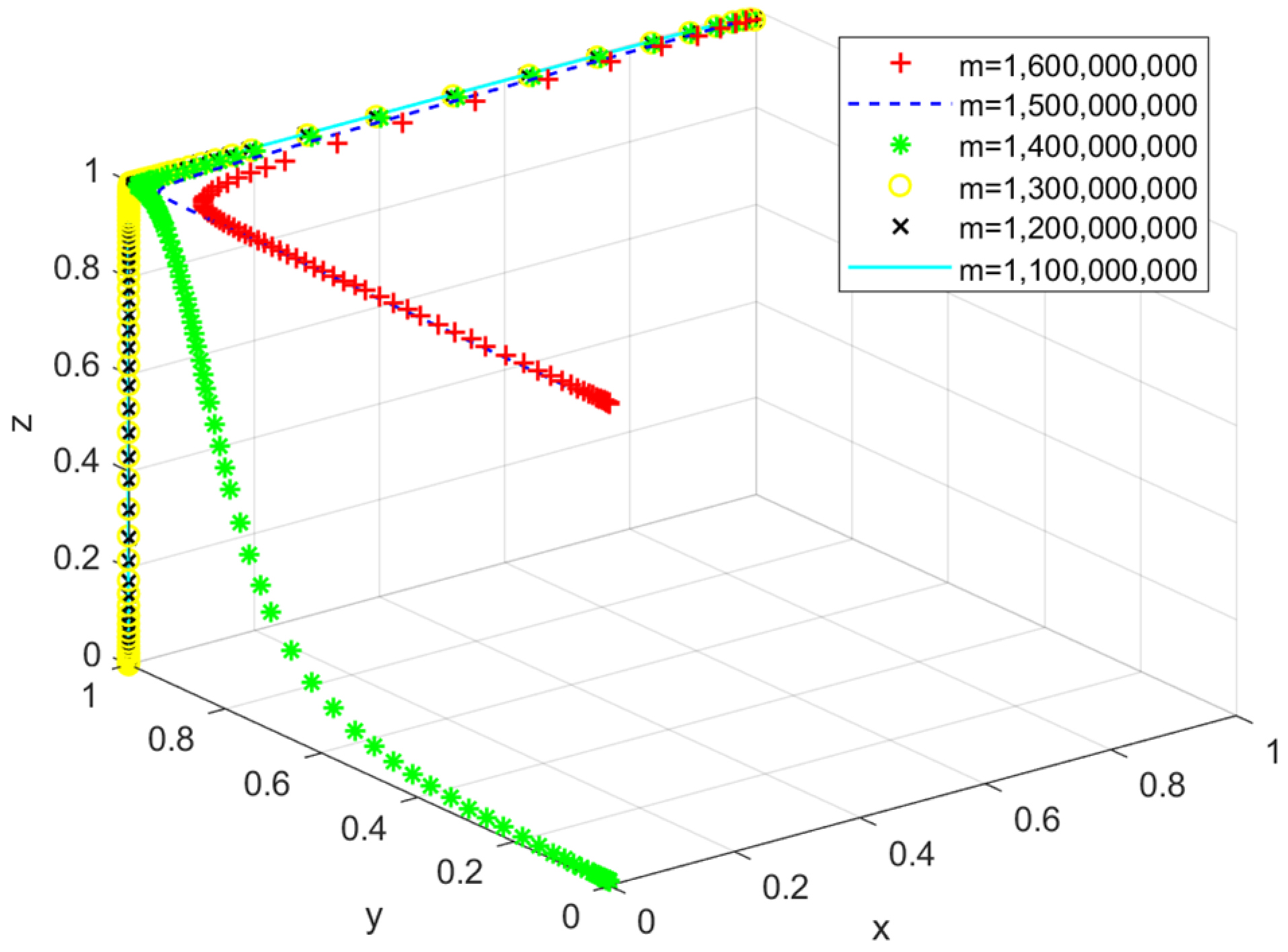

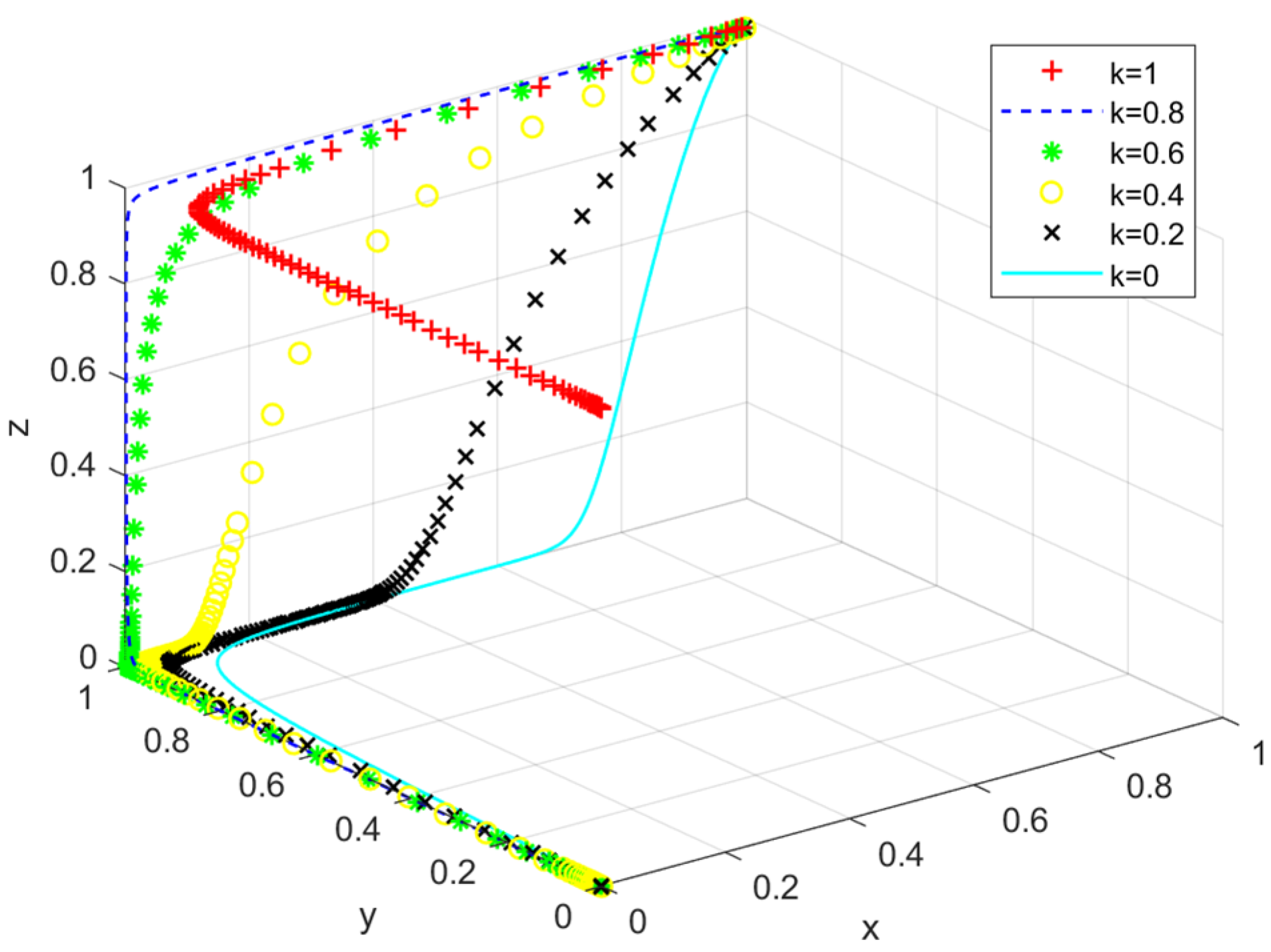

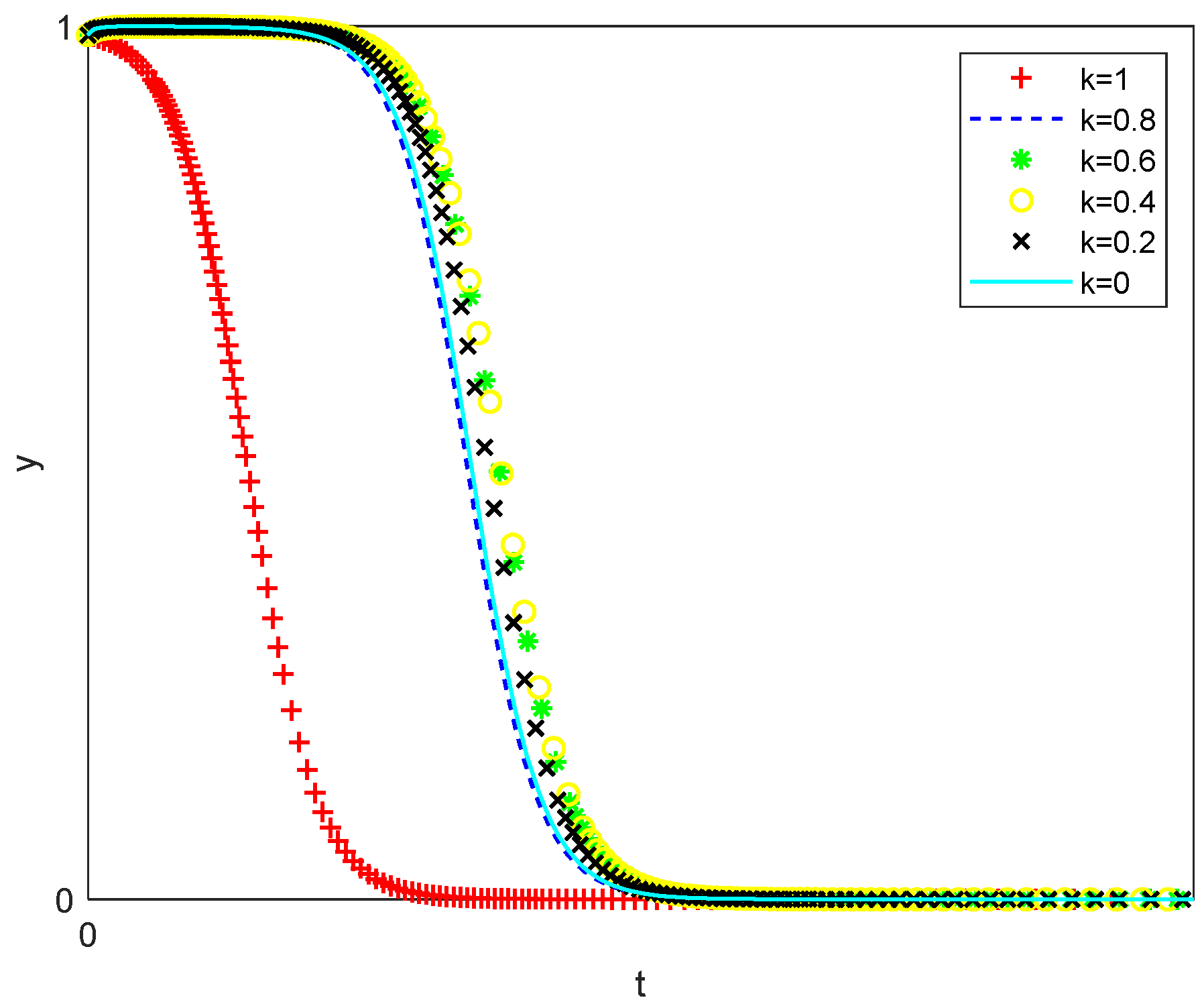

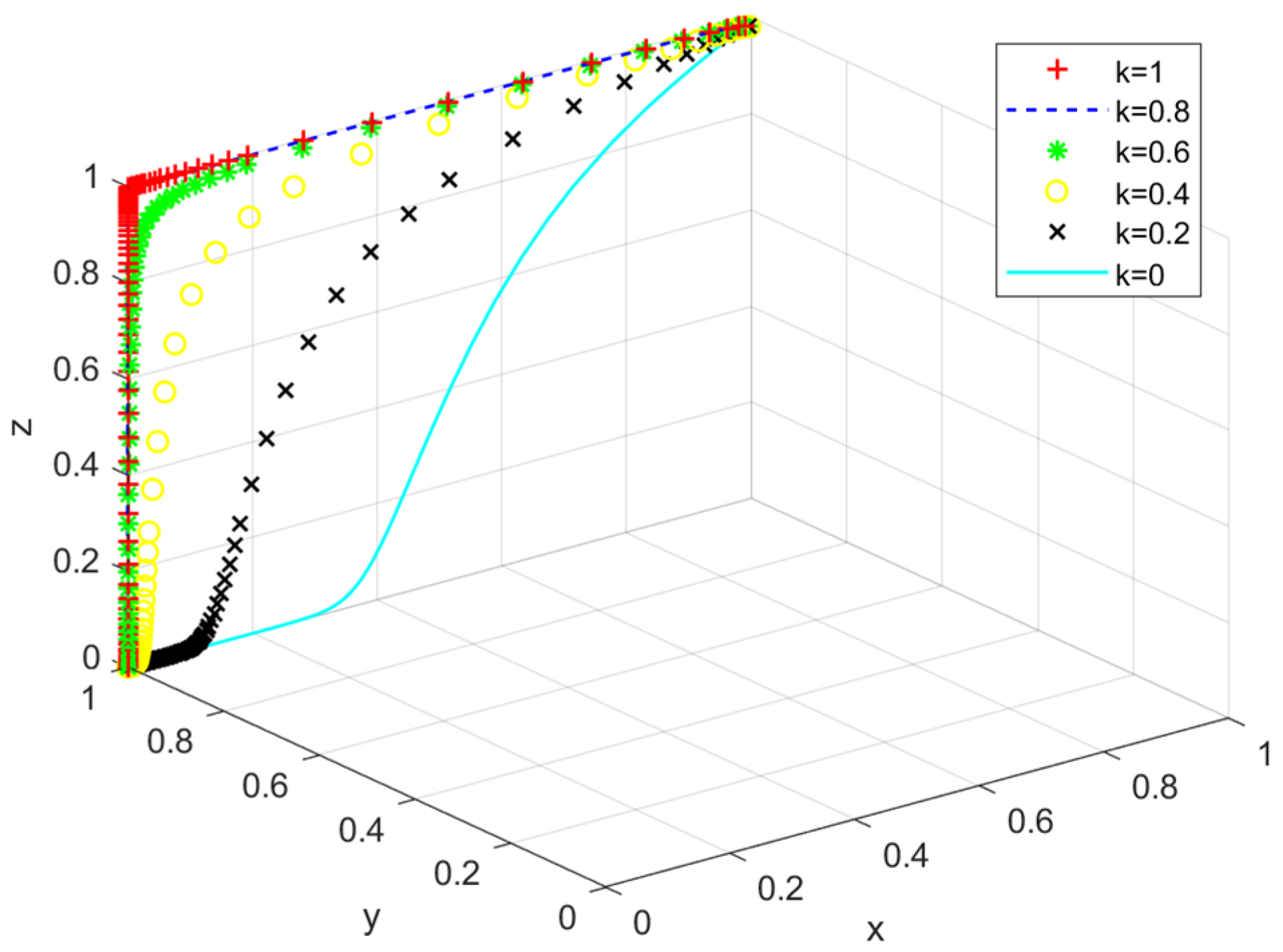

5.2.4. Green Credit Adjustment Factor

6. Conclusions

7. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Cui, R.Y.; Hultman, N.; Cui, D.; McJeon, H.; Yu, S.; Edwards, M.R.; Sen, A.; Song, K.; Bowman, C.; Clarke, L.; et al. A plant-by-plant strategy for high-ambition coal power phaseout in China. Nat. Commun. 2021, 12, 1468. [Google Scholar] [CrossRef] [PubMed]

- Kou, J.; Sun, F.; Li, W.; Jin, J. Could China Declare a “Coal Phase-Out”? An Evolutionary Game and Empirical Analysis Involving the Government, Enterprises, and the Public. Energies 2022, 15, 531. [Google Scholar] [CrossRef]

- Mi, Z.F.; Pan, S.Y.; Yu, H.; Wei, Y.M. Potential impacts of industrial structure on energy consumption and CO2 emission: A case study of Beijing. J. Clean. Prod. 2015, 103, 455–462. [Google Scholar] [CrossRef]

- Li, J.; Zhang, Y.; Tian, Y.; Cheng, W.; Yang, J.; Xu, D.; Ku, A.Y. Reduction of carbon emissions from China’s coal-fired power industry: Insights from the province-level data. J. Clean. Prod. 2020, 242, 118518. [Google Scholar] [CrossRef]

- Li, C.K.; Caineng, Z.; Weihe, H.; Jianning, Y.; Haixia, H. China’s Energy Demand Projection and Energy Transition Trends under Carbon Peak and Carbon Neutrality Situation. Pet. Sci. Technol. Forum. 2022, 41, 9–17. [Google Scholar] [CrossRef]

- Su, D.; Lian, L. Does green credit policy affect corporate financing and investment? Evidence from publicly listed enterprises in pollution-intensive industries. J. Financ. Res. 2018, 12, 123–137. Available online: http://www.jryj.org.cn/EN/Y2018/V462/I12/123 (accessed on 7 July 2022).

- Ling, S.; Han, G.; An, D.; Hunter, W.C.; Li, H. The impact of green credit policy on technological innovation of enterprises in pollution-intensive industries: Evidence from China. Sustainability 2020, 12, 4493. [Google Scholar] [CrossRef]

- Amore, M.D.; Schneider, C.; Žaldokas, A. Credit supply and corporate innovation. J. Financ. Econ. 2013, 109, 835–855. [Google Scholar] [CrossRef]

- Nanda, R.; Nicholas, T. Did bank distress stifle innovation during the Great Depression? J. Financ. Econ. 2014, 114, 273–292. [Google Scholar] [CrossRef]

- Kim, J.; Park, K. Financial development and deployment of renewable energy technologies. Energy Econ. 2016, 59, 238–250. [Google Scholar] [CrossRef]

- Kang, H.; Jung, S.Y.; Lee, H. The impact of Green Credit Policy on manufacturers’ efforts to reduce suppliers’ pollution. J. Clean Prod. 2020, 248, 119271. [Google Scholar] [CrossRef]

- Hu, Y.; Jiang, H.; Zhong, Z. Impact of green credit on industrial structure in China: Theoretical mechanism and empirical analysis. Environ. Sci. Pollut. Res. 2020, 27, 10506–10519. [Google Scholar] [CrossRef] [PubMed]

- Sun, J.; Wang, F.; Yin, H.; Zhang, B. Money talks: The environmental impact of China’s green credit policy. J. Policy Anal. Manag. 2019, 38, 653–680. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Wang, Z.; Huang, Z. Green loan and subsidy for promoting clean production innovation. J. Clean. Prod. 2018, 187, 421–431. [Google Scholar] [CrossRef]

- Zhang, D. Green credit regulation, induced R&D and green productivity: Revisiting the Porter Hypothesis. Int. Rev. Financ. Anal. 2021, 75, 101723. [Google Scholar] [CrossRef]

- Xing, C.; Zhang, Y.; Wang, Y. Do banks value green management in China? The perspective of the green credit policy. Financ. Res. Lett. 2020, 35, 101601. [Google Scholar] [CrossRef]

- Song, M.; Xie, Q.; Shen, Z. Impact of green credit on high-efficiency utilization of energy in China considering environmental constraints. Energy Policy 2021, 153, 112267. [Google Scholar] [CrossRef]

- Zhang, K.; Li, Y.; Qi, Y.; Shao, S. Can green credit policy improve environmental quality? Evidence from China. J. Environ. Manag. 2021, 298, 113445. [Google Scholar] [CrossRef]

- Wang, F.; Yang, S.; Reisner, A.; Liu, N. Does green credit policy work in China? The correlation between green credit and corporate environmental information disclosure quality. Sustainability 2019, 11, 733. [Google Scholar] [CrossRef]

- Yao, S.; Pan, Y.; Sensoy, A. Green credit policy and firm performance: What we learn from China. J. Energy Econ. 2021, 101, 105415. [Google Scholar] [CrossRef]

- Wen, H.; Lee, C.C.; Zhou, F. Green credit policy, credit allocation efficiency and upgrade of energy-intensive enterprises. Energy Econ. 2021, 94, 105099. [Google Scholar] [CrossRef]

- Wang, E.; Liu, X.; Wu, J.; Cai, D. Green credit, debt maturity, and corporate investment—Evidence from China. Sustainability 2019, 11, 583. [Google Scholar] [CrossRef]

- Xu, X.; Li, J. Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. J. Clean. Prod. 2020, 264, 121574. [Google Scholar] [CrossRef]

- He, L.; Liu, R.; Zhong, Z.; Wang, D.; Xia, Y. Can green financial development promote renewable energy investment efficiency? A consideration of bank credit. Renew. Energ. 2019, 143, 974–984. [Google Scholar] [CrossRef]

- Berrou, R.; Ciampoli, N.; Marini, V. Defining Green Finance: Existing Standards and Main Challenges. In The Rise of Green Finance in Europe; Palgrave Studies in Impact Finance; Migliorelli, M., Dessertine, P., Eds.; Palgrave Macmillan: Cham, Switzerland, 2019. [Google Scholar] [CrossRef]

- Hafezalkotob, A.; Alavi, A.; Makui, A. Government financial intervention in green and regular supply chains: Multi-level game theory approach. Int. J. Manag. Sci. Eng. Manag. 2016, 11, 167–177. [Google Scholar] [CrossRef]

- Hafezalkotob, A.; Mahmoudi, R. Selection of energy source and evolutionarily stable strategies for power plants under financial intervention of government. J. Ind. Eng. Int. 2017, 13, 357–367. [Google Scholar] [CrossRef]

- Kuang, Y. Research on the Game Theory and Logic Optimization and the Applications on Construction of China’s New Energy Subsidy System. DEStech Transactions on Social Science Education and Human Science (asshm). 2016. Available online: http://dpi-journals.com/index.php/dtssehs/article/view/8366 (accessed on 21 January 2022).

- Tian, Y.; Govindan, K.; Zhu, Q. A system dynamics model based on evolutionary game theory for green supply chain management diffusion among Chinese manufacturers. J. Clean. Prod. 2014, 80, 96–105. [Google Scholar] [CrossRef]

- Xu, A.; Zhou, Z. A Game Model for the Pricing of the Government’s Subsidy in the Green Supply Chain for Home Appliances Industry in China. WHICEB 10. 2013. Available online: https://aisel.aisnet.org/cgi/viewcontent.cgi?article=1109&context=whiceb2013 (accessed on 17 March 2022).

- Sheu, J.B.; Chen, Y.J. Impact of government financial intervention on competition among green supply chains. Int. J. Prod. Econ. 2012, 138, 201–213. [Google Scholar] [CrossRef]

- Geng, Y.; Xinbei, W.; Qinghua, Z.; Hengxin, Z. Regional initiatives on promoting cleaner production in China: A case of Liaoning. J. Clean. Prod. 2010, 18, 1502–1508. [Google Scholar] [CrossRef]

- Dong, F.; Shi, L.; Ding, X.; Li, Y.; Shi, Y. Study on China’s Renewable Energy Policy Reform and Improved Design of Renewable Portfolio Standard. Energies 2019, 12, 2147. [Google Scholar] [CrossRef]

- Zhao, R.; Neighbour, G.; Han, J.; McGuire, M.; Deutz, P. Using game theory to describe strategy selection for environmental risk and carbon emissions reduction in the green supply chain. J. Loss. Prev. Process. Ind. 2012, 25, 927–936. [Google Scholar] [CrossRef]

- Zhang, T.; Cao, S.; Pan, L.; Zhou, C. A Policy Effect Analysis of China’s Energy Storage Development Based on a Multi-Agent Evolutionary Game Model. Energies 2020, 13, 6293. [Google Scholar] [CrossRef]

- Friedman, D. Evolutionary games in economics. Econometrica 1991, 59, 637–666. [Google Scholar] [CrossRef]

- China Electricity Council. 2019–2020 National Electricity Supply and Demand Situation Analysis and Forecast Report 2020. Available online: https://cec.org.cn/detail/index.html?3-277104 (accessed on 17 March 2022).

- Zhao, X.; Bai, Y.; Ding, L.L. Can carbon sentiment contribute to the development of carbon capture and storage projects? China Manag. Sci. 2020. (In Chinese) [Google Scholar] [CrossRef]

- National Development and Reform Commission of the People’s Republic of China. National Development and Reform Commission National Energy Administration on Notice on the Orderly Release of Electricity Consumption Plans 2017. Available online: https://www.ndrc.gov.cn/fzggw/jgsj/yxj/sjdt/201704/t20170410_986939.html?code=&state=123 (accessed on 18 March 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Subject | Parameters | Definition |

|---|---|---|

| Government | Socio-economic benefit function | |

| Socio-environmental benefit function | ||

| Regulatory costs | ||

| Green credit financial subsidy | ||

| Coal power enterprises | Electricity prices | |

| Coal prices | ||

| Green transition enterprise power generation | ||

| Passive reduction of enterprise power generation | ||

| Green transition carbon emissions | ||

| Passive reduction of carbon emissions | ||

| Carbon emission allowance | ||

| Carbon emission trading price | ||

| Commercial Banks | Loan interest rate | |

| Project loan amount | ||

| Green adjustment factor | ||

| Implementation of green credit bank costs | ||

| Implementation of traditional credit bank costs |

| Subject | Banks | ||||

|---|---|---|---|---|---|

| Implementation of Green Credit Policy (z) | Implementation of Traditional Credit Policies (1 − z) | ||||

| Govern-ment | Coal power enterprises | Green transformation | |||

| 0 | 0 | ||||

| Green transformation | |||||

| 0 | 0 | ||||

| Equilibrium Point | Eigenvalue | Symbols | Stability | ||

|---|---|---|---|---|---|

| λ1 | λ2 | λ3 | |||

| (0,0,0) | 0 | −, N, 0 | Instability | ||

| (1,0,0) | 0 | +, N, 0 | Instability | ||

| (0,1,0) | −, N, − | Uncertain | |||

| (0,0,1) | 0 | −, N, 0 | Instability | ||

| (1,1,0) | +, N, N | Instability | |||

| (1,0,1) | 0 | +, N, 0 | Instability | ||

| (0,1,1) | −, N, + | Instability | |||

| (1,1,1) | +, N, − | Instability | |||

| Equilibrium Point | Scenario 1 | Scenario 2 | ||

|---|---|---|---|---|

| Eigenvalue Symbols | Stability | Eigenvalue Symbols | Stability | |

| (0,0,0) | −, −, 0 | Unstable | −, +, 0 | Unstable |

| (1,0,0) | +, −, 0 | Unstable | +, +, 0 | Unstable |

| (0,1,0) | −, +, − | Unstable | −, −, − | Stable |

| (0,0,1) | −, N, 0 | Unstable | −, N, 0 | Unstable |

| (1,1,0) | +, +, N | Unstable | +, −, N | Unstable |

| (1,0,1) | +, N, 0 | Unstable | +, N, 0 | Unstable |

| (0,1,1) | −, N, + | Unstable | −, N, + | Unstable |

| (1,1,1) | +, N, − | Unstable | +, N, − | Unstable |

| Subject | Parameters | Unit | Assignment |

|---|---|---|---|

| Government | / | / | |

| / | / | ||

| CNY | 5,000,000 | ||

| CNY | 30,000,000 | ||

| Coal power enterprises | CNY/kWh | 0.40/0.41/0.42/0.43/0.44/0.45 | |

| CNY/kWh | 0.3 | ||

| kWh | 1,200,000,000 | ||

| kWh | 960,000,000 | ||

| Tonnes | 18,000 | ||

| Tonnes | 748,800 | ||

| / | / | ||

| CNY/tonne | 50/55/60/65/70/75 | ||

| Banks | / | 0.0445 | |

| CNY | 1,600,000,000/1,500,000,000 /1,400,000,000/1,300,000,000 /1,200,000,000/1,100,000,000 | ||

| / | 0/0.2/0.4/0.6/0.8/1 | ||

| CNY | 15,000,000 | ||

| CNY | 10,000,000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cui, F.; Han, C.; Liu, P.; Teng, M. Green Credit of China’s Coal Power Enterprises during Green Transformation: A Tripartite Evolutionary Game Analysis. Energies 2022, 15, 5911. https://doi.org/10.3390/en15165911

Cui F, Han C, Liu P, Teng M. Green Credit of China’s Coal Power Enterprises during Green Transformation: A Tripartite Evolutionary Game Analysis. Energies. 2022; 15(16):5911. https://doi.org/10.3390/en15165911

Chicago/Turabian StyleCui, Feng, Chuanfeng Han, Pihui Liu, and Minmin Teng. 2022. "Green Credit of China’s Coal Power Enterprises during Green Transformation: A Tripartite Evolutionary Game Analysis" Energies 15, no. 16: 5911. https://doi.org/10.3390/en15165911