1. Introduction

Pakistan is among the vulnerable nations to climate change, as it is for the most part energized with contamination [

1]. Because of huge Green House Gas (GHG) emissions, it is positioned as the world’s second worst country in the World Air Quality Index Report 2020 [

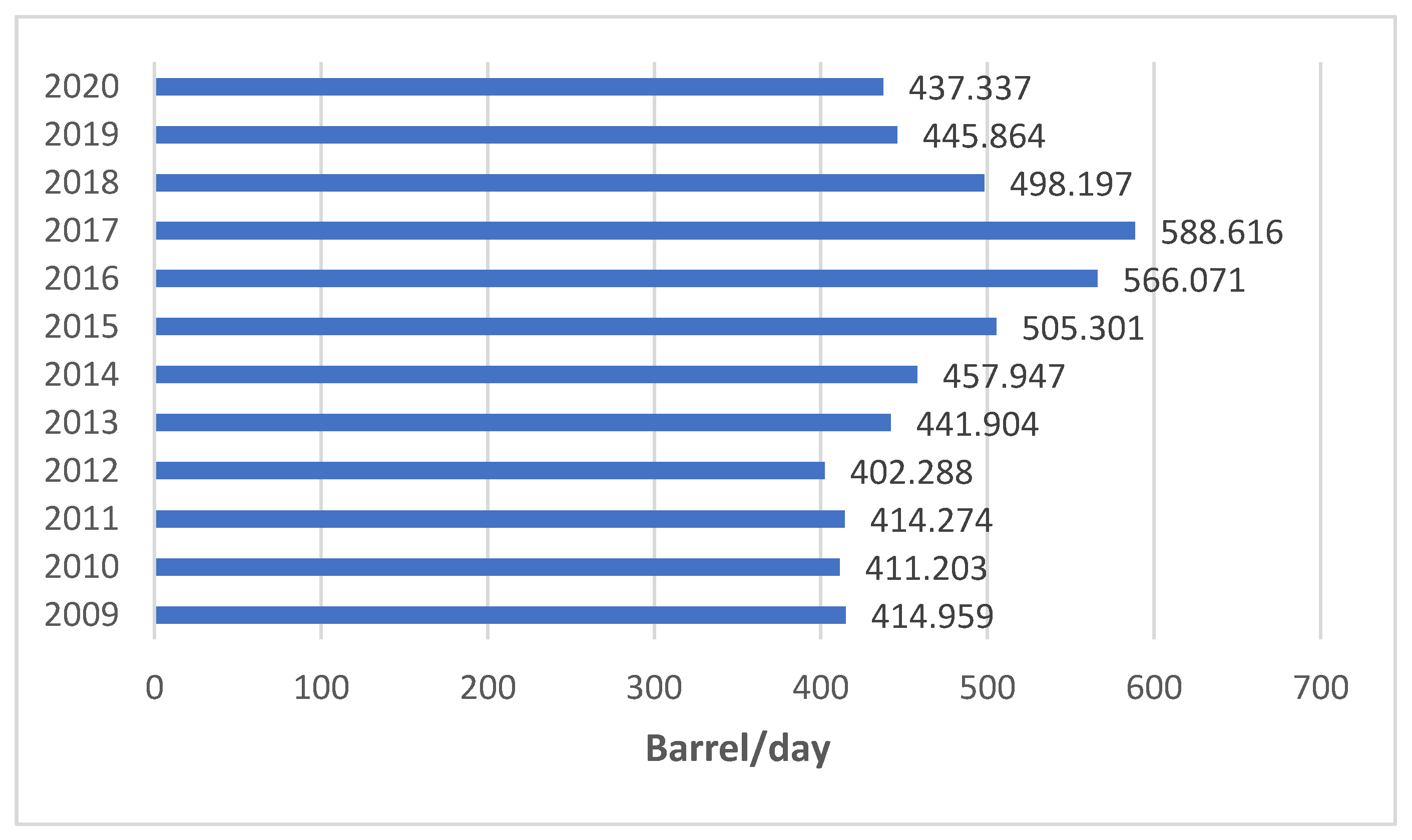

2]. Every year, tons of oil are imported with high obligation charges as shown in

Figure 1. As indicated in the most recent information from the Pakistan Bureau of Statistics (PBS), oil imports for July–October of 2020–2021 added up to USD 3.15 billion, showing that petroleum product utilization is not simply deteriorating the climate impact but also additionally impacting the economy. In any case, because of COVID-19, a reduction of 24.56% in oil imports was accounted for, facilitating the weight on the country’s unfamiliar trade savings. Simultaneously, an overall downfall of 7% in CO

2 outflows from petroleum products was noticed, as distributed in Nature Climate Change [

3].

A detailed literature review is provided in

Table 1 below.

The change in outlook from FFVs to EVs is a countermeasure to these issues of the overabundance of electrical power in MWs, decreasing the oil import bills, and assisting Pakistan with having a green revolution. To advance nearby utilization of EVs, efficient charging is required, and an essential half-and-half charging office that utilizes sustainable power and is grid-connected.

These examinations make sense of the significance of electric vehicles; however, give no conjecture about its development. This paper rather centers around the demonstrating and stacking of EVs in this decade’s thought of the excess energy generation.

This research work would be instrumental in providing a direction for the future integrated energy policies and planning in Pakistan with a special focus on national electricity and transportation policies and planning, providing a road map with solutions to resolve Pakistan’s chronic energy challenges pertaining to excess power generation and mitigation of the carbon footprint apart from resolving associated economic challenges such as circular debt. On the academic front, the work provides a new scope of research cluster for the faculty and students to join and conduct their research work accordingly as per the emerging needs of the society.

This paper is divided into the following sections:

Section 2,

Section 3 and

Section 4 discuss the transport sector, electricity situation, and national electric vehicle policy of Pakistan, respectively.

Section 5 confers modeling of load growth, and

Section 6 provides the result-based discussion.

Section 7 provides a brief conclusion and recommendations.

2. Transport Sector of Pakistan and Associated Issues

The transport sector of Pakistan can be divided into three categories that are commercial, private, and public transport:

Vehicles that move commodities or resources from one location to another are referred to as commercial transport. Heavy-duty vehicles such as box trucks, cargo vans, cargo trains, and cement mixers utilize diesel as their primary fuel, because diesel provides the higher torque, which is a critical need for bulky vehicles, as well as cost, compression rate, and combustion [

10].

- ii.

Private Transport:

Individually owned vehicles, such as a car, bike, or bicycle, fall under the category of private transportation. Petrol and compressed natural gas (CNG) are the two major fuel types used in this form of transportation.

- iii.

Public Transport:

Travelers share a form of transportation to travel along the characterized routes for which a charge should be paid in this mode. Trains, airplanes, buses, and taxis are examples of public travel vehicles. With Pakistan’s rising populace, the proportion of creation to deals of this kind of vehicle is expanding. Taxis, for instance, work on petrol or CNG, trains run on coal, oil, or diesel, buses and vans commonly run on diesel or petroleum, and nearby rickshaws run on petrol or CNG [

10].

Public expressways and common roadways represent 13,000 and 93,000 km, separately, with lengths of the different areas, commonplaces, and city roads filling the gaps [

10]. This transport network is expanding because of the implementation of the ambitious China Pakistan Economic Corridor (CPEC), with the construction of 3070 km of new road and railway routes under construction. While this will improve the current shipping lane, it will likewise overburden the current street network [

9].

In contrast with the past financial year, the populace moved from 208.57 to 212.48 million individuals in 2020–21, and the proportion of the street transport area expanded also. As per [

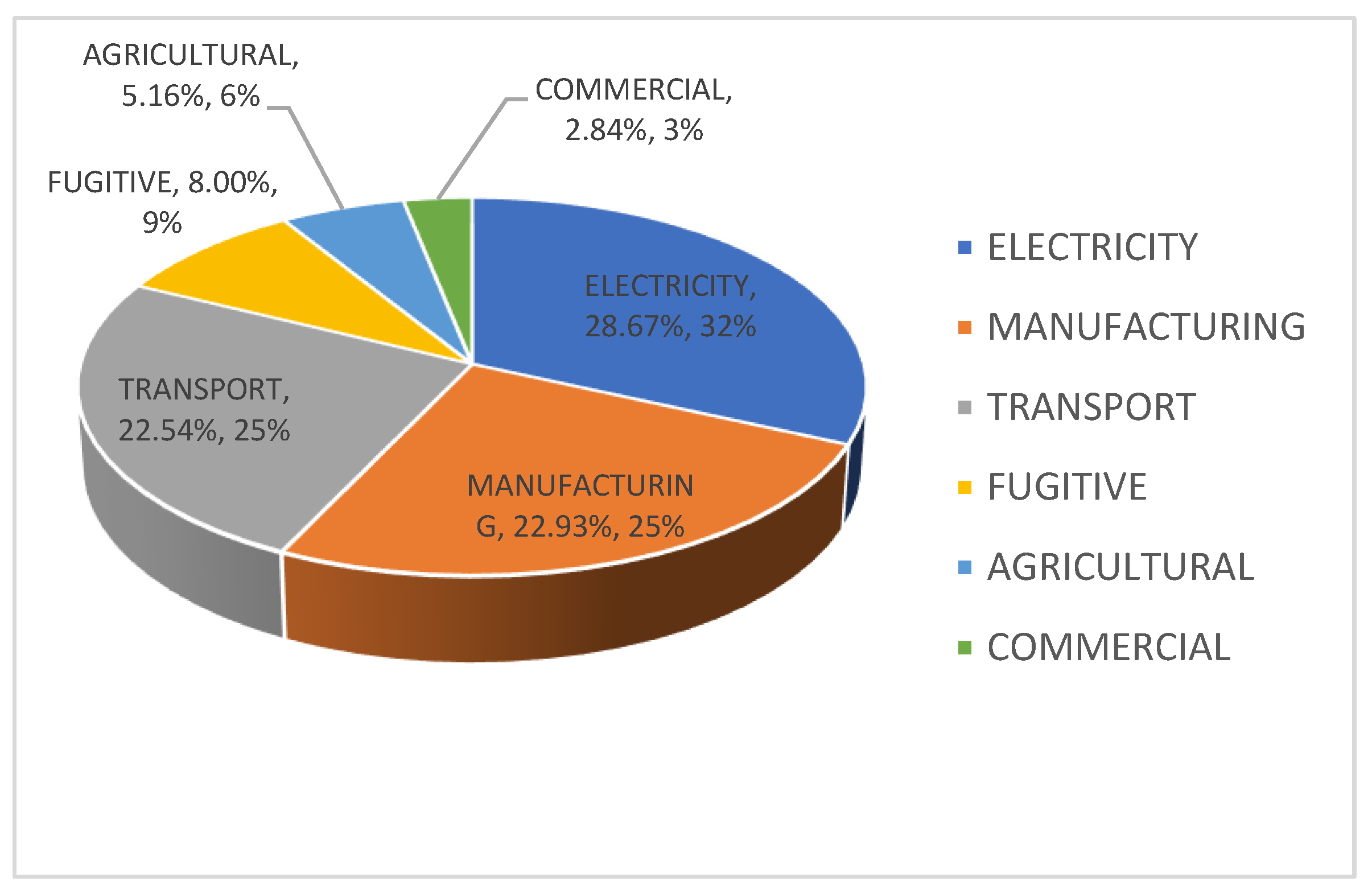

9], the typical thickness of vehicles per 1000 individuals is 16 which is probably going to increment as Pakistan is heavily pushing towards urbanization. As per the 2018 review, around 17 million vehicles were enrolled, with that number anticipated to increase by 30 million by 2025, and the transportation sector’s oil utilization was almost 302,000 barrels each day, with that number expected to increase by 2025 according to the transportation expansions plan, displayed in

Figure 2 [

11].

Pakistan’s massive dependence on oil imports has occurred for decades, but as the usage of gas increased in the 1990s, oil imports were substantially lowered until 2016. Our country returned to oil in 2017 due to a lack of natural gas supplies and a drop in worldwide oil prices. Pakistan’s road transport is currently mostly dependent on oil and gas.

The transport sector is intertwined with many other industries, and this tremendous expansion of the transportation system will have a significant influence on them. It will harm the already polluted environment and increase imports, resulting in a trade imbalance that the government will have to overcome. The country may experience socio-economic depravity if appropriate actions are not adopted.

Pakistan is one of the key nations affected by environmental change, according to the LUMS EV Report [

12], with liquefying icy masses, floods, heat waves, dry seasons, and heavy smog clouding most parts of Sindh and Punjab during winters.

Figure 2 shows the high development in the vehicle area from 2018 to 2025.

4. National Electric Vehicle Policy of Pakistan 2020–2030

The EV policy 2020–2030 covers different categories of electric vehicles that are cars, 2/3 wheelers, and heavy-duty vehicles such as trucks and buses [

16]. This policy provides a transition from FFVs to EVs without adversely affecting the existing transport industry which is a source of direct and indirect income of three million people and generates an approximate total of Rs. 100 billion in revenues to the government [

16].

4.1. Main Objectives of the Electric Vehicle Policy

The policy objectives are enumerated as follows:

Encourage Pakistan’s auto and associated industries to adopt electric vehicle manufacturing as a pivot to country’s industrial progress [

16].

Curtail the current negative climate impact on Pakistan by introducing and incorporating green energy technologies in the transport sector to reduce the carbon footprint [

16].

Generate employment opportunities as new companies would invest in the transition [

16].

To ensure reduction of external deficit by decreasing oil import through clean transportation [

16].

4.2. Summarized Recommendations of the Policy

The EV policy can be summarized for the different categories as follows:

4.2.1. Two/Three Wheelers

For five years, the EV policy period, the general sales tax (GST) for the 2/3 wheelers is to be fixed at the 1% at sales stage. Whereas at the importing stage, the sales tax is to be renounced off (0%) to avoid refunds.

The specific parts of electric 2/3 wheelers to be imported would have custom duty (CD) standing at 1% for the EV policy period.

Registration and annual token tax exemption for 2/3 wheelers. Tolls for electric vehicles will be reduced by 50%.

The existing manufacturing industry for traditional 2/3 wheelers in terms of non-electric parts should be preserved to maintain the previously obtained localization until a strategy on conventional vehicle retirement is developed and implemented.

The new and existing manufacturers should both benefit from the EV policy.

Import of new electric 2/3 wheelers in CBU condition at the concessionary pace of obligation (50% of the common pace of custom obligation) to be connected with foundation of assembling offices, i.e., 10 units for every variation with a limit of 200 units permitted to be imported under a concessionary system in an auto area neighborhood. In any case, advancement of cross breed innovation is not tended to in this strategy.

4.2.2. Heavy Commercial Vehicles

The complete build up (CBUs) of EV buses, trucks, and prime movers would have 1% CD on import. Import of entire Completely Knocked Downs (CKD) allowed to have a CD of 1% to the local manufacturers.

General sales tax of 1% at the point of sale and 0% at the point of import.

Registration, yearly renewal, and permit fees are waived, and toll taxes are reduced by half for HCVs.

4.3. Generalized Recommendations

Review of localization of parts and machineries should be done periodically after 2 years of the announcement of policy.

Both current and new entrants in both 2/3 wheelers and HCVs would be granted duty and tax-free import of equipment and machinery.

Manufacturing of car components and building of manufacturing facilities for EV-related equipment will be eligible for a five-year income tax exemption.

Tax and duty exemptions to be sanctioned for EV vendors for 5 years (applies to in-house manufacturing by OEMs also).

The States Bank of Pakistan’s funding facility program for encouraging green infrastructure investments will incorporate EV manufacturing, i.e., EV parts, components, and module manufacturing, EV infrastructure development including charging stations, etc.

Chargers imported with the CKD will be subject to a 1% customs duty and 1% sales tax, while charging stations for electric vehicles imported under HS Code 8504.4030 will continue to be subject to a 0% customs duty.

4.4. Limitation of EV Policy

As Pakistan is a developing country, with average road infrastructure, implementation of the national EV policy contains definite limitations and bottlenecks especially in terms of incentivizing the EV industry and market. These limitations are discussed as follows:

The policy targets mitigation of carbon footprint with green infrastructure. However, a subsequent vehicle retirement policy analogous to the power plant retirement policy has not been formulated yet and conventional vehicles in the form of a car, bus, and truck are a great source of GHG emissions. Therefore, organized efforts by the concerned stakeholders will be required for achieving the targets effectively.

EVs reflect the most recent technical trend and are costly, particularly in terms of battery costs, which are a significant component of the technology under consideration. Because its lifespan is typically five years, clients in Pakistan may be hesitant to pay the upfront amount in advance. However, batteries for motorcycles and rickshaws are either inexpensive or may be utilized in these 2/3 wheelers with regular batteries.

Hybrid automobiles are also more expensive, and buyers may be enticed to spend more because they are regarded like regular gasoline vehicles.

The EVs offer basically robust and lightweight conveyance which may not be suitable to operate on the roads of Pakistan, especially the ones in the less developed areas owing to poor road network infrastructure.

The Govt. of Pakistan through its planning division must ensure finance to establish localized industry manufacturing for gradual import substitution. This will pay the path for cost reduction and bright prospects for future investment.

Due to Pakistan’s underdeveloped conformity assessment framework, standardization, quality, and equipment safety would be a challenge.

There is no availability of charging infrastructure which poses a major challenge and hence invites attention to future investment in this area.

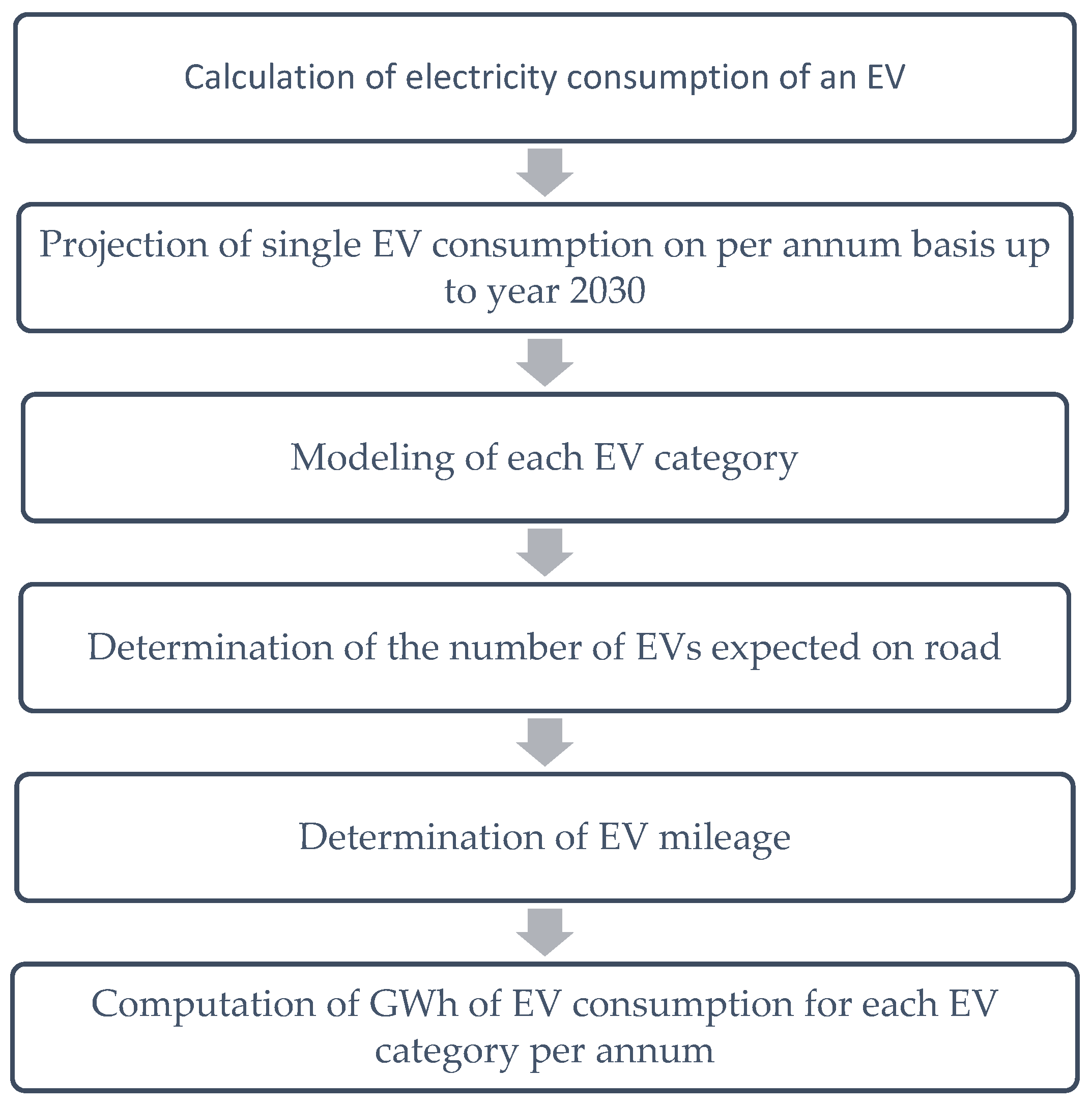

To realize the potential of clean transport transition in Pakistan and understand the future of EV transportation in Pakistan, opportunities, challenges, and way forward, modeling and analysis of the load growth to be incurred by EV induction were carried out.

7. Conclusions and Future Recommendations

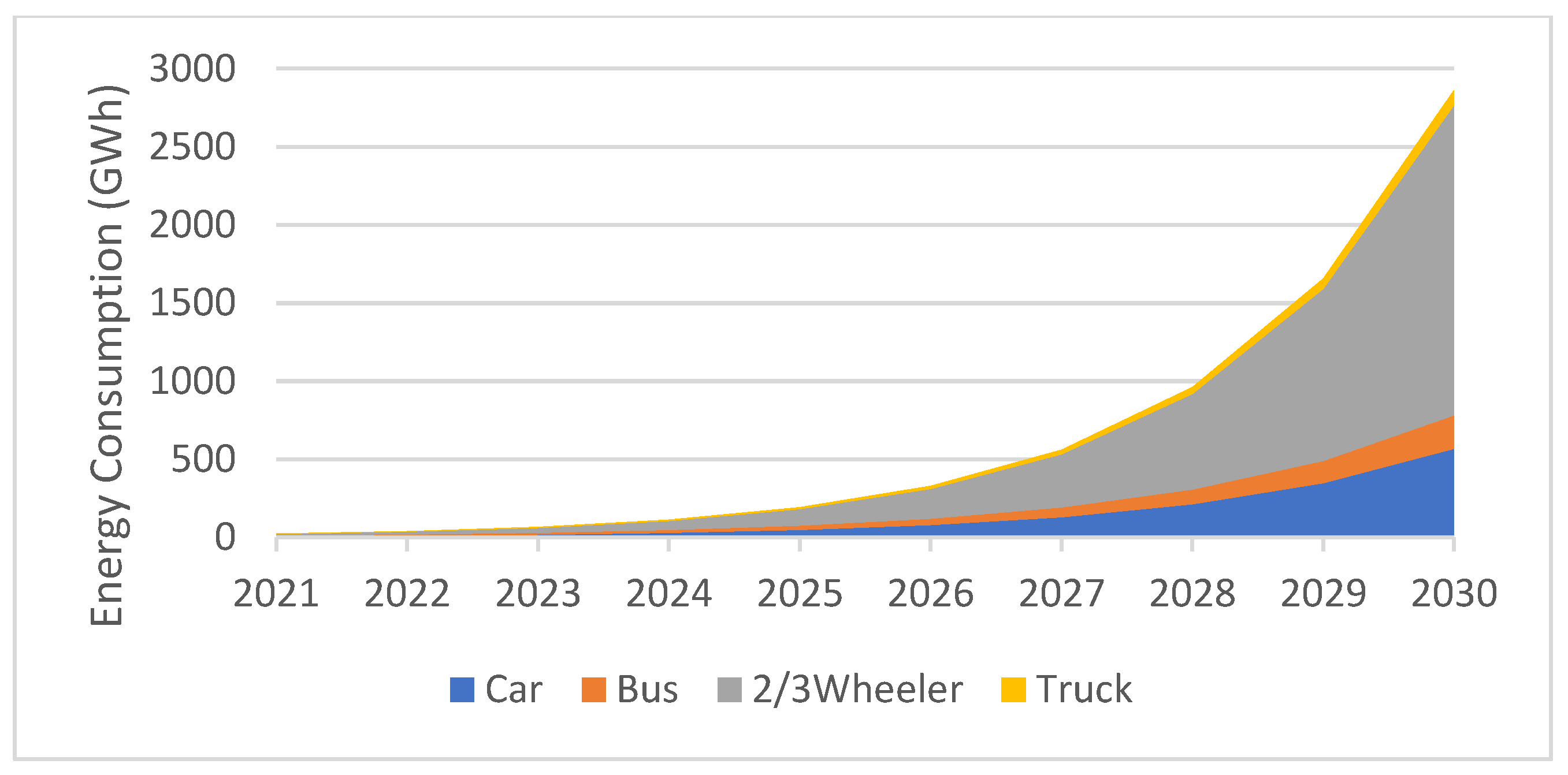

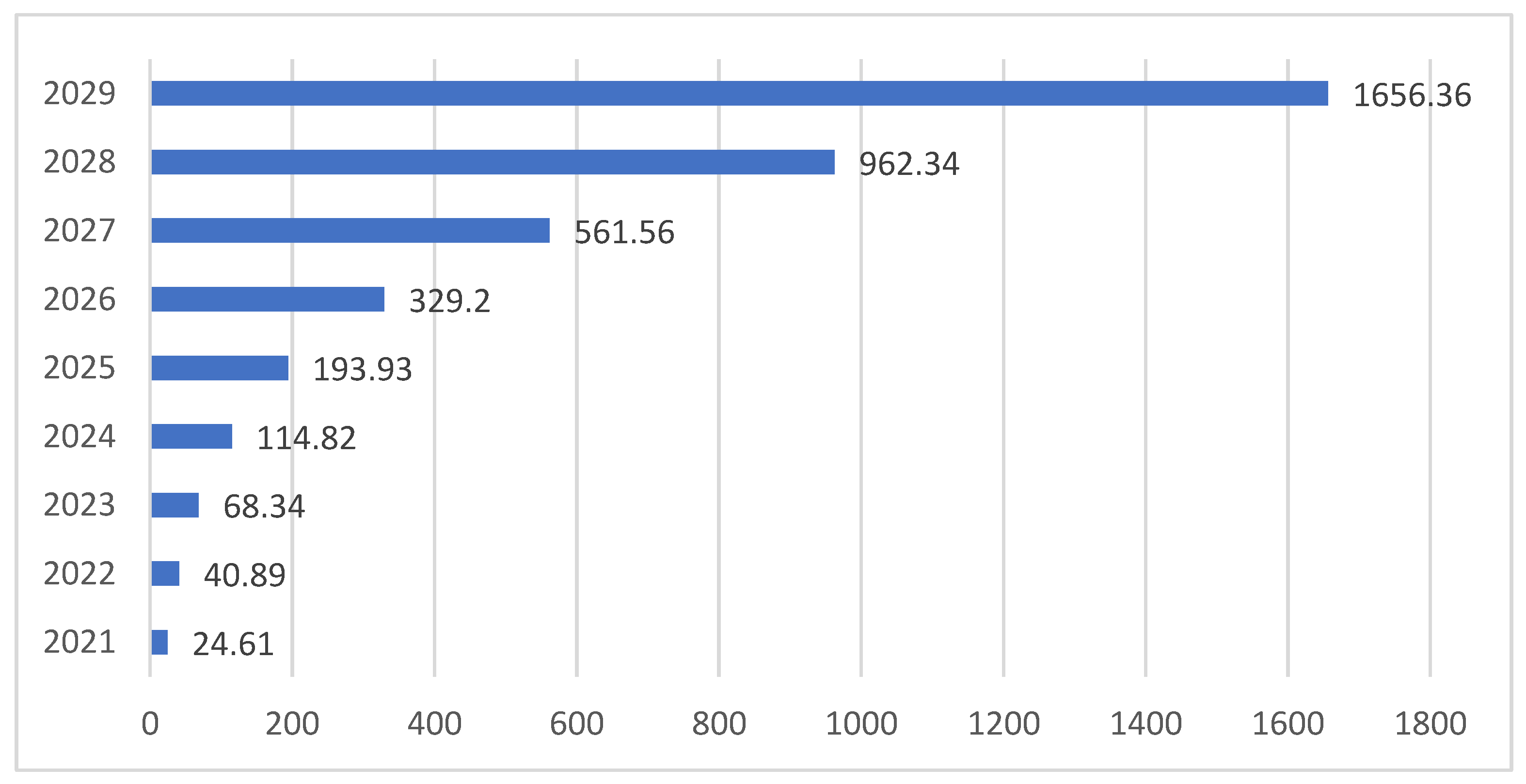

This paper proposed an electricity load growth model used to forecast the load growth expected for electric vehicles in Pakistan for the period from 2021 to 2030. A bottom-up approach was adopted for the calculation of EV electric power consumption. In this paper, each type of EV category, i.e., car, 2/3 wheeler, truck, and bus was modeled separately. EV consumption in GWh for each EV category was calculated on a per annum basis. The updated results of the model used an exponential trend curve of EVs on the road instead of a linear trend curve. The load data was simulated in the WASP model with the impact of EV charging at peak load duration. According to the revised model, total EV power stood at 24.61 GWh in 2021 and increased up to 2862.54 GWh in 2030.

Modeling and analysis of load growth for electric vehicle deployment in Pakistan can be extended to 2050 based on similar quantitative and qualitative assumptions with certain improvements and revisions to achieve greater accuracy and reliability in line with Pakistan’s 2047 Vision for clean energy transition when the country will observe its centennial independence celebrations. The energy modeling then can be carried out with advanced computer aided applications such as Plexos (energy market simulation software) to improve the model. The study can be further optimized by considering the number of vehicles to be retired in the future in line with vehicle retirement policy (under inception).

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}