1. Introduction

The transition from conventional energy consumption to renewable energy at the aggregate level has been considered a strategic decision in the process of greenhouse gas (GHG, hereafter) emission [

1]. The output from investment in research and development, i.e., the effects on macro economy positively guided by RE integration in economic activities [

2]; in addition, the literature suggests that RE assists in thriving the aggregate output with minimal environmental cost [

3]. The growing damage of environmental degradation, with a heavy application of non-renewable energy, intensifies the concern of future consequences for climate change, especially for achieving sustainable development [

4]. Thus, protecting the environment and eliminating the impact of climate change the normal course of humanity. Countries have constantly invested in energy diversification by moving to

RE application instead of orthodox energy [

5]. The recent literature has produced a plethora of empirical studies pertinent to renewable energy and, considering the motivation of respective studies, and we sub-grouped studies into two directions. First, the role of renewable energy integration in the economy, and the benefits for an economy, have been promoting green energy integration, such as economic growth acceleration, environmental protection cost reduction, financial development, agro-productivity, induced foreign investors. The second line of empirical findings explore the key determents for renewable energy integration and studies reveal several factors, including technological innovation, public debt, government expenditure, environmental policies, and financial integration.

However, the effects of policy uncertainties on energy transformation, namely, clean energy integration, have yet to be empirically investigated. The effects of economic policy uncertainty (

EPU, hereafter) have been extensively investigated, focusing on diverse key macro and micro features of the economy, such as economic growth [

6], financial development [

7], foreign direct investment, trade openness [

8], and oil price shocks [

9,

10]. However, the impact of

EPU on environmental and climate change aspects has been yet to be investigated in empirical literature extensively. The demand and use of renewable energy (RE, hereafter) consumption in the aggregate domestic production process is unnecessary, but an imperative issue due to environmental consequences, cost of production, and, most importantly, future economic sustainability [

11]. Intense use of RE, primarily guided by the threat of global warming associated with greenhouse gas emission, articulately supplants carbon dioxide injection to the economy [

12].

The motivation of this study is to gauge the nexus between economic policy uncertainty and renewable energy consumption in BRIC countries for the period from 1997q1 to 2018q4 with the moderating effects of foreign direct investment and financial development. The study applied several econometrical tools, such as stationary properties, that were evaluated by implementing Ng and Perron [

13] and Zivot and Andrews [

14] one structural break unit root tests, along with the conventional test of stationary, namely, the ADF test [

15], P-P test [

16], GS-ADF test [

17], and KPSS test [

18]. The long-run cointegration between economic policy uncertainty, foreign direct investment, financial development, and renewable energy consumption was documented by employing the Bayer and Hanck [

19] combined cointegration test. The autoregressive distributed lagged (ARDL) test was implemented for detecting the magnitudes of EPU, FDI and

FD on

REC both in the long-run and short-run by following Pesaran, et al. [

20], moreover, the asymmetric effects of EPU, FDI, and

FD on renewable energy consumption evaluated through non-linear framework offered by Shin, et al. [

21]. Finally the directional association in empirical assessment, study considered non-granger causality test which was familiarized by Toda and Phillips [

22].

The present study contributes to the existing literature in the following manners: First, the nexus between economic policy uncertainty and energy consumption has been extensively investigated in literature [

12,

23,

24,

25]. Existing literature suggests that uncertainties have two dimensions, i.e., geo-political risk and economic policy uncertainty (EPU), which critically induces energy consumption and investment in energy diversifications. More precisely, geo-political risk deals with international energy supply, energy prices, and territorial issues, while

EPU deals with fundamental macro behavior, including monetary and fiscal policies, energy policies, international trade, and so on. However, the role of

EPU on renewable energy is yet to be unleashed in an extensive name even though, in recent periods, researchers have invested time and efforts in detecting the positive association between

EPU and renewable energy consumption in the economy.

Second, the role of financial development in energy development has been extensively investigated, see for instance Salim, et al. [

26], Wang and Jiayu [

27] Polat [

28], and documented both positive and negative associations between them. However, the relationship between financial development and renewable energy consumption has yet to be extensively investigated, especially considering BRIC nations. Nonetheless, in the recent period, a few researchers, for instance, Anton and Afloarei Nucu [

29], Burakov and Freidin [

30], have tried to explore the nexus between

FD and

REC by taking a panel dataset to see. The contribution of the study is the contest of selecting an appropriate measurement of financial development, implying that, as a measurement of financial development, several proxies have been revealed in empirical studies, and, most importantly, the large number of researchers rely on a single indicator, namely, domestic credit to private section (DCP) [

31]. However, very few studies considered the financial development index constructed by taking more than one proxy variable by implementing principal component analysis (PCA). Therefore, this study has extended the financial development proxy index with four proxy measures that are extensively considered by researchers in several occasions. The construction of the FDI index with more proxies will result in capturing the linkage and magnitudes in an efficient manner, and this, moreover, assists in understanding the true relationship with renewable energy output growth.

Third, according to existing literature, the role of foreign direct investment has been extensively appreciated for technological advancement and promotion of energy efficiency in the economy. Inflows of

FDI bring foreign ownership in industrial development with higher energy demand. Therefore, the use of conventional sources of energy, namely, fossil fuels, has been intensified. Over the past decade, the adverse environmental consequences and environmental protection costs have been inducing the economy toward clean energy integration that applies renewable energy for industrial output. In the recent period, a significant amount of research has examined the impact of renewable energy impact on FDI [

28,

32], but the role of

FDI in accelerating renewable energy growth is yet to be examined extensively. This study has extended the existing belief that is

FDI brings energy efficiency with technological progress, implying that the role of

FDI in augmenting renewable energy consumption in BRIC nations.

Study findings document long-run associations between economic policy uncertainty, foreign direct investment, financial development, and renewable energy consumption in BRIC nations, according to Bayer and Hanck [

19] combined cointegration test. Empirical model estimation with ARDL [

20] reveals an adverse statistically significant association between

EPU and renewable energy consumption and positive statistically significant effects running from

FDI and financial development to renewable energy consumption, especially in the long run. According to asymmetry assessment of

EPU,

FDI, and

FD on

REC following Shin, Yu and Greenwood-Nimmo [

21], the study disclosed asymmetric effects running from explanatory variables to renewable energy consumption both in the long-run and short-run. The rest of the article, apart from the introduction in

Section 1, is as follows.

Section 2 deals with the literature survey and conceptual framework of the study. The data, variables definition, and econometrical methodology are explained in

Section 3. Empirical model estimation and interpretation report in

Section 4. Finally, the discussion and conclusion display in

Section 5.

4. Model Estimation and Interpretation

An econometric model based on secondary time series data demands initial validation for appropriate model selection [

105]. It is because of variables integration order immensely essential further advanced model estimation. The study performs the test of stationary following DF-GLS test [

106] and Ng test (Ng and Perron) [

13] along with conventional unit root tests, such as ADF [

15], P-P [

16], and KPSS test [

18]. The results of unit root tests display in

Table 3 and

Table 4. Refers to unit test results display in

Table 3, it is apparent that variables are integrated in mixed order, indicating that variables are stationary either at a level or after the first difference.

The result of Ng and Perron [

13] unit root test display in

Table 1 with four sets of output such as MZa, MZt, MSB, and MPT. According to test statistics, study documents variables are integrated in mixed order that is either at a level or after the first difference.

The unit root test with a structural break following Zivot and Andrews [

14] has been initiated, and results display in

Table 5. Study findings documents that the t-statistics are statistically significant at a 1% significance level, indicating stationary variables after the first difference with one structural break. Specifically, for the series of

REC (2001q2 in Brazil, 2009q3 in Russia, 2002q4 in India, and 2009q4 in China), for economic policy uncertainty (2014q4 in Brazil, 2010q3 in Russia, 2003q2 in India, and 1997q4 in China), for foreign direct investment (2000q4 in Brazil, 2011q1 in Russia, 2018q1 in India, and 2001q4 in China) and financial development (2002q4 in Brazil, 1998q2 in Russia, 2002q3 in India, and 2011q2 in China).

Determination of appropriate optimal lag is critically important, especially for efficient empirical model estimation. The study implements lag length selection criteria under VAR estimation. The results of lag length criteria estimation display in

Table 6. According to AIC, the VAR estimation establishes the optimal lag for further estimation is 2 for all sample countries.

For ascertaining the long-run association between

EPU,

RE,

FDI, and

FD by implementing the Bayer and Hanck [

19] combined cointegration. The cointegration test results are displayed in

Table 7. The F- of cointegrated equations are higher than the critical values at a 1% significance level. These findings suggest the rejection of the null hypothesis of “no-cointegration” and establish the long-run association between

RE,

EPU,

FDI, and

FD. The study documents several cointegrated equations, most importantly the cointegration equation with renewable energy consumption as a dependent variable in all countries’ concerns.

The results of nexus between

EPU and RE consumption in BRIC nations display in

Table 8, including long-run cointegration in Panel A, long-run coefficients in Panel B, the short-run coefficient in Panel C, and residual diagnostic test in Panel D, respectively.

Panel A in

Table 8 reports the result of long-run cointegration, and the study performed standard Wald test for Fpass following Pesaran, Shin, and Smith [

20], Wpass for joint probability test and tBDM test following Banerjee, Dolado, and Mestre [

96]. The test statistics of all three estimations exposed statistically significant at a 1% significance level, implying the rejection of the null hypothesis. The study establishes long-run cointegration between

RE,

EPU, and foreign direct investment in BRIC nations. Once the long-run association ascertains, we move to investigate the magnitudes of

EPU and

FDI on RE consumption in BRIC nations during studied period.

Long-run coefficients display in Panel B of

Table 8. For the impact of

EPU on

RE consumption, the study establishes negative, statistically adverse impacts running from

EPU to

RE consumption in Brazil (a coefficient of −0.168), in Russia (a coefficient of −0.170), in India (a coefficient of −0.131) and China (a coefficient of −0.181), which is aligned with the existing literature, see Sohail, Xiuyuan, Usman, Majeed, and Ullah [

36]. The study findings suggest that achieving stability in

EPU, countries can assist in thriving the present pattern of RE consumption in the economy. More precisely, a 10% stability, if achievable by BRIC nations, in

EPU can have positive growth in RE consumption in the economic activities over the present state by 1.68% in Brazil, by 1.7% in Russia, by 1.13% in India, and by 1.81% in China. Among BRIC nations, the Chinese economy exhibits more inclination in absorbing the benefits in

RE consumption. Refers to

FDI impacts on

REC, the study documents positive statistically significant connection in Russia (a coefficient of 0.198) and in India (a coefficient of 0.065), which is supported by exiting literature, such as Qamruzzaman and Jianguo [

3], Rezagholizadeh, Aghaei, and Dehghan [

70], Khandker, Amin, and Khan [

63]. Renewable energy consumption, especially in developing becomes costly due to a higher degree of capital investment; therefore, the recipients of

FDI create an opportunity for the economy with energy investment.

FDI investment in renewable energy intensifies the energy output in the economy and assists in the energy transition from fossil to renewable energy [

107]. In a study, Doytch and Narayan [

65] document the halo effects of

FDI on energy consumption in the economy, implying that

FDI enhances the environmental economy by transforming into a green energy-based economy with capital assistance in renewable energy production. In addition, the study reveals adverse associations in Brazil (a coefficient of −0.173) and China’s coefficient (a coefficient of −0.055). It is in line with existing studies by Lee [

108], Pao and Tsai [

109].

The impact of financial development on

REC, study documents positive association in Brazil (a coefficient of 0.134), in Russia (a coefficient of 0.049), and in India (a coefficient of 0.071) and in China (a coefficient of 0.049), indicating the financial expansion enhances the green energy consumption through investing in the energy sector, especially for the production of renewable energy. Study findings are in line with Eren, Taspinar, and Gokmenoglu [

78], Naqvi, et al. [

110], Mukhtarov, Humbatova, Hajiyev, and Aliyev [

79]. More specifically, a 10% growth in financial development can result in Brazil’s renewable energy consumption by 1.34%, in Russia by 0.49%, in India by 0.71%, and in China by 0.49%, respectively. A strong and established financial system encourages more financing for the renewable energy sector at reduced prices, resulting in increased investment, which increases energy demand. In the long term, well–functioned capital markets provide valuable assistance for companies seeking to reduce liquidity risk and obtain the money necessary to develop energy-efficient technology [

111]. Additionally, financial development may enable the transfer of money away from inefficient conventional energy sources and renewable energy development [

112].

For the short-run (see, panel–C,

Table 8. The coefficients of error correction terms are negative and statistically significant at a 1% level of significance, suggesting the long-run disequilibrium due to prior period shocks in explanatory variables can be adjusted with the speed of 37.1% in Brazil, by 55.1% in Russia, by 25.2% in India and by 4.36% in China, respectively. Refers to

EPU impacts on REC, the study discloses negative and statistically significant linkage, but in terms of elasticity of

EPU, the magnitudes are minimal compared to long-run estimation. The inflows of

FDI expose positive and statistically significant with

REC in Brazil and Russia, while adverse association in India and China. Financial development establishes a positive linkage with

REC in BRIC countries.

Finally, the empirical model passes with several residual diagnostic tests. The study confirms that the empirical models are free from serial correlation, residuals are normally distributed, and no problem with heteroskadacity. Moreover, the RESET test ascertains efficient estimation for output.

Next, the asymmetric effects of economic policy uncertainty, foreign direct investment, and financial development were evaluated by implementing the asymmetric ARDL equation (see Equation (10)). The results of asymmetric estimation display in symmetric shocks in financial development unveil a positive statistically significant linkage with REC. A 10% development in the financial sector results in increasing REC in Brazil by 0.034%, in Russia by 0.022%, in India by 0.75%, and in China by 0.01%. Meanwhile, a 10% degradation in financial development can decrease the propensity of REC by 0.071% in Brazil, by 0.015% in Russia, by 0.002% in India, and by 0.073% in China. Study findings suggest that even though the magnitude of asymmetric shocks in FD on REC is minimal, the association indicates.

Panel C of

Table 9 reports the standard Wald test for both long-run and short-run symmetry. It is apparent from the test statistics that all the test statistics, i.e., WLR and WSR, are statistically significant at a 1% level of significance. These findings suggest the asymmetric effects of

EPU,

FID, and

FD on

REC both in the long-run and short-run. Furthermore, residual diagnostic tests confirm the empirical model’s internal consistency and efficiency to reach the optimum empirical outcome with no issues in the spurious outcome with four panels of output, which includes long-run asymmetric cointegration in Panel A, long-run asymmetric coefficients in Panel B, short-run asymmetric coefficients in Panel C and residual diagnostic tests in Panel D, respectively.

The study implements Fpass following Pesaran, Shin, and Smith [

20], the joint probability test Wpass and tBDM following, for detecting asymmetric long-run cointegration between renewable energy consumption, economic policy uncertainty, foreign direct investment, and financial development in BRIC nations. It is apparent from the test statistics that there is the rejection of null hypothesis for “no cointegration” since all the test statistics are statistically significant at a 1% level, irrespective of sample countries selection. These findings are suggesting asymmetric effects can be observed from

EPU,

FDI, and

FD on

REC in BRIC nations. Once the asymmetric cointegration is established, the study moves to evaluate the asymmetric shocks that are positive and negative shocks of explanatory variables on

REC.

The long-run asymmetric coefficients are displayed in Panel B. The study documents negative statistically significant linkage between EPU and REC, indicating economic uncertainties create discomfort for renewable energy consumption in the eco. Alternatively, economic uncertainty reduction plays a positive role in energy transformation from fossil to renewable energy. More specifically, a 10% positive variation in EPU can result in REC reduction by 1.68% in Brazil, by 2.11% in Russia, by 1.21 in India, and by 0.021% in China, respectively. Although a 10% reduction in EPU can augment REC in Brazil by 2.01%, in Russia by 0.60%, in India by 1.09%, and in China by 1.14%, respectively. Study findings suggest that energy transformation from fossil to renewable energy, economic stability is critically important due to steady economic progress and effective economic and fiscal policy implementation allows green energy investment, thus eventually intensifying the state of renewable energy demand. Considering the asymmetric effects of foreign direct investment and renewable energy consumption, the study discloses a positive statistically significant tie. More specifically, a 10% positive shock in FDI can result in increasing the REC in Brazil by 6.70%, in Russia by 1.34%, in India by 2.49%, and in China by 2.76%, whereas a 10% negative shock in FDI can play a detrimental role and decrease the present state of REC in Brazil by 3.28%, in Russia by 0.52%, in India by 2.61%, and in China by 3.41%, respectively. Study findings suggest that positive shocks in FDIs can positively influence renewable energy consumption, indicating that the availability of advanced technological assistance in the economy increases the production of green energy. This refers to asymmetric effects of financial development on REC; the study documents the asymmetric shock that is positive and negative variations in FD positively interconnected with REC in BRIC nations. More precisely, a 10% enhancement in the process of financial development results in increasing the consumption REC in Brazil by 3.59%, in Russia by 0.23%, in India by 0.57%, and in China by 1.82%.

On the other hand, a similar rate of adverse shocks in FD (FD) can produce a disadvantageous situation in accelerating the REC in Brazil by 5.10%, in Russia by 4.41%, in India by 1.55%, and in China by 8.08%. It is evident from asymmetric magnitudes that negative shocks in financial development are more significant than improvements in financial development. The study suggests that expansionary policies for financial sector growth can increase green energy investment, but constricting financial policies are more critical for renewable energy output because of limited investment in the energy sector, particularly the renewable energy sector.

For the short-run, the coefficient of error correction terms (ζ) is negative statistically significant at a 1% level of significance, implying the speed of long-run disequilibrium correction due to short-run shocks in explanatory variables. This refers to the asymmetric shocks of EPU on REC, the study documents a negative statistically significant association that is economic stability can boost the renewable energy demand and expand the use of green energy sources. However, concerning asymmetric elasticity on REC are minimal in comparison with long-run coefficients. For inflows of FDI and REC, the study reveals statistically insignificant impacts running from asymmetric shocks except for positive shocks in Brazil exposed to negative statistically significant linkage (a coefficient of −0.022). The asymmetric shocks in financial development unveil a positive statistically significant linkage with REC. A 10% development in the financial sector results in increasing REC in Brazil by 0.034%, in Russia by 0.022%, in India by 0.75%, and in China by 0.01%. Meanwhile, a 10% degradation in financial development can decrease the propensity of REC by 0.071% in Brazil, by 0.015% in Russia, by 0.002% in India, and by 0.073% in China. Study findings suggest that even though the magnitude of asymmetric shocks in FD on REC is minimal, the association indicates.

Panel C of

Table 9 reports the standard Wald test for both long-run and short-run symmetry. It is apparent from the test statistics that all the test statistics, i.e., W

LR and W

SR, are statistically significant at a 1% level of significance. These findings suggest the asymmetric effects of

EPU, FID, and

FD on

REC both in the long-run and short-run. Furthermore, residual diagnostic tests confirm the empirical model’s internal consistency and efficiency to reach the optimum empirical outcome with no issues in the spurious outcome.

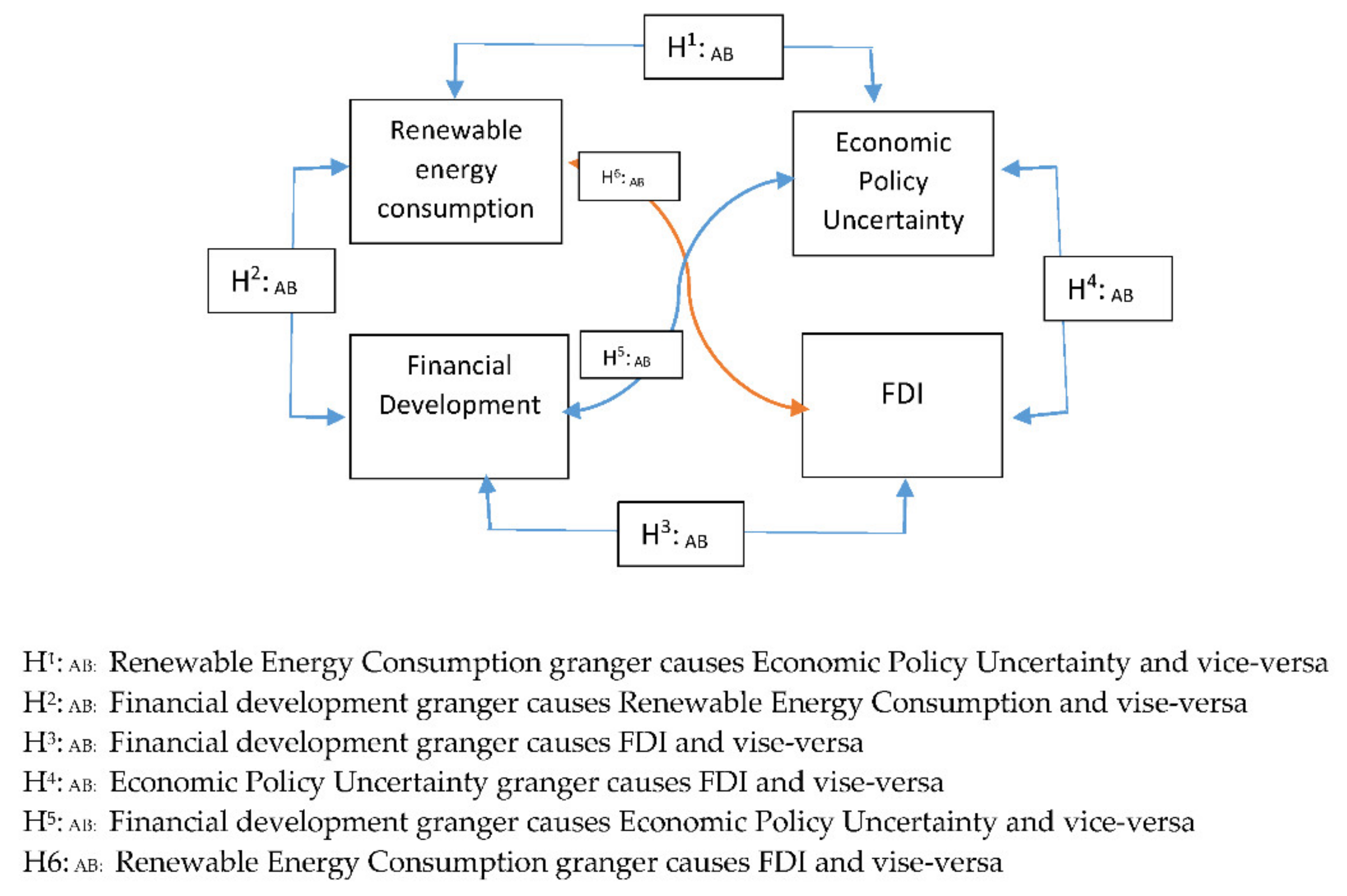

The following section deals with detecting a directional association between REC,

FDI, FD, and

EPU through implementing a non-granger causality equation by following Toda and Phillips [

22]. Causality results are displayed in the

Table 10 with four panels such as Panel A for Brazil, Panel B for Russia, Panel C for India, and Panel D for China. This refers to causal effects between

EPU and REC, the study documents unidirectional causal effects from economic policy uncertainty to renewable energy consumption (

EPU→REC) in BRIC nations. On the other hand, regarding causality between

FDI and REC, the study disclosed bidirectional causality (

FDI↔REC) in Russia and India and unidirectional causality (

FDI→REC) in Brazil and China, which is in line with Eren, Taspinar, and Gokmenoglu [

78]. For directional causality effects between financial development and renewable energy consumption, the study unveils bidirectional causality (FD↔REC) in Brazil and unidirectional causality (FD→REC) in Russia, India, China, respectively.

To ascertain the long-run impact of economic policy uncertainty, foreign direct investment, financial development, and renewable energy consumption in BRIC nations. The study further implements fully-modified OLS introduced by Phillips and Hansen [

113] and dynamic OLS and canonical cointegrating regression (CCR), familiarized by Stock and Watson [

114] and results display at

Table 11. Study findings reveal the expected sign for each explanatory variable in explaining the association to renewable energy consumption. More precisely, the elasticity of

EPU exposes negative association, and

FDI inflows and

FD positively assist in improving the application of renewable energy in the economy.

5. Discussion

The role of green energy integration and application is critically important for establishing an environmental quality, and, therefore, reliance on renewable energy and their integration as an alternative to fossil energy has been extensively considered. The growth of renewable energy and its integration has been investigated by considering various macro-fundamentals and exploring their role in developing renewable energy output and its demand. This study focused on assessing the impact of economic policy uncertainty on renewable energy consumption in BRIC nations with the mediating role of inflows of foreign direct investment and financial development. The long-run cointegration tests, such as Bayer and Hanck [

19], combined the cointegration test, Fpass, following Pesaran Pesaran, Shin, and Smith [

20], joint probability test, and tBDM test, following Banerjee, Dolado, and Mestre [

96]. The study findings confirmed the long-run association between

EPU,

FDI,

FD, and

REC, indicating the co-movement due to variability in any regression. Furthermore, the ultimate effects in

REC will have experienced variations as the results of changes happened in

EPU,

FDI, and

FD in BRIC nations. Now, the study moves on gauging the magnitudes of

EPU,

FDI, and

FD on

REC through implementing ARDL bound testing. The asymmetric effects of

EPU,

FDI, and

FD on renewable energy consumption were investigated by implementing nonlinear ARDL following Shin, Yu, and Greenwood-Nimmo [

21], and, finally, the directional causalities were evaluated through implementing the non-granger causality test, following Toda and Phillips [

22], under VAR environment. The Kay study findings of the study are as follows:

First,

EPU impact on renewable energy consumption. Refers to ARDL estimation, it is apparent that adverse statistically significant effects are running from

EPU to

REC, indicating that economic instability and adverse shocks create tension in implementing green energy policies, which result in decreasing the renewable energy output and the integration process. In a study, Burns [

115] documents with sector-level data that

EPU discourages investment in renewable energy sectors, such as the wind and solar energy sector. This refers to asymmetric elasticity of economic policy uncertainty on renewable energy consumption. The study reveals that the test statistics of the standard Wald test are statistically significant, both in the long-run and short-run, suggesting that the asymmetric effects running from

EPU to

REC both in the long-run and short-run. In the long run, according to the asymmetric coefficients that are the positive and negative shocks of

EPU was exposed negative statistically significant linkage with

REC in BRIC nations. Study findings explained that reducing

EPU through innovation and effective policy implementation could open an avenue for renewable energy integration in economic activities and eventually accelerates renewable energy output. Uncertainties, according to Balcilar, et al. [

116], impact renewable energy growth can be observed; first, the macroeconomic effect on the economy makes it difficult for RE growth because of the lack of available investment and cheap energy sources. It is because, in the initial period, the renewable energy sector requires substantial capital investment. The second effect of uncertainty is that it makes politicians more hesitant to implement renewable energy legislation because the actions of consumers and producers, who remain cautious, may not make the switch to renewables.

The effects of

FDI inflows on

REC reveals a positive statistically significant impact, especially in the long run, according to ARDL estimation. It is in line with Lau, et al. [

117], Omri and Kahouli [

118]. Energy diversification transitioning from fossil energy to renewable energy reliance is one of the critical aspects of foreign investment presence in the economy; moreover, technological progress and energy-efficient production processes act as motivational factors in the energy selection process to encourage renewable energy growth [

119]. This refers to asymmetric shocks of

FDI on renewable energy consumption, according to NARDL estimation, the asymmetric shocks in

FDI are positive statistically linked with

REC in BRIC nations, which is aligned with Qamruzzaman and Jianguo [

3]. Foreign direct investment and equity investment positively impacted the economy’s aggregated output through industrialization and infrastructure development. It has long been assumed that foreign direct investment (

FDI) is linked to transferring knowledge, managerial experience, and technological innovation from home nations to host countries [

109]. In addition to scale impacts, foreign direct investment (

FDI) may have various effects on the economy, including technique effects and composition effects. The impact of the foreign direct investment may be seen by reducing the size of one sector while increasing the size of another; for example, the

FDI-led service industry uses less energy than the

FDI-led manufacturing industry [

83].

Financial development positively entices the growth of renewable energy consumption in BRIC nations, especially in the long run, which is align existing literature see, for instance, Shahbaz, et al. [

120]; Alsaleh and Abdul-Rahim [

121], Liu, et al. [

122], and Burakov and Freidin [

30]. Renewable energy has the potential to be a useful instrument in the pursuit of energy diversification through reduced reliance on fossil fuel supplies. Furthermore, the generation of green energy has the potential to avoid future environmental damage. Nonetheless, making the shift from fossil-fuel-based energy to renewable energy generation may be difficult because of the higher cost associated with implementing renewable energy, which is one of the most significant obstacles that have to be overcome. Compared to fossil-fuel-based energy investments, there are many financial hurdles to overcome, including greater infrastructure, start-up, and operational expenses, among other things. As a result, it is critical to have a stable financial system that can efficiently handle price discovery and financing, market liquidity, and risk management. The financial environment enables families, legal organizations, and people to readily get cash (and credit) from financial institutions, thus expanding their consumption and production capacity. These conditions and scenarios contribute to an increase in energy usage. The beneficial effect of financial growth on energy demand is critical for implementing suitable energy policies that include alternative energy sources. If financial development results in a reduction in fossil fuel energy consumption, it may be inferred that these phenomena, as well as an increase in the use of efficient and environmentally friendly energy sources (RES), is accomplished via financial development. Energy-finance nexus theorists propose that financial growth leads to increased energy use in the economy in three distinct ways. First, direct effects, such as increased purchasing power and additional financing from banks result in increased demand for energy consumption [

3]. Second, indirect effects, such as increased purchasing power and the availability of additional financing from banks result in increased demand for energy consumption. Second, the commercial impacts of free access to financial possibilities reduce borrowing costs and enable companies to expand their existing company operations and operations. As a result, the growth of the business process produces an increase in the need for electricity. Third, wealth effects are concerned with the development of the stock market and the confidence in economic growth, which have a positive spillover impact on actual economic activity and a rise in energy consumption [

30]. Increased energy efficiency in the economy may be encouraged by the impacts of efficient and developed financial sectors, which can be achieved by developing better financial instruments to increase and use renewable energy. Furthermore, Tamazian, et al. [

123] advocate that financial development fosters efficiency in financial services and institutional effectiveness, which stimulates technical innovation and the use of new technology in services, resulting in a decrease in electricity consumption.

{kind=link}